Laos Telecom Towers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

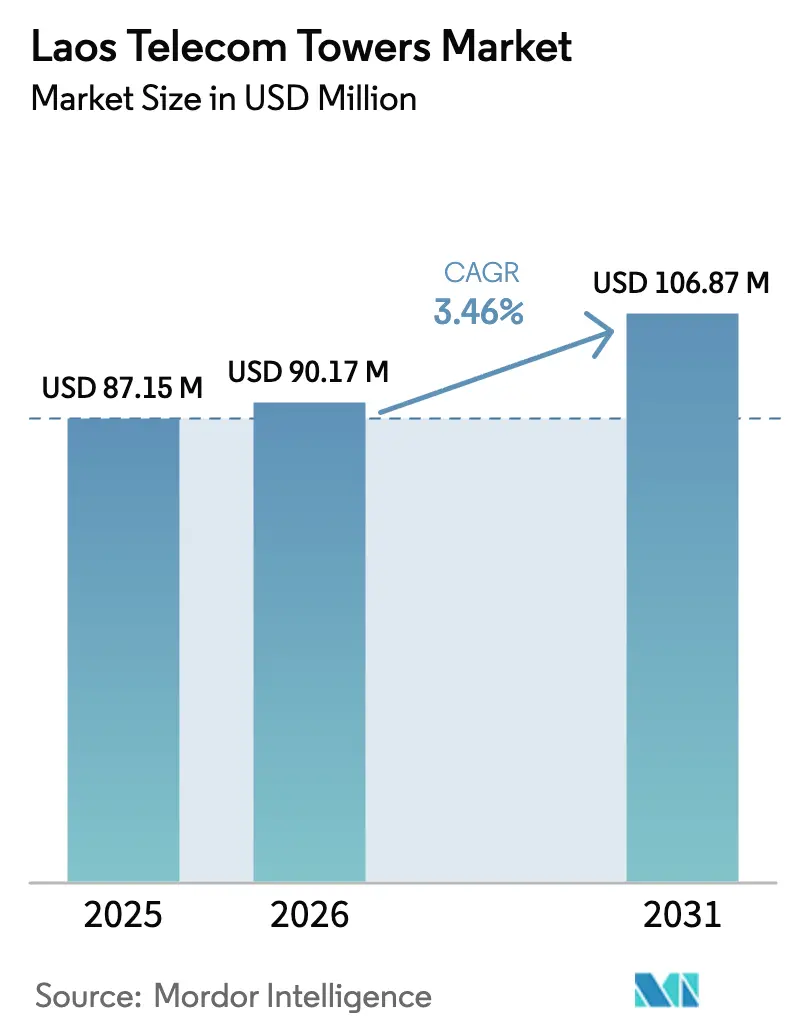

| Base Year Market Size (2025) | USD 87.15 Million |

| Market Size (2026) | USD 90.17 Million |

| Market Size (2031) | USD 106.87 Million |

| Growth Rate (2026 - 2031) | 3.46% CAGR |

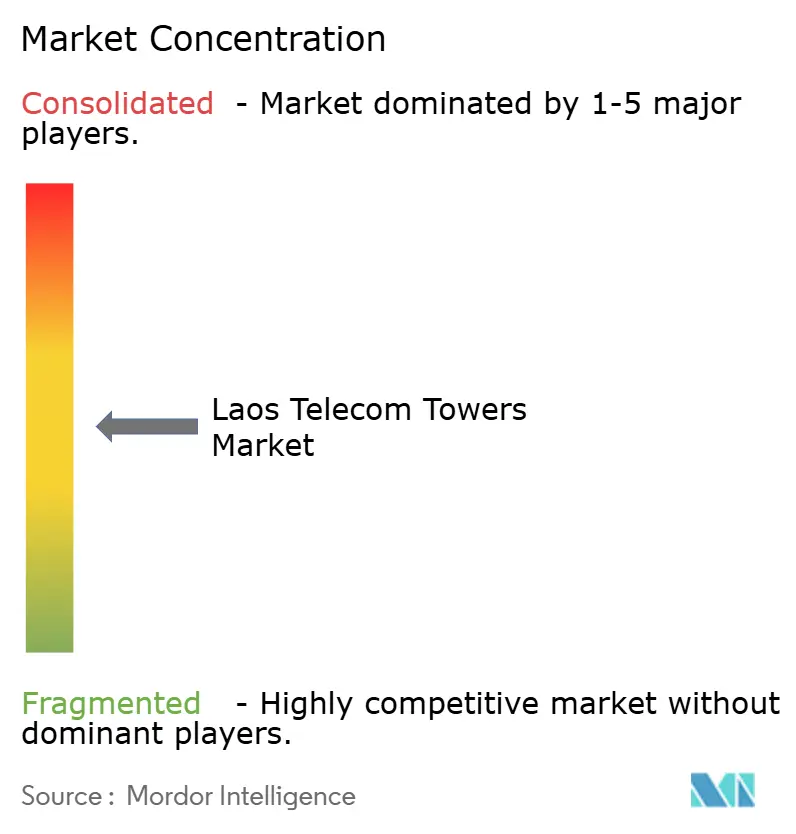

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Laos Telecom Towers Market Analysis by Mordor Intelligence

Laos Telecom Towers Market size in 2026 is estimated at USD 90.17 million, growing from 2025 value of USD 87.15 million with 2031 projections showing USD 106.87 million, growing at 3.46% CAGR over 2026-2031.

Growth is propelled by Laos’ position as the land-linked node for fiber and power corridors that connect Thailand, China, Vietnam, and Myanmar. Progressive passive-infrastructure-sharing guidelines issued in 2024, a surge in 5G densification projects, and renewable energy wheeling deals with neighboring grids together reinforce demand for new build-to-suit towers. Independent TowerCos are scaling faster than operator-owned models as mobile network operators focus capital on spectrum, while rooftop and stealth solutions gain traction in UNESCO-sensitive tourist areas. The mix of hydropower abundance and diesel-backup dependence shapes investment in hybrid and green power systems, and policy incentives tied to Laos’ Universal Service Fund narrow the rural connectivity gap.

Key Report Takeaways

- By ownership, operator-owned sites held 46.98% revenue in 2025, whereas independent TowerCos are advancing at a 11.58% CAGR through 2031.

- By installation, ground-based structures commanded 68.83% of the Laos telecom tower market share in 2025, while rooftop systems are forecast to grow at a 5.18% CAGR to 2031.

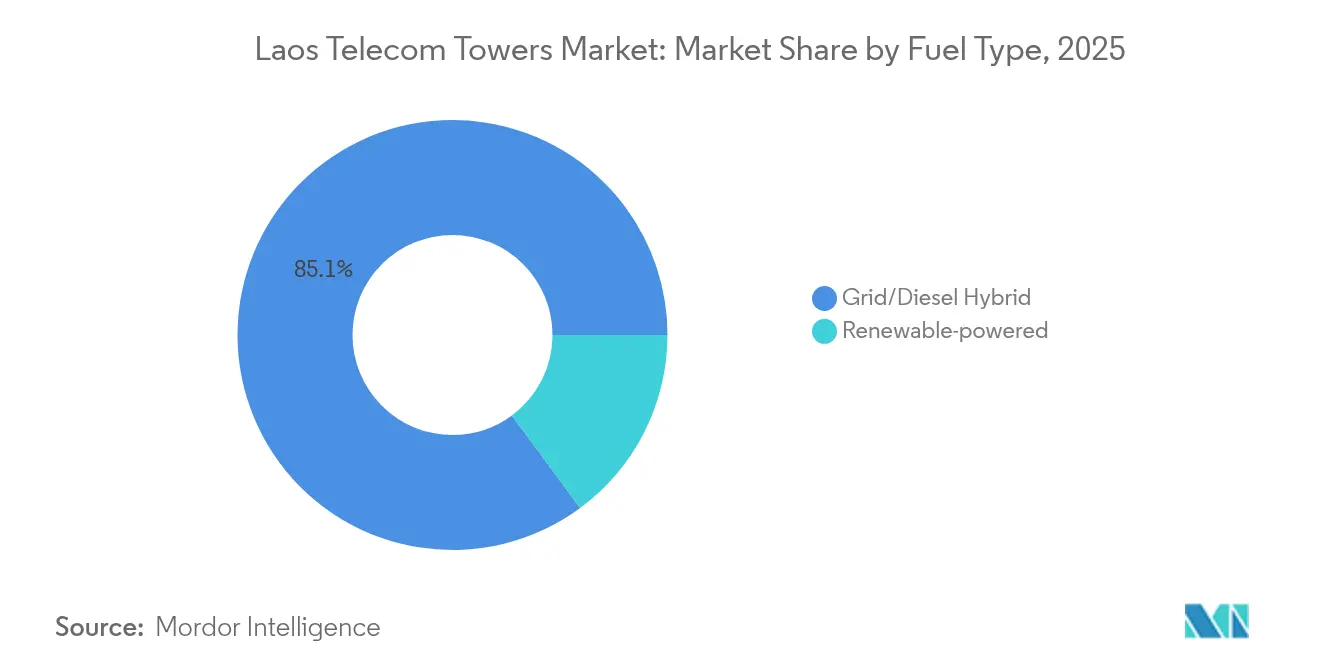

- By fuel type, grid/diesel hybrids accounted for 85.12% of the Laos telecom tower market size in 2025, whereas renewable-powered sites are projected to expand at a 19.84% CAGR through 2031.

- By tower type, monopole designs captured 40.12% of the Laos telecom tower market size in 2025, whereas stealth and concealed formats are on track for a 10.37% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Laos Telecom Towers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated 5G rollout commitments by Unitel and Lao Telecom | +1.2% | Vientiane, Luang Prabang, Pakse | Medium term (2-4 years) |

| Explosive mobile-data demand (>30% CAGR) fueling densification | +0.8% | Urban centers and tourist corridors | Short term (≤ 2 years) |

| Universal Service Fund subsidies for rural coverage (2024-2026) | +0.6% | Northern and southern rural provinces | Medium term (2-4 years) |

| Progressive passive-infrastructure-sharing guidelines (MPT, 2024) | +0.4% | Nationwide, early adoption in major cities | Long term (≥ 4 years) |

| Laos-China Railway corridor: co-location along 422 km fiber right-of-way | +0.3% | 422 km corridor Vientiane to the Chinese border | Long term (≥ 4 years) |

| Cross-border hydro power wheeling enabling 100% renewable tower sites | +0.2% | Border zones with Thailand, Vietnam, China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated 5G rollout commitments drive network densification

Unitel’s commercial 5G launch in November 2024 and Lao Telecom’s parallel expansion amplify tower demand by shifting planning from macro-coverage to small-cell density. Urban clusters now require three times the node count of 4G networks to deliver ultra-low-latency services. Independent TowerCos have responded: OCK Group signed a multi-tenant leasing deal with Best Telecom in May 2024 that earmarks new colocation sites expressly for 5G, illustrating how asset-light partnerships unlock faster rollouts [1]OCK Group, “Corporate Presentation 2025,” ock.com.my. Spectrum clarity under the 2021 Telecommunications Law further reduces investor risk. The outcome is a visible uplift in order books for tower suppliers across Vientiane, Pakse, and emerging economic zones.

Mobile-data explosion outpaces existing infrastructure capacity

Smartphone adoption and 37 government e-services pushed mobile-data traffic well above a 30% annual run rate, and average mobile download speeds jumped 17.8% in early 2025 [2]Laotian Times, “Digital Growth in Laos with Internet Faster by 17.8 Percent in Early 2025,” laotiantimes.com. Congestion is now acute along tourist routes such as Vang Vieng and the Plain of Jars, where seasonal visitors can double local traffic volumes. Operators are mitigating pressure through tower-sharing deals that deliver incremental capacity without linear capex. This data boom, therefore, cements the Laos telecom tower market as the critical bottleneck that determines user-experience gains.

Universal Service Fund subsidies unlock rural tower economics

The Universal Service Fund earmarks support through 2026 for villages where coverage falls below 50%. Subsidy design rewards facilities that host multiple operators, accelerating neutral-host adoption in mountainous districts where build costs can be triple the central-region average. By linking payouts to renewable power integration, the scheme simultaneously de-risks clean-energy deployments that replace trucked diesel, an expense that can consume 40% of annual operating budgets in off-grid areas [3]Asian Development Bank, “Lao PDR Energy Sector Assessment,” adb.org.

Infrastructure-sharing guidelines transform market structure

The Ministry of Posts and Telecommunications mandated in 2024 that operators prove their inability to share before green-field builds receive permits. Standardized technical templates and published lease-rate ceilings shrink negotiation cycles and make the independent TowerCo model the de facto route for expansion. The regulation draws on Thai precedent where compulsory sharing covered 2,000 sites, highlighting regional best practice. As a result, the Laos telecom tower market now attracts regional portfolio investors that value predictable tenancy revenues anchored by transparent rules.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic grid unreliability and diesel logistics costs in remote provinces | –0.7% | Mountainous northern and eastern provinces | Short term (≤ 2 years) |

| Low ARPU limiting operator capex head-room | –0.5% | Nationwide, sharpest in rural zones | Medium term (2-4 years) |

| Complex communal land-lease negotiations and title ambiguities | –0.3% | Areas with customary land tenure | Long term (≥ 4 years) |

| Shortage of certified riggers and O&M technicians outside Vientiane | –0.2% | Provinces outside Vientiane capital region | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid unreliability constrains remote tower deployment

Seasonal hydropower shortfalls force operators in off-grid provinces to run gensets for extended periods, adding 40-60% to yearly opex and lowering site profitability. Laos’ four-segment transmission grid also produces regional reliability gaps, with the north hardest hit by voltage drops. Though a China Southern Power Grid partnership upgraded bulk lines, last-mile distribution still suffers in steep terrain. Renewable-powered towers need a consistent grid to recharge batteries, so an unstable supply slows the conversion from diesel to solar in high-rainfall zones.

Low-ARPU environment limits infrastructure investment

Monthly mobile ARPU hovers in the USD 2-4 range, well below the USD 8-12 threshold typically required to self-finance dense rollouts. Five operators compete on price, compressing margins and pushing spectrum costs to the balance sheet’s forefront. Consequently, operators re-prioritize capital toward radio assets and rely on TowerCos for passive plant. While the Universal Service Fund offsets part of the rural economics, low end-user spending power remains a brake on the Laos telecom tower market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ownership: Independent models gain strategic momentum

Independent TowerCos secured a 11.58% CAGR outlook to 2031 as operators increasingly divest passive assets. Although operator-owned structures retained 46.98% of the Laos telecom tower market share in 2025, the absolute count is plateauing while TowerCo tenancy ratios climb. The Laos telecom tower market size attributed to independent portfolios is projected to widen as OCK Group scales a 70% stake in OCK Laos TowerCo and EDOTCO explores fiber-power bundles for railway corridors. These entities deploy dedicated maintenance crews and analytics platforms that raise uptime and cut energy waste.

Regulatory alignment with the 2024 sharing decree removes duplication barriers and lowers rural per-site economics, further tilting preference toward neutral hosts. Joint-venture TowerCos that mix state or operator equity with professional management offer a middle ground where sovereignty or security concerns exist. Captive sites, meanwhile, are preserved for mission-critical gateways and border checkpoints where payload requirements extend beyond standard cellular kits.

By Installation: Rooftops accelerate urban densification

Ground-based assets still accounted for 68.83% of deployments in 2025, yet rooftops are clocking a 5.18% annual upswing as zoning curbs freestanding masts in Vientiane’s municipal limits. Hotels, malls, and transport hubs now monetize vertical real estate by leasing space to TowerCos, converting sunk construction into recurring revenue. In the UNESCO-listed Luang Prabang, authorities favor concealed rooftop poles painted to match historic façades, aligning aesthetics with heritage rules.

The Laos telecom tower market size for ground sites remains high in rural plains where land is inexpensive and propagation range is critical. Hybrid layouts, ground power cabinets feeding rooftop antennas, are emerging in peri-urban belts where congestion meets space scarcity. These configurations lower cable run losses and satisfy both coverage and civic-design requirements without inflating capex.

By Fuel Type: Renewable transition gathers pace

Grid/diesel hybrids represented 85.12% of installed sites in 2025, but renewable towers are rising 19.84% annually as Laos exports surplus hydropower to neighbors. Power-purchase-agreement wheeling lets TowerCos tap 100% clean supply without investing in on-site generation, underpinning the fastest-growing slice of the Laos telecom tower market. Solar-battery kits supplement hydropower along border stretches where feed stability is lower, reducing diesel truck rolls that once consumed 30% of opex.

Remote mountains still depend on hybrid systems because cloud cover in the monsoon season cuts photovoltaic yield. Yet floating solar pilots on hydropower reservoirs promise new capacity that could be dispatched directly to colocation clusters. Cost per kilowatt of solar hardware has dropped 48% since 2020, further enhancing the renewables business case.

By Tower Type: Stealth solutions address aesthetic rules

Monopole designs secured 40.12% revenue in 2025, illustrating operator preference for standardized kits that shorten build times. However, stealth and concealed units are expanding 10.37% per year owing to tourism-driven design codes and community pushback against metallic silhouettes in scenic valleys. Laminated fiberglass wraps, shrouded antennas, and tree-mimic cladding now feature in procurement tenders issued by Unitel for heritage districts.

The Laos telecom tower market size for lattice builds is steady for multi-tenant high-load hubs, while guyed masts stay niche where soil conditions allow economical anchoring. Advances in lightweight radios and integrated remote radio heads lower the payload threshold, enabling monopoles to handle capacity formerly requiring lattice structures.

Geography Analysis

Central provinces centered on Vientiane host the densest node grid and account for the largest slice of the Laos telecom tower market. Unitel alone runs more than 9,000 base stations that give 83% 4G coverage, and the city forms the launch pad for 5G clusters. Reliable grid supply drawn from cross-border lines with Thailand underpins low downtime and keeps diesel top-ups to a minimum. Seasonal tourist flows along the Vientiane-Vang Vieng corridor raise traffic intensity, justifying rooftop infill and multi-band antennas.

Northern provinces such as Phongsaly and Luang Prabang confront the steepest deployment economics. Mountain road access and an 11-person/km² density stretch logistics cycles and can triple tower foundation costs. Nonetheless, the Laos-China Railway’s 422 km fiber easement offers turnkey power and backhaul that lowers incremental opex for co-located poles. Chinese e-commerce providers looking to speed cross-border delivery fuel data requirements along the railway, creating pockets of high return despite sparse resident populations.

Southern provinces, notably Champasak and Savannakhet, straddle economic gateways to Thailand and Vietnam. Hydropower export projects funnel stable power to these areas, raising uptime and making renewable tower pilots viable. Median village distance to essential services still reaches 22.5 km, exposing a last-mile void that the Universal Service Fund now targets. As Greater Mekong Subregion logistics projects mature, southern border posts emerge as key build-to-suit clusters that complement the Laos telecom tower market expansion in the core.

Competitive Landscape

The Laos Telecom Towers Market's concentration is moderate, with five mobile operators creating demand, and a growing pool of TowerCos supplying passive gear. Unitel's tower ownership is trending down as sale-and-lease-back talks progress. EDOTCO first entered in 2019 through an 80% stake in Mekong Tower Company and now holds a larger footprint tied to Laos-Thailand-Vietnam fiber rings. OCK Group’s 2024 lease pact with Best Telecom grants immediate revenue from 5G densification sites, accelerating tenancy ratios and positioned growth.

Strategic themes converge on asset-light conversion, renewable integration, and AI-driven remote monitoring that cuts site visits by one-third. The 2024 sharing decree checks duplication and channels savings to spectrum and core upgrades. Rural deployment remains the white space where TowerCos differentiate through mastery of complex land titles and microgrid engineering. Overall, the top five suppliers still account for under 50% of revenue, placing the market in the mid-fragmented bracket without a single dominant landlord.

Laos Telecom Towers Industry Leaders

EDOTCO Group Sdn Bhd

OCK Group Bhd

Southeast Asia Tower Company

Lao Telecommunication Public Company Ltd. (Lao Telecom)

Unitel (Star Telecom Co., Ltd.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Laotian Times reported nationwide mobile download speeds rose 17.8% after coordinated operator capacity upgrades, signaling tangible user-experience gains.

- May 2024: OCK Group signed a comprehensive tower-leasing agreement with Best Telecom to support Laos’ 5G rollout, marking deeper international TowerCo participation.

Laos Telecom Towers Market Report Scope

Telecom towers, essential for wireless transmission, support antennas and communication equipment. These towers enable mobile networks to span extensive areas, ensuring smooth signal broadcasting and reception between mobile devices and the network. Depending on location and network needs, telecom towers vary in design and size, including lattice towers, monopoles, and guyed towers.

The Laos telecom towers market is segmented by ownership (operator-owned, private-owned, and MNO captive sites), by installation (rooftop and ground-based), and by fuel type (renewable and non-renewable).

The Market Size and Forecasts are Provided in Terms of Value (USD) for all the Above Segments.

| Operator-owned |

| Independent TowerCo |

| Joint-Venture TowerCo |

| MNO Captive |

| Rooftop |

| Ground-based |

| Renewable-powered |

| Grid/Diesel Hybrid |

| Monopole |

| Lattice |

| Guyed |

| Stealth / Concealed |

| By Ownership | Operator-owned |

| Independent TowerCo | |

| Joint-Venture TowerCo | |

| MNO Captive | |

| By Installation | Rooftop |

| Ground-based | |

| By Fuel Type | Renewable-powered |

| Grid/Diesel Hybrid | |

| By Tower Type | Monopole |

| Lattice | |

| Guyed | |

| Stealth / Concealed |

Key Questions Answered in the Report

What is the 2026 value of the Laos telecom tower market?

The Laos telecom tower market size stands at USD 90.17 million in 2026.

How fast is independent TowerCo ownership growing?

Independent portfolios are expanding at a 11.58% CAGR as operators pivot toward asset-light strategies.

Which installation format is gaining ground in urban Laos?

Rooftop deployments are increasing 5.18% annually because zoning rules restrict new ground masts in cities.

Why are renewable-powered towers important in Laos?

Hydropower wheeling agreements enable 100% green energy sites, cutting diesel opex in remote areas.

How do infrastructure-sharing rules affect new builds?

The 2024 guidelines force operators to prove sharing infeasibility before erecting new towers, accelerating neutral-host adoption.

What hampers tower deployment in northern provinces?

Grid instability, mountainous terrain, and lengthy land-lease negotiations raise costs and slow rollout.

Page last updated on: