Managed Print Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

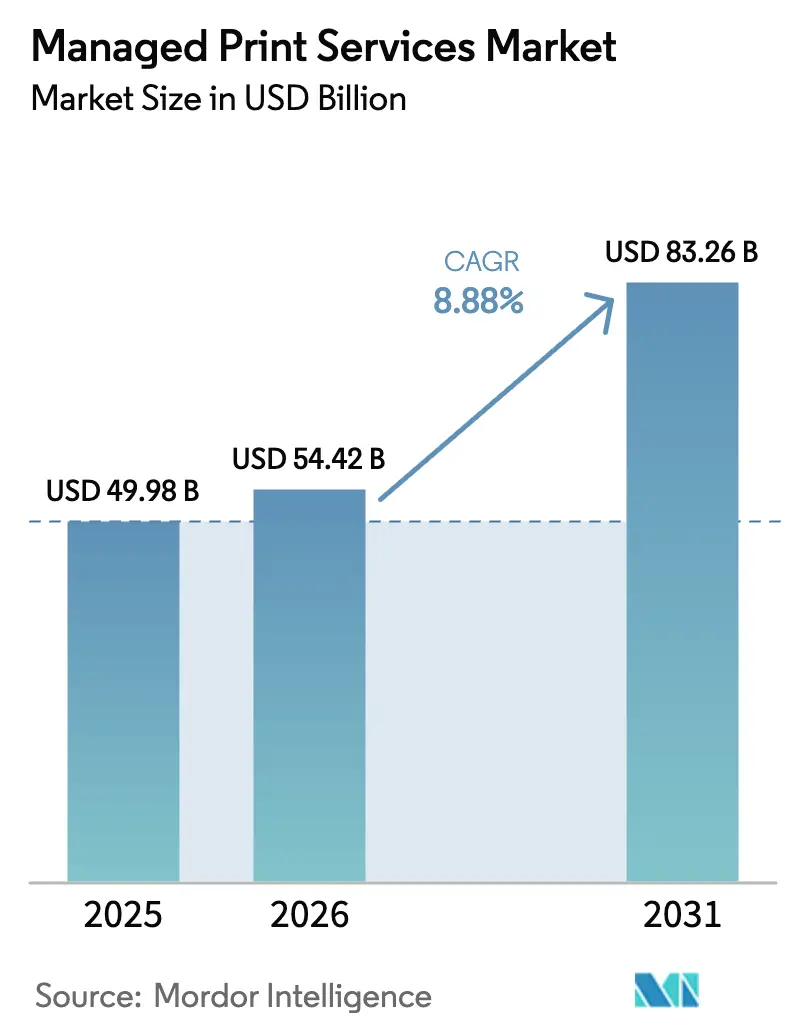

| Market Size (2026) | USD 54.42 Billion |

| Market Size (2031) | USD 83.26 Billion |

| Growth Rate (2026 - 2031) | 8.88% CAGR |

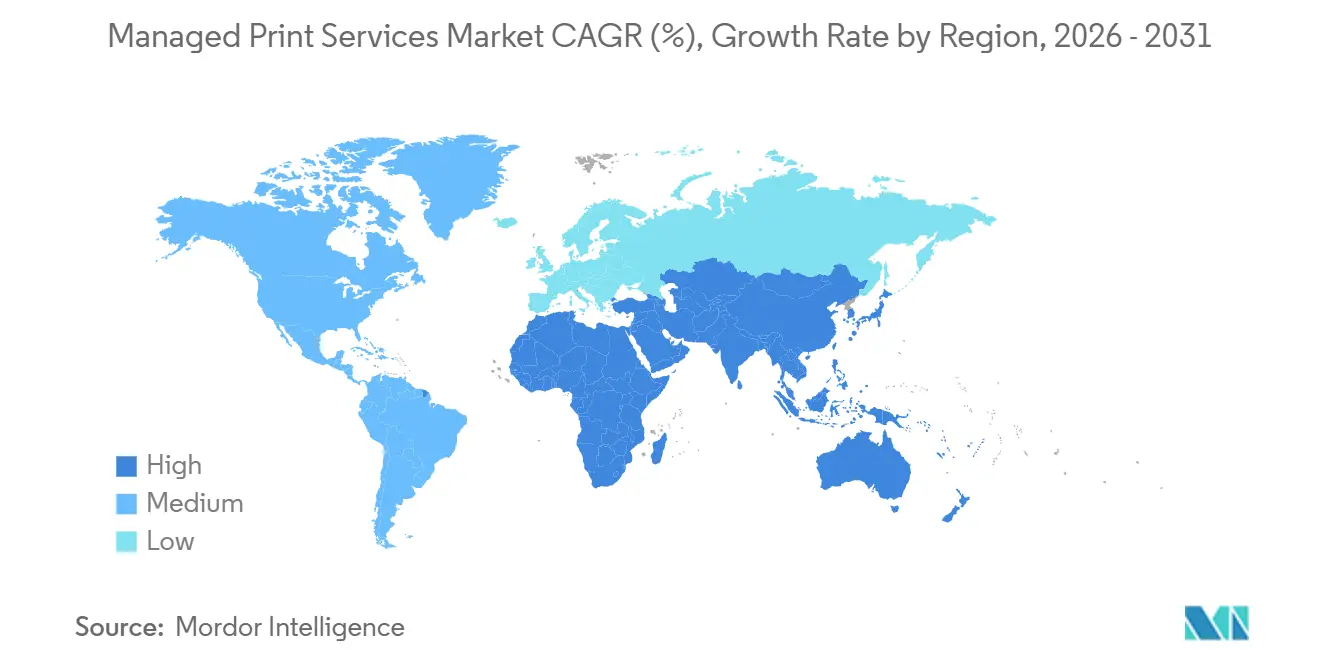

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Managed Print Services Market Analysis by Mordor Intelligence

The Managed Print Services market size reached USD 54.42 billion in 2026 and is forecast to advance to USD 83.26 billion by 2031, registering an 8.88% CAGR over 2026-2031. The headline expansion reflects the shift from capital-intensive device ownership toward subscription models that blend predictive analytics, zero-trust security, carbon accounting, and real-time fleet orchestration. Growth momentum stems from higher per-seat spending on compliance automation, anywhere-access printing, and usage-based provisioning rather than from rising page counts, which remain on a structural decline. Cloud-native architectures now dominate new installations because they let IT leaders extend secure print to hybrid workforces without on-premise servers, while analytics-driven uptime guarantees reduce unplanned outages. Competitive dynamics are changing as independent software vendors (ISVs) disaggregate OEM-centric value chains, and sustainability mandates create premium demand for page-level emissions tracking.

Key Report Takeaways

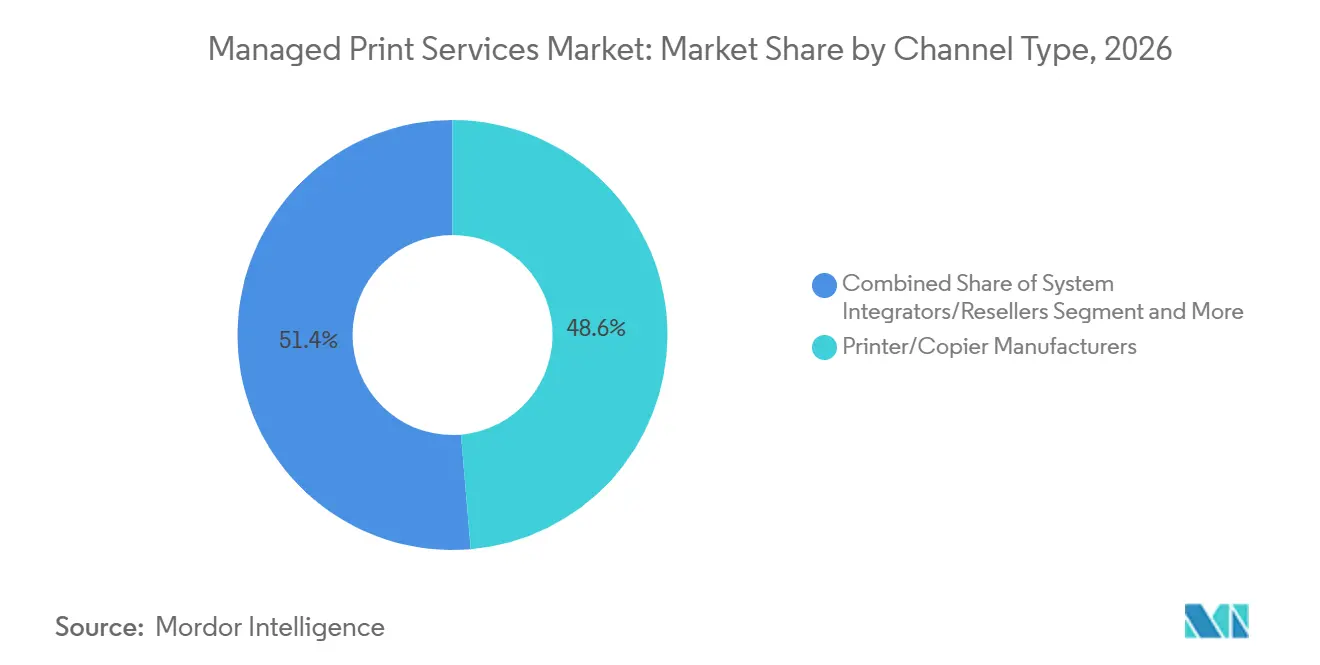

- By channel type, printer and copier manufacturers accounted for 48.64% of 2025 channel revenue, whereas independent software vendors are expanding at a 10.24% CAGR through 2031.

- By service type, managed print operations contributed 35.54% of 2025 service-type revenue, yet cloud print services post the fastest trajectory at a 9.22% CAGR to 2031.

- By deployment mode, cloud-based deployment models represented 64.78% of 2025 installations and are projected to grow at 10.56% annually through 2031.

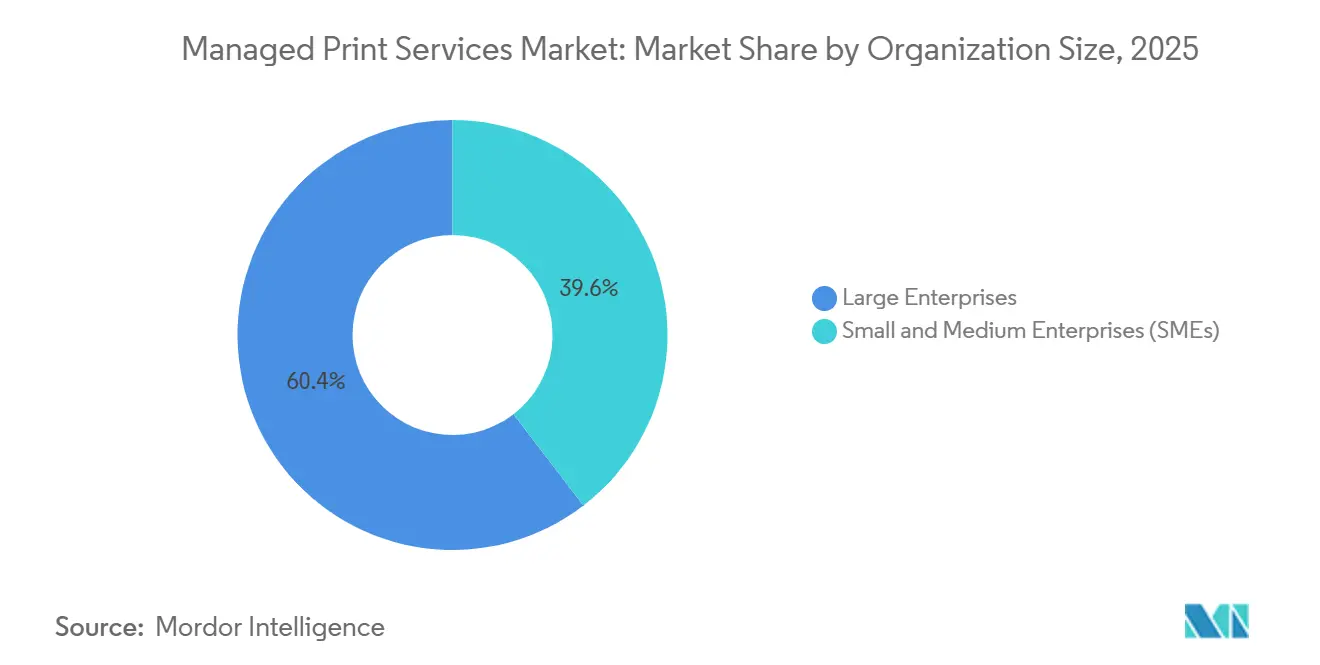

- By organization size, large enterprises captured 60.42% of 2025 spending, but small and medium enterprises are forecast to grow at a 9.56% CAGR over the outlook period.

- By vertical, healthcare generated 24.44% of 2025 vertical revenue, while education is advancing at a 9.02% CAGR to 2031.

- By geography, North America held 40.78% of 2025 geographic revenue, whereas Asia Pacific is on track for a 10.48% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Managed Print Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Remote Work Print Infrastructure Optimisation Driving MPS Adoption in North America | +1.8% | North America, Europe | Medium term (2-4 years) |

| Sustainability and Carbon Footprint Mandates Accelerating EU Corporate MPS | +1.5% | Europe, Global spillover | Long term (≥ 4 years) |

| Subscription-Based Everything-as-a-Service Adoption Among SMEs | +1.6% | Global, with concentration in North America and Asia Pacific | Short term (≤ 2 years) |

| Print-Device Security and Compliance Requirements in Regulated Sectors | +1.4% | Global, especially North America and Europe | Medium term (2-4 years) |

| IoT-Enabled Fleet Analytics Reducing Downtime in Large Asian Enterprises | +1.2% | Asia Pacific core, spillover to Middle East and Africa | Medium term (2-4 years) |

| Generative-AI-Driven Predictive Maintenance and Auto-Replenishment | +1.0% | Global, early adoption in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Remote Work Print Infrastructure Optimisation Driving MPS Adoption In North America

Hybrid work models fragmented device footprints across homes, co-working sites, and partially occupied headquarters, forcing IT departments to swap static fleets for usage-based provisioning. Secure print release, identity-aware access, and VPN-free job submission became baseline requirements, repositioning the Managed Print Services market as a security solution rather than a cost-center. Xerox’s Virtual Print Management service allows workers to send a job from any location and collect it at the nearest authenticated device, eliminating on-premise servers and bespoke VPN tunnels.[1]Source: Xerox Corporation, “Virtual Print Management,” xerox.com Enterprises now value zero-trust print architecture and on-demand capacity rightsizing, which explains why cloud-based contracts command premium seat fees while still outpacing the overall growth curve.

Sustainability And Carbon Footprint Mandates Accelerating EU Corporate MPS

The European Union’s Corporate Sustainability Reporting Directive compels companies with over 250 employees to disclose Scope 3 emissions, including those from printing, starting in 2025.[2]European Commission, “Corporate Sustainability Reporting Directive,” europa.eu Print fleet management therefore shifted into the compliance domain. Ricoh reported that 36% of its Office Services clients subscribed to carbon-accounting modules in 2025, a 10-point leap year-over-year, and expects sustainability-linked contracts to exceed 50% of new European bookings by 2027.[3]Ricoh Company, “Integrated Report 2025,” ricoh.com Procurement guidelines in Germany, France, and the Nordic region now prefer providers that supply page-level emissions data, effectively sidelining vendors lacking granular telemetry.

Subscription-Based Everything-As-A-Service Adoption Among SMEs

Small and medium enterprises lack dedicated IT staff, so they prioritize turnkey subscriptions that bundle hardware, software, security, and auto-replenishment. PaperCut’s Hive platform scales per active user and eliminates on-premise servers, expanding to 70,000 organizations by 2025 with SMEs as the fastest cohort.[4]PaperCut Software, “About PaperCut,” papercut.com For these firms, value resides less in per-page cost savings and more in outsourcing complexity. Vendors that offer frictionless onboarding, user-friendly interfaces, and month-to-month pricing are capturing disproportionate share of the Managed Print Services market.

Print-Device Security And Compliance Requirements In Regulated Sectors

Healthcare, finance, and government agencies face steep fines for data breaches involving printed documents. The U.S. Department of Health and Human Services recorded 133 HIPAA enforcement actions in 2025, some linked to unsecured printer hard drives. HP embeds biometric authentication, data-in-transit encryption, and automatic memory wiping into its Managed Print Services package, aligning with HIPAA, GDPR, and ISO 27001 mandates. Heightened regulatory scrutiny means secure-by-design fleets are now non-negotiable, positioning security as a growth catalyst across the Managed Print Services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining Office Print Volumes Amid Digital Transformation | -1.2% | Global, most pronounced in North America and Europe | Long term (≥ 4 years) |

| Data Sovereignty Concerns Hindering Cloud-Based MPS | -0.8% | Asia Pacific, Middle East, selective European markets | Medium term (2-4 years) |

| Vendor Lock-In Perception and Contract Complexity Discouraging SMEs | -0.6% | Global, particularly acute in SME segment | Short term (≤ 2 years) |

| Complexity of Edge Zero-Trust Print Architectures | -0.5% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Declining Office Print Volumes Amid Digital Transformation

Companies in mature economies cut office print usage by up to 20% between 2020 and 2025 as e-signatures, electronic invoicing, and cloud collaboration displaced paper workflows. Lower page counts erode per-click revenue models embedded in legacy contracts, forcing providers to pivot toward value-added modules such as workflow automation and compliance dashboards. Vendors that cling to volume-based billing risk margin compression even as the need for secure fleet oversight increases across the Managed Print Services market.

Data Sovereignty Concerns Hindering Cloud-Based MPS

National data-localization statutes in China, India, and parts of the Middle East require that print-job metadata stay within borders, limiting adoption of hyperscaler-hosted services. Global providers must either fund regional data centers or partner with domestic infrastructure firms, extending payback periods and complicating go-to-market plans. Until these sovereignty hurdles ease, a sizable share of Asia Pacific customers will retain on-premise or hybrid deployments, tempering growth in the region’s otherwise high-velocity Managed Print Services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Channel Type: ISVs Disrupt OEM Dominance

Independent software vendors erode incumbent share by selling cloud-first, vendor-agnostic platforms that manage fleets spanning HP, Canon, Xerox, Ricoh, and more. Printer and copier makers still generated the largest 2025 channel contribution, but the ISV cohort is outgrowing the total Managed Print Services market by more than one percentage point annually. The Xerox-Lexmark acquisition underscored OEM urgency to acquire software muscle, while Canon’s subscription-bundled imageFORCE suite tries to lock mid-market buyers into vertically integrated stacks. Still, large enterprises with heterogeneous fleets gravitate toward ISVs that reduce switching costs and accelerate feature rollouts. As a result, OEM service attach rates are slipping, and channel alliances between resellers and ISVs are proliferating to defend relevance.

ISVs differentiate through rapid cloud releases, open APIs, and analytics that benchmark utilization across mixed fleets, feeding continuous improvement loops. OEMs counter with device-embedded telemetry and hardware-software bundles, but price-to-value gaps remain. Enterprises recognize that renewal flexibility outweighs vendor homogeneity, pushing the Managed Print Services market toward a bifurcated structure. Vendor-agnostic orchestration appeals to global corporations that centralize governance, while integrated OEM suites still resonate with single-brand midsize operations seeking one-throat-to-choke accountability. Competitive intensity will deepen as hyperscaler marketplaces make independent print-management apps discoverable to IT buyers worldwide.

By Service Type: Cloud Print Services Outpace Traditional Operations

Cloud Print Services are expanding faster than the overall Managed Print Services market, bolstered by Microsoft Universal Print becoming the de facto enterprise standard. Managed Print Operations retain sizeable share because they encompass device monitoring and break-fix support, but cloud delivery models remove on-premise server costs and shrink deployment cycles from weeks to hours. Universal Print integration cuts driver management overhead for IT departments and unlocks secure printing for remote employees without VPN configurations.

Document workflow optimization, though the smallest current revenue pool, unlocks structural savings by automating capture, routing, and archiving. Konica Minolta’s AI-enabled Workplace Hub trims redundant prints and reduces processing time for HR and finance documents, illustrating the pivot from device management to process transformation. Providers that marry fleet analytics with workflow re-engineering can decouple earnings from declining page volumes and defend margins, a critical maneuver as print counts fall yet complexity rises across the Managed Print Services market size.

By Deployment Mode: Cloud-Based Models Dominate New Installations

Cloud-based deployments already constitute nearly two-thirds of active contracts and are outgrowing on-premise counterparts by two full percentage points annually. Elastic consumption converts fixed capital outlays into variable expenses, aligning spend with headcount fluctuations and remote-work patterns. SMEs embrace per-user pricing that sidesteps server acquisition and maintenance, while global enterprises value centralized policy enforcement and real-time analytics.

On-premise and hybrid models persist where data-localization or ultra-low-latency mandates apply, especially in banking and government. Even in those sectors, analytics dashboards and reporting layers commonly run in the cloud, creating mixed environments. Vendors that lack native multi-tenant architectures face upgrade headwinds, as customers reject lift-and-shift retrofits. Consequently, cloud-ready platforms increasingly win competitive tenders, reinforcing the Managed Print Services market share advantage of early movers.

By Organization Size: SMEs Accelerate Adoption Via Subscription Models

Large enterprises still drive absolute revenue because of massive, multisite fleets, but SMEs represent the fastest incremental dollar growth. Subscription bundles reduce procurement friction and sidestep multiyear commitments, so adoption accelerates even when per-page pricing exceeds self-managed alternatives. Brother’s compact MFC-L9670CDN, paired with optional cloud fleet management, embodies this SME-targeted value proposition.

Enterprise buyers focus on economies of scale, central governance, and global SLAs, while SMEs covet simplicity and predictable monthly bills. ISVs fine-tune onboarding wizards and self-service portals that require no training and deliver near-instant fleet visibility. As SME word of mouth spreads, the Managed Print Services market size for the segment is forecast to expand at a 9.56% CAGR, outpacing the corporate tier even as absolute dollars remain lower.

By End-User Vertical: Healthcare Leads, Education Accelerates

Healthcare’s strict HIPAA environment drives adoption of encrypted print workflows, secure release, and audit trails that track every page. HP, Xerox, and Ricoh market specialized offerings with built-in compliance dashboards, helping hospitals avoid regulatory penalties. Healthcare’s share leadership anchors the Managed Print Services market size in regulated sectors, while document-intensive workflows keep page volumes relatively resilient.

Education’s nine-percent CAGR stems from mobile student populations and tight budgets that favor cloud-hosted print servers. Universities deploy pull-print solutions so students release jobs at any campus device, trimming abandoned print waste. BFSI, government, manufacturing, and retail add steady demand but with distinct drivers: zero-trust security for banks, data localization for public agencies, IoT uptime guarantees for factories, and cost control for retailers. Providers tailoring vertical modules enjoy higher renewal rates and cross-sell margins across the Managed Print Services market.

Geography Analysis

North America generated the largest 2025 revenue thanks to early hybrid-work adoption and stringent cybersecurity mandates. Enterprises value zero-trust prints and advanced analytics, lifting average revenue per user above the global mean. Canada mirrors U.S. patterns, while Mexican corporations modernize fleets as part of near-shoring manufacturing expansions.

Asia Pacific, however, is the fastest-growing region with a 10.48% CAGR. Chinese, Indian, Japanese, and South Korean manufacturers integrate IoT telemetry to minimize downtime, directly linking printer availability to production throughput. Local data-sovereignty laws slow pure cloud adoption but boost hybrid deployments supported by regionally hosted analytics. Government digitization agendas in India and smart-factory incentives in China further elevate demand, solidifying the region’s outsized contribution to Managed Print Services market growth.

Europe’s trajectory hinges on carbon-accounting regulations. German, French, and Nordic enterprises embed lifecycle emissions tracking into vendor scorecards, rapidly expanding contracts that include sustainability dashboards. The Middle East and South America log steady, mid-single-digit expansion as digital government programs and corporate modernization projects unfold. Africa remains nascent yet opportunity-rich for vendors willing to offer low-capex subscription bundles that accommodate infrastructure variability. Collectively, these dynamics diversify revenue sources and hedge currency exposure for global providers in the Managed Print Services market.

Regulatory Landscape

Managed print services (MPS) procurement is increasingly shaped by security, privacy, and public-sector contracting requirements. In regulated industries, providers align device, workflow, and cloud controls with frameworks such as HIPAA (45 CFR 164.312) for protected health information and the FTC Safeguards Rule (16 CFR Part 314) for financial institutions. This raises expectations for encryption and auditability across scan-to-email and print-release workflows. For cloud-delivered MPS used by U.S. federal agencies and contractors, FedRAMP Authorization to Operate (ATO) and continuous monitoring obligations tied to NIST SP 800-53 have become a gating criterion in sourcing decisions.

Standardization is also tightening at the device-security layer. ISO/IEC 7184:2024 sets baseline security requirements for hard copy devices, including identification and authentication and software update controls, reinforcing secure-by-design expectations for printers and multifunction devices managed under MPS contracts. On the procurement side, the U.S. Government Publishing Office (GPO) continues to govern federal print contracting through its Printing Procurement Regulations (PPR) and Materials Management Acquisition Regulation (MMAR); GPOExpress program documentation updates effective May 1, 2026 reflect ongoing modernization of print-on-demand processes that influence how qualifying vendors structure compliance, job specifications, and fulfillment workflows.

Value Chain Analysis

The MPS value chain begins with OEMs supplying printers/MFPs, embedded firmware, parts, and consumables, and then extends into software layers such as print management, secure release, fleet telemetry, and workflow automation delivered by OEM platforms and independent software vendors. System integrators, resellers, and managed service providers assemble these components into contracted offerings by adding assessment, device deployment, monitoring, break-fix, supplies logistics, help desk, and reporting. Cloud infrastructure and identity ecosystems (for example, directory services and zero-trust access) sit upstream of cloud print services, while security and sustainability specialists contribute controls such as encryption, audit trails, and page-level emissions tracking that increasingly affect vendor selection.

Execution and margin performance depend on logistics and data visibility across distributed fleets. Bottlenecks often stem from fragmented procurement across sites, inefficient distribution and field-service routing, high inventory carrying costs for consumables and spares, and weak utilization telemetry that can drive over-provisioning. The chain is shifting from reactive device maintenance toward AI-assisted predictive maintenance, remote diagnostics, and centralized portals that connect device signals to automated replenishment and service dispatch, helping providers defend profitability as per-click economics soften and contracts incorporate security, compliance, and analytics deliverables.

Competitive Landscape

Competition remains moderate, with the top five OEMs capturing roughly 55-60% of 2025 revenue, yet share is slipping as ISVs and system integrators offer vendor-agnostic cloud platforms. Xerox’s USD 1.5 billion Lexmark acquisition added the Optra Edge software stack, highlighting the strategic pivot toward platform capabilities over hardware scale. HP, Canon, Ricoh, and Konica Minolta respond by bundling analytics, security, and workflow add-ons to defend accounts.

ISVs such as PaperCut, PrintFleet, and Vasion innovate at cloud cadence, releasing quarterly features that span mixed fleets and integrate with Microsoft 365 ecosystems. Their open APIs let enterprises consolidate governance and analytics across multibrand environments, shrinking OEM lock-in. Partnerships between resellers and ISVs flourish, delivering turnkey solutions and heightening service differentiation within the Managed Print Services market.

Technology moats now rely on generative AI, fleet-wide IoT telemetry, and carbon-accounting engines. Xerox’s Intelligent Document Processing predicts component failures 30 days ahead, cutting customer downtime and inventory costs. Ricoh’s data-driven maintenance reduced Asia Pacific fleet outages by 18%, proving operational ROI. As software value eclipses hardware specs, market leaders accelerate R&D budgets for cloud platforms, while late adopters risk relegation to commodity device suppliers.

Managed Print Services Industry Leaders

Xerox Corporation

Ricoh Company Ltd.

HP Inc.

Brother Industries, Ltd.

Canon Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Contract structures are moving beyond page-based optimization toward bundles that include cloud administration, security controls, and analytics. This creates whitespace for providers that can standardize print governance across hybrid work and mixed fleets. Public sector and higher education sourcing offers a concrete entry point for scaled deployments: University of California Systemwide Procurement renewed a 5-year managed print services agreement with Ricoh USA effective January 26, 2026 through January 25, 2031, and also renewed an agreement with Xerox covering managed print and IT services spanning November 2025 to November 2030. These renewals point to demand for multi-year, fleet-wide programs that combine MPS with cloud and IT service elements, while also raising expectations for service-level reporting, security posture, and device-to-cloud integration.

Cloud-native platforms and vendor-agnostic software also support another opportunity area, especially where customers want rapid rollout without on-premise print servers and where they run heterogeneous fleets across HP, Canon, Xerox, Ricoh, and others. The installed base creates further room for device-security upgrades driven by ISO/IEC 7184:2024 baseline hard-copy device security expectations and U.S. compliance frameworks affecting regulated workflows (HIPAA and the FTC Safeguards Rule). At the same time, data sovereignty constraints in parts of Asia Pacific and the Middle East sustain demand for hybrid architectures, which favors providers that can offer regional hosting options, localized metadata handling, and consistent policy enforcement across cloud and on-premise nodes.

Recent Industry Developments

- February 2026: Texas Department of Information Resources posted a contract for Xerox-branded hardware and managed print services, effective February 9, 2026. The award mechanism supports standardized public-sector procurement and reinforces the role of state-level contract vehicles in scaling MPS deployments. It also elevates requirements for security, reporting, and service coverage across dispersed agency fleets.

- January 2026: University of California Systemwide Procurement renewed a 5-year agreement with Ricoh USA for managed print services, effective January 26, 2026 through January 25, 2031. The renewal signals continued institutional demand for consolidated fleet governance, with scope that includes cloud and IT analytics elements alongside core MPS. Multi-year systemwide agreements also tighten competitive differentiation around SLA performance and program-level transparency.

- August 2025: Xerox launched an AI-powered Intelligent Document Processing capability integrated into its managed print services suite, designed to predict failures 30 days in advance. By linking document workflows and device telemetry to proactive service actions, the launch supports higher uptime guarantees and helps providers shift value toward analytics-driven outcomes. This also strengthens cross-sell potential into workflow optimization as print volumes structurally decline.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the managed print services market is defined as outsourced, contract-based services used by organizations to monitor, optimize, secure, and maintain their printer and MFP fleets, usually with software, consumables replenishment, and ongoing support bundled into a recurring fee.

Scope exclusions: One-off printer or copier hardware purchases made without an ongoing managed service agreement are not counted.

Segmentation Overview

- By Channel Type

- Printer/Copier Manufacturers

- System Integrators/Resellers

- Independent Software Vendors (ISVs)

- By Service Type

- Print Infrastructure Assessment

- Managed Print Operations

- Device and Fleet Management

- Document Workflow Optimisation

- Cloud Print Services

- By Deployment Mode

- On-Premise

- Cloud-Based

- By Organisation Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By End-User Vertical

- BFSI

- Healthcare

- IT and Telecom

- Government

- Education

- Other End-User Verticals

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Nordics

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Middle East

- GCC (Saudi Arabia, United Arab Emirates, Qatar)

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the demand environment that sits behind MPS contracts, then to sanity check the service revenue pool across regions. We relied on public sources such as the US Census Bureau, the US Bureau of Labor Statistics, Eurostat, the World Bank, and OECD indicators to understand office employment, business formation, and macro shifts that change print volumes over time.

To keep the model grounded, we also reviewed company annual reports, SEC filings, investor presentations, reputable press coverage, and trade association websites that publish statements on print security, hybrid work, and sustainability reporting. Where needed, paid subscriptions for company financials and news were used to standardize revenue disclosures and track major contract announcements, and patent databases helped confirm the pace of innovation in print analytics and document security features. The sources listed here are illustrative, and many other public references were also reviewed for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with MPS program owners, channel partners, IT and procurement leaders, and operations managers who run print fleets day to day. Respondent input was used to confirm what is typically bundled in contracts, how pricing is linked to devices and page volumes, and which deployment choices (cloud versus on-premise) are changing renewal behavior across major regions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 15% | APAC: 43% |

| Mid tier: 56% | Functional/Unit leaders: 25% | EMEA: 35% |

| Smaller Players: 19% | Managers: 60% | Americas: 22% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where the addressable enterprise print environment is reconstructed using indicators that proxy MPS-eligible demand, then converted into service revenue using validated commercial ratios. Inputs used in the model include installed base direction for office print fleets, likely page-volume mix by office intensity, the share of managed contracts in large enterprises versus SMBs, average contract value ranges by fleet size, and regional differences in security and compliance requirements that influence adoption.

After the demand pool is built, we corroborate totals using selective bottom-up approximations, such as sampled contract pricing checks, channel-level revenue splits, and service attach rate assumptions gathered from interviews. When gaps appear in smaller country markets, we used transparent proxy steps, including enterprise density and IT services spending direction, before the numbers were rechecked with regional experts.

For forecasting, we used scenario analysis because MPS demand is sensitive to hybrid work intensity and print digitization pace, and those drivers do not move in a straight line each year. Assumptions on device refresh cycles, consumables bundling, and cloud migration were reviewed with interviewees and applied consistently across the forecast window.

Data Validation & Update Cycle

Validation is done through multiple checks so the final numbers stay tied to real market signals. Model outputs are compared against independent indicators such as enterprise IT outsourcing direction, office employment movement, and the spread of print security mandates, then any large variance is traced back to the exact assumption that caused it.

Before sign-off, the build goes through step-by-step analyst review, followed by a second pass focused on anomaly detection, currency conversions, and year alignment across regions. Reports are refreshed annually, and interim revisions are triggered when major contract shifts, regulatory changes, or macro shocks materially alter adoption or pricing. Right before delivery, we run a final update sweep so clients receive the most current view available.

Mordor Intelligence's Managed Print Services Market Size Compared Against Other Published Estimates

Published market sizes for managed print services can look different even when the topic name is the same, because the boundaries are not always drawn in the same way. Differences usually come from what gets counted inside a contract, which buyers are considered in-scope, and how pricing is carried forward year to year.

Key gap drivers in this market often include whether bundled consumables are included, whether document management and adjacent workflow software is pulled into the total, and how cloud-based contract pricing is treated as page volumes shift. Some sources also apply conservative growth paths due to lower print volumes, while others assume security-led upgrades increase recurring fees faster than the installed base changes.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 49.80 B (2025) | |

| Global Consultancy A | USD 49.33 B (2025) | This estimate appears to align closely on year, but its inclusions can differ by treating some workflow and document-related elements as part of MPS, which can shift how contract value is allocated. |

| Industry Publisher B | USD 40.36 B (2025) | The lower value suggests a tighter scope, often closer to core fleet management and support, with less emphasis on bundled supplies or advanced analytics and security features inside the recurring fee. |

Contract bundle checks and region-level adoption sanity checks are the evidence used to keep Mordor Intelligence tied to MPS agreements that include monitoring, optimization, and maintenance plus commonly bundled items like consumables and security tooling. With the same year and currency, the spread in the table is mostly explained by how narrowly each publisher defines what belongs inside an MPS contract, and whether adjacent document workflow value is counted as part of this market.

Key Questions Answered in the Report

How big is the Managed Print Services market in 2026 and what growth rate is expected?

The Managed Print Services market size reached USD 54.42 billion in 2026 and is projected to grow at an 8.88% CAGR to USD 83.26 billion by 2031.

Which service category is growing the fastest?

Cloud Print Services post the highest expansion at a 9.22% CAGR because cloud platforms remove on-premise servers and enable secure hybrid-work printing.

Why are SMEs adopting managed print services rapidly?

Subscription pricing converts capex to opex, while cloud portals provide enterprise-grade security and automated supplies without internal IT overhead.

Why are independent software vendors gaining share against printer OEMs?

ISVs deliver vendor-agnostic, cloud-native platforms that manage mixed fleets and integrate quickly with Microsoft 365, reducing switching costs for enterprises.

What role does sustainability play in Managed Print Services adoption?

EU carbon-reporting regulations require page-level emissions data, so enterprises subscribe to MPS modules that automate tracking and help meet disclosure mandates.

Which region offers the highest growth opportunity?

Asia Pacific leads with a 10.48% CAGR, driven by manufacturing digitization, IoT-enabled fleet analytics, and government modernization programs.

How are SMEs benefiting from Managed Print Services?

Subscription bundles eliminate capital expenditure, offload IT complexity, and allow per-user scaling, making MPS attractive even when per-page costs are higher than self-management.

Page last updated on: