Linear LED Strip Fixture Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

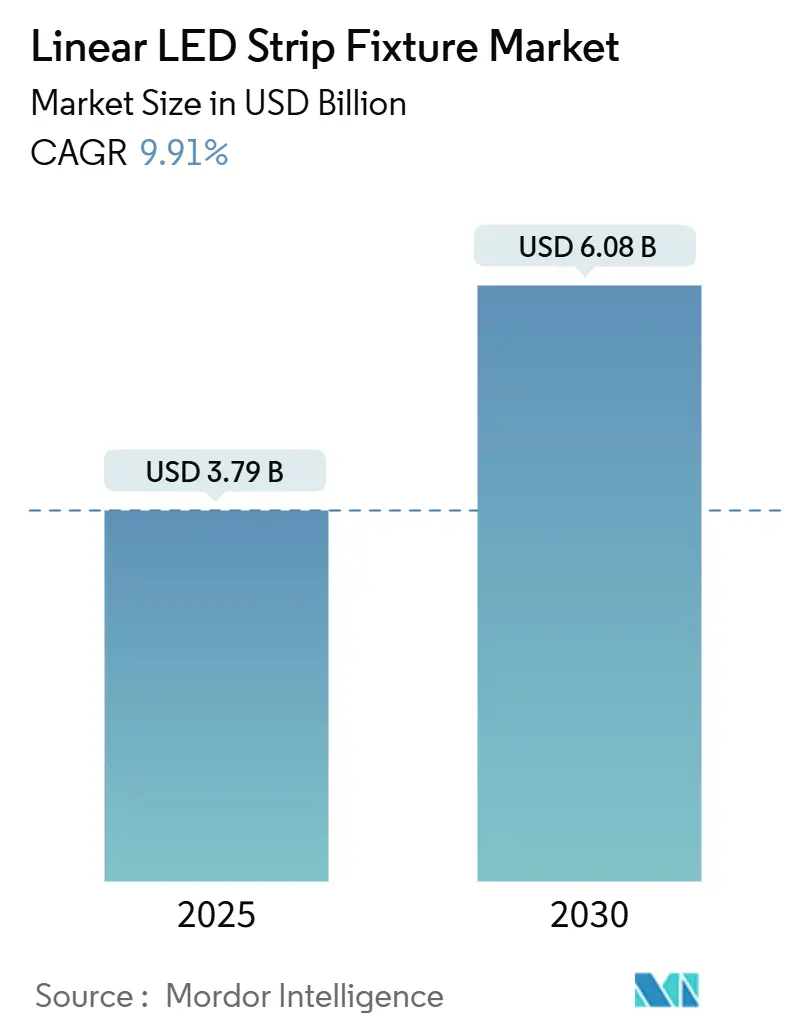

| Market Size (2025) | USD 3.79 Billion |

| Market Size (2030) | USD 6.08 Billion |

| Growth Rate (2025 - 2030) | 9.91% CAGR |

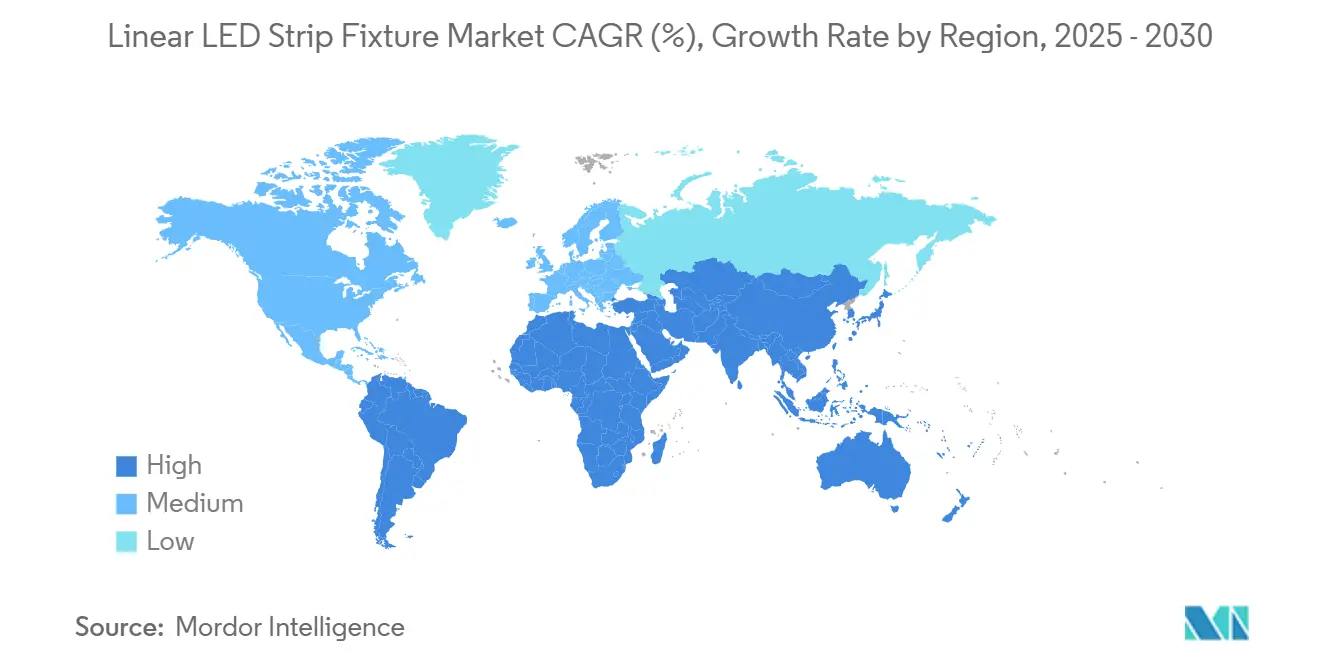

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

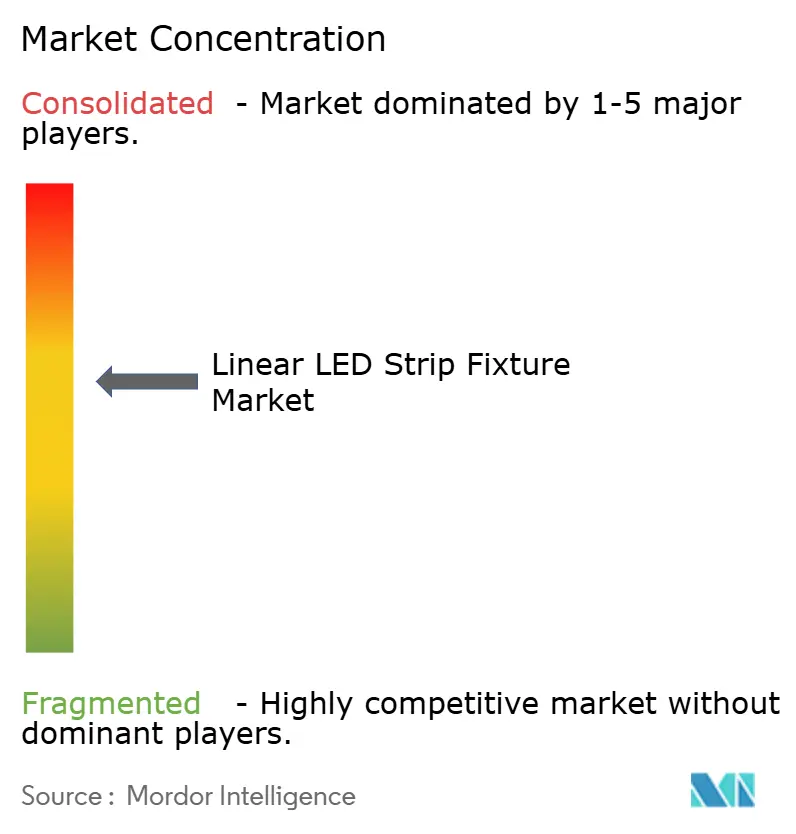

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Linear LED Strip Fixture Market Analysis by Mordor Intelligence

The linear LED Strip Fixture market size is estimated at USD 3.79 billion in 2025 and is projected to reach USD 6.08 billion by 2030, representing a 9.91% CAGR over the forecast period. The expansion rests on three pillars: the phase-out of fluorescent and incandescent lamps, a significant decline in LED chip production costs, and robust policy pressure to reduce building energy demand. Corporate net-zero targets, faster payback periods, and the spread of IoT-enabled controls further strengthen the investment case for linear strips in offices, stores, factories, homes, and vehicles. The Asia Pacific region retains volume leadership due to its integrated supply chain, which shortens lead times, while the Middle East records the fastest unit growth as large infrastructure projects specify connected LED lighting. Commercial construction still accounts for the bulk of shipments; however, automotive ambient lighting, hospitality retrofits, and premium residential projects collectively deliver the highest incremental value. Manufacturers, therefore, balance cost-optimized high-volume ranges with specialty versions that embed sensors, wireless drivers, and software hooks to secure recurring service revenue.

Key Report Takeaways

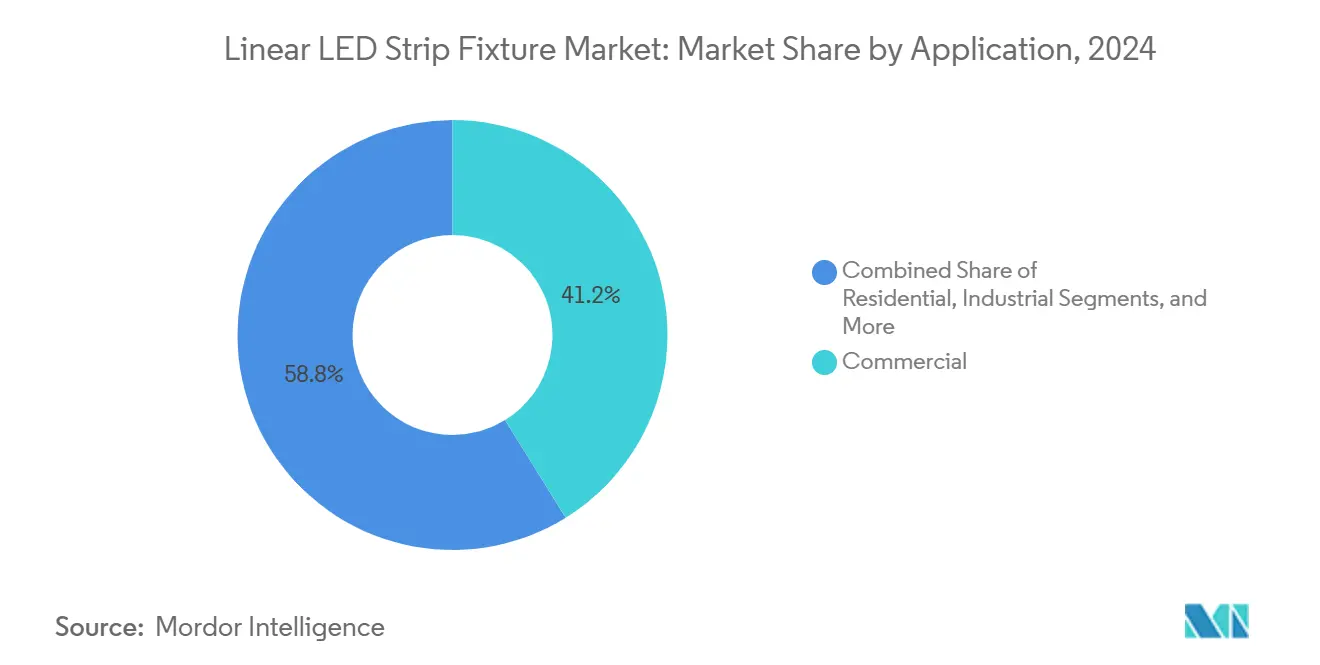

- By application, commercial spaces held 41.18% of the Linear LED Strip Fixture market share in 2024, while automotive interiors are projected to post the fastest growth, with a 9.92% CAGR from 2024 to 2030.

- By installation type, surface-mounted products captured 52.34% of the Linear LED Strip Fixture market size in 2024, whereas suspended fixtures are forecast to expand at a 10.78% CAGR.

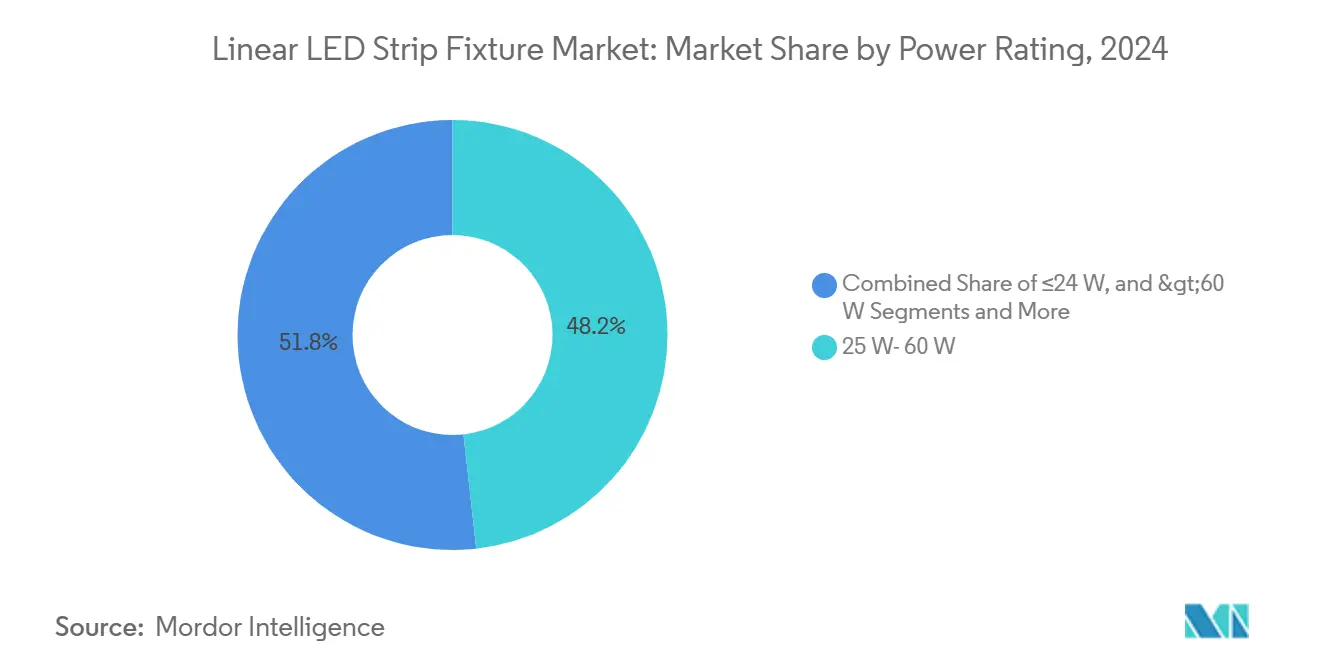

- By power rating, the 25 W–60 W class led with 48.23% of the Linear LED Strip Fixture market share in 2024; however, units with a power rating of ≤24 W are expected to grow the fastest at a 10.41% CAGR.

- By distribution channel, electrical wholesalers held a 38.46% share of the Linear LED Strip Fixture market size in 2024, and online retail is projected to grow at an 11.16% CAGR through 2030.

- By region, Asia Pacific commanded 33.71% of the Linear LED Strip Fixture market size in 2024 and the Middle East is estimated to generate a 10.78% CAGR up to 2030.

Global Linear LED Strip Fixture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of energy-efficient lighting solutions | +2.1% | North America, Europe | Medium term (2-4 years) |

| Declining LED chip prices and manufacturing costs | +1.8% | Asia Pacific, spill-over global | Short term (≤ 2 years) |

| Stringent global regulations on energy consumption | +1.6% | North America, EU, expanding Asia Pacific | Long term (≥ 4 years) |

| Rapid expansion of smart building infrastructure | +1.4% | Global urban centers | Medium term (2-4 years) |

| Integration of LED strips in automotive ambient lighting | +0.9% | Germany, Japan, China | Medium term (2-4 years) |

| Emergence of flexible printed circuit substrates | +0.7% | Asia Pacific manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Energy-Efficient Lighting Solutions

Commercial property owners accelerate LED strip retrofits because LEDs reduce electricity use by up to 75% compared to incandescent lamps.[1]U.S. Department of Energy, “LED Lighting,” ENERGY.GOV Energy-efficiency directives in the European Union and updated codes such as California’s Title 24 make LED compliance almost mandatory for new and remodeled spaces. Shorter two- to three-year payback horizons spur CFO approval, even without rebates. Corporate carbon neutrality pledges expand the addressable base, as lighting upgrades provide quantifiable Scope 2 savings. Growing retrofit volume keeps fixture prices competitive, thus reinforcing demand momentum.

Declining LED Chip Prices and Manufacturing Costs

Average packaged LED prices have slipped about 15% per year since 2023, driven by higher fab yields and bigger wafer sizes in China and South Korea. Cost relief lets vendors add sensors or premium optics yet still meet tender ceilings. Lower die costs also unlock profitable entry-level strips below 24 W, a segment where price elasticity is strongest. The resulting volume gives fabs further scale, so a virtuous cycle of cost and demand continues through the forecast horizon.

Stringent Global Regulations on Energy Consumption

Forty-plus countries now enforce building-lighting efficacy floors that only LED technology can satisfy, according to the International Energy Agency. Ecodesign in Europe and minimum luminous efficacy rules in the United States remove inefficient lamps from catalogs, pushing specifiers toward strip fixtures that combine high lm/W ratios with optical uniformity. Certification schemes such as LEED and BREEAM give developers extra points for controllable LEDs, which further deepens penetration in commercial pipelines.

Rapid Expansion of Smart Building Infrastructure

Roughly 60% of Acuity Brands' commercial LED orders already integrate connectivity features, illustrating the market shift toward data-rich lighting. Linear strips are well-suited for zone-level control and discrete occupant sensing, eliminating the need for structural ceiling changes. Wireless protocols, including Zigbee, Thread, and Bluetooth, enable quick commissioning, saving labor on-site. Smart algorithms trim another 20–30% of energy compared to manual switching and feed occupancy analytics into facility dashboards, making the business case compelling for landlords seeking operational savings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply chain volatility for key electronic components | -1.2% | Global, acute Asia Pacific | Short term (≤ 2 years) |

| Photobiological safety concerns among consumers | -0.8% | Developed markets | Medium term (2-4 years) |

| High initial capital outlay for commercial retrofits | -0.6% | Developing regions | Medium term (2-4 years) |

| Market saturation in developed retail channels | -0.4% | North America, Western Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Volatility for Key Electronic Components

Lead times for LED drivers and flexible printed circuits stretched to 16–20 weeks in 2024 as semiconductor backlogs converged with logistics bottlenecks. Makers responded by dual-sourcing, qualifying alternative materials, and increasing buffer inventory, but these steps tie up capital and pressure margins. Persistent tension in the Taiwan Strait or further pandemic flare-ups could renew shortages, so buyers lock in blanket orders months ahead, limiting agility.

High Initial Capital Outlay for Commercial Retrofits

Comprehensive strip-lighting upgrades often cost USD 50,000 to USD 500,000 per mid-size facility, a hurdle for cash-constrained owners despite a four-year median payback.[2]U.S. General Services Administration, “LED Lighting Retrofit Guidelines,” GSA.GOV Financing solutions such as energy-service contracts or on-bill repayment grow, but uptake remains uneven outside Tier-1 cities. Legacy wiring and ceiling grids add engineering complexity that inflates install budgets, especially in buildings erected before 2000.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Rating: Efficiency Gains Favor Low-Wattage Solutions

The 25 W–60 W band retained 48.23% of the Linear LED Strip Fixture market size in 2024, serving general illumination where buyers want a balance of lumen output and cost. The ≤24 W class is projected to clock a 10.41% CAGR because smart controls and high efficacy chips now deliver design-level lux with lower wattage, a decisive advantage for green-building certifications. OSRAM’s 200 lm/W strips demonstrate how premium dies enhance output while reducing energy consumption, encouraging specifiers to adopt multi-string, low-power layouts. In hospitality lobbies, retail shelving, and residential cove lighting, architectural teams increasingly choose multiple low-wattage lines to create visual nuance. High-power (>60 W) products remain niche, mostly in factories or façades where lumen density overrules energy constraints; yet, stronger thermal-management technology could improve their appeal post-2027.

Second-tier cities across Asia are retrofitting older fluorescent fixtures with 30 W replacements because the wiring remains compatible, and labor is scarce. In contrast, North American offices deploy 15 W connected strips at desk height to harness daylight, reducing total wattage per square foot. The contrast shows that one power segment rarely dominates every use case; rather, code stringency, utility rebates, and ceiling height dictate final specification, keeping three power classes active within the Linear LED Strip Fixture market.

By Installation Type: Surface-Mounted Leads, Suspended Accelerates

Surface units held 52.34% share of the Linear LED Strip Fixture market size in 2024, thanks to quick screw-fix installation on existing substrates, a key selling point for budget-sensitive retrofits. Suspended systems, however, are growing at a rate of 10.78% annually, as designers favor visual float and indirect uplight for open-plan offices. Ultra-thin cables and wireless power kits allow pendants as slim as 8 mm, reducing visual clutter and simplifying height adjustment.[3]IEEE Standards Association, “LED Lighting Systems,” STANDARDS.IEEE.ORG Recessed lines remain popular in high-end retail,l where hidden sources accent merchandise without driver glare.

In new airports and civic buildings, architects specify continuous suspended runs to unify vast halls, while hotels adopt recessed lines in corridors to prevent dust accumulation. Surface types still dominate educational and industrial stock, where facility budgets prioritize speed and robustness over aesthetics. Over the forecast window, hybrid projects that combine recessed coves with surface-mounted task zones are expected to rise, keeping all three formats in play within the Linear LED Strip Fixture market.

By Application: Commercial Supremacy Meets Automotive Upswing

Commercial spaces controlled 41.18% of the Linear LED Strip Fixture market share in 2024 as offices, big-box retail, and distribution centers replaced troffers with efficient strips to meet code. Automotive interiors are expected to outpace all other applications with a 9.92% CAGR through 2030, driven by premium carmakers who view ambient lighting as a low-cost avenue for perceived luxury. Residential remodeling is gaining traction, especially in kitchens and smart-home ecosystems, yet the value per unit remains lower than in contract projects.

Electric-vehicle OEMs integrate dynamic color lines into door panels and footwells to signal charging status or driving modes, adding electronic content specific to each vehicle. Warehouses continue to favor wide-beam commercial strips to satisfy ASHRAE illuminance targets at 30 ft mounting heights. Meanwhile, art museums employ tunable strips to align color temperature with daylight that enters skylights. This breadth of use keeps the Linear LED Strip Fixture market diversified, insulating vendors from single-sector downturns.

By Distribution Channel: Wholesalers Retain Core Buyers, Online Rises

Electrical wholesalers owned 38.46% of the Linear LED Strip Fixture market size in 2024 by bundling logistics, credit, and specification support for contractors. Online marketplaces are expected to register an 11.16% CAGR because spec chapters and datasheets enable buyers to self-qualify products without requiring showroom visits. Specialist lighting stores cater to boutique hospitality jobs, where hands-on mock-ups influence purchasing decisions, and direct OEM sales target multinational rollouts that require uniform part numbers.

Wholesalers strengthen digital portals that show real-time inventory and offer kitting, thereby defending share even as pure-play e-commerce lures small installers. Live-chat engineering support and same-day pickup also remain valued for fast-track renovations. Between 2025 and 2030, dual-channel strategies prevail, with vendors listing core SKUs online to capture emerging do-it-yourself buyers while feeding margin-rich custom orders through distribution partners, thereby sustaining channel equilibrium in the Linear LED Strip Fixture market.

Geography Analysis

The Asia Pacific captured 33.71% of the Linear LED Strip Fixture market size in 2024, driven by vertically integrated LED fabs, competitive labor, and public schemes such as India’s Smart Cities Mission, which mandate efficient street and building lighting. China supplies over 60% of global LED die output, enabling domestic brands to price aggressively while shipping surplus to Latin America and Africa. South Korean and Japanese firms contribute innovation in chip architecture and phosphor blends, which diffuses across the regional supply chain. ASEAN governments issue tax credits for LED imports, further widening provincial adoption.

The Middle East is forecast to post a 10.78% CAGR through 2030, the fastest worldwide, as megaprojects tied to Saudi Vision 2030 and the UAE Energy Strategy specify connected strips for stadiums, hospitals, and metro stations.[4] Saudi Vision 2030, “Energy Efficiency Program,” VISION2030.GOV.SA High ambient temperatures favor LEDs because they have a lower heat output, which reduces HVAC loads in malls and airports. Local distributors in Dubai and Riyadh partner with European brands to meet stringent photobiological safety standards, while free-trade zones facilitate the re-export of finished fixtures into Africa.

North America and Europe form mature demand centers where retrofit volume dominates new builds. Utility rebates and performance contracting support federal building upgrades such as the GSA program that sourced LED strips for 500 facilities in late 2024. European policy under the Green Deal treats efficient lighting as taxonomy-eligible, unlocking cheaper green finance for landlords. Adoption now shifts from energy savings alone to circadian and human-centric features that raise productivity. Both regions also adopt centralized lighting platforms that feed data into building-wide analytics, thereby enhancing the total addressable software layer adjoining the Linear LED Strip Fixture market.

Competitive Landscape

The Linear LED Strip Fixture market is moderately fragmented. Multinationals like Signify, OSRAM, and Acuity Brands preserve leadership through broad catalogs, R&D scale, and multi-tier distribution, yet Asian entrants erode price points by leveraging captive chip fabs. Signify’s USD 150 million expansion in Eindhoven underscores its pivot toward embedded sensors and wireless stacks, which lock customers into cloud subscriptions. OSRAM’s Taiwan PCB acquisition secures flexible substrate capacity, trimming the bill of materials by up to 20% and shrinking form factors that architects demand.

Semiconductor specialists such as Seoul Semiconductor and Nichia gain market share through proprietary dies that achieve efficiency highs of 250 lm/W, enabling fixture makers to comply with upcoming stricter efficacy standards without redesign. European premium brands differentiate themselves via bespoke optics and strict flicker compliance, which is sought by museums and medical facilities. Meanwhile, direct-to-consumer start-ups exploit social media and AR visualization apps to sell pre-configured strip kits, especially in the DIY residential segment.

Competitive tactics increasingly center on bundled hardware-software deals, open APIs, and integration with building operating systems. Patent filings trend toward thermal management, flexible substrates, and chip-scale packaging, a sign that form-factor miniaturization remains a key battlefield. Vendors also invest in regional assembly to mitigate tariff risks and qualify for procurement rules that favor local content. Overall, rivalry remains dynamic, yet the top five suppliers together control roughly 45% of global revenue.

Linear LED Strip Fixture Industry Leaders

Signify N.V.

Acuity Brands Inc.

OSRAM GmbH

Lutron Electronics Co., Inc.

Cree Lighting, A Division of IDEAL INDUSTRIES, INC.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Nichia received recognition from the Japan Institute of Energy for a new phosphor that enhances CRI without compromising efficacy.

- January 2025: Havells India rolled out locally made smart LED strips priced 30% below imports, integrated with popular Indian home-automation apps.

- January 2025: Signify announced a USD 150 million upgrade of its Eindhoven plant to produce connected strip fixtures with embedded sensors and wireless radios.

- December 2024: OSRAM completed an USD 85 million purchase of a Taiwanese flexible PCB firm, aiming at 15–20% cost cuts on key lines.

Global Linear LED Strip Fixture Market Report Scope

| ≤24 W |

| 25 W- 60 W |

| >60 W |

| Surface Mounted |

| Recessed |

| Suspended |

| Commercial |

| Residential |

| Industrial |

| Automotive Interior |

| Architectural and Decorative |

| Direct Sales |

| Specialist Lighting Stores |

| Online Retail |

| Electrical Wholesalers |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Power Rating | ≤24 W | |

| 25 W- 60 W | ||

| >60 W | ||

| By Installation Type | Surface Mounted | |

| Recessed | ||

| Suspended | ||

| By Application | Commercial | |

| Residential | ||

| Industrial | ||

| Automotive Interior | ||

| Architectural and Decorative | ||

| By Distribution Channel | Direct Sales | |

| Specialist Lighting Stores | ||

| Online Retail | ||

| Electrical Wholesalers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the Linear LED Strip Fixture market in 2025?

The Linear LED Strip Fixture market size is valued at USD 3.79 billion in 2025 and is projected to grow at a 9.91% CAGR through 2030.

Which region leads global demand for linear LED strip fixtures?

Asia Pacific holds the largest share at 33.71% thanks to its integrated manufacturing base and aggressive infrastructure programs.

What segment shows the fastest growth by application?

Automotive interior lighting is forecast to post the highest 9.92% CAGR as premium brands add ambient and dynamic features.

Why are suspended LED strip fixtures gaining popularity?

Minimalist architecture and better wireless power options push suspended fixtures to a 10.78% growth rate, appealing to designers who want floating light lines.

How are declining LED chip prices influencing adoption?

A 15% annual drop in chip prices lowers fixture costs, letting buyers add smart controls without exceeding retrofit budgets, which propels volume growth.

Page last updated on: