Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Optical Character Recognition Market is Segmented by Type (Software [Mobile OCR Software, and More], Services [Professional Services, and More]), Deployment Mode (On-Premise, and Cloud), Technology (Conventional OCR, and More), Application (Invoice and Bill Processing, and More), End-User Industry (BFSI, Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

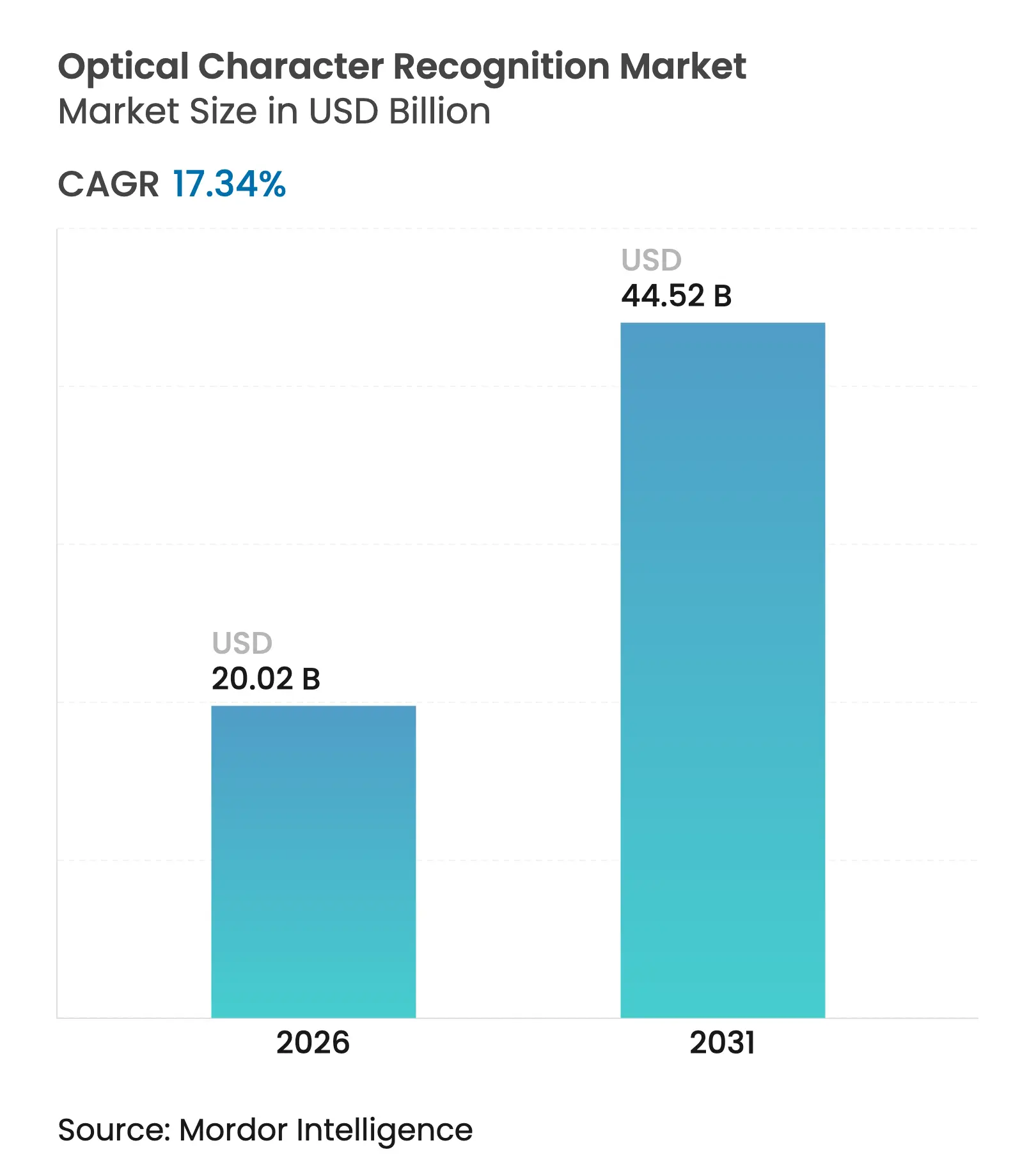

| Market Size (2026) | USD 20.02 Billion |

| Market Size (2031) | USD 44.52 Billion |

| Growth Rate (2026 - 2031) | 17.34 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

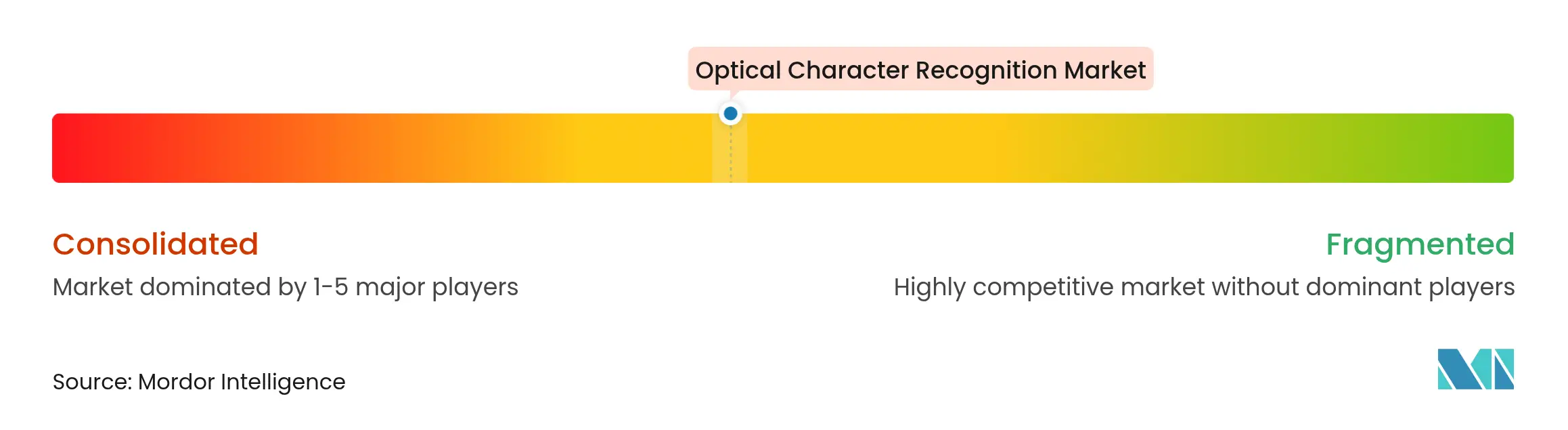

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The optical character recognition market size is expected to grow from USD 17.06 billion in 2025 to USD 20.02 billion in 2026 and is forecast to reach USD 44.52 billion by 2031 at 17.34% CAGR over 2026-2031. Growth is propelled by AI-driven accuracy gains, expanding cloud deployment, and tighter regulatory mandates that encourage automated compliance checks. Technology vendors are shifting from standalone OCR engines to full-stack document-intelligence platforms that combine recognition, classification, and validation in a single workflow. Multimodal large language models, which read both images and text, are lowering per-page processing costs and widening adoption across small and midsize enterprises. Intensifying competition is pushing suppliers to differentiate through domain-specific templates, language support, and value-added analytics rather than pure extraction speed.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising automation in industries

Rising automation in industries

| +3.5% | North America, Europe | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+3.5%

|

Geographic Relevance

:

North America, Europe

|

Impact Timeline

:

Medium term (2-4 years)

|

Adoption of cloud technology

Adoption of cloud technology

| +2.8% | North America (early), global | Short term (≤ 2 years) | |||

Integration with IDP platforms

Integration with IDP platforms

| +2.1% | North America, Europe, advanced Asia-Pacific | Medium term (2-4 years) | |||

AI-powered OCR for healthcare claims

AI-powered OCR for healthcare claims

| +1.9% | North America, Europe, advanced Asia-Pacific | Medium term (2-4 years) | |||

Accessibility-compliance regulations

Accessibility-compliance regulations

| +1.4% | North America, Europe, emerging Asia-Pacific | Long term (≥ 4 years) | |||

Low-code OCR SDK uptake by SMBs

Low-code OCR SDK uptake by SMBs

| +1.2% | Emerging markets worldwide | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Rising automation in industries

Manufacturing and logistics organizations are embedding AI-driven OCR in supply-chain workflows to capture data from shipping labels, invoices, and pick-lists in real time. Accuracy levels of 97% under challenging lighting conditions increase throughput and cut manual touchpoints by 50% [1]Zebra Technologies, “A Deeper Dive on Deep Learning OCR,” zebra.com. Automatic number-plate recognition aligns with warehouse gates to speed vehicle entry, demonstrating how the optical character recognition market extends beyond documents to physical assets.

Adoption of cloud technology

Consumption-based cloud OCR removes up-front capital requirements and delivers instant algorithm updates. Azure Form Recognizer exemplifies this shift, providing pay-as-you-go pricing that attracts firms with variable document volumes. Browser-based engines using WebAssembly process IDs locally to satisfy privacy rules, allowing SMEs in stringent jurisdictions to benefit from cloud scalability without sending data off-site.

Integration with IDP platforms

Vendors bundle OCR, classification, and validation into end-to-end intelligent document processing suites. ABBYY FlexiCapture offers pre-built templates for mortgage applications and healthcare claims, reducing processing times by 80% and error rates by 95% [2]ABBYY, “Recent News & Activity,” abbyy.com. This platform orientation positions the optical character recognition market as a linchpin of broader automation strategies.

AI-powered OCR for healthcare claims

Healthcare payers automate extraction from explanation-of-benefit forms to structured ERA files, accelerating reimbursement and lowering administrative overhead. HIPAA-compliant security frameworks ensure protected health information remains encrypted throughout the workflow, addressing a critical adoption barrier.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High initial investment costs

High initial investment costs

| -1.2% | Emerging markets, SMBs | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-1.2%

|

Geographic Relevance

:

Emerging markets, SMBs

|

Impact Timeline

:

Short term (≤ 2 years)

|

Data-privacy concerns in cloud OCR

Data-privacy concerns in cloud OCR

| -0.8% | Europe, regulated sectors worldwide | Medium term (2-4 years) | |||

Low-resource language handwriting limits

Low-resource language handwriting limits

| -0.7% | Asia-Pacific, MEA, LATAM | Long term (≥ 4 years) | |||

GPU supply constraints for deep-learning OCR

GPU supply constraints for deep-learning OCR

| -0.5% | Global | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

High initial investment costs

Enterprise-grade OCR deployments entail software licenses, systems integration, and process re-engineering that many SMEs struggle to afford. While subscription pricing mitigates capex, customizing workflows and linking legacy systems keep total cost of ownership high, slowing penetration in price-sensitive segments.

Data-privacy concerns in cloud OCR

European Data Protection Board guidance underscores risks linked to processing sensitive personal data with OCR, compelling many financial and healthcare entities to retain on-premise engines despite higher maintenance overhead. Vendors respond by offering containerized deployments and in-browser processing to balance efficiency and compliance.

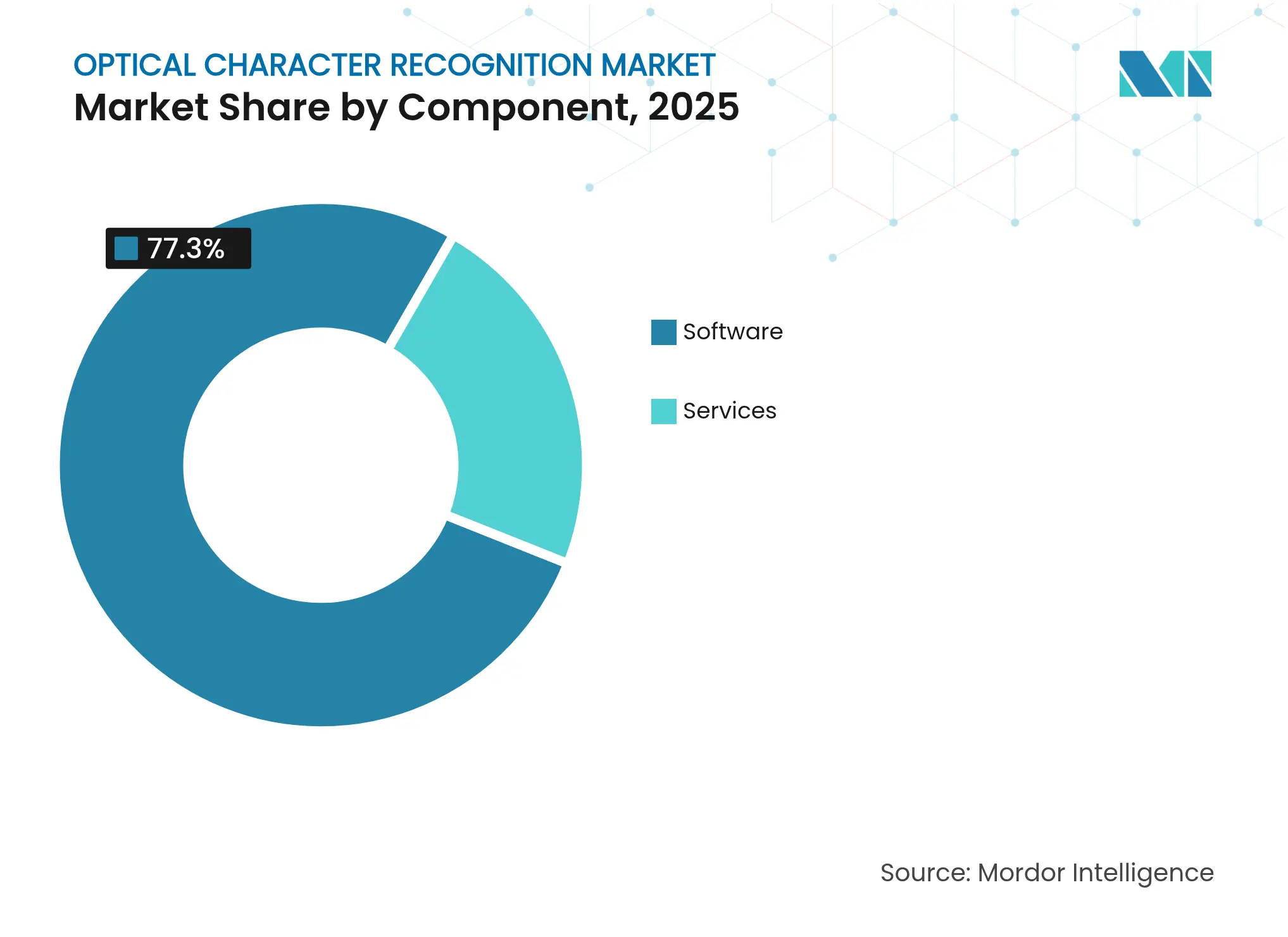

By Component: Services Growth Outpaces Software Dominance

The software segment held a 77.30% revenue stake in 2025, establishing a solid base for the optical character recognition market. Services, however, are projected to deliver a 17.36% CAGR through 2031 as organizations demand consulting, customization, and managed operations to realize full ROI. This pivot shows that expertise, not merely code, now unlocks the value of OCR deployments.

Professional-services providers build vertical playbooks that embed industry terminology and regulatory templates into OCR pipelines. Healthcare integrators, for instance, supply medical lexicons to raise extraction precision, whereas banking specialists focus on AML and KYC documents. Managed services relieve internal IT teams from tuning recognition models, ensuring the systems stay current with new document formats.

Note: Segment shares of all individual segments available upon report purchase

By Deployment Mode: Cloud Leads While On-Premise Gains Strategic Importance

Cloud deployments generated 65.20% of 2025 revenue, reflecting customer preference for elastic scaling and automatic algorithm improvements. Even so, on-premise solutions are set to rise at 15.45% CAGR as regulated sectors require data residency. Financial institutions often keep cheque imaging on local servers while shifting less sensitive workflows to the cloud.

Hybrid architectures dominate. Microsoft ships its OCR containers to customer data centers, letting firms process documents locally and still connect to Azure AI for advanced post-processing. This configuration positions the optical character recognition market as both a SaaS and an appliance play, depending on compliance thresholds.

By Technology: Intelligent Character Recognition Disrupts Traditional OCR

Conventional OCR retained 70.40% of 2025 revenue, yet Intelligent Character Recognition is forecast to advance 18.95% CAGR because it deciphers cursive scripts and semi-structured forms. Deep-learning ICR engines now hit 85% accuracy on clear handwriting, expanding the addressable workload beyond typed invoices.

Optical mark and intelligent word recognition modules complement ICR, processing check-boxes and short free-text notes. Multimodal AI models, capable of reading entire document layouts, further erode the distinction between OCR and natural language processing, creating a convergence zone that redefines the optical character recognition market.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

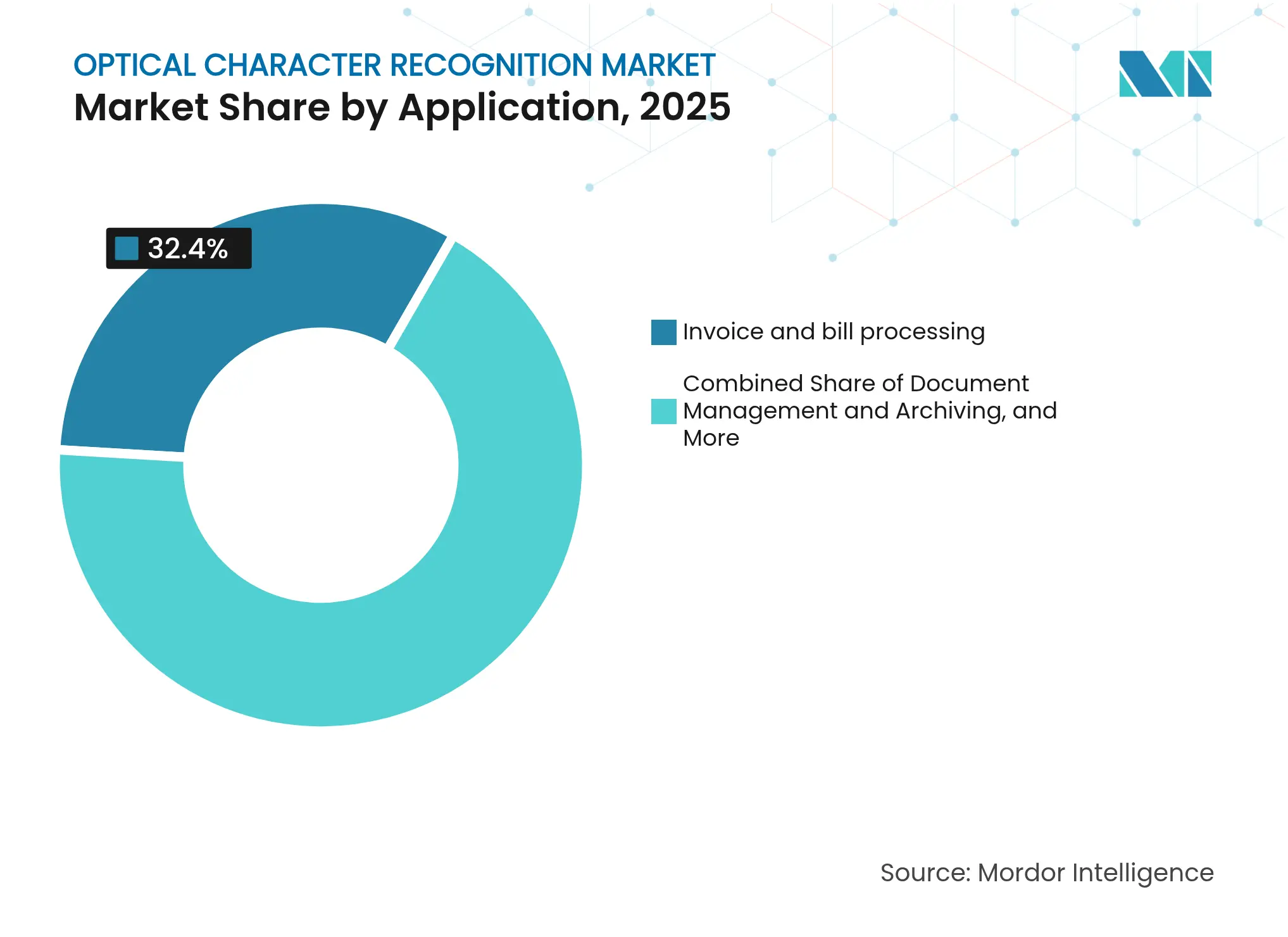

By Application: Identity Verification Emerges as Growth Leader

Invoice and bill processing kept 32.40% share in 2025, anchoring core demand, while Identity Verification and KYC is projected to scale at 17.85% CAGR. Banks and fintechs integrate OCR with facial recognition to authenticate documents during mobile onboarding, cutting customer acquisition times from days to minutes.

Document management, although mature, remains essential as firms digitize archives for searchability. Packaging and label recognition leverages OCR for traceability across manufacturing lines, while healthcare providers combine OCR with clinical NLP to code unstructured notes. These specialized cases expand the optical character recognition market beyond accounts-payable hubs.

Note: Segment shares of all individual segments available upon report purchase

By End-Use Industry: Healthcare Digitization Drives Fastest Growth

BFSI controlled 25.60% revenue in 2025 through loan files, statements, and compliance records. Healthcare is poised for a 19.45% CAGR, fueled by electronic health-record mandates and the need to automate claims. OCR engines trained on clinical vocabularies extract diagnosis codes directly from scanned charts, improving billing accuracy.

Retail and e-commerce businesses employ OCR for product-label capture and customer ID checks at pickup points. Government agencies digitize land records and passports to modernize citizen services. Manufacturing plants embed OCR in quality-control stations, ensuring regulatory labels match batch data.

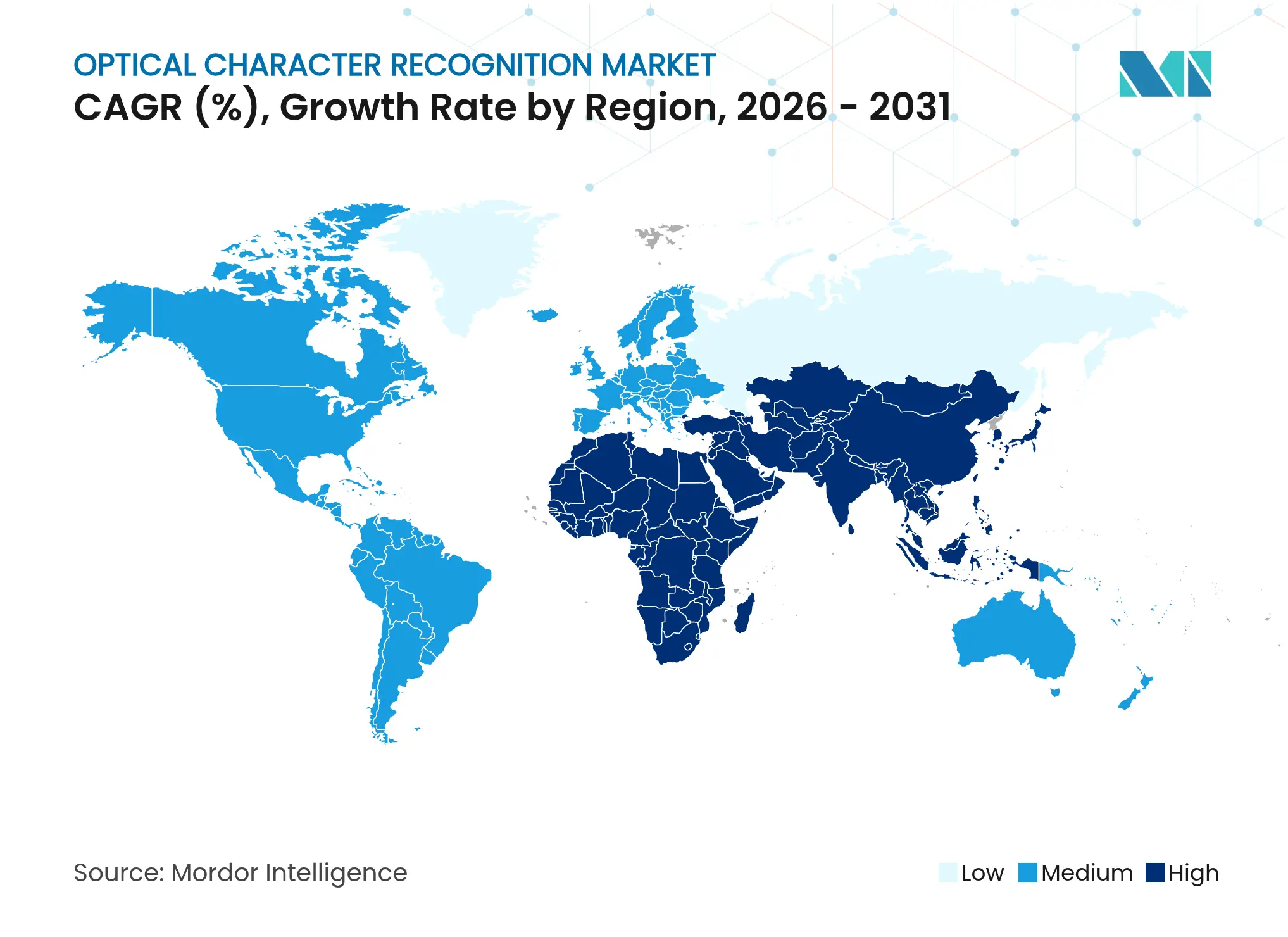

North America commanded 39.50% of optical character recognition market revenue in 2025, underpinned by high labor costs that justify automation and by a dense cluster of technology suppliers. HIPAA and KYC regulations accelerate adoption in healthcare and banking. Vendors in the region integrate OCR with robotic-process-automation bots, generating compound efficiency gains.

Asia-Pacific is the fastest-growing territory at 17.58% CAGR. China’s cloud providers, such as Alibaba Cloud and Tencent Cloud, bundle recognition services with broader AI suites, lowering entry barriers for local firms. India’s digitization programs and high-volume banking sector create fertile ground for KYC OCR, while Japan and South Korea focus on manufacturing quality control.

Europe shows strong uptake across public and private sectors but remains cautious on data sovereignty. Germany and France favor on-premise or sovereign-cloud installations to meet GDPR. Supply-chain resiliency goals push logistics firms toward automated document capture for end-to-end visibility, sustaining steady growth in the region.

Market Concentration

The optical character recognition market features a mix of diversified software giants and niche AI entrants. Adobe, Google, and Microsoft embed OCR into broader productivity suites, offering wide reach. ABBYY, Kofax, and UiPath differentiate through vertical templates and workflow orchestration. Startups such as Mistral AI use large language models to reach 99% accuracy at USD 1 per 1,000 pages, raising the competitive bar [3]Campus Technology, “Mistral AI Introduces AI-Powered OCR,” campustechnology.com.

Strategic moves include API launches for developer ecosystems, acquisitions that add regulatory expertise, and containerized deployments for edge processing. Descartes Systems Group’s purchase of OCR Services expands trade-compliance coverage, while ABBYY’s new API targets low-code integration. White-space remains in low-resource language support and blockchain-verified document authenticity.

As vendors converge on similar deep-learning techniques, differentiation shifts to pre-built domain knowledge, governance features, and total cost of ownership. Partnerships with hyperscale clouds and RPA platforms extend market reach, keeping competition active yet preventing monopolistic dominance.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Market Definitions and Key Coverage

Our study defines the optical character recognition (OCR) market as all licensed software, embedded engines, and bundled services that transform scanned or photographed text into machine-encoded data across desktop, mobile, and cloud environments. The model counts revenue generated from initial licenses, subscription fees, and recognized implementation or managed support linked directly to OCR functionality.

Scope Exclusion: Pure handwriting-only transcription services and single-purpose barcode readers are outside this assessment.

Segmentation Overview

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed OCR engine developers, system integrators, banking operations leads, and health-records administrators across North America, Europe, and Asia-Pacific. The discussions validated average selling prices, deployment preferences, and regional adoption hurdles, letting us refine assumptions that public data alone cannot surface.

Desk Research

We began by harvesting foundational indicators from open sources such as the US Census Bureau, Eurostat trade codes for image-processing software, India's MeitY export registers, and filings to the SEC and F-SAs. Patent analytics from Questel, shipment data via Volza, and news coverage indexed on Dow Jones Factiva helped us trace technology diffusion and pricing shifts. Additional context came from industry associations, AIIM for document management, NACHA for check processing volumes, and HIMSS for healthcare digitization. These references anchor baseline demand signals, while company 10-Ks and investor decks clarify monetization pathways. The sources listed are illustrative; many others informed our evidence gathering.

Market-Sizing & Forecasting

A top-down build starts with worldwide business software outlays, which are then filtered through document-intensive vertical shares and OCR penetration ratios. Select bottom-up checks, supplier roll-ups and sampled ASP × volume, for key geographies temper the totals. Critical variables include check-processing volumes, electronic medical-record mandates, mobile banking user counts, average scan resolution trends, and cloud migration rates; each was projected using ARIMA and cross-checked by multivariate regression where data series allow. Gaps in bottom-up estimates, especially for emerging markets, were bridged by applying validated adoption curves from comparable regions.

Data Validation & Update Cycle

Outputs pass variance scans against external benchmarks, peer review by a senior analyst, and a reconciliation meeting before sign-off. We refresh every twelve months, while extraordinary events, major regulatory change or landmark acquisition, trigger interim updates, ensuring clients receive the latest outlook.

Why Mordor's Optical Character Recognition Baseline Commands Reliability

Benchmark comparison

Published numbers often differ because firms apply unique service scopes, pricing capture points, and refresh rhythms.

By rooting estimates in verifiable adoption metrics and cross-continent interviews, our baseline stays balanced and transparent.

Key gap drivers include narrower component coverage, untested historical extrapolations, or slower refresh cadence at other publishers.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 17.06 Bn (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 12.56 Bn (2023) | Regional Consultancy A | Excludes services revenue and mobile OCR apps | ||

USD 12.25 Bn (2024) | Trade Journal B | Relies on straight-line growth from 2020 without field validation | ||

USD 12.21 Bn (2024) | Global Consultancy C | Counts only on-premise deployments; cloud uptake ignored |

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

A Leading Sanitaryware Company’s Journey in Saudi Arabia

4 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.