LED Driver Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 24.71 Billion |

| Market Size (2031) | USD 67.84 Billion |

| Growth Rate (2026 - 2031) | 22.38% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

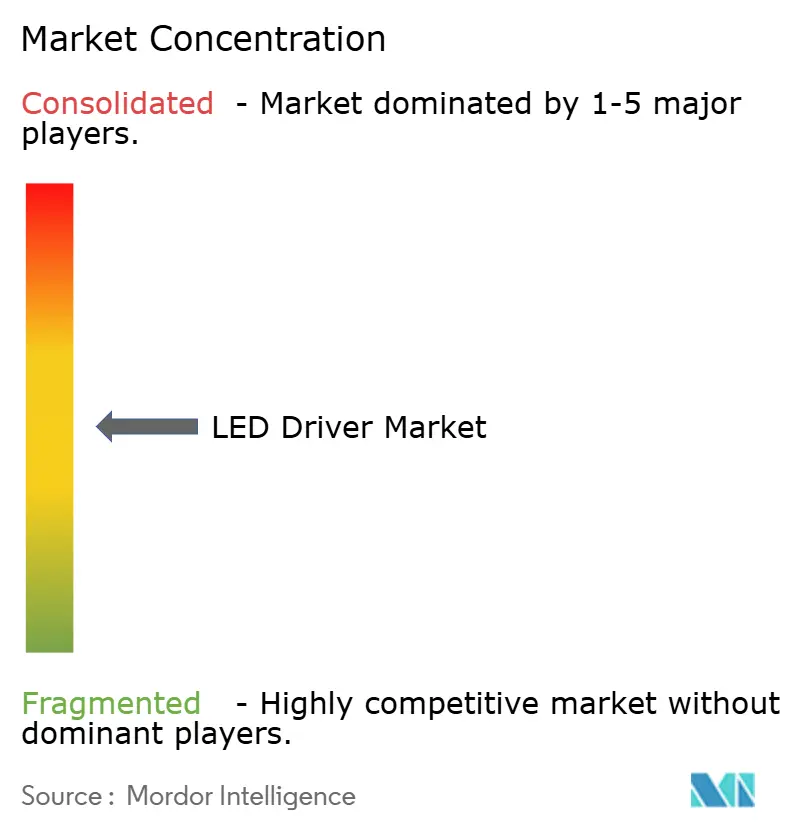

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

LED Driver Market Analysis by Mordor Intelligence

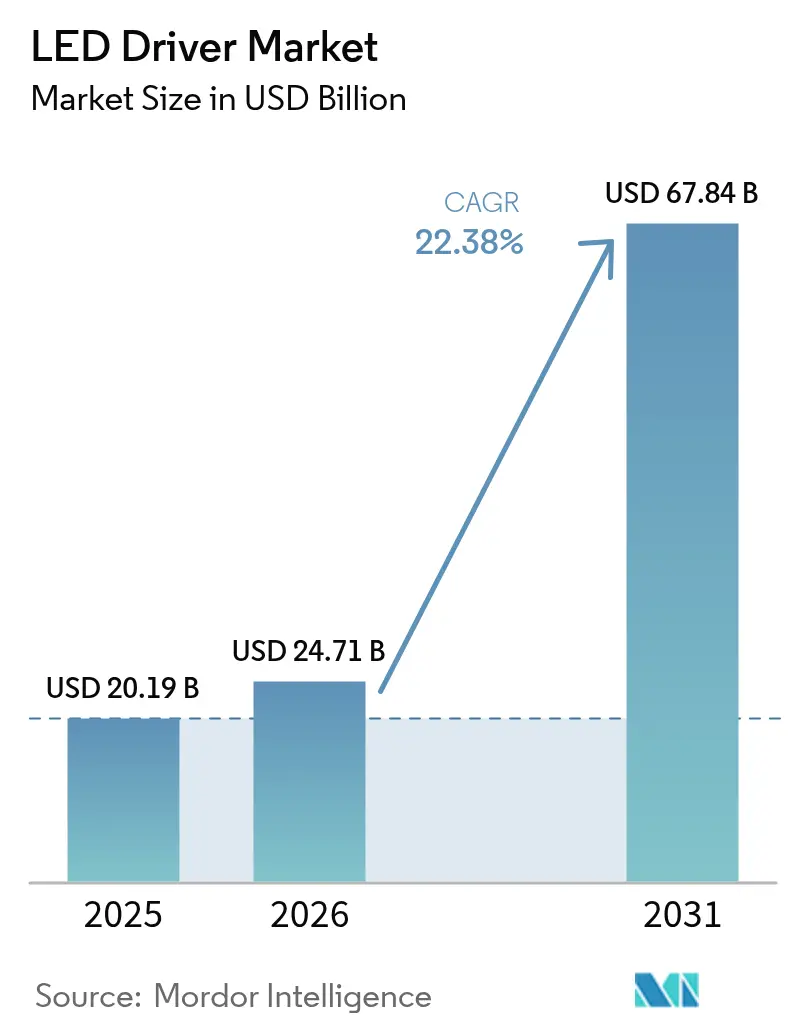

LED driver market size in 2026 is estimated at USD 24.71 billion, growing from 2025 value of USD 20.19 billion with 2031 projections showing USD 67.84 billion, growing at 22.38% CAGR over 2026-2031. This expansion is underpinned by the alignment of national energy-efficiency mandates, accelerating wireless-control adoption and the deployment of silicon-carbide and gallium-nitride semiconductors that raise conversion efficiency and shrink driver footprints. Government-funded retrofit programs, particularly in Asia-Pacific, intersect with net-zero commitments to lift large-scale replacement demand, while new-build codes in North America and Europe push integrated intelligent-lighting specifications. Automotive electrification further widens the addressable base for compact, high-temperature drivers, and Matter/Thread standardization dismantles long-standing interoperability barriers. Collectively, these shifts elevate the LED driver market from a component-supply business to a strategic enabler of connected-building platforms and energy-management services.

Key Report Takeaways

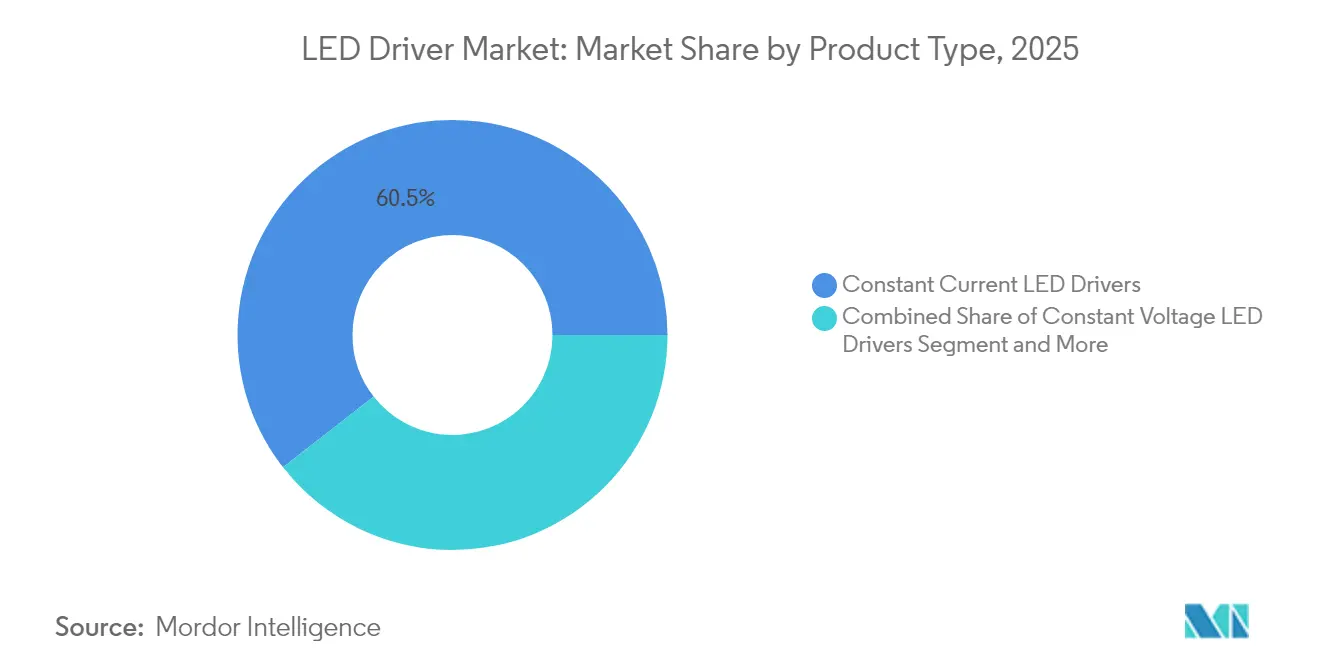

- By product type, constant current devices commanded 60.55% of LED driver market share in 2025; constant power drivers post the fastest 22.96% CAGR through 2031.

- By control feature, wired systems held 64.82% share of the LED driver market in 2025, while wireless protocols expand at a 23.62% CAGR to 2031.

- By power output, the 25-65 W range accounted for 31.74% of the LED driver market size in 2025; sub-25 W units grow at 23.15% CAGR on the back of IoT lighting nodes.

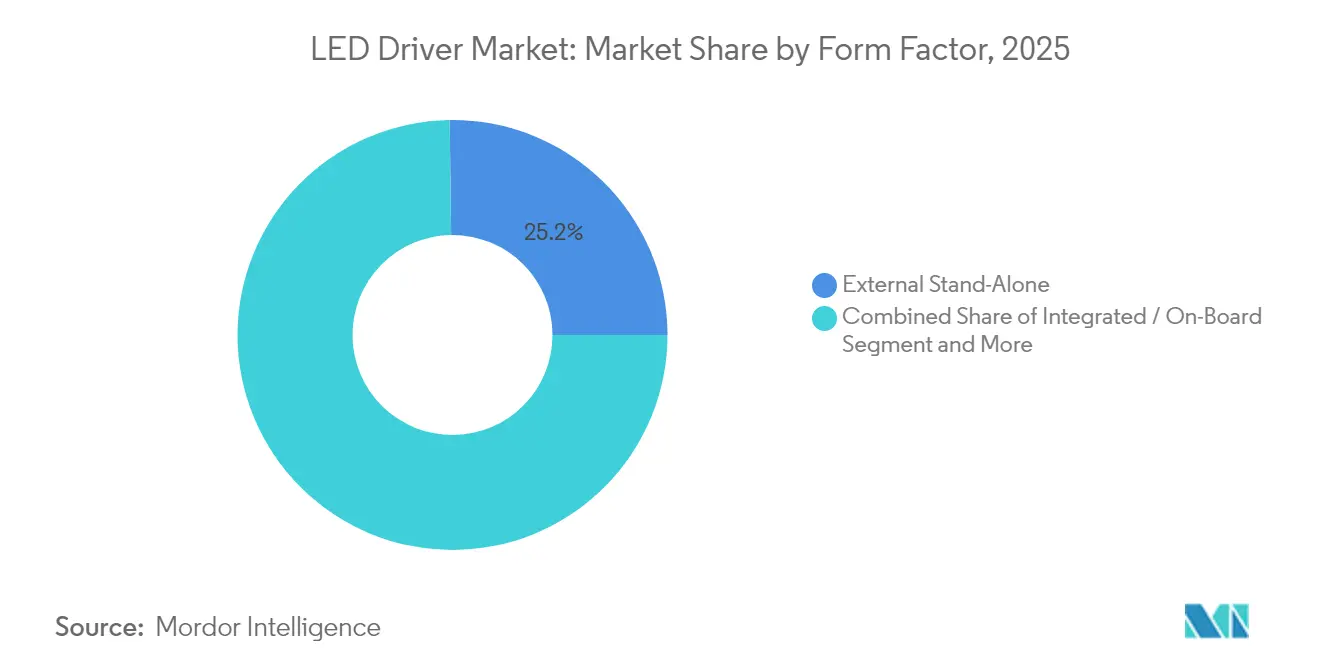

- By form factor, external stand-alone models represented 25.21% share in 2025, whereas compact/module drivers record a 22.85% CAGR through 2031.

- By end-use application, commercial and office lighting delivered 44.68% revenue in 2025; retail and hospitality luminaires accelerate at 24.18% CAGR to 2031.

- By geography, North America generated 31.96% LED driver market revenue in 2025; Asia-Pacific leads growth with a 23.51% CAGR forecast to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global LED Driver Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Subsidy-fuelled LED retrofit programs (post-2025 roll-outs) | +4.2% | Global, with concentration in Asia-Pacific and Europe | Medium term (2-4 years) |

| Rapid price declines in GaN-on-Si driver ICs | +3.8% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Smart-lighting mandates in new-build codes | +3.1% | North America and EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Mainstream adoption of Matter/Thread wireless controls | +2.9% | Global, early adoption in North America | Medium term (2-4 years) |

| Surge in EV headlamp LED driver demand | +2.7% | Asia-Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| Corporate net-zero targets accelerating industrial upgrades | +2.4% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Subsidy-fuelled LED Retrofit Programs Drive Market Acceleration

India’s UJALA initiative illustrates how large-scale distribution of efficient lamps can slash electricity demand by 20 GW and avoid 80 million t of CO₂ annually.[1]U.S. Department of Energy, “ANSI/ASHRAE/IES Standard 90.1-2022,” energy.gov Unlike earlier discount schemes, the program’s market-based approach sustained vendor margins, encouraging continual product upgrades that now emphasize advanced drivers with energy-monitoring functions. Similar schemes in China, Malaysia and the European Union are moving from bulb replacements toward holistic luminaire swaps, triggering demand for drivers that support wireless controls, target power factors above 0.9 and meet IEC flicker criteria. Because early LED waves entered service around 2015, a secondary replacement cycle of 5.8 billion units begins peaking between 2025 and 2028. These programs collectively add momentum to the LED driver market by ensuring predictable, large-volume procurement pipelines over the forecast period.

Rapid Price Declines in GaN-on-Si Driver ICs Enable Mass Adoption

Texas Instruments’ migration from 6-inch to 8-inch GaN wafers cuts die cost while improving yield consistency, pushing power-conversion efficiency beyond 92% and shrinking thermal budgets.[2]LED Lights Data Team, “Impact Analysis of India’s UJALA Scheme,” ledlightsdata.comInfineon’s 300 mm pilot line is expected to reach silicon-parity pricing in 2025, opening mainstream channels such as retail track lighting and appliance illumination. GaN’s higher switching frequencies reduce magnetics size by up to 40%, enabling slimmer luminaire profiles and lowering enclosure temperatures, a critical factor for chip-on-board modules. Automotive headlamp systems benefit from GaN’s resilience at high junction temperatures, supporting adaptive-beam architectures in electric vehicles. These economics support a virtuous cycle of integration: as volumes climb, cost drops deepen, broadening the LED driver market even further.

Smart-Lighting Mandates in New-Build Codes Create Compliance-Driven Demand

ANSI/ASHRAE/IES 90.1-2022 mandates a 9.8% site-energy reduction over the prior edition, compelling developers to specify drivers capable of continuous dimming, occupancy awareness and daylight harvesting.[3]Texas Instruments, “GaN Technology Scaling,” ti.com California’s Title 24 raises the bar by tying performance credits to networked-lighting control capability. In Europe, Ecodesign Regulation 2019/2020 projects 96 TWh annual savings by 2030, obliging separate control gear and modular serviceability. These regulations shift procurement decisions from luminaire efficacy alone to system-level intelligence, favouring drivers with integrated radio modules and diagnostic telemetry. As more jurisdictions pivot to performance-based codes, the compliance incentive becomes a structural driver for the LED driver market.

Mainstream Adoption of Matter/Thread Wireless Controls Standardizes Connectivity

Tridonic’s Matter-certified drivers show how Thread mesh networking can coexist with DALI and Bluetooth in a single PCB footprint. Nordic Semiconductor’s nRF52840 SoC enables concurrent Thread and BLE, simplifying bridge-free upgrades in hybrid networks. MEAN WELL’s XLC-MA platform extends the concept to power classes from 25 W to 60 W, letting OEMs address residential, hospitality and light-commercial scenes with one SKU. Standardized commissioning trims installation labour, cuts interoperability troubleshooting and unlocks data-layer services that monetize lighting assets. Together, these advances accelerate the LED driver market transition toward software-defined luminaires.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent silicon supply constraints for driver ICs | -2.8% | Global, acute in automotive and industrial segments | Short term (≤ 2 years) |

| Limited interoperability across legacy wired protocols | -1.9% | Global, concentrated in retrofit markets | Medium term (2-4 years) |

| Design-in complexity for non-isolated drivers | -1.4% | Global, affecting compact form factor adoption | Long term (≥ 4 years) |

| High import tariffs on Chinese constant-current modules | -1.2% | North America and Europe primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Silicon Supply Constraints Create Bottlenecks in Driver IC Production

Wolfspeed’s liquidity pressures threaten silicon-carbide wafer availability for high-power lighting and EV applications. Foundries prioritize advanced 3-nm logic, leaving 16-90 nm capacity thin for the mixed-signal processes used in LED drivers. Lead times exceed 40 weeks for common MOSFETs; speciality PMICs stretch beyond a year, forcing design pivots and multi-sourcing strategies. The constraint drives price volatility that squeezes mid-tier OEM margins, dampening near-term shipment potential in segments such as outdoor lighting projects with firm bid ceilings. Until capacity additions in Southeast Asia come online, silicon shortfalls remain a measurable drag on the LED driver market.

Limited Interoperability Across Legacy Wired Protocols Fragments Market Adoption

Commercial facilities often retain DALI, DMX or 0-10 V wiring to avoid tenant disruption, compelling driver makers to maintain protocol-specific SKUs. This fragmentation elevates inventory costs and complicates installer training. Unlike wireless ecosystems rapidly converging on Matter, the wired domain lacks an agreed convergence roadmap. Small manufacturers therefore shoulder disproportionate firmware-validation burdens, delaying product cycles. In high-security sites where wireless is prohibited, the absence of cross-protocol translation hardware will continue to curb the LED driver market’s retrofit velocity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Constant Power Drivers Gain Traction

Constant current devices held 60.55% LED driver market share in 2025, driven by decades of design familiarity in high-lumen applications. However, constant power drivers deliver up to 92% conversion efficiency and accommodate variable-voltage LED loads without redesign, supporting a projected 22.96% CAGR between 2026 and 2031. In the automotive front-lighting niche, Infineon’s Litix Power Flex series illustrates the performance jump: SPI-controlled dimming and multi-string protection broaden functionality without thermal penalty.

The rise of adaptive lighting scenarios reinforces the shift. Architectural façades, sports arenas and tunable-white office fixtures benefit when output can adjust dynamically while current remains within diode tolerances. This versatility lowers SKU proliferation for luminaire makers and enhances field-upgrade paths. As wireless protocols proliferate, firmware-selectable power curves make constant power designs the preferred platform in the evolving LED driver market.

By Control Feature: Wireless Protocols Accelerate Market Transformation

Wired systems, led by DALI and 0-10 V, accounted for 64.82% of the LED driver market size in 2025 because existing-bearing structures embed control cabling. Yet wireless features head into the steep part of the adoption curve, with a 23.62% CAGR through 2031. Legrand’s Matter-approved wall-box dimmers demonstrate consumer enthusiasm for app-based commissioning.

From a total-cost lens, eliminating control wires trims labour 15–25% in commercial retrofit budgets, often swinging ROI in favour of LED plus controls. Thread’s IPv6 foundation eases building-management integration, and BLE mesh provides low-energy fallback for emergency lighting checks. With over-the-air firmware updates now mainstream, wireless drivers extend operating lifetimes by accommodating future features. These advantages cement wireless as a pillar of the LED driver market.

By Power Output: Compact Applications Drive Sub-25 W Growth

The 25-65 W bracket maintained the biggest revenue slice at 31.74% in 2025, covering downlights and linear troffers in offices, schools and supermarkets. Nonetheless, the sub-25 W class grows fastest at 23.15% CAGR thanks to smart bulbs, track spots and decorative fixtures packing sensors, radios and edge processors. Compact drivers integrate step-down regulators for MCUs and maintain flicker-free dimming at deep modulation ratios, critical for HDTV-equipped retail venues.

As hospitality operators pursue human-centric lighting, multi-channel sub-25 W drivers support correlated-color-temperature tuning without bulky external gear. MEAN WELL’s latest constant-power micro-drivers illustrate the density race: power, Thread radio and NFC commissioning occupy a board smaller than a visiting card. These capabilities ensure the growth path for the lower-wattage segment within the LED driver market.

By Form Factor: Module Integration Transforms Driver Architecture

External stand-alone units still made up 25.21% of 2025 shipments, favored for serviceable streetlights and high-bay luminaires where thermal isolation is paramount. Yet module drivers, shipped as ready-to-embed cassettes, show a 22.85% CAGR outlook. Inventronics’ purchase of OSRAM Digital Systems extends its LED driver industry footprint into fully sealed IP67 modules with native D4i intelligence.

The module trend dovetails with OEM cost-downs: fewer connectors mean faster line throughput and lower field-failure rates. Automotive suppliers likewise migrate toward PCB-embedded drivers to reclaim engine-bay space. As global plastics regulations tighten, integrated metal-core boards also aid recyclability. This convergence positions module solutions as a central growth axis in the LED driver market.

By End-Use Application: Retail Transformation Drives Adoption

Commercial and office estates generated 44.68% of 2025 revenue, buoyed by tenant fit-out cycles and ESG-linked financing. Yet retail and hospitality lighting captures the speed crown at 24.18% CAGR, leveraging dynamic color and targeted accent zones that boost dwell time. 7-Eleven’s retrofit across 4,760 U.S. stores saves USD 15.3 million yearly while improving shelf visibility and security.

Newer installations deploy multichannel drivers that orchestrate circadian-aligned spectra and per-aisle analytics services only feasible when drivers report telemetry via wireless backhaul. Hotels adopt similar logic, trimming operational expense and enabling guest-controlled ambience through branded mobile apps. These use-case expansions continue to diversify the LED driver market.

Geography Analysis

North America’s 31.96% revenue share in 2025 derives from rigorous lamp-efficacy rules that raise the bar to 83–195 lm/W, steering specifiers toward high-efficiency drivers. Corporate retrofits such as Coca-Cola Consolidated’s six-facility upgrade realize USD 97,063 annual savings and underline the quick payback narrative. The CHIPS Act allocates USD 200 billion for domestic fabs, improving resilience for analog and power components. Canada and Mexico leverage integrated supply chains to share technical standards and qualification labs, smoothing cross-border shipments.

Asia-Pacific exhibits the fastest structural rise, projecting a 23.51% CAGR through 2031. China’s manufacturing depth slashes BOM costs, and its municipal smart-city grants stimulate local demand for drivers with NB-IoT or LoRa gateways. India’s record-scale UJALA program replenishes lamp inventories at end-of-life, kick-starting a second-wave luminaire upgrade cycle. Japan, South Korea and Taiwan channel EV-led headlamp innovations into exportable adaptive-beam drivers. ASEAN markets absorb supply-chain diversification, with Vietnam emerging as a finish-and-assembly hub for North American brands.

Europe sustains momentum through Ecodesign 2019/2020, which targets 96 TWh savings annually by 2030. Germany’s KfW-bank subsidies tie preferential interest rates to intelligent-lighting deployment, accelerating driver replacements in logistics warehouses. Eastern European retrofit pipelines receive cohesion-fund backing, while the United Kingdom’s Building Regulations Part L references dynamic-lighting guidance that favours drivers capable of open-protocol communication. The Middle East and Africa supplement the global LED driver market with Vision 2030 programs, typified by Saudi Arabia’s 9.6% CAGR LED adoption outlook underpinned by local assembly ventures.

Competitive Landscape

The LED driver marketplace shows moderate concentration: the combined share of the top five suppliers hovers near 45%, reflecting a balance between global incumbents and specialized challengers. Signify capitalizes on Philips Lumileds vertical integration, marketing D4i-ready drivers bundled with Interact IoT services. ams OSRAM sustains premium positioning by pairing high-CRI emitters with OPTOTRONIC constant-power gear, while Acuity Brands extends Atrius cloud analytics across its digitally addressable drivers.

Strategic activity aligns to platform plays. Inventronics’ acquisition of OSRAM Digital Systems extends its footprint into Europe and deepens R&D for modular IP67 devices. Havells Lighting’s 2025 entry into the United States through a joint venture with Krut LED underscores the vertical-integration thesis—own the driver, the fixture and the service layer. Semiconductor specialists likewise eye the lighting channel: Navitas Semiconductor’s 650 V bi-directional GaNFast IC shrinks BOM counts, freeing board space for sensors and radios that differentiate smart luminaires.

Innovation focus migrates from raw efficiency to software extensibility. Patenting trends see an uptick in firmware-defined power curves and secure over-the-air update frameworks, indicating that competitive advantage now lies in lifecycle adaptability rather than static specifications. This evolution keeps pricing pressure moderate yet fosters service-based revenue that enlarges the overall LED driver market envelope.

LED Driver Industry Leaders

Acuity Brands Lighting

Signify

ams OSRAM

Eaton (Cooper Lighting)

Hubbell Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Havells Lighting LLC launched U.S. operations with Krut LED, creating an integrated fixtures-and-drivers platform.

- April 2025: Navitas Semiconductor unveiled production-ready 650 V bi-directional GaNFast ICs at PCIM 2025.

- March 2025: Wolfspeed received USD 192.1 million in IRS refunds under Section 48D, bolstering silicon-carbide expansion plans.

- January 2025: ams OSRAM and LEDVANCE renewed a decade-long global brand-licensing accord covering luminaires outside China.

- January 2025: Acuity Brands closed its USD 1.1 billion QSC acquisition, adding cloud-managed AV and control systems to its portfolio.

Global LED Driver Market Report Scope

An electrical circuit that powers a light-emitting diode is an LED circuit or LED driver in electronics. The course must restrict the current to avoid harming the LED while supplying enough current to illuminate the LED at the necessary brightness. The Global LED Driver Market is segmented by Product Type (Constant Current and AC LED, Constant Voltage), Control Feature (Wired, Wireless), Channel Count (Single, Dual, Three, and Above), End User (Residential, Office, Retail and Hospitality, Outdoor, Healthcare and Educational Institutions, Industrial), and by Geography. The report offers the market size in value terms in USD for all the abovementioned segments.

| Constant Current LED Drivers |

| Constant Voltage LED Drivers |

| Constant Power LED Drivers |

| Wired | 0-10 V |

| DALI | |

| DMX | |

| PLC | |

| Trailing-Edge | |

| Wireless | Wi-Fi |

| Bluetooth/BLE | |

| Zigbee | |

| Thread / Matter | |

| Li-Fi |

| Less than 25 W |

| 25 - 65 W |

| 65 -150 W |

| Greater than 150 W |

| External Stand-Alone |

| Integrated / On-Board |

| Linear Drivers |

| Compact / Module Drivers |

| Residential |

| Commercial and Office |

| Retail and Hospitality |

| Outdoor and Street Lighting |

| Industrial |

| Healthcare and Education |

| Automotive Lighting Systems |

| Horticulture and Agriculture |

| Consumer-Electronics Backlighting |

| Other Applications |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Product Type | Constant Current LED Drivers | ||

| Constant Voltage LED Drivers | |||

| Constant Power LED Drivers | |||

| By Control Feature | Wired | 0-10 V | |

| DALI | |||

| DMX | |||

| PLC | |||

| Trailing-Edge | |||

| Wireless | Wi-Fi | ||

| Bluetooth/BLE | |||

| Zigbee | |||

| Thread / Matter | |||

| Li-Fi | |||

| By Power Output | Less than 25 W | ||

| 25 - 65 W | |||

| 65 -150 W | |||

| Greater than 150 W | |||

| By Form Factor | External Stand-Alone | ||

| Integrated / On-Board | |||

| Linear Drivers | |||

| Compact / Module Drivers | |||

| By End-Use Application | Residential | ||

| Commercial and Office | |||

| Retail and Hospitality | |||

| Outdoor and Street Lighting | |||

| Industrial | |||

| Healthcare and Education | |||

| Automotive Lighting Systems | |||

| Horticulture and Agriculture | |||

| Consumer-Electronics Backlighting | |||

| Other Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Qatar | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current LED driver market size and projected growth?

The LED driver market size stands at USD 24.71 billion in 2026 and is expected to reach USD 67.84 billion by 2031, delivering a 22.38% CAGR over 2026-2031.

Which product type leads the LED driver market?

Constant current drivers lead with 60.55% market share in 2025, although constant power designs are the fastest-growing segment at 22.96% CAGR.

Why are wireless LED drivers gaining traction?

Thread- and Matter-based wireless drivers cut installation labour, offer seamless smart-home integration and post a 23.62% CAGR through 2031, outpacing wired alternatives.

Which region exhibits the highest growth rate?

Asia-Pacific shows the fastest expansion, forecast at 23.51% CAGR, fueled by infrastructure investments, policy incentives and expanding manufacturing capacity.

How are GaN devices influencing LED driver design?

Rapid cost declines in GaN-on-silicon driver ICs boost efficiency beyond 92%, reduce form factors by up to 40% and open new high-density applications such as EV headlamps.

Page last updated on: