Laser Marking Machine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

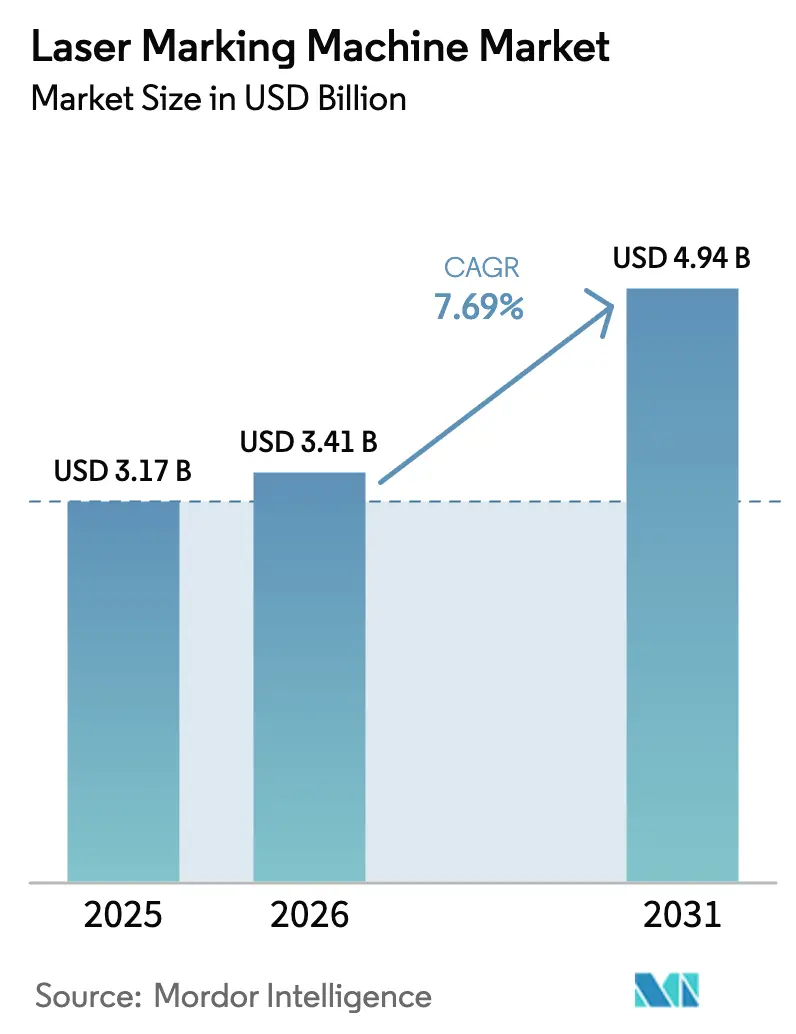

| Market Size (2026) | USD 3.41 Billion |

| Market Size (2031) | USD 4.94 Billion |

| Growth Rate (2026 - 2031) | 7.69% CAGR |

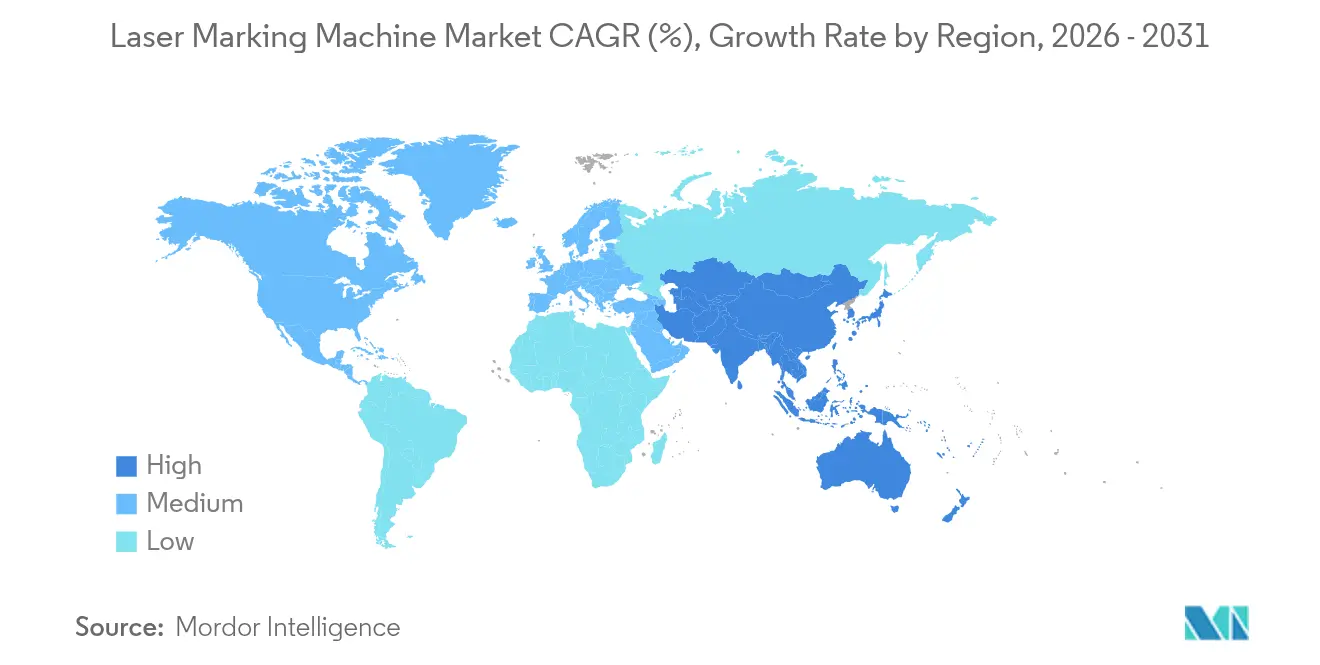

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Laser Marking Machine Market Analysis by Mordor Intelligence

The laser marking machine market size was valued at USD 3.17 billion in 2025 and estimated to grow from USD 3.41 billion in 2026 to reach USD 4.94 billion by 2031, at a CAGR of 7.69% during the forecast period (2026-2031). Demand accelerates because permanent, high-resolution codes have become essential for product traceability, anti-counterfeiting and regulatory compliance in sectors ranging from medical devices to automotive assemblies. Integration with Industry 4.0 smart factories positions each laser workstation as a data-capture node that feeds real-time quality information into manufacturing execution systems. Meanwhile, falling component prices-especially for high-power fiber sources-open the technology to mid-market manufacturers. Asia-Pacific retains a dominant production base for electronics and vehicles, so investments in fast, automated laser lines continue to outpace other regions. On the supplier side, fiber lasers maintain broad appeal for their efficiency and low maintenance, yet UV platforms post the fastest growth as medical, semiconductor and plastics applications call for minimal heat-affected zones.

Key Report Takeaways

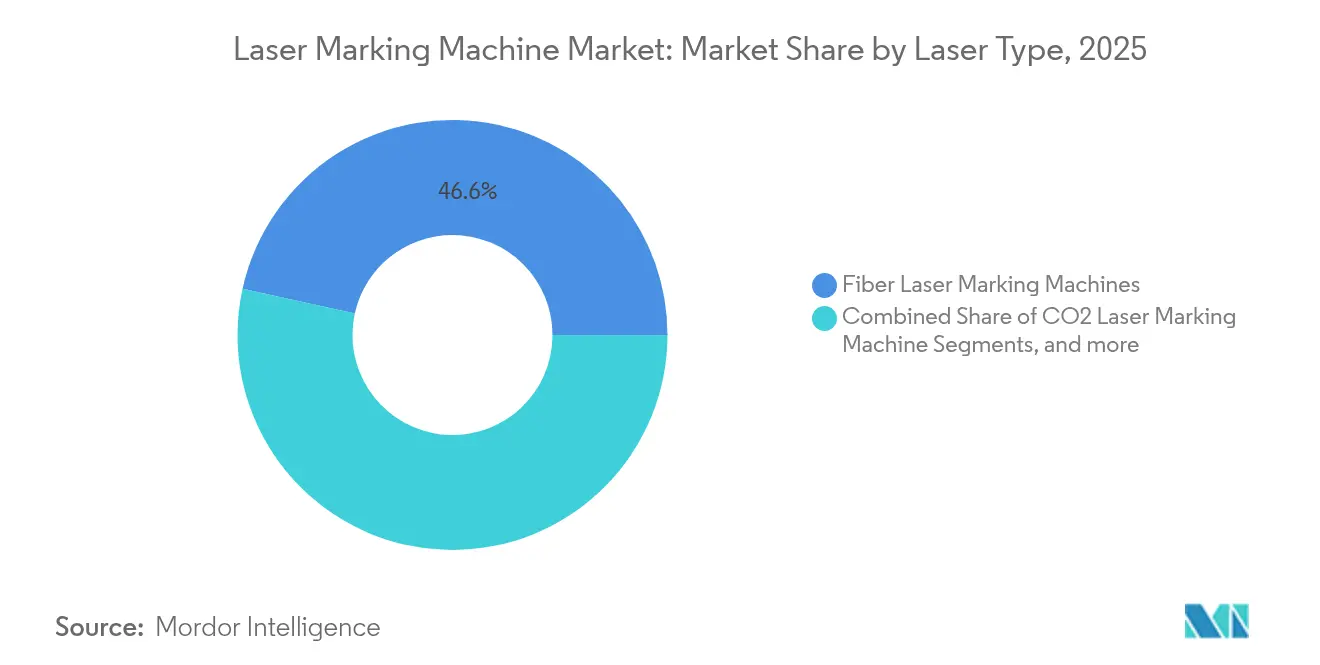

- By laser type, fiber systems led with 46.55% of laser marking machine market share in 2025; UV platforms are projected to grow at a 9.42% CAGR through 2031.

- By end-use industry, automotive captured 24.35% revenue share in 2025, while energy and battery manufacturing is forecast to expand at an 10.72% CAGR to 2031.

- By offering, equipment accounted for 74.45% of the laser marking machine market size in 2025; software is advancing fastest at 11.55% CAGR.

- By power range, 20-50 W units held 38.15% share of the laser marking machine market size in 2025; systems above 100 W show the highest 7.72% CAGR outlook.

- By region, Asia-Pacific controlled 43.65% of the laser marking machine market in 2025 and is pacing at a 8.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Laser Marking Machine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Product traceability and anti-counterfeiting demand | +1.8% | Global, strongest in North America and EU | Medium term (2-4 years) |

| UDI and EU-MDR compliance for medical devices | +1.2% | North America and EU, expanding to APAC | Short term (≤ 2 years) |

| Industry 4.0 smart-factory integration | +2.1% | Germany, Japan, South Korea; spreading worldwide | Long term (≥ 4 years) |

| High-power fiber price erosion | +0.9% | APAC core, spill-over global | Medium term (2-4 years) |

| Asia-Pacific capacity expansion | +0.6% | China, Japan, South Korea | Short term (≤ 2 years) |

| Software-driven automation adoption | +0.5% | Global, with focus in advanced manufacturing economies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing demand for product traceability and anti-counterfeiting

Global regulators clamp down on counterfeit goods, a USD 200 billion problem in pharmaceuticals alone, pushing enterprises toward laser serialization that survives logistics, sterilization and field use.[1]Laser Photonics Corporation, “Laser Photonics Sets Bold Growth Strategy for 2025,” laserphotonics.comAutomotive OEMs engrave codes on engine and brake components so that recalls can be executed in hours rather than weeks, while electronics firms slash warranty investigations by 60% through chip-level ID marks.[2]MECCO, “MECCO Showcases New Automated Marking Technologies at IMTS 2024,” mecco.comSupply shocks from 2020-2024 showed executives the value of granular, always-readable data embedded at the part level, propelling fresh cap-ex across the laser marking machine market.

Regulatory push for UDI and EU-MDR compliance in medical devices

The FDA’s Unique Device Identification rule and the EU-MDR, fully enforced since May 2024, mandate direct, long-lasting codes on reusable surgical tools and implants. UV lasers excel on titanium and stainless surfaces, generating biocompatible marks that remain legible through repeated sterilization cycles.[3]FOBA Laser Marking + Engraving, “White Paper UDI Marking on Medical Devices,” pdf.medicalexpo.comDevice makers report 40% lower compliance cost versus adhesive labels, and multinational firms now harmonize global production lines around laser standards, extending demand beyond Europe and the United States. Post-market surveillance likewise depends on the data embedded in every laser-marked device.

Integration with Industry 4.0 smart factories

Modern laser cells connect to MES platforms that auto-load job files, adjust power settings, and confirm mark quality in real time. Set-up times fall by 75%, and embedded sensors feed predictive-maintenance dashboards that trim unplanned downtime by 30%. Digital-twin models allow engineers to simulate new marks, reducing product launch cycles. Suppliers such as Coherent have released turnkey cells that operate with minimal manual intervention, matching the labor-scarce reality of advanced plants.

Cost reduction from high-power fiber-laser price erosion

Competition among Chinese diode and fiber suppliers drove a 25% year-on-year drop in high-power module pricing in 2024. Mid-sized manufacturers previously limited to dot-peen or inkjet solutions can now afford deep-engraving lasers that run consumable-free. Equipment leasing further lowers barriers, with lease-to-own terms becoming standard for systems priced above USD 50,000.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cap-ex for UV systems | -0.7% | Global, especially SMEs | Short term (≤ 2 years) |

| Talent gap in ultrafast-laser programming | -0.5% | North America and EU | Long term (≥ 4 years) |

| Tight financing amid rising interest rates | -0.4% | Emerging markets | Short term (≤ 2 years) |

| Margin pressure from price competition | -0.3% | APAC and global commodity segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High upfront cap-ex for high-precision UV systems

Premium UV units needed for sub-micron marks often exceed USD 150,000. Compared with fiber or CO₂ platforms that cost 60% less, the longer payback discourages small manufacturers, especially after 2024’s rate hikes lifted financing costs. Leasing helps, yet monthly payments can still surpass the outright price of a basic fiber unit.

Talent gap in ultrafast-laser process programming

Femtosecond and picosecond applications demand specialists who grasp optics, material science and production engineering. Universities graduate too few, and firms report four-month hiring cycles for laser technicians.[4]U.S. Department of Energy, “Basic Research Needs Workshop on Laser Technology 2023 Report,” science.osti.govWithout the right skills, mis-tuned parameters can ruin high-value workpieces, so some manufacturers delay adoption until adequate training programs catch up.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Laser Type: Fiber Dominance Faces UV Challenge

Fiber platforms held 46.55% of the laser marking machine market in 2025 because of high electrical efficiency, compact footprints and virtually maintenance-free operation. CO₂ remains popular on plastics and packaging, but UV systems are projected to post a 9.42% CAGR through 2031 as medical, semiconductor and plastics processors pursue mark quality that avoids heat-affected zones. Fiber suppliers respond by scaling power and refining beam quality to defend share, while UV vendors push cost and reliability improvements that bring premium capability into high-volume plants. The segment’s evolution underscores how end-user demands for miniaturization and material diversity dictate laser-type selection.

Fiber’s influence spreads across automotive VIN engraving, aircraft part identification, and electronics serial-numbering, confirming its role as a production workhorse. Yet applications such as wafer scribing or implant coding favor UV’s cold-processing characteristics. Suppliers therefore broaden portfolios to straddle both regimes, illustrating how the laser marking machine market rewards firms that pair core laser physics with application-specific expertise.

By Power Range: High-Power Systems Drive Innovation

Units rated 20-50 W commanded 38.15% of the laser marking machine market size in 2025 because they balance throughput with modest cooling needs. Systems exceeding 100 W, however, are projected to grow at 7.72% CAGR as automotive and aerospace lines demand deeper engraving and faster cycle times. Suppliers invest in novel two-phase cooling plates that dissipate heat while preserving compact footprints, enabling high duty cycles even in tight factory cells.

For labels on soft polymers or sensitive electronics, sub-20 W platforms remain sufficient, but EV battery housings and turbine blades increasingly require multi-hundred-micron penetration. The resulting segmentation shows users scaling power not merely for speed but to unlock new materials and geometries, reinforcing the strategic link between laser physics and evolving part designs.

By Cooling Method: Water-Cooled Systems Gain Momentum

Air-cooled designs captured 62.35% share in 2025 owing to simple installation and maintenance. Still, water-cooled machines will grow 8.47% annually because high-power beams need tight thermal control to sustain beam quality over long shifts. Closed-loop solutions reduce water consumption, and hybrid air-liquid circuits emerge as a bridge technology that offers higher stability without the plumbing complexity of full liquid systems.

Decision criteria now extend beyond upfront cost to total cost of ownership. In high-utilization environments-battery lines running 24/7, for example-liquid cooling lowers unplanned downtime and consumable fan replacement. Consequently, the cooling choice increasingly correlates with utilization intensity rather than company size.

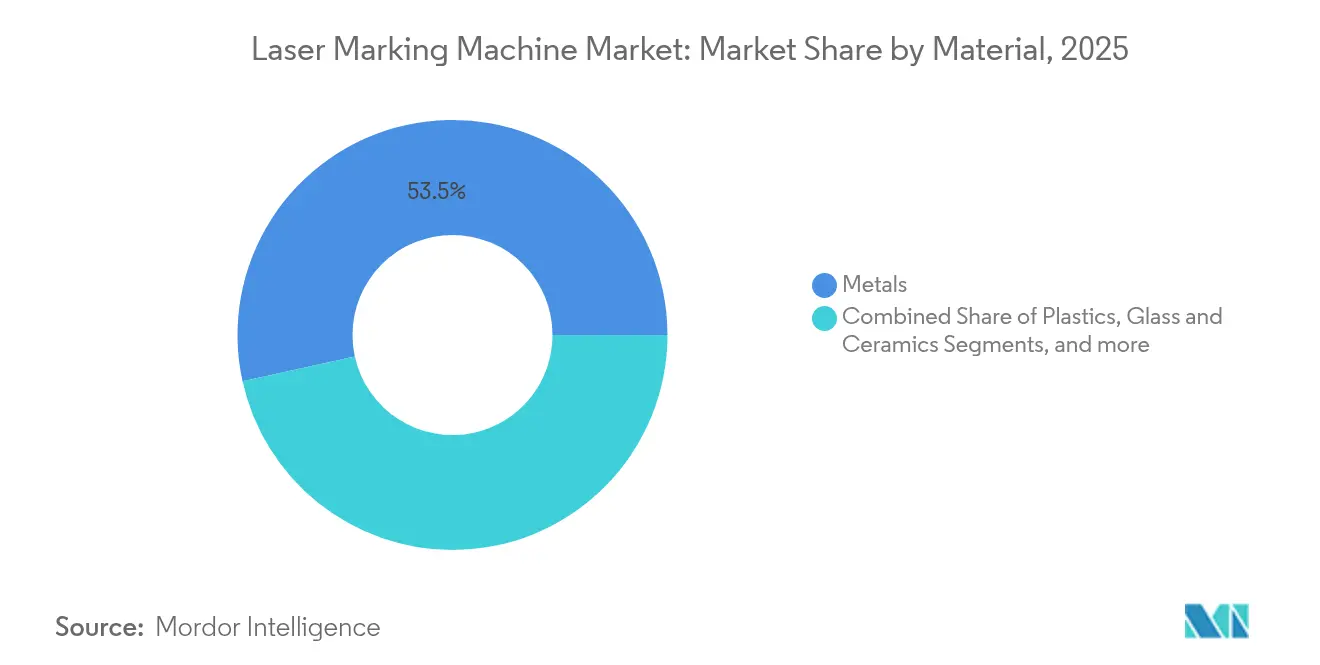

By Material: Plastics Emerge as Growth Driver

Metal substrates still represented 53.45% of revenue in 2025, anchored by steel, aluminum and titanium parts across automotive, aerospace and machinery plants. Plastics, however, will post a 9.11% CAGR to 2031 as laser-markable additives produce sharp, high-contrast codes on polymer packaging that replace solvent-based inkjets. Glass, ceramics and composite materials likewise expand as UV and green lasers enable crack-free marks on brittle or transparent surfaces.

Sustainability regulations accelerate plastic adoption because laser marks eliminate consumables and are recyclable-stream friendly. The trend illustrates how regulatory and environmental pressures can reshape material mixes and, by extension, laser selections that fit each substrate’s optical absorption profile.

By End-Use Industry: Energy Storage Drives Future Growth

Automotive lines contributed 24.35% of revenue in 2025, yet battery and energy-storage plants will outpace all sectors with 10.72% CAGR through 2031. EV cell manufacturers now engrave QR codes on each cylindrical, pouch or prismatic cell to enable lifetime tracking. Semiconductor packaging, medical devices and aerospace also maintain solid demand as each field embeds traceability deeper into quality frameworks.

The convergence of electrification and stricter warranty management ensures that battery makers will keep investing in fast, automated, and dust-resistant laser workstations. These specialized environments value closed, Class 1 laser cabinets with integrated fume extraction, reinforcing the premium placed on turnkey design expertise.

Geography Analysis

Asia-Pacific held 43.65% of the laser marking machine market in 2025 and is projected to grow 8.95% annually through 2031. China’s electronics and automotive hubs invest in high-throughput, integrated laser islands to support export-oriented production. Japan’s precision engineering culture fuels demand for ultrafast and UV variants that address semiconductor wafers and medical implants. South Korea’s display and battery giants similarly drive adoption, supported by national Industry 4.0 incentives that subsidize smart-equipment upgrades.

North America remains a steady adopter as reshoring policies and FDA UDI enforcement sustain capital budgets for new cells. U.S. automakers, having weathered chip shortages, now emphasize part traceability to mitigate future disruptions, while Mexico’s tier-1 suppliers deploy lasers to ensure seamless customs compliance for cross-border assemblies.

Europe posts moderate growth anchored in Germany’s advanced-manufacturing base and the EU’s sustainability agenda. The EU-MDR spurs hospitals and suppliers to demand biocompatible marks, and automotive electrification efforts stimulate battery-component coding. Brexit-triggered documentation requirements have further highlighted the value of durable, machine-readable marks that speed border procedures.

Competitive Landscape

The supplier base is moderately fragmented. IPG Photonics, TRUMPF and Coherent leverage vertical integration, controlling laser-diode production, resonator design and system-level assembly. IPG reports 87.7% of 2024 revenue from materials processing, affirming its dominance in fiber sources. TRUMPF combines lasers with automated handling, while Coherent’s wider photonics portfolio enables cross-selling into adjacent processes such as welding.

Growth strategies increasingly hinge on software differentiation and vertical solutions. Laser Photonics’ acquisition of Control Micro Systems broadened reach into medical and pharmaceutical niches, while MECCO and United Winners Laser showcase turnkey cells aimed at battery-cell makers. Chinese entrants keep prices low, squeezing margins but also expanding the addressable customer base.

M&A activity is expected to continue as firms pursue scale and complementary IP, yet the interplay of price erosion and software value will determine who secures premium positioning.

Laser Marking Machine Industry Leaders

Han's Laser Technology Industry Group Co., Ltd.

Telesis Technologies, Inc.

Videojet Technologies Inc.

Trotec Laser GmbH

Epilog Laser Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Laser Photonics’ Control Micro Systems won a robotic dental-bit marking order from a global implant provider, highlighting specialized medical growth.

- January 2025: Laser Photonics announced a USD 1 million Control Micro Systems acquisition and unveiled a growth plan aimed at double-digit medical and pharma CAGR

- October 2024: The Battery Show USA spotlighted automated laser welding and marking as the emerging standard for lithium battery production lines.

- August 2024: MECCO unveiled LightWriter PRO Connect automation-ready workstations featuring multi-option software suites at IMTS 2024.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the laser marking machine market as factory-built systems that employ fiber, CO2, UV, green, or solid-state beams to produce permanent alphanumeric, 2-D code, or graphic marks on metals, plastics, glass, ceramics, and silicon; sales of integrated software and essential services are counted alongside equipment.

Scope exclusion: We purposely leave out laser cutting, welding, engraving platforms, and all handheld inkjet or thermal coding units.

Segmentation Overview

- By Laser Type

- Fiber Laser Marking Machines

- CO2 Laser Marking Machines

- UV Laser Marking Machines

- Green Lasers

- Solid-state Nd:YAG Lasers

- By Power Range

- Less than 20 W

- 20-50 W

- 50-100 W

- Higher than 100 W

- By Cooling Method

- Air-Cooled

- Water-Cooled

- By Material

- Metals

- Plastics

- Glass and Ceramics

- Semiconductor and Silicon

- Other Materials

- By End-use Industry

- Automotive

- Electronics and Semiconductor

- Machine Tool and Heavy Engineering

- Aerospace and Defense

- Medical and Healthcare Devices

- Packaging and FMCG

- Energy and Battery Manufacturing

- Jewelry and Artisanal

- Other Industries

- By Offering

- Equipment

- Software

- Services

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Australia and New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- GCC

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed machine tool distributors, automation integrators, regulatory auditors, and maintenance contractors across Asia-Pacific, Europe, and North America. These conversations tested duty-cycle assumptions, average selling prices, retrofit ratios, and the real pace of migration from ink-based coders, helping us close gaps flagged during desk analysis.

Desk Research

We began with open datasets from bodies such as the United States Census Bureau, Eurostat Prodcom, China Customs HS 8456 exports, and the Laser Institute of America, which outline output volumes, trade flows, and adoption rules. Standards documents (ISO / IEC 15459 serialization, EU-MDR, UDI) clarified the compliance triggers that push machine demand, while company 10-Ks, investor decks, and patent families retrieved through Questel revealed pricing falls for high-power fiber sources. D&B Hoovers and Dow Jones Factiva added revenue splits for leading OEMs, letting us cross-check channel mix. This list is illustrative; many other secondary sources informed our desk work.

Market-Sizing & Forecasting

A top-down build starts with production and trade statistics to size annual unit flows and is then balanced through selective bottom-up checks using sampled ASP × volume rolls from tier-1 vendors. Variables such as fiber-laser price erosion, automotive light-vehicle output, Industry 4.0 capital-expenditure indices, mandatory device serialization deadlines, and regional purchasing manager indexes feed a multivariate regression that projects demand to 2030. Where channel data lag, we align totals to installed-base growth revealed in field interviews before locking the baseline.

Data Validation & Update Cycle

Outputs pass two-layer analyst review, variance tests against independent indicators, and automated anomaly flags. Reports refresh each year; material events, major regulation or supply disruption, trigger interim reruns, ensuring clients see the latest view before delivery.

Why Mordor's Laser Marking Machine Baseline Commands Reliability

Published estimates rarely match because firms choose different scopes, price ladders, and refresh cadences. We set expectations early, explaining every inclusion and exclusion so buyers know exactly what our 3.17 billion-dollar 2025 value covers.

Key gap drivers include whether secondary processes (engraving, cutting) are bundled, the treatment of software revenues, and how gray-market Asian suppliers are counted; Mordor's disciplined definition, annual refresh, and dual-path modeling resolve these variances.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.17 B (2025) | Mordor Intelligence | |

| USD 3.22 B (2024) | Global Consultancy A | Adds handheld coding units and hybrid laser modules, expanding scope |

| USD 3.17 B (2023) | Industry Association B | Uses shipment data only and omits software, narrowing coverage |

| USD 3.03 B (2024) | Trade Journal C | Excludes tier-2 Asian OEMs, undercounting volume |

Taken together, the comparison shows that when scope creep or omission is removed, our balanced, source-traceable baseline stands as the dependable reference point for strategic planning.

Key Questions Answered in the Report

What is driving the rapid growth of the laser marking machine market in Asia-Pacific?

The combination of expanding electronics and EV production in China, Japan and South Korea, plus government Industry 4.0 subsidies, gives the region 43.65% share and a 8.95% CAGR outlook.

Why are UV laser systems the fastest-growing type?

Medical devices, semiconductors and plastic packaging require cold processing that UV beams deliver, supporting a 9.42% CAGR for UV units through 2031.

How is software changing competitive dynamics?

Software revenues are rising 11.55% annually as factories adopt predictive analytics, remote diagnostics and MES integration that add value beyond the initial hardware sale.

Which end-use sector will add the most new installations?

Battery and energy-storage plants are forecast to grow 10.72% per year because each lithium cell now needs a durable, high-contrast code for lifecycle tracking.

What remains the biggest barrier for small and midsize enterprises?

The initial cost of high-precision UV equipment, often above USD 150,000, combined with limited financing options, slows adoption among SMEs.

How permanent are laser-applied marks compared with labels or inkjet codes?

Laser marks are etched or ablated directly into the substrate, making them resistant to abrasion, heat, chemicals and sterilization cycles, thereby outperforming adhesive labels and solvent inks in durability.

Page last updated on: