Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

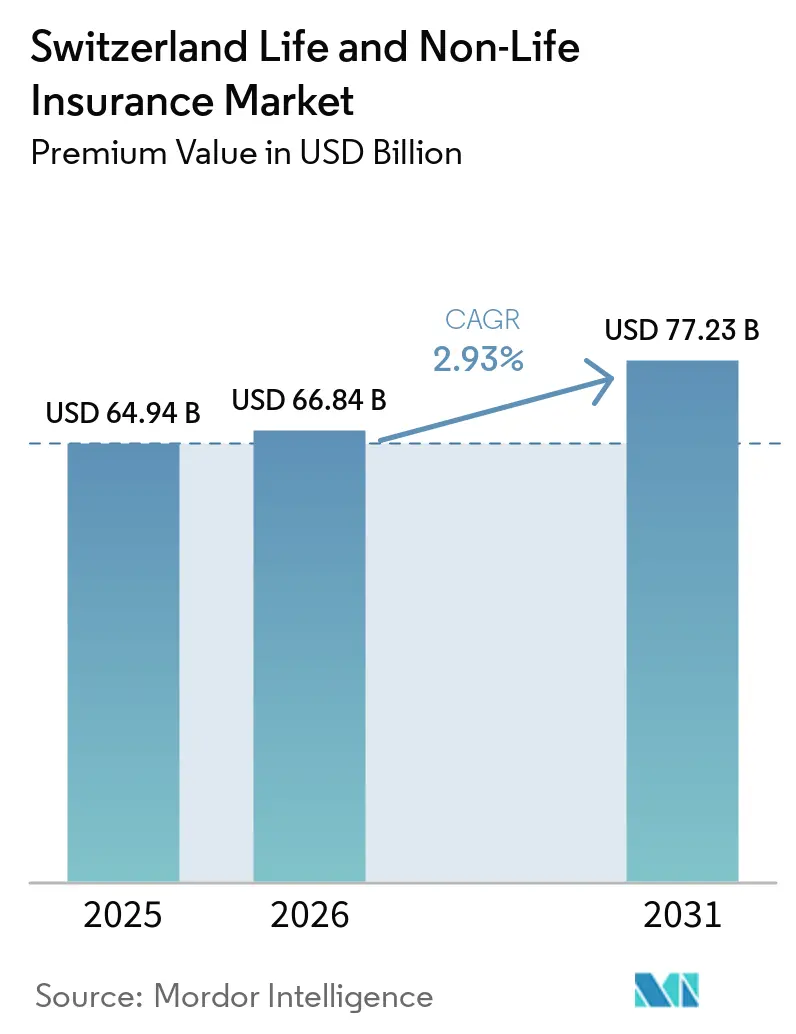

| Base Year Market Size (2025) | USD 64.94 Billion |

| Market Size (2026) | USD 66.84 Billion |

| Market Size (2031) | USD 77.23 Billion |

| Growth Rate (2026 - 2031) | 2.93% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Switzerland Life and Non-Life Insurance Market Analysis by Mordor Intelligence

The Switzerland Life And Non-Life Insurance Market size in terms of premium value is projected to be USD 64.94 billion in 2025, USD 66.84 billion in 2026, and reach USD 77.23 billion by 2031, growing at a CAGR of 2.93% from 2026 to 2031.

This steady expansion of the Switzerland life and non-life insurance market reflects structural product shifts rather than pure volume growth, as insurers redesign savings solutions to cope with chronically low yields and invest in data-driven underwriting capabilities. Digital distribution, mandatory accident coverage reform, and climate-risk regulation jointly broaden the risk pool, while unit-linked life products offset the profitability pressures created by negative interest rates. Supplemental health covers, green property insurance, and usage-based motor policies emerge as the fastest-growing niches within the Switzerland life and non-life insurance market, underpinning insurer revenue resilience despite saturated core lines. Competitive strategies increasingly revolve around actuarial talent acquisition, cyber-underwriting depth, and ESG-aligned portfolios under FINMA’s stress-testing regime.

Key Report Takeaways

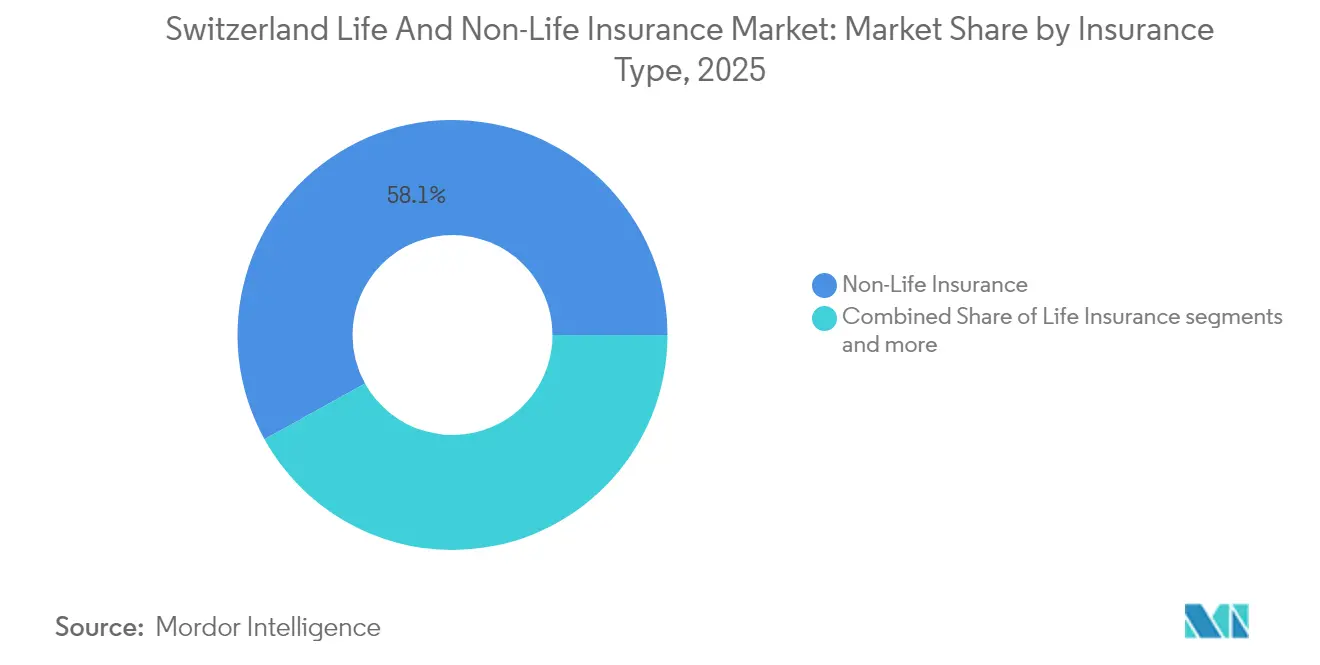

- By insurance type, non-life business retained a 58.05% Switzerland life and non-life insurance market in 2025, whereas life products are forecast to post the highest 4.06% CAGR through 2031.

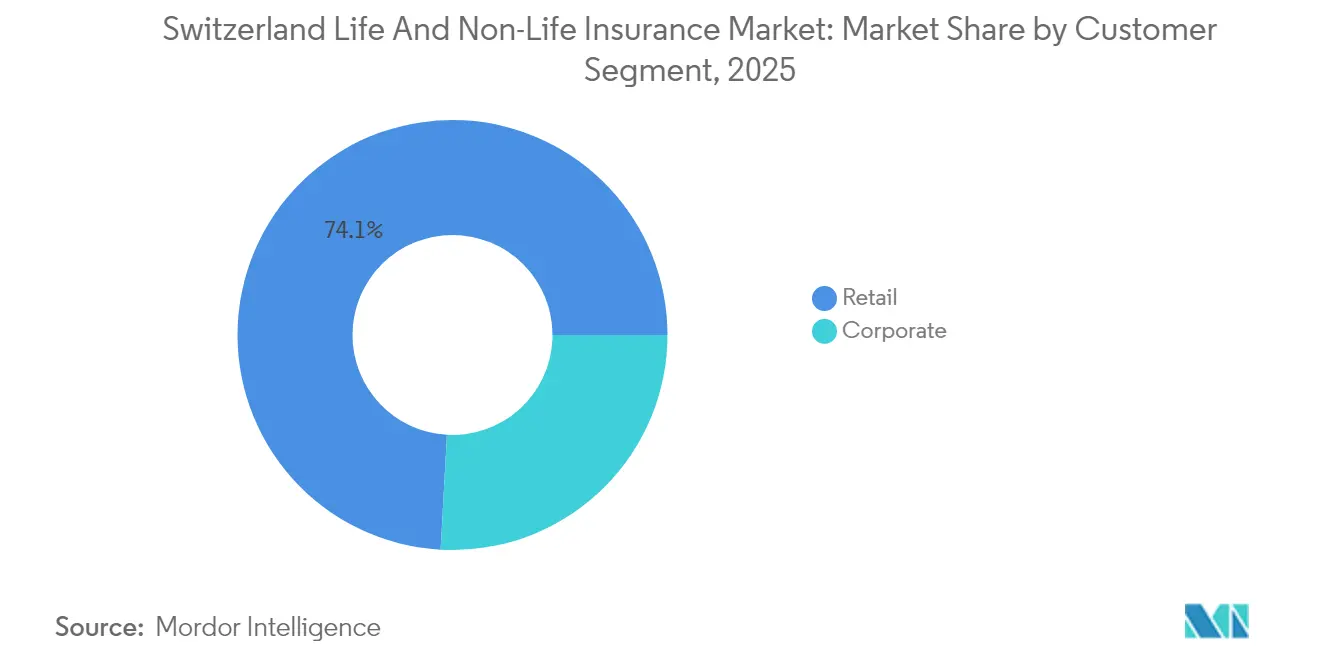

- By customer segment, retail clients held 74.12% of the Switzerland life and non-life insurance market size in 2025, while corporate business is expanding at a faster 3.25% CAGR to 2031.

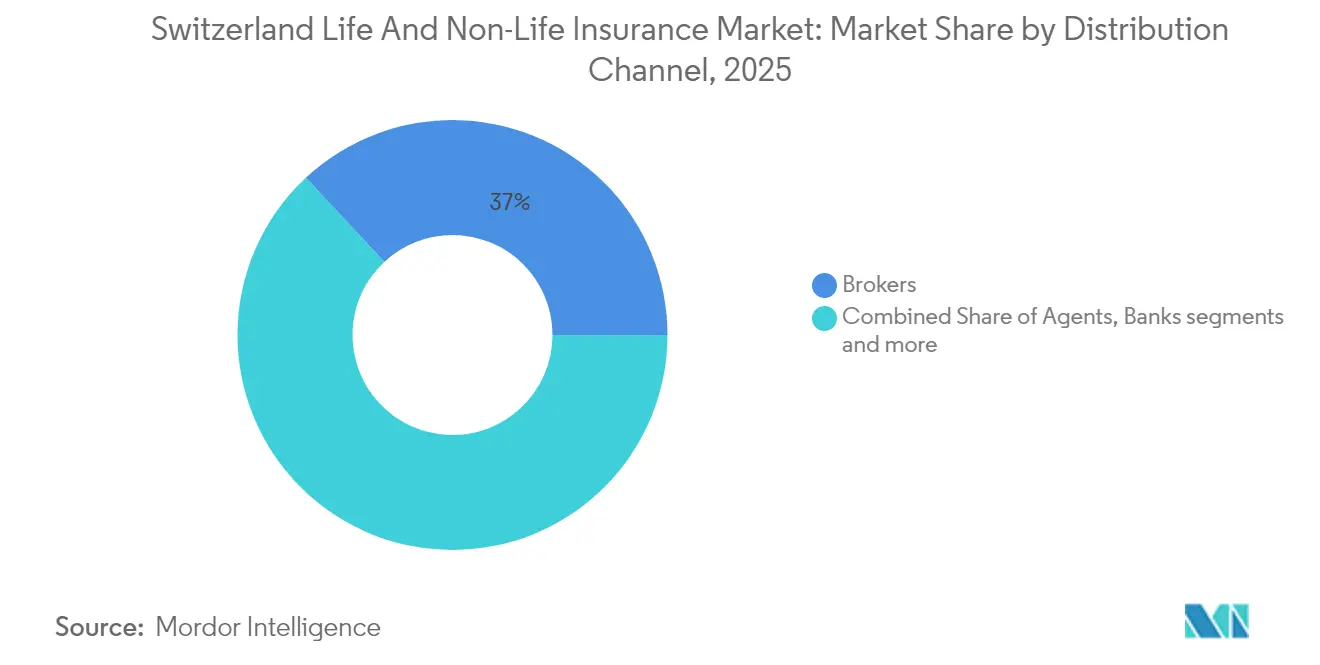

- By distribution channel, brokers controlled 36.95% of written premiums in 2025; however, direct digital sales are advancing at a 2.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Switzerland Life and Non-Life Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustained ultra-low interest-rate environment boosting unit-linked life products | +0.8% | Switzerland nationwide, spillover to Liechtenstein | Medium term (2-4 years) |

| Rising health-care expenditure is pushing supplemental health covers | +0.6% | Switzerland nationwide, concentrated in urban cantons | Long term (≥ 4 years) |

| Mandatory accident cover reform widening retail client pool | +0.4% | Switzerland nationwide | Short term (≤ 2 years) |

| Growing usage-based telematics is driving motor premium re-pricing | +0.3% | Switzerland, early adoption in German-speaking regions | Medium term (2-4 years) |

| Embedded-insurance partnerships with Swiss neo-banks | +0.2% | Switzerland, concentrated in fintech hubs | Short term (≤ 2 years) |

| Climate-risk stress-testing requirements are accelerating green-property covers | +0.3% | Alpine regions, expanding to lowland areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ultra-Low Interest Rates Reshape Life Insurance Product Mix

Unit-linked contracts have displaced capital-guaranteed savings because negative Swiss-franc yields eroded spread earnings. Swiss Life disclosed double-digit unit-linked premium growth in 2024, confirming a secular pivot toward fee-based solutions[1]Source: Swiss Life Holding, “Annual Report 2024,” swisslife.ch. FINMA now obliges life carriers to stress-test liabilities under prolonged low-rate scenarios, incentivizing hybrid savings policies that combine a floor with equity participation. These designs reduce duration mismatch and attract policyholders seeking upside exposure. The Switzerland life and non-life insurance market, therefore, channels more capital to mutual-fund-linked wrappers while shrinking traditional conversion reserves.

Healthcare Cost Inflation Drives Supplemental Coverage Demand

Total health expenditure hit USD 104.9 billion (CHF 97.1 billion) in 2024, lifting average mandatory-premium increases to 6% in 2025[2]Federal Office of Public Health, “Health Expenditure Statistics 2024,” bag.admin.ch.. Employers respond by enriching voluntary group health plans to retain talent in high-cost cantons. Private insurers benefit because outpatient services migrate away from cantonal budgets and fall under mandatory cover caps, motivating households to purchase add-ons for dental, semi-private wards, and alternative therapies. Over the forecast period, supplemental health will remain the second-fastest expanding line within the Switzerland life and non-life insurance market, only behind unit-linked life.

Mandatory Accident Coverage Reform Expands Market Reach

Amendments to Switzerland’s accident-insurance law now compel coverage for employees working fewer than eight hours per week, a group that includes gig-economy staff and seasonal laborers. This widens the retail client base for occupational accident policies and offers private carriers a chance to compete against SUVA in non-industrial risks. Employers are turning to bundled accident-plus-health packages that simplify administration and meet new legal standards. At the same time, remote work and digital tools introduce fresh ergonomic and mental-health exposures that insurers are learning to price. Underwriters able to tailor coverage to these emerging risks gain an edge when group contracts come up for renewal.

Telematics Technology Transforms Motor Pricing

Major carriers accelerated usage-based programs in 2024, with Zurich’s MyWay offering pay-per-kilometer policies for low-mileage urban drivers[3]Zurich Switzerland, “MyWay Usage-Based Insurance,” zurich.ch. . Real-time data allows premiums to reflect driving behavior rather than broad demographic factors, sharpening risk segmentation across the motor book. The spread of electric vehicles adds new telematics use cases, including battery-health monitoring and charging-station liability cover. FINMA requires explicit customer consent for data harvesting, pushing insurers to differentiate on transparency and cybersecurity safeguards. Safer motorists now earn lower rates, while high-risk behaviors carry steeper prices, disrupting the traditional cross-subsidy embedded in Swiss motor pools.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pension-fund consolidation shrinking group-life policy counts | -0.4% | Switzerland, nationwide, concentrated in industrial cantons | Medium term (2-4 years) |

| Cross-border data localization costs for EU-resident clients | -0.3% | Border regions, financial centers | Short term (≤ 2 years) |

| Rising catastrophe-loss ratios in Alpine regions | -0.2% | Alpine cantons, expanding to pre-Alpine areas | Long term (≥ 4 years) |

| Talent shortage in actuarial & cyber-underwriting specialties | -0.3% | Switzerland nationwide, acute in urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Pension Fund Consolidation Reduces Group Life Volumes

Dozens of small occupational pension schemes merged into large collective foundations during 2024 to cut administrative costs and meet stricter governance rules. Fewer buying entities mean group-life insurers must fight harder for each mandate and often concede on price. Larger pension funds also self-insure more mortality risk, shrinking the market for external cover. Mid-tier carriers that once specialized in SME pension business are pivoting toward individual policies or value-added wellness services to offset lost volume. The trend is expected to continue as regulatory oversight grows more demanding over the medium term.

Cross-Border Data Compliance Creates Operational Friction

Switzerland’s revised Federal Act on Data Protection took effect in 2023 and, together with EU localization rules, forces insurers to store and process EU-resident data within approved jurisdictions. Firms must adopt Swiss-specific contractual clauses and keep dual IT infrastructures, raising fixed costs. FINMA now mandates 24-hour reporting of material cyber incidents, heightening the operational burden for carriers with cross-border clients. Smaller insurers lacking dedicated compliance teams face proportionally higher expense ratios and may quit certain markets altogether. This complexity is spawning insurtech vendors that sell turnkey regulatory-technology solutions to traditional players.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insurance Type: Life Products Regain Momentum

Life products generated 41.95% of written premiums in 2025 and are expected to expand at a 4.06% CAGR through 2031, eclipsing non-life’s 2.03% pace. Guaranteed-rate portfolios declined, yet unit-linked policy penetration rose to 37% of new life sales in 2025 as customers chased capital-market returns. Swiss Re’s life reinsurance results surged to USD 3.2 billion profit in 2024, signaling healthy mortality-risk transfer appetite. The Switzerland life and non-life insurance market size for life lines is projected to reach USD 32.68 billion by 2031, while non-life will touch USD 44.55 billion. Climate-adjusted property cover and telematics-enabled motors continue dominating non-life, but profitability swings with catastrophe activity in Alpine zones.

Non-life remains the revenue anchor because mandatory motor, accident, and property policies sustain premium flow. Nevertheless, environmental liability and cyber covers grow at mid-single-digit rates as Swiss boards integrate TCFD reporting. The Switzerland life and non-life insurance market faces lower combined ratios in motor thanks to safer connected cars, yet mountainous terrain and hail events still challenge property profitability. Insurers, therefore, diversify into preventive-services subscriptions, embedding sensors in buildings to reduce loss frequency.

By Customer Segment: Corporate Premiums Outpace Retail Growth

Retail clients accounted for roughly three-quarters of premiums in 2025, but corporate portfolios will rise faster at a 3.25% CAGR. Embedded insurance alliances with neobanks and payroll platforms integrate fleet, cyber, and key-man covers into digital finance ecosystems, lifting penetration among SMEs. The Helvetia-Baloise merger purposely targets multinational program capacity, bundling P&C and employee benefits for cross-border firms. The Switzerland life and non-life insurance market share for corporate business is projected to climb to 28.40% by 2031 as ESG disclosure obligations increase demand for specialized liability lines.

Household budgets remain stretched by higher health premiums, tempering retail uptake of discretionary policies. Still, demographic aging boosts long-term care riders, and mandatory accident reform enlarges the youth insured base. Direct-to-consumer apps simplify onboarding and micro-duration travel or gadget insurance, preserving relevance among millennials. Corporate buyers, meanwhile, seek data analytics, risk-prevention consulting, and captive-fronting services, expanding fee income beyond pure underwriting.

By Distribution Channel: Digital Direct Gains Speed

Brokers retained a 36.95% premium share in 2025 because complex corporate and life products still require tailored advice. Yet direct digital sales grew 2.86% annually as insurers optimized web funnels, robo-advice, and instant issuance for standard motor and travel covers. AXA Switzerland’s bancassurance platform with Additiv illustrates convergence between banking and insurance journeys. The Switzerland life and non-life insurance market size captured through direct channels is expected to surpass USD 12.58 billion by 2031, underpinned by API-enabled quote engines.

Agency networks rationalize as small independents struggle with regulatory training costs and technology investment. Larger brokerages launch risk-advisory consultancies and absorb agents to consolidate bargaining power. Bank distribution remains steady but is limited by anti-tying rules that restrict cross-selling. Insurtech white-label portals empower brokers to maintain relational capital while delivering digital experiences, preventing abrupt disintermediation.

Geography Analysis

Economic prosperity, political stability, and stringent oversight position Switzerland as one of the most sophisticated insurance environments worldwide. FINMA’s proactive governance, including climate-stress pilots and cyber-resilience reporting, enforces prudence that safeguards policyholders and sustains foreign-client confidence. The Switzerland life and non-life insurance market benefits from Zurich and Geneva’s financial clusters, which demand professional indemnity, D&O, and art-insurance solutions for wealth-management activities. Cross-border commuters in cantons adjoining Germany, France, and Italy drive niche demand for international health, accident, and motor covers, although data-localization rules inflate compliance overhead.

Regional adoption of telematics and digital channels skews toward German-speaking areas, where high broadband penetration and urban car-sharing norms accelerate pay-per-use motor policies. French-speaking cantons favor traditional broker consultation, reflecting cultural preferences for face-to-face advice. Italian-speaking Ticino’s SME landscape leans heavily on bancassurance through local cooperative banks. These nuances require multi-lingual policy wording and channel flexibility, complicating scale strategies for newcomers to the Switzerland life and non-life insurance market.

The Alpine topography imposes unique catastrophe exposures, particularly rockfalls and glacial lake outbursts. The 2024 Blatten glacier collapse resulted in USD 345.6 million (CHF 320 million) of insured losses. Property insurers revise zoning premiums and invest in satellite-based early-warning systems to mitigate claim volatility. Climate-risk regulation also obliges disclosure of insured CO₂ footprints, steering capital toward energy-efficient building covers. Healthcare cost differentials across cantons further diversify supplemental-health penetration, as Zurich, Basel-Stadt, and Geneva record the highest outpatient spending per capita.

Competitive Landscape

Helvetia and Baloise agreed to merge, forming Helvetia Baloise Holding with CHF 20 billion business volume, making it Switzerland’s second-largest insurer. Market share leadership brings scale advantages in reinsurance purchases and regulatory capital efficiency that smaller carriers struggle to match. FINMA nonetheless notes that competitive tension persists because niche specialists still capture corporate and high-net-worth segments.

Technology spending now separates leaders from followers. Zurich Insurance hired more than 1,000 digital specialists in analytics and cybersecurity during 2024-2025 to refine pricing and claims automation. Swiss Re applies proprietary climate models to secure long-term catastrophe treaties and deepen client retention. AXA’s bancassurance portal with Additiv embeds instant quotes in retail banking apps, illustrating how incumbents defend share against fintech entrants.

Start-ups in Zug and Zurich supply white-label APIs that let e-commerce firms add travel, gadget, and cyber covers at checkout, widening embedded-insurance penetration. Pension consolidators such as Liberty focus on plans that draw affluent retirement savings away from traditional life portfolios. The actuarial talent gap inflates salary costs and can delay product launches, turning specialist boutiques into attractive takeover targets for global groups. ESG reporting rules also reshape underwriting appetite as carriers disclose portfolio carbon footprints and shift assets toward lower-emission sectors.

Switzerland Life and Non-Life Insurance Industry Leaders

Zurich Insurance Company

Swiss Re

Helvetia Group

Baloise Group

Swiss Life

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Helvetia and Baloise agreed to merge, forming Helvetia Baloise Holding Ltd with USD 21.6 billion (CHF 20 billion) combined business volume and targeted CHF 350 million (USD 378 million) pre-tax collaborations.

- February 2025: Swiss Re posted a 2024 net profit of USD 3.2 billion and raised its dividend to USD 7.35 per share, underlining strong life and non-life reinsurance momentum.

- January 2025: Allianz reported USD 4.3 billion (EUR 4.2 billion) operating profit for Q1 2025, equaling 26% of its full-year outlook, with life/health segments leading growth.

- October 2024: Swiss health insurance premiums rose by 6% for 2025, building on an 8.7% surge in 2024. The Federal Office of Public Health cited escalating healthcare costs and insurers' anticipation of a 4.2% cost growth as the primary drivers behind the hikes.

Switzerland Life and Non-Life Insurance Market Report Scope

Insurance exists as a legal agreement between an insurer and an insured where the insured receives financial assistance in the occurrence of an unobserved event. The insurance products are divided into categories of life and non-life, where life insurance protects against human injury, and non-life insurance protects physical assets. The study gives a brief description of Switzerland's life & non-life insurance market. It includes details on market sales of different types of insurance products, investments by insurance companies, and the launch of new insurance products in Switzerland. The life and non-life insurance market in Switzerland is segmented by insurance type (life insurance (individual and group) and non-life insurance (home, motor, and other non-life insurance)) and by distribution channel (direct, agency, banks, and other distribution channels). The report also covers the market sizes and forecasts for the Switzerland life & non-life insurance market in value (USD) for all the above segments.

By Insurance Type

| Life Insurance | |

| Non-Life Insurance | Motor Insurance |

| Health Insurance | |

| Property Insurance | |

| Liability Insurance | |

| Other Insurance |

By Customer Segment

| Retail |

| Corporate |

By Distribution Channel

| Brokers |

| Agents |

| Banks |

| Direct Sales |

| Other Channels |

| By Insurance Type | Life Insurance | |

| Non-Life Insurance | Motor Insurance | |

| Health Insurance | ||

| Property Insurance | ||

| Liability Insurance | ||

| Other Insurance | ||

| By Customer Segment | Retail | |

| Corporate | ||

| By Distribution Channel | Brokers | |

| Agents | ||

| Banks | ||

| Direct Sales | ||

| Other Channels | ||

Key Questions Answered in the Report

What is the current size of the Switzerland life and non-life insurance market?

The Switzerland life and non-life insurance market size stood at USD 66.84 billion in 2026.

How fast will premiums grow through 2031?

Aggregate written premiums are forecast to rise at a 2.93% CAGR, reaching USD 77.23 billion by 2031.

Which insurance line is expanding the quickest?

Unit-linked life products lead growth, supported by a 4.06% CAGR between 2026-2031 amid persistent low interest rates.

Why are supplemental health plans gaining traction?

Escalating healthcare expenditure, USD 104.9 billion (CHF 97.1 billion) in 2024, drives employers and households to buy additional coverage.

How is digitalization affecting distribution?

Direct online channels are the fastest-growing avenue, advancing at a 2.86% CAGR as insurers invest in self-service platforms and automated underwriting.

What impact does the Helvetia-Baloise merger have on competition?

The merger lifts the combined group to second place by premiums and is expected to deliver USD 378 million in annual synergies, intensifying scale-driven competition.

Page last updated on: