Automotive Lightweight Material Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

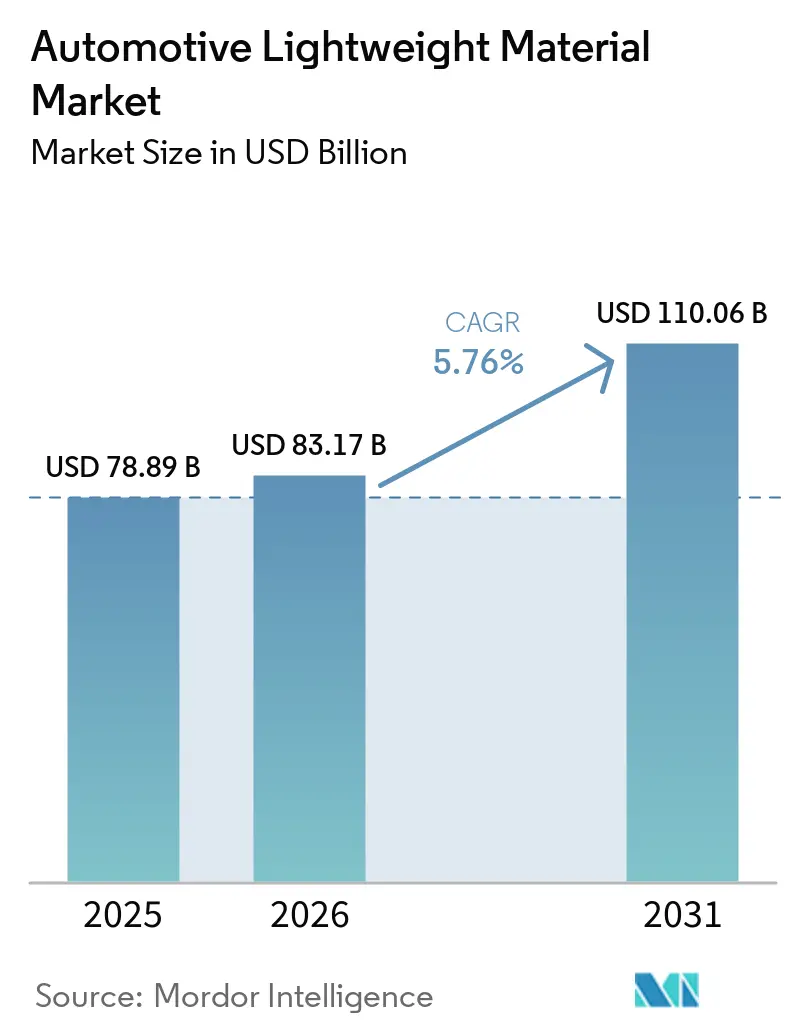

| Market Size (2026) | USD 83.17 Billion |

| Market Size (2031) | USD 110.06 Billion |

| Growth Rate (2026 - 2031) | 5.76% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Lightweight Material Market Analysis by Mordor Intelligence

The Automotive Lightweight Material Market size is projected to expand from USD 78.89 billion in 2025 and USD 83.17 billion in 2026 to USD 110.06 billion by 2031, registering a CAGR of 5.76% between 2026 and 2031. China's 2026 battery-electric energy-consumption norm, coupled with its dominance in gigacasting capacity, is driving the momentum. Polymers and composites, which make up a significant portion of the volume, are achieving substantial mass reductions. This directly enhances the vehicle's range and reduces battery costs. At the same time, next-generation aluminum alloys, ultra-high-strength steels, and magnesium castings are carving out specialized roles in crash zones, motor housings, and sensor mounts. Suppliers are increasingly pursuing vertical integration in component engineering, sourcing regionally to comply with trade regulations, and exploring carbon-free smelting and chemical-recycling technologies.

Key Report Takeaways

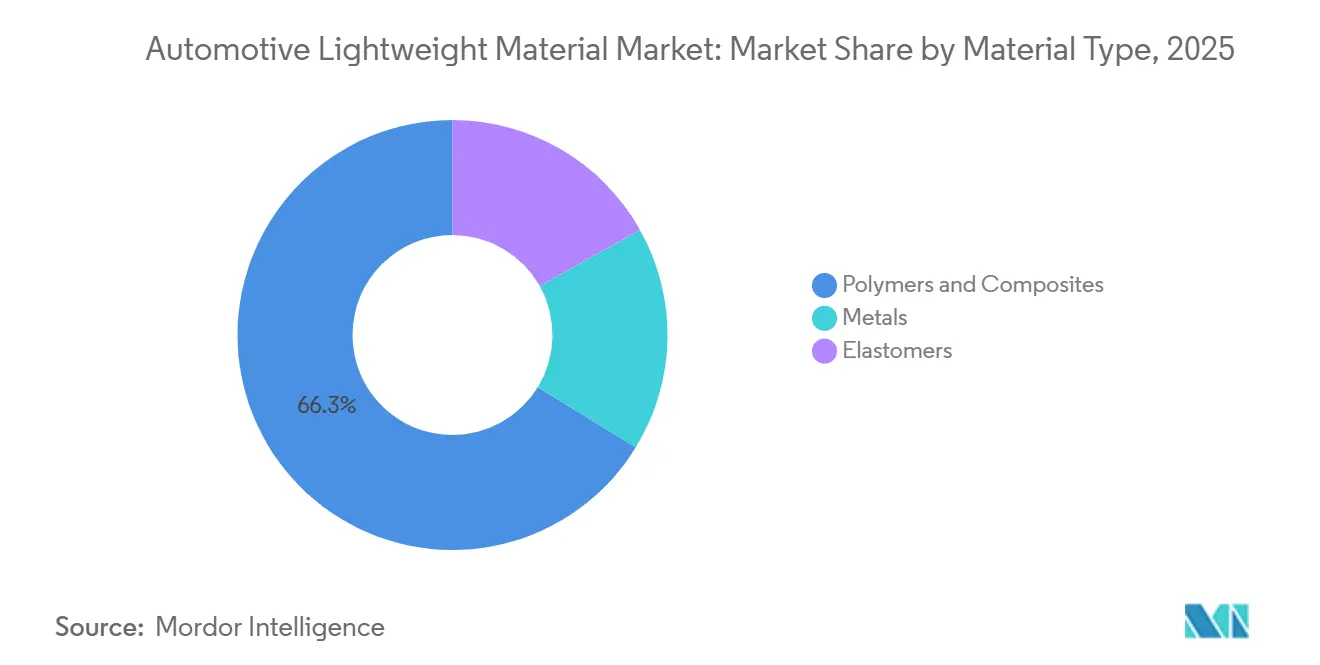

- By material type, polymers and composites accounted for 66.25% of the global automotive lightweight material market in 2025, while this segment is projected to post the fastest 6.56% CAGR between 2026 and 2031.

- By application, body‑in‑white represented 25.30% of the automotive lightweight material market size in 2025, whereas battery enclosures and thermal systems are forecast to expand at a 7.05% CAGR over 2026-2031.

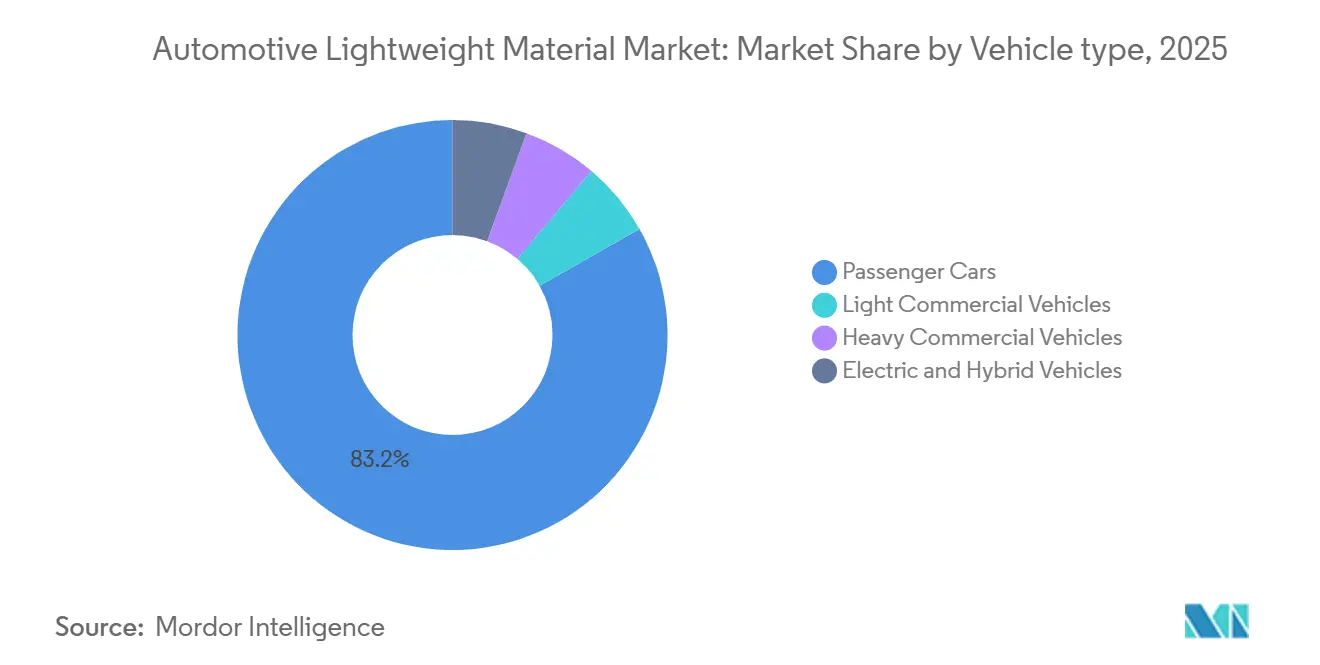

- By vehicle type, passenger cars captured 83.20% share in 2025; light commercial vehicles are expected to register a 7.01% CAGR between 2026 and 2031.

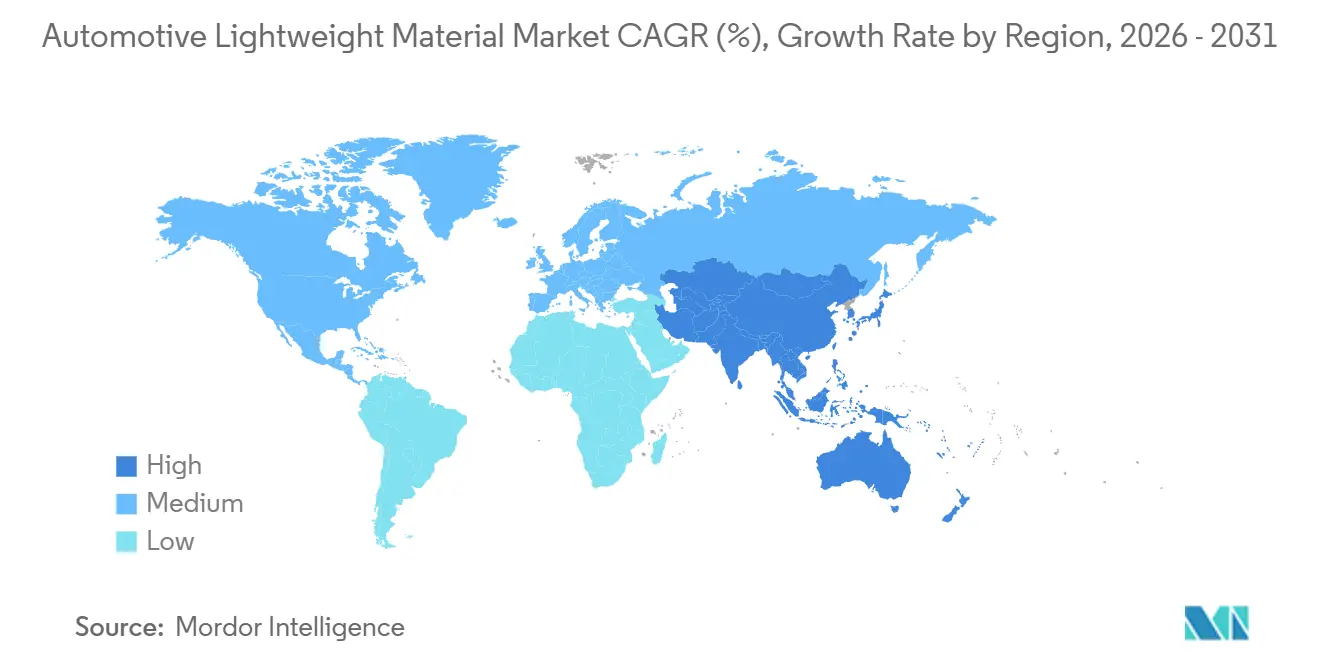

- By geography, Europe held 35.70% of global revenue in 2025, while Asia‑Pacific is projected to advance at the highest 7.12% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Lightweight Material Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for fuel-efficiency and CO₂-reduction | +1.80% | Global, EU, and China lead | Medium term (2-4 years) |

| Rising adoption of electric and hybrid vehicles | +2.10% | Global, concentrated in China, Europe, and North America | Short term (≤ 2 years) |

| Stringent global and regional vehicle-weight legislation | +1.20% | EU, China, North America | Long term (≥ 4 years) |

| Lightweighting for AI-sensor payload in autonomous cars | +0.40% | North America, Europe, China | Long term (≥ 4 years) |

| Circular-economy credits for embedded-carbon reduction | +0.70% | EU, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Fuel-Efficiency and CO₂-Reduction

Lifecycle-carbon accounting now prioritizes materials made with low-emission energy and a high recycled content. The European Union has set a target to significantly cut fleet carbon dioxide emissions by 2030. Importantly, the European Union will phase out super-credits after 2027, pushing automakers to make real reductions in emissions rather than depending on regulatory loopholes. In a move underscoring this trend, Mercedes-Benz has integrated low-emission aluminum into its electric compact luxury automobile, leading to a marked decrease in the vehicle's lifecycle emissions[1]Source: Sustainable Industry, “Mercedes and Low-Carbon Aluminium in EV Manufacturing,” sustainableindustry.co.uk. China's dual-credit system offers extra points for battery-electric models with lower curb weight. This incentive promotes the use of magnesium die castings and thermoplastic composites in compact platforms. Toyota has committed to increasing the use of recycled material by weight starting in 2030, highlighting the strategic importance of recycling. Reducing the weight of a battery-electric vehicle enhances its range and lowers battery costs, improving overall cost-of-ownership advantages.

Rising Adoption of Electric and Hybrid Vehicles

Battery packs are reshaping material economics: European battery-electric vehicles are set to increase aluminum usage, particularly in enclosures and motor housings. Giga-casting technology is consolidating multiple stamped parts into a single rear-floor module, leading to notable weight reductions and simplified welding. The use of composite battery enclosures is on the rise, with carbon fiber reinforced polymer providing significant weight savings over steel and added electromagnetic shielding. Chinese automakers are skipping traditional body-in-white lines in favor of advanced high-capacity presses, greatly speeding up their product cycles. With hybrids featuring both an engine and a battery, adopting lightweight closures and Advanced High-Strength Steel structures becomes vital to counterbalance the extra weight from the dual powertrain.

Stringent Global and Regional Vehicle-Weight Legislation

China's GB 43258-2024 energy regulation, set to take effect in 2026, caps energy consumption in kilowatt-hours per 100 kilometers, directly tying it to the vehicle's curb weight. This emphasizes the growing significance of lightweighting for compliance. In the United States, updated greenhouse gas standards, effective until the early 2030s, are steering larger sport utility vehicles toward lighter alloys and composites, especially as aerodynamic benefits plateau. Europe's End-of-Life Vehicles Regulation mandates a certain percentage of recycled content in vehicles by the decade's end, favoring thermoplastic composites for their remeltable properties. In India, the Phase II Corporate Average Fuel Economy target is tightening carbon dioxide emission limits. To achieve these goals, there is a shift toward ultra-high-strength steel and selective aluminum in budget segments, keeping vehicles affordable.

Lightweighting for AI-Sensor Payload in Autonomous Cars

Level 3-4 autonomy layers are integrating significant amounts of light detection and ranging systems, radar, and computing hardware into vehicles, which is reducing both their range and payload capacity. In 2024, Toyota Boshoku introduced a resin front-end module that consolidates multiple components into a single unit, effectively reducing its weight to accommodate sensors. Magnesium housings, which are considerably lighter than their aluminum counterparts, not only reduce weight but also offer enhanced electromagnetic shielding. The global magnesium die-casting market has been experiencing steady growth. Additionally, structural battery packs that serve a dual purpose as crash members have the potential to reduce overall vehicle mass. This reduction creates additional space for sensor suites without compromising the cabin area.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced composites and alloys | -1.40% | Global, acute in India and Southeast Asia | Short term (≤ 2 years) |

| Manufacturing and repair complexity | -0.80% | Global, mass-market segments | Medium term (2-4 years) |

| Supply-chain volatility in critical minerals | -0.60% | Global, aluminum, magnesium, carbon-fiber precursors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Composites and Alloys

Carbon-fiber polymers, which are significantly more expensive than high-strength steel, are primarily used in premium cars priced at the higher end of the market[2]Source: CompositesWorld, “Toray develops rapid integrated press molding technology for CFRP mobility components,” compositesworld.com . Toray's innovative press-molding technique reduces production time considerably; however, it remains costlier than aluminum, limiting its broader adoption. Magnesium die castings provide notable weight reduction but are more expensive, restricting their application mainly to sensor housings. In India, original equipment manufacturers focus on advanced high-strength steel and selective use of aluminum to achieve a balance between reducing vehicle weight and maintaining affordability, reflecting the region's sensitivity to pricing.

Manufacturing and Repair Complexity

Adhesive bonding, self-piercing rivets, and friction-stir welding are essential for multi-material bodies, which add complexity to crash repairs. While aluminum-steel hybrids significantly reduce weight, they also increase the risk of galvanic corrosion and lead to higher body-shop insurance premiums. The high cost of thermoplastic-composite compression molds, which are considerably more expensive than steel dies, discourages their use in programs with lower production volumes. Even with Teijin's efficient production cycle for the General Motors Company Sierra pickup box, this option still involves a notable cost premium.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Composites Leverage Superior Range Economics

Polymers and Composites dominated with 66.25% of the automotive lightweight material market share in 2025 and are projected to post a 6.56% CAGR from 2026 to 2031. Carbon-fiber enclosures, lighter than aluminum by a significant percentage, boost electric-vehicle range and reduce battery size. The automotive lightweight material market, focusing on polymers and composites, is expected to experience substantial growth from the latter part of this decade into the early 2030s, driven by the adoption of glass-fiber shields, wheel-arch liners, and underbody panels in mainstream models. Engineering plastics like polyamide and polypropylene benefit from BASF’s chemically recycled Cycled feedstock, aligning with circular-content mandates without the need for requalification.

While metals held a notable share in recent years, they are still adapting. Aluminum leads in volume, thanks to established supply chains and its superior thermal conductivity, making it a top choice for battery housings. Advanced high-strength steels, known for their exceptional tensile strength, are now prioritized for crash-critical pillars and rails, allowing for localized thickness reduction without compromising weldability. Magnesium alloys, with a modest share, find their niche in steering and sensor housings, though oxidation control inflates casting costs. Due to its high cost, titanium is a luxury reserved for supercars. Looking ahead to the early 2030s, metals are set to maintain a significant portion of the automotive lightweight material market, as innovations like next-generation alloys and carbon-free smelting bridge the carbon gap with composites.

By Application: Battery Enclosures Outpace Traditional Structures

Body-in-white claimed 25.30% revenue in 2025, mirroring the legacy steel platform mix, yet battery enclosures and thermal systems are advancing at a 7.05% CAGR from 2026 to 2031. Novelis' Gen2 multi-material housing is designed to achieve significant improvements in energy density while reducing overall mass compared to earlier aluminum solutions. As the adoption of battery electric vehicles continues to grow, the market for lightweight materials in automotive battery enclosures is expected to expand substantially by 2031.

Chassis and suspension components are increasingly being manufactured using aluminum control arms and magnesium cross-members. This transition helps reduce unsprung mass and enhances the efficiency of regenerative braking systems. Similarly, powertrain and drivetrain casings are shifting from cast iron to aluminum. For instance, BMW has integrated the motor and power electronics in its iX3 model into a single aluminum casting, resulting in a notable reduction in weight. Interior components are now being developed with glass-fiber polyamide, which offers significant weight savings and allows for clip-in features, eliminating the need for traditional fasteners. On the exterior, fascias are being produced using polycarbonate and thermoplastic olefins, ensuring compliance with pedestrian impact standards.

By Vehicle Type: Commercial Fleets Prioritize Payload Preservation

Passenger cars represented 83.20% of demand in 2025 due to regulatory fleet-average targets and consumer range expectations. However, light commercial vehicles will see the fastest 7.01% CAGR between 2026 and 2031 as last-mile delivery fleets transition to electric; the weight of a seventy-five kilowatt-hour battery adds significant weight compared to diesel. This weight increase is prompting operators to turn to aluminum cargo boxes and composite panels, helping them reclaim some of the lost payload. Over the coming years, the market size for lightweight materials in vans is expected to grow substantially.

In the near future, electric and hybrid vehicles are anticipated to account for a considerable share of lightweight material consumption, despite holding a smaller share in production. European battery electric vehicles are projected to use significantly more aluminum compared to their internal combustion engine counterparts. Meanwhile, hybrid vehicles are strategically using advanced high-strength steel cores combined with aluminum closures to mitigate the weight penalty of their dual powertrains. While heavy trucks traditionally rely on steel, they are now incorporating aluminum cabs and composite fairings, especially in long-haul tractors. In such cases, even a small reduction in weight can lead to noticeable improvements in fuel economy.

Geography Analysis

With Europe accounting for 35.70% of the automotive lightweight material market size in 2025, German original equipment manufacturers are optimizing performance to-cost ratios by rolling out aluminum giga-cast rear structures, advanced high-strength steel crash zones, and composite liftgates on the same platform. BMW’s iX3 demonstrates that high-quality scrap, when paired with artificial intelligence defect detection, can meet safety-critical standards, as it incorporates a significant proportion of recycled aluminum in its wheel-carrier castings. These moves come as the European Union sets ambitious fleet carbon dioxide emission reduction targets, imposes tariffs on carbon-intensive imports, and mandates increased use of recycled content in manufacturing by the end of the decade.

Asia-Pacific will expand at a 7.12% CAGR from 2026 to 2031. China, with a significant primary-aluminum output, continues to tighten its supply ceiling. Yet, the nation leads in large-scale casting operations, utilizing high-capacity presses at plants for BYD, NIO, and Xiaomi. Over the coming years, extrusion capacity for automotive profiles is expected to grow substantially, driven by the increasing adoption of battery electric vehicle platforms. Japan is advancing techniques for the rapid welding of thermoplastic composites. Meanwhile, India, aiming to achieve a notable share of electric vehicle penetration by the end of the decade, is investing in advanced high-strength steel cold-rolling and aluminum production to strengthen its localized supply chain.

North America captured a significant portion of the market, supported by local-content mandates under the United States-Mexico-Canada Agreement and incentives for battery sourcing introduced by the Inflation Reduction Act. Novelis is set to commission a major mill in the United States in the latter half of the decade, which will supply automotive sheet and enclosure stock to leading manufacturers such as Tesla, General Motors, and Ford. Mexico is emerging as a key hub for large-scale casting operations to support regional supply chains. At the same time, Canada is piloting carbon-free smelting technology under the ELYSIS initiative, aiming to differentiate itself based on embodied-carbon metrics.

Competitive Landscape

The Automotive Lightweight Material Market is moderately consolidated. Adhesive suppliers that can validate faster cure cycles at elevated temperatures, all while minimizing volatile emissions, stand poised to replace traditional spot-welding in aluminum-steel joints. The European Union-backed aluminum nanocomposites project achieves substantial weight reduction but still faces hurdles in scaling up non-destructive testing protocols. The race for patents is intensifying, centering on giga-casting process control, composite recycling, and topology optimization. Notably, Bayerische Motoren Werke AG secured intellectual property rights in Europe for its innovative injector casting, which boasts a lower-temperature mold filling technique that enhances mechanical properties.

Automotive Lightweight Material Industry Leaders

ArcelorMittal

Toray Industries, Inc.

Alcoa Corporation

Novelis

BASF

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The BMW Group, along with its partners, has earned the renowned JEC Composites Innovation Award for its work on series-production exterior components in automobiles. In June 2025, the company announced the integration of flax fiber-based natural composites in series-production vehicles to reduce the CO₂e footprint and achieve lightweight construction objectives.

- October 2025: Hyundai Motor Group and Toray Industries signed a Strategic Joint Development Agreement to co-develop advanced composite materials, integrating research and development, production, and commercialization for next-generation high-performance vehicles and mobility solutions.

Global Automotive Lightweight Material Market Report Scope

Automotive lightweight materials are advanced substances designed to reduce vehicle weight while maintaining strength, safety, and performance. Common examples include aluminum alloys, high-strength steel, magnesium, carbon fiber, and reinforced plastics. By lowering mass, these materials improve fuel efficiency, enhance handling, and reduce emissions. They are essential in modern automotive engineering, supporting sustainability goals and enabling innovative designs in electric and conventional vehicles alike.

The Automotive Lightweight Material Market is segmented by material type, application, vehicle type, and geography. By material type, the market is segmented into metals, polymers and composites, and elastomers. By application, the market is segmented into body-in-white, chassis and suspension, powertrain and drivetrain, interior components, exterior/trim, and battery enclosures and thermal systems. By vehicle type, the market is segmented into passenger cars, light commercial vehicles, heavy commercial vehicles, and electric and hybrid vehicles. The report also covers the market size and forecasts for the automotive lightweight material market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Metals | Aluminum |

| High-Strength Steel (AHSS/UHSS) | |

| Magnesium Alloys | |

| Titanium Alloys | |

| Polymers and Composites | Carbon-Fiber-Reinforced Polymer (CFRP) |

| Glass-Fiber-Reinforced Polymer (GFRP) | |

| Engineering Plastics | |

| Elastomers |

| Body-in-White |

| Chassis and Suspension |

| Powertrain and Drivetrain |

| Interior Components |

| Exterior/Trim |

| Battery Enclosures and Thermal Systems |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Electric and Hybrid Vehicles |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Material Type | Metals | Aluminum |

| High-Strength Steel (AHSS/UHSS) | ||

| Magnesium Alloys | ||

| Titanium Alloys | ||

| Polymers and Composites | Carbon-Fiber-Reinforced Polymer (CFRP) | |

| Glass-Fiber-Reinforced Polymer (GFRP) | ||

| Engineering Plastics | ||

| Elastomers | ||

| By Application | Body-in-White | |

| Chassis and Suspension | ||

| Powertrain and Drivetrain | ||

| Interior Components | ||

| Exterior/Trim | ||

| Battery Enclosures and Thermal Systems | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Heavy Commercial Vehicles | ||

| Electric and Hybrid Vehicles | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the automotive lightweight material market?

The automotive lightweight material market stands at USD 83.17 billion and is forecast to reach USD 110.06 billion by 2031 at a 5.76% CAGR from 2026 to 2031.

Which region is growing the fastest for lightweight materials in vehicles?

Asia-Pacific is projected to experience the highest 7.12% CAGR through 2031, driven by China’s giga-casting capacity and energy-consumption standards.

Why are battery enclosures a key growth application?

Battery housings account for the heaviest single component in electric vehicles, and multi-material enclosures can cut weight by up to 50%, directly extending driving range.

What share of demand do polymers and composites hold?

They captured 66.25% of global demand in 2025 and continue to gain share due to superior weight reduction and regulatory credit benefits.

How are suppliers differentiating in this market?

Leading companies are vertically integrating into component engineering, investing in low-carbon smelting, and developing fast multi-material joining technologies to win Original Equipment Manufacturer (OEM) programs.

Page last updated on: