US Prostate Laser Surgery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

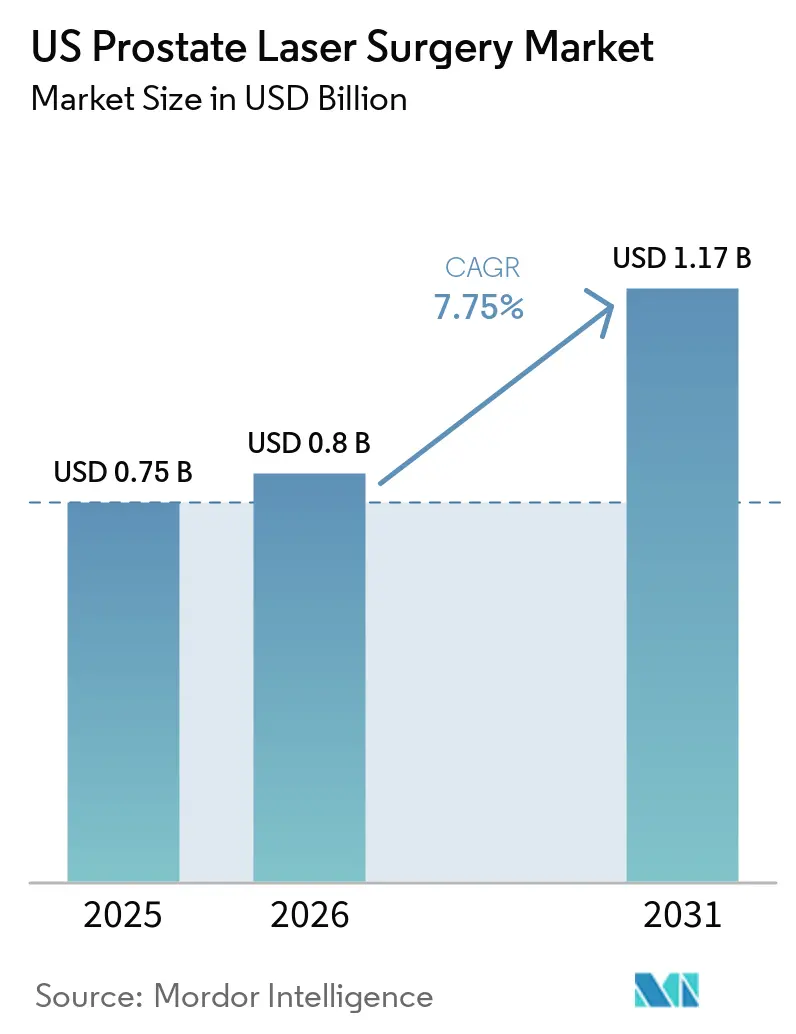

| Base Year Market Size (2025) | USD 0.75 Billion |

| Market Size (2026) | USD 0.8 Billion |

| Market Size (2031) | USD 1.17 Billion |

| Growth Rate (2026 - 2031) | 7.75% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

US Prostate Laser Surgery Market Analysis by Mordor Intelligence

The US Prostate Laser Surgery Market size is projected to be USD 0.75 billion in 2025, USD 0.8 billion in 2026, and reach USD 1.17 billion by 2031, growing at a CAGR of 7.75% from 2026 to 2031.

The United States prostate laser surgery market is growing due to an aging patient population with complex medical needs. Laser procedures offer a lower bleeding risk compared to traditional resection methods. Medicare data indicate a BPH/LUTS prevalence of 29% to 35% among men aged 65 and older, with 600,000 new cases identified annually.[1]National Institute of Diabetes and Digestive and Kidney Diseases, “Urologic Diseases in America Annual Data Report, Benign Prostatic Hyperplasia and Associated Lower Urinary Tract Symptoms,” U.S. Department of Health and Human Services, niddk.nih.gov The American Urological Association supports this trend by recognizing HoLEP and ThuLEP as size-independent surgical options and recommending them, along with photoselective vaporization, for patients at higher bleeding risk.

Laser procedures performed in these centers are more cost-effective for the healthcare system compared to equivalent hospital outpatient procedures. This cost advantage further supports the adoption of laser surgery in the United States.

Key Report Takeaways

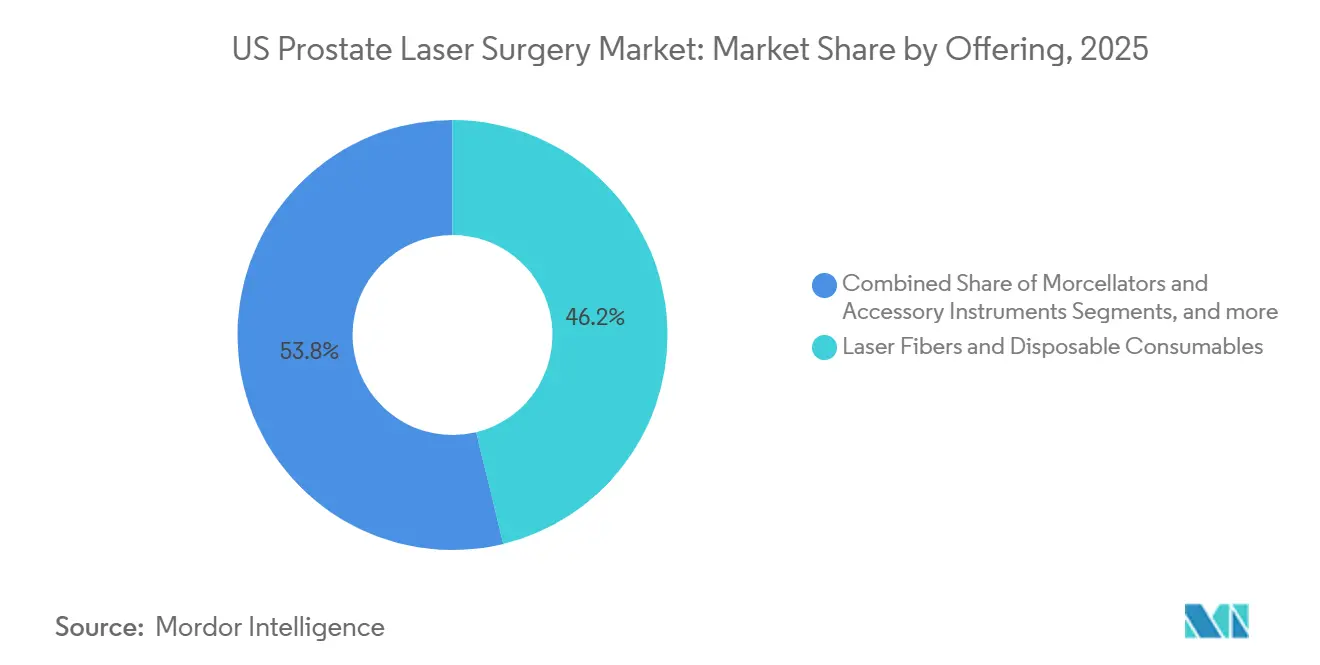

- By offering laser fibers and disposable consumables, which held 46.21% of revenue in 2025, while morcellators and accessory instruments recorded the highest projected CAGR at 8.12% through 2031.

- By procedure type, photoselective vaporization of the prostate accounted for 40.45% of revenue in 2025, while thulium fiber laser enucleation of the prostate is projected to expand at a 7.12% CAGR through 2031.

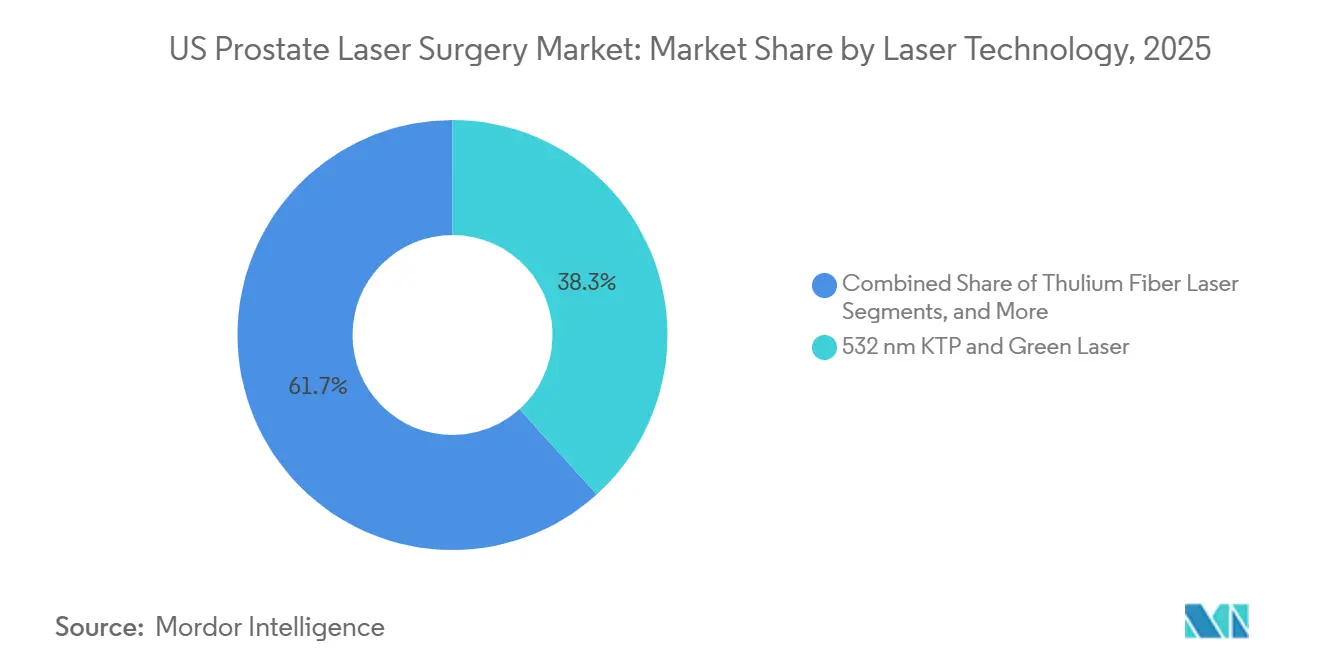

- By laser technology, the 532 nm KTP and green laser segment held 38.30% of revenue in 2025, while the thulium fiber laser is projected to grow at a 9.10% CAGR through 2031.

- By site of care, hospital outpatient departments held 54.66% of the US prostate laser surgery market share in 2025, while ambulatory surgery centers are projected to grow at a 9.05% CAGR through 2031.

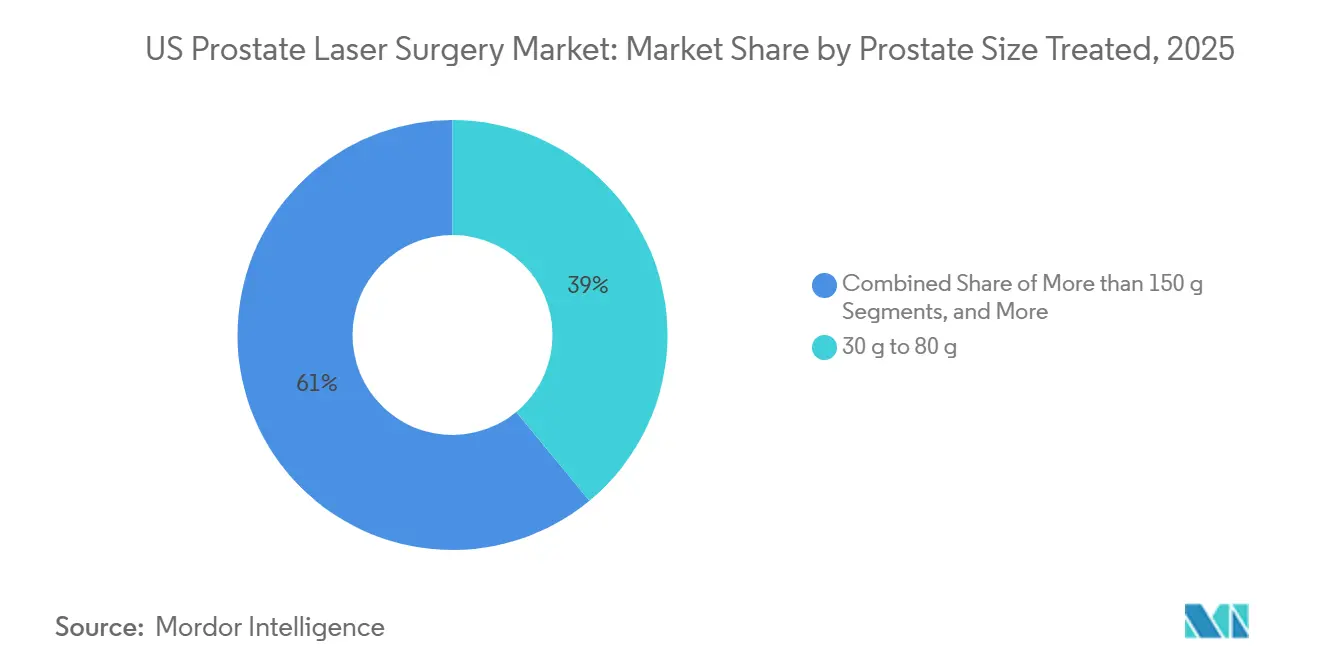

- By prostate size treated, the 30 g to 80 g segment accounted for 38.99% of the US prostate laser surgery market size in 2025, while the more-than-150 g segment is expected to grow at an 8.77% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

US Prostate Laser Surgery Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Aging US BPH burden and rising surgical complexity | +2.1% | National, with highest surgical burden concentration in Southeast and Midwest states | Long term (≥ 4 years) |

| Guideline-backed shift toward size-independent laser procedures | +1.8% | National, concentrated in academic and tertiary-care referral centers in Northeast and West Coast | Medium term (2-4 years) |

| Outpatient migration and bleeding-risk advantages | +1.3% | National, with early ASC penetration in Texas, Florida, and Arizona | Short term (≤ 2 years) |

| Wait-list pressure for catheter-dependent BPH patients | +0.9% | National, most acute in community hospital and rural settings with limited surgeon access | Medium term (2-4 years) |

| Compact plug-and-play platforms expand market reach | +0.7% | National, with earliest penetration in smaller ASCs and office-based urology suites | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging US BPH Burden and Rising Surgical Complexity

The aging male population in the United States, particularly those with BPH and LUTS, is driving the prostate laser surgery market. BPH prevalence among men aged 65 and older ranged from 29% to 35% annually in Medicare populations, with 600,000 new cases identified each year. This group, burdened with comorbidities like hypertension (81%), coronary artery disease (39%), and diabetes (35%), increasingly prefers procedures offering better hemostasis and simpler perioperative management.[2]American Urological Association, “Benign Prostatic Hyperplasia (BPH) Guideline,” AUA Quality and Guidelines, auanet.org Despite this, only 2% of BPH surgeries involved enucleation from 2014 to 2023, indicating significant growth potential as referrals shift to high-volume laser centers equipped for complex cases.

Guideline-Backed Shift Toward Size-Independent Laser Procedures

The United States prostate laser surgery market gained momentum when the AUA recommended HoLEP and ThuLEP as size-independent solutions for LUTS and BPH, alongside GreenLight PVP for patients at higher bleeding risk. This guidance removed the perception that enucleation is only for large glands. Academic centers have already seen laser enucleation rise from 13.7% of BPH surgeries 27.7% in early 2024, with annual utilization increasing by 52%. Community practices are also aligning with these guidelines, ensuring evidence-based case selection over outdated practices.

Outpatient Migration and Bleeding-Risk Advantages

The United States prostate laser surgery market is benefiting from the shift to outpatient care. Most prostate laser procedures are now performed in outpatient settings, supported by Medicare reimbursement favoring ASCs over hospital outpatient departments. A 2025 review showed 91% of HoLEP patients achieved same-day discharge with fewer complications than inpatient cases. Laser procedures for anticoagulated patients reduce scheduling and recovery challenges, enabling streamlined same-day care.[3]James W. Greenberg et al., “Contemporary Trends of Benign Prostatic Hyperplasia Procedures in the AUA Quality Registry, Are We Moving the Needle Toward More Minimally Invasive Treatments?,” AUA Journals, auajournals.org This trend is driving demand for disposable fibers and accessories, as ASCs prefer single-use workflows.

Wait-List Pressure for Catheter-Dependent BPH Patients

The United States prostate laser surgery market faces a backlog of patients awaiting care. A study on 91 BPH patients in urinary retention awaiting HoLEP reported a median wait time of 220 days, with complications in 56% of cases, including urinary tract infections (63%), hematuria (47%), and urosepsis (16%). The median care cost per patient was USD 5,315.95, highlighting clinical and financial burdens. Patients delayed over six months from catheterization to surgery had a 2.11 times higher treatment failure risk compared to catheter-naive peers. Addressing this backlog requires more trained surgeons and operating room access to convert delayed cases into procedures.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| HoLEP And ThuLEP Training Bottleneck | -0.6% | National, most acute in rural and non-academic community hospital settings | Long term (≥ 4 years) |

| Non-Laser BPH Alternatives Divert Capital And Case Volume | -0.8% | National, particularly in office-based and ASC settings competing for 30-80 g prostate cases | Medium term (2-4 years) |

| Tissue-Free Vaporization Reduces Incidental Pathology Yield | -0.4% | National, most acute in rural and non-academic community hospital settings | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

HoLEP and ThuLEP Training Bottleneck

The United States prostate laser surgery market faces a significant challenge in surgeon training. As of 2024, only 12% of endourology fellowships in the country included formal HoLEP training, and 25% of surveyed HoLEP surgeons reported not teaching the technique. Achieving proficiency in HoLEP and ThuLEP typically requires 40 to 60 supervised cases, a hurdle for community hospitals with limited procedure volumes. This has created a divide where academic and regional centers advance enucleation expertise, while community practices focus on PVP or non-laser MIST. Without scalable training pathways, growth in the United States prostate laser surgery market will remain uneven across regions and facility types.

Non-Laser BPH Alternatives Divert Capital and Case Volume

The United States prostate laser surgery market competes with non-laser BPH therapies that require lower capital investment and simpler office setups. Established options like UroLift, Rezūm, and aquablation have strong clinical evidence and reimbursement frameworks, diverting demand from laser surgeries. In June 2025, Boston Scientific's Rezūm system received FDA clearance to treat prostates up to 150 cm³, encroaching on a segment traditionally served by laser procedures. PROCEPT BioRobotics has also strengthened aquablation's position for larger prostates, with studies showing comparable efficacy to laser enucleation and reduced ejaculatory dysfunction.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Consumables Economics Underpin Recurring Revenue Dominance

In 2025, Laser Fibers and Disposable Consumables contributed 46.21% of the revenue, making them the largest offering in the United States prostate laser surgery market. This reflects the recurring revenue model, as each HoLEP or ThuFLEP procedure requires single-use fibers and related items. With case volumes expected to rise from 2026 to 2031, this category will remain a reliable revenue stream, scaling directly with procedure counts.

Capital Laser Systems held a smaller share but are critical for driving future disposable demand. Each new platform placed in an ASC or community hospital secures long-term accessory and fiber usage. Morcellators and Accessory Instruments, growing at 8.12% CAGR through 2031, are driven by the increasing adoption of enucleation procedures, where morcellation is essential post-adenoma separation.

By Procedure Type: Enucleation's Evidence Base Challenges PVP's Procedural Primacy

Photoselective Vaporization of the Prostate (PVP) accounted for 40.45% of procedure-type revenue in 2025, maintaining its lead in the United States prostate laser surgery market. Its dominance stems from widespread adoption, familiarity with the GreenLight platform, and suitability for lower-complexity cases in outpatient settings. However, enucleation procedures are steadily gaining traction, reshaping the procedural mix.

Laser enucleation increased from 13.7% of BPH surgical procedures in 2018 to 24.4% in 2021-2022 across academic centers. Thulium Fiber Laser Enucleation of the Prostate, growing at 7.12% CAGR through 2031, is supported by FDA clearances and clinical evidence. This shift creates a balanced procedure mix, with PVP retaining its broad base and enucleation expanding in complex cases.

By Laser Technology: Thulium Fiber Laser Accelerates While Green Laser Defends Its Base

The 532 nm KTP and Green Laser segment held 38.30% of technology revenue in 2025, leading the United States prostate laser surgery market. Its position is supported by a large installed base, clinical history, and alignment with bleeding-risk indications. However, its narrower procedural range compared to thulium platforms limits its versatility.

Thulium fiber laser, growing at 9.10% CAGR through 2031, is gaining traction due to its procedural flexibility and recent FDA-cleared systems. Holmium:YAG systems remain relevant due to surgeon familiarity and their role in enucleation-heavy programs, creating a competitive landscape as providers weigh mature platforms against newer options.

By Site of Care: Ambulatory Surge Redefines Capital and Consumable Demand Geography

Hospital Outpatient Departments (HOPDs) accounted for 54.66% of site-of-care revenue in 2025, maintaining their lead in the United States prostate laser surgery market. Their dominance is attributed to high-powered lasers, anesthesia support, and trained teams, making them the preferred setting for complex cases. However, alternative care models are emerging.

Ambulatory Surgery Centers (ASCs), growing at 9.05% CAGR through 2031, are gaining traction due to compact platforms and same-day discharge protocols. A systematic review in 2025 reported 91% same-day discharge for HoLEP patients, driving faster growth in ambulatory settings compared to hospitals. Disposable fibers benefit from ASCs' preference for streamlined workflows.

By Prostate Size Treated: Very-Large-Gland Volume Reshapes the Procedure Mix

In 2025, the 30 g to 80 g prostate-size band accounted for 38.99% of revenue, making it the largest treated-size segment in the United States prostate laser surgery market. This range covers most BPH referrals and is served by multiple technologies, though it faces competition from non-laser MIST therapies.

The more-than-150 g cohort is projected to grow at 8.77% CAGR through 2031, driven by laser enucleation's ability to manage very large glands endoscopically. Evidence supports ThuFLEP's non-inferiority to HoLEP for large-gland enucleation, while aquablation adds competitive pressure with comparable efficacy and reduced ejaculatory dysfunction in large prostates.

Geography Analysis

In 2025, Hospital Outpatient Departments accounted for 54.66% of the United States prostate laser surgery market share. This reflects a trend where large urban and suburban health systems dominate procedural volumes. The Southeast and Midwest states experience the highest surgical demand due to aging male populations and a significant chronic disease burden. Additionally, academic and tertiary-care referral centers in the Northeast and West Coast lead the market, driven by early adoption of enucleation training and advanced case management practices.

Ambulatory Surgery Centers (ASCs) are projected to grow at a 9.05% CAGR through 2031, strengthening the United States prostate laser surgery market in Sun Belt states like Texas, Florida, and Arizona. These regions attract investments due to their aging populations, high procedural demand, and readiness to adopt compact laser platforms. This shift moves growth opportunities from traditional hospital campuses to cost-efficient outpatient networks, increasing the importance of vendors capable of supporting deployment, training, and disposables across dispersed ASC networks.

Community hospitals and rural areas face significant training challenges, limiting their ability to meet surgical demand. Catheter-dependent BPH patients in these regions experience acute wait-list pressures, leading to complications from delayed treatment and higher failure rates after prolonged catheterization. Consequently, the growth of the United States prostate laser surgery market is influenced as much by provider capacity as by patient demand.

Competitive Landscape

In the US prostate laser surgery market, Boston Scientific, Olympus, and KARL STORZ dominate the capital-system level, leveraging their established training ecosystems, extensive service coverage, and long-standing clinical credibility in hospital-based urology. Below this top tier, the market becomes more fragmented. Specialist firms like biolitec, OmniGuide, LISA Laser, Quanta System, and Dornier MedTech are competing through technology differentiation rather than scale. The disposable segment is even less concentrated, with multiple fiber suppliers vying for attention based on compatibility, pricing, and single-use convenience.

Recent moves by companies highlight a trend: vendors are expanding their focus beyond just laser hardware. For instance, in May 2026, Olympus made headlines with a USD 270 million deal to acquire BioProtect, signaling its ambition to broaden its footprint in prostate care, venturing into both oncology and urology procedures.

The supply side of the US prostate laser surgery market is buzzing with activity. Thulium platforms, once considered niche, are now gaining traction in the commercial realm. In September 2025, the Elyra and Elyra Plus Thulium Fiber Laser Systems secured FDA 510(k) clearance for BPH ablation, LEP, and laser resection, offering providers another option for platform upgrades. Following a July 2025 FDA nod, biolitec swiftly obtained CE marking in August 2025, bolstering its position in both markets and underscoring the global nature of thulium competition. The primary growth opportunities lie in facilitating easier surgeon adoption, particularly with tools that minimize technique variability during enucleation and bolster community-site training.

US Prostate Laser Surgery Industry Leaders

-

Boston Scientific Corporation

-

Cook Medical LLC

-

Olympus Corporation

-

Teleflex Incorporated

-

Richard Wolf GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Olympus Corporation finalized an agreement to acquire BioProtect Ltd. for USD 270 million, to expand Olympus's urology and prostate cancer portfolio beyond laser and endoscopy devices.

- March 2026: Boston Scientific received FDA 510(k) clearance for the Asurys Fluid Management System, designed for irrigation and distention in endoscopic urologic procedures. The system was launched in the US market as a workflow tool for high-volume laser programs.

- September 2025: The Elyra Thulium Fiber Laser System and Elyra Plus received FDA 510(k) clearance for prostate laser surgery applications, broadening the US thulium fiber laser market within a 12-month period.

- August 2025: biolitec obtained CE marking for the LEONARDO Duster Super Pulsed Thulium Fiber Laser, complementing its FDA approval in July 2025 and enabling dual-market deployment for BPH enucleation and laser lithotripsy.

US Prostate Laser Surgery Market Report Scope

As per the scope of the report, prostate laser surgery is a minimally invasive procedure that uses concentrated light energy to remove or shrink excess prostate tissue blocking urine flow. It is primarily used to treat Benign Prostatic Hyperplasia (BPH).

The US prostate laser surgery market is segmented by offering, procedure type, laser technology, site of care, and prostate size treated. By offering, the market includes capital laser systems, laser fibers and disposable consumables, morcellators and accessory instruments, and service, maintenance, and software. By procedure type, the market is segmented into photoselective vaporization of the prostate, holmium laser enucleation of the prostate, thulium laser enucleation of the prostate, thulium fiber laser enucleation of the prostate, thulium laser vaporization and vaporesection, and diode laser vaporization. By laser technology, the market is categorized into 532 nm KTP and green laser, holmium:YAG laser, thulium fiber laser, thulium:YAG laser, and diode laser. By site of care, the market is segmented into hospital inpatient, hospital outpatient department, ambulatory surgery center, and office-based urology suite. By prostate size treated, the market is segmented into less than 30 g, 30 g to 80 g, more than 80 g to 150 g, and more than 150 g. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Capital Laser Systems |

| Laser Fibers and Disposable Consumables |

| Morcellators and Accessory Instruments |

| Service, Maintenance and Software |

| Photoselective Vaporization of the Prostate |

| Holmium Laser Enucleation of the Prostate |

| Thulium Laser Enucleation of the Prostate |

| Thulium Fiber Laser Enucleation of the Prostate |

| Thulium Laser Vaporization and Vaporesection |

| Diode Laser Vaporization |

| 532 nm KTP and Green Laser |

| Holmium:YAG Laser |

| Thulium Fiber Laser |

| Thulium:YAG Laser |

| Diode Laser |

| Hospital Inpatient |

| Hospital Outpatient Department |

| Ambulatory Surgery Center |

| Office-Based Urology Suite |

| Less than 30 g |

| 30 g to 80 g |

| More than 80 g to 150 g |

| More than 150 g |

| By Offering | Capital Laser Systems |

| Laser Fibers and Disposable Consumables | |

| Morcellators and Accessory Instruments | |

| Service, Maintenance and Software | |

| By Procedure Type | Photoselective Vaporization of the Prostate |

| Holmium Laser Enucleation of the Prostate | |

| Thulium Laser Enucleation of the Prostate | |

| Thulium Fiber Laser Enucleation of the Prostate | |

| Thulium Laser Vaporization and Vaporesection | |

| Diode Laser Vaporization | |

| By Laser Technology | 532 nm KTP and Green Laser |

| Holmium:YAG Laser | |

| Thulium Fiber Laser | |

| Thulium:YAG Laser | |

| Diode Laser | |

| By Site of Care | Hospital Inpatient |

| Hospital Outpatient Department | |

| Ambulatory Surgery Center | |

| Office-Based Urology Suite | |

| By Prostate Size Treated | Less than 30 g |

| 30 g to 80 g | |

| More than 80 g to 150 g | |

| More than 150 g |

Key Questions Answered in the Report

What is the 2031 outlook for prostate laser surgery in the United States?

The US prostate laser surgery market is projected to reach USD 1.17 billion by 2031 from USD 0.80 billion in 2026, growing at a 7.75% CAGR.

What is driving demand for laser surgery in BPH treatment?

Demand is being supported by an aging male population, high BPH and LUTS prevalence in Medicare populations, heavy comorbidity burden, and guideline support for laser procedures in bleeding-risk patients.

Which product category generates the most revenue?

Laser Fibers and Disposable Consumables led with 46.21% of revenue in 2025 because active programs consume fibers on a repeat basis with every case.

Which procedure type is growing the fastest?

Thulium Fiber Laser Enucleation of the Prostate is the fastest-growing procedure type, with a projected 7.12% CAGR through 2031.

Why are ambulatory surgery centers becoming more important?

ASCs are projected to grow at a 9.05% CAGR through 2031 because same-day discharge pathways are improving and compact platforms are making outpatient deployment easier.

What is the main barrier to broader enucleation adoption?

The biggest barrier is training capacity, since HoLEP and ThuLEP require meaningful supervised case volume and many US programs still do not teach the technique at scale.

Page last updated on: