Hair Removal Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

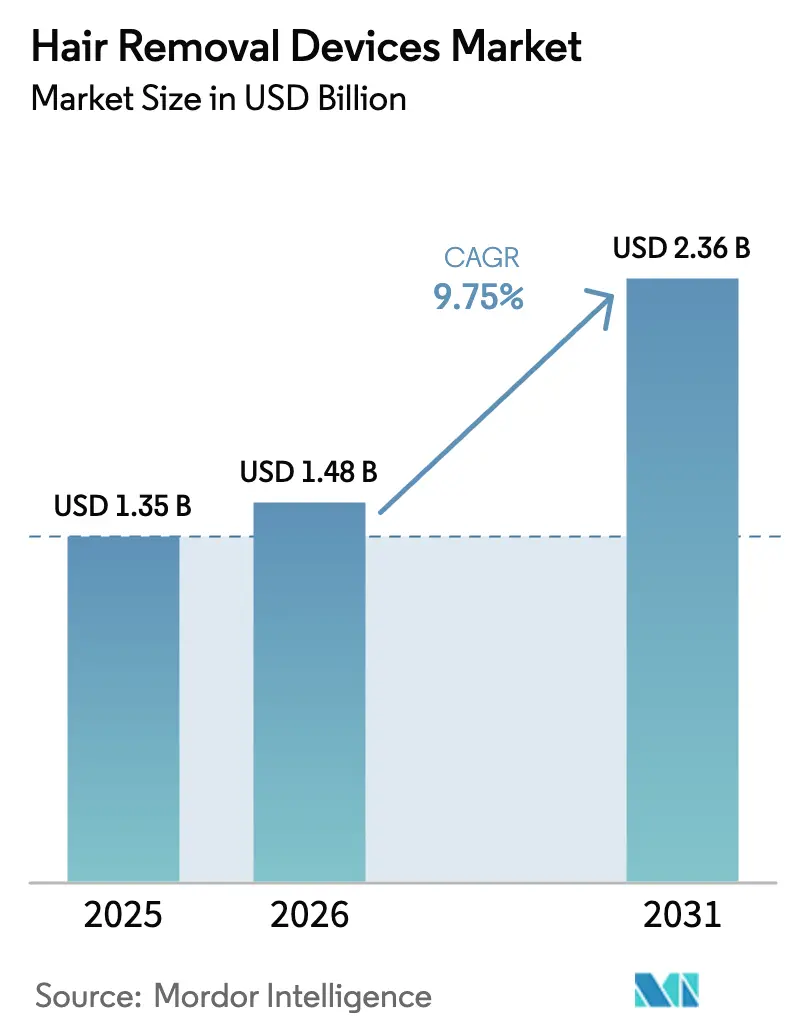

| Market Size (2026) | USD 1.48 Billion |

| Market Size (2031) | USD 2.36 Billion |

| Growth Rate (2026 - 2031) | 9.75% CAGR |

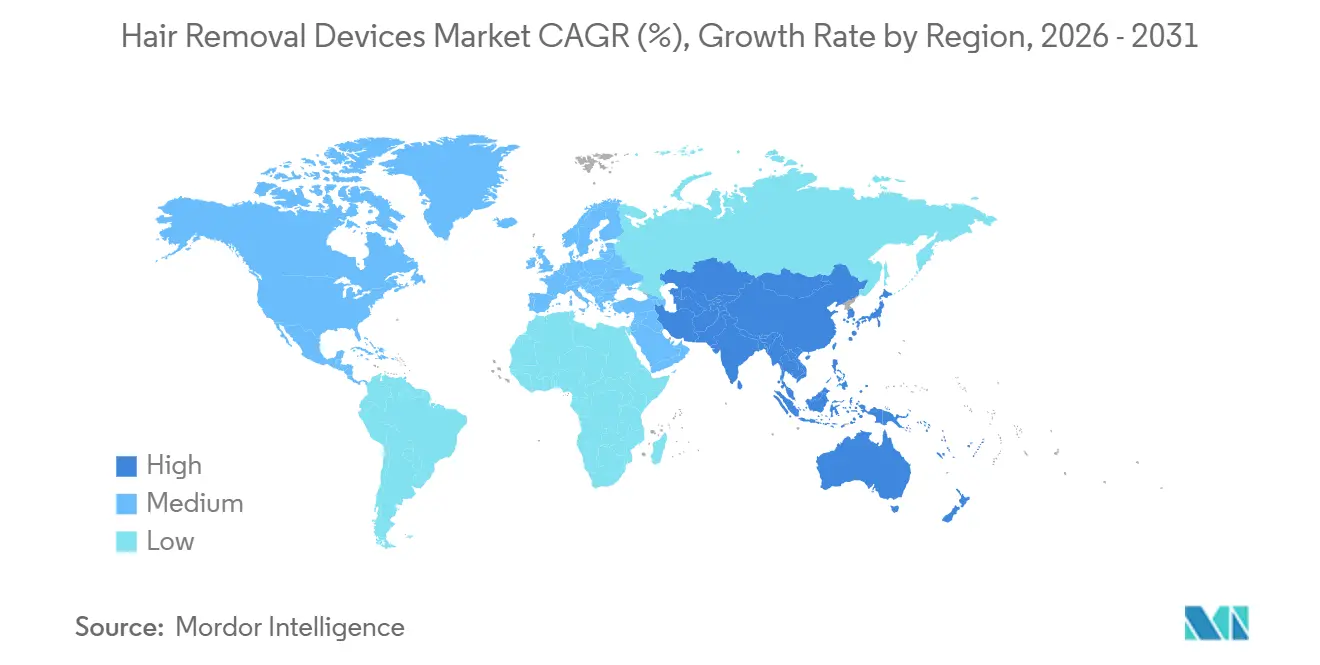

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hair Removal Devices Market Analysis by Mordor Intelligence

The Hair Removal Devices Market size was valued at USD 1.35 billion in 2025 and is estimated to grow from USD 1.48 billion in 2026 to reach USD 2.36 billion by 2031, at a CAGR of 9.75% during the forecast period (2026-2031).

The growth trajectory stems from converging factors such as gender-affirming care coverage, AI-enabled skin-tone matching that expands safe treatment to Fitzpatrick IV–VI users, and regulatory harmonization that shortens device-approval cycles. Manufacturers now emphasize software-driven personalization over raw energy output, while lower device prices and bundled e-commerce offerings shift purchasing power toward consumers. Competitive strategies revolve around consumable lock-ins in professional channels and subscription models in direct-to-consumer sales. Regulatory agencies intensify post-market surveillance, raising entry barriers for low-quality imports yet rewarding brands that combine clinical efficacy with robust safety features.

Key Report Takeaways

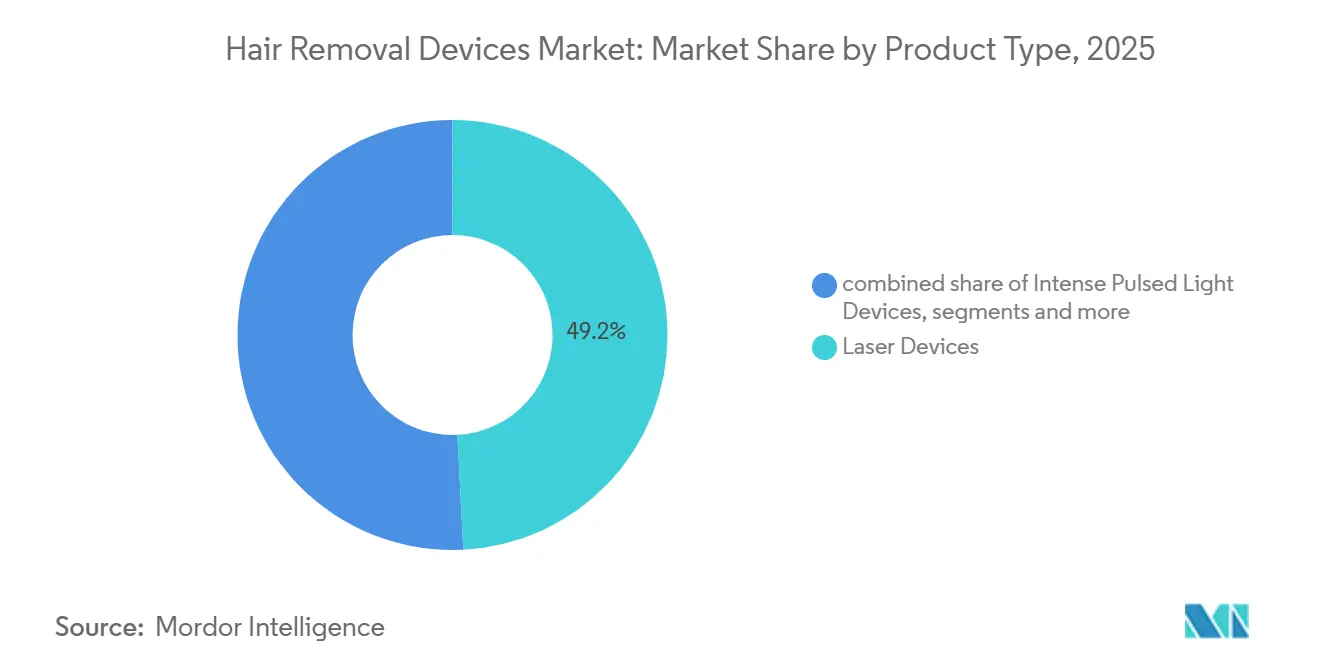

- By product type, Laser Devices led with 49.2% of the Hair Removal Devices market share in 2025. Intense Pulsed Light Devices are forecast to expand at a 10.32% CAGR through 2031.

- By treatment area, Legs and arms captured 34.34% of Hair Removal Devices market share in 2025. Bikini and other intimate-zone treatments are projected to expand at a 12.45% CAGR through 2031.

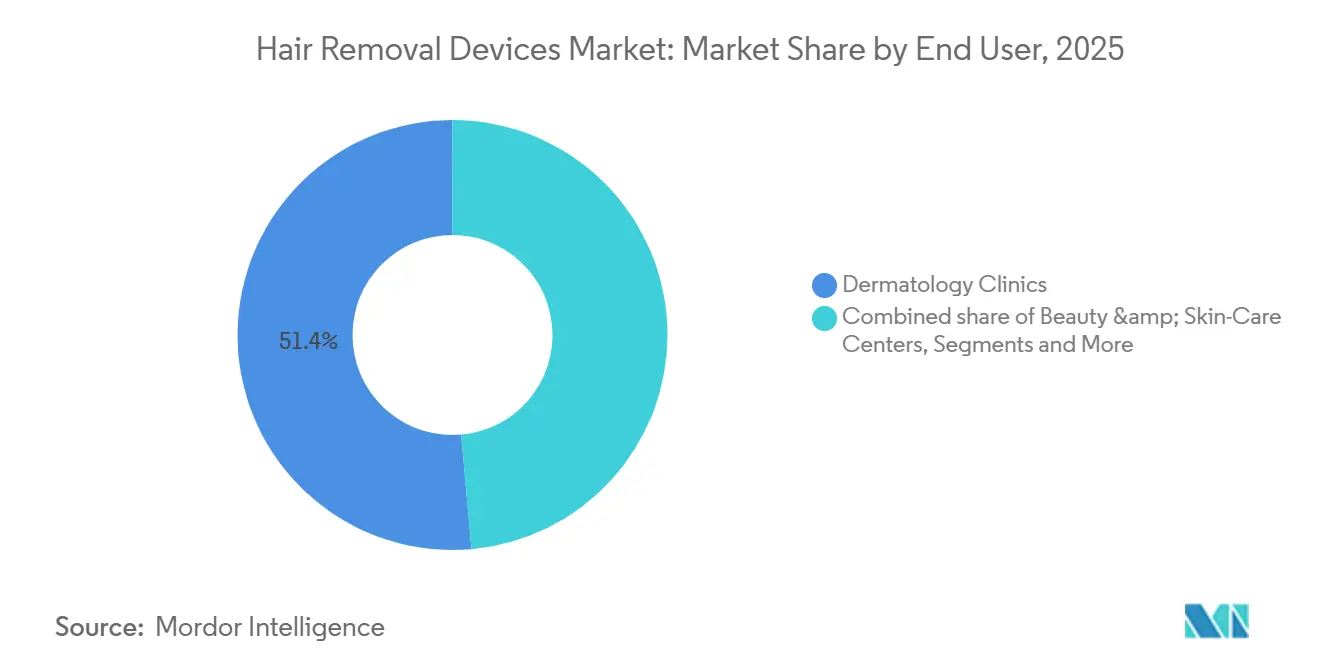

- By end user, Dermatology Clinics commanded a 51.4% share of the Hair Removal Devices market size in 2025. Home-use Consumers are advancing at an 11.32% CAGR between 2026 and 2031.

- By geography, North America held 43.4% of the Hair Removal Devices market share in 2025. Asia-Pacific is projected to grow at a 10.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hair Removal Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Innovative & technologically advanced devices | +2.1% | North America, Western Europe | Medium term (2–4 years) |

| Rising disposable incomes & personal-care spend | +1.8% | Asia-Pacific core, Latin America | Long term (≥ 4 years) |

| Growth in non-invasive aesthetic procedures | +1.5% | North America, European Union, GCC | Medium term (2–4 years) |

| E-commerce-driven at-home device adoption | +2.3% | North America, China | Short term (≤ 2 years) |

| AI-driven personalization for broader skin-tone coverage | +1.4% | Global, critical for APAC & MEA markets | Medium term (2-4 years) |

| Insurance pilots for gender-affirming care reimbursements | +0.7% | North America, select EU markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

The Advent of Innovative & Technologically Advanced Devices

Manufacturers embed real-time skin-tone sensors and adaptive energy modulation in both professional and consumer platforms, closing the efficacy gap that once confined laser hair removal to lighter skin. Philips launched the Lumea Prestige with SenseIQ in late 2025, integrating a spectrophotometer that auto-calibrates fluence across 250,000 pulses, extending safe use to Fitzpatrick IV–VI users [1]Philips, “Lumea Prestige IPL Hair Removal Device,” philips.com. FDA clearances for multiple AI-enabled IPL devices from Shenzhen-based firms in 2024–2025 underscore a shift toward software-defined performance. Competitive advantage now hinges on algorithm quality rather than proprietary laser cavities, enabling nimble entrants to challenge incumbents without massive capital investment. Device lifecycles shorten as over-the-air firmware updates add features post-sale, fostering brand loyalty through continual performance improvements. This dynamic positions technology leadership as a decisive growth catalyst for the hair removal devices market.

Rising Disposable Incomes & Personal-Care Spend

Household disposable income growth in Southeast Asia and Latin America fuels discretionary spending on grooming solutions that promise long-term cost savings. China’s urban middle class expanded 12% between 2024 and 2025, spurring sales of at-home IPL devices priced between USD 200 and USD 400. Ulike shipped more than 2 million units in 2025 by targeting tier-2 and tier-3 cities with limited clinic access. Comparable trends in Brazil and Mexico mirror this substitution effect, where repeated salon visits cost more than a single device purchase within eighteen months. Rising incomes, therefore, accelerate penetration beyond metropolitan centers, broadening the addressable base for the Hair Removal Devices market.

Growth in Non-Invasive Aesthetic Procedures

Laser hair removal topped global non-surgical aesthetic procedures in 2024 with 1.9 million treatments, a 7% year-over-year increase. High procedure volumes strain clinic capacity, extending wait times and nudging time-sensitive clients toward do-it-yourself solutions. The proliferation of medical spas normalizes energy-based hair removal but also triggers regulatory interventions; cease-and-desist orders in Texas during 2025 highlight the need for licensed operation. As compliance costs rise, some operators reposition as premium providers offering value-added skin assessments. Increased procedural visibility, coupled with supply-side constraints, therefore creates parallel demand streams for both professional and home channels, reinforcing expansion of the hair removal devices market.

Surge in E-Commerce-Driven At-Home Device Adoption

Direct-to-consumer channels now account for the majority of at-home device sales. Tria Beauty launched a cartridge-free diode laser in early 2025 at USD 449, eliminating recurring consumable costs and strengthening its one-time value proposition. E-commerce platforms integrate AI recommendation engines that bundle treatment guides with skincare, lifting average order values significantly. Subscription models, such as Ulike’s Air 10 kit priced at USD 49 per quarter, convert one-off purchases into recurring revenue streams. These developments reduce information asymmetry, flatten global launch cycles, and embed software updates that refine device performance, boosting near-term growth in the hair removal devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance |

|---|---|---|

| High Device & Treatment Costs | -1.8% | Global, with acute pressure in Asia-Pacific, Middle East & Africa, and South America where disposable incomes lag; home-use segment faces steeper price elasticity |

| Risk of Adverse Skin Reactions: Need for Skilled Operators | -1.2% | Global, particularly pronounced in markets with limited dermatology training infrastructure; APAC and MEA face operator-skill gaps that slow clinic expansion |

| Limited Insurance Coverage for Cosmetic Procedures | -1.0% | Global, with sharper impact in North America and Europe where out-of-pocket healthcare spending sensitivity is rising; emerging markets already assume self-pay models |

| Counterfeit Devices & Forthcoming Stricter Emission Norms | -0.7% | Counterfeit prevalence highest in Asia-Pacific and select MEA markets; emission-standard tightening affects all regions but compliance costs weigh more on smaller manufacturers globally |

| Source: Mordor Intelligence | ||

High Device & Treatment Costs

Professional sessions cost USD 200–400, with full protocols exceeding USD 3,000, limiting access for median-income consumers [2]American Academy of Dermatology, “Laser Hair Removal,” aad.org. At-home devices priced from USD 200 to USD 600 remain a significant discretionary outlay in regions where monthly disposable income falls below USD 500. Limited installment financing outside North America further constrains uptake, as fewer than 15% of e-commerce platforms offered pay-later plans in 2025. While declining component prices help, affordability remains a gating factor that tempers absolute growth in the hair removal devices market.

Risk of Adverse Skin Reactions & Need for Skilled Operators

The FDA logged more than 200 adverse event reports related to laser and IPL hair removal in 2024, citing burns and hyperpigmentation, with the majority of cases involving at-home devices [3]U.S. Food and Drug Administration, “Intense Pulsed Light Hair Removal Devices for Home Use,” fda.gov. Operator licensing varies: California mandates 600 hours of electrology training, while Texas allows medical assistants under indirect supervision, creating safety inconsistencies. Manufacturers add fail-safes, yet these raise bill-of-materials costs. Heightened regulatory scrutiny following the FDA’s October 2025 RF advisory may soon extend to laser and IPL platforms, posing compliance risks that could slow professional-channel expansion and dampen momentum in the hair removal devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: IPL Gains on Multi-Wavelength Versatility

Laser Devices maintained a 49.2% share in 2025, yet Intense Pulsed Light Devices will outpace them at a 10.32% CAGR through 2031. IPL units cost USD 15,000–40,000 for clinics versus USD 60,000–150,000 for medical-grade lasers, and at-home IPL devices retail below USD 400, broadening reach among first-time buyers. Philips’ 2025 corded Lumea model at USD 299 illustrates price-led penetration in Eastern Europe and Latin America. Hybrid platforms like Venus Concept’s Epileve, combining IPL with bipolar RF, reduce adverse events by 35% in clinical trials, appealing to clinics that serve diverse skin tones. Although an October 2025 FDA advisory on RF microneedling created temporary hesitation, software-controlled pulse durations and sapphire cooling continue to make IPL an attractive alternative, propelling segment revenue within the Hair Removal Devices market.

Other energy-based platforms, including fractional lasers and E-light hybrids, address niche needs such as pseudofolliculitis barbae in Fitzpatrick V–VI populations. FDA-cleared picosecond lasers minimize epidermal melanin absorption, a refinement that may help lasers recapture share if long-term efficacy data holds. The evolving competitive canvas underscores how multi-wavelength versatility and AI-enabled personalization drive purchasing decisions, cementing IPL’s role as the fastest-growing segment in the Hair Removal Devices market.

By Treatment Area: Intimate Zones Outpace Traditional Segments

Legs and arms captured 34.34% of Hair Removal Devices market share in 2025, underscoring the appeal of treating the largest and most visible body areas first. Yet bikini and other intimate-zone treatments are projected to expand at a 12.45% CAGR through 2031 as shifting attitudes toward body hair, combined with the privacy of do-it-yourself platforms, motivate users to move beyond legacy waxing routines. At-home IPL systems with precision tips such as Philips Lumea’s 2 cm² cartridge and Ulike models with adjustable intensity, let consumers treat sensitive regions without the vulnerability of salon visits.

Discretion resonates most with first-time buyers aged 18–34, who view full-body grooming as part of everyday self-care rather than a special-occasion service. These trends collectively position intimate-area solutions as the fastest-growing slice of the Hair Removal Devices market size over the forecast horizon.

By End User: Home Channels Disrupt Clinical Incumbents

Dermatology Clinics accounted for 51.4% of revenue in 2025, leveraging insurance coverage for gender-affirming care in select U.S. states to maintain pricing power. Yet Home-use Consumers are projected to grow at an 11.32% CAGR, fueled by influencer-led marketing and mobile apps that guide treatment intervals in real time. Armed with Bluetooth-enabled devices that log sessions, brands cultivate user data to upsell consumables and upgrades, transforming a one-time purchase into a lifetime relationship.

Regulatory crackdowns on unlicensed medical spas in Texas and Florida funnel budget-conscious consumers toward do-it-yourself alternatives, magnifying home-use gains. Hospitals remain a niche end user, typically applying laser hair removal adjunctively within reconstructive or gender-affirming surgeries. Meanwhile, beauty and skin-care centers navigate tightening rules by partnering with supervising physicians, but these collaborations raise overhead, squeezing margins. In sum, consumer empowerment and e-commerce efficiency reshape the revenue mix of the hair removal devices market.

Geography Analysis

North America captured 43.4% of the Hair Removal Devices market share in 2025, supported by high per-capita aesthetic spending and Medicaid pilots reimbursing laser treatments for gender-affirming care in California and New York. The FDA’s 2026 alignment of its Quality Management System Regulation with ISO 13485 shortens 510(k) clearance times by up to six months, accelerating product refresh cycles. Yet, fragmented state licensing complicates clinic expansion and prompts capital to favor low-overhead direct-to-consumer models.

Europe trails North America in absolute terms but benefits from CE-Mark harmonization that enables cross-border commerce. The European Medicines Agency’s 2025 mandate for annual adverse-event reporting filters out non-compliant imports, fortifying incumbents. Germany and France pilot reimbursement for laser hair removal tied to hirsutism diagnoses, signaling incremental institutional demand. The United Kingdom’s independent approval pathway offers a time-to-market hedge, letting manufacturers soft-launch devices in London before broader European roll-outs.

Asia-Pacific is the fastest-growing region, expected to deliver a 10.98% CAGR through 2031. China’s National Medical Products Administration cleared 18 new AI-driven IPL devices in 2024–2025, enabling domestic brands to compete on feature parity at 40–60% lower price points. Japan’s fast-track pathway for incremental innovations further accelerates introductions of sapphire cooling and picosecond lasers. India, though underpenetrated, recorded a 25% rise in dermatology clinic openings in 2025, indicating latent demand poised to materialize as incomes climb above USD 3,000 per capita. Middle East & Africa and South America present smaller but growing opportunities. Dubai’s bundled medical-tourism packages attract international patients seeking multi-procedure deals at prices 30–50% below U.S. equivalents. Brazil approved a dozen new laser and IPL devices in 2024, although tariffs inflate retail prices, limiting at-home adoption to affluent consumers.

Competitive Landscape

The Hair Removal Devices industry exhibits moderate concentration. The top five manufacturers—Lumenis, Candela Medical, Cutera, Hologic (Cynosure), and Philips held the majority of professional-channel revenue in 2025. Incumbents guard their positions via consumable lock-ins and multi-year service contracts that boost switching costs.

Simultaneously, they launch sub-USD 500 home devices to defend share: Lumenis introduced IPL Home Pro in January 2026 at USD 499, featuring 300,000 flashes and a skin-tone sensor. Disruptors like Ulike leverage influencer marketing and Bluetooth analytics to ship 2 million units in 2025, capturing price-sensitive segments. Strategic pivots toward hybrid energy platforms populate patent filings, with Venus Concept and Sciton licensing university algorithms rather than building proprietary cavities.

Regulatory risk intensifies: the FDA’s October 2025 advisory on RF devices compels manufacturers to allocate up to 15% of R&D budgets to post-market surveillance, a burden that pressures smaller entrants yet also elevates the credibility gap between cleared and counterfeit devices. Overall, competitive dynamics reward brands that balance clinical efficacy, price agility, and software-enabled personalization, sustaining expansion in the Hair Removal Devices market.

Hair Removal Devices Industry Leaders

Lumenis Be Ltd.

Candela Medical

Cutera

Hologic

Philips

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Lumenis unveiled the Stellar M22 with XPL Technology, expanding indication coverage to thirty conditions

- April 2025: Alma Lasers launched a special edition Soprano Titanium that delivers a 20% treatment-speed boost.

- January 2025: LEAFLIFE introduced the Rocozyer Depi, an "AI robot" laser hair removal machine that leverages intelligent technology and robotic automation for enhanced precision and efficiency in professional settings.

Global Hair Removal Devices Market Report Scope

As per the scope of the report, hair removal devices are non-invasive tools designed to remove unwanted hair by targeting the hair shaft or follicle, offering an alternative to traditional methods such as shaving, waxing, or chemical depilatories. Hair removal devices are commonly used in areas such as the face, legs, arms, underarms, and bikini line.

The hair removal devices market is segmented by product type, end user, and geography. By product type, the market is categorized into laser devices, intense pulsed light devices, and other energy-based devices. By end user, the segmentation includes dermatology clinics, beauty & skin-care centers, hospitals, and home-use consumers. Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Laser Devices | Diode Lasers |

| Alexandrite Lasers | |

| Nd:YAG Lasers | |

| Ruby Lasers | |

| Intense Pulsed Light Devices | |

| Other Energy-based Devices (e.g., RF, E-light) |

| Facial |

| Under-arm |

| Bikini & Intimate |

| Legs & Arms |

| Dermatology Clinics |

| Beauty & Skin-Care Centers |

| Hospitals |

| Home-use Consumers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of APAC | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of MEA | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Laser Devices | Diode Lasers |

| Alexandrite Lasers | ||

| Nd:YAG Lasers | ||

| Ruby Lasers | ||

| Intense Pulsed Light Devices | ||

| Other Energy-based Devices (e.g., RF, E-light) | ||

| By Treatment Area | Facial | |

| Under-arm | ||

| Bikini & Intimate | ||

| Legs & Arms | ||

| By End User | Dermatology Clinics | |

| Beauty & Skin-Care Centers | ||

| Hospitals | ||

| Home-use Consumers | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of APAC | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of MEA | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the Hair Removal Devices Market?

The market is expected to reach USD 1.48 billion in 2026 and is projected to reach USD 2.36 billion by 2031, advancing at a 9.75% CAGR over the forecast period.

Why are IPL platforms gaining adoption relative to lasers?

IPL devices treat a wider range of hair colors and skin types and cost significantly less.

Which region will add the most incremental revenue by 2031?

Asia-Pacific is expected to grow at a 10.98% CAGR through 2031, led by China’s rapid device approvals and lower-price domestic brands that undercut Western offerings significantly.

How is AI personalization helping reach darker skin tones?

Real-time skin-tone sensors and adaptive energy modulation, such as Philips SenseIQ, auto-calibrate fluence for Fitzpatrick IV–VI users, cutting adverse events significantly.

Which region has the biggest share in Hair Removal Devices Market?

In 2025, North America accounts for the largest market share in Hair Removal Devices Market.

Why are at-home buyers increasing faster than clinic patients?

E-commerce now drives the majority of at-home sales, with Bluetooth-enabled devices priced at USD 200-600 offering a lower entry point than professional protocols that exceed USD 3,000.

Page last updated on: