Decorative Concrete Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

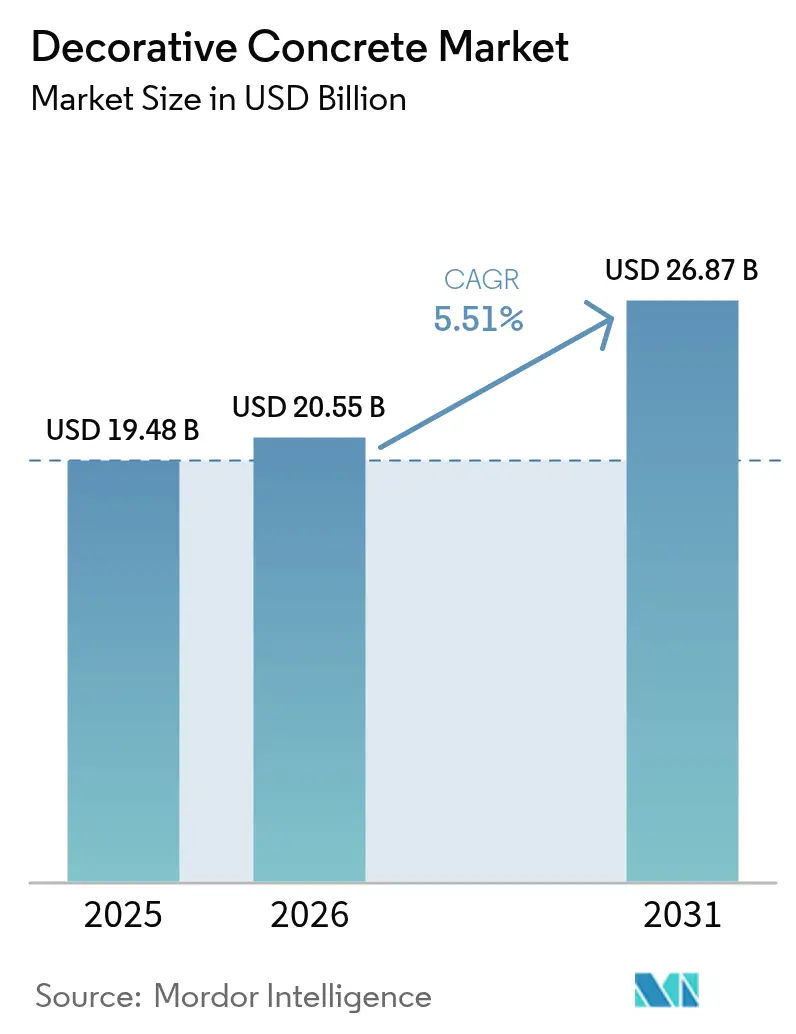

| Market Size (2026) | USD 20.55 Billion |

| Market Size (2031) | USD 26.87 Billion |

| Growth Rate (2026 - 2031) | 5.51% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Decorative Concrete Market Analysis by Mordor Intelligence

The Decorative Concrete market size is expected to grow from USD 19.48 billion in 2025 to USD 20.55 billion in 2026 and is forecast to reach USD 26.87 billion by 2031 at 5.51% CAGR over 2026-2031. This sustained expansion reflects a decisive shift in global construction priorities toward materials that marry long-term durability with design versatility, especially as residential remodeling budgets remain elevated and commercial facilities continue to modernize. Heightened post-pandemic home-improvement outlays, an aging housing stock with a median age of 41 years, and growing preference for low-maintenance surfaces are reinforcing demand. In parallel, commercial refurbishments are adopting polished and stamped concrete to meet foot-traffic durability targets, while net-zero building mandates push producers toward bio-based admixtures and low-VOC mixes. Tariffs on imported cement, coupled with volatile pigment supply, amplify cost pressures but also open opportunities for vertically integrated suppliers and innovators in carbon-reduced formulations.

Key Report Takeaways

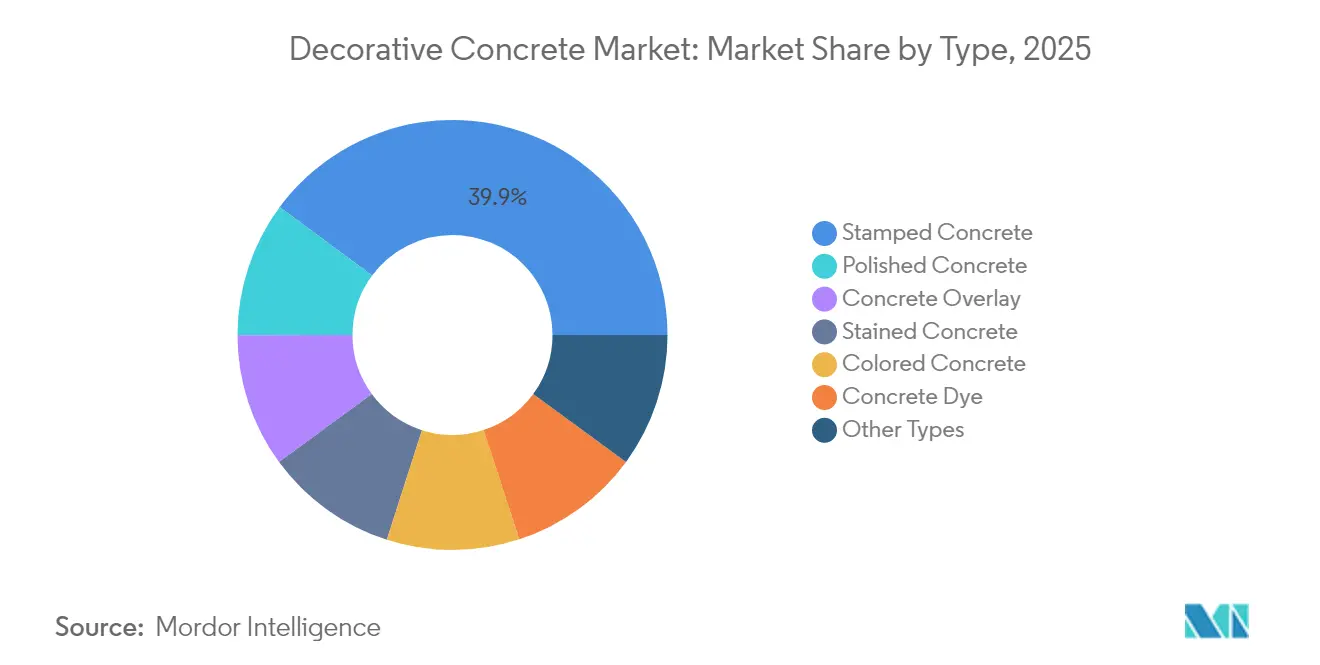

- By product type, stamped concrete led with 39.86% of decorative concrete market share in 2025; polished concrete is projected to expand at a 6.12% CAGR through 2031.

- By application, floor installations accounted for 54.72% of the decorative concrete market size in 2025 and are advancing at a 5.95% CAGR through 2031.

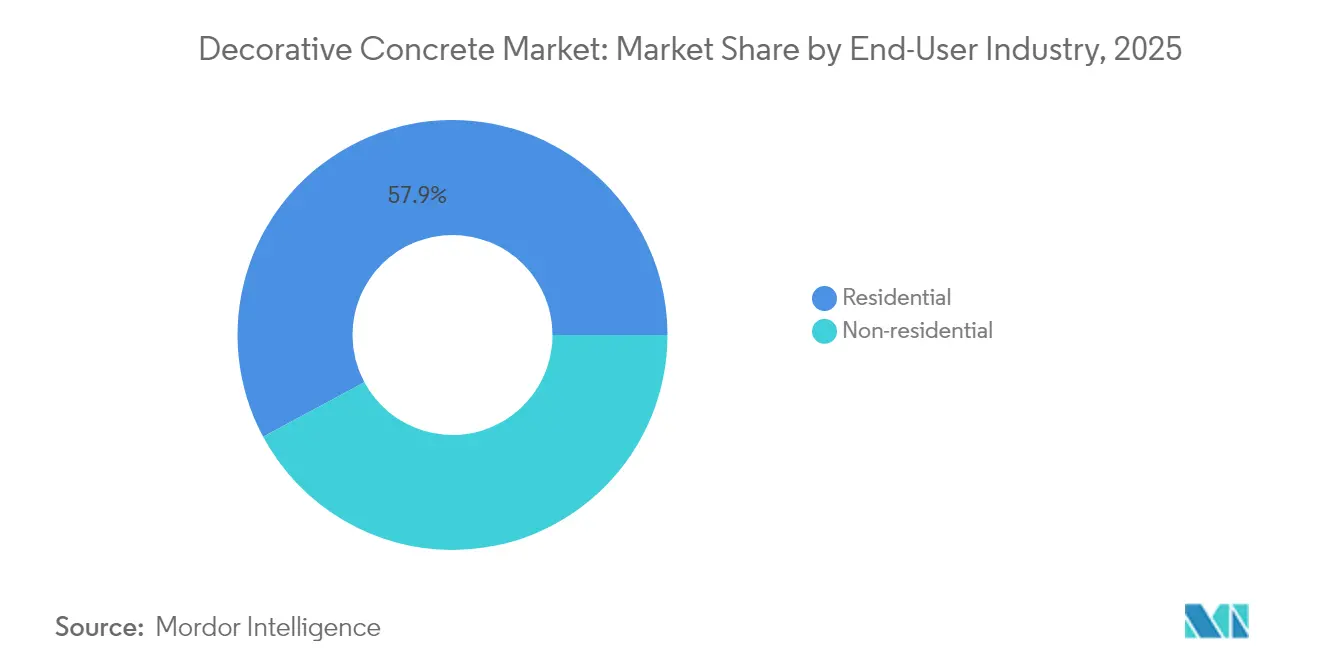

- By end-user industry, residential construction held 57.85% of 2025 revenue, while the non-residential segment records the highest projected CAGR at 6.17% to 2031.

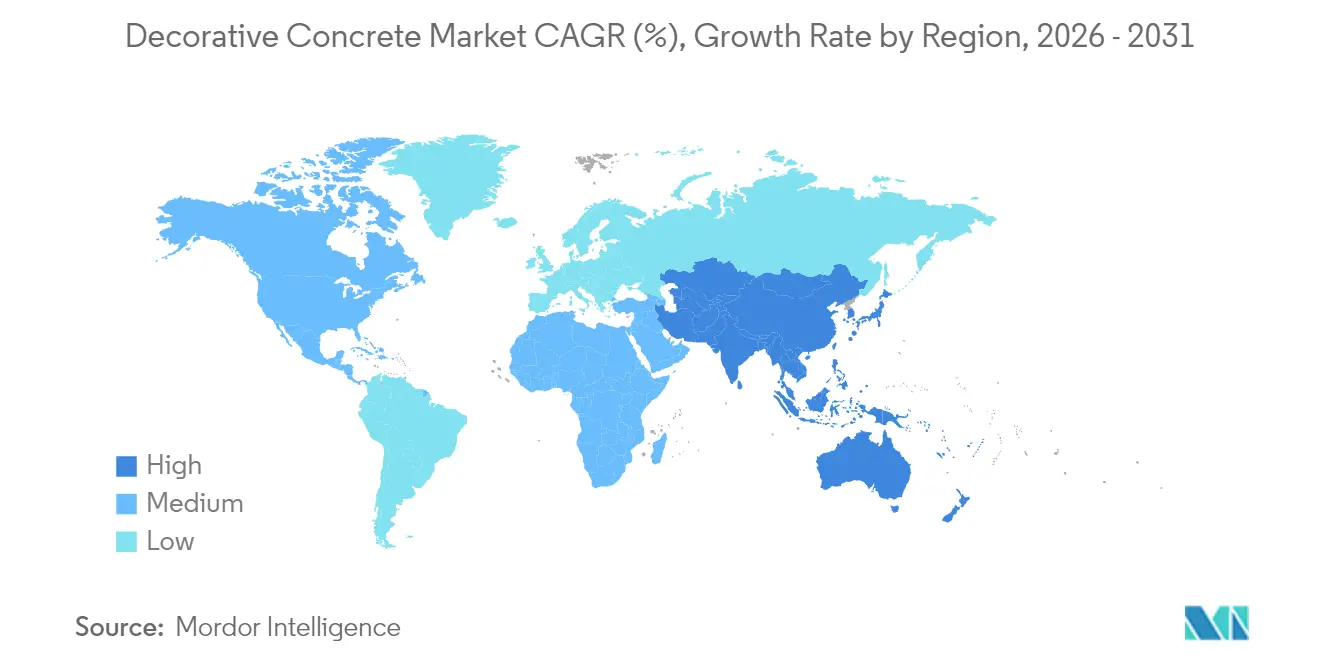

- By geography, Asia-Pacific commanded 37.60% revenue in 2025 and maintains the fastest pace with a 6.44% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Decorative Concrete Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising residential remodeling and refurbishment spend post-pandemic | +1.2% | North America & Europe, spill-over to APAC | Medium term (2-4 years) |

| Preference for stamped concrete in new-build outdoor living spaces | +0.9% | Global, with early gains in North America, Europe, APAC | Long term (≥ 4 years) |

| Net-zero and green-building certification pushing colored/low-VOC mixes | +0.8% | Europe & North America core, expanding to APAC | Long term (≥ 4 years) |

| Growth of decorative concrete overlays in fast-track renovation projects | +0.7% | Global, particularly North America residential | Short term (≤ 2 years) |

| Adoption of bio-based admixtures to cut embodied-carbon footprint | +0.6% | Europe regulatory-driven, North America voluntary adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Residential Remodeling and Refurbishment Spend Post-Pandemic

Elevated remodeling budgets have shifted toward fewer but higher-value projects, strengthening demand for surface upgrades that combine aesthetics with long service life. Average homeowner spend increased 12% in 2023 despite a brief dip in overall project volume, signaling a willingness to pay for premium finishes that raise property value and support aging-in-place needs. Decorative concrete aligns well because its 20–30-year life span outperforms many alternative pavements, limiting future repair cycles. An aging housing stock motivates extensive outdoor and basement renovations where stamped slabs and polished floors deliver quick visual impact. Mortgage rates trending toward 5.5% by mid-2025 should further unlock renovation funding, amplifying demand throughout the forecast window.

Preference for Stamped Concrete in New-Build Outdoor Living Spaces

Advances in stamping mats and integral coloring have dispelled dated perceptions of stamped surfaces and now enable convincingly natural textures that last beyond two decades when properly sealed. Unit installation costs retain a favorable spread versus quarried stone, enabling contractors to target broader demographic segments. Cool-tone pigments and geometric templates resonate with modern landscaping trends while permeable variants address storm-water mandates in dense urban projects. Integrated LED channels and metallic highlights differentiate premium installations, particularly around pool decks where cooler surface temperatures and slip resistance improve safety.

Net-Zero and Green-Building Certification Pushing Colored/Low-VOC Mixes

Europe’s Energy Performance of Buildings Directive mandates on-site zero emissions in new dwellings from 2030, spurring uptake of cement-replacement admixtures and low-VOC sealers that can secure LEED, BREEAM, or DGNB credits. The Ecodesign for Sustainable Products Regulation obliges product-specific carbon disclosure, rewarding suppliers with transparent digital passports. Admixtures such as bio-based binders or slag blends lower embodied carbon without compromising compressive strength, meeting EU Taxonomy thresholds that now demand 70% waste recovery on large projects. U.S. green-building assessments echo this trajectory, placing colored but VOC-compliant mixes in competitive specification shortlists[1]Passive House Plus Team, “EPBD Revision Sets 2030 Zero-Emission Target,” passivehouseplus.ie.

Growth of Decorative Concrete Overlays in Fast-Track Renovation Projects

Overlay systems have grown popular because they can transform worn substrates with minimal demolition. Polymer-modified micro-toppings achieve strong adhesion, while spray-down and trowel-down variants install in days, making them ideal where business operations cannot pause for full slab replacement. Although unit pricing is higher than basic resurfacing, the reduced downtime offsets upfront cost in restaurants, retail, and institutional settings. Multi-layer stenciling and acid-free staining broaden design options without extending curing schedules, sustaining momentum for overlays in both residential patios and commercial lobbies.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of specialty pigments, molds and sealers | -0.8% | Global, particularly emerging markets | Short term (≤ 2 years) |

| Volatility in cement and pigment supply chains inflating prices | -1.1% | Global, acute in North America due to tariffs | Short term (≤ 2 years) |

| Shortage of certified decorative concrete installers | -0.7% | North America & Europe, emerging in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Specialty Pigments, Molds and Sealers

Decorative concrete commands USD 200–300 per cubic yard against USD 100–150 for standard mixes, a gap driven by expensive iron-oxide pigments, silicone molds, and multi-layer sealing systems. Contractors pass these costs to homeowners and small developers, curbing uptake in price-sensitive regions. Labor premiums also arise because stamped or polished finishes require slower placement rates and specialized finishing skills. Smaller contractors hesitate to purchase proprietary stamp libraries or diamond-polishing equipment, limiting service availability in secondary cities and slowing rural penetration[2]Evenson Concrete Systems, “2025 Price Guide for Decorative Finishes,” evensonconcretesystems.com.

Volatility in Cement and Pigment Supply Chains Inflating Prices

The 25% tariff imposed in February 2025 on cement imports from Canada and Mexico tightened North American supply, lifting delivered prices and compressing ready-mix margins. Simultaneous steel import levies elevate rebar and formwork costs, compounding total project budgets. Larger vertically integrated producers have absorbed part of the increase by reallocating clinker between regions, but smaller plants face spot-market volatility that translates into quotation surcharges. Pigment supply is equally exposed to freight disruptions and energy-price swings, prompting architects to specify color ranges with contingency allowances.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Stamped Concrete Dominance Drives Innovation

Stamped concrete retained a 39.86% decorative concrete market share in 2025, underpinned by its adaptability across driveways, patios, and commercial plazas. Enhanced tool libraries offer slate, timber, and even integrated logo impressions, enabling contractors to court hospitality and branded retail chains. Polished concrete, while holding a smaller base, is forecast to grow at a 6.12% CAGR to 2031 as facility managers appreciate seamless floors that resist forklift abrasion and ease cleaning protocols. Decorative concrete market size benefits from overlays that extend surface life without structural demolition, and from emerging self-healing capsules that release lime to seal microcracks and prolong service intervals. Overall, diversified type options help suppliers meet both budget and performance briefs, reinforcing the decorative concrete market’s resilience.

Continued R&D targets color-fast dyes and rapid-cure sealers that shorten turnover cycles. Colored mixes leverage finer pigment dispersions to avoid streaking, whereas translucent dye systems permit artistic gradients favored in boutique venues. Fiber-reinforced designs alleviate shrinkage cracking, while UV-resistant topcoats guard against fade in open-air entertainment spaces. Collectively, these advances widen use cases and deepen penetration into high-visibility architectural elements, bolstering long-term decorative concrete market growth.

By Application: Floor Applications Drive Revenue Growth in 2024

Floors accounted for 54.72% of revenue in 2025 and carry the highest growth rate at 5.95% CAGR, cementing their status as the largest and fastest-advancing category. Developers of distribution centres, schools, and airports gravitate toward polished finishes that tolerate constant foot and trolley traffic while cutting life-cycle maintenance spend. The decorative concrete market size for floors is widening as matte sealers satisfy gloss reduction requirements in healthcare settings that struggle with overhead glare.

Pool decks, patios, and driveways follow closely, benefitting from heat-reflective options that reduce surface temperatures up to 7 °C compared with conventional grey slabs. LED-ready joint configurations unlock lighting design freedom for premium residential backyards, while slip-resistant micro-textures meet evolving building-code thresholds. Wall and vertical-cast elements remain niche but are gaining traction in feature façades where integral coloring and sand-blasted reveals offer visual focal points with minimal upkeep.

By End-User Industry: Residential Construction Drives Decorative Concrete Demand in 2024

Residential construction generated 57.85% of 2025 demand thanks to homeowners’ desire for curb-appeal upgrades and aging-in-place investments that favor low-maintenance surfaces. Decorative concrete market share within single-family renovations continues to climb as homeowners replace wooden decks prone to rot with stamped slabs that require only periodic resealing. Detached garage conversions and basement waterproofing projects further expand residential scope by integrating polished or stained finishes that tolerate moisture.

The commercial segment is projected to outpace residential at a 6.17% CAGR through 2031 as office retrofits, logistics hubs, and hospitality refurbishments specify polished or epoxy-guarded decorative floors that support heavy loads and scrubbing machines. Federal infrastructure stimulus funnels capital into civic plazas, transit stations, and school expansions, each representing substantial square footage. Green-leasing models are also nudging landlords to favor durable, low-VOC surfaces that ease compliance reporting and attract ESG-aligned tenants, accelerating commercial uptake of decorative concrete.

Geography Analysis

Asia-Pacific held 37.60% of 2025 revenue and posts a leading 6.44% CAGR to 2031, reinforcing its dual role as market leader and primary growth driver. China alone consumed 6.6 gigatons of cement between 2011–2013, dwarfing 20th-century U.S. usage, and still accounts for more than half of global output. Massive housing-relocation schemes and megaprojects such as Indonesia’s USD 5 billion industrial park underscore structural demand, while permeable decorative slabs respond to stringent storm-water ordinances in rapidly urbanizing cities. Local producers are scaling low-clinker binders to align with national decarbonization pledges, broadening the product mix and tempering import dependence.

North America faces pronounced cost volatility after 2025 import tariffs but retains growth potential supported by mortgage-rate easing and continued public-sector outlays. An aging housing stock boosts residential resurfacing, while the Bipartisan Infrastructure Law extends opportunities in public plazas and transit hubs. Supply-chain headwinds encourage integrated suppliers to expand captive quarry and terminal capacity, securing raw materials and stabilizing decorative concrete market pricing.

Europe’s stringent carbon directives recalibrate specifications toward low-embodied materials, catalyzing uptake of bio-based admixtures and recycled aggregates. Producers investing in waste-heat recovery kilns and bio-char co-firing earn procurement preference under EU Taxonomy rules, reinforcing regional competitive advantages. Meanwhile, Middle East, Africa, and South America register steady gains anchored by urban population growth, though currency volatility and limited installer capacity temper immediate upside potential. Across all regions the decorative concrete market demonstrates capacity to align with local policy imperatives and construction-sector cycles, sustaining a broad demand base.

Competitive Landscape

The decorative concrete market remains fragmented, with innovation, vertical integration, and sustainability credentials acting as the main competitive levers. Sika’s 2023 acquisition of MBCC Group broadened its admixture portfolio and is projected to yield CHF 180–200 million in annual synergies by 2026, illustrating how consolidation strengthens R&D scale and raw-material bargaining power. Holcim US added quarries in the Mid-Atlantic to secure aggregate supply, buffering against haulage cost spikes and ensuring feedstock for its ready-mix operations. CEMEX, leveraging Microsoft Azure OpenAI, launched an AI-enabled sales assistant to shorten quotation cycles and upscale cross-selling of decorative solutions, reflecting the sector’s digitalization trend.

Sustainability-focused chemistry provides another differentiation path. BASF’s MasterFiber synthetic-fiber line reduces steel-mesh usage and speeds placement, particularly attractive for fast-track warehouse slabs. PPG Industries reported USD 18.2 billion in 2023 net sales, underscoring the scale at which coatings firms are aligning colorant systems and low-VOC sealers with decorative concrete installers. Smaller disruptors pursue carbon-negative admixtures such as Solid Carbon’s BioLock, appealing to projects seeking to outperform carbon baselines. Across the board, firms that can cushion tariff-driven cost swings and offer verifiable carbon-footprint reductions are best placed to capture incremental decorative concrete market share.

Decorative Concrete Industry Leaders

Sika AG

RPM International Inc.

BASF

CEMEX S.A.B. de C.V.

Heidelberg Materials

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Sherwin-Williams High Performance Flooring has been awarded the esteemed 2025 Concrete Contractor Top Products Award for its innovative Accelera One. This advanced product, a clear urethane grout and topcoat, establishes new standards in decorative concrete flooring technology.

- May 2023: Following the receipt of all necessary regulatory approvals, Sika has successfully completed the acquisition of MBCC Group. This acquisition significantly enhances Sika's global presence, strengthens its portfolio of products and services, including decorative concrete.

Global Decorative Concrete Market Report Scope

The decorative concrete market report includes:

| Stamped Concrete |

| Polished Concrete |

| Concrete Overlay |

| Stained Concrete |

| Colored Concrete |

| Concrete Dye |

| Other Types |

| Footpath and Driveway |

| Patio |

| Pool Deck |

| Floor |

| Wall |

| Other Applications |

| Residential |

| Non-residential |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Stamped Concrete | |

| Polished Concrete | ||

| Concrete Overlay | ||

| Stained Concrete | ||

| Colored Concrete | ||

| Concrete Dye | ||

| Other Types | ||

| By Application | Footpath and Driveway | |

| Patio | ||

| Pool Deck | ||

| Floor | ||

| Wall | ||

| Other Applications | ||

| By End-user Industry | Residential | |

| Non-residential | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Decorative Concrete Market size?

The market is valued at USD 20.55 billion in 2026 and is projected to reach USD 26.87 billion by 2031.

Which product type leads the decorative concrete market?

Stamped concrete holds the top position with 39.86% of 2025 revenue.

Which application segment is growing fastest?

Floor installations post the strongest outlook, advancing at a 5.95% CAGR through 2031.

Why is Asia-Pacific so influential in this industry?

Asia-Pacific commands 37.60% of revenue and enjoys the highest regional CAGR at 6.44% thanks to large-scale infrastructure development, particularly in China and Southeast Asia.

Page last updated on: