Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 77.95 Billion |

| Market Size (2026) | USD 81.59 Billion |

| Market Size (2031) | USD 102.51 Billion |

| Growth Rate (2026 - 2031) | 4.67% CAGR |

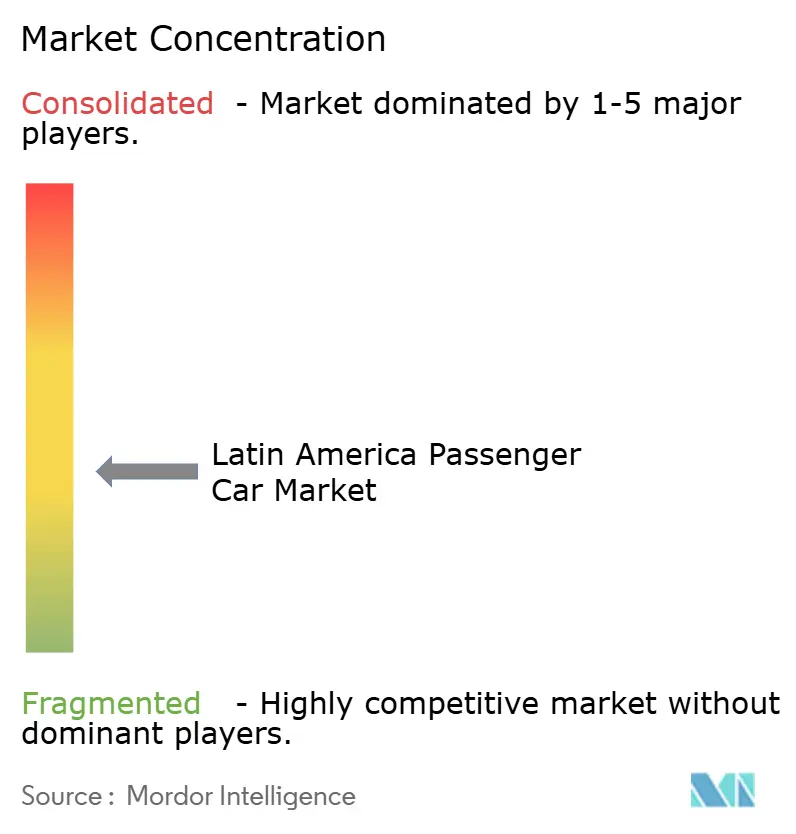

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Latin America Passenger Car Market Analysis by Mordor Intelligence

Latin America passenger car market size in 2026 is estimated at USD 81.59 billion, growing from 2025 value of USD 77.95 billion with 2031 projections showing USD 102.51 billion, growing at 4.67% CAGR over 2026-2031. Robust household demand, accelerating electrification, and on-shoring of vehicle production continue to underpin this growth despite currency volatility and shifting trade policies. Manufacturers are scaling regional plants to comply with USMCA and Mercosur content rules, while government incentives—led by Brazil’s Mover program—stimulate domestic EV output. Chinese brands capitalize on these dynamics with cost-effective models that pressure incumbent OEMs to update product portfolios and pricing strategies. Meanwhile, stabilizing semiconductor supplies restores production rhythm, enabling automakers to address deferred orders accumulated during 2021-2023 shortages.

Key Report Takeaways

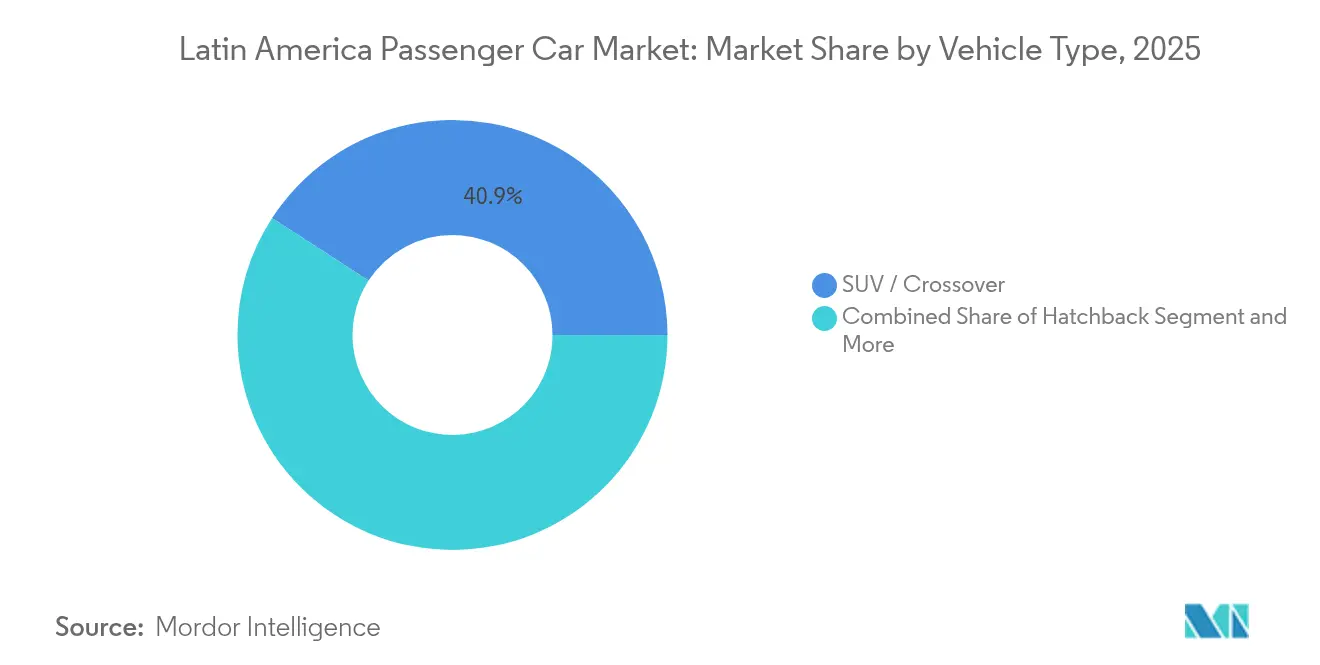

- By vehicle type, SUVs/Crossovers held 40.85% of the Latin America passenger car market share in 2025; the segment is projected to expand at a 4.88% CAGR during the forecast period (2026-2031).

- By vehicle class, entry-level A/B cars accounted for 47.83% share of the Latin America passenger car market size in 2025 and are expected to advancing at a 5.08% CAGR during the forecast period (2026-2031).

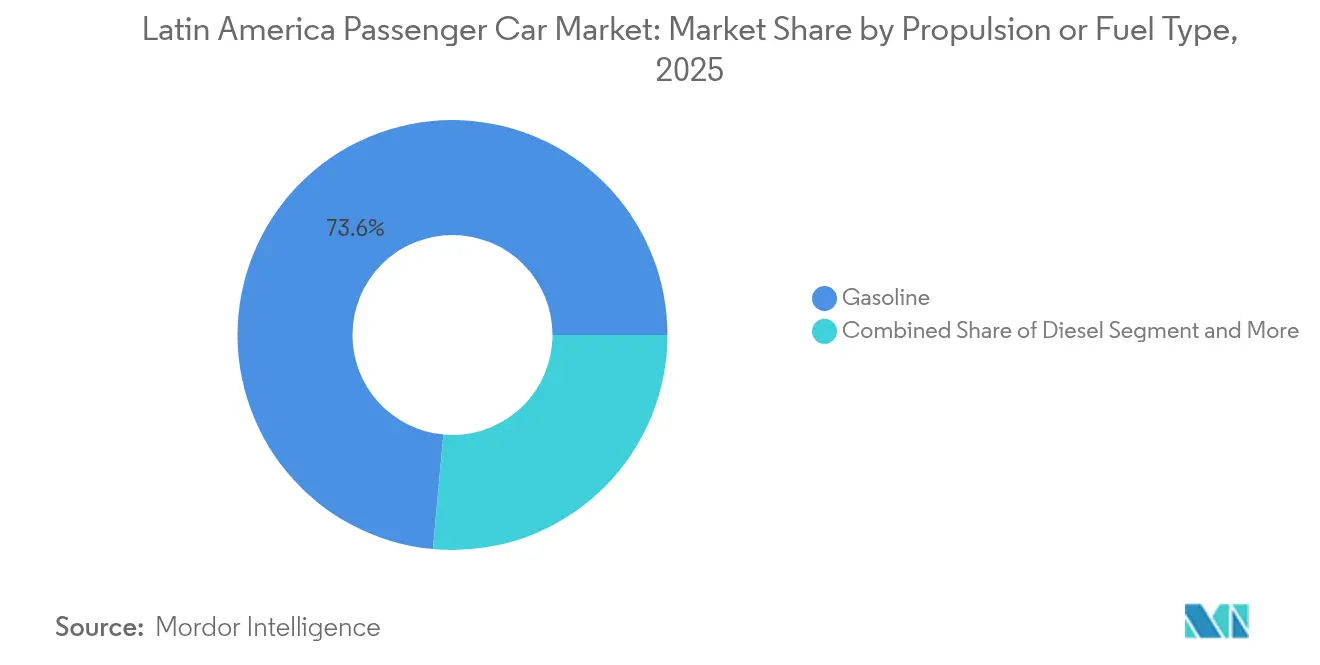

- By propulsion/fuel type, gasoline models commanded 73.55% share of the Latin America passenger car market size in 2025, while battery-electric vehicles is expected to led growth at a 6.78% CAGR during the forecast period (2026-2031).

- By sales channel, independent dealers represented 63.45% of the Latin America passenger car market share in 2025; OEM-owned stores record the highest projected CAGR at 6.05% during the forecast period (2026-2031).

- By country, Brazil captured 47.79% revenue share in 2025, whereas Colombia is expected to posted the fastest trajectory at a 5.55% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Latin America Passenger Car Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Resilient Car Ownership Rebound | +1.2% | Brazil, Mexico, Colombia | Short term (≤ 2 years) |

| Chinese EV Capital Inflow | +1.1% | Region-wide, Brazil and Mexico focus | Short term (≤ 2 years) |

| OEM On-Shoring To Skirt Tariffs | +0.9% | Mexico, Brazil | Long term (≥ 4 years) |

| Automaker Flex-Fuel Programs | +0.8% | Brazil, Argentina | Medium term (2-4 years) |

| EV-Friendly Fiscal Credits | +0.7% | Brazil, Colombia, Chile | Medium term (2-4 years) |

| Stabilizing Semiconductor Supply Chain | +0.6% | Major manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Resilient Post-Pandemic Rebound in Household Car Ownership

As pandemic restrictions eased, personal vehicle ownership saw a notable uptick. This surge was fueled by changing work habits, a diminished reliance on shared mobility, and a notable migration trend towards suburban areas. In Mexico, this shift has led to a pronounced increase in light-vehicle sales, a momentum that's projected to persist into 2025, buoyed by an improving economy. Meanwhile, in Brazil, a recent economic upswing has rekindled consumer confidence, prompting many to make vehicle purchases they had previously postponed. Notably, demand is particularly robust in secondary cities. Here, a limited public transportation infrastructure has resulted in consistent showroom traffic and a sustained appetite for personal mobility solutions.

Rapid Inflow of Chinese OEM Capital and Low-Cost EV Imports

Chinese automakers, bolstered by robust domestic battery supply chains and state-backed financing, are making significant inroads into Latin America. BYD, for instance, has swiftly captured market share in Brazil by localizing its production. This strategy not only sidesteps import tariffs but also allows for more competitive pricing. Following suit, brands like GWM and Chery are amplifying price competition in the region. While this surge in competition offers consumers a wider array of affordable electric vehicle choices, it simultaneously strains established manufacturers, squeezing their profit margins and altering the competitive dynamics.

OEM On-Shoring to Skirt USMCA/Mercosur Tariff Escalation

Trade agreements such as the USMCA and changing Mercosur regulations are pushing automakers to bolster their manufacturing footprint in Latin America. A case in point is Volkswagen's recent investment in Argentina, underscoring the industry's pivot towards platform localization. This strategy not only sidesteps hefty import tariffs but also ensures adherence to regional compliance standards. Such maneuvers highlight a tactical evolution, with global manufacturers striving to harmonize regulatory obligations, cost efficiency, and supply chain robustness. Mexico’s export-oriented plants adjust sourcing mixes to meet 75% regional value requirements, sustaining production even as trade frictions introduce cost uncertainty [1]USTR, “USMCA Rules of Origin for Autos,” ustr.gov. Long-term, diversified regional manufacturing networks should buffer currency swings and improve just-in-time logistics.

Resumption of Automaker Flex-Fuel Investment Programs

Global and domestic automakers are turning to ethanol-capable powertrains as a viable and economical path to decarbonization, leading to significant investments in research and production in Brazil. Major players, including General Motors and Toyota, are pouring resources into the development of ethanol-hybrid technologies and the expansion of local manufacturing. Ethanol's consistent pricing compared to gasoline, coupled with its alignment to forthcoming fuel blend standards, fuels the demand for flex-fuel vehicles. These investments are poised to bolster local supply chains, enhance technological advancements, and pave the way for new export avenues in Mercosur markets. Additionally, the focus on ethanol-capable powertrains aligns with global sustainability goals, further solidifying Brazil's position as a key player in the renewable energy landscape.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Peso and Real Depreciation Inflating Imports | -0.7% | Argentina, Brazil | Short term (≤ 2 years) |

| Accelerating Bus Rapid Transit Expansion | -0.4% | São Paulo, Mexico City, Bogotá, Buenos Aires | Medium term (2-4 years) |

| Limited Public Charging Density | -0.3% | Secondary cities | Long term (≥ 4 years) |

| Tightening 2027 CO₂ Fleet Targets | -0.2% | Brazil, Mexico | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Peso and Real Depreciation Inflating Import Costs

Key Latin American markets are feeling the pinch of macroeconomic pressures, impacting automotive affordability. Brazil grapples with external trade imbalances, and Argentina's industrial capacity remains underutilized, both highlighting broader economic strains. Concurrently, local currency weaknesses are inflating the costs of imported components. In response, automakers are hiking vehicle prices, potentially elongating replacement cycles and curbing demand for non-essential upgrades. Such dynamics could temper growth forecasts and complicate efforts to maintain long-term market expansion.

Acceleration of BRT Expansion in Major Metros

World Bank-sponsored mass transit corridors cut commute times and emissions, making public transport attractive in dense urban cores [2]World Bank, “Latin America Urban Mobility Update 2024,” worldbank.org. Sao Paulo and Bogota are expanding their BRT lanes, aiming to reduce the demand for private cars, especially as parking costs and congestion charges increase. This development is part of broader urban mobility initiatives designed to enhance public transportation infrastructure, alleviate traffic congestion, and promote sustainable transportation alternatives. These measures are expected to encourage a shift toward public transit usage, particularly in high-density urban areas. While the overall regional impact remains modest, it is beginning to dent sales in densely populated areas, signaling a gradual shift in consumer behavior.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: SUVs/Crossovers Extend Leadership

SUVs/Crossovers accounted for 40.85% of the Latin America passenger car market in 2025 and are forecast to outpace all other body styles at a 4.88% CAGR during the forecast period (2026-2031). Buoyed by the increasing availability of sub-compact and B-segment variants, entry prices have seen a decline. Demand is driven by the vehicles' higher ground clearance, making them suitable for unpaved or flood-prone roads, and a prevailing perception of enhanced safety. Toyota's hybrid-flex SUV initiative not only leverages the current ethanol infrastructure but also tackles emissions caps. Meanwhile, Chinese newcomers are introducing feature-rich crossovers, priced similarly to traditional compacts, swaying consumer preference towards these taller vehicles.

Sedans and hatchbacks maintain relevance where urban congestion and fuel economy dominate decision factors, particularly across Brazil’s coastal cities. However, their combined share continues to decline as households upgrade during replacement cycles. Multi-purpose vehicles remain niche, catering mainly to fleet operators and large families in rural areas where passenger capacity trumps efficiency.

By Vehicle Class: Entry-Level Vehicles Retain Primacy

Entry-level A/B models captured 47.83% of the Latin America passenger car market share in 2025, and with a 5.08% CAGR during the forecast period (2026-2031). Driven by competitive financing and governmental tax credits for compact cars. Credit access improvements in Brazil and Mexico expand the eligible buyer pool, while OEMs utilize platform commonality to cut per-unit costs.

Mid-size C-segment offerings cater to an expanding middle class, yet they face substitution risk as consumers transition directly to compact SUVs. Premium D/E classes stay limited to affluent urban professionals and government fleets, although EV variants add a new aspirational layer. BYD’s Dolphin Mini illustrates how low-priced electric compacts can accelerate technology diffusion when paired with tax exemptions.

By Propulsion/Fuel Type: Gasoline Maintains Edge, EVs Surge

Gasoline models remain dominant at 73.55% share in 2025, but battery-electric vehicles exhibit the fastest trajectory at 6.78% CAGR to 2031. As long as charging infrastructure and fiscal incentives remain in place, the market for battery-electric passenger cars in Latin America is poised for growth. In Brazil, flex-fuel powertrains play a crucial role in the automotive fleet, offering protection against fluctuations in oil prices and aligning seamlessly with the nation's agricultural ethanol policies.

Hybrid systems bridge the gap in markets where charging density lags; they satisfy tightening emission caps without demanding new behaviors from drivers. Diesel is relegated to specific utility niches due to elevated fuel taxes and rising NOx standards. OEMs experiment with ethanol-hybrid combinations to meet CO₂ targets while leveraging pre-existing fuel supply chains.

By Sales Channel: Retail Modernization Accelerates

Independent dealers commanded 63.45% share in the Latin America Passenger Car Market in 2025, leveraging local trust and aftermarket services. Nevertheless, OEM-owned outlets are projected to notch a 6.05% CAGR, reflecting automakers’ pursuit of direct consumer data and controlled EV charging experiences. Latin America passenger car market size, attributed to OEM-owned stores, could double by 2030 as brands roll out city-center showrooms with integrated digital configurators.

Traditional dealers defend their share by partnering with Chinese entrants and upgrading service facilities. Multi-brand distributor Inchcape expanded its Latin network through alliances with Geely, BYD, and Chery, bundling financing and insurance to retain traffic.

Online marketplaces remain auxiliary but grow as complementary channels, particularly for used EVs, where transparency on battery health is critical.

Geography Analysis

Brazil dominated the Latin America passenger car market with 47.79% revenue share in 2025, aided by robust local manufacturing, a maturing ethanol ecosystem, and generous incentives for zero-emission vehicles. Brazil is witnessing a surge in electric vehicle adoption, bolstered by an expanding network of public charging stations and supportive tax incentives. Initiatives such as the government's Mover program are drawing significant investments in the automotive sector, with a spotlight on flex-fuel hybrids as pivotal to Brazil's future mobility vision. These endeavors aim to bolster local supply chains and unlock fresh export avenues within Mercosur, cementing Brazil's status as a key player in the regional push for sustainable transportation technologies.

Mexico remains pivotal in North America's vehicle production scene, with most of its output aimed at exports, chiefly to the U.S. While fresh tariffs from the U.S. threaten export volumes, Mexico is mitigating this by luring an increasing number of Chinese component suppliers eager to tap into regional trade agreements. Global automakers, including Audi and BMW, are bolstering local electric vehicle production. Meanwhile, regional governments, notably in Nuevo León, are rolling out incentives to bolster lithium-ion battery manufacturing and fortify domestic supply chains.

Colombia leads growth at a 5.55% CAGR during the forecast period (2026-2031), as fiscal credits boost affordability, and public charging points have jumped since 2022. Eight domestic assembly lines supply taxis and entry-level cars, though parts imports expose the industry to peso swings. Argentina, grappling with economic hurdles like currency depreciation and underutilized factories, remains a magnet for substantial automotive investments, underscoring a steadfast commitment to the industry. Global automakers, through their major programs, are placing their bets on Argentina's local platforms and production prowess. On the other hand, while Chile and Peru may churn out fewer vehicles, they're witnessing steady growth, buoyed by copper sector revenues and a surge in urbanization. Collectively, these developments hint at a regional pivot: bolstering domestic automotive landscapes and broadening market prospects.

Regulatory Landscape

Regulation is fragmented across Latin America, with market entry tied to country-level homologation and safety and emissions compliance rather than a single regional standard. In Brazil, the MOVER (Mobilidade Verde e Inovacao) framework anchors current passenger-car policy, established by Law 14,902/2024 and detailed by Decree 12,435/2025, linking eligibility for incentives and market positioning to measured improvements in energy efficiency and safety, alongside sustainability requirements such as recyclability targets, with implementation milestones beginning June 1, 2025.

Mexico continues to formalize technical compliance through national standards, including NOM-194-SE-2021 for mandatory safety equipment on new light vehicles and NOM-163-SEMARNAT-SCFI-2023 governing CO2 emissions and energy-efficiency limits across model years 2019-2027. In the Southern Cone, Argentina requires model approvals via LCM (Licencia para Configuracion de Modelo) and environmental licensing via LCA, while Uruguay regulates new-vehicle homologation through MIEM under Law 19,061 and Decree 81/014, with administrative updates reflected in a DNI resolution dated December 23, 2024.

Value Chain Analysis

The regional passenger-car value chain is increasingly organized around two anchors: Mexico as an export-oriented manufacturing base tied to USMCA rules of origin, and Brazil as the largest South American production and engineering hub, with flex-fuel expertise and growing electrification localization under MOVER. Vehicle and subsystem sourcing flows are shaped by trade architecture and bilateral arrangements, including the Mexico-Brazil automotive framework under ACE 55, while OEMs and suppliers weigh cost, localization content, and exposure to currency depreciation for imported electronics, powertrain parts, and battery materials.

Recent investment actions point to a shift from import-led sales toward deeper regional assembly and manufacturing. In Brazil, Changan and CAOA started local production of the UNI-T in Anapolis alongside a USD 950 million (R$ 5 billion) 2026-2028 investment cycle, while GWM announced a second plant in Aracruz, Espirito Santo, to expand electrified-vehicle capacity. MG (SAIC) also confirmed local assembly of EV models using SKD kits. Downstream, independent dealers still dominate retailing across much of Latin America, but OEM-controlled formats and structured partnerships with distributor groups are increasingly used to manage pricing, financing, aftersales, and the EV customer experience.

Competitive Landscape

As Chinese automakers penetrate deeper into Latin America's passenger car market, competition is heating up, driven by aggressive pricing and localized manufacturing. BYD's newly established production facility in Brazil underscores the potential of domestic assembly, not only in surmounting trade barriers but also in accelerating market growth, especially in the electric vehicle sector. Meanwhile, Stellantis, a dominant player in South America, is making record investments to craft future models that resonate with regional demands. This changing tableau highlights a pivotal shift in market dynamics, underscoring the importance of innovation, localization, and strategic investments in staying competitive.

Strategic alliances multiply: General Motors and Hyundai plan five jointly developed vehicles aimed at 800,000 annual Latin sales by 2028, leveraging shared platforms to trim R&D costs[3]General Motors, “GM–Hyundai Latin America JV Fact Sheet,” gm.com. GWM has inaugurated a new manufacturing facility in Brazil, a pivotal move aimed at efficiently rolling out HAVAL SUVs. In Latin America, automakers are finding that consumer priorities, like affordability, fuel flexibility, and dependable after-sales service, are taking precedence over luxury features like high-end autonomy. This trend underscores a practical approach to innovation, with companies tailoring their product strategies to resonate with regional demands, thereby carving out a competitive edge through localized value.

Regulatory adherence shapes competitive posture. Brands able to meet PROCONVE L-8 emissions and USMCA content thresholds without price hikes secure durable advantages. Flexible production footprints, electronics sourcing diversification, and resilient logistics capacity emerge as decisive factors in sustaining long-term profitability.

Latin America Passenger Car Industry Leaders

General Motors Company

Volkswagen AG

Stellantis N.V.

Toyota Motor Corporation

Hyundai Motor Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Localized electrified-vehicle manufacturing and hybrid-flex product programs represent a clear whitespace where policy and capital are converging, particularly in Brazil under MOVER. Concrete evidence is visible in the 2026 wave of plant commitments and line launches, with Changan and CAOA commissioning an automated line in Anapolis with a stated 90,000-unit annual capacity and a USD 950 million investment cycle for 2026-2028, and GWM announcing a second industrial plant in Aracruz after establishing production in Iracemapolis. These actions create opportunity for regional suppliers in body, paint, stamping, thermal systems, power electronics, and localization engineering that helps OEMs meet energy-efficiency and safety requirements while reducing exposure to import cost inflation.

Mexico offers an adjacent opportunity in EV-capable upgrades and North America-aligned supply chains, supported by capacity commitments such as Kia citing a USD 600 million investment to upgrade its Pesqueria, Nuevo Leon plant for EV production. Across the region, co-manufacturing and plant-sharing models can speed market entry and portfolio expansion, including arrangements that rely on established industrial footprints in Brazil. Together with the continued dominance of entry-level segments and the shift toward SUVs/crossovers, these developments increase the need for cost-optimized platforms, localized component ecosystems, and dealer and OEM-owned channel capabilities to support electrified and hybrid offerings beyond tier-1 cities.

Recent Industry Developments

- July 2026: Stellantis began production of the Jeep Avenger at the Porto Real Automotive Polo in Rio de Janeiro, Brazil, alongside the opening of a second production shift and new hiring. The move operationalizes a stated R$ 3 billion investment tied to the site and strengthens Stellantis positioning in locally built compact SUVs as electrified and value-focused nameplates expand in the region.

- June 2026: General Motors increased its investment plan for Brazil by announcing an additional R$ 3.5 billion, taking planned spending to R$ 10.5 billion through 2028, aimed at hybrid-powertrain development and plant modernization in Sao Paulo. The expanded capex supports faster regional product refresh cycles and improves competitiveness against newer Asian entrants using aggressive pricing and localized assembly.

- March 2024: Stellantis announced a EUR 5.6 billion (R$ 30 billion) investment program for South America running through 2030. The program underpins regional platform renewal and electrification initiatives and reinforces the scale advantage of established production networks across key Mercosur markets.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the value generated from new passenger car sales across Latin America, counted at the point of sale and expressed in USD for the study timeline.

Scope exclusions: Used car transactions, light commercial vehicles, two wheelers, and heavy trucks are not counted in this market value.

Segmentation Overview

- By Vehicle Type

- Hatchback

- Sedan

- SUV / Crossover

- Multi-Purpose Vehicle (MPV)

- By Vehicle Class

- Entry-Level (A/B)

- Mid-Size (C)

- Full-Size (D/E)

- By Propulsion / Fuel Type

- Gasoline

- Diesel

- Flex-Fuel

- Hybrid Electric Vehicle

- Battery-Electric Vehicle

- By Sales Channel

- OEM-Owned Stores

- Independent Dealers

- By Country

- Brazil

- Mexico

- Argentina

- Colombia

- Chile

- Peru

- Rest of Latin America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by anchoring the demand base using public vehicle registration and parc indicators, along with new vehicle sales and production context for key countries. For this, we rely on sources such as OICA production statistics, UN Comtrade trade flows for vehicles and parts, national statistics bodies and transport ministries in large markets, and central bank releases for inflation and FX assumptions.

To keep the model practical, we also review company annual reports, investor presentations, and OEM and dealer association updates, since they help validate model direction on price, mix, and inventory cycles. Patent databases and reputable journals are used selectively to sanity check the pace of electrification and technology shifts that can change mix faster than volumes. We also use paid subscriptions for company financials and intelligence, along with shipment-level import and export data, to spot breaks in trends that are not obvious in annual summaries. The sources listed here are illustrative, and many additional public and paid references were consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure test the desk assumptions on sales momentum, pricing moves, and mix shifts by body type and propulsion, which can differ across Brazil, Mexico, Argentina, and smaller country markets. We spoke with automaker-facing channel participants, component and logistics stakeholders, and country-level market specialists, so gaps like incentive timing, credit availability, and inventory normalization could be handled before finalizing the numbers.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 19% | |

| Mid tier: 47% | Functional/Unit leaders: 21% | |

| Smaller Players: 19% | Managers: 60% |

Market-Sizing & Forecasting

Sizing is built using a top-down flow where country-level passenger car demand is reconstructed from new sales signals and macro conditions, and then translated into value using observed price and mix behavior. Inputs that matter in this market include new passenger car unit sales by country, shifts across hatchback, sedan, and SUV shares, financing availability and interest rate direction, import reliance versus local production, and FX and inflation pass-through to transaction prices.

After the demand pool is set, we run selective bottom-up checks, such as sampling typical transaction price bands by class and comparing implied revenue against dealer and channel feedback, then adjusting where the mix is clearly shifting. When country data is incomplete for a year, we fill gaps using proxy indicators like registrations, import volumes, and production ramps, and then re-check the implied unit growth against interview guidance.

For forecasting, we use scenario analysis around currency stability, credit cycles, and policy incentives, since these can change affordability and mix quickly. The final trajectory stays consistent with what interviewees expect for the next few years on inventory, pricing discipline, and electrified model introductions, while still being anchored to observable macro and trade indicators.

Data Validation & Update Cycle

Outputs are cross-checked against independent signals such as production and import trends, sales seasonality patterns, and country-level macro consistency, so the totals do not move in ways the real market cannot support. Any large variance triggers an analyst review where assumptions on price, mix, or unit momentum are revisited, and follow-up calls are done when a specific country shows a break from expected direction.

Before sign-off, a second analyst reviews the logic, calculations, and year-to-year movements to catch outliers and to confirm that the same scope rules were applied across countries. The report is refreshed annually, and interim updates are done when material events occur, such as major policy changes or sharp FX moves. Right before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Latin America Passenger Car Market Outlook Market Size Compared Against Other Published Estimates

Published market values for passenger cars in Latin America can differ even when the topic name looks similar, because the counting point, geography set, and price basis are not always aligned. Differences also come from how firms treat inflation, currency conversion timing, and whether they lean more on production, imports, or retail sales as the main demand anchor.

By tracking country-level new passenger car sales and refreshing transaction price and FX assumptions each year, Mordor Intelligence keeps the model tied to retail value only, while some estimates blend in broader automotive categories or apply uniform price growth that does not match local inflation and devaluation patterns.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 77.95 B (2025) | |

| Industry Research Publisher A | USD 70.00 B (2024) | Uses an earlier base year and appears to apply a single regional growth curve, which can understate value in years where inflation and FX pass-through raise transaction prices unevenly by country. |

| Industry Research Publisher B | USD 120.00 B (2032) | Extends the forecast horizon and may assume aggressive penetration and price expansion, and the scope can be wider if adjacent vehicle categories or broader automotive revenue streams are included. |

The spread in the table mostly comes from year selection, boundary choices, and how price and currency are handled across very different national markets. Our approach stays traceable because each country total is built from clear volume signals and then translated to value with local price and FX checks, which makes the result easier to reproduce and defend on a client call.

Key Questions Answered in the Report

What is the forecast value of the Latin America passenger car market by 2031?

The market is projected to reach USD 102.51 billion by 2031.

Which body style leads vehicle demand across Latin America?

SUVs/Crossovers hold the lead with 40.85% share in 2025 and maintain the fastest growth through 2031.

How fast are battery-electric passenger cars growing in Latin America?

Battery-electric models register a 6.78% CAGR from 2026-2031, the highest among all propulsion types.

Which country is the largest contributor to regional passenger-car revenue?

Brazil commands 47.79% of sales thanks to expansive manufacturing and strong flex-fuel infrastructure.

Page last updated on: