Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

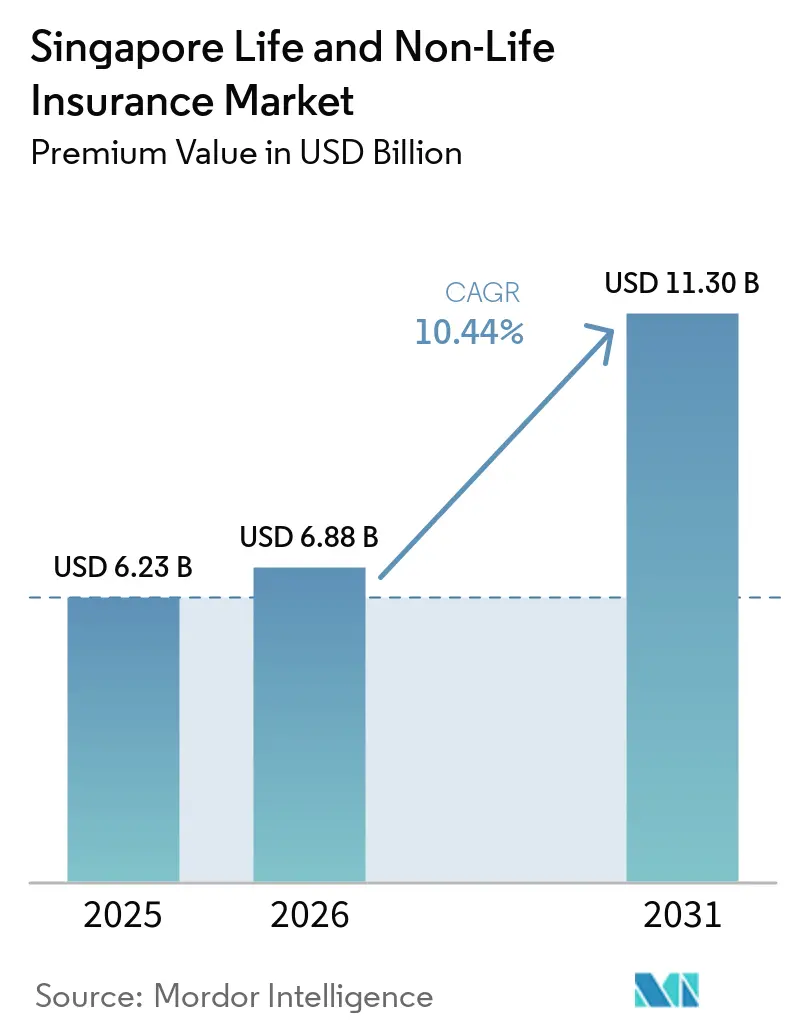

| Base Year Market Size (2025) | USD 6.23 Billion |

| Market Size (2026) | USD 6.88 Billion |

| Market Size (2031) | USD 11.30 Billion |

| Growth Rate (2026 - 2031) | 10.44% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Life and Non-Life Insurance Market Analysis by Mordor Intelligence

The Singapore Life And Non-Life Insurance Market size in terms of premium value is expected to increase from USD 6.23 billion in 2025 to USD 6.88 billion in 2026 and reach USD 11.30 billion by 2031, growing at a CAGR of 10.44% over 2026-2031.

Rising mandatory health coverage, rapid digitalisation, and sustained wealth accumulation among high-net-worth residents underpin this momentum. The strong showing of non-life lines, generous government grants for fintech, and expanding retirement needs jointly reinforce premium growth. Meanwhile, tighter Monetary Authority of Singapore (MAS) capital rules elevate compliance costs, prompting consolidation among incumbents even as insurtech entrants use regulatory sandboxes to scale. Private insurers also benefit from the limited public safety-net of MediShield Life, which drives consumers toward supplementary health and retirement products.

Key Report Takeaways

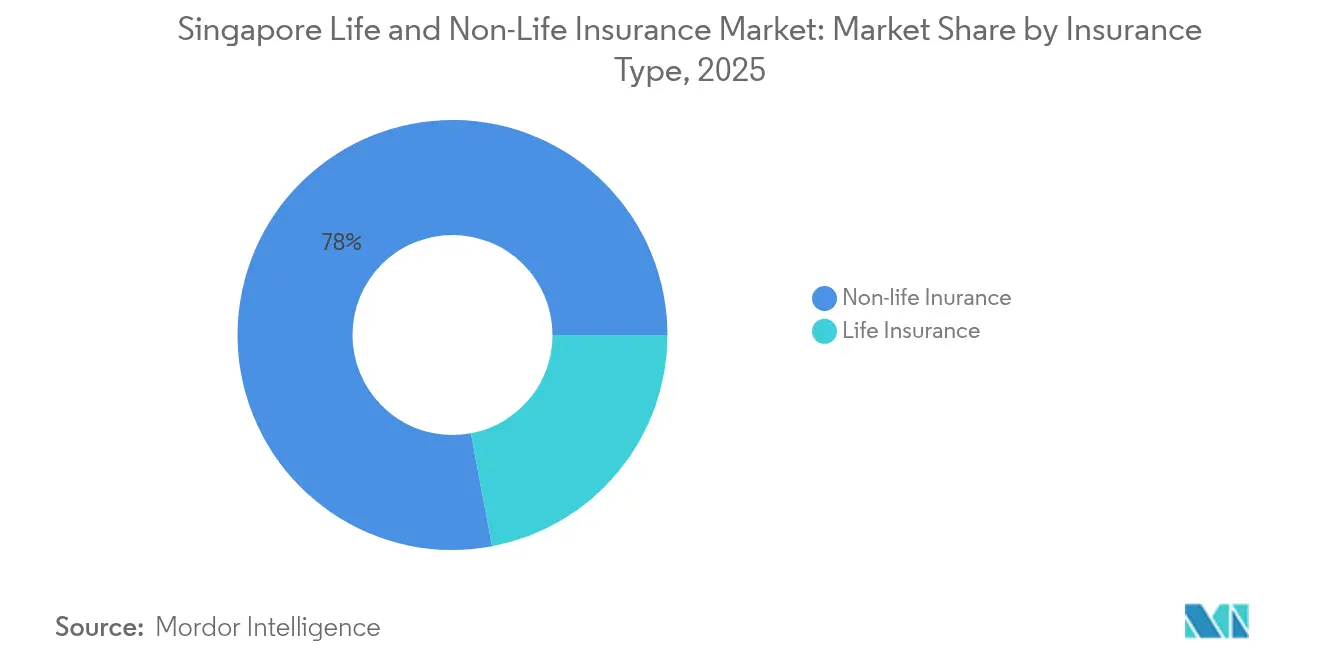

- By type, non-life lines led with 77.95% of Singapore life and non-life insurance market share in 2025, while life lines are forecast to grow the fastest at an 11.54% CAGR to 2031.

- By distribution channel, captive and exclusive agents held 37.45% of revenue in 2025; direct online and insurtech platforms are expanding at 16.98% CAGR through 2031.

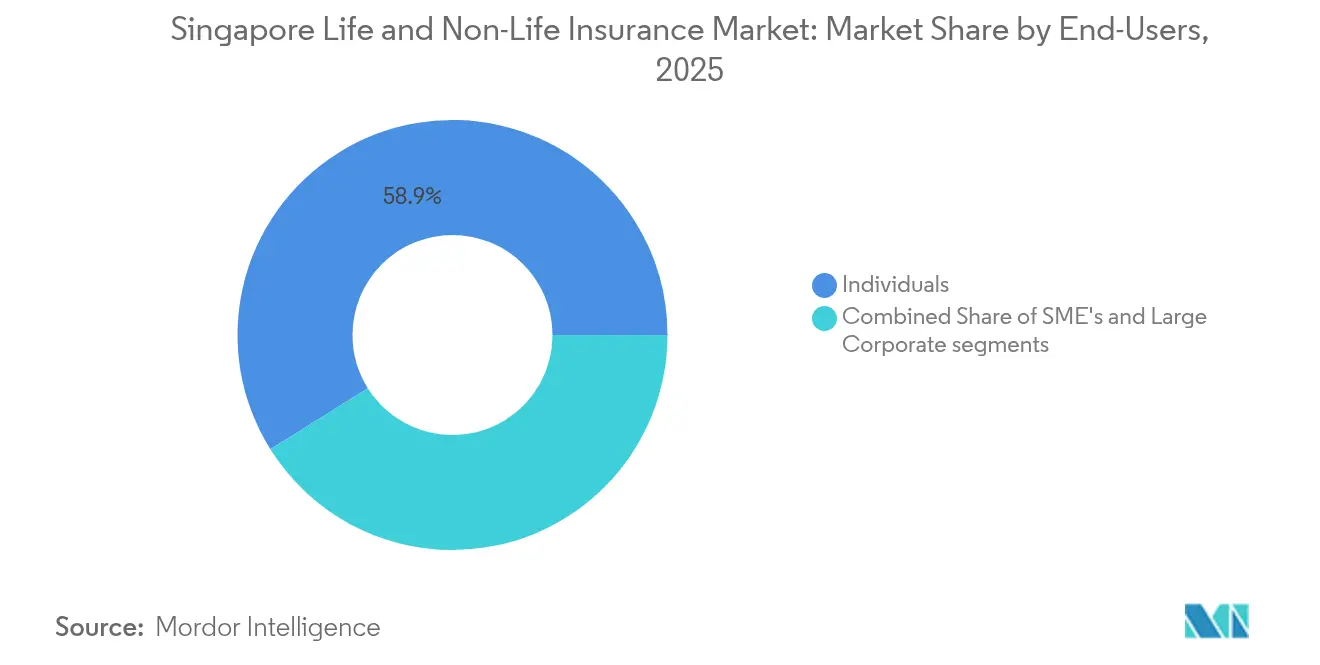

- By end user, individuals accounted for 58.92% of written premiums in 2025; the SME segment is pacing forward at an 8.41% CAGR to 2031.

- By premium type, renewal business represented 57.02% of Singapore life and non-life insurance market size in 2025, while new business premiums are growing at 8.28% annually.

- By region, the Central Region captured 34.95% revenue in 2025; the North Region is projected to advance at a 10.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Singapore Life and Non-Life Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory health insurance and CPF Life reform | +2.1% | National – higher in Central and North | Medium term (2-4 years) |

| Digital adoption backed by MAS grants | +1.8% | National – urban centres | Short term (≤ 2 years) |

| Ageing population raising demand for retirement solutions | +2.3% | National – Central and East | Long term (≥ 4 years) |

| Car-population controls supporting motor premium base | +1.4% | National – West and North | Medium term (2-4 years) |

| Rising HNW segment boosting single-premium ILPs | +1.6% | Central and East | Medium term (2-4 years) |

| Government climate-resilience programs | +1.2% | National – coastal areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory health insurance and CPF Life reform accelerating life-coverage uptake

Singapore’s compulsory MediShield Life coverage and the recently enhanced CPF Life annuity scheme stimulate incremental demand for supplementary policies rather than crowding out private insurers. The Ministry of Health will phase in USD 1.332 billion of extra premiums between 2025 and 2027, offset by USD 3.03 billion of subsidies through MediSave top-ups, sustaining affordability for most residents[1]Ministry of Health, “Enhancements to MediShield Life and CareShield Life,” moh.gov.sg. Annual claim limits rise to USD 148,000 with no lifetime cap, prompting consumers to layer integrated shield plans for additional benefits. Around 70% of citizens already hold these riders, underscoring the opportunity for insurers to upsell higher-end covers. Foreign workers, excluded from MediShield, must rely solely on private solutions, forming a captive risk pool that provides recurring revenue. These structural factors strengthen the Singapore life and non-life insurance market growth outlook across both the individual and group segments.

Rapid digital adoption and MAS grants fuelling online-distribution expansion

Globally recognised as a fintech sandbox, Singapore offers streamlined licensing and co-funding schemes that lower barriers for insurtech start-ups. The extension of MAS Fair Dealing Guidelines to every financial institution in May 2024 sharpens product-suitability standards and fosters trust [2]Monetary Authority of Singapore, “Annual Report 2023/2024,” mas.gov.sg . Consumers increasingly prefer friction-less online journeys for motor, travel, and personal-accident policies, a trend magnified by high mobile-internet penetration and advanced e-payment rails. Digital distributors therefore gain share quickly, eroding the 38.24% share held by traditional agency networks while exerting downward pressure on acquisition costs across the Singapore life and non-life insurance market.

Ageing population driving demand for retirement and whole-life products

By 2030, one in four Singapore residents will be at least 65, intensifying interest in annuities, critical-illness, and long-term-care covers. CareShield Life payouts climbed to USD 480.3 per month in 2024 and will continue to escalate by 2% annually, yet remain insufficient for all medical contingencies. Households, therefore, pivot to whole-life and endowment plans promising guaranteed cash values. The rapid rise in family offices from 400 in 2020 to 1,650 by 2024 amplifies demand for capital-efficient single-premium solutions suitable for wealth transfer. The above-mentioned pointers boost the Singapore life and non-life insurance market's long-run revenue and product-innovation pipeline.

Car-population policies sustaining the motor-insurance premium base

The Certificate of Entitlement (COE) quota caps total vehicles, preventing fleet oversupply and supporting relatively stable premium revenue despite ridesharing. Q1 2025 saw 2,834 COE renewals, the highest since 2020, as households deferred new purchases amid economic uncertainty. High COE prices and a 40% share of electric vehicles among new registrations create more expensive replacement costs, sustaining robust motor-insurer margins. Against this backdrop, the Singapore life and non-life insurance market maintains a predictable motor-premium runway.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low interest rates diluting investment returns | -1.7% | National – all insurers | Long term (≥ 4 years) |

| Stagnant population growth limiting risk-pool expansion | -1.2% | National – mature estates | Long term (≥ 4 years) |

| Stricter MAS RBC 2 capital rules | -0.9% | National – all licensees | Medium term (2-4 years) |

| Price-sensitive consumers using comparison portals | -1.1% | National – commodity products | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Low interest-rate environment compressing insurers’ investment returns

Persistently slim bond yields challenge the traditional surplus-generation model that relies on investment income to subsidise underwriting. The January 2025 MAS Monetary Policy Statement anticipates core inflation of 1–2%, reinforcing a lower-for-longer yield curve. Life insurers must reprice or curtail dividends on participating policies, while pivoting toward unit-linked offerings that transfer market risk to policyholders. Although top players such as AIA maintain solvency ratios above 250%, smaller carriers face capital strain, curbing product-development agility and thereby constraining the Singapore life and non-life insurance market over the next decade.

Price-sensitive consumers and comparison portals intensifying premium competition

Well-informed policyholders use aggregators to benchmark prices instantly, commoditising standard motor and travel covers. MAS has warned of phishing scams mimicking premium-collection calls, illustrating both high digital sophistication and potential downside from misplaced trust. Transparent quoting forces incumbents to trim margins or add service layers, whereas digital-first newcomers leverage lean cost structures to undercut legacy pricing. The net result is slimmer profitability across commodity lines in the Singapore life and non-life insurance market, compelling carriers to seek differentiation in speciality or value-added segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insurance Type: Life Insurance Accelerates Despite Non-Life Dominance

Non-life lines commanded 77.95% of premiums in 2025, yet life products are projected to deliver an 11.54% CAGR to 2031, making them the primary engine of future growth in the Singapore life and non-life insurance market. Motor insurance remains the largest non-life contributor, supported by controlled vehicle numbers, premium vehicle values, and consistent COE renewals. Health and medical lines also expand as MediShield Life claim limits rise, driving uptake of supplementary covers. Property insurance gains traction as climate-resilience spending accelerates, while marine and transit products benefit from Singapore’s status as a logistics hub.

The life segment’s momentum stems from demographic ageing and surging wealth-management activity. Whole-life, endowment, and investment-linked policies appeal to households seeking guaranteed cash values or market participation. AIA Singapore posted a 15% jump in the value of new business in 2024, validating this shift. The Singapore life and non-life insurance market size for life lines is therefore slated to expand meaningfully, even as non-life retains the larger absolute share of written premiums.

By Distribution Channel: Digital Disruption Reshapes Traditional Models

Captive and exclusive agents held 37.45% of premiums in 2025, underscoring the enduring importance of face-to-face advice in complex policies. Yet direct online and insurtech platforms clock a 16.98% CAGR, the fastest trajectory within the Singapore life and non-life insurance market. Consumers favour instant quotes, e-KYC, and electronic policy issuance for motor, travel, and term-life lines. AIA’s bancassurance tie-up with Citibank illustrates how incumbents combine bank partnerships and digital upgrades to reach affluent clients.

Independent advisers retain relevance by comparing multiple carriers and providing high-touch service to SMEs and high-net-worth segments. Brokers focus on speciality commercial risks, leveraging analytical tools and global market access. Traditional phone and mail channels shrink rapidly. The net result is an omnichannel landscape where incumbents digitise agency workflows to protect renewal books while new entrants compete on convenience and price, sustaining competitive intensity across the Singapore life and non-life insurance industry.

By End User: SME Segment Emerges as Growth Driver

Individuals still account for 58.92% of premiums, reflecting broad penetration across life, motor, and health products. However, the SME segment is forecast to grow at 8.41% annually, aided by higher regulatory compliance thresholds, cyber-risk awareness, and government incentives for enterprise development. Around 75% of self-employed persons now make timely MediSave contributions, a proxy for insurance engagement. Corporates remain steady buyers of specialised covers such as directors’ and officers’ and trade-credit insurance.

The swelling SME base signals a multi-year opportunity for carriers to bundle property, liability, benefits, and cyber policies. Insurers with modular platforms can underwrite smaller risks profitably at scale, enhancing the Singapore life and non-life insurance market size attributed to commercial lines. Individual demand also remains buoyant owing to wealth accumulation and the migration of family offices, boosting uptake of single-premium estate-planning solutions.

By Premium Type: Renewal Business Stability Supports Growth

Renewal business generated 57.02% of 2025 premiums, underscoring customer stickiness and predictable cashflows within the Singapore life and non-life insurance market. New business, while smaller, is advancing at 8.28% a year as carriers attract first-time buyers and upsell supplementary riders. AIA’s Annualised New Premiums spiked 52% to USD 897 million in 2024, demonstrating vigorous client acquisition.

Steady renewal inflows finance technology upgrades and regulatory-capital buffers, whereas rising new-business volumes expand the addressable market. Price competition is particularly strong in renewal cycles for motor and health riders, incentivising loyalty programs and digital-claims service to retain policyholders. Together, healthy renewal streams and growing new sales sustain balanced expansion in the Singapore life and non-life insurance industry.

Geography Analysis

Singapore’s compact geography means regional insurance patterns mirror economic-activity clusters rather than climatic risk differentials. Central Region dominance stems from its role as the financial hub, generating outsized demand for commercial property, directors and officers, and high-net-worth personal lines. Multinationals headquartered here purchase expansive cyber and professional-indemnity covers. Singapore attracted USD 230 billion of ASEAN foreign-direct investment in 2023, much of which flows through the central business district, reinforcing premium volumes.

To the north, large-scale residential projects and new MRT lines stimulate property and motor-policy sales. Leasehold condominiums near emerging stations record median gains that drive mortgage-linked insurance take-up. The Singapore life and non-life insurance market therefore benefits from urban-redevelopment initiatives that broaden the insurable asset base. East and West regions cater to established residential and industrial estates. Logistics hubs in the West seek tailored cargo and marine policies, while the East’s ageing housing stock prompts higher sums insured for renovations and flood-mitigation riders.

The island-wide climate-resilience program, including drainage upgrades and sea-wall pilots, raises awareness of catastrophe cover, diversifying the risk pool. Motor insurers likewise adapt to rising electric-vehicle penetration, adding battery-replacement clauses and home-charger liabilities. Collectively, regional trends affirm a broadening Singapore life and non-life insurance market that is less dependent on any single zone for growth and instead reflects coordinated urban-planning priorities.

Competitive Landscape

The market features a solid core of long-established carriers complemented by agile digital entrants. AIA, Great Eastern, Prudential, and NTUC Income form the top tier, leveraging multi-channel distribution, deep capital bases, and strong claims reputations to maintain leadership. AIA grew Value of New Business 15% and retained its title as best employee-benefits provider for the 19th straight year [3]AIA Group Ltd., “2024 Full-Year Results,” aia.com.

Strategically, incumbents invest heavily in straight-through processing, tele-medical underwriting, and predictive claims analytics to defend their share against lean digital challengers. Insurtechs differentiate through usage-based pricing, instant issuance, and embedded-finance partnerships, particularly in travel and gadget covers. The MAS supervisory sandbox fosters innovation while maintaining customer safeguards, enabling newcomers to pilot novel models before full licence roll-out.

Capacity for specialised risks such as cyber and renewable-energy projects has attracted international reinsurers that provide underwriting expertise and balance-sheet strength. United Overseas Insurance maintained its AM Best A+ rating in 2024, reinforcing market confidence. Ongoing consolidation illustrated by the proposed Income-Allianz transaction viewed as competition-neutral by MAS could further reshape the competitive set yet is unlikely to dislodge the front-runner cohort over the forecast horizon. Consequently, the Singapore life and non-life insurance market exhibits moderate concentration with vigorous rivalry in digital distribution and specialty lines.

Singapore Life and Non-Life Insurance Industry Leaders

AIA Singapore Pte Ltd

Great Eastern Life

Prudential Assurance Company Singapore

NTUC Income Insurance Co-operative

Manulife (Singapore)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Great Eastern has expanded its strategic focus on the high-net-worth (HNW) segment by introducing Great Eastern Private, a service designed to address the financial needs of affluent individuals and their families across Asia.

- March 2026: Etiqa Insurance Singapore and AIA Singapore have established a strategic distribution agreement to enhance the availability of Shariah-compliant Takaful products within the Singaporean market.

- June 2025: Ant International signaled intent to secure stable coin-issuer licenses in Singapore and Hong Kong, paving the way for new premium-collection and claims-payment options that integrate digital assets

- May 2025: The Ministry of Health accepted MediShield Life Council recommendations to raise benefits and fund USD 1.33 billion of premium increases with USD 3.03 billion in subsidies, reshaping the health-insurance landscape.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Singapore life and non-life insurance market as all written premiums collected by licensed insurers for individual and commercial risk coverage, including group life, general accident, motor, property, marine, liability, health, and investment-linked products that are booked in Singapore and regulated by the Monetary Authority of Singapore (MAS).

Scope exclusion: reinsurance inflows, offshore captives, takaful products written outside Singapore, and self-funded employer benefit schemes lie outside the modeled boundary.

Segmentation Overview

- By Type

- Life Insurance

- Term Life

- Whole Life / Endowment

- Unit-Linked / Investment-Linked

- Annuities / Pension

- Group Life

- Non-Life Insurance

- Motor Insurance

- Health / Medical Insurance

- Property Insurance

- Marine, Aviation & Transit Insurance

- Liability Insurance

- Travel Insurance

- Personal Accident

- Life Insurance

- By Distribution Channel

- Captive / Exclusive Agents

- Independent Agents

- Bancassurance

- Brokers

- Direct Online / Insurtech Platforms

- Other Direct (Telephone & Mail)

- By End User

- Individuals

- SMEs

- Large Corporates

- By Premium Type

- New Business Premium

- Renewal Premium

- By Region (Singapore)

- Central Region

- East Region

- North Region

- North-East Region

- West Region

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview underwriting heads, bancassurance managers, insurtech founders, and brokers across Singapore's five planning regions. Guided conversations test secondary assumptions on average selling price shifts, digital uptake, lapse behavior, and new-business sentiment. Follow-up surveys with actuaries and compliance officers help us stress-check regulatory cost impacts before assumptions are frozen.

Desk Research

We begin by mining authoritative public sources such as MAS quarterly premium filings, Life Insurance Association performance bulletins, General Insurance Association factbooks, SingStat macro indicators, and ASEANstats trade tables. Company filings, prospectuses, and investor decks add product mix and pricing clues, while global multilaterals like the World Bank give baseline demographic and income trajectories. To deepen competitive intelligence, our analysts tap D&B Hoovers and Dow Jones Factiva for insurer financials and deal news. This mosaic supplies hard numbers that anchor our model and reveal early trend inflections.

A second pass verifies regulatory updates (for instance, Risk-Based Capital 2, CPF Life revisions) and captures policy levers that sway premium flows, followed by a literature sweep across peer-reviewed journals and reputable press for mortality, morbidity, and climate-risk signals. The sources listed are illustrative, and many additional references were consulted for validation and clarification purposes.

Market-Sizing & Forecasting

We adopt a top-down framework that reconstructs market value from MAS production data and trade-adjusted GWP, which is then sense-checked through selective bottom-up roll-ups of sampled ASP-times-policy counts from large agents and digital channels. Key model drivers include weighted new business premiums, renewal ratios, motor vehicle Certificates of Entitlement issuances, MediShield Life enrollment, household disposable income, and property transaction volumes. Missing micro inputs are bridged using calibrated penetration factors anchored to historical elasticity tests. Forecasts are produced through multivariate regression blended with scenario analysis, letting us adjust for GDP shocks and regulatory swings flagged during primary interviews.

Data Validation & Update Cycle

Outputs pass a three-layer internal review, starting with variance checks against LIA and GIA benchmarks, followed by senior analyst reconciliation of outliers, and concluding with editorial sign-off. We refresh every twelve months, and we trigger interim updates when MAS issues material guideline changes or large merger deals close; a final recency sweep is done before each client delivery.

Why Mordor's Singapore Life and Non-Life Insurance Baseline Commands Reliability

Published estimates often diverge because researchers choose different premium classes, convert currencies at varied dates, and refresh their files on separate schedules.

Key gap drivers include whether offshore reinsurance and investment-linked assets are folded into totals, the cut-off between in-force and new business, and how conversion from SGD to USD is timed when exchange rates swing. Mordor's scope mirrors MAS's resident insurer universe, applies a single mid-year SGD-USD rate, and is updated annually, giving users a clean, transparent anchor.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.23 B (2025) | Mordor Intelligence | - |

| USD 66.41 B (2024) | Global Consultancy A | Includes offshore reinsurance flows and uses gross global premiums |

| USD 5.87 B (2024) | Trade Association B | Counts only new-business weighted premiums, omits renewal pool |

| USD 17 B (2024) | Regional Consultancy C | Blends life and general lines but excludes group health riders |

These comparisons show that when differing scopes and timing are stripped away, Mordor's disciplined variable selection and consistent refresh cadence deliver a balanced, reproducible baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the current size of the Singapore life and non-life insurance market?

The market is valued at USD 6.88 billion in 2026 and is forecast to reach USD 11.3 billion by 2031.

Which segment is growing the fastest?

Life insurance products are projected to post an 11.54% CAGR through 2031, outpacing non-life lines.

How significant is digital distribution in Singapore insurance?

Direct online and insurtech channels are expanding at a 16.98% CAGR, steadily eroding the market share of traditional agents.

Why is motor insurance in Singapore relatively resilient?

The Certificate of Entitlement system caps vehicle numbers, stabilizing the premium pool despite changes in mobility preferences.

Page last updated on: