Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Vision Positioning System Market Report Segments the Industry Into by Component (Cameras, Sensors, and Other Components), by Location (Indoor, and Outdoor), by Platform (Unmanned Aerial Vehicles, Automated Guided Vehicles, Industrial Robots, Other Platforms), by End-User (Retail, Industrial and Manufacturing, Defense and Security, Transportation and Logistics, Healthcare, and Other End-Users), and by Geography.

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

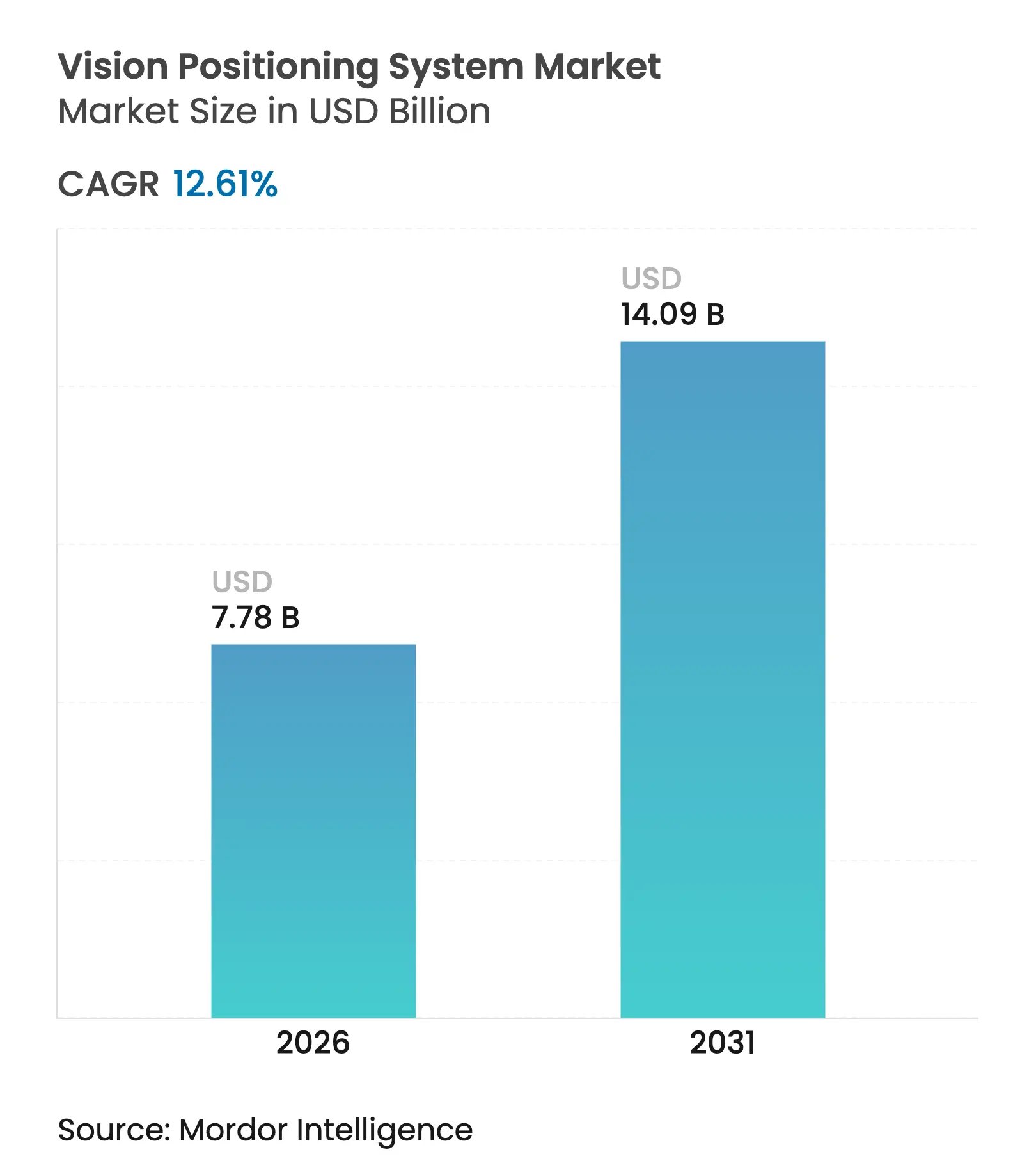

| Market Size (2026) | USD 7.78 Billion |

| Market Size (2031) | USD 14.09 Billion |

| Growth Rate (2026 - 2031) | 12.61 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The vision positioning system market size is expected to grow from USD 6.91 billion in 2025 to USD 7.78 billion in 2026 and is forecast to reach USD 14.09 billion by 2031 at 12.61% CAGR over 2026-2031. A surge in autonomous mobile robots, regulatory emphasis on machine safety, and rapid progress in edge artificial intelligence are reshaping technology roadmaps. Defense programs continue to demand ruggedized solutions, while e-commerce and healthcare providers scale indoor-navigation platforms for time-critical workflows. At the same time, falling LiDAR prices and software-defined simultaneous localization and mapping (SLAM) services are lowering entry barriers for mid-tier manufacturers. These forces collectively position the vision positioning system market for sustained double-digit growth through the end of the decade.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Surge in autonomous mobile robots in e-commerce fulfillment centers Surge in autonomous mobile robots in e-commerce fulfillment centers | +2.1% | Global, with concentration in North America and Europe | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+2.1% | Geographic Relevance:Global, with concentration in North America and Europe | Impact Timeline:Medium term (2-4 years) |

Rapid adoption of vision-guided drones for delivery and inspection Rapid adoption of vision-guided drones for delivery and inspection | +1.8% | Global, early adoption in North America and Asia-Pacific | Short term (≤ 2 years) | |||

Falling LiDAR and 3D-sensor ASPs enable mid-tier robotics OEMs Falling LiDAR and 3D-sensor ASPs enable mid-tier robotics OEMs | +1.5% | Asia-Pacific core, spill-over to global markets | Medium term (2-4 years) | |||

EU Machinery Regulation 2023/1230 mandates vision-based safety EU Machinery Regulation 2023/1230 mandates vision-based safety | +1.2% | Europe, with regulatory influence spreading globally | Long term (≥ 4 years) | |||

Edge-AI/on-sensor processing cuts latency and bandwidth Edge-AI/on-sensor processing cuts latency and bandwidth | +1.7% | Global, with early deployment in developed markets | Short term (≤ 2 years) | |||

SLAM-as-a-Service accelerates brown-field fleet retrofits SLAM-as-a-Service accelerates brown-field fleet retrofits | +1.4% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Surge in Autonomous Mobile Robots in E-commerce Fulfillment Centers

Locus Robotics and DHL crossed 500 million picks across 35 sites in 2024, demonstrating that camera-centric navigation can scale reliably in high-velocity environments[1]DHL Supply Chain, “DHL and Locus Robotics Reach 500 Million Picks,” dhl.com. Higher uptime, faster deployment cycles, and reduced fixed infrastructure make vision positioning the default for next-generation robotic fleets. Fulfillment operators report throughput gains that shorten payback periods to less than 18 months, reinforcing capital spending plans. Leading platforms now embed AI inference directly into image sensors, cutting cycle times and allowing robots to adjust dynamically to inventory re-slotting. Vendors are also integrating crowd-analytics to manage mixed-traffic aisles where humans and robots share the same path. These advances underpin the robust expansion of the vision positioning system market in logistics.

Rapid Adoption of Vision-Guided Drones for Delivery and Inspection

Utility operators using Skydio’s autonomous systems achieve inspection rates three times faster than manual workflows while maintaining centimeter-level accuracy in GPS-denied zones. DJI’s Dock 3 enables 24/7 flight rotations with IP56 protection, positioning drones for critical asset monitoring in harsh climates. Remote operations remove the requirement for on-site pilots and align with emerging European BVLOS frameworks, broadening serviceable use cases. Dual-sensor payloads—thermal and high-resolution optics—expand into leak detection, corrosion monitoring, and emergency response. As air-traffic regulators streamline permissions, enterprises view autonomous drones as an operational necessity rather than a pilot project, energizing the vision positioning system market.

Falling LiDAR and 3D-Sensor ASPs Enable Mid-Tier Robotics OEMs

Hesai plans to halve automotive-grade LiDAR prices in 2025, signaling a structural cost reset that puts 3D sensing within reach of budget-constrained robot builders. Velodyne’s USD 100 Velabit and Livox’s USD 599 Mid-40 illustrate mass-manufacturing economics that were unattainable five years ago. Price elasticity drives incremental unit demand, and combined camera-LiDAR stacks deliver redundancy for navigation in variable lighting. Component diversification also reduces supply-chain risk, enabling OEMs to negotiate multi-source agreements. As sensor affordability converges with edge compute cost declines, the vision positioning system market enjoys a broader customer base.

EU Machinery Regulation 2023/1230 Mandates Vision-Based Safety

The regulation requires inherently safe design for AI-enabled machinery, compelling equipment manufacturers to embed vision systems that can detect human presence in real time. Compliance shifts vision technologies from optional to mandatory, directly boosting procurement volumes. Early movers such as OMRON partner with Digimarc to combine digital watermarking and machine vision, offering turnkey packages that satisfy both traceability and safety requirements. Multinational OEMs adopt these standards across global product lines to streamline certification, extending the regulation’s reach beyond Europe. As a result, the vision positioning system market benefits from a regulatory floor that stabilizes demand across economic cycles.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High integration and calibration costs High integration and calibration costs | -1.3% | Global, particularly affecting smaller manufacturers | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-1.3% | Geographic Relevance:Global, particularly affecting smaller manufacturers | Impact Timeline:Medium term (2-4 years) |

Privacy regulations curb video analytics in retail and public areas Privacy regulations curb video analytics in retail and public areas | -0.8% | Europe and North America, expanding globally | Long term (≥ 4 years) | |||

Volatile CMOS image-sensor supply chain Volatile CMOS image-sensor supply chain | -1.1% | Global, with acute impact in Asia-Pacific manufacturing | Short term (≤ 2 years) | |||

Cyber-security gaps in vision-based localisation data Cyber-security gaps in vision-based localisation data | -0.7% | Global, with heightened concern in defense and critical infrastructure | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High Integration and Calibration Costs

The complexity of integrating vision positioning systems into existing industrial infrastructure continues to create significant barriers to adoption, particularly for smaller manufacturers with limited technical resources. Advantech's vision positioning solution for wafer cleaning achieved 99.9% yield rates but required extensive calibration and integration work to replace mechanical positioning systems. The challenge extends beyond initial setup to ongoing maintenance, as vision systems require regular recalibration to maintain accuracy in dynamic industrial environments. For instance, G4 Technology's CNC machine vision system reduced alignment time from 60 seconds to 15 seconds but demanded significant upfront investment in system integration and operator training. The expertise gap in vision system integration is creating bottlenecks, with specialized integrators commanding premium pricing that can double total system costs. This challenge is particularly acute in brown-field installations where legacy equipment must interface with modern vision systems, often requiring custom solutions that increase complexity and cost.

Privacy Regulations Curb Video Analytics in Retail and Public Areas

Stringent privacy regulations are constraining the deployment of vision positioning systems in consumer-facing environments, limiting market expansion in high-volume applications. The EU's GDPR requirements mandate that video footage identifying individuals be treated as personal data, necessitating anonymization or redaction technologies that add complexity and cost to vision systems. Retail implementations face particular challenges, as computer vision systems must balance operational insights with privacy compliance, often requiring real-time data processing that obscures individual identification while maintaining analytical value. Microsoft Research's development of privacy-preserving image-based localization using 3D line clouds demonstrates the technical complexity required to address these concerns while maintaining system functionality. The regulatory landscape is creating a two-tier market where privacy-compliant systems command premium pricing while limiting deployment in public spaces. This constraint is particularly impactful for vision positioning applications in smart cities and public transportation, where regulatory uncertainty is delaying large-scale deployments.

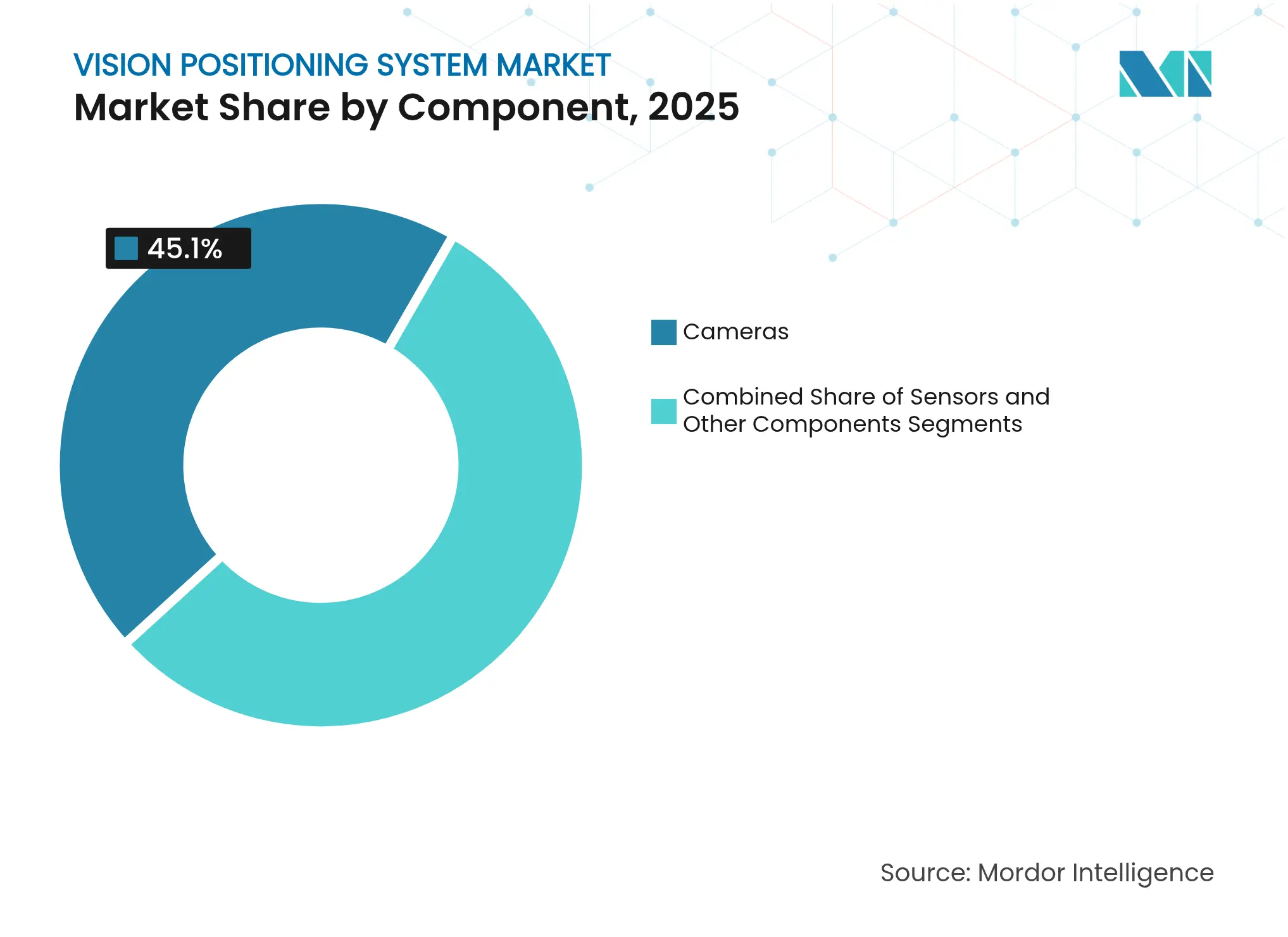

By Component: Cameras Lead Multi-Sensor Integration

Advanced camera systems captured 45.10% market share in 2025, driven by the integration of AI processing capabilities directly into imaging hardware. The segment's 18.35% CAGR through 2031 reflects the transition from traditional CMOS sensors to AI-enabled vision systems that can perform real-time object recognition and positioning calculations. onsemi's AR0145CS Hyperlux SG image sensors exemplify this evolution, featuring global shutter design and automatic exposure control optimized for machine vision applications. The shift toward multi-spectral imaging is creating new opportunities, with near-infrared spatiotemporal color vision emerging as a transformative technology for healthcare applications, projected to grow from USD 285 million in 2019 to USD 485 million by 2030.

Sensors represent the second-largest component category, benefiting from the convergence of multiple sensing modalities within single positioning systems. Other components, including processing units and software platforms, are experiencing rapid growth as edge AI capabilities become standard requirements. The component landscape is shifting toward integrated solutions that combine imaging, processing, and communication capabilities, reducing system complexity while improving performance. Supply chain dynamics are influencing component selection, with Apple's shift from Sony to Samsung for iPhone 16 camera sensors highlighting the importance of diversified sourcing strategies.

Note: Segment shares of all individual segments available upon report purchase

By Location: Indoor Applications Dominate Current Deployments

Indoor applications commanded 60.80% market share in 2025, reflecting the controlled environment advantages that enable higher positioning accuracy and system reliability. Slamcore's visual spatial intelligence solutions demonstrate how indoor positioning systems can achieve centimeter-level accuracy without external infrastructure, enabling seamless integration with existing warehouse operations. The indoor segment benefits from predictable lighting conditions and reduced environmental variables, allowing for optimized algorithm performance and lower maintenance requirements. Healthcare facilities are emerging as a key growth area, with BLE beacon systems providing cost-effective indoor positioning for patient and asset tracking.

Outdoor applications are experiencing accelerated growth at 12.74% CAGR, driven by advances in GPS-independent positioning technologies and improved weather resistance. The outdoor segment faces greater technical challenges, including variable lighting conditions, weather interference, and the need for longer-range detection capabilities. However, breakthrough technologies like gyroscope-on-a-chip navigation systems are addressing GPS vulnerability concerns, particularly for military applications where jamming and spoofing represent significant threats. The convergence of indoor and outdoor positioning capabilities is creating new hybrid applications that can maintain accuracy across diverse environments.

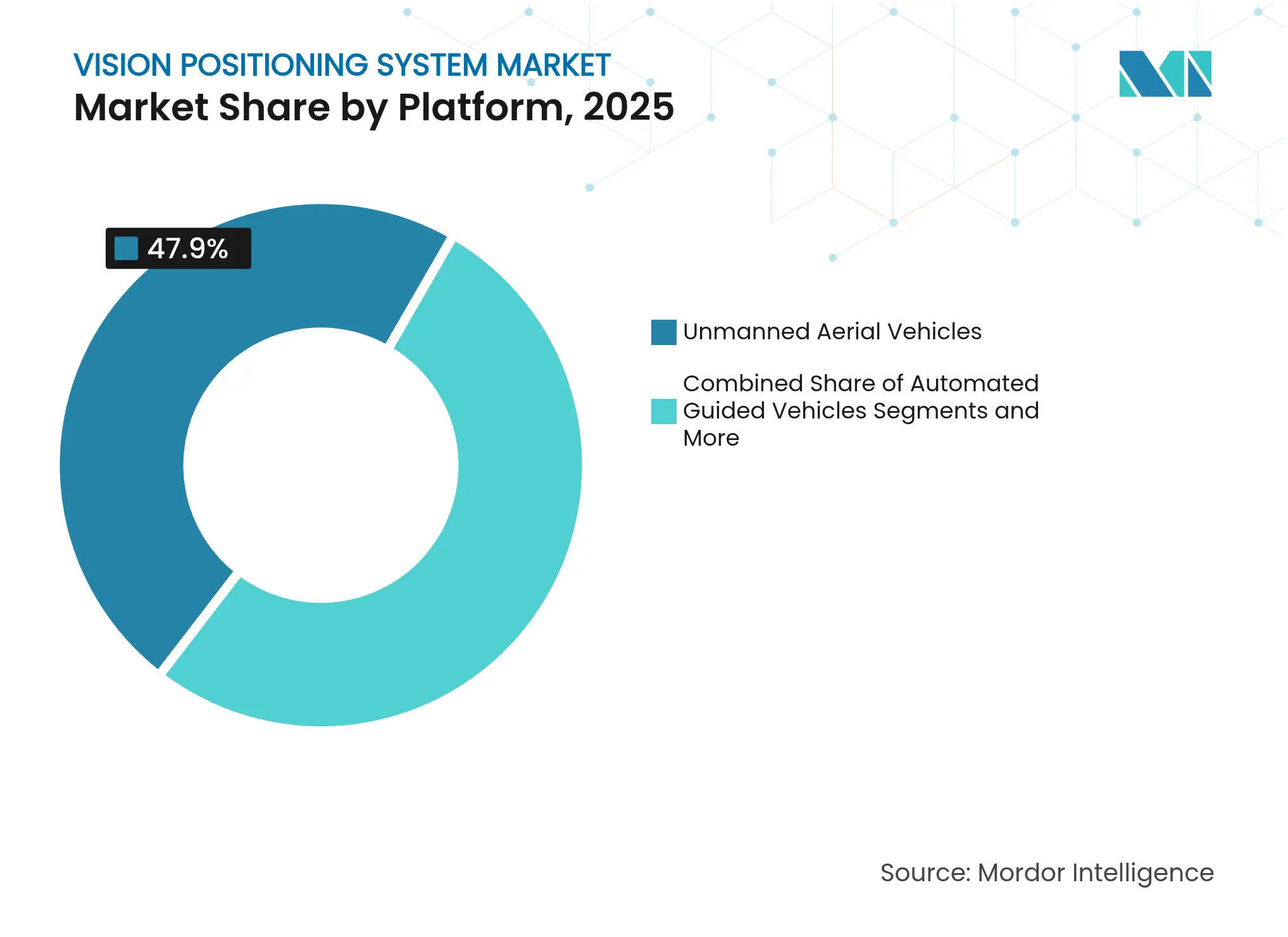

By Platform: UAVs Lead While AGVs Show Explosive Growth

Unmanned aerial vehicles maintained 47.90% market share in 2025, supported by expanding applications in infrastructure inspection, delivery services, and surveillance operations. DJI's Matrice 4 Series integration of GNSS+Vision Fusion Positioning demonstrates how UAV platforms are combining multiple positioning technologies to achieve reliable navigation in challenging environments. The UAV segment benefits from regulatory approvals for BVLOS operations and increasing acceptance of autonomous drone operations in commercial applications. Defense applications are driving premium UAV positioning requirements, with L3Harris receiving USD 263 million in ENVG-B orders that incorporate advanced vision positioning capabilities.

Automated guided vehicles are experiencing the highest growth rate at 23.95% CAGR, reflecting the warehouse automation boom and the shift toward flexible manufacturing systems. KINEXON's Fleet Manager platform demonstrates how AGV positioning systems are evolving toward multi-vendor integration and real-time coordination capabilities. Industrial robots represent a stable platform category, benefiting from the integration of vision positioning with collaborative robotics applications. Other platforms, including handheld devices and wearable systems, are emerging as growth areas driven by augmented reality applications and portable inspection tools.

Note: Segment shares of all individual segments available upon report purchase

By End-user: Industrial Manufacturing Leads, Healthcare Surges

Industrial and manufacturing applications captured 32.10% market share in 2025, driven by quality control automation and precision assembly requirements. Cognex's customer implementations demonstrate the breadth of manufacturing applications, from EV battery pack assembly to bakery production optimization, highlighting the versatility of vision positioning systems across diverse industrial processes. The manufacturing segment benefits from established ROI models and proven integration pathways, making it attractive for vision system deployments. OMRON's launch of the VT-S10 Series 3D-AOI inspection system exemplifies how manufacturers are integrating AI with vision positioning to address increasingly complex PCB assembly requirements.

Healthcare emerges as the fastest-growing end-user segment at 15.05% CAGR, propelled by surgical robotics and patient monitoring applications. Apple Vision Pro's historic use in shoulder replacement surgery demonstrates the potential for vision positioning systems to enhance surgical precision and outcomes. GE Healthcare's collaboration with NVIDIA to develop autonomous X-ray and ultrasound systems represents the convergence of AI and vision positioning in medical imaging applications. Retail, defense and security, and transportation and logistics segments each contribute significant market share, with retail applications facing privacy regulation challenges while defense applications drive premium positioning requirements. Other end-users, including agriculture and construction, are emerging as growth areas driven by precision agriculture and automated construction equipment.

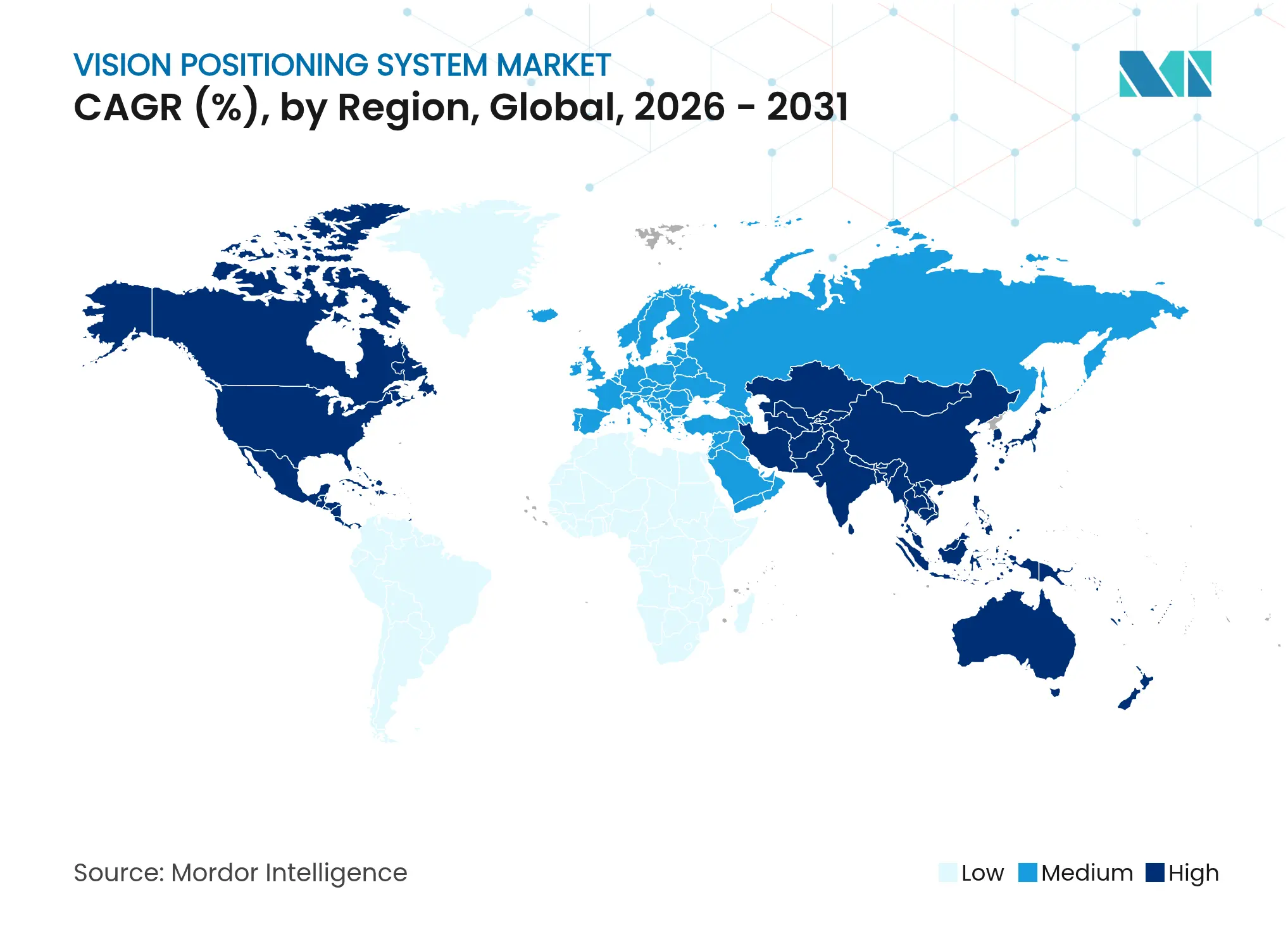

North America dominated the vision positioning system market with 38.40% market share in 2025, driven by defense spending, industrial automation investments, and early adoption of autonomous systems. The region's growth is supported by significant military contracts, including L3Harris's USD 263 million ENVG-B order and Elbit Systems' USD 139 million night vision contract, demonstrating the defense sector's commitment to advanced vision positioning technologies. The regulatory environment in North America is generally supportive of vision system deployments, with fewer privacy restrictions compared to Europe, enabling broader commercial applications. Industrial automation adoption is accelerating, with companies like Cognex reporting growth in logistics and automotive sectors despite overall market challenges. The region's established technology infrastructure and skilled workforce provide competitive advantages for complex vision system integrations.

Asia-Pacific represents the fastest-growing regional market with 17.25% CAGR through 2031, driven by manufacturing expansion, smart city initiatives, and aggressive automation adoption. China's leadership in LiDAR technology is exemplified by Hesai's plan to halve sensor prices, potentially disrupting global cost structures and accelerating adoption across price-sensitive applications. Japan's focus on precision manufacturing and robotics creates sustained demand for high-accuracy vision positioning systems, with companies like ViXion developing advanced autofocus eyewear priced at 80,000 yen (USD 533) for global markets. The region's manufacturing-centric economy drives demand for industrial vision applications, while emerging economies are adopting vision positioning systems to leapfrog traditional automation approaches.

Europe maintains significant market presence despite privacy regulation challenges, with the EU Machinery Regulation 2023/1230 creating mandatory demand for vision-based safety systems across industrial applications. The region's emphasis on worker safety and environmental sustainability aligns with vision positioning system capabilities, creating regulatory-driven growth opportunities. HENSOLDT's development of CERETRON software for digitally networked sensor technology demonstrates European innovation in defense applications, while Safran's laser optical communication solutions highlight the region's expertise in advanced positioning technologies. The regulatory framework, while creating compliance challenges, is establishing Europe as a leader in privacy-preserving vision technologies that may influence global standards.

Market Concentration

The vision positioning system market exhibits moderate concentration with established players maintaining technological leadership while emerging specialists capture niche opportunities. Market leaders like Cognex Corporation demonstrate resilience through diversified applications, reporting 5% revenue growth in Q1 2024 despite challenging conditions, while launching AI-enabled 3D vision systems that position the company for next-generation applications. Strategic partnerships are becoming increasingly important, exemplified by OMRON's collaboration with Cognizant to integrate IT and OT capabilities across manufacturing applications, leveraging OMRON's 200,000+ SKU product lineup for comprehensive automation solutions. The competitive landscape is characterized by technology convergence, with traditional vision companies expanding into AI and robotics while semiconductor companies integrate vision capabilities into their platforms.

White-space opportunities are emerging in SLAM-as-a-Service offerings and edge AI processing, where companies like Slamcore are developing platform-agnostic solutions that enable brown-field retrofits without infrastructure overhauls. Emerging disruptors are leveraging specialized technologies to challenge incumbents, with companies like Inbolt developing AI-powered systems that enable robots to track moving assemblies in real-time, addressing previously unsolvable manufacturing challenges. The integration of vision positioning with broader automation ecosystems is creating new competitive dynamics, where success depends on platform compatibility and ecosystem integration rather than standalone product performance. Patent activity in adversarial attack detection and privacy-preserving localization indicates the industry's focus on addressing security and regulatory challenges that could reshape competitive positioning.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECAST (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Market Definitions and Key Coverage

Mordor Intelligence defines the vision positioning system (VPS) market as all hardware, embedded software, and integration services that allow unmanned aerial vehicles, automated guided vehicles, industrial robots, and other mobile assets to calculate location and orientation by matching live images with a stored visual map. This study values only factory-built systems sold to end users or OEMs and reports revenue in constant 2024 USD.

Scope Exclusion: Pure-play indoor Bluetooth or Wi-Fi based positioning tags without a machine vision element are out of scope.

Segmentation Overview

Detailed Research Methodology and Data Validation

Primary Research

We interviewed VPS hardware designers in North America, robotics integrators in Europe, component distributors in Asia-Pacific, and defense program managers in the Middle East. These conversations validated adoption rates, price dispersion, and service attach ratios that were only partly visible in secondary data.

Desk Research

Our analysts began with public data from civil aviation regulators, the International Federation of Robotics, drone shipment customs records, and trade association white papers such as those from AUVSI and the European Machine Vision Association. Academic journals that track simultaneous localization and mapping (SLAM) patent filings, plus respected news aggregators like Dow Jones Factiva, supplied technology maturity signals. Company 10-Ks, investor decks, and procurement portals were then screened to extract average selling prices (ASPs) for industrial-grade optical sensors and camera modules. Select paid databases, notably D&B Hoovers for revenue splits and Questel for patent counts, filled corporate and IP gaps. The sources listed are illustrative; many additional references supported data checks and context building.

Market-Sizing & Forecasting

A top-down reconstruction starts with global drone, AGV, and industrial robot production, which is then adjusted for VPS penetration by platform and location setting. Results are sense checked through bottom-up roll-ups of sampled supplier revenue and channel ASP times volume snapshots. Key variables include drone unit production, AGV installations, industrial robot shipments, optical sensor ASP trends, beyond visual line of sight regulatory approvals, and R&D spending on visual SLAM. Multivariate regression complemented by three scenario analysis projects these inputs to 2030; platform specific growth paths supplied by our primary experts guide coefficient calibration. Where supplier splits are incomplete, conservative interpolation using regional averages bridges the gap.

Data Validation & Update Cycle

Every draft model runs through automated variance checks, peer review, and a senior analyst sign off. Annual report refreshes are mandatory, and ad hoc updates trigger when material events such as major platform recalls or regulatory shifts move any key variable.

Why Mordor's Vision Positioning System Baseline Earns Trust

Benchmark comparison

Published VPS numbers vary because firms pick different platform mixes, price bases, and refresh cadences.

Key Gap Drivers include whether outdoor only drone revenues are counted, how aggressively future ASP compression is modeled, and if secondary research figures are re validated with live channel checks before publication.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 6.91 B (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 6.18 B (2024) | Global Consultancy A | Excludes industrial robot retrofits; single scenario forecast | ||

USD 5.70 B (2022) | Trade Journal B | Uses list prices, not blended ASPs; outdated base year | ||

USD 10.06 B (2024) | Regional Consultancy C | Bundles indoor Bluetooth tags; limited primary validation |

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.