Market Overview

| Study Period | 2021 - 2031 |

|---|---|

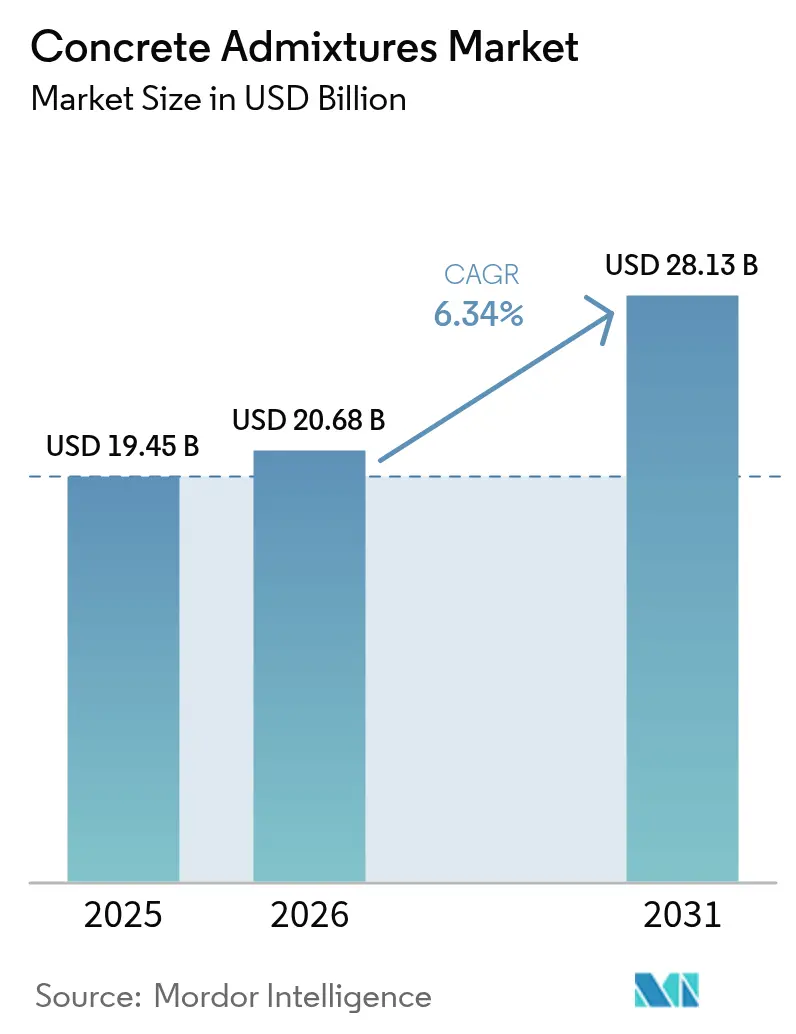

| Market Size (2026) | USD 20.68 Billion |

| Market Size (2031) | USD 28.13 Billion |

| Growth Rate (2026 - 2031) | 6.34% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Concrete Admixtures Market Analysis by Mordor Intelligence

The Concrete Admixtures Market size is expected to grow from USD 19.45 billion in 2025 to USD 20.68 billion in 2026 and is forecast to reach USD 28.13 billion by 2031 at 6.34% CAGR over 2026-2031. Demand is moving toward performance-engineered mixes that accelerate setting, limit embodied carbon, and cut on-site labor. Infrastructure investment programs in the United States, India, and China are tying funding to lower water-cement ratios, which directly lifts superplasticizer consumption. Extreme-temperature pours in the Middle-East and Southeast Asia are sustaining growth in retarder and shrinkage-reducing chemistries. Meanwhile, AI-guided batching platforms are spreading from North America and Europe to large Asian ready-mix fleets, trimming waste and improving compliance documentation. Petrochemical feedstock volatility and tightening formaldehyde rules continue to squeeze legacy naphthalene and melamine products, pushing producers toward bio-based lignin alternatives.

Key Report Takeaways

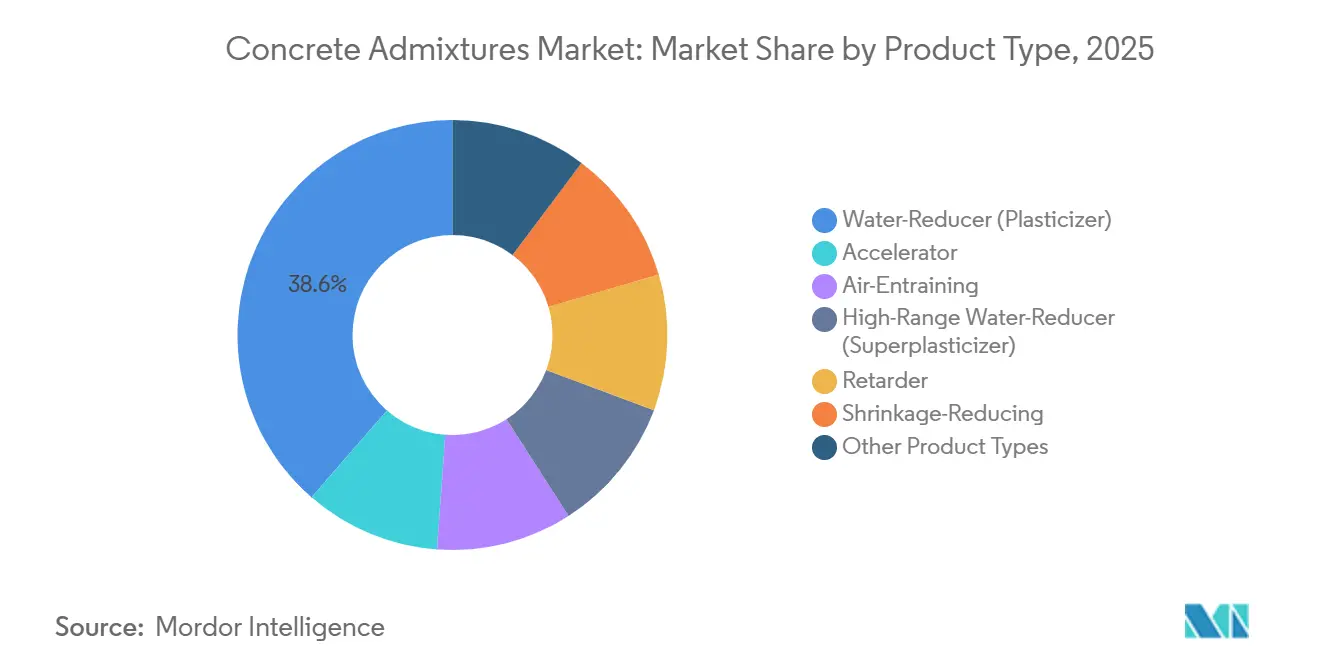

- By product type, water-reducer (plasticizer) held 38.61% of concrete admixtures market share in 2025, while high-range water-reducer (superplasticizer) is advancing at a 6.99% CAGR through 2031.

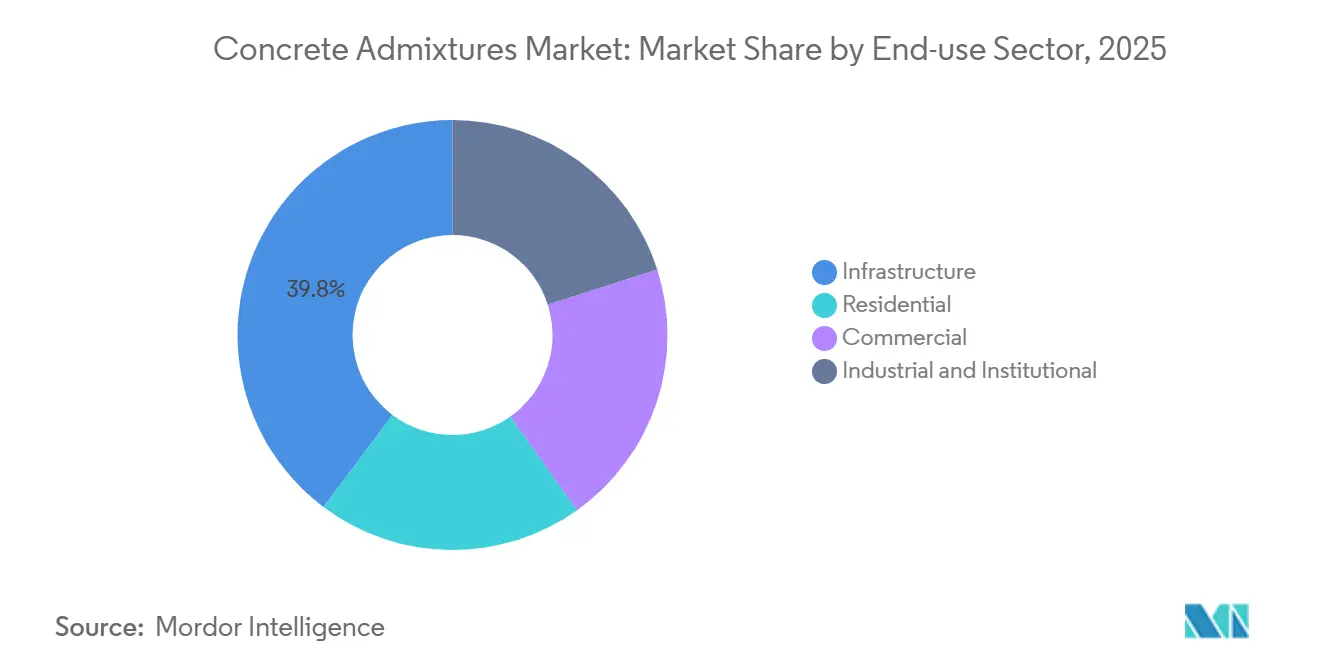

- By end-use sector, infrastructure led with 39.77% of concrete admixtures market share in 2025; residential is forecast to grow at a 6.81% CAGR through 2031.

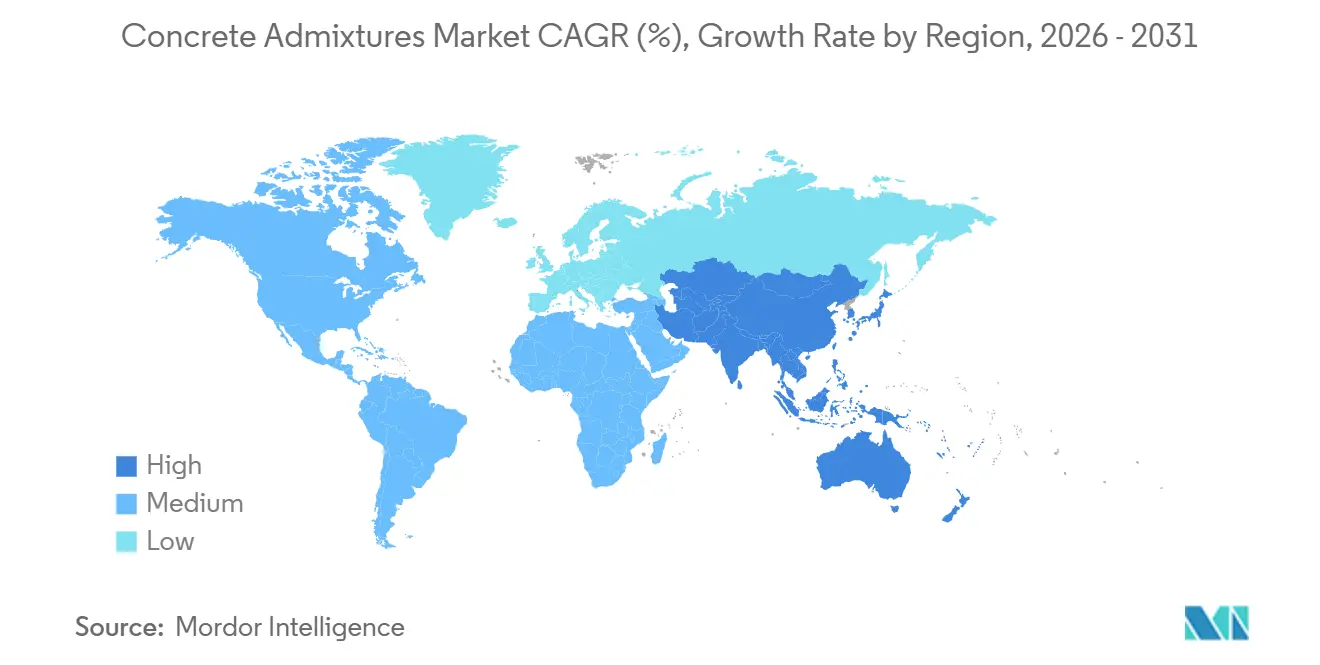

- By geography, Asia-Pacific accounted for 31.59% of concrete admixtures market size in 2025 and is expanding at a 6.81% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Concrete Admixtures Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption of UHPC and SCC Concrete | +1.2% | Global, with concentration in Asia-Pacific and North America | Medium term (2–4 years) |

| Stricter Global Water-Reduction and CO₂ Rules | +1.5% | Global, led by EU, California, China | Long term (≥ 4 years) |

| Government Green-Stimulus for Low-Carbon Construction | +1.1% | North America, Europe, China, India | Medium term (2–4 years) |

| AI-Guided Dosage Optimisation and Digital Twin Batching | +0.8% | North America, Europe, early adoption in China | Short term (≤ 2 years) |

| Bio-Based Lignin/Agri-Waste Superplasticizers | +0.6% | Europe, North America, pilot projects in India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of UHPC and SCC Concrete

Ultra-high-performance concrete (UHPC) and self-compacting concrete (SCC) call for superplasticizer doses two to three times higher than conventional mixes, lifting admixture intensity per cubic meter. UHPC’s 150 MPa-plus compressive strength allows thinner bridge decks and core walls, lowering steel reinforcement and embodied carbon. National bridge codes in Japan and coastal states in the United States now specify UHPC for durability under salt-spray and seismic loading. SCC, which flows without vibration, is shortening prefabrication cycles at modular plants and lowering labor risk on high-rise sites. Momentum is strongest in China, South Korea, and the United States, where labor shortages and tight project timelines reward faster cures and precise rheology control.

Stricter Global Water-Reduction and CO₂ Rules

Updated regulations cap embodied CO₂ and mandate Environmental Product Declarations. The EU’s Construction Products Regulation effective 2025 limits public-works concrete to 310 kg CO₂ e/m³, effectively requiring high-range water reducers to enable 30–40% cement substitution. California’s expanded Buy Clean Act penalizes water-cement ratios above 0.42, and Guangdong’s rebate scheme rewards certified low-carbon admixtures. These rules are phasing out naphthalene plasticizers and boosting demand for polycarboxylate-ether (PCE) and lignin-based products that deliver low-slump retention with negligible formaldehyde.

Government Green-Stimulus for Low-Carbon Construction

Infrastructure stimulus bills now bundle carbon incentives. The U.S. Infrastructure Investment and Jobs Act offers 10% bonus payments for projects cutting embodied carbon 20% below 2020 baseline[1]U.S. Department of Transportation, “Infrastructure Investment and Jobs Act Guidance,” transportation.gov . Germany’s KfW green-building loans shave 50 basis points off interest for concrete below 280 kg CO₂ e/m³. India’s housing ministry ties subsidy eligibility to mixes with water-cement ratios ≤ 0.45, directly driving nationwide plasticizer uptake. Suppliers that can certify low-carbon performance win preferred-bidder status and long-term supply contracts.

AI-Guided Dosage Optimization and Digital Twin Batching

Machine-learning platforms now adjust admixture dosing in real time based on temperature, humidity, and aggregate moisture. Early adopters in Europe and North America cut superplasticizer overdosing by 18% in 2025 and trimmed rejected batches below 1%. Digital twins generate auto-populated Environmental Product Declarations, speeding compliance paperwork. Capital costs remain USD 200,000–500,000 per plant, limiting penetration among small ready-mix operators in emerging markets, but national firms across China and Mexico have launched rollouts tied to performance-based procurement mandates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Petro-Chemical Feedstock Prices | -0.9% | Global, acute in regions dependent on naphthalene and formaldehyde imports | Short term (≤ 2 years) |

| Low-Cost Conventional Concrete and Fly-Ash Blends | -0.7% | Asia-Pacific, Latin America, Sub-Saharan Africa | Medium term (2–4 years) |

| Formaldehyde and VOC-Compliance Risks | -0.5% | North America (California), EU, South Korea | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Volatile Petro-Chemical Feedstock Prices

Naphthalene and formaldehyde spot prices swung more than 35% in 2024–2025 amid refinery outages and gas disruptions, squeezing gross margins at admixture producers without long-term supply contracts. One global player cited a 2.1-percentage-point margin hit in 2025 and accelerated pivot to lignin-based chemistries. Smaller firms lacking hedging scale saw margin erosion exceeding 4 percentage points, prompting exits from commodity plasticizers and a wave of consolidation deals in Europe.

Formaldehyde and VOC-Compliance Risks

California, the EU, and South Korea have set new formaldehyde and VOC thresholds that legacy melamine and naphthalene products cannot meet without expensive vapor-recovery upgrades. California's Air Resources Board lowered the formaldehyde emission threshold for construction chemicals to 9 parts per billion in 2024, effectively banning traditional melamine-formaldehyde superplasticizers unless manufacturers install vapor-recovery systems costing USD 1–3 million per plant[2]California Air Resources Board, “Formaldehyde Emission Limits for Building Products,” arb.ca.gov . Producers already invested in PCE lines are capturing churn-driven share, but laggards risk write-downs as non-compliant inventories become unsalable in regulated regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Superplasticizers Outpace Legacy Chemistries

High-range water reducers are growing at a 6.99% CAGR through 2031, the fastest among all product classes, reflecting demand for concrete mixes above 60 MPa compressive strength and slump flows over 600 mm. Water-Reducer (Plasticizer) retained 38.61% of Concrete Admixtures market share in 2025 thanks to their low unit cost in residential pours, yet the share is slipping as PCE superplasticizers gain regulatory favor.

Accelerators, particularly chloride-free blends, are rising in cold-climate bridge decks and data-center slabs where rapid strength gain shortens construction schedules. Air-entraining admixtures hold steady in freeze-thaw regions, while retarders enjoy renewed traction in Gulf Coast and Southeast Asian projects battling 35 °C heat. Shrinkage-reducing admixtures remain niche but deliver gross margins, supporting specialized suppliers that focus on tunnel linings and large-format industrial floors. Other product types are serving marine docks, desalination plants, and architectural facades.

By End-use Sector: Residential Gains on Urbanization

Infrastructure dominated with 39.77% of Concrete Admixtures market share in 2025, fueled by bridge rehabilitation, highway extensions, and metro lines that specify high-durability mixes. Yet Residential is the fastest-growing segment, advancing at a 6.81% CAGR through 2031 as Asia-Pacific cities absorb 60 million new urban residents each year. Government housing schemes in India and green-retrofit subsidies in Europe bake low water-cement ratios into tender documents, lifting plasticizer penetration.

Commercial building demand centers on Tier-2 Chinese cities and U.S. Sun Belt states where office vacancies are tightening. Industrial projects, notably data centers and e-commerce warehouses, require floor slabs with strict shrinkage tolerances, spurring uptake of shrinkage-reducing admixtures. The industrial demand is sustained by logistics and semiconductor fab construction. Institutional projects—hospitals and universities—contribute steady demand for air-entraining and corrosion-inhibiting blends that extend life-cycle service beyond 50 years.

Geography Analysis

Asia-Pacific held 31.59% of Concrete Admixtures market size in 2025 and is expanding at 6.81% through 2031. China’s dual-carbon plan subsidizes PCE adoption, and India’s USD 1.4 trillion National Infrastructure Pipeline embeds water-reduction clauses in tenders. Japan’s 2025 bridge code mandates UHPC on coastal crossings, and Southeast Asian high-rise builders favor SCC to mitigate labor shortages.

In North America, the U.S. infrastructure act funds bridge and highway projects that earn bonus payments for 20% embodied-carbon cuts, accelerating superplasticizer use. Canada’s infrastructure program ties grant scoring to low water-cement ratios, while Mexico’s nearshoring boom is spurring industrial slab pours that rely on accelerators for rapid commissioning.

The EU’s 310 kg CO₂ e/m³ cap essentially mandates water reducers in public works, and Germany’s KfW loans reward projects verified below 280 kg CO₂ e/m³. The UK’s ISO 14067 procurement rules favor suppliers with digital EPD workflows. Russia’s market remains subdued but shows localized innovation as domestic cement groups build small PCE units to cut import dependence.

South America and the Middle-East and Africa combined for lower share in 2025. Brazil’s infrastructure acceleration program and Saudi Arabia’s NEOM mega-project are major retarder and superplasticizer consumers. Sub-Saharan Africa’s admixture penetration is lower, yet wind-farm foundations in South Africa and Kenya are opening niches for high-early-strength mixes.

Competitive Landscape

The top five suppliers—Sika, Sobute New Materials Co., Ltd., MAPEI, Saint-Gobain, and RPM International—command roughly 43% of global volume, leaving significant room for regional specialists. Sika’s CHF 5.5 billion acquisition of MBCC in 2025 tightened its grip on polycarboxylate-ether technology and broadened its Asia-Pacific footprint. CEMEX’s digital-twin batching network spans 180 plants, reducing average superplasticizer use 18% and locking in multi-year supply deals. Saint-Gobain’s zero-formaldehyde accelerator line secured ISO 14067 verification, positioning the firm for EU green-procurement tenders.

Regional challengers leverage local feedstocks and nimble R&D cycles. Pidilite’s Dr. Fixit brand grew 34% in 2025 by targeting India’s self-build housing market with small-pack plasticizers. Sobute New Materials commissioned a 100,000-ton PCE plant in Jiangsu featuring AI quality-control loops that adjust polymer chain length in real time. Patent filings for AI-guided dosing and bio-based chemistries jumped 28% year-on-year as firms race to secure intellectual property around low-carbon formulations.

Consolidation is accelerating as feedstock shocks expose smaller players. RPM International bought two European formulators totaling 35,000 tons of annual capacity in 2025, while Kao Corporation is commercializing lignin-derived plasticizers offering 40% lower formaldehyde. Niche opportunities persist in hybrid admixtures that combine PCE with nano-silica, delivering both improved rheology and long-term durability for offshore wind foundations and nuclear-waste storage casks.

Concrete Admixtures Industry Leaders

Sika AG

Saint-Gobain

MAPEI S.p.A.

RPM International

Sobute New Materials Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Sika AG expanded its manufacturing operations in Kazakhstan with the inauguration of a new production facility in Ust-Kamenogorsk, its fourth plant in the country. The facility manufactures concrete admixtures and includes a modern laboratory to address the growing demand from the local mining and construction industries.

- December 2024: Chryso, a Saint-Gobain company, developed EnviroMix C-Clay, a range of specialized concrete admixtures designed specifically for low-carbon concrete utilizing calcined clay-based cements. These admixtures enhanced the workability and compressive strength of concrete containing sustainable, high-water-demand calcined clays.

Global Concrete Admixtures Market Report Scope

Concrete admixtures are natural or synthetic chemical or mineral additives added to concrete during mixing to improve properties such as durability, workability, setting time, and strength. Available in liquid or powder form, these materials enable contractors to customize concrete for specific requirements, such as accelerated setting, enhanced flowability, or greater resistance to environmental factors, thereby reducing construction costs and improving structural performance.

The concrete admixtures market is segmented by product-type, end-use sector, and geography. By product type, the market is segmented into water-reducer (plasticizer), accelerator, air-entraining, high-range water-reducer (superplasticizer), retarder, shrinkage-reducing, and other product types. By end-use sector, the market is segmented into infrastructure, residential, commercial, and industrial and institutional. The report also covers the market size and forecasts for concrete admixtures in 22 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Product Type

| Water-Reducer (Plasticizer) |

| Accelerator |

| Air-Entraining |

| High-Range Water-Reducer (Superplasticizer) |

| Retarder |

| Shrinkage-Reducing |

| Other Product Types |

By End-use Sector

| Infrastructure |

| Residential |

| Commercial |

| Industrial and Institutional |

By Geography

| Asia-Pacific | China |

| India | |

| Indonesia | |

| Japan | |

| Malaysia | |

| South Korea | |

| Thailand | |

| Australia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle-East and Africa |

| By Product Type | Water-Reducer (Plasticizer) | |

| Accelerator | ||

| Air-Entraining | ||

| High-Range Water-Reducer (Superplasticizer) | ||

| Retarder | ||

| Shrinkage-Reducing | ||

| Other Product Types | ||

| By End-use Sector | Infrastructure | |

| Residential | ||

| Commercial | ||

| Industrial and Institutional | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Indonesia | ||

| Japan | ||

| Malaysia | ||

| South Korea | ||

| Thailand | ||

| Australia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle-East and Africa | ||

Market Definition

- END-USE SECTOR - Concrete admixtures consumed in the construction sectors such as commercial, residential, industrial, institutional, and infrastructure are considered under the scope of the study.

- PRODUCT/APPLICATION - Under the scope of the study, the consumption of concrete admixture products such as water reducers (plasticizers), retarders, accelerators, air-entraining admixture, viscosity modifiers, shrinkage-reducing admixture, high-range water reducers (superplasticizers), and other types are considered.

| Keyword | Definition |

|---|---|

| Accelerator | Accelerators are admixtures used to fasten the setting time of concrete by increasing the initial rate and speeding up the chemical reaction between cement and the mixing water. These are used to harden and increase the strength of concrete quickly. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Adhesives | Adhesives are bonding agents used to join materials by gluing. Adhesives can be used in construction for many applications, such as carpet laying, ceramic tiles, countertop lamination, etc. |

| Air Entraining Admixture | Air-entraining admixtures are used to improve the performance and durability of concrete. Once added, they create uniformly distributed small air bubbles to impart enhanced properties to the fresh and hardened concrete. |

| Alkyd | Alkyds are used in solvent-based paints such as construction and automotive paints, traffic paints, flooring resins, protective coatings for concrete, etc. Alkyd resins are formed by the reaction of an oil (fatty acid), a polyunsaturated alcohol (Polyol), and a polyunsaturated acid or anhydride. |

| Anchors and Grouts | Anchors and grouts are construction chemicals that stabilize and improve the strength and durability of foundations and structures like buildings, bridges, dams, etc. |

| Cementitious Fixing | Cementitious fixing is a process in which a cement-based grout is pumped under pressure to fill forms, voids, and cracks. It can be used in several settings, including bridges, marine applications, dams, and rock anchors. |

| Commercial Construction | Commercial construction comprises new construction of warehouses, malls, shops, offices, hotels, restaurants, cinemas, theatres, etc. |

| Concrete Admixtures | Concrete admixtures comprise water reducers, air entrainers, retarders, accelerators, superplasticizers, etc., added to concrete before or during mixing to modify its properties. |

| Concrete Protective Coatings | To provide specific protection, such as anti-carbonation or chemical resistance, a film-forming protective coat can be applied on the surface. Depending on the applications, different resins like epoxy, polyurethane, and acrylic can be used for concrete protective coatings. |

| Curing Compounds | Curing compounds are used to cure the surface of concrete structures, including columns, beams, slabs, and others. These curing compounds keep the moisture inside the concrete to give maximum strength and durability. |

| Epoxy | Epoxy is known for its strong adhesive qualities, making it a versatile product in many industries. It resists heat and chemical applications, making it an ideal product for anyone needing a stronghold under pressure. It is widely used in adhesives, electrical and electronics, paints, etc. |

| Fiber Wrapping Systems | Fiber Wrapping Systems are a part of construction repair and rehabilitation chemicals. It involves the strengthening of existing structures by wrapping structural members like beams and columns with glass or carbon fiber sheets. |

| Flooring Resins | Flooring resins are synthetic materials applied to floors to enhance their appearance, increase their resistance to wear and tear or provide protection from chemicals, moisture, and stains. Depending on the desired properties and the specific application, flooring resins are available in distinct types, such as epoxy, polyurethane, and acrylic. |

| High-Range Water Reducer (Super Plasticizer) | High-range water reducers are a type of concrete admixture that provides enhanced and improved properties when added to concrete. These are also called superplasticizers and are used to decrease the water-to-cement ratio in concrete. |

| Hot Melt Adhesives | Hot-melt adhesives are thermoplastic bonding materials applied as melts that achieve a solid state and resultant strength on cooling. They are commonly used for packaging, coatings, sanitary products, and tapes. |

| Industrial and Institutional Construction | Industrial and institutional construction includes new construction of hospitals, schools, manufacturing units, energy and power plants, etc. |

| Infrastructure Construction | Infrastructure construction includes new construction of railways, roads, seaways, airports, bridges, highways, etc. |

| Injection Grouting | The process of injecting grout into open joints, cracks, voids, or honeycombs in concrete or masonry structural members is known as injection grouting. It offers several benefits, such as strengthening a structure and preventing water infiltration. |

| Liquid-Applied Waterproofing Membranes | Liquid-Applied membrane is a monolithic, fully bonded, liquid-based coating suitable for many waterproofing applications. The coating cures to form a rubber-like elastomeric waterproof membrane and may be applied over many substrates, including asphalt, bitumen, and concrete. |

| Micro-concrete Mortars | Micro-concrete mortar is made up of cement, water-based resin, additives, mineral pigments, and polymers and can be applied on both horizontal and vertical surfaces. It can be used to refurbish residential complexes, commercial spaces, etc. |

| Modified Mortars | Modified Mortars include Portland cement and sand along with latex/polymer additives. The additives increase adhesion, strength, and shock resistance while also reducing water absorption. |

| Mold Release Agents | Mold release agents are sprayed or coated on the surface of molds to prevent a substrate from bonding to a molding surface. Several types of mold release agents, including silicone, lubricant, wax, fluorocarbons, and others, are used based on the type of substrates, including metals, steel, wood, rubber, plastic, and others. |

| Polyaspartic | Polyaspartic is a subset of polyurea. Polyaspartic floor coatings are typically two-part systems that consist of a resin and a catalyst to ease the curing process. It offers high durability and can withstand harsh environments. |

| Polyurethane | Polyurethane is a plastic material that exists in various forms. It can be tailored to be either rigid or flexible and is the material of choice for a broad range of end-user applications, such as adhesives, coatings, building insulation, etc. |

| Reactive Adhesives | A reactive adhesive is made of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Rebar Protectors | In concrete structures, rebar is one of the important components, and its deterioration due to corrosion is a major issue that affects the safety, durability, and life span of buildings and structures. For this reason, rebar protectors are used to protect against degrading effects, especially in infrastructure and industrial construction. |

| Repair and Rehabilitation Chemicals | Repair and Rehabilitation Chemicals include repair mortars, injection grouting materials, fiber wrapping systems, micro-concrete mortars, etc., used to repair and restore existing buildings and structures. |

| Residential Construction | Residential construction involves constructing new houses or spaces like condominiums, villas, and landed homes. |

| Resin Fixing | The process of using resins like epoxy and polyurethane for grouting applications is called resin fixing. Resin fixing offers several advantages, such as high compressive and tensile strength, negligible shrinkage, and greater chemical resistance compared to cementitious fixing. |

| Retarder | Retarders are admixtures used to slow down the setting time of concrete. These are usually added with a dosage rate of around 0.2% -0.6% by weight of cement. These admixtures slow down hydration or lower the rate at which water penetrates the cement particles by making concrete workable for a long time. |

| Sealants | A sealant is a viscous material that has little or no flow qualities, which causes it to remain on surfaces where they are applied. Sealants can also be thinner, enabling penetration to a certain substance through capillary action. |

| Sheet Waterproofing Membranes | Sheet membrane systems are reliable and durable thermoplastic waterproofing solutions that are used for waterproofing applications even in the most demanding below-ground structures, including those exposed to highly aggressive ground conditions and stress. |

| Shrinkage Reducing Admixture | Shrinkage-reducing admixtures are used to reduce concrete shrinkage, whether from drying or self-desiccation. |

| Silicone | Silicone is a polymer that contains silicon combined with carbon, hydrogen, oxygen, and, in some cases, other elements. It is an inert synthetic compound that comes in various forms, such as oil, rubber, and resin. Due to its heat-resistant properties, it finds applications in sealants, adhesives, lubricants, etc. |

| Solvent-borne Adhesives | Solvent-borne adhesives are mixtures of solvents and thermoplastic or slightly cross-linked polymers such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers. |

| Surface Treatment Chemicals | Surface treatment chemicals are chemicals used to treat concrete surfaces, including roofs, vertical surfaces, and others. They act as curing compounds, demolding agents, rust removers, and others. They are cost-effective and can be used on roadways, pavements, parking lots, and others. |

| Viscosity Modifier | Viscosity Modifiers are concrete admixtures used to change various properties of admixtures, including viscosity, workability, cohesiveness, and others. These are usually added with a dosage of around 0.01% to 0.1% by weight of cement. |

| Water Reducer | Water reducers, also called plasticizers, are a type of admixture used to decrease the water-to-cement ratio in the concrete, thereby increasing the durability and strength of concrete. Various water reducers include refined lignosulfonates, gluconates, hydroxycarboxylic acids, sugar acids, and others. |

| Water-borne Adhesives | Water-borne adhesives use water as a carrier or diluting medium to disperse resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a dilutant rather than a volatile organic solvent. |

| Waterproofing Chemicals | Waterproofing chemicals are designed to protect a surface from the perils of leakage. A waterproofing chemical is a protective coating or primer applied to a structure's roof, retaining walls, or basement. |

| Waterproofing Membranes | Waterproofing membranes are liquid-applied or self-adhering layers of water-tight materials that prevent water from penetrating or damaging a structure when applied to roofs, walls, foundations, basements, bathrooms, and other areas exposed to moisture or water. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms