Smart Lighting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

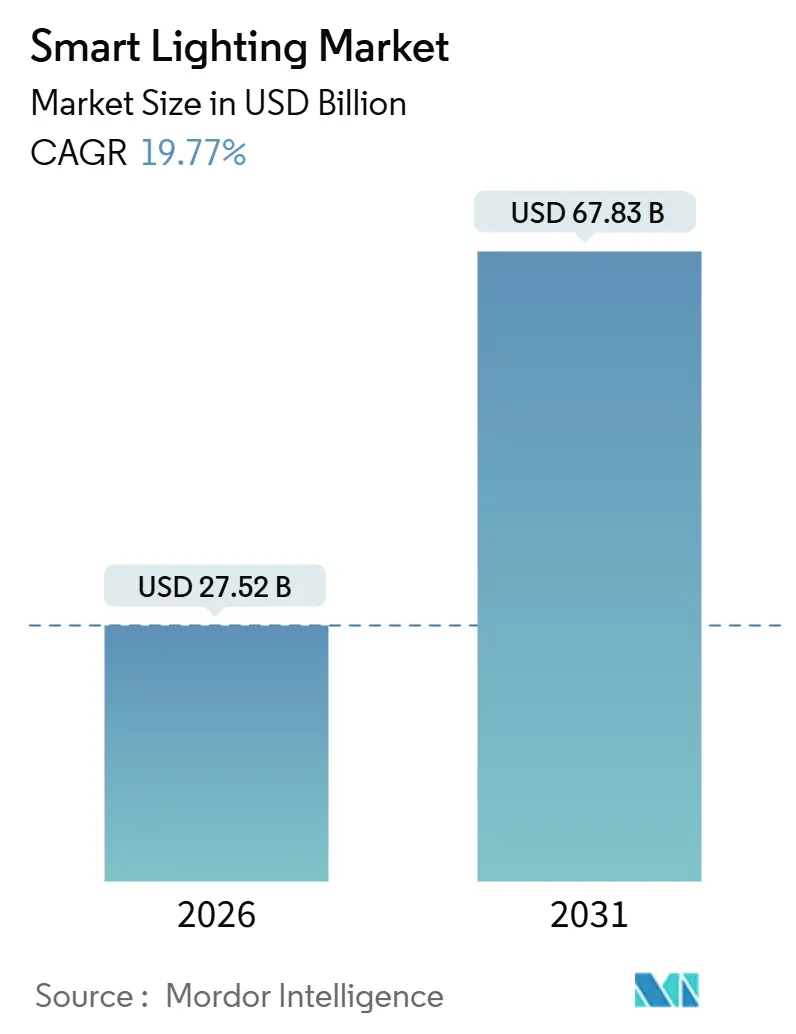

| Market Size (2026) | USD 27.52 Billion |

| Market Size (2031) | USD 67.83 Billion |

| Growth Rate (2026 - 2031) | 19.77% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Lighting Market Analysis by Mordor Intelligence

The smart lighting market size reached USD 27.52 billion in 2026 and is projected to climb to USD 67.83 billion by 2031, translating into a 19.77% CAGR across the forecast horizon, a trajectory that underlines the sector’s transition from early-adopter novelty to mainstream building-performance technology. Three structural shifts are shaping this expansion: national net-zero building codes that took effect in 2025, utility programs now covering 30-50% of retrofit capital outlays, and the arrival of Matter 1.4, which finally harmonized fragmented connectivity protocols. Vendors are weaving value-added software edge-AI dimming, Li-Fi data backhaul, and grid-interactive demand-response into hardware, turning luminaires into data nodes and service gateways. Competitive intensity remains elevated because legacy lighting majors, consumer-electronics brands, and specialist start-ups are converging on the same addressable opportunity. Asia-Pacific is the scale leader, but sovereign smart-city mandates in the Middle East give that sub-region the fastest growth runway.

Key Report Takeaways

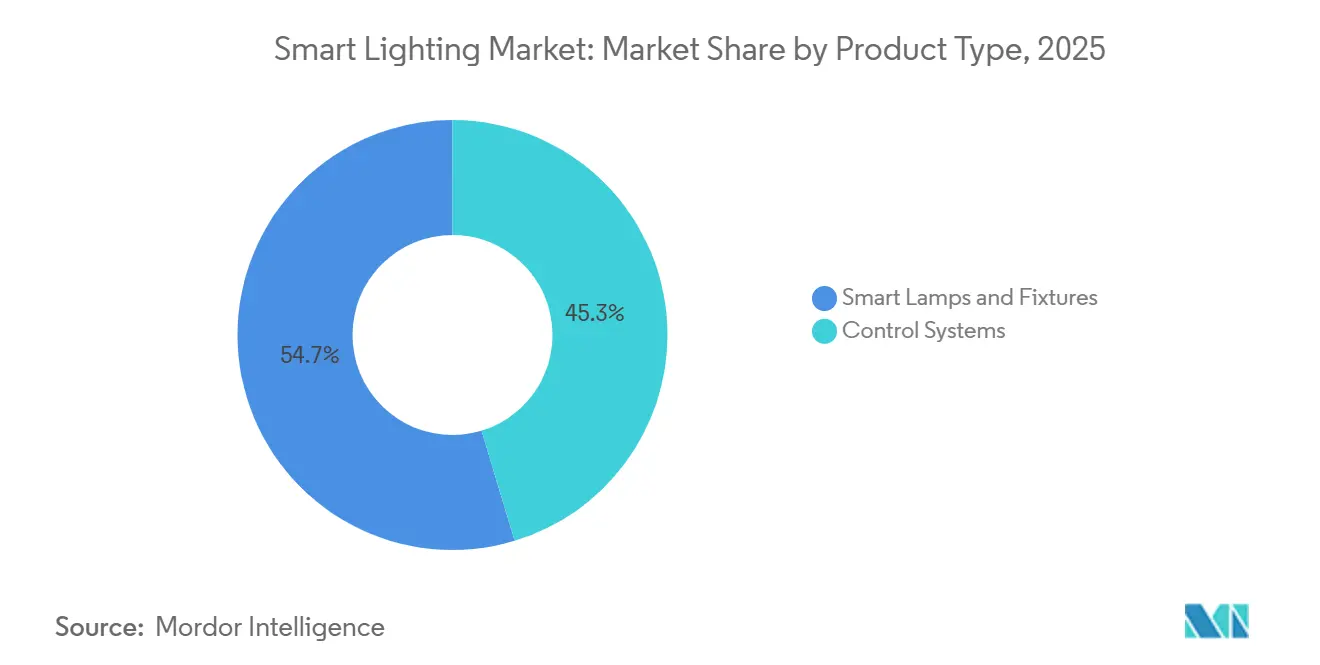

- By product category, smart lamps and fixtures captured 54.67% of the smart lighting market share in 2025, while control systems are set to register the fastest 20.19% CAGR through 2031.

- By installation type, retrofits dominated with 62.91% of the smart lighting market share in 2025; new construction, however, is forecast to expand at a 20.13% CAGR on the back of net-zero building codes.

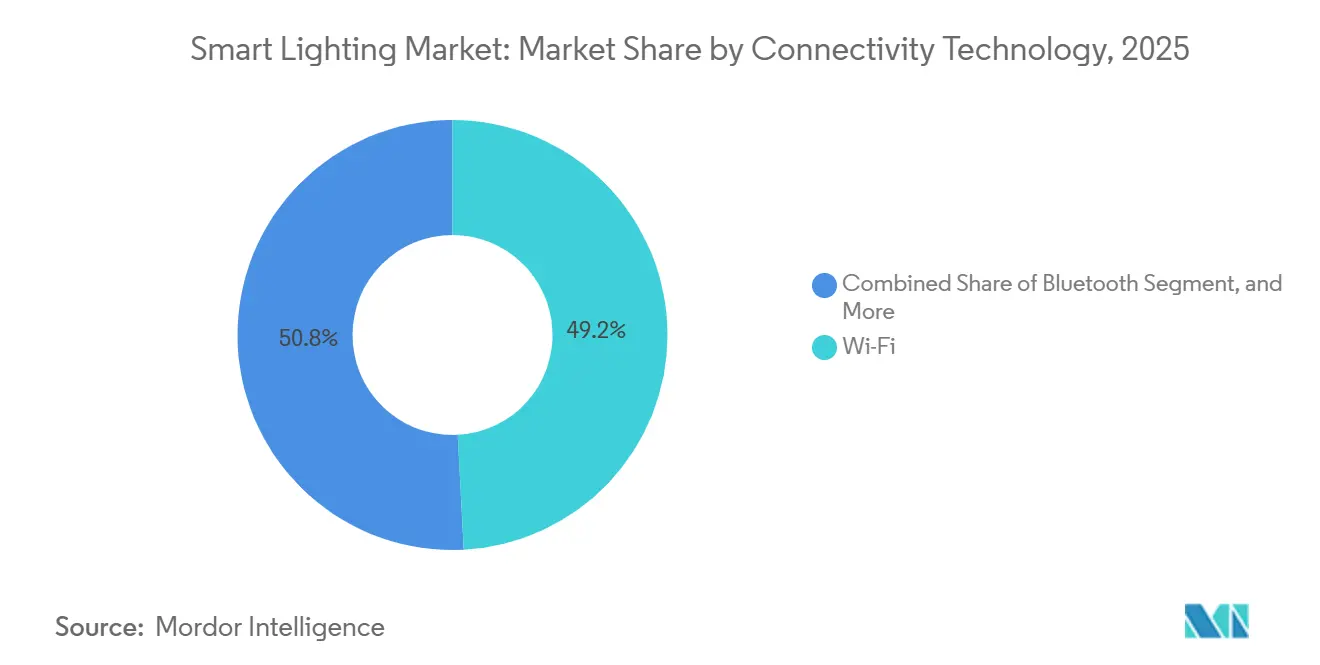

- By connectivity technology, Wi-Fi accounted for 49.17% of 2025 revenue, whereas Bluetooth mesh is poised to advance at a 20.58% CAGR over the forecast period.

- By end user, residential households accounted for 46.73% of the smart lighting market share in 2025, yet industrial facilities are projected to deliver the highest 20.53% CAGR through 2031.

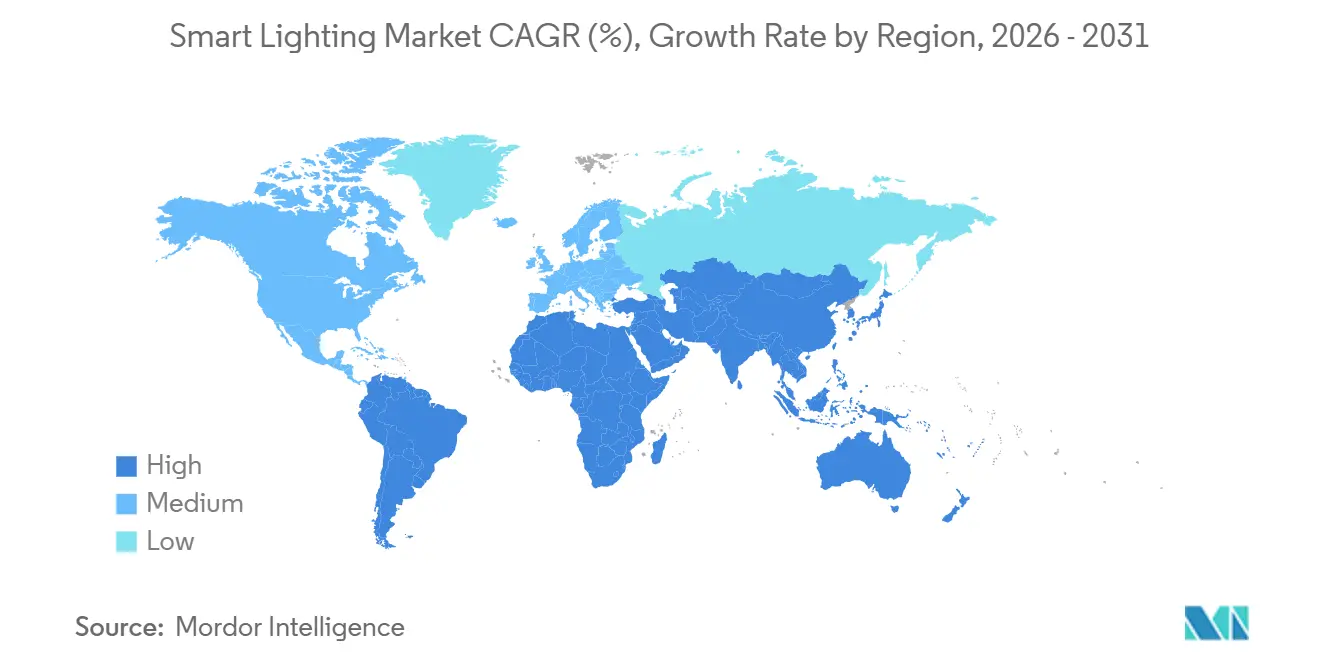

- By geography, Asia-Pacific led with a 37.38% revenue share in 2025, but the Middle East is positioned for the strongest 20.71% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Smart Lighting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Smart-Home Ecosystem Integration | +3.8% | Global, with concentration in North America, Western Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Rapid LED Cost Reductions Improve ROI | +4.2% | Global, strongest in price-sensitive markets including India, Southeast Asia, Latin America | Short term (≤ 2 years) |

| Utility-Funded Demand-Side-Management Incentives | +3.5% | North America and Europe, emerging in Australia and select Middle East utilities | Medium term (2-4 years) |

| National Net-Zero Building Codes (2025-2030 Roll-outs) | +4.1% | California, European Union, Japan, South Korea, with pilot adoption in China and India | Long term (≥ 4 years) |

| Li-Fi-Enabled Lighting Pilots in Warehouses | +1.2% | Industrial hubs in Germany, United States, China, and United Arab Emirates | Long term (≥ 4 years) |

| Edge-AI-Powered Adaptive Dimming Algorithms | +2.3% | Commercial and industrial segments in developed markets, gradual diffusion to emerging economies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Smart-Home Ecosystem Integration

Voice-assistant platforms and Matter 1.4 certification have reduced purchase friction by enabling a single firmware image to interoperate with Apple HomeKit, Google Home, Amazon Alexa, and Samsung SmartThings, removing vendor lock-in and lowering support costs.[1]Connectivity Standards Alliance, “Matter 1.4 Specification and Device Certification,” csa-iot.org Thread 1.4’s low-power mesh has raised the device limit to 250 nodes per network, while self-healing routes alleviate reliability complaints that dogged early Zigbee rollouts. Smart-bulb average selling prices fell 22% between 2024 and 2025 as Asian contract manufacturers scaled production, expanding the addressable household base. Retrofit-oriented business models benefit disproportionately because consumers can swap bulbs without rewiring. Commercially, hospitality chains now bundle Matter-certified downlights with occupancy sensors so guestrooms automatically adjust to preferred scenes at check-in, improving the guest experience while shaving energy bills.

Rapid LED Cost Reductions Improve ROI

High-bay fixtures suitable for warehouses now retail at USD 120–180, down from USD 250–350 just three years earlier, while efficacy leapt to 150 lumens per watt, nearly double that of metal-halide incumbents.[2]U.S. Department of Energy, “Lighting Facts Database – High-Bay LED Fixtures,” energy.gov Utility incentives in Massachusetts and Connecticut shave 40–50% off material costs, routinely compressing payback to 12 months. Chinese and South Korean chip foundries are pushing gallium nitride epitaxy yields higher, cutting die costs by a further 10–15% each year. Cities are capitalizing: Dubai retrofitted 900 luminaires on Sheikh Rashid Street in 2024, netting 60% energy savings and a 4-year payback, even without subsidies. The cost curve keeps steepening, reinforcing price elasticity across commercial, industrial, and municipal segments.

Utility-Funded Demand-Side-Management Incentives

Regulated utilities treat lighting upgrades as the least-cost alternative to building peaking plants. Connecticut approved USD 45 million for 2025 lighting rebates, offering USD 30–80 per LED fixture and USD 15 more for networked controls.[3]Connecticut Public Utilities Regulatory Authority, “Energy Efficiency Program Approvals for 2025,” portal.ct.gov/pura Massachusetts disbursed USD 78 million in 2024, reporting an average 62% reduction in lighting energy use across participating sites. Program design is evolving from one-time rebates toward performance-based compensation: facilities that allow remote curtailment during grid stress secure capacity payments worth 10-15% of project value. The U.S. General Services Administration has embedded such grid-interactive requirements in all federally funded retrofits.

National Net-Zero Building Codes

California’s 2025 Title 24 update mandates networked lighting with occupancy sensing, daylight harvesting, and demand-response in non-residential buildings above 10,000 square feet, cutting lighting energy 35% relative to 2022 baselines. The European Union’s Energy Performance of Buildings Directive requires near-zero-energy construction by 2028, with lighting controls contributing 15–20% toward compliance. Japan and South Korea enacted analogous codes in 2025, while China pilots net-zero standards in tier-one cities. For supply chains, the shift means sensors and wireless modules must be standard bill-of-materials items rather than optional add-ons. Design-build firms are responding by embedding smart lighting into initial construction documents rather than value-engineering it out later.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-Security Vulnerabilities in Wireless Protocols | -2.1% | Global, with heightened concern in critical infrastructure and government facilities | Short term (≤ 2 years) |

| Fragmented Inter-Operability Standards | -1.8% | Global, gradually diminishing as Matter adoption scales | Medium term (2-4 years) |

| Supply Chain Volatility in Rare-Earth Phosphors | -1.3% | Global, most acute in high-color-rendering applications for retail and hospitality | Medium term (2-4 years) |

| Smart-Home Privacy Regulation Uncertainty | -0.9% | European Union, California, and emerging frameworks in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cyber-Security Vulnerabilities in Wireless Protocols

The National Institute of Standards and Technology warned in 2024 that Zigbee and Bluetooth LE lack robust authentication, exposing networks to spoofing when default credentials persist. CVE-2024-41126 demonstrated remote takeover of luminaires via unauthorized pairing, spurring critical-facility operators to air-gap lighting networks or revert to wired DALI-2 buses. Such precautions add USD 8–15 per fixture, lengthening payback and complicating building-automation integration. Matter’s device-attestation aims to neutralize the threat by cryptographically verifying hardware provenance, but full mitigation requires field replacements over several product cycles.

Fragmented Inter-Operability Standards

Before Matter, buyers had to juggle Zigbee, Z-Wave, proprietary Wi-Fi, and Bluetooth mesh, each requiring separate hubs and mobile apps, while commercial sites had to balance DALI, BACnet, and vendor-specific protocols. As of mid-2025, fewer than 30% of smart-lighting SKUs carried Matter certification, and legacy estates still require protocol gateways, which cost USD 200–500 per building and add another point of failure. Although adoption is accelerating, many facility managers defer upgrades until a majority of their installed base is natively compliant.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Control Systems Capture Value Beyond Hardware

Smart lamps and fixtures captured 54.67% of the smart lighting market share in 2025, while control systems are set to register the fastest 20.19% CAGR through 2031. Energy-service companies increasingly position controls as the gateway to demand-response revenue, predictive maintenance, and occupant-centric comfort. In value terms, lamps and fixtures still dominated 2025 sales, but commoditization is squeezing margins below 25%. Helvar’s ActiveAhead deployment at Volvo Trucks’ Swedish plant illustrates the control-centric thesis: edge AI learned work-cell occupancy, pre-dimmed aisles, and harvested daylight to trim an additional 23% of power. Residential buyers, meanwhile, gravitate toward bulbs that require no wiring changes; average retail pricing for a Matter-certified lamp fell to USD 12 in 2025, democratizing access. The shifting stack means firmware, analytics, and cloud dashboards, not raw lumens, determine vendor differentiation.

Smart lamps and fixtures, nonetheless, remain indispensable. Circadian-tuning is gaining traction in offices and hospitality as facility managers quantify productivity gains tied to light spectra, while decorative luminaires support branded ambience in retail. Yet even here, controls are subsuming the narrative: tunable fixtures ship with embedded drivers that listen for Matter or DALI-2 commands out of the box. As the installed base saturates, software upgrades will extract recurring revenue, transforming lamps from capital goods into digital platforms.

By Installation Type: Net-Zero Codes Tip the Scale Toward New Builds

Retrofits accounted for 62.91% of the smart lighting market share in 2025, reflecting the significant inventory of fluorescent and metal-halide luminaires still in use in global building stock. Utility incentives underwrite much of the swap-out cost, translating into 12- to 18-month paybacks that meet even CFO-level hurdle rates. Yet the compliance tide is turning: new construction is accelerating at a 20.13% CAGR because updated energy codes make networked lighting mandatory at the blueprint stage. When lighting is specified early, contractors prewire for sensors and provide low-voltage power for gateways, slashing future labor costs.

Retrofit economics bifurcate. Simple lamp-for-lamp replacements yield 50-60% energy cuts but miss the incremental 20–30% available from occupancy-aware dimming. Building owners now select integrated control packages to unlock utility performance-based incentives. Municipal case studies reinforce the point: Dubai’s 2024 Sheikh Rashid Street project realized 60% savings on a four-year unsubsidized payback and immediately initiated trials on secondary roads for adaptive dimming.

By Connectivity Technology: Bluetooth Mesh Surges on Gateway-Free Economics

Wi-Fi accounted for 49.17% of revenue in 2025, thanks to the ubiquity of routers and consumer familiarity, but its single-point-of-failure profile and upstream bandwidth demands are liabilities. Bluetooth mesh, advancing at a 20.58% CAGR, eliminates the need for dedicated gateways, cutting USD 3–5 from the bill of materials and simplifying commissioning. Networks can scale to 32,000 devices, auto-reconfigure routes, and operate without touching the building’s IT VLAN, an advantage in retail and hospitality. Matter 1.4’s standardized commissioning further accelerates adoption because a single QR code brings devices online regardless of smartphone OS.

Zigbee endures in commercial sites where legacy building-management systems already run Zigbee sensors for HVAC, but security concerns after CVE-2024-41126 have stalled new bids in government and healthcare. Li-Fi remains niche yet strategic: warehouses running autonomous mobile robots now pilot luminaires modulated at 224 Gb/s to sidestep RF interference. As chipsets mature, Li-Fi may carve a defensible beachhead in industrial automation long before it permeates offices.

By End-User: Industrial Facilities Embrace Data-Centric Lighting

Residential users accounted for 46.73% of 2025 revenue, driven by sub-USD 15 smart bulb pricing and voice assistant convenience. Yet warehouses, factories, and logistics hubs will deliver the steepest CAGR of 20.53% through 2031. High-bay LEDs at 150 lumens per watt, coupled with 18- to 24-month simple paybacks, put lighting top of the industrial energy-efficiency stack. Edge-AI controls go further, adjusting luminance per zone, per shift, and per daylight condition. Li-Fi pilots add a data-comms layer, enabling robots to localize and communicate without congesting the 2.4 GHz Wi-Fi band.

Commercial real estate pursues human-centric metrics such as circadian lighting and color-tunable luminaires for retail visual merchandising. These applications require high color-rendering LEDs that depend on rare-earth phosphors, a supply chain vulnerable to geopolitical shocks. Meanwhile, municipalities in emerging economies allocate constrained budgets to smart street lighting, drawn by lower maintenance costs and 40-60% energy savings.

Geography Analysis

L37: Asia-Pacific commanded 37.38% of the smart lighting market share in 2025, anchored by China’s manufacturing scale, India’s urbanization, and Japan’s tech-savvy construction sector. The region’s growth is steady but moderating as early adopters transition from fixture swaps to incremental control-system upgrades. Middle East and Africa, conversely, will post the quickest 20.71% CAGR because sovereign smart-city mandates hard-code LED conversion deadlines as early as 2027. Qatar’s Public Works Authority committed to nationwide smart LED streetlighting in October 2025, aiming for 40–50% energy savings.

North America and Europe remain crucibles of innovation. California’s 2025 Title 24 revision and Massachusetts’ generous DSM rebates shorten payback cycles, embedding lighting controls during schematic design. The European Union’s near-zero-energy directive requires member states to incorporate networked lighting in all new buildings by 2028. These policies keep the regions’ aggregate revenue base resilient despite lower headline growth.

South America and Africa still lag in penetration due to budget constraints and electricity tariff subsidies that dilute ROI. Brazil and South Africa are piloting municipal conversions, but fiscal austerity limits scale. As LED module pricing falls below USD 1 per kilolumen in 2026, these markets will gradually migrate from pilot to portfolio execution.

Regulatory Landscape

Smart lighting regulation is tightening around three compliance pillars: building-energy performance, product cyber security, and market-access conformity for connected radios. California advanced this shift with the 2025 Title 24 update mandating networked lighting controls (occupancy sensing, daylight harvesting, and demand-response) for large non-residential buildings, while the European Union moved toward near-zero-energy requirements under the Energy Performance of Buildings Directive timeline referenced in the report. In China, GB 30255-2026 introduced an updated indoor LED energy-efficiency framework that explicitly covers smart dimming and sensor-based products, with an effective date in 2027, shaping product design choices ahead of enforcement.

In 2026, the European Union added new technical barriers that pull smart lighting deeper into regulated IoT. EN 63284-1:2026 enforcement began in June 2026 with electromagnetic compatibility and firmware security verification, and the Cyber Resilience Act obligations started to phase in during 2026 for products with digital elements. Separately, the EU published a CE-RED amendment (EU) 2026/1183 that ties certain Wi-Fi 7 IoT devices, including smart lighting, to mandated Matter protocol compliance from October 1, 2026, moving interoperability from an optional capability to a de facto requirement. Outside standards, 2026 tariff actions in the United States (Section 232 and proposed Section 301 measures cited in the evidence pack) elevated landed-cost risk for luminaires and components, reinforcing the need for regionalized assembly and documented origin strategies alongside technical compliance.

Value Chain Analysis

The smart lighting value chain starts upstream with LED chips and packaging, phosphors and optics, drivers and power electronics, and a growing share of sensors and wireless modules (Wi-Fi, Bluetooth mesh, Zigbee, Thread). Midstream value concentrates in luminaire and lamp manufacturing, firmware and connectivity stacks, gateways where required, and lighting-management software that increasingly enables commissioning, analytics, and grid-interactive control. Downstream channels split between DIY retail and e-commerce for residential bulbs and switches, and specification-driven routes for commercial, industrial, and municipal projects led by electrical contractors, system integrators, ESCOs, and building-automation partners.

Recent ecosystem moves point to where value capture is shifting. In June 2026, Signify expanded Philips Hue hardware and advanced interoperability through collaboration with Silicon Labs on concurrent multiprotocol support (Zigbee plus Matter-over-Thread), underscoring that connectivity silicon, device firmware, and certification readiness are becoming as central as the luminaire bill of materials. On the demand side, code-driven specification (for example, the report-cited California Title 24 networked-controls requirements starting 2025) is pulling sensors, secure wireless modules, and commissioning tools into standard project scope, increasing the role of software onboarding and lifecycle updates. At the same time, supply chains remain sensitive to rare-earth phosphors and trade friction, pushing vendors toward multi-sourcing and regional final assembly so they can meet lead-time expectations while handling compliance testing and documentation.

Competitive Landscape

Industry structure is moderately fragmented. The top five incumbents, Signify, Acuity Brands, Hubbell, Samsung, and Xiaomi control a combined 42–47% of 2025 revenue, with the remaining share scattered among regional specialists, IoT start-ups, and DIY-focused brands. Incumbents defend their share by bundling hardware, controls, and cloud analytics into subscription packages. Signify’s Interact suite monetizes remote condition monitoring and utility DR participation, converting once-off fixture sales into annuity revenue. Acuity’s 2024 nLight AIR release brought BACnet integration without gateways, easing commercial retrofits.

Consumer-electronics challengers leverage existing smart-home channels. Snap One’s Lux by Control4, shipping since Q2 2025, supports 600-watt loads and 19 tunable colors, aiming at upscale residential projects. Matter certification is leveling the field: Nanoleaf and Sengled rushed to certify in early 2025, undermining incumbents’ proprietary ecosystem moat.

White-space opportunities align with three vectors. Edge-AI platforms such as Helvar ActiveAhead distill occupancy data to enable real-time dimming, adding 15–25% additional savings over static scheduling. Li-Fi-enabled fixtures solve RF-challenged warehouse automation. Finally, grid-interactive controls unlock DSM revenue streams, improving payback by up to 18 months. Vendors that package these capabilities into turnkey offerings stand to outpace commodity hardware rivals.

Smart Lighting Industry Leaders

Signify N.V.

Acuity Brands Inc.

Hubbell Inc.

Eaton Corp.

Lutron Electronics Co. Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Interoperability and multi-ecosystem control are active whitespace areas where vendors can reduce installation friction and lower support costs across residential and light-commercial deployments. The Connectivity Standards Alliance released Matter 1.6 in June 2026 with Joint Fabric to unify control across multiple ecosystems, and Signify followed in the same month with concurrent multiprotocol work on select Philips Hue bulbs (Zigbee plus Matter-over-Thread) through Silicon Labs. Together, these moves suggest product roadmaps are being rebuilt around cross-platform operation rather than proprietary hubs.

That shift supports opportunity in control systems, gateways where needed, and software experiences that simplify commissioning at scale, particularly in retrofit-heavy building stock where mixed protocols persist. Compliance-driven product refresh is also extending replacement and upgrade cycles, including in regions where requirements expand beyond energy savings into security, safety, and sustainability documentation. The EU enforcement of EN 63284-1:2026 (June 2026) and the phased application of Cyber Resilience Act obligations in 2026 raise the bar for firmware security practices and update mechanisms, while UL 60335-2-107:2026 (published June 2026, effective September 2026) and additional testing expectations cited in the evidence pack expand validation needs for RF immunity and driver safety. Separately, EU carbon-footprint verification requirements tied to Implementing Regulation (EU) 2026/1189 starting October 1, 2026 create a procurement lever for suppliers that can provide verified lifecycle documentation. In response, manufacturers and platform providers that can operationalize retesting, certification, OTA updates, and sustainability reporting across broad SKU portfolios should be positioned to keep channel availability while meeting these expanding requirements.

Recent Industry Developments

- July 2026: Luminii acquired Filix Lighting to broaden its urban, exterior, and underwater lighting portfolio, extending its reach into specialized outdoor and marine applications. The combination strengthens breadth for specification-driven projects where connected controls, durability, and system integration requirements favor suppliers with wider, application-specific catalogs.

- June 2026: Signify expanded the Philips Hue portfolio with new wired switches, Play lamps, and next-generation candle bulbs, reinforcing its focus on both new form factors and the installed-base upgrade path. In the same month, Signify worked with Silicon Labs to add concurrent multiprotocol capability on select Hue bulbs so Zigbee and Matter-over-Thread can operate together, easing migration toward standardized smart-home interoperability.

- October 2025: Qatar’s Public Works Authority launched a nationwide conversion of streetlights to smart LED by 2027, targeting 40-50% energy savings. The program supports large-scale, networked outdoor deployments that pull through luminaires, controls, and ongoing management software, and it adds a clear public-sector anchor for smart-city procurement in the Middle East.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue from smart lighting products and related software that enable connected, remote, and automated lighting control across indoor and outdoor environments. It includes connected lamps and fixtures, sensors, gateways, and lighting management software sold for smart lighting use.

Scope exclusions: Stand-alone, non-networked LED fixtures and traditional incandescent or fluorescent lamps are excluded from this sizing.

Segmentation Overview

- By Product Type

- Control Systems

- Smart Lamps and Fixtures

- By Installation Type

- New Construction

- Retrofit

- By Connectivity Technology

- Wi-Fi

- Bluetooth

- Zigbee

- Other Connectivity Technologies

- By End-User

- Residential

- Commercial

- Industrial

- Other End-Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the foundation on adoption, regulations, and the overall lighting demand pool that smart products tie into. Public sources such as the US Department of Energy, the International Energy Agency (IEA), the World Bank, and national statistics agencies were reviewed to anchor building activity, energy use, and retrofit direction. For definitions and implementation patterns, we also referred to standards and technical guidance from standards bodies and public building-code resources.

On the supply side, company annual reports, investor presentations, and product catalogs helped separate smart lighting system revenue from adjacent conventional lighting and generic controls. Paid subscriptions were used selectively for company financials and intelligence, patent databases, and shipment-level import and export checks when product mapping across countries was unclear. These desk sources are illustrative rather than exhaustive, since many other public documents were also used for data collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what qualifies as smart lighting in real purchasing and deployment decisions, and on stress-testing pricing and mix assumptions that desk sources do not fully capture. We spoke with a mix of manufacturers, software and platform participants, channel partners, contractors and integrators, and commercial and public buyers, then used inputs across APAC, EMEA, and the Americas to reflect differences in retrofit intensity, codes, and project economics.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 14% | APAC: 51% |

| Mid tier: 40% | Functional/Unit leaders: 40% | EMEA: 30% |

| Smaller Players: 21% | Managers: 46% | Americas: 19% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where demand is reconstructed from construction activity, retrofit cycles, and smart penetration assumptions by end-use and region, then translated into revenue using typical system configurations. Since smart lighting is usually sold as a connected setup rather than a single lamp, the model treats a deployment as a bundle that can include lamps or luminaires, controls, sensors, gateways, and lighting management software when sold with the system.

To keep totals realistic, results are corroborated with selective bottom-up approximations, including sampled ASP times estimated shipment volumes for key connected product groups, plus channel checks on project mix between new build and retrofit. Inputs that matter in this market include the split of new construction versus retrofit, indoor versus outdoor deployments, adoption of connectivity and control protocols (for example Bluetooth, Zigbee, and Matter ecosystems), sensor attachment rates per site, and ASP movement as systems shift from basic control to more software-led management. Forecasting uses scenario analysis supported by expert views on policy push, construction cycles, and retrofit program continuity, and then the final track is chosen where assumptions stay consistent across regions. When bottom-up visibility is weaker in smaller countries, gaps are handled through proxy ratios anchored to lighting stock and building activity, and then re-checked through follow-up conversations.

Data Validation & Update Cycle

Validation is completed through several checks so one data point does not drive the final number. Model outputs are compared against independent signals such as construction spending direction, retrofit program activity, and the expected mix shift toward connected control systems, and then large variances are reviewed by region and end-use before sign-off.

If an anomaly shows up, assumptions are revisited and respondents may be re-contacted to confirm whether the change is structural or data-driven. Reports are refreshed annually, with interim updates for material events such as policy changes or demand shocks. Before delivery, a final analyst pass is completed so clients receive the latest updated view.

Mordor Intelligence's Smart Lighting Market Size Versus Other Published Estimates

Published smart lighting market values can vary a lot, even when the topic name looks the same, because the counted products and the revenue boundary are not always consistent. The year chosen as the starting point and the way software and services are treated can also move the total.

The benchmark table shows a noticeable spread, and in Mordor Intelligence's model the total is built from connected lamps and luminaires plus sensors, gateways, and lighting management software sold for addressable wired or wireless systems, while excluding stand-alone, non-networked LED fixtures that sit outside the smart scope. Differences can also come from how each publisher applies ASP progression over time, the assumed speed of protocol adoption in retrofit-heavy markets, and the refresh timing for currency conversion and regional weighting.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 27.52 B (2026) | |

| Global Research Publisher A | USD 22.45 B (2024) | Uses an earlier base year and a longer forward window, and its component framing can blend smart lighting with broader connected lighting spend, which shifts totals depending on what is treated as a complete system versus a smart-enabled light. |

| Industry Research Publisher B | USD 34.40 B (2025) | Often applies a wider inclusion of hardware, software, and services with less explicit separation from adjacent lighting controls, and the higher starting value can also reflect more aggressive penetration and pricing assumptions ahead of verified retrofit cycles. |

Looking across the three figures, most of the gap is explained by year alignment and by whether non-networked LED lighting and broader control spend gets included in the same bucket. Our method stays tied to clear connected system elements and practical adoption indicators, which makes the number easier to reproduce and update as inputs change.

Key Questions Answered in the Report

What is the projected value of the smart lighting market in 2031?

The sector is forecast to reach USD 67.83 billion by 2031, growing at a 19.77% CAGR.

Which region will post the fastest revenue growth through 2031?

The Middle East is set to expand at a 20.71% CAGR, propelled by sovereign smart-city mandates.

How are utility incentives shaping commercial retrofits?

Rebates covering up to 50% of fixture costs shorten paybacks to as little as 12 months, accelerating adoption.

Why is Bluetooth mesh gaining popularity over Wi-Fi in residential lighting?

Bluetooth mesh removes the need for dedicated gateways, lowers hardware cost, and operates without relying on congested home-router bandwidth.

How do net-zero building codes influence new-construction demand?

Codes enacted since 2025 require networked lighting controls at the design stage, driving a 20.13% CAGR in new-build installations.

What security measures address wireless-protocol vulnerabilities?

Matter’s cryptographic device-attestation and, in critical sites, wired DALI-2 buses mitigate risks uncovered in Zigbee and Bluetooth LE.

Page last updated on: