Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

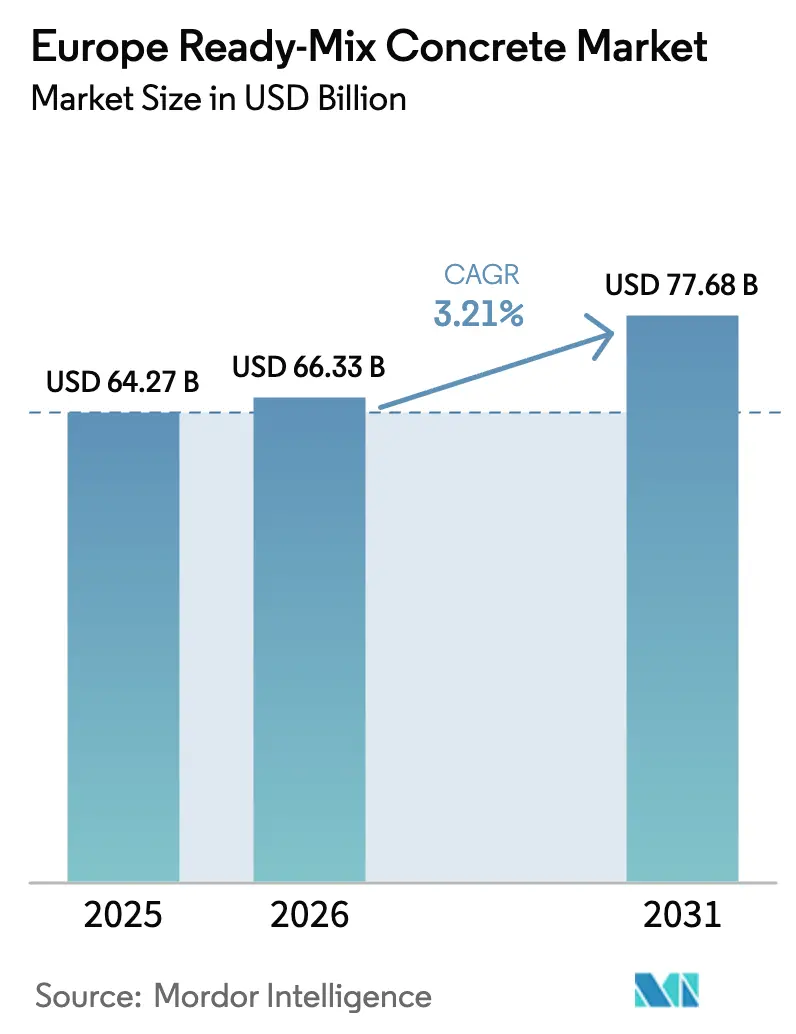

| Base Year Market Size (2025) | USD 64.27 Billion |

| Market Size (2026) | USD 66.33 Billion |

| Market Size (2031) | USD 77.68 Billion |

| Growth Rate (2026 - 2031) | 3.21% CAGR |

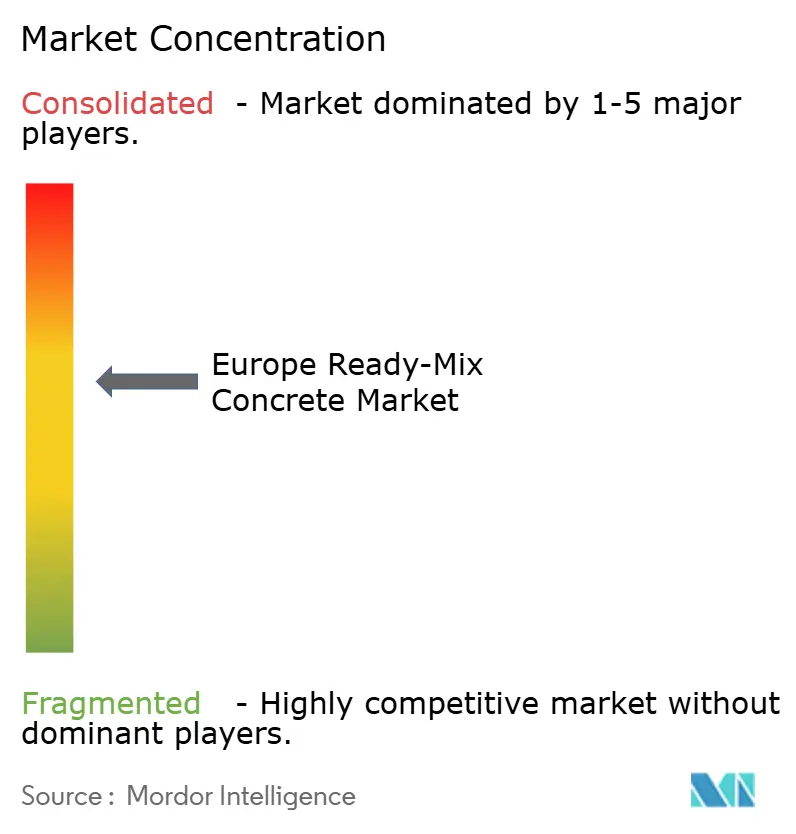

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Ready-Mix Concrete Market Analysis by Mordor Intelligence

The Europe Ready-Mix Concrete Market size is expected to grow from USD 64.27 billion in 2025 to USD 66.33 billion in 2026 and is forecast to reach USD 77.68 billion by 2031 at 3.21% CAGR over 2026-2031. Consistent infrastructure spending, rising sustainability mandates and digitalization of dispatch operations underpin this steady expansion even as financing constraints curb new-build residential activity. Public sector transport programs now provide a floor under demand, limiting the cyclical swings that weighed on the sector between 2020 and 2023. Market leadership is gradually shifting eastward as cohesion-fund inflows accelerate Polish transport projects while Germany pivots from pure volume growth to efficiency-led spending. Competitive intensity is moving away from price toward technology and carbon credentials as EU Emissions Trading System (EU ETS) costs reshape producer economics.

Key Report Takeaways

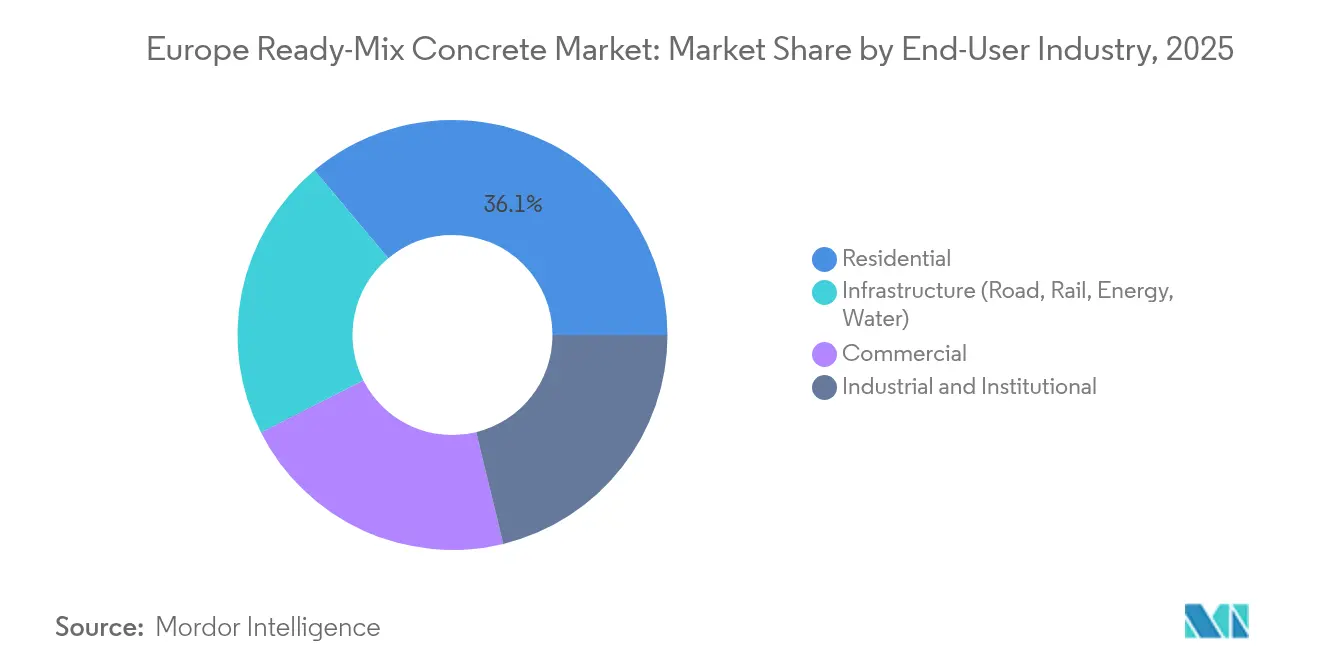

- By end-user industry, the residential segment held 36.10% of the Europe ready-mix concrete market share in 2025, while infrastructure is projected to rise at a 5.65% CAGR through 2031.

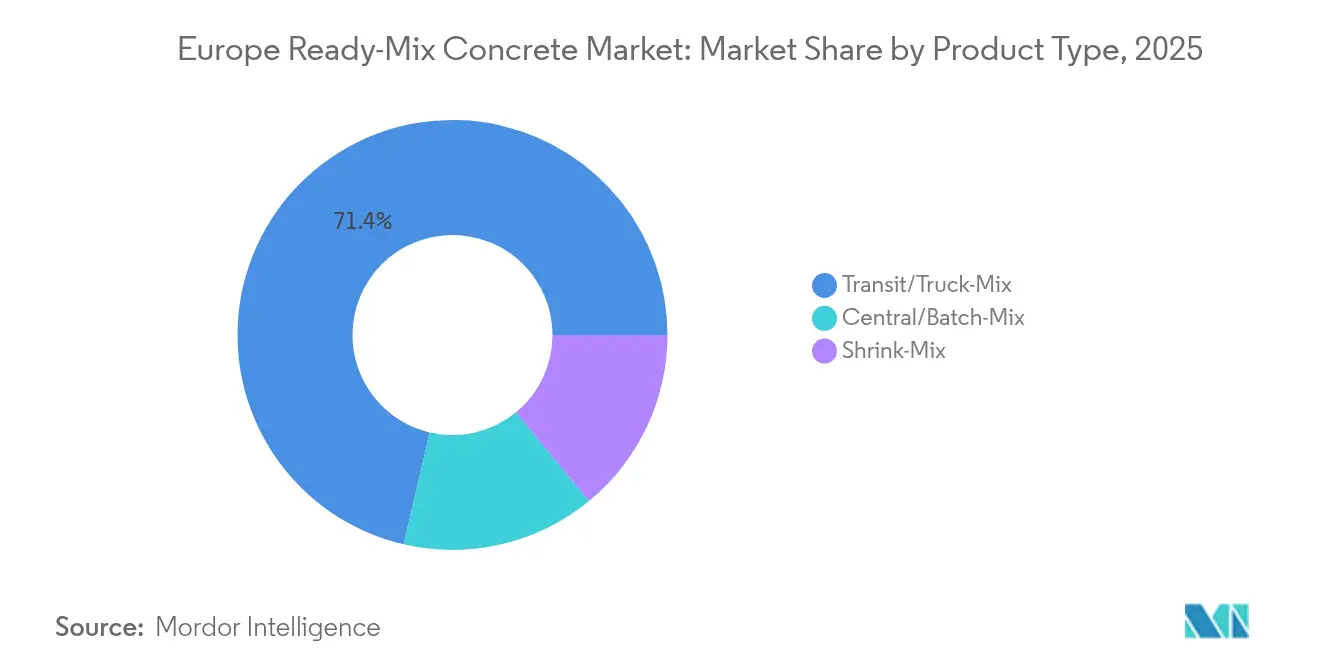

- By product type, transit/truck-mix concrete accounted for 71.35% of the Europe ready-mix concrete market size in 2025 and central/batch-mix is expanding at a 5.14% CAGR to 2031.

- By geography, Germany led with 20.20% revenue share in 2025, whereas Poland records the highest projected CAGR at 5.55% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Ready-Mix Concrete Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing residential and urban-infill demand | +0.80% | Germany, France, Netherlands, Nordic Countries | Medium term (2–4 years) |

| EU Green Deal / TEN-T infrastructure stimulus | +1.20% | Poland, Germany, France, Italy, Spain | Long term (≥4 years) |

| Prefabrication & digital dispatch efficiency | +0.70% | Germany, Netherlands, Nordic Countries | Short term (≤2 years) |

| Decarbonization push for low-carbon mixes | +0.50% | Germany, Netherlands | Long term (≥4 years) |

| Uptake of 3-D concrete printing | +0.10% | Germany, Netherlands, UK | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Demand from Residential and Urban-Infill Construction

Urban densification policies are increasing the concrete intensity per dwelling, even as overall housing starts soften. German building codes that tighten thermal-performance thresholds require thicker, higher-strength walls, increasing ready-mix volumes per unit. The Netherlands’ EUR 35 billion Climate Fund channels grants to convert former industrial zones into mid-rise residential districts, creating repeat business for suppliers that excel at narrow-site logistics[1]Government of the Netherlands, “Climate Policy,” government.nl . In France, renovation approvals now dominate permits, favoring specialized mixes formulated for structural reinforcement and energy upgrades. Nordic municipalities continue to subsidize concrete-frame housing that withstands freeze-thaw cycles. Across these markets, producers that couple technical advisory services with just-in-time delivery gain a competitive edge.

Infrastructure Stimulus via EU Green Deal / TEN-T Corridors

The EU has earmarked EUR 2.8 billion for 94 Trans-European Transport Network (TEN-T) projects in 2024, catalyzing sustained demand for bridge decks, viaducts, and rail sub-bases[2]European Commission, “TEN-T Days 2024,” ec.europa.eu . Poland’s role on the Baltic–Adriatic corridor underpins a 5.63% CAGR, while Germany allocates EUR 38.26 billion to transport in the 2025 federal budget, with EUR 2.5 billion ring-fenced for autobahn bridge rehabilitation. France’s Grand Paris Express and Turin-Lyon links widen the civil-work pipeline through 2026. Italy channels recovery funds toward flood control and seismic retrofit concrete, sustaining order books for specialized suppliers. These multi-year programs buffer the Europe ready-mix concrete market against housing downturns.

Prefabrication and Digital Dispatch Platforms Enhancing Time-Cost Efficiency

Algorithm-driven dispatch software now optimizes fleet routes in real-time, reducing truck waiting by up to 7.6% and cutting idle fuel consumption. German and Dutch plants integrate IoT sensors and edge computing to predict mixer downtime, raising overall equipment effectiveness. Prefabricators require narrow-tolerance mixes delivered in rapid succession, pushing producers toward automated central batching that ensures consistency. Digital twins enable managers to simulate demand spikes and balance plant loads, resulting in higher margins even as input prices fluctuate. Early adopters report payback periods of under 24 months, encouraging broader rollouts across Northern Europe.

Uptake of 3-D Concrete Printing Requiring Specialized Mixes

Large-scale printers for façades, foundations and site furnishings demand pumpable, rapid-setting formulations. Pilot projects in Germany and the Netherlands demonstrate 40% labor savings and material waste reductions, but require suppliers to fine-tune rheology and curing trajectories. Universities and OEMs are collaborating on printable geopolymer blends that cut Portland clinker dependency. While volumes remain small, early movers secure intellectual property and qualification data that create high barriers for later entrants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in cement and energy prices | -0.60% | Germany, Italy, France; Eastern Europe partly insulated | Short term (≤2 years) |

| Shortage of SCMs after coal-plant closures | -0.40% | Germany, UK, Netherlands | Medium term (2–4 years) |

| Stricter EU ETS costs inflating expenses | -0.40% | EU27 markets | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Volatility in Cement and Energy Prices Squeezing Margins

Cement prices climbed in Ireland between 2021 and 2024, mirroring surges across Western Europe as gas markets swung and kiln operators passed on higher energy costs. German contractors report input-cost inflation at 16-month highs in early 2025, prompting tender delays that dampen concrete call-offs. Fuel surcharges only partially offset cost spikes because multi-year supply contracts often cap escalation. Eastern European imports further compress margins in mature markets. Producers respond with dynamic pricing clauses and fleet route optimization to shave diesel use, yet profitability remains sensitive to gas-benchmark volatility until alternative-fuel substitution rises above today’s 53% share.

Shortage of SCMs After Coal-Plant Closures

Coal exits remove fly ash streams that once supplied up to 30% of binder needs. Germany’s rapid phase-out caused local fly-ash availability to slump, forcing ready-mix plants to scramble for imported slag or resort to higher-clinker mixes that raise both cost and CO₂. Alternative SCMs such as calcined clay and recycled fines require new grinding, calcination and quality-control investments. Smaller producers lack capital for such upgrades, risking market share erosion. Harmonized European standards for novel SCMs are progressing, yet certification timelines delay widespread adoption, capping near-term substitution potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-user Industry: Infrastructure Drives Long-Term Growth

Infrastructure applications captured a 5.65% CAGR, well ahead of residential, underpinned by EU recovery funds and climate-resilience mandates. Transport authorities in Germany alone earmarked EUR 166 billion through 2029 for highway bridges and rail upgrades. This pipeline stabilizes ordering cycles, allowing plants to run near rated capacity. The commercial segment remains steady as e-commerce drives warehouse construction, while industrial reshoring fuels demand for concrete flooring. Institutional refurbishments across schools and hospitals pivot on low-carbon specifications that favor suppliers with certified mixes. Overall, infrastructure’s share of the Europe ready-mix concrete market size is set to expand as public budgets prioritize asset resilience over new dwellings.

Infrastructure’s outperformance also elevates specification complexity. Bridge decks require high early strength and chloride resistance; tunnel sections need fiber-reinforced, micro-silica-enhanced mixes. Producers investing in central labs and mobile testing win supply contracts on performance rather than lowest-price bids. Logistics sophistication—night pours, rail-car feeding and on-site silos—becomes critical on mega-projects, giving vertically integrated majors a scale advantage.

By Product Type: Digital Efficiency Reshapes Mix Preferences

Transit/truck-mix concrete still commands 71.35% of the Europe ready-mix concrete market share, sustained by dense batching-plant networks and customer familiarity. However, central/batch-mix systems are registering a 5.14% CAGR as contractors demand tighter quality control and reduced onsite waste. Automated plants equipped with real-time moisture probes and AI dosing algorithms deliver slump variations under ±15 mm, outperforming truck-mounted mixers that adjust manually on route. Shrink-mix serves niche long-haul or architectural projects requiring extended workability.

Digital twins intertwine batching and dispatch, letting managers simulate order books and schedule preventive maintenance. As driver shortages persist, fleet productivity hinges on precise slotting; companies using predictive algorithms cut empty kilometers by 12%, cushioning diesel inflation. The Europe ready-mix concrete market size for central plants is therefore poised to expand, though capital outlays remain a hurdle for smaller independents.

Geography Analysis

Germany retains a 20.20% share of the Europe ready-mix concrete market, anchored by EUR 11.71 billion annual allocations from the Infrastructure and Climate Neutrality fund. Near-term headwinds stem from permitting delays and tighter residential credit, but bridge rehabilitation and rail electrification ensure baseline demand. Advanced digital adoption—GPS-tagged mixers, e-ticketing, and EPD-linked invoicing—further entrenches incumbents.

Poland is the fastest-growing geography at a 5.55% CAGR, propelled by cohesion-fund-backed highway, port, and rail builds. Project clustering around the Baltic–Adriatic corridor lets producers run high-throughput central plants with minimal haul distances, boosting margins despite lower average selling prices. Domestic groups collaborate with multinationals to upskill workforces and embed low-carbon mix design, fortifying supply security.

France balances weak housing starts with robust civil-work packages. The Grand Paris Express, Lyon–Turin link and renovation grants channel consistent orders through 2026. Tight labor markets encourage prefabrication, raising demand for factory-consistent mixes. Italy leverages NRRP grants to retrofit flood defenses and seismic-proof buildings, opening niches for sulfate-resistant and fiber-reinforced formulations.

The United Kingdom, Netherlands, Belgium and Nordic countries jointly contribute significant tonnes by focusing on climate-resilient infrastructure—offshore wind foundations, flood barriers, Arctic-grade housing and logistics hubs. The Netherlands’ 2030 Climate Fund earmarks concrete-intensive projects in Amsterdam’s harbor and Rotterdam’s wind-port upgrades. Belgium’s Oosterweel Link demands high-flow, low-shrink mixes for tunnel sections under Antwerp’s river estuary. Nordic governments’ procurement rules already cap embodied carbon per cubic meter, accelerating adoption of SCM-rich blends.

Competitive Landscape

The Europe ready-mix concrete market is moderately fragmented. Heidelberg Materials, CRH, and Holcim operate vertically integrated cement, aggregate, and concrete assets, leveraging 1,270-plus ready-mix sites worldwide and capturing scale synergies. These majors emphasize sustainability differentiation—ECOPact, ECOPlanet, Vertua—rather than price, because EU ETS exposure and SCM scarcity squeeze traditional cost levers.

Strategic M&A remains active. CRH’s USD 2.1 billion purchase of Eco Material in 2025 enhances access to reclaimed fly-ash streams and geopolymer know-how. Buzzi Unicem trimmed Italian capacity by divesting the Fanna plant to Alpacem Italia, freeing capital for carbon-capture retrofits. Cemex installs photovoltaics at Berlin batching sites to hedge electricity costs and power an emerging electric mixer fleet.

Digital ecosystems are a competitive frontier. Start-ups offering cloud dispatch integrate with ERP and telematics, enabling real-time KPI dashboards. Majors co-develop platforms to retain data ownership and lock in customers via application-programming-interface (API) bundles. Suppliers strong in performance concretes—high-alumina, 3-D printable, carbon-mineralized—win specification-heavy tenders. Meanwhile, smaller independents rely on local relationships and niche service, but face capital hurdles in meeting looming EN-15804+A2 EPD mandates.

Europe Ready-Mix Concrete Industry Leaders

Buzzi Unicem SpA

CEMEX S.A.B. de C.V.

CRH

HeidelbergCement

HOLCIM

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Cemex is expanding its photovoltaic farms in Central Europe to reduce reliance on traditional energy sources and achieve long-term energy cost savings. This initiative aligns with environmental standards. In Berlin, Germany, Cemex announced to add a 30 kWp solar installation at a Ready-Mix Plant to power the batching plant and its electric mixer fleet.

- September 2025: CRH announced that it has acquired Eco Material Technologies for a sum of USD 2.1 billion. This acquisition not only bolsters CRH's portfolio in sustainable building materials but also enhances its ready-mix concrete capacity in Europe, leveraging Eco Material's eco-centric offerings and advanced technologies.

Europe Ready-Mix Concrete Market Report Scope

Ready-mix concrete (RMC) is concrete that is delivered to the job site to be used directly after being batched at a central plant. RMC finds its applications in foundations, walls, floors and bases, driveways, and other constructional activities owing to its excellent properties. The European ready-mix concrete market is segmented by end-user industry and geography. By end-user industry, the market is segmented into residential, commercial, industrial/institutional, and infrastructure. By geography, the market is segmented into Germany, United Kingdom, Italy, France, and Rest of Europe. The report covers the market sizes and forecasts for four countries across the region. For each segment, market sizing and forecasts have been provided on the basis of value (USD billion).

By End-user Industry

| Residential |

| Commercial |

| Industrial and Institutional |

| Infrastructure (Road, Rail, Energy, Water) |

By Product Type

| Transit/Truck-Mix |

| Central/Batch-Mix |

| Shrink-Mix |

By Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Poland |

| Netherlands |

| Belgium |

| Nordic Countries |

| Rest of Europe |

| By End-user Industry | Residential |

| Commercial | |

| Industrial and Institutional | |

| Infrastructure (Road, Rail, Energy, Water) | |

| By Product Type | Transit/Truck-Mix |

| Central/Batch-Mix | |

| Shrink-Mix | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Poland | |

| Netherlands | |

| Belgium | |

| Nordic Countries | |

| Rest of Europe |

Key Questions Answered in the Report

What is the 2026 value of the Europe ready-mix concrete market?

The market is valued at USD 66.33 billion in 2026.

How fast is the sector expected to grow through 2031?

It is projected to expand at a 3.21% CAGR, reaching USD 77.68 billion by 2031.

Which country is the fastest-growing market in the region?

Poland leads with a projected 5.55% CAGR through 2031, driven by EU-funded infrastructure.

Why are low-carbon mixes gaining traction?

Rising EU ETS costs and public procurement rules that favor products with lower embodied CO₂ are accelerating adoption.

Which product type is gaining share over transit-mix concrete?

Central/batch-mix systems are growing at 5.14% CAGR because centralized batching improves quality control and reduces waste.

How are producers dealing with cement-price volatility?

Many adopt dynamic pricing clauses, invest in alternative-fuel kilns and deploy digital dispatch tools to cut operating costs.

Page last updated on: