United States Outdoor LED Lighting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

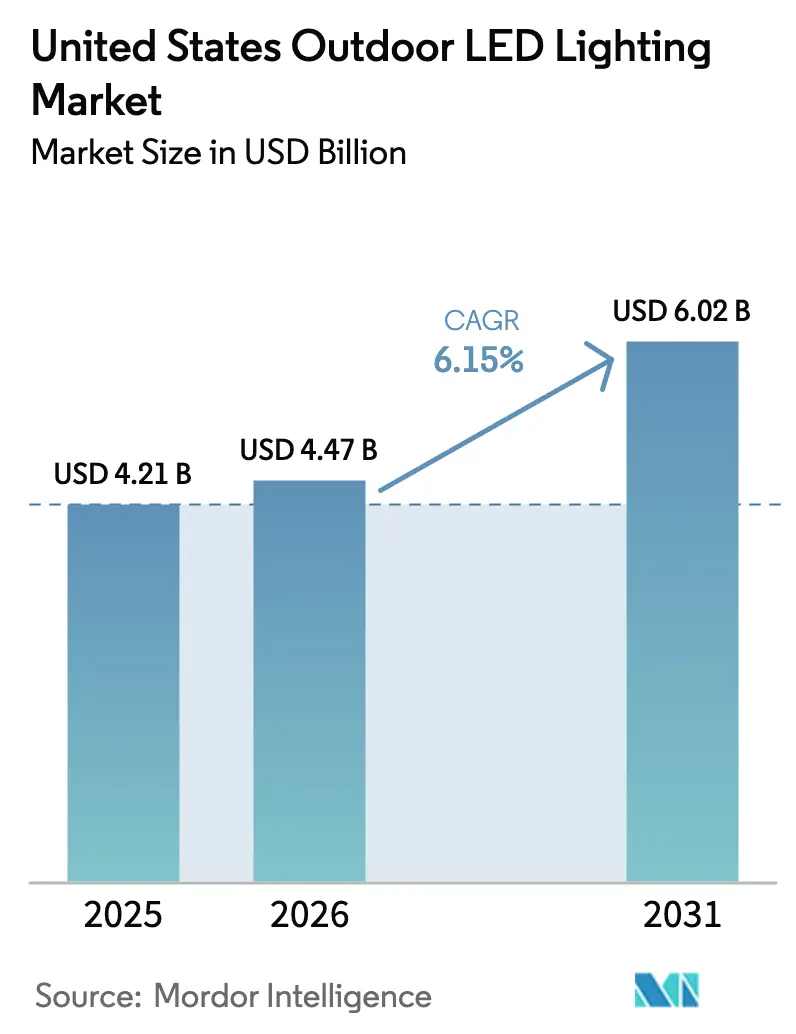

| Base Year Market Size (2025) | USD 4.21 Billion |

| Market Size (2026) | USD 4.47 Billion |

| Market Size (2031) | USD 6.02 Billion |

| Growth Rate (2026 - 2031) | 6.15% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Outdoor LED Lighting Market Analysis by Mordor Intelligence

The US outdoor LED lighting market size is expected to grow from USD 4.21 billion in 2025 to USD 4.47 billion in 2026 and is forecast to reach USD 6.02 billion by 2031 at 6.15% CAGR over 2026-2031. Municipal clean-energy mandates, federal roadway modernization funding, and rapidly expanding smart-city programs are simultaneously lifting product demand, accelerating technology replacement cycles, and reshaping public procurement priorities.[1]U.S. Department of Transportation, “Biden Administration Announces Historic Investment in America's Infrastructure,” transportation.gov Street, roadway, and parking projects dominate current unit volumes, yet connected luminaires with embedded sensors, wireless controls, and cyber-secure firmware are widening the total addressable value as cities shift from basic lamp swaps to full-system overhauls. Technological progress, most notably 150-lumens-per-watt efficacies and integrated edge-computing modules, has compressed payback periods below three years, motivating municipalities to bundle lighting with environmental monitoring, traffic analytics, and small-cell 5G hardware. Cost headwinds created by 2024 semiconductor shortages have begun easing, but component-level price volatility still influences bid calendars and encourages near-shoring strategies among U.S. fixture assemblers.

Key Report Takeaways

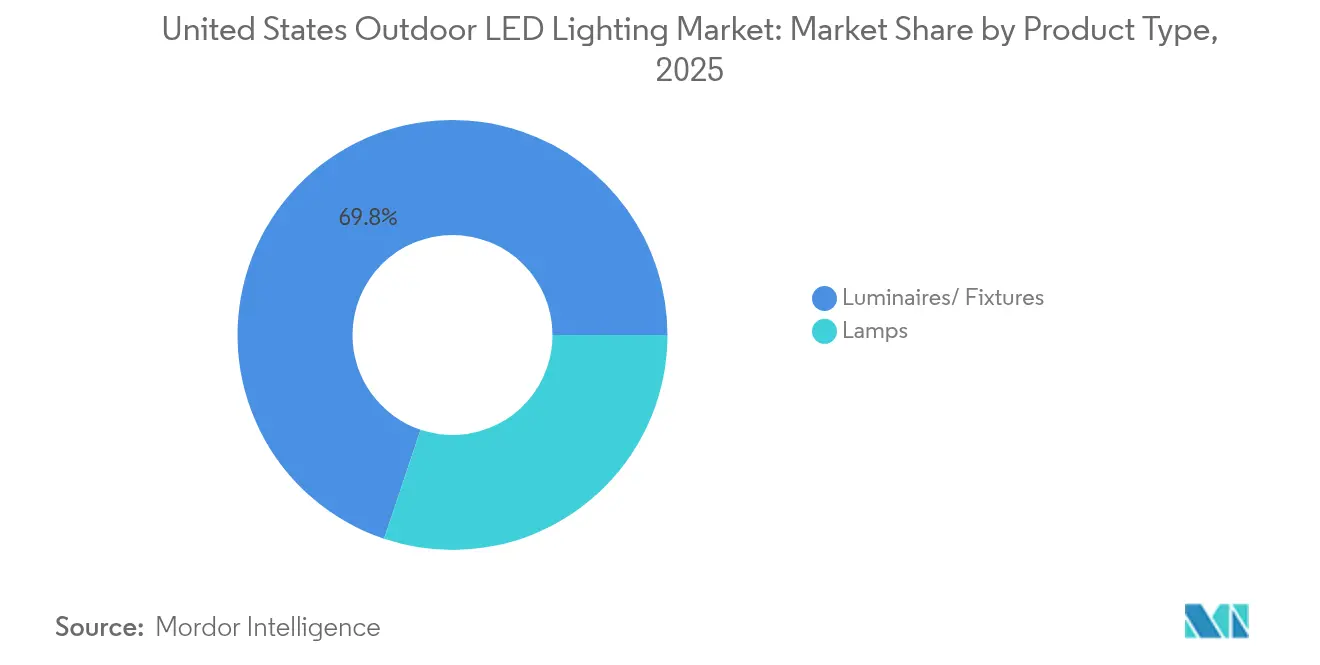

- By product type, luminaires captured 69.84% of the US outdoor LED lighting market share in 2025, while lamps are projected to expand at a 6.02% CAGR through 2031.

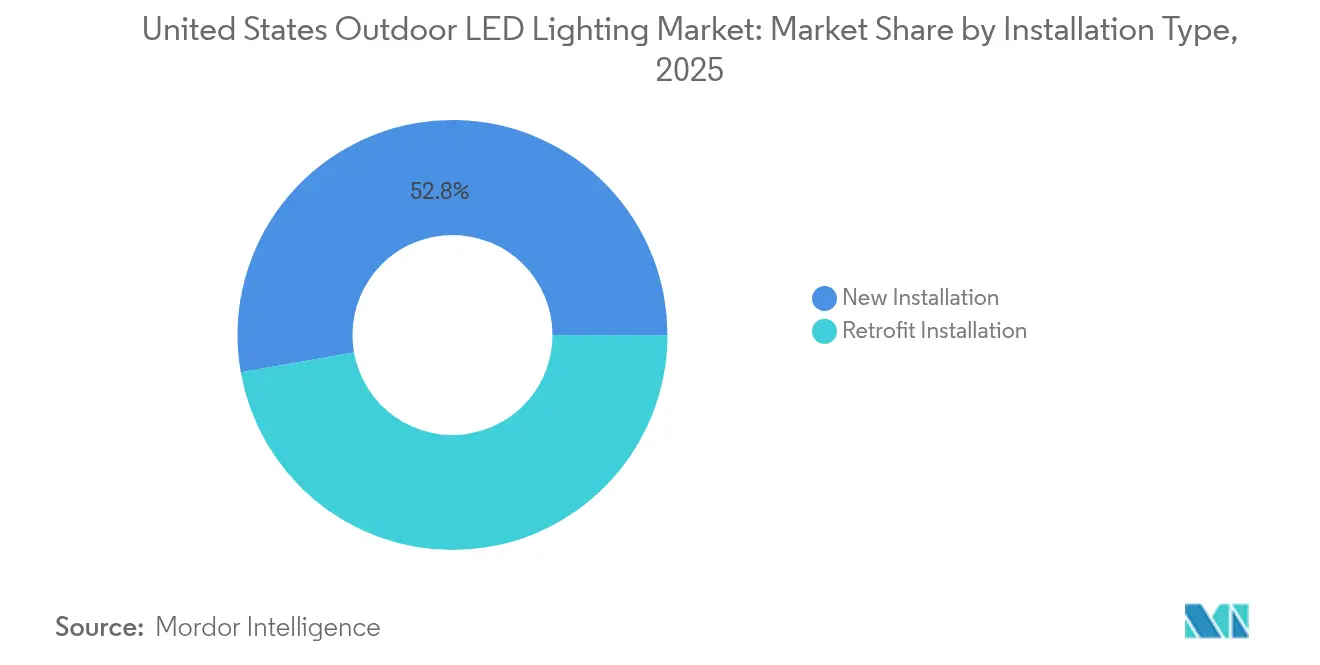

- By installation type, the US outdoor LED lighting market size for new installations accounted for 52.78% of the revenue in 2025; retrofit projects are projected to grow at a 5.07% CAGR between 2026 and 2031.

- By application, street and roadway lighting held 42.35% of the US outdoor LED lighting market size in 2025, whereas sports and stadium venues are poised to advance at a 4.63% CAGR through 2031.

- By distribution channel, direct sales accounted for 62.95% of the US outdoor LED lighting market size in 2025, and e-commerce is forecasted to rise at a 4.29% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Outdoor LED Lighting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Municipal energy-efficiency mandates and utility rebates | +1.8% | National, with concentration in California, New York, Texas | Medium term (2-4 years) |

| Declining LED fixture costs and rising efficacy | +1.2% | Global supply chain benefits, strongest impact in cost-sensitive markets | Short term (≤ 2 years) |

| Smart-city demand for connected lighting networks | +0.9% | Metropolitan areas, early adoption in Northeast and West Coast | Long term (≥ 4 years) |

| Secondary-replacement wave of early LED installs | +0.6% | National, concentrated in early-adopter municipalities from 2015-2018 | Medium term (2-4 years) |

| Climate-resilient solar-hybrid lighting adoption | +0.4% | Hurricane-prone regions (Southeast, Gulf Coast), wildfire areas (West) | Long term (≥ 4 years) |

| IIJA-funded roadway lighting upgrades | +0.5% | National infrastructure corridors, rural and underserved areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Municipal Energy-Efficiency Mandates and Utility Rebates

Power-sector decarbonization targets have shifted from voluntary benchmarks to binding municipal ordinances that mandate high-performance LED fixtures equipped with adaptive dimming and daylight-responsive shut-off features. Title 24 revisions now require 50% after-hours load reductions for most exterior luminaires in California, while Con Edison's commercial rebate program offers up to USD 400 per qualifying fixture, closing capital gaps for budget-constrained precincts.[2]California Energy Commission, “Building Energy Efficiency Standards,” energy.ca.gov Cities such as San Diego report streetlighting energy cuts near 20% after layering grid-responsive controls atop networked LED retrofits, and the ENERGY STAR program's tighter optical-control requirements funnel spending toward premium vendors that can guarantee sub-3-year paybacks. As utilities expand performance-based incentives, procurement officers are increasingly bundling monitoring software, predictive maintenance analytics, and cybersecurity overlays into bid specifications to lock in energy savings and operational resilience. The cascading effect accelerates follow-on retrofits across parking, pathway, and tunnel assets once street corridors prove their economic and safety advantages.

Declining LED Fixture Costs and Rising Efficacy

Annual fixture price drops of roughly 12-15% through 2024, paired with efficacy increases above 150 lm/W, have decisively tipped total-cost assessments toward immediate HID replacement. Even communities that converted earlier-generation LEDs in 2015-2018 now find that new luminaires cut wattage by another 30-40%, justifying a second upgrade cycle. Semiconductor scale economies, miniaturization of optics, and streamlined thermal designs account for most cost relief, although tariffs on Chinese components temporarily raised U.S. landed costs by 8-12% in late 2024. High-end suppliers, therefore, pursue margin retention through tunable-white modules, on-board sensing suites, and field-adjustable lumen outputs that simplify inventory management for contractors. Mid-tier manufacturers, squeezed between bargain imports and innovation leaders, are merging to attain purchasing clout and R&D breadth, setting the stage for further consolidation.

Smart-City Demand for Connected Lighting Networks

Outdoor LED poles now serve as strategic real estate for IoT nodes, 5G small cells, and edge computers that power transportation, environmental, and public safety analytics. Chicago, Boston, and Miami each monetize data streams or lease pole rights to telecom operators, effectively turning lighting assets into revenue generators. Procurement requests, therefore, specify open-protocol wireless radios, over-the-air security patches, multi-layer encryption, and API-ready data lakes to future-proof infrastructure. While cybersecurity audits and interoperability testing lengthen project timelines, the ability to piggyback air-quality sensors or gunshot-detection devices onto existing power runs strengthens municipal business cases. Long-term service model lighting-as-a-service contracts, which bundle equipment, software, energy guarantees, and insurance, are gaining traction, shielding cities from rapid tech obsolescence while ensuring vendors remain accountable for uptime.

IIJA-Funded Roadway Lighting Upgrades

The Infrastructure Investment and Jobs Act earmarks USD 7.5 billion for roadway safety projects that stipulate dark-sky compliant, fully shielded LED fixtures with a correlated color temperature of under 3000 K. Federal emphasis on underserved rural corridors opens a pipeline of projects for manufacturers equipped with Buy American Act supply chains and certified recycling programs. Integrated asset-management sensors, capable of tracking power consumption and pole vibrations, are becoming mandatory because the Federal Highway Administration now prioritizes measurable safety and energy metrics for grant eligibility. Vendors offering turnkey packages from photometric design to long-horizon performance guarantees are winning multi-county awards, encouraging smaller jurisdictions to piggyback onto master contracts to secure volume pricing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of smart/connected systems | -0.4% | National, particularly affecting smaller municipalities and rural areas | Short term (≤ 2 years) |

| Blue-rich-light ordinances and community backlash | -0.2% | Concentrated in environmentally conscious communities, West Coast and Northeast | Medium term (2-4 years) |

| Semiconductor supply-chain volatility | -0.3% | Global impact with regional variations based on supplier relationships | Short term (≤ 2 years) |

| Cyber-security and protocol-compatibility gaps | -0.1% | Metropolitan areas with advanced smart city initiatives | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Smart/Connected Systems

Networked luminaires featuring radios, sensors, and cybersecurity firmware can cost two to three times more than conventional LED fixtures, straining budgets already stretched by capital improvement backlogs. For towns without access to green bonds or federal matching grants, financing hurdles deter comprehensive upgrades, prompting officials to opt for piecemeal deployments that limit economies of scale. The expense increases further once backhaul connectivity, cloud storage, and security certificates are factored in, often doubling per-pole project totals in early bids. To mitigate sticker shock, vendors are introducing phased rollouts and performance-based savings models; however, credit-rating constraints and procurement rules continue to slow deal closure. Consequently, the US outdoor LED lighting market occasionally sees delayed purchase orders and re-scoped project scopes until grant cycles align with council approvals.

Semiconductor Supply-Chain Volatility

LED driver ICs, power transistors, and high-efficacy chips are still concentrated in a handful of Taiwanese and South Korean fabs, leaving production vulnerable to trade disputes, energy shortages, and natural disasters. During 2024, component spot prices increased by 15-25%, prompting manufacturers to include variable-price clauses and extend delivery promises from eight to 20 weeks.[3]U.S. Department of Commerce, “Commerce Department Launches CHIPS America Task Force,” commerce.gov For fixed-bid municipal contracts, these swings erode contractor margins and can trigger penalty clauses tied to missed completion milestones. Several suppliers have started dual-sourcing critical parts and expanding U.S. assembly lines, but substrate and phosphor bottlenecks remain firmly offshore. Until redundancy programs mature, procurement officers will incorporate contingency buffers into their schedules, and the US outdoor LED lighting market will continue to experience a modest drag on acceleration due to supply uncertainty.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Luminaires Drive Integration Trends

Luminaires controlled 69.84% of 2025 sales, underscoring a shift toward fully integrated fixtures that combine optical precision, surge protection, and edge-computing connectivity in a single housing. This dominance reflects both municipal preference for unitary warranties and federal incentives favoring Buy American-compliant assemblies, even when printed circuit boards originate overseas. The luminaires sub-segment within the US outdoor LED lighting market, therefore, captures high-margin service contracts tied to predictive maintenance dashboards. Lamps, while historically relegated to quick-fix retrofits, now enjoy a 6.02% CAGR as field-adjustable products offer several lumen packages and color temperatures in a single SKU. These versatile solutions align with budget-restrained towns seeking incremental upgrades before embarking on full network conversions. Despite rising lamp volume, revenue share skews toward luminaires because each pole replacement often bundles sensors, remote controllers, and anti-glare optics at premium pricing. Over the 2026-2031 period, vendors expect luminaires to anchor platform ecosystems, while lamps will find niches in heritage fixtures, temporary work zones, and emergency rebuilds following weather events.

Second-generation luminaires integrate multi-band radios, Bluetooth beacons, and self-diagnosing drivers, effectively future-proofing assets for forthcoming 5G densification. Open-protocol designs ease compatibility with third-party CMS software, reducing vendor lock-in concerns among procurement managers. Conversely, lamp suppliers differentiate themselves via plug-and-play gear trays, enabling one-for-one swaps without bucket-truck downtime a feature attractive to facility owners operating around-the-clock transit terminals. As prices converge, the US outdoor LED lighting market sees a transition from a rivalry based on cost leadership to one centered on functionality wars, with a focus on cybersecurity certifications, over-the-air upgrade capability, and lifecycle environmental scores. That competitive narrative encourages continuous R&D spend, protecting margins even as raw luminosity improvements plateau.

By Application: Sports Venues Lead Innovation Adoption

Street and roadway corridors retained 42.35% of the revenue in 2025, thanks to a vast installed base and ongoing conversions of high-pressure sodium fixtures to full-cutoff LED optics. Federal visibility mandates and rising pedestrian safety campaigns keep this segment baseline robust. Yet sports and stadium projects register the fastest trajectory at 4.63% CAGR, catalyzed by broadcast rights deals and evolving spectator expectations that demand flicker-free, high-CRI illumination adaptable for slow-motion replays. Cricket grounds, soccer arenas, and collegiate football stadiums are increasingly specifying programmable RGB-white fixtures capable of instant show-light sequences, thereby heightening fan engagement and securing sponsorship activations. Architectural accents, tunnels, and bridge niches also gain momentum as design-build teams incorporate color-tunable floodlights to reinforce civic landmarks and enhance tourist experiences.

Sports venue clients prioritize glare control, camera-ready uniformity, and dynamic scene setting, pushing manufacturers to develop narrow-beam precision optics and fanless heat sinks for acoustically sensitive arenas. Premium specification unlocks accessory revenue, wireless DMX controls, cloud-based content servers, and interactive fan apps, extending wallet share well beyond initial fixture sales. Conversely, roadway buyers remain cost-focused, valuing vandal-resistant housings, tilt-adjustable brackets, and lumen maintenance with a lifespan of over 100,000 hours. In response, vendors segment product families, ensuring the US outdoor LED lighting market can satisfy both commodity highway rollouts and high-spec sports contracts without cannibalizing margin structure.

By Installation Type: Retrofit Acceleration Signals Market Maturity

New installations accounted for 52.78% of 2025 revenues across subdivision builds, interstate expansions, and downtown revitalization programs. These projects generally specify smart-ready poles capable of hosting air-quality sensors, ALPR cameras, and small cell radios features that justify premium fixture costs and multi-year service attachments. The growing preference for integrated poles supports steady unit growth, particularly along federally funded corridors and smart district pilot zones. Emerging net-zero building codes further elevate demand for adaptive dimming and renewable energy-paired luminaires, magnifying the value per installation. Retrofit activity, however, is growing faster, increasing 5.07% annually as municipalities revisit first-wave LEDs from 2015-2018 whose photometric performance and control protocols are now outdated. Many early adopters discover upward of 30% additional energy savings and new revenue streams from data applications, turning secondary retrofits into investment enablers rather than cost obligations.

Accelerated retrofit momentum signals market maturation, with an emphasis shifting from raw replacement counts to lifecycle management and software-driven asset optimization. Contractors develop specialized crews trained in wireless commissioning and GIS data capture, which reduces the number of labor hours per fixture and enables nighttime swap programs that minimize traffic disruption. Capital constraints remain, yet lighting-as-a-service models, offering zero-down financing with guaranteed savings, have unlocked credit-averse districts. Consequently, the US outdoor LED lighting market is finding that retrofit schedules are synchronizing with broader municipal broadband rollouts, allowing one trenching event to accommodate fiber pulls, conduit upgrades, and lighting controls simultaneously, thereby minimizing public inconvenience and maximizing grant alignment.

By Distribution Channel: E-Commerce Disrupts Traditional Models

Direct sales accounted for 62.95% of the 2025 value, driven by the provision of complex specification support, Buy American compliance documentation, and turnkey project management, all bundled into manufacturer or lighting-agent proposals. National accounts teams cultivate multi-phase agreements that fold controls software and 15-year warranties into a single procurement package, meeting the risk-mitigation appetite of public agencies. That said, e-commerce is outpacing every other channel at a 4.29% CAGR, boosted by intuitive configurators, BIM-friendly download libraries, and real-time inventory status, which is beneficial to contractors on accelerated schedules. Standardized roadway luminaires now list on governmental e-marketplaces, reducing paperwork friction and shortening purchase-order cycles.

Wholesalers and brick-and-mortar distributors have responded by launching hybrid click-and-collect models; however, their growth lags due to the provision of thinner value-added services compared to manufacturer portals, which offer instant photometric files and dynamic pricing. Smaller towns appreciate the transparency of online platforms, though many still route final approvals through regional energy offices to certify rebate eligibility. Over the forecast horizon, the US outdoor LED lighting market is expected to exhibit a channel blend, where e-commerce will capture routine replacements and add-ons, while direct sales will dominate large-scale, integrated infrastructure packages that require field engineering, commissioning, and post-occupancy analytics.

Geography Analysis

Regional adoption within the US outdoor LED lighting market differs sharply because state codes, utility incentives, and climate-resilience priorities vary. California and New York anchor penetration levels above 80% across arterial roads, leveraging Title 24 mandates and CLCPA net-zero statutes that oblige municipalities to adopt adaptive controls and low-CCT optics. West Coast cities integrate networked poles into disaster-readiness protocols, earthquake early-warning sensors piggyback on lighting networks, reinforcing smart-city valuations. Northeastern metros, confronting aging infrastructure and rising congestion tolls, incorporate lighting upgrades into broader curb-management initiatives that synchronize curbside pickups, bus lanes, and pedestrian crossings with real-time data feeds, thereby maximizing asset utilization.,

The Southeast and Gulf Coast post-accelerating demand as hurricane-recovery funds finance hardened, quick-deploy LED poles with battery-backed electronics. Florida's Turnpike Enterprise replaces legacy HID fixtures with solar-hybrid units capable of autonomous operation during grid outages, thereby improving evacuation route safety. Texas municipalities, flush with sales-tax revenue from population inflows, apply surplus cash to downtown corridor beautification projects that prioritize color-tunable façade illumination for placemaking. Midwest adoption trails coastal leaders yet gains impetus from USDA rural-development grants that subsidize high-mast LEDs at grain terminals, ethanol plants, and rail yards critical nodes for Midwest commodity logistics.

Mountain and desert states showcase advanced dark-sky ordinances, capping CCT at 3000 K to protect astrophotography and wildlife. Tucson's countywide retrofit aggregates 100,000 smart LEDs linked to a cloud-based platform that dims lamps until motion sensors detect approaching cars, demonstrating that sustainability and stargazing tourism can align. The aggregation model informs similar consortium bids across Nevada and Utah, where small municipalities pool volumes to entice tier-one suppliers. Across all zones, the US outdoor LED lighting market is converging toward tunable controls and asset-monitoring software; however, the adoption pace hinges on each region's access to funding, climatic threats, and regulatory requirements.

Competitive Landscape

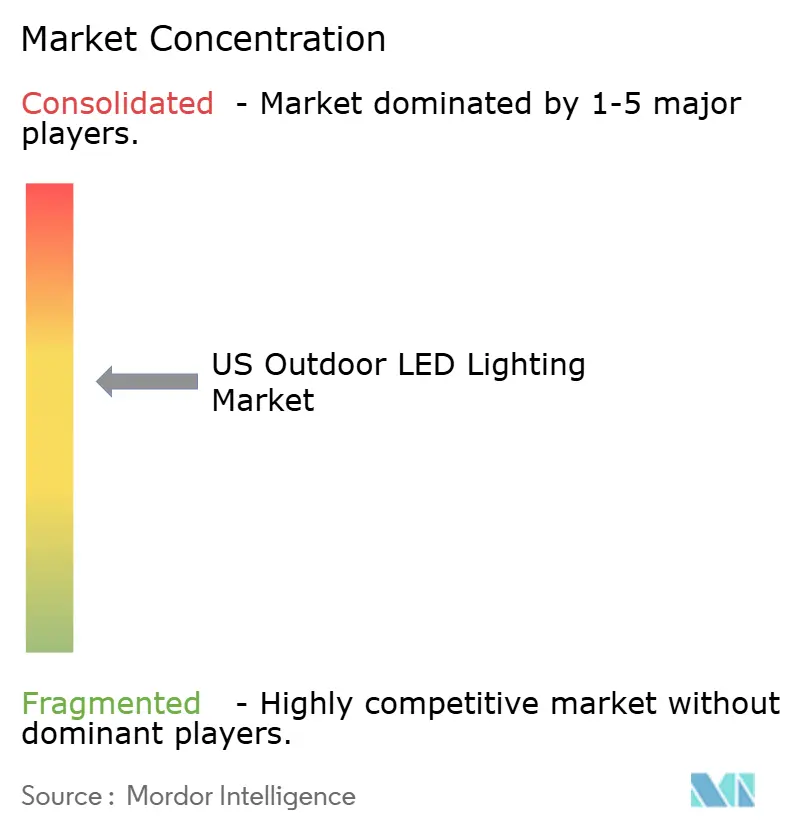

Competitive intensity is moderate, with the five largest suppliers holding roughly 38-45% of the collective revenue, leaving a meaningful space for specialists. Acuity Brands, Signify, and Eaton anchor the top tier due to their vertical integration, domestic assembly lines, and broad agent networks that penetrate municipal specification committees. Their dominance stems not only from product breadth but also from bundled analytics services that transform luminaires into data hubs feeding building-management platforms. Cooper and Hubbell reinforce positions via proprietary controls, protocols, and cybersecurity certifications, often winning institutional bids where network resilience proof is mandatory.

Emerging disruptors carve niches through sports lighting engineering, solar-hybrid poles, and ultra-narrow beam optics for historic districts. Firms such as Musco and Ephesus engineer flicker-free broadcast systems, while start-ups targeting wildlife corridors offer amber-rich spectra below 2200 K. Private-equity-backed consolidators have acquired regional rep agencies to achieve scale in technical sales, as illustrated by LSI Industries' purchase of Canada's Best Holdings, an approach that merges signage fabrication with lighting, cross-selling to quick-service retail chains.[4]Inside Lighting, “LSI Industries Bolsters Display Business with CBH Acquisition,” inside.lighting Intellectual property litigation, exemplified by Cooper's indemnification suit against the Ephesus founders, underscores the value and risk associated with optical patents and driver algorithms.

Strategic moves center on software ecosystems, with Signify expanding the Interact platform's edge-processing modules to enable predictive maintenance and intrusion detection. Eaton recently integrated its power-distribution assets into its lighting business, offering turnkey microgrid-plus-lighting contracts to industrial customers seeking enhanced resilience. Acuity's 2024 manufacturing expansion in Mexico supports Buy American compliance while mitigating tariff exposure, demonstrating supply chain agility as a competitive advantage. Looking ahead, suppliers will compete on security credentials, lifecycle carbon transparency, and the ability to integrate third-party IoT devices, pushing the US outdoor LED lighting market toward a platform-centric rivalry.

United States Outdoor LED Lighting Industry Leaders

Acuity Brands, Inc.

Signify N.V.

Eaton Corporation plc

Hubbell Incorporated

LSI Industries Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: LSI Industries completed the acquisition of Canada's Best Holdings for USD 31 million, including performance-based earn-outs, adding USD 24.2 million in annual sales and expanding the company's display business to 60% of total revenue while maintaining lighting as a core segment with cross-selling opportunities for integrated fixture and signage solutions.

- February 2025: Cooper Lighting filed a lawsuit against Ephesus Lighting founders Joe and Amy Casper, seeking USD 3.5 million in indemnification related to patent infringement claims from TruSun Technologies, highlighting ongoing intellectual-property challenges in the LED sports-lighting segment and the complex legacy issues from industry consolidation.

- January 2025: Acuity Brands reported record fiscal 2024 results with net sales of USD 4.1 billion, driven by strong demand for smart-lighting solutions and integrated building-management systems, while expanding manufacturing capabilities to support growing municipal and commercial LED-lighting projects across North America.

- December 2024: Eaton Corporation completed its acquisition of Power Distribution Inc. for approximately USD 2.6 billion, strengthening the company's electrical infrastructure portfolio and enhancing capabilities to support large-scale LED-lighting installations in industrial and municipal applications.

United States Outdoor LED Lighting Market Report Scope

Public Places, Streets and Roadways, Others are covered as segments by Outdoor Lighting.| Lamps |

| Luminaires/Fixtures |

| Street and Roadway Lighting |

| Architectural and Landscape |

| Sports and Stadium |

| Tunnel and Bridge |

| Parking and Transit Areas |

| Other Applications |

| New Installation |

| Retrofit Installation |

| Direct Sales |

| Wholesale |

| Retail |

| E-commerce |

| By Product Type | Lamps |

| Luminaires/Fixtures | |

| By Application | Street and Roadway Lighting |

| Architectural and Landscape | |

| Sports and Stadium | |

| Tunnel and Bridge | |

| Parking and Transit Areas | |

| Other Applications | |

| By Installation Type | New Installation |

| Retrofit Installation | |

| By Distribution Channel | Direct Sales |

| Wholesale | |

| Retail | |

| E-commerce |

Market Definition

- INDOOR LIGHTING - It incorporates all LED based lamps and fixtures/luminaire that are used to illuminate indoor section of residential, commercial, industrial buildings and agricultural lighting. LED offers efficient brightness with higher durability in comparison to other lighting technology.

- OUTDOOR LIGHTING - It incorporates the LED lighting fixtures that is used for illumination for exterior/outdoor illumination. For instance, LED lighting fixtures used to illuminate streets and highways, transport hubs, stadiums and other public places such as parking spaces.

- AUTOMOTIVE LIGHTING - It refers to the lighting fixtures installed for illumination and signaling purposes. It is used in both exterior and interior lighting of the vehicle. Headlamps, fog lamp, daytime running light (DRLs) are examples of exterior light whereas cabin light are interior lights.

- END USER - It refers to the end use application area where the LED fixture will be installed. For instance, in terms of indoor lighting, we have residential, commercial and industrial as end user category. For automotive lighting, primary end user considered are automotive manufacturers and aftermarket sale

| Keyword | Definition |

|---|---|

| Lumen | Lumen is a unit of luminous flux in the International System of Units that is equal to the amount of light given out through a solid angle by a source of one-candela intensity radiating equally in all directions. |

| Footcandle | A foot-candle (or foot-candle, fc, lm/ft2, or ft-c) is a measurement of light intensity. One foot-candle is defined as enough light to saturate a one-foot square with one lumen of light. |

| Colour Rendering Index (CRI) | Color Rendering Index (CRI) is a measurement of how natural colors render under an artificial white light source when compared with sunlight. The index is measured from 0-100, with a perfect 100 indicating that colors of objects under the light source appear the same as they would under natural sunlight. |

| Luminous flux | Luminous flux is a measure of the power of visible light produced by a light source or light fitting. It is measured in lumens (lm). |

| Annual Energy Cost | Annual Energy Cost means the average daily energy consumption multiplied by 365 (days per year), expressed in kilowatt hour per year (kWh/a). |

| Constant voltage drivers | Constant voltage drivers are designed for a single direct current (DC) output voltage. Most common constant voltage drivers (or Power Supplies) are 12VDC or 24VDC. An LED light that is rated for constant voltage usually specifies the amount of input voltage it needs to operate correctly. |

| Constant Current Driver | Constant current LED drivers are designed for a designated range of output voltages and a fixed output current (mA). LEDs that are rated to operate on a constant current driver require a designated supply of current usually specified in milliamps (mA) or amps (A). These drivers vary the voltage along an electronic circuit which allows current to remain constant throughout the LED system. |

| Minimum Energy Performance Standards (MEPS) | Minimum Energy Performance Standards specify the minimum level of energy performance that appliances and equipment must meet or exceed before they can supply or used for commercial purposes. |

| Luminous Efficacy | Luminous efficacy is a measurement commonly used in the lighting industry that indicates the ability of a light source to emit visible light using a given amount of power. |

| Solid State Lighting | Solid-state lighting (SSL) is a type of lighting that uses semiconductor light-emitting diodes (LEDs), organic light-emitting diodes (OLED), or polymer light-emitting diodes (PLED) as sources of illumination rather than electrical filaments, plasma (used in arc lamps such as fluorescent lamps), or gas. |

| Rated Lamp Life | Lamp life, also referred to as rated life, is the time in hours a lamp will last before a percentage of lamps will burn out. |

| Color Temperature | Colour temperature is a scale that measures how ‘warm’ (yellow) or ‘cool’ (blue) the light from a particular source is. It is measured in degrees of the Kelvin scale (abbreviated to K), and the higher the number, the ‘cooler’ the light. The lower the ‘K’ number, the ‘warmer’ the light. |

| Ingress Protection rating (IP rating) | The IP (Ingress Protection) rating of a bulb or light fixture declares the level of protection it has against dirt and water. |

| Fidelity Index | The general colour fidelity index, Rf, represents how closely the colour appearances of the entire sample set are reproduced (rendered) on average by a test light as compared to those under a reference illuminant. |

| Gamut Index | The gamut area is defined as “the area enclosed by a set of test color samples illuminated by a light source, in a two-dimensional chromaticity diagram or a plane of color space.”1 Within a defined color space, a “gamut” describes the subset of colors that can be perceived under specific lighting conditions. |

| Binning | In the lighting industry, the act of "binning" of LEDs is the process of sorting LEDs by certain characteristics, such as color, voltage, and brightness. |

| Accent lighting | Accent lighting, also called highlighting, emphasizes objects by focusing light directly on them. Accent lighting is used inside and outside the home to feature locations such as an entrance or to create dramatic effects. |

| Dimmable driver | A dimming driver has two functions: As a driver, it converts the 230V AC mains input to a low voltage DC output. As a dimmer, it reduces the amount of electrical energy flowing to the LEDs, thereby causing them to dim. |

| Flicker | Flicker is the repeated and frequent variation in the output of a light source over time. |

| Fluorescent | A property of materials defined as the ability to emit light after absorbing electromagnetic radiation such as visible or UV light. |

| Candela | The candela is the unit of luminous intensity in the International System of Units. It measures the light output per unit solid angle emitted from a light source in a specific direction. |

| LUX | Lux is used to measure the amount of light output in a given area - one lux is equal to one lumen per square meter. It enables us to measure the total "amount" of visible light present and the intensity of the illumination on a surface. |

| Uniformity (U0) | The uniformity of lighting has significant effects on visual performance in both indoor and outdoor areas. Uniformity (represented as U0) value can be found by dividing the minimum brightness (Emin) resulting from calculations according to the current lighting order, to the average brightness value (Eavg). |

| Visible Light Spectrum | The visible light spectrum is the segment of the electromagnetic spectrum that the human eye can view. More simply, this range of wavelengths is called visible light. Typically, the human eye can detect wavelengths from 380 to 700 nanometers. |

| Ambient Temperature | Ambient Temperature is the temperature of the air surrounding an electrical enclosure. |

| Current-controlled dimming control | Current-controlled dimming controls LED brightness by varying the applied current using a 0-10V dimmer. Current-controlled dimming is smooth and HD-video friendly. It can only dim to a minimum of 5% of light output. |

| Design Light Consortium | It is a partnership of energy efficiency stakeholders in the United States and Canada to “promote quality, performance and energy efficient lighting solutions for the commercial sector”. |

| Pulse Width Modulation | Pulse-width modulation, or pulse-duration modulation, is a method of controlling the average power delivered by an electrical signal. |

| Surface Mounted Device | A surface mount device (SMD) is an electronic device whose components are mounted or placed directly on the surface of a printed circuit board. |

| Alternating Current | Alternating current is an electric current which periodically reverses direction and changes its magnitude continuously with time, in contrast to direct current, which flows only in one direction. |

| Direct Current | Direct current (DC) is an electric current that is uni-directional, so the flow of charge is always in the same direction. |

| Beam Angle | Beam angle (also called beam spread) is a measure of how light is distributed. On any plane perpendicular to the centerline of the light, the beam angle is the angle between two rays where the light intensity is 50% of the maximum light intensity. |

| LED Based Solar High Mast Lighting Systems | A Solar LED High Mast Light is a raised source of High illumination lights (6~8 lights) and with high intensity on the middle of major junctions (Ring roads, Outer Ring roads), turned on or lit automatically in the absence of light (at specified timings or at periodic times, every night). |

| Surface Mounted Diode (SMD) LEDs | A surface mount diode is a type that emits light and is flat mounted and soldered onto a circuit board. |

| Chip on Board (COB) LEDs | A COB LED is basically multiple LED chips (usually 9 or more) glued directly onto a substrate by the manufacturer to form a single module. |

| Dual In-Line Package (DIP) LEDs | A dual in-line package (DIP or DIL) is an electronic component package with a rectangular case and two parallel rows of electrical connector pins. |

| Graphene LED Lights | A graphene LED light bulb is simply an LED light bulb where the filament has been coated in graphene. A graphene LED bulb is reported to be 10% more efficient than regular LED light bulbs and they are cheaper to manufacture and buy. |

| LED Corn Bulbs | LED Corn lights are designed as an energy efficient alternative to high intensity discharge (HID) and SON lamps. It uses a large number of LEDs on a metal structure to provide sufficient light. This arrangement of LEDs looks a lot like a corn cob, hence the name "corn light". |

| Per Capita Income | Per capita income or total income measures the average income earned per person in a given area in a specified year. It is calculated by dividing the area's total income by its total population. Per capita income is national income divided by population size. |

| Charging Stations | A charging station, also known as a charging station or electric vehicle utility, is a power supply that provides electrical energy for charging plug-in electric vehicles. |

| Headlight | A headlight is a light that is mounted on the front of a car and illuminates the road in front of it. Low beam and high beam LED headlights are additional categories for these LED headlights. |

| Day Time Running Light (DRLs) | A daytime running lamp is a white, yellow, or amber lighting device mounted on the front of a road-going motor vehicle or bicycle. |

| Directional Signal Light | Directional signal lights are the front and rear lights on an automobile that flash to show the direction of a turn. |

| Stop Light | A red light that is mounted to the back of a car and turns on when the brakes are used to show that the car is stopped. |

| Reverse Light | The reverse light is at the back of the vehicle to indicate its backward motion. |

| Tail Light | A red light that can be seen in the dark is mounted on the rear of a road vehicle. Stop, reverse, and directional signal lights are all part of it. |

| Fog Light | Bright lights in automobiles used to increase visibility on the road in foggy conditions or to warn other drivers of the presence of the vehicle. |

| Passenger Vehicle | A passenger vehicle is a road vehicle, other than a moped or a motorcycle, intended for the transportation of people and designed for up to 8 to 9 seats. |

| Commercial Vehicle | A commercial vehicle (Bus, Truck, Van) is any type of motor vehicle used to transport goods or pay passengers. |

| Two Wheelers (2W) | A two-wheeler is a vehicle that runs on two wheels. |

| Streets & Roadways | Both roads and streets refer to hard, flat surfaces on the ground on which vehicles, people, and animals can travel. Since streetways are usually in cities and towns, they often have houses and buildings on both sides. The roadway is in the countryside and sometimes passes through forests and fields |

| Horticulture Lighting | Horticulture is the science and art of sustainably growing, producing, marketing and using high quality, intensively cultivated food and ornamental plants. |

Research Methodology

Mordor Intelligence has followed the following methodology in all our data center reports.

- Step 1: Raw Data Collection: To understand the market, initially, all crtical data points were identified. Critical information about countries and regions of interest including Per-capita Income, Population, Automotive Production, Interest rate on Auto-Loans, Number of Automobiles on Road, Total LED Import, Lighting Electricity Consumption among others were recorded or estimated based on internal calculations.

- Step 2: Identify Key Variables: To build a robust forecasting model, key variables such as Number of Households, Automotive Production, Road Networks among others were identified. Through an iterative process, the variables required for the market forecast were set, and the model was built using these variables.

- Step 3: Build a Market Model: Based on data and critical industry trend data (variables), including LED pricing, LED penetration rate, and project macro and micor economic factors were utilized for building the market forecasting.

- Step 4: Validate and Finalize: In this crucial step, all market numbers and variables derived through an internal mathematical model were validated through an extensive network of primary research experts from all the markets studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step 5: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms