Cotton Seed Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.65 Billion |

| Market Size (2031) | USD 2.19 Billion |

| Growth Rate (2026 - 2031) | 5.80% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia-Pacific |

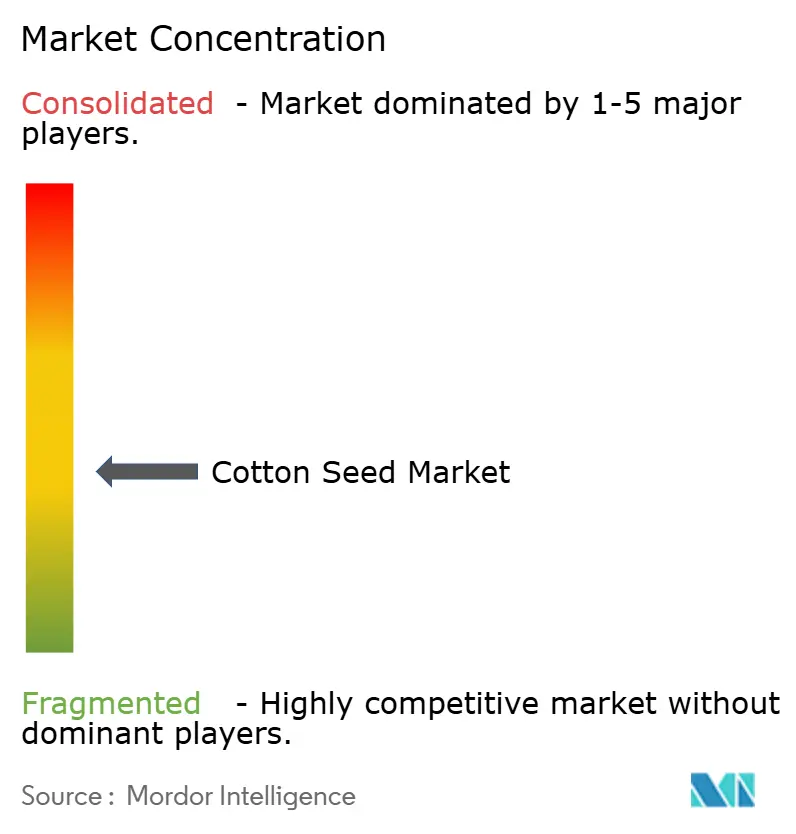

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cotton Seed Market Analysis by Mordor Intelligence

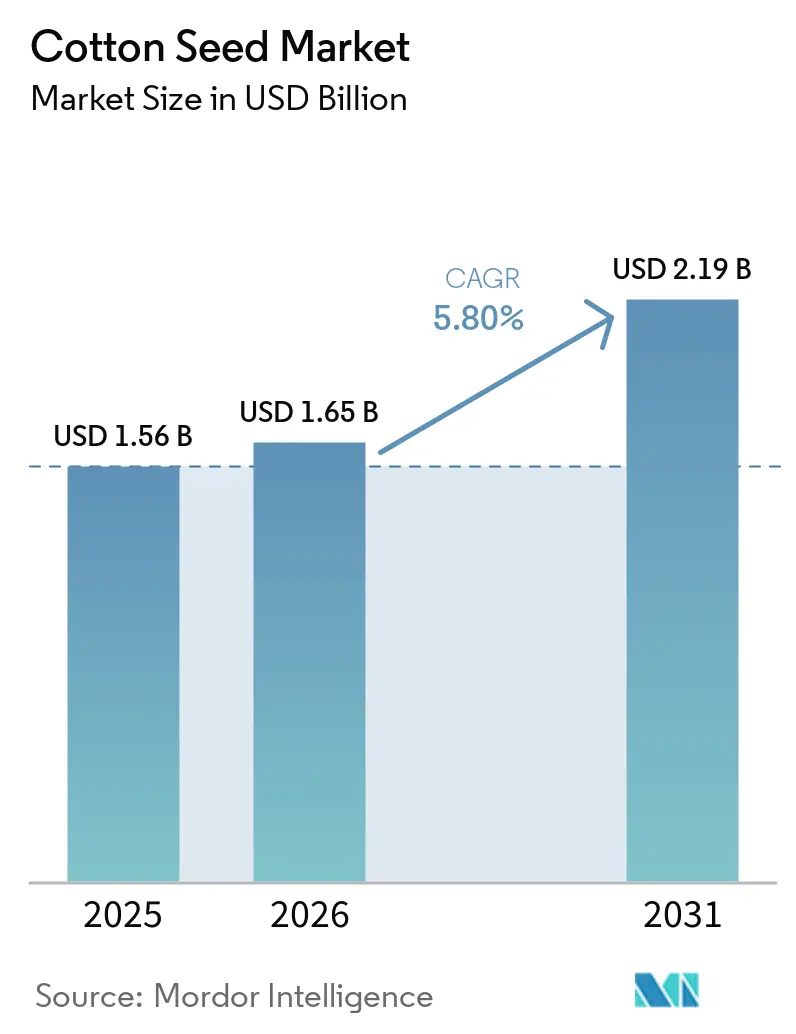

The Cotton Seed Market size is projected to expand from USD 1.56 billion in 2025 and USD 1.65 billion in 2026 to USD 2.19 billion by 2031, registering a CAGR of 5.80% between 2026 and 2031. The main support for the cottonseed market is the shift from farm-saved seed to certified hybrid seed across Asia-Pacific, which increases commercial seed purchases without requiring a matching increase in cotton acreage. Seed replacement in branded hybrids is also rising in South Asia and Sub-Saharan Africa, expanding the addressable base of the cotton seed market in regions where historical replacement rates were low. Policy support is strengthening the demand backdrop, especially in India, where the Mission for Cotton Productivity and the Sub-Mission on Seed and Planting Material support certified seed distribution, quality testing, and higher-yield planting systems. The cotton seed market still faces real pressure from pink bollworm resistance, softer cotton prices, crop switching risk, and rising scrutiny of seed treatment chemistry in major producing regions. As a result, competitive gains in the cotton seed market depend less on simple volume expansion and more on trait innovation, local agronomic fit, regulatory timing, and distribution strength.

Key Report Takeaways

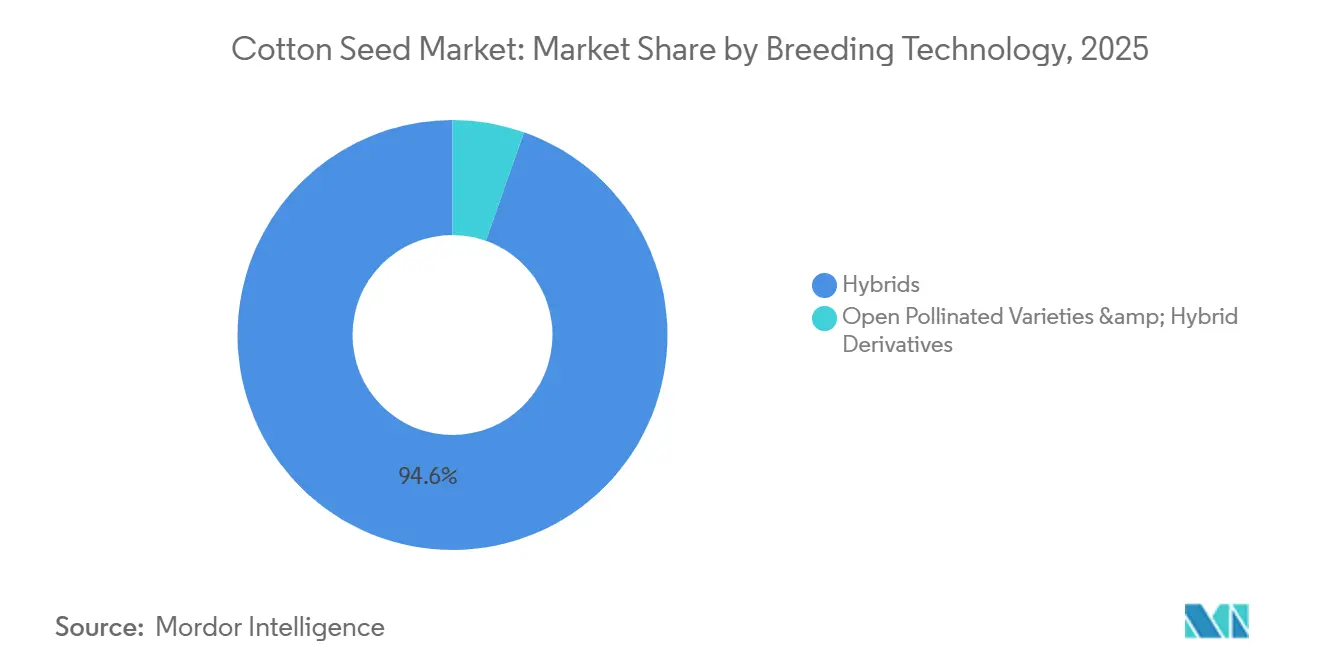

- By breeding technology, hybrids were the largest segment, with 94.6% of the cotton seed market share in 2025, and they are also the fastest-growing segment, with a projected CAGR of 5.9% between 2026 and 2031.

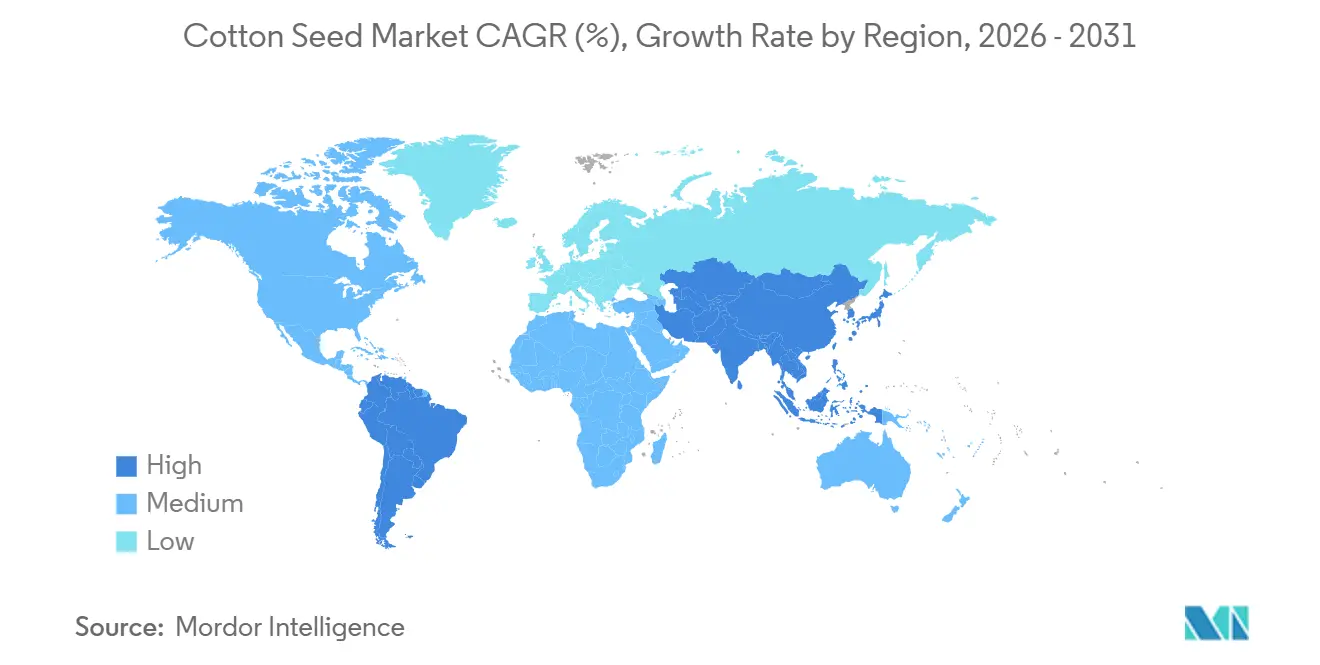

- By geography, Asia-Pacific was the largest region, accounting for 74.4% of the cottonseed market in 2025, while South America will be the fastest-growing region, with a 6.8% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cotton Seed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hybrid and transgenic seed adoption | +2.0% | Global, concentrated in Asia-Pacific and South America | Medium term (2-4 years) |

| Seed subsidy and cotton mission support in India | +1.0% | Asia-Pacific, India primary, with spillover to South Asia | Medium term (2-4 years) |

| Higher seed replacement rates in branded hybrids | +0.8% | Global, with early gains in India, Pakistan, and Sub-Saharan Africa | Medium term (2-4 years) |

| Textile demand supporting cotton acreage | +0.6% | Global, leading in Bangladesh, Vietnam, Turkey, and India | Medium term (2-4 years) |

| High-density planting increasing seed use per acre | +0.5% | Asia-Pacific core, with spillover to the Middle East and Africa | Medium term (2-4 years) |

| Low-gossypol cottonseed commercialization | +0.3% | North America initially, expanding to Central Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hybrid and Transgenic Seed Adoption

The strongest support for the cotton seed market comes from a change in seed mix rather than a broad increase in cultivated area. Purchased hybrid and transgenic seed has become central to commercial cotton production in major producing countries, keeping the cotton seed market tied to annual repurchase cycles rather than farm-saved seed reuse. That annual repurchase pattern helps seed companies protect both volume and pricing in the cotton seed market, where traited and branded products hold a clear agronomic position. The next stage of competition is moving toward new stacked events, including Vip3A-based traits and gene-edited lines, because older Bt platforms are under pressure from resistance in key markets. BASF SE’s January 2026 launch of new Stoneville varieties with Axant Flex herbicide tolerance and TwinLink Plus insect control shows how rapidly trait stacking is now shaping product refresh cycles[1]Source: BASF SE, “BASF Introduces New Stoneville Cotton Seed Varieties for the 2026 Season,” basf.com.

Seed Subsidy and Cotton Mission Support in India

India has become a major policy anchor for the cotton seed market through direct support for seed quality and productivity programs. The Mission for Cotton Productivity carries an outlay of INR 5,659.22 crore, equivalent to USD 669.73 million, for 2026-27 to 2030-31, and aims to lift lint productivity from 440 kg per hectare to 755 kg per hectare[2]Source: Prime Minister of India, “Cabinet Approves ‘Mission for Cotton Productivity’ With Rs.5659.22 Crore Outlay,” pmindia.gov.in. The program covers high-yielding seeds, pest and disease resistance, extra-long staple cotton, and high-density planting systems across 140 districts in 14 states.The Sub-Mission on Seed and Planting Material offers state-level support for certified seed distribution, processing infrastructure, and quality testing. This initiative enhances the operational framework of the cotton seed market in India. It is anticipated to boost branded hybrid volumes, although suppliers unable to demonstrate clear yield or quality differentiation may face pricing pressures.

Higher Seed Replacement Rates in Branded Hybrids

Higher seed replacement rates are driving increased demand through formal channels in the cotton seed market, particularly in regions where farmers previously relied on saved seeds. The seed replacement rate represents the proportion of seeds purchased from certified sources. In India, the support system includes financial assistance of INR 100 (USD 1.05) per quintal of treated seed to enhance access and distribution. Branded hybrid cotton seeds lose their original heterosis when replanted, necessitating fresh purchases for each crop cycle. This biological characteristic provides the cotton seed market with a repeat-purchase advantage not commonly seen in other crop categories. Additionally, improved agrodealer coverage in Telangana, Maharashtra, and Gujarat is encouraging a shift from informal to formal branded channels, despite acreage pressures in key states. These factors collectively indicate a positive growth trajectory for the formal cotton seed market.

Textile Demand Supporting Cotton Acreage

Textile demand still matters to the cotton seed market, but the link runs through fiber prices and acreage incentives rather than direct seed buying in garment-focused countries. As per United States Department of Agriculture (USDA), Global cotton mill use is forecast at 121.7 million bales in 2026-27, which is the highest level in 5 years, supported by restocking in Bangladesh, Vietnam, and India[3]Source: USDA Economic Research Service, “Cotton and Wool Outlook, April 2026,” ers.usda.gov. That recovery helps keep acreage stable in producing countries and supports procurement activity across the cotton seed market. Bangladesh and Vietnam are not major cotton producers, so their stronger mill demand can support global cotton prices and influence planting decisions in India, Pakistan, and Egypt.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pink bollworm resistance reducing Bt trait value | -1.5% | Asia-Pacific, India and Pakistan primary, with spillover to South Africa | Medium term (2-4 years) |

| Cotton price volatility and crop switching | -0.8% | Global, concentrated in India, the United States, and Turkey | Short term (≤ 2 years) |

| Illegal herbicide-tolerant seed channels in India | -0.7% | South Asia, India national, with early gains in Maharashtra and Gujarat | Medium term (2-4 years) |

| Neonicotinoid seed treatment scrutiny | -0.4% | North America and Europe, extending to the United Kingdom and parts of South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Pink Bollworm Resistance Reducing Bt Trait Value

Pink bollworm resistance represents a significant biological challenge for the cottonseed market in India. Research published in the Journal of Cotton Research in 2026 reported high resistance ratios to Cry1Ac and Cry2Ab in field populations, with extreme resistance observed in the Nagpur strain. In the same year, India’s Minister of State for Agriculture confirmed in Parliament that pink bollworm resistance is prevalent across cotton-growing regions and is becoming a major pest issue. This development has reduced the premium that farmers are willing to pay for older Bt hybrids, as field protection no longer meets expectations. The cottonseed market requires a new trait cycle to regain pricing power, however, the current pipeline remains in pre-commercial stages. As the yield advantage of older Bt platforms diminishes, farmers are less inclined to pay for branded hybrid seeds. This situation creates opportunities for Vip3A-based and stacked-gene products, though their commercial availability is contingent on uncertain regulatory approvals in India and China.

Cotton Price Volatility and Crop Switching

Price volatility creates a direct planning problem for the cottonseed market because seed production decisions are made before planting intentions are fully clear. As per the Foreign Agricultural Service of the United States Department of Agriculture (FAS USDA), in the United States, upland cotton farm prices fell to 60 cents per pound in 2025-26 from 63.2 cents per pound in 2024-25. In India, seed cotton prices in 2025-26 were reported below the revised minimum support price of INR 8,060 per 100 kg, equivalent to USD 96.5 per 100 kg. Softer returns increase the risk of acreage switching to soybeans, corn, and other competing crops, which directly reduces seed demand while leaving seed suppliers with sunk inventory costs. That makes the cottonseed market more exposed to planting cycles than downstream fiber traders and processors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Breeding Technology: Hybrids Lock In Recurring Seed Demand Across All Geographies

Market share data show that hybrids were the largest breeding technology segment, accounting for 94.6% in 2025, and this segment of the cotton seed market is also the fastest, with a 5.9% CAGR through 2031. That position is self-reinforcing because growers must buy fresh hybrid seed each season to avoid yield loss from saved progeny. Bayer AG advanced fresh Deltapine varieties with Bollgard 3 ThryvOn XtendFlex stacks for the year 2023-2024. India also released 22 new Bt cotton variety notifications in January 2026, which support another round of varietal replacement in the cotton seed industry.

Market growth for non-hybrid breeding technologies will remain modest because open-pollinated varieties are most relevant in regions with less developed commercial distribution and seed storage systems. This residual category still serves parts of Sub-Saharan Africa and some Central Asian markets, but it is losing relevance in the more organized cottonseed market. The performance gap has widened as private companies invest in multi-trait hybrids, while public programs still carry much of the burden for alternative germplasm. Compact-architecture materials suited for high-density planting sit near the boundary between conventional breeding and hybrid development, and that space could gain importance later in the forecast period. For now, the cotton seed industry is moving toward deeper hybrid concentration, while open-pollinated options remain a secondary part of the cotton seed market size.

Geography Analysis

Asia-Pacific held 74.4% of the global total in 2025, but the structure of the cotton seed market differs sharply across the region. China concentrates nearly 90% of its cotton production in Xinjiang, where mechanized harvesting and locally adapted seed programs support a more structured procurement model. China’s 2025-26 harvested area is forecast at nearly 3.1 million hectares, with yields of 2,556 kg per hectare, reflecting intensive agronomic management rather than a smallholder replacement story. India’s cotton acreage fell, yet the cotton seed market remained resilient, as higher seed replacement and certified hybrid adoption offset the area loss. As per the United States Department of Agriculture (USDA), Pakistan maintained a harvested area of nearly 2 million hectares in 2025-26, which supported stable demand conditions, while Australia’s yield levels kept it a smaller but premium mechanized niche.

South America is the fastest-growing region in the cottonseed market, with a projected CAGR of 6.7% through 2031. Brazil stands out due to its large-scale farming operations, extensive use of high-trait seeds, and strong demand for agronomy-supported hybrids. Europe, while smaller in terms of cultivated area, remains significant for compliance-driven product positioning, as cotton production is concentrated in Greece and Spain, where regulatory standards are more stringent. The Middle East and Africa offer long-term growth opportunities for the cotton seed market, driven by Turkey's textile demand, Egypt's niche in extra-long staple cotton, and West Africa's potential for future expansion of hybrid seed supply. Although these regions do not currently rival Asia-Pacific in scale, they offer selective growth opportunities through specialized genetics and improved commercial infrastructure.

North America remains a commercially attractive market due to factors beyond acreage, including a structural shift in licensing and product competition. Corteva, Inc. is set to enter the cotton trait out-licensing market in the United States following its 2026 resolution with Bayer AG, introducing a third significant trait owner to a previously more concentrated market. Concurrently, BASF SE and Bayer AG are enhancing their premium portfolios, increasing the value mix within the regional cotton seed market. Additionally, prospective planting data for 2026 indicates an acreage recovery, providing the region with both volume and pricing support.

Competitive Landscape

The cotton seed market has a two-layer competitive structure, with moderate concentration in proprietary trait technology and far looser concentration in seed distribution and local germplasm. BASF SE, Bayer AG, and Corteva, Inc. hold the strongest positions in advanced trait platforms, including stacked insect control and multi-herbicide tolerance systems. Indian suppliers such as Kaveri Seed Company Limited, Nuziveedu Seeds Limited, Maharashtra Hybrid Seeds Company Private Limited, Rasi Seeds Private Limited, and JK Agri Genetics Limited compete more on local fit, dealer access, and pricing than on proprietary global traits. BASF’s Agricultural Solutions R&D spend reached EUR 919 million, equivalent to USD 992 million in 2024, underscoring how capital-intensive the technology layer of the cotton seed market has become. Regulatory delays in India continue to protect incumbent trait platforms, even as the downstream branded seed layer remains fragmented.

Illegal herbicide-tolerant Bt seed has become one of the biggest commercial distortions in the cotton seed market, diverting large acreages away from formal branded channels. USDA estimated that this unapproved segment covered 15% to 25% of India’s cotton acreage, meaning legitimate players are competing with an informal system that still meets a major farmer's need for weed control costs. Kaveri Seed Company Limited reported a 15% decline in cotton hybrid volumes in Q1 FY26, and the company later linked illegal seed usage to a 12.9% revenue contraction in its cotton segment during H1 FY26. Kaveri has responded by reducing dependence on cotton, cutting breeding cycles by more than 50% through speed breeding, and using KaveriQC for real-time seed quality monitoring. It also built a wide domestic channel with 3,222 direct distributors and 68,500 retailers across 23 states, underscoring that local reach still matters in a fragmented cotton seed market.

Recent strategic moves indicate that competition in the cotton seed market centers on trait refresh, yield defense, and supply-chain control. BASF introduced 3 new Stoneville varieties for the 2026 U.S. season, while Corteva launched PHY 859 RF in February 2026 and had already introduced 2 new upland varieties for the same season in July 2025. In June 2025, Archer Daniels Midland Company also formed cotton seed processing ventures with Planters Cotton Oil Mill and PYCO Industries, which tied upstream handling more closely to downstream processing infrastructure. The distribution layer remains fragmented, so the biggest practical barrier to new entrants in the cotton seed market is still channel creation rather than basic germplasm access.

Cotton Seed Industry Leaders

BASF SE

Bayer AG

Corteva, Inc.

Syngenta AG

Kaveri Seed Company Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: India's Union Cabinet approved the "Mission for Cotton Productivity" with an outlay of Rs. 5,659.22 crore (USD 669.73 million) for 2026–27 to 2030–31, targeting lint productivity enhancement from 440 kg per hectare to 755 kg per hectare across 140 districts and approximately 32 lakh farmers. This represents the largest coordinated government commitment to cotton seed technology upgrade in India's history.

- February 2026: Corteva, Inc. (PhytoGen brand) launched PHY 859 RF, a new Pima cotton variety with industry-leading yield potential and increased tolerance to Fusarium Race 4 (FOV4), averaging 1,403 pounds per acre in trials.

- January 2026: BASF SE introduced three new Stoneville cotton seed varieties for the 2026 U.S. season, ST 4130AXTP, ST 4650AXTP, and ST 5260AXTP, all featuring Axant Flex quad-stacked herbicide tolerance technology and TwinLink Plus three-gene insect control, tailored for Eastern Cotton Belt and Mid-South growing conditions.

Global Cotton Seed Market Report Scope

Cotton is a crop primarily used in the textile industry. It is a perennial crop that is harvested in moderate rainfall and during a frost-free period with plenty of sunshine. It is somewhat salt- and drought-tolerant, making it an attractive crop for arid and semi-arid regions. However, the major problems with the cotton crop are pest control, extensive farming, and labor requirements.

The cottonseed market report is segmented by breeding technology (Hybrids, Open-pollinated Varieties, and Hybrid Derivatives) and by geography (North America, South America, Europe, Asia-Pacific, the Middle East, and Africa). The market forecasts are provided in terms of value (USD) and volume (metric tons).

| Hybrids |

| Open Pollinated Varieties and Hybrid Derivatives |

| North America | United States |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Greece |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Pakistan | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Turkey |

| Israel | |

| Rest of Middle East | |

| Africa | Egypt |

| Nigeria | |

| South Africa | |

| Rest of Africa |

| Breeding Technology | Hybrids | |

| Open Pollinated Varieties and Hybrid Derivatives | ||

| By Geography | North America | United States |

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Greece | |

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Pakistan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Turkey | |

| Israel | ||

| Rest of Middle East | ||

| Africa | Egypt | |

| Nigeria | ||

| South Africa | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current outlook for the cotton seed market?

The cotton seed market stands at USD 1.65 billion in 2026 and is projected to reach USD 2.19 billion by 2031 at a 5.8% CAGR. Demand is being supported more by certified seed adoption than by broad acreage growth.

Why is certified hybrid adoption important for cotton seed demand?

Certified hybrid and traited seed drives annual repurchase behavior because hybrid performance does not hold when seed is replanted. That keeps formal channel demand stronger than in crops where farm-saved seed remains practical.

Which region leads global cotton seed sales?

Asia-Pacific led with 74.4% of global demand in 2025, supported by the scale of cotton production in India, China, and Pakistan and the shift toward certified hybrids.

What are the main risks for cotton seed suppliers?

Pink bollworm resistance, cotton price volatility, illegal herbicide-tolerant seed channels in India, and tighter seed treatment regulation are the main risks. These issues can reduce willingness to pay for premium seed or push acreage away from cotton.

Which companies are shaping competition in cotton seed?

BASF, Bayer, and Corteva are important at the trait level, while Kaveri, Nuziveedu, MAHYCO, Rasi, and JK Agri Genetics are important in local germplasm and distribution. Recent launches by BASF and Corteva show that product refresh remains a major competitive tool.

Page last updated on: