Laser Hair Removal Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

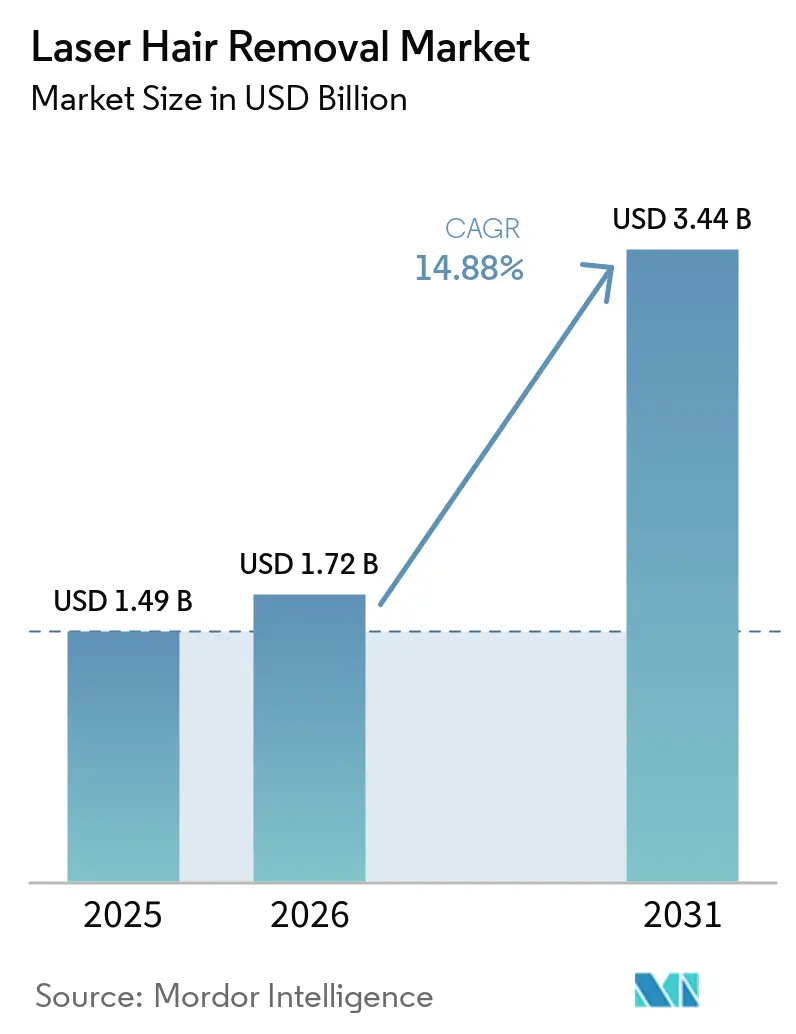

| Market Size (2026) | USD 1.72 Billion |

| Market Size (2031) | USD 3.44 Billion |

| Growth Rate (2026 - 2031) | 14.88% CAGR |

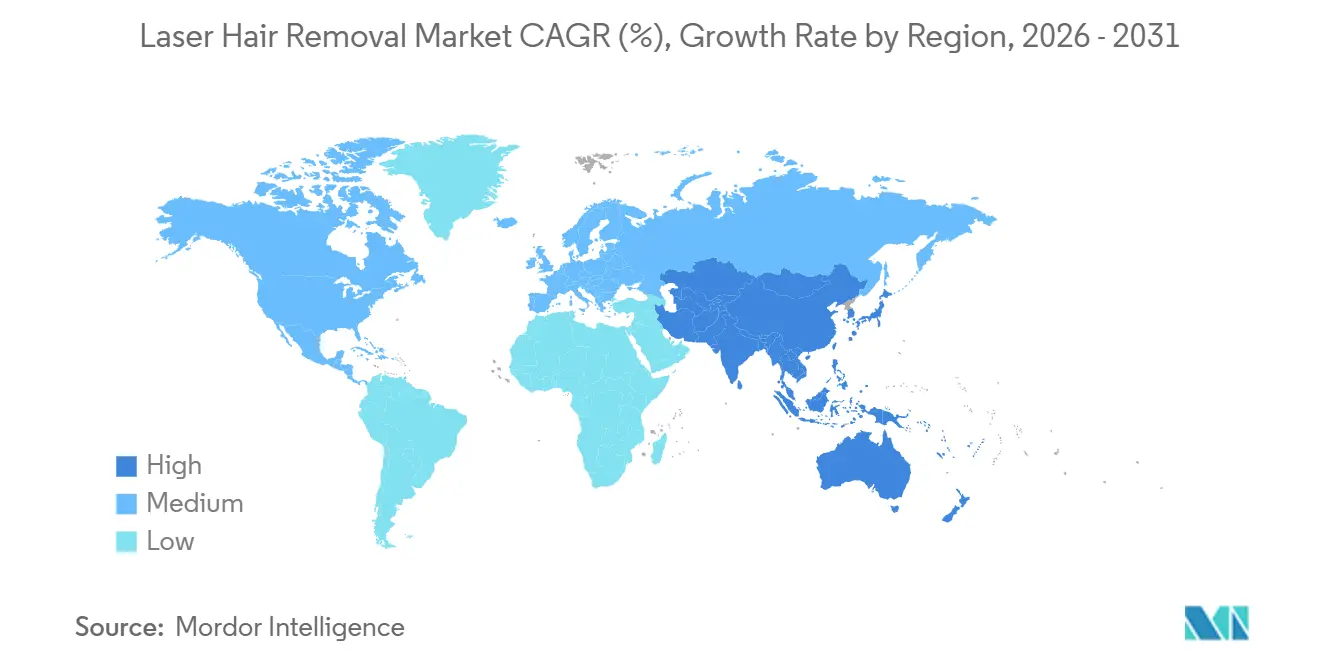

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

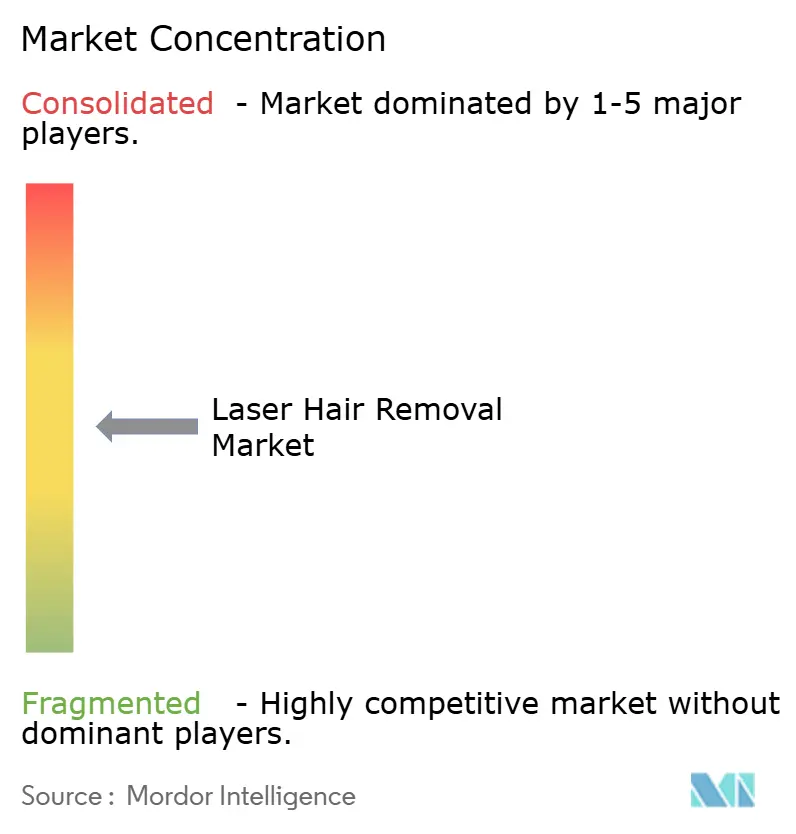

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Laser Hair Removal Market Analysis by Mordor Intelligence

The Laser Hair Removal Market size is expected to grow from USD 1.49 billion in 2025 to USD 1.72 billion in 2026 and is forecast to reach USD 3.44 billion by 2031 at 14.88% CAGR over 2026-2031.

Demand is rising because permanent hair reduction is moving ahead of repeat shaving, waxing, and other cyclical methods in many urban consumer groups. The laser hair removal market is also reaching a broader customer base as dedicated clinic chains expand through franchise and corporate-owned models across more cities. At the same time, home-use devices and direct-to-consumer digital channels are bringing in consumers who earlier viewed treatment as too expensive or difficult to access. Demand for systems that work safely across darker Fitzpatrick skin types is also reshaping the laser hair removal market and pushing vendors toward broader treatment capability. Competition remains active as premium OEMs focus on faster platforms, wider skin-tone coverage, and digital service tools, while smaller manufacturers continue to compete more heavily on price.

Key Report Takeaways

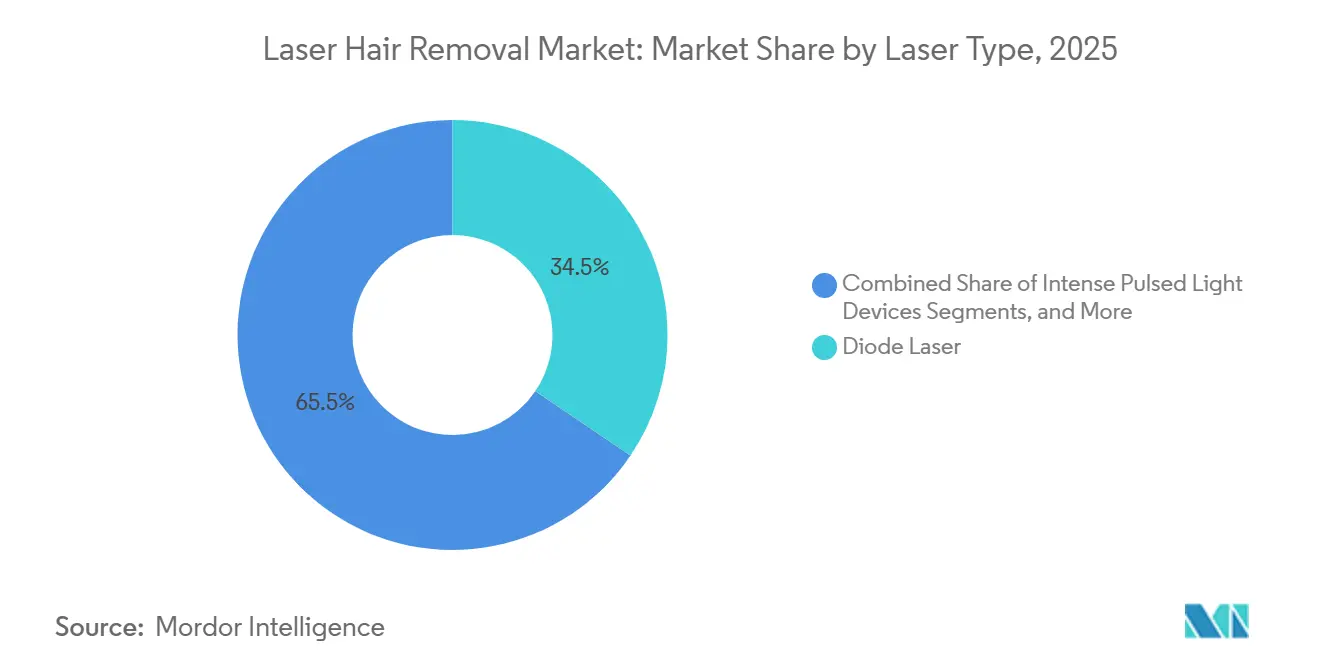

- By laser type, the diode laser held 34.45% of revenue in 2025, while the Nd:YAG laser is forecasted to expand at a 15.35% CAGR through 2031.

- By product type, standalone laser devices accounted for 56.88% of revenue in 2025, while multi-functional laser devices are projected to grow at a 15.78% CAGR over 2026-2031.

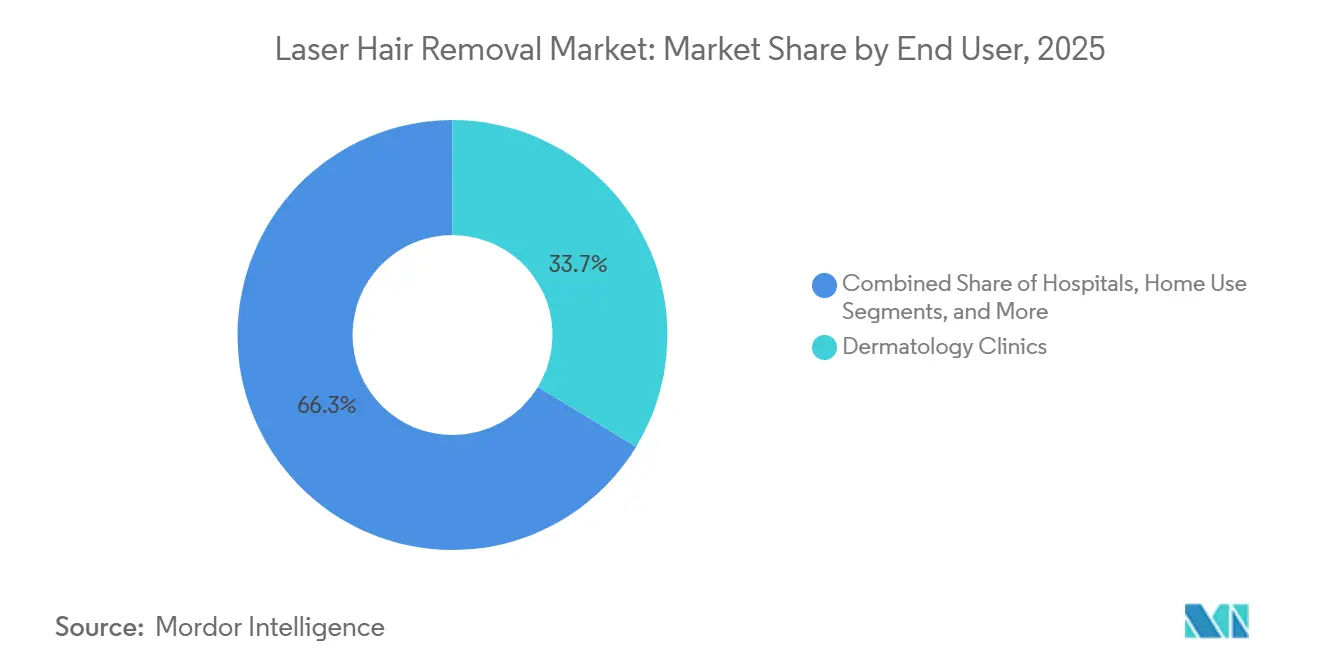

- By end user, dermatology clinics represented 33.68% of revenue in 2025, while home-use devices are projected to record the fastest growth at a 16.56% CAGR through 2031.

- By gender, female consumers held 68.97% of the gender-segmented market in 2025 and also recorded the fastest projected growth through 2031.

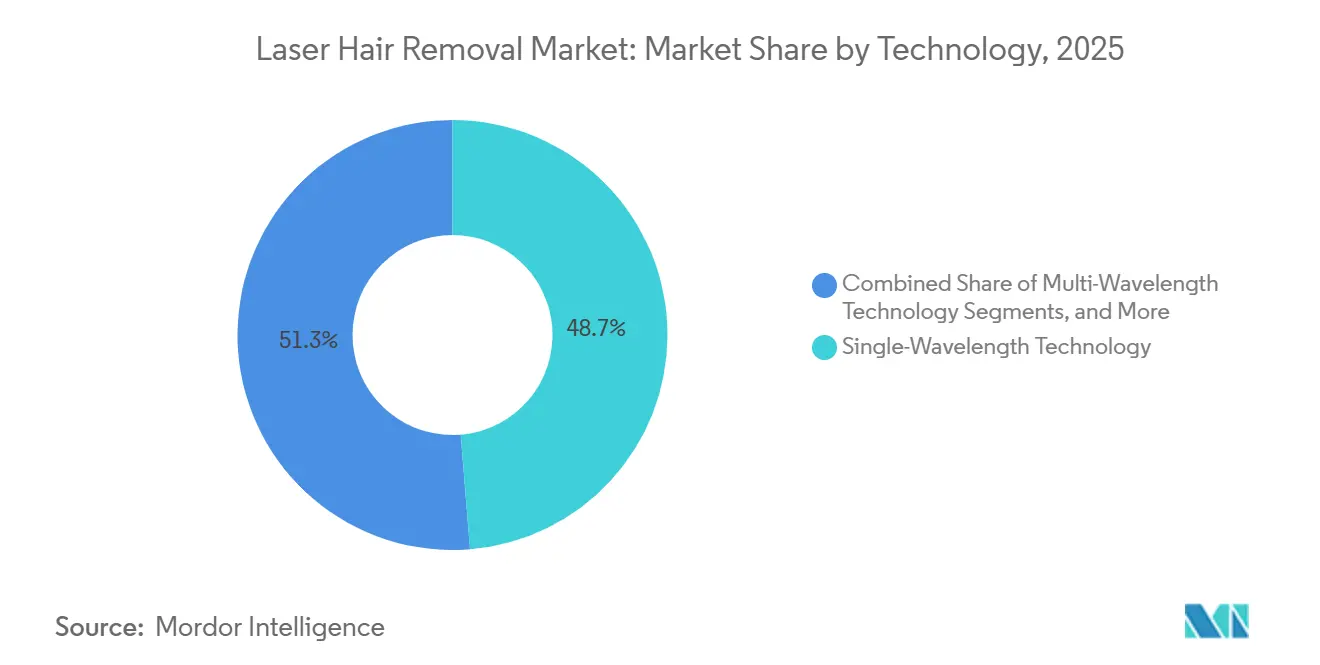

- By technology, single-wavelength systems captured 48.67% of revenue in 2025, while multi-wavelength systems are forecasted to grow at a 17.24% CAGR over 2026-2031.

- By distribution channel, offline retail held 65.98% of revenue in 2025, while online retail is projected to expand at a 16.98% CAGR through 2031.

- By geography, North America held 41.25% of global revenue in 2025, while Asia-Pacific is projected to advance at a 16.52% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Laser Hair Removal Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising preference for non-invasive aesthetic procedures | +2.8% | Global | Short term (≤ 2 years) |

| Expansion of premium aesthetic clinic networks and franchises | +2.3% | North America, Europe & APAC core | Medium term (2-4 years) |

| Technology shift toward faster multi-wavelength platforms | +2.5% | Global | Medium term (2-4 years) |

| Home-use device adoption through e-commerce and DTC channels | +2.0% | APAC, North America, Europe | Short term (≤ 2 years) |

| Male grooming normalization in high-disposable-income markets | +1.7% | North America, Europe, APAC urban | Long term (≥ 4 years) |

| Demand for skin-tone inclusive systems in multicultural demographics | +1.9% | North America, MEA, APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Preference for Non-Invasive Aesthetic Procedures

Many consumers now view laser hair removal as a regular personal care service rather than an occasional luxury. This shift is significant, as it boosts repeat visits and encourages larger multi-session packages in the laser hair removal market. By August 2025, Milan Laser Hair Removal had expanded to over 400 locations across 38 U.S. states, focusing on lifetime guarantee packages instead of one-off sessions.[1]Milan Laser Hair Removal, “Milan Laser Hair Removal Celebrates Opening of 400th Clinic,” PR Newswire, prnewswire.com This approach ties customers to a longer relationship, making it challenging for them to switch once treatment begins. It also benefits larger operators, allowing them to distribute marketing and service costs across a wider clinic network. Consequently, the market is witnessing a distinct divide: organized chains are thriving, while smaller providers struggle, often relying on single-visit demand.

Technology Shift Toward Faster Multi-Wavelength Platforms

Innovations in devices are not only enhancing clinical outcomes but also reshaping the economics of treatment rooms. In April 2025, Candela announced that its GLX Delivery System, paired with GentleMax Pro Plus, cut the time between treatments by 81% and reduced session durations by 21%. Following suit, Sciton unveiled its OMNI platform in June 2025. This 5,000W system, featuring a blend of 760 nm, 810/940 nm, and 1060 nm wavelengths, caters to all skin types and practice sizes. Such advancements enable clinics to manage high volumes more efficiently, broadening patient eligibility and optimizing room usage. In contrast, clinics sticking to older, single-wavelength systems may struggle with reduced throughput and limited treatment options. This widening gap is bolstering premium positioning in the market and intensifying the urgency for upgrades.

Home-Use Laser Hair Removal Device Adoption Through E-Commerce and DTC Channels

Demand for home-use laser devices is rising, driven by innovations like subscription refills, guided routines, and digital support that ensure consistent usage. A 2025 study highlighted that while professional treatments yield stronger results, home-use IPLs demonstrated comparable efficacy under controlled conditions.[2]Candela and Ideal Image, “Ideal Image Elevates Its Hair Removal Laser Fleet with Candela's GentleMax Pro Plus Laser and the New GLX Delivery System,” PR Newswire, prnewswire.com Such findings boost consumer confidence, making home treatments more appealing to newcomers. Brands are also enhancing online shopping experiences with skin-tone assessments and device-matching tools, reducing uncertainty for buyers. This strategy is attracting new users to the laser hair removal market, many of whom may transition from home care to professional treatments.

Expansion of Premium Aesthetic Clinic Networks and Franchises

As premium clinics expand, they are creating demand in areas where branded laser treatments were previously limited. By November 2025, LaserAway celebrated its 200th clinic milestone across 35 U.S. states, noting two decades without a single closure. In Canada, Laser Clinics opened its 8th location at Vaughan Mills in May 2025, with plans to expand to 40 sites nationwide. Each new clinic increases local awareness and makes treatments more accessible to mainstream consumers. This expansion also strengthens the chains' influence in procurement, marketing, and pricing, making it harder for independent clinics, especially in secondary cities, to sustain premium pricing.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Risk of burns, pigment changes, and operator-dependency in treatment outcomes | -1.3% | Global | Short term (≤ 2 years) |

| High upfront cost of professional systems and recurring maintenance commitments | -1.6% | MEA, South America, emerging APAC | Medium term (2-4 years) |

| At-home IPL and low-cost device substitution pressure on professional treatments | -0.9% | North America, Europe, APAC | Medium term (2-4 years) |

| Limited efficacy on light hair, hormonal regrowth, and certain dark skin tone profiles | -0.8% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Professional Systems and Recurring Maintenance

Smaller operators face significant challenges due to the high initial investment required for professional systems. Annual maintenance costs, accounting for 10% to 15% of the system's price, further strain profitability for clinics with lower treatment volumes. This issue is more pronounced in regions like parts of the Middle East, South America, and emerging Asia-Pacific markets, where limited financing options and high import duties increase costs. InMode, in its full-year 2025 results, announced plans to launch two new laser-based platforms in 2026, reflecting a rapid product cycle. This shortens the timeframe before systems become outdated, creating difficulties for clinics still paying off older equipment and widening the gap between large networks and smaller operators.

Risk of Burns, Pigment Changes, and Operator-Dependency in Treatment Outcomes

Clinical risks remain a key concern, as treatment outcomes depend heavily on wavelength selection, settings, and operator expertise. Darker Fitzpatrick skin types are more prone to adverse effects like post-inflammatory hyperpigmentation when parameters are not properly matched. Additionally, delayed complications such as Fox-Fordyce disease have been observed post-laser hair removal, particularly in darker skin types. These risks can undermine patient trust and increase reputational challenges for clinics. They highlight the importance of operator training and standardized treatment protocols. While stricter oversight in some markets drives compliance, it also raises the cost of maintaining qualifications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Laser Type: Nd:YAG Gains Ground as Skin-Tone Inclusivity Reshapes Device Mix

In 2025, the diode laser held 34.45% of the global laser hair removal market share, making it the leading laser type. Its popularity stems from a strong clinical track record, broad vendor availability, and lower capital costs compared to premium alternatives. Diode systems are well-suited for high-volume clinics due to their balance of efficacy and operational practicality across diverse patient groups. With a dermal penetration of 3 mm to 4 mm, they effectively target follicles in light-to-medium skin types while minimizing epidermal absorption.

Nd:YAG is projected to grow at a 15.35% CAGR from 2026 to 2031, making it the fastest-growing laser type. Its safety profile for darker Fitzpatrick IV-VI skin types is driving demand in multicultural markets. The 1064 nm wavelength offers deeper penetration and reduces epidermal injury risk when applied correctly. Alexandrite remains a strong choice for lighter skin treatments due to higher melanin absorption and faster cycles. Ruby is becoming obsolete, while IPL faces competition from advanced laser platforms. Hybrid and multi-wavelength platforms are gaining traction, supported by FDA clearance for dual-wavelength emission across all Fitzpatrick types, pushing the market toward inclusivity.

By Product Type: Multi-Functional Platforms Drive Revenue Intensity per Clinical Unit

Standalone laser devices accounted for 56.88% of product-type revenue in 2025, as clinics favored systems that are easier to train on, maintain, and purchase. These platforms are ideal for clinics focused solely on hair removal, maintaining relevance in single-service practices. Their established base remains significant due to gradual replacement cycles.

Multi-functional devices are expected to grow at a 15.78% CAGR from 2026 to 2031 as clinics aim to maximize revenue per machine. Sciton's OMNI platform, launched in June 2025, and Alma Harmony, introduced in March 2025, reflect this trend. These platforms support multiple indications, spreading equipment costs across procedures and increasing utilization. They also create upgrade pressure on older standalone systems, signaling a shift toward platform-based economics in the market.

By End User: Clinical Settings Lead but Home Use Redefines the Addressable Market

Dermatology clinics led the market in 2025 with 33.68% of end-user revenue, driven by physician oversight, patient trust, and the use of high-fluence systems. Clinics also benefit from adjacent medical use cases, such as pseudofolliculitis barbae treatment. Beauty and aesthetic centers followed, offering easier access and competitive pricing, while hospitals played a smaller role in cases requiring medical supervision.

Home-use devices are forecast to grow at a 16.56% CAGR through 2031, making them the fastest-growing segment. Direct-to-consumer brands are capturing early customer relationships and shaping treatment expectations. Evidence supporting home-use IPL devices' effectiveness boosts consumer confidence, particularly among first-time users. Clinics must adapt to this trend as the market expands across both clinical and consumer channels.

By Gender: Female Segment Broadens Addressable Zones as Male Grooming Scales

Female consumers accounted for 68.97% of the market in 2025, remaining the dominant segment and recording the fastest growth through 2031. This growth is driven by expanded treatment zones, repeat-package structures, and accessible home-use options. Franchise chains offering lifetime packages further support this trend, ensuring a broad female consumer base across channels.

The male segment, representing nearly 31% of the market in 2025, is concentrated in back, chest, neck, and shoulder treatments. Male demand is strongest in high-income urban areas, with growth seen in GCC cities, Japan, and South Korea. Clinics view male customers as a growth opportunity, particularly as many are first-time visitors with less service history compared to female clients.

By Technology: Multi-Wavelength Systems Create a Two-Tier Clinic Market

Single-wavelength systems held 48.67% of revenue in 2025, supported by a large installed base. These systems remain effective for lighter skin and dark hair, meeting the needs of high-volume clinics. Their established presence ensures stability, even as newer technologies grow faster.

Multi-wavelength systems are projected to grow at a 17.24% CAGR from 2026 to 2031. Lumenis highlighted this trend with its SPLENDOR X platform, featuring digital service capabilities and simultaneous dual-wavelength technology. This innovation broadens eligibility across all Fitzpatrick types and reduces seasonal treatment limitations. Clinics with these systems can treat a wider patient mix, while those without face challenges in patient retention and pricing flexibility, creating a two-tier market structure.

By Distribution Channel: Offline Channels Anchor Professional Sales as Online Reshapes Consumer Behavior

Offline retail accounted for 65.98% of the market in 2025, as professional systems require consultative sales processes, including demonstrations, training, and maintenance. This approach favors direct sales teams and distributors, allowing OEMs to bundle services into their offerings. Offline channels remain central for professional buyers despite the growth of digital discovery.

Online retail is expected to grow at a 16.98% CAGR through 2031, driven by home-use and mid-range consumer devices. Consumers increasingly compare specifications and prices online, influencing professional demand as well. Clinics must enhance digital visibility to capture demand early in the purchase journey. While offline channels dominate professional sales, online platforms are reshaping consumer behavior and expectations, making both channels essential for market growth.

Geography Analysis

In 2025, North America dominated the global laser hair removal market, holding a significant 41.25% share. The region benefits from a dense clinic network, strong awareness of aesthetic procedures, and the presence of leading device OEMs. The U.S. remains the largest national market, with major chains achieving nationwide reach. By August 2025, Milan Laser Hair Removal operated over 400 locations across 38 states, while LaserAway expanded to over 200 clinics in 35 states, improving access and driving price normalization across metropolitan areas.

Canada, though earlier in its clinic expansion cycle, is progressing steadily. In May 2025, Laser Clinics Canada opened its 8th location at Vaughan Mills and announced plans to expand to 40 locations nationwide. Mexico, while smaller, is an emerging market supported by urban middle-class spending and medical tourism. The Asia-Pacific region is projected to grow at a 16.52% CAGR from 2026 to 2031, making it the fastest-growing region. China leads the region, with regulatory access improving as Cynosure Lutronic's Clarity II received hair reduction approval from the National Medical Products Administration in February 2026.

Japan advanced when Clarity II gained PMDA clearance for long-term hair reduction in January 2026, a notable achievement in a market known for stringent device approvals. South Korea influences regional standards with its dense clinic network, training culture, and strong role in aesthetic exports. India is a high-growth market driven by its young urban population, expanding clinic network, and growing e-commerce access to home-use devices. Australia shows steady growth due to strong awareness and an established professional services base. Europe remains a mature but receptive market, with Germany, the UK, France, Italy, and Spain driving demand. The EU MDR framework favors products with robust clinical documentation.

Competitive Landscape

In the laser hair removal market, a select group of premium OEMs, including Candela, Lumenis Be Ltd., Cynosure Lutronic, Alma Lasers, and Sciton, dominate the global landscape. These industry leaders prioritize clinical performance, platform diversity, service support, and geographic reach in their competition, steering clear of a sole focus on pricing. Meanwhile, the market's broader landscape is more fragmented, with numerous smaller regional manufacturers and home-use brands operating across various countries.

Recent strategic moves underscore the efforts of leading suppliers to further distinguish themselves. In April 2025, Candela strengthened its collaboration with Ideal Image by introducing a performance-driven upgrade featuring the GentleMax Pro Plus and the GLX Delivery System. Lumenis launched an enhanced SPLENDOR X in the same month, integrating digital tools for large accounts and updated clinical data supporting BLEND X technology for all Fitzpatrick skin types. Sciton introduced OMNI in June 2025, a multi-wavelength platform designed for all skin types and various practice sizes. In February 2026, Cynosure Lutronic secured dual approvals for Clarity II in China and Japan, further solidifying its regional presence.

Another competitive front is emerging in the home-use segment, where brands such as Braun, Philips, and Tria Beauty focus on direct-to-consumer experiences, subscription models, and e-commerce strategies. This shift is significant as consumer engagement often begins before clinic visits. There is also a growing demand for skin-tone-inclusive treatments, as many providers still rely on systems unsuitable for darker skin types. Additionally, the gap between consumer devices and comprehensive clinical care remains largely untapped.

Laser Hair Removal Industry Leaders

Candela Corporation

Alma Lasers Ltd.

Cynosure, LLC

Cutera, Inc.

Venus Concept Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Cynosure Lutronic achieved dual regulatory approvals for its Clarity II dual-wavelength laser platform. The approvals were granted by China's National Medical Products Administration on February 12, 2026, and Japan's Pharmaceuticals and Medical Devices Agency on January 9, 2026. These approvals, targeting long-term hair reduction, represent a significant milestone in the APAC region due to the market size and regulatory complexities involved.

- August 2025: Milan Laser Hair Removal opened its 400th clinic on August 19, 2025, across 38 U.S. states. The company operates a corporate-owned model focused exclusively on laser hair removal, performing over 50,000 treatments monthly and offering lifetime guarantee packages.

- June 2025: Sciton launched OMNI, a next-generation platform, on June 21, 2025. Featuring 5,000W power and wavelength options of 760 nm, 810/940 nm blend, and 1060 nm, OMNI is designed to treat all Fitzpatrick skin types and cater to practices of varying sizes.

- May 2025: Laser Clinics Canada opened its 8th location at Vaughan Mills in May 2025 and announced plans to expand to nearly 40 locations across Ontario, Alberta, British Columbia, and the Atlantic provinces.

- April 2025: Lumenis Be Ltd. introduced an enhanced version of SPLENDOR X at the ASLMS Annual Conference in Orlando on April 21, 2025. The updated platform includes a user-focused design, advanced digital features for large account data services, and clinical validation of BLEND X's safety and efficacy across Fitzpatrick skin types I-VI. It remains the only FDA-cleared simultaneous dual-wavelength laser hair removal platform.

Global Laser Hair Removal Market Report Scope

As per the scope of the report, laser hair removal is a non-invasive cosmetic procedure that uses a concentrated beam of light (laser) to significantly reduce or eliminate unwanted body hair.

The laser hair removal market is segmented by laser type, product type, end-user, gender, technology, and distribution channel. By laser type, the market includes diode laser, alexandrite laser, Nd:YAG laser, ruby laser, intense pulsed light devices, and hybrid and multi-wavelength systems. By product type, the market is segmented into standalone laser devices and multi-functional laser devices. By end-user, the market is categorized into dermatology clinics, beauty and aesthetic centers, hospitals, and home use. By gender, the market is segmented into female and male. By technology, the market includes single-wavelength technology, multi-wavelength technology, and combination laser technology. By distribution channel, the market is divided into online retail and offline retail. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Diode Laser |

| Alexandrite Laser |

| Nd:YAG Laser |

| Ruby Laser |

| Intense Pulsed Light Devices |

| Hybrid and Multi-Wavelength Systems |

| Standalone Laser Devices |

| Multi-Functional Laser Devices |

| Dermatology Clinics |

| Beauty and Aesthetic Centers |

| Hospitals |

| Home Use |

| Female |

| Male |

| Single-Wavelength Technology |

| Multi-Wavelength Technology |

| Combination Laser Technology |

| Online Retail |

| Offline Retail |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Laser Type | Diode Laser | |

| Alexandrite Laser | ||

| Nd:YAG Laser | ||

| Ruby Laser | ||

| Intense Pulsed Light Devices | ||

| Hybrid and Multi-Wavelength Systems | ||

| By Product Type | Standalone Laser Devices | |

| Multi-Functional Laser Devices | ||

| By End User | Dermatology Clinics | |

| Beauty and Aesthetic Centers | ||

| Hospitals | ||

| Home Use | ||

| By Gender | Female | |

| Male | ||

| By Technology | Single-Wavelength Technology | |

| Multi-Wavelength Technology | ||

| Combination Laser Technology | ||

| By Distribution Channel | Online Retail | |

| Offline Retail | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the laser hair removal market?

The laser hair removal market is valued at USD 1.72 billion in 2026 and is forecast to reach USD 3.44 billion by 2031 at a 14.88% CAGR.

Which region leads global demand for laser hair removal?

North America held the largest regional share at 41.25% in 2025, supported by strong clinic density, consumer awareness, and major OEM presence.

Which region is growing the fastest through 2031?

Asia-Pacific is the fastest-growing region with a projected 16.52% CAGR over 2026-2031, helped by urban demand, regulatory approvals, and wider access.

Which laser type is growing the fastest?

Nd:YAG is the fastest-growing laser type with a 15.35% CAGR because it is better suited to darker Fitzpatrick skin types and diverse patient populations.

Why are home-use devices expanding so quickly?

Home-use devices are projected to grow at a 16.56% CAGR in the end-user segment because DTC models, guided usage, and e-commerce reduce access and affordability barriers.

What is changing competition among device makers and clinics?

Competition is shifting toward faster multi-wavelength systems, broader skin-tone coverage, stronger digital services, and larger clinic networks that can scale pricing and marketing.

Page last updated on: