Autonomous Demand Sensing And Cognitive Forecasting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

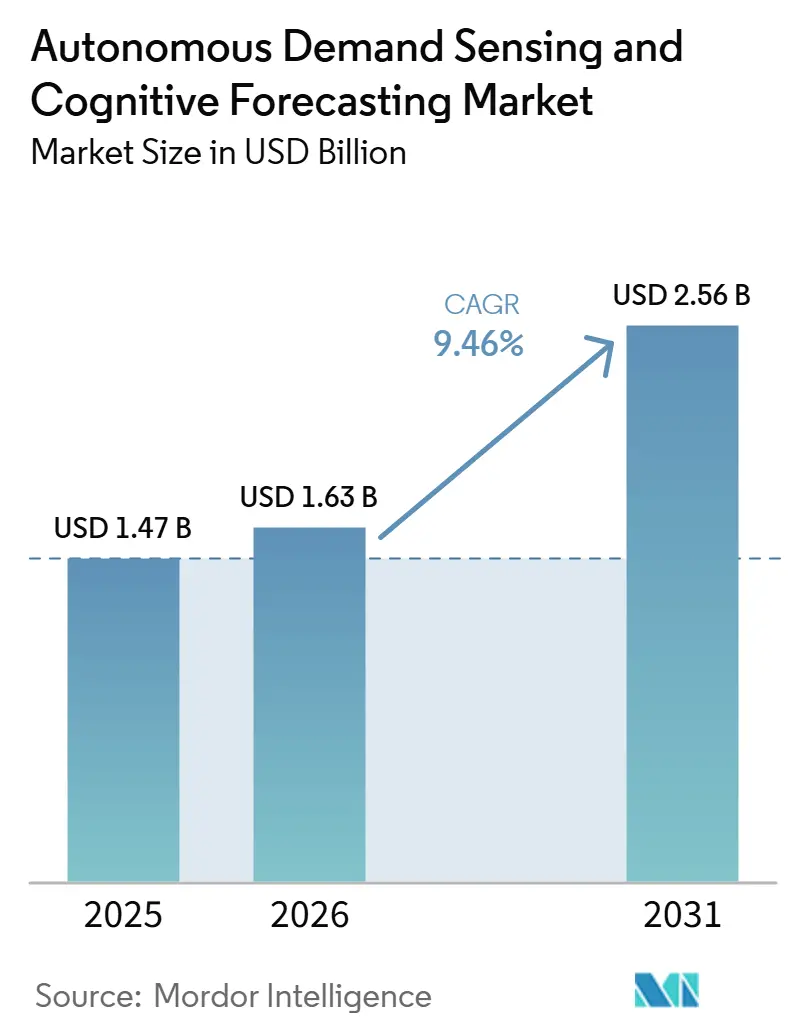

| Market Size (2026) | USD 1.63 Billion |

| Market Size (2031) | USD 2.56 Billion |

| Growth Rate (2026 - 2031) | 9.46% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Autonomous Demand Sensing And Cognitive Forecasting Market Analysis by Mordor Intelligence

The autonomous demand sensing and cognitive forecasting market size is expected to increase from USD 1.47 billion in 2025 to USD 1.63 billion in 2026 and reach USD 2.56 billion by 2031, growing at a CAGR of 9.46% over 2026-2031. Robust growth reflects the enterprise pivot from periodic replenishment to AI-enabled, signal-driven planning that draws on point-of-sale feeds, e-commerce baskets, IoT telemetry, and external data lakes. Software continued to dominate revenue in 2025, yet advisory and managed-service spending is scaling faster as organizations seek help with data-architecture cleanups, model retraining, and change management. Cloud remains the preferred deployment environment, but highly regulated sectors such as healthcare and banking are accelerating hybrid rollouts to reconcile data-sovereignty mandates with elastic compute needs. Vertical uptake is broad; consumer packaged goods, retail, automotive, and healthcare rely on real-time demand sensing to trim forecast error, compress working capital, and respond to supply volatility. Competitive intensity is rising as hyperscalers embed native forecasting engines, prompting specialist vendors to differentiate through pre-trained vertical models, probabilistic outputs, and no-code configuration options.

Key Report Takeaways

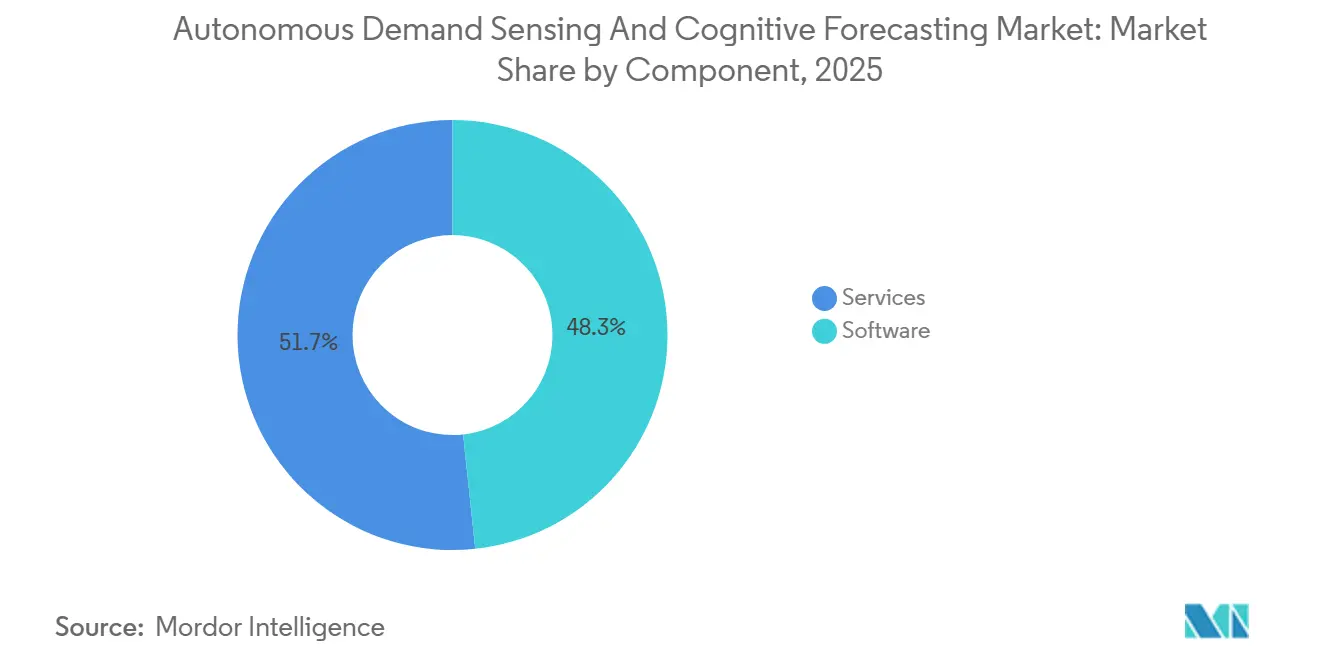

- By component, software held 48.31% of the autonomous demand sensing and cognitive forecasting market share in 2025, while services are set to expand at a 9.86% CAGR through 2031.

- By deployment mode, cloud commanded 56.43% revenue share in 2025, whereas hybrid architectures are projected to grow at a 10.06% CAGR over 2026-2031.

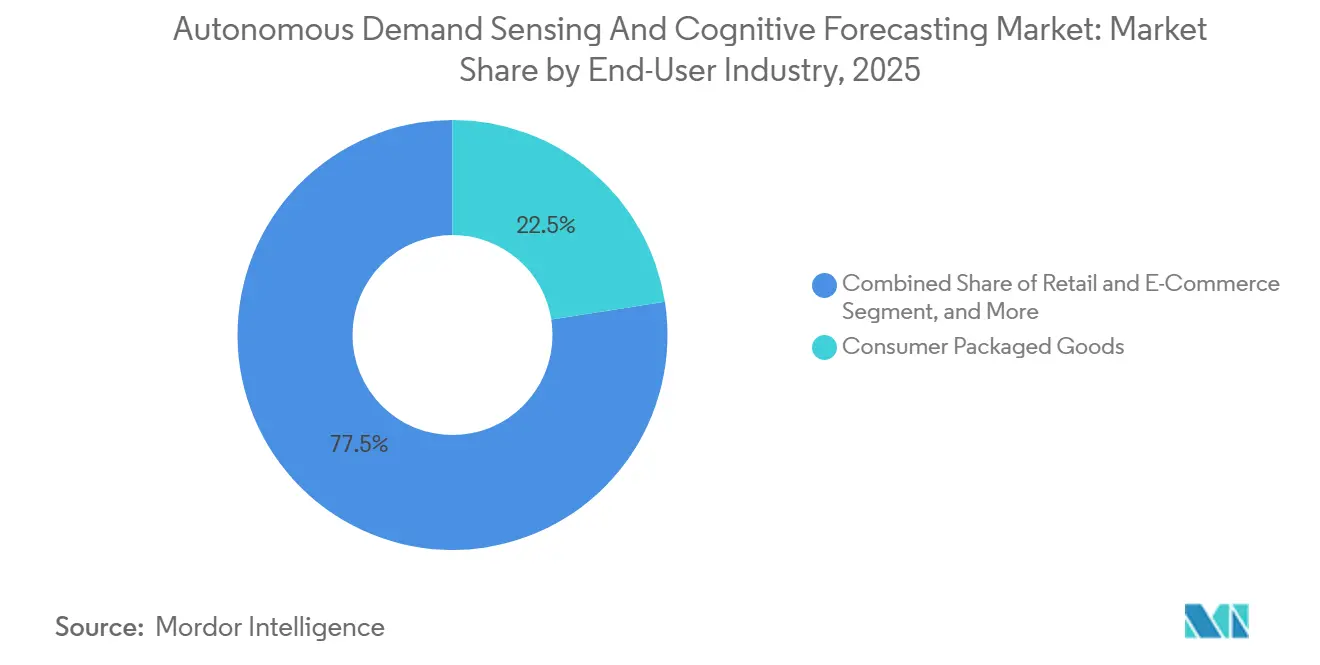

- By end-user industry, consumer packaged goods led with a 22.53% revenue share in 2025; healthcare and life sciences are forecast to register the fastest growth at 10.46% CAGR during the same horizon.

- By forecasting technique, machine learning accounted for 41.39% of revenue share in 2025, and deep learning models are poised to grow at a 10.26% CAGR through 2031.

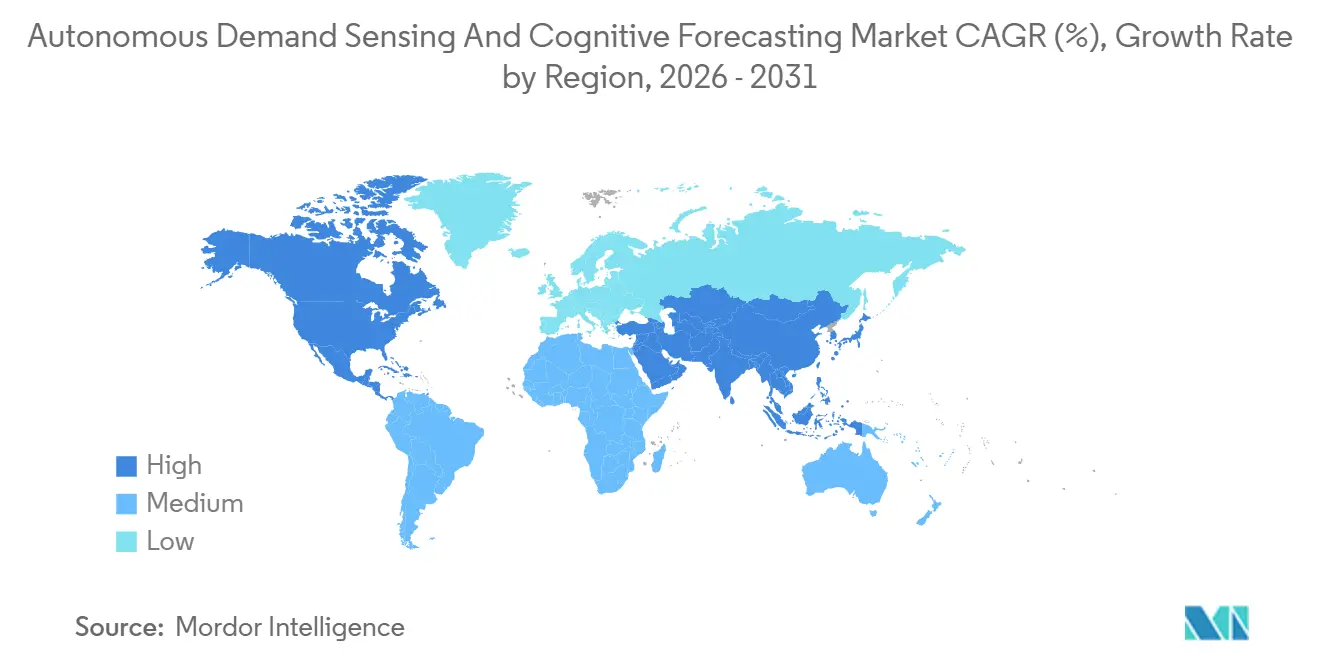

- By geography, North America dominated with a 34.74% share in 2025, whereas Asia-Pacific is expected to post a 10.67% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Autonomous Demand Sensing And Cognitive Forecasting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Based Real-Time Demand Signal Capture | +2.3% | Global, focus on North America and Asia-Pacific | Medium term (2-4 years) |

| Rising Adoption of Cloud-Native Platforms | +2.1% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Rapid Proliferation of IoT Sensors | +1.8% | Asia-Pacific core, spillover to Middle East and Africa | Medium term (2-4 years) |

| Integration of Generative AI for Forecasting | +1.6% | North America and Europe, early Asia-Pacific uptake | Long term (≥ 4 years) |

| Increasing Use of External Data Lakes | +1.2% | Global, advanced use in North America and Europe | Medium term (2-4 years) |

| Vendor-Managed Inventory in Tier-2 Cities | +0.9% | Asia-Pacific and South America, emerging Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-Based Real-Time Demand Signal Capture from POS and E-Commerce Channels

Retailers and consumer packaged goods brands have upgraded from weekly batch forecasts to streaming pipelines that parse checkout, clickstream, and social media sentiment at sub-second intervals. Walmart’s roll-out of 90 million IoT sensors across its network funnels temperature, humidity, and position data into edge devices that cleanse and compress signals before dispatching them to cloud models, cutting latency and bandwidth costs. Enterprises that combine these leading indicators with weather data report 15%-25% lower forecast error and 5%-8% additional accuracy when sentiment spikes or regional heatwaves influence demand. Continuous recalculation narrows planning cycles from monthly to hourly, letting planners adjust safety-stock settings the moment anomalies surface.

Rising Adoption of Cloud-Native Supply-Chain Platforms

Cloud-native suites such as SAP Integrated Business Planning and Kinaxis RapidResponse attracted more than 1,200 new logos in 2025 as supply chain chiefs de-risked legacy upgrades by moving to subscription pricing and elastic compute.[1]SAP Product Marketing, “SAP Integrated Business Planning,” sap.com Public-cloud scalability underpins Monte Carlo simulations that test thousands of scenarios per hour, while out-of-the-box connectors pull data from sales, finance, and logistics systems without custom code. Hybrid topologies further accelerate adoption by keeping personally identifiable information on-premise while bursting model-training workloads to public regions during peak cycles, satisfying European and Chinese data-residency rules.

Rapid Proliferation of IoT Sensors across Logistics Nodes

Logistics providers instrumented 900,000 pallets, containers, and parcels with Bluetooth Low Energy and LoRaWAN tags in 2025, up 50% from 2024, shrinking the cost per tag below USD 15 for active units. Maersk routes sensor feeds through predictive engines that reroute freight when ports back up, improving on-time arrival and aligning inbound inventory levels with real-time demand fluctuations. End-to-end visibility lets planners shift from store-level allocation to network-level optimization, dynamically repositioning stock between regional hubs when transit delays accumulate.

Integration of Generative AI for Scenario-Driven Forecasting

Large language models fine-tuned on historical demand, product reviews, and regulatory text now generate thousands of what-if scenarios in minutes. Supply planners at leading automotive and electronics manufacturers cut decision latency by synthesizing unstructured data into structured demand adjustments. Vendors such as RELEX Solutions deploy agentic AI that flags anomalies and proposes corrective actions, trimming planner workloads by 40% and shortening cycle times for decision approval. Forthcoming transparency clauses in the European Union’s AI Act are prompting companies to build audit trails that document model inputs, parameter weights, and override decisions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Silos and Poor Master-Data Quality | −1.4% | Global, acute in fragmented enterprises | Short term (≤ 2 years) |

| High Total Cost of Ownership for SMEs | −1.1% | Global, most pronounced in South America and tier-2 Asia-Pacific | Medium term (2-4 years) |

| Regulatory Barriers on Cross-Border Data | −0.8% | Europe, China, emerging markets with evolving localization mandates | Long term (≥ 4 years) |

| Shortage of Domain-Specific AI Talent | −0.6% | Global, acute gaps in Asia-Pacific and the Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Silos and Poor Master-Data Quality

Many enterprises still house demand, product, and customer records in isolated enterprise resource planning, warehouse management, and customer relationship management systems. Duplicate SKUs, inconsistent units of measure, and missing hierarchy fields undermine model accuracy and extend implementation timelines. Mid-sized organizations often face 12- to 18-month master-data harmonization projects that add USD 0.5 million to USD 2 million in up-front cost, delaying autonomous demand sensing and cognitive forecasting market deployments. Mergers and acquisitions compound the challenge as acquirers must reconcile disparate schemas before model training can begin.

High Total Cost of Ownership for SMEs

Small and medium-sized enterprises encounter five-year spending envelopes of USD 1 million to USD 5 million once software, cloud infrastructure, data integration, and model retraining are factored in. Return-on-investment uncertainty and limited in-house data science expertise lead many firms in South America, Africa, and tier-2 Asian cities to stick with spreadsheets. Carnegie Mellon University, in collaboration with the United Nations International Computing Centre, is crafting open-source demand-sensing frameworks. These frameworks promise to slash licensing costs by 70% to 80%. However, they fall short of offering the pre-built connectors and industry-specific models that commercial platforms boast. As a result, users face increased labor during implementation.[2]UN International Computing Centre Communications, “Frugal AI Hub Launched to Lower AI Adoption Barriers,” unicc.org Open-source frameworks lower license fees but still require skilled staff for connector development and vertical model tuning. Subscription bundles that package software, infrastructure, and support into a predictable monthly charge are gaining traction, yet skepticism endures until suppliers can demonstrate measurable forecast-accuracy gains within one fiscal year.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain as Complexity Rises

The services segment of the autonomous demand sensing and cognitive forecasting market is projected to grow at a 9.86% CAGR through 2031 as enterprises lean on consultants to clean data, retrain models, and manage agentic AI workflows. The software segment retained a 48.31% revenue share, reflecting license commitments to platforms that bundle data ingestion, feature engineering, and probabilistic forecasting engines. Demand for managed services has intensified as organizations realize that forecast accuracy hinges on continuous feature updates, prompt engineering, and guardrail monitoring that internal teams often lack the bandwidth to perform.

Implementation partners embed industry know-how, whether it is seasonality curves for fashion retailers or serialization workflows for pharmaceutical manufacturers. They also orchestrate hybrid deployments that synchronize on-premise master data with public-cloud training clusters, a prerequisite for regulated sectors. This services momentum is widening partner ecosystems around core platforms and is likely to reshape vendor revenue mixes by 2031.

By Deployment Mode: Hybrid Architectures Accelerate

Cloud configurations accounted for 56.43% of the autonomous demand sensing and cognitive forecasting market share in 2025, as elastic compute simplifies Monte Carlo runs and external data ingestion. Hybrid setups are on track for a 10.06% CAGR, the fastest among deployment modes, as European and Chinese data-residency statutes require sensitive data to remain on local servers while permitting anonymized aggregates to flow to cloud training nodes. Kubernetes-centric orchestration abstracts workload placement, enabling data scientists to prototype locally and deploy models to production clusters without code rewrites.

Hybrid adoption also supports a gradual and systematic migration process. Organizations typically begin by transitioning demand-sensing workloads to the new system, ensuring that initial changes are manageable and low-risk. Once this phase is successfully implemented, they proceed with migrating supply planning, network design, and integrated business-planning modules. This step-by-step approach minimizes the risks associated with large-scale transformations and allows companies to realize incremental value at each stage. Furthermore, it ensures that mission-critical on-premises systems remain operational and unaffected during the transition, providing a seamless, efficient migration experience.

By End-User Industry: Healthcare Surges on Serialization

Consumer packaged goods accounted for 22.53% of 2025 revenue as brands tackled perishability, promotional elasticity, and SKU proliferation. Healthcare and life sciences are forecast to grow at 10.46% CAGR through 2031, the highest among verticals, propelled by vaccine cold-chain mandates and serialization laws that tighten traceability. Hospitals and distributors use real-time demand sensing to avoid stockouts of critical medicines, while medical device makers integrate IoT telemetry from sterilization trays and surgical kits to predict replenishment. Automotive, retail, and industrial manufacturing collectively account for over 40% of current market revenue. In the automotive sector, manufacturers align their production schedules with fluctuating semiconductor supply to ensure seamless operations.

Retail chains, on the other hand, utilize advanced price-sensing agents to dynamically adjust markdowns and optimize pricing strategies. Meanwhile, industrial manufacturers leverage installed-base sensors to predict spare-part demand, enabling efficient inventory management and reducing downtime. Additionally, energy, utilities, and logistics are emerging as significant growth areas. These sectors face unique forecasting challenges, such as managing the variability of renewable energy sources and optimizing routes for logistics operations, which require specialized solutions to address their complexities effectively.

By Forecasting Technique: Deep Learning Gains Traction

Machine learning methods, including gradient-boosted trees, random forests, and support vector machines, accounted for 41.39% of the revenue share in 2025. These methods have gained significant traction for their ability to handle structured data effectively and deliver accurate predictions across industries. Deep learning models, on the other hand, are projected to grow at a compound annual growth rate (CAGR) of 10.26%, driven by the superior performance of transformer architectures. These architectures excel at processing sparse, high-dimensional inputs, such as social media chatter and weather data grids, making them increasingly valuable for complex data analysis. Reinforcement learning, while still in its early stages, is showing promising results by delivering measurable margin improvements in areas such as promotion planning and markdown timing. It achieves this by optimizing sequential decision-making under uncertainty.

Hybrid stacks, which combine neural networks for feature extraction with tree-based ensembles for final predictions, offer a balance between accuracy and interpretability. This approach is particularly appealing to industries such as food, pharmaceuticals, and medical devices, where strict regulatory requirements demand transparent and explainable models. In 2025, ToolsGroup's SO99-plus platform rolled out a new feature: probabilistic forecasting. This innovation produces comprehensive demand distributions instead of mere point estimates. As a result, planners can now better gauge forecast uncertainties and adjust safety-stock levels, striking a balance between service-level goals and the costs of holding inventory.[3]ToolsGroup Press Office, “ToolsGroup Introduces Inventory-Aware Demand Shaping,” toolsgroup.com Additionally, the adoption of probabilistic outputs is shifting planners away from relying solely on deterministic point estimates.

Geography Analysis

North America accounted for 34.74% of global revenue in 2025, buoyed by Fortune 500 retailers, automotive OEMs, and consumer packaged goods giants that embedded demand-sensing engines in enterprise suites during pandemic recovery. The region benefits from mature cloud stacks and an abundant data-science talent pool. Federal food-safety and pharmaceutical traceability laws encourage continuous monitoring, while nearshoring trends drive cross-border synchronization with Mexican facilities.

Asia-Pacific is forecast to post a 10.67% CAGR between 2026 and 2031, the highest worldwide. China’s cross-border e-commerce surge, India’s tier-2 city digitization, and Japan’s aging-workforce automation imperatives underpin spending. Updated 2026 Chinese data-transfer guidelines clarify that anonymized aggregates can be sent out of the country for analysis, catalyzing hybrid adoption. In India, public cloud price drops and government AI roadmaps have driven adoption across retail and manufacturing. South Korea, Australia, and ASEAN countries mirror this trajectory, albeit from smaller bases.

Europe, the Middle East and Africa, and South America share the remaining revenue. Europe’s General Data Protection Regulation lengthens project lead times, yet the bloc’s advanced industrial base drives sustainability and waste-minimization use cases. The Middle East, led by the United Arab Emirates and Saudi Arabia, funds smart-city pilots that integrate demand sensing with urban logistics. South America’s e-commerce accelerationis drivings marketplaces to optimize fulfillment locations, though macroeconomic volatilityis temperings spending outside Brazil and Argentina.

Competitive Landscape

The autonomous demand sensing and cognitive forecasting industry is moderately concentrated; the top ten vendors captured roughly 55%-60% of global revenue in 2025. Enterprise software incumbents such as SAP, Oracle, and Microsoft bundle native forecasting engines that ride existing customer footprints, while specialists including o9 Solutions, Blue Yonder, Kinaxis, and RELEX Solutions differentiate through pre-trained vertical models and no-code interfaces. WiseTech Global’s pending USD 2.1 billion purchase of E2open underscores consolidation as vendors assemble control-tower suites spanning demand, logistics, and trade compliance.[4]WiseTech Global Investor Relations, “WiseTech Global to Acquire E2open for USD 2.1 Billion,” wisetechglobal.com

Strategic advantage rests on three pillars. First, real-time ingestion of IoT and POS feeds allows sub-hourly recalibration. Second, generative AI merges unstructured text with numerical series to enrich feature sets and simulate macro shocks. Third, probabilistic distributions replace point estimates, arming planners with confidence intervals to balance service targets against inventory cost. Niche challengers such as Lokad and Prevedere leverage open-source libraries and serverless infrastructure to undercut pricing for mid-market firms, broadening adoption outside the Fortune 500.

All vendors are increasingly investing in agentic AI to enhance operational efficiency and decision-making processes. For instance, RELEX Solutions successfully deployed more than ten autonomous agents in live environments during 2025. These agents are specifically designed to detect anomalies and issue replenishment orders without manual intervention, streamlining supply chain operations. Similarly, ToolsGroup’s SO99-plus release introduces inventory-aware demand shaping, enabling businesses to optimize inventory levels across multiple responding to fluctuating demand patterns. Additionally, Aera Technology has integrated decision bots into its platform, which autonomously execute safety-stock adjustments when transit delays pose a risk to service levels. These advancements highlight the growing reliance on agentic AI to address complex challenges and improve performance across industries.

Autonomous Demand Sensing And Cognitive Forecasting Industry Leaders

Blue Yonder Group Inc.

Kinaxis Inc.

o9 Solutions Inc.

E2open Parent Holdings Inc.

ToolsGroup B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: o9 Solutions completed global deployment at Indorama Ventures, integrating demand, supply, and financial planning across 26 countries.

- March 2026: RELEX Solutions and Accenture launched an AI-driven demand-forecasting project for Lowe’s 1,700-plus North American stores, aiming to reduce stockouts by 15%.

- January 2026: Algo acquired Demand Driven Technologies, adding Intuiflow’s demand-driven material requirements planning to its optimization suite.

- December 2025: RELEX Solutions purchased Ida, a Finnish retail analytics start-up specializing in pricing optimization agents, for EUR 25 million (USD 26.8 million).

Global Autonomous Demand Sensing And Cognitive Forecasting Market Report Scope

The Autonomous Demand Sensing and Cognitive Forecasting Market refers to the market for advanced analytics and AI-driven solutions that enable organizations to predict demand patterns with high accuracy by leveraging real-time data, machine learning, and cognitive computing techniques. These solutions integrate internal and external data sources, such as sales data, market signals, weather patterns, and consumer behavior, to provide dynamic, automated, and self-learning forecasting capabilities that enhance supply chain planning, inventory optimization, and decision-making.

The Autonomous Demand Sensing and Cognitive Forecasting Market Report is Segmented by Component (Software, and Services), Deployment Mode (Cloud, On-Premise, and Hybrid), End-User Industry (Consumer Packaged Goods, Retail and E-Commerce, Automotive and Transportation, Industrial Manufacturing, Healthcare and Life Sciences, Food and Beverage, Logistics and Supply Chain, Energy and Utilities, and Other End-User Industries), Forecasting Technique (Machine Learning Based Forecasting, Deep Learning Based Forecasting, Traditional Statistical Models Enhanced with AI, Reinforcement Learning Approaches, and Hybrid Models), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premise |

| Hybrid |

| Consumer Packaged Goods |

| Retail and E-Commerce |

| Automotive and Transportation |

| Industrial Manufacturing |

| Healthcare and Life Sciences |

| Food and Beverage |

| Logistics and Supply Chain |

| Energy and Utilities |

| Other End-User Industries |

| Machine Learning Based Forecasting |

| Deep Learning Based Forecasting |

| Traditional Statistical Models Enhanced with AI |

| Reinforcement Learning Approaches |

| Hybrid Models |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Component | Software | ||

| Services | |||

| By Deployment Mode | Cloud | ||

| On-Premise | |||

| Hybrid | |||

| By End-User Industry | Consumer Packaged Goods | ||

| Retail and E-Commerce | |||

| Automotive and Transportation | |||

| Industrial Manufacturing | |||

| Healthcare and Life Sciences | |||

| Food and Beverage | |||

| Logistics and Supply Chain | |||

| Energy and Utilities | |||

| Other End-User Industries | |||

| By Forecasting Technique | Machine Learning Based Forecasting | ||

| Deep Learning Based Forecasting | |||

| Traditional Statistical Models Enhanced with AI | |||

| Reinforcement Learning Approaches | |||

| Hybrid Models | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the autonomous demand sensing and cognitive forecasting market in 2031?

It is forecast to reach USD 2.56 billion by 2031, reflecting a 9.46% CAGR over 2026-2031.

Which component segment is expanding the fastest?

Services are expected to grow at 9.86% CAGR as firms rely on consulting, integration, and managed-service partners for ongoing model stewardship.

Why is hybrid deployment gaining popularity?

Hybrid architectures balance on-premise data governance with cloud scale, supporting jurisdictions that enforce data-residency mandates while still enabling elastic compute.

Which end-user industry will grow the quickest to 2031?

Healthcare and life sciences, driven by vaccine cold-chain visibility and serialization compliance, is projected to post the highest CAGR at 10.46%.

How does deep learning improve forecast accuracy?

Transformer-based deep learning models handle sparse, high-dimensional inputs and generate probabilistic distributions, outperforming traditional methods on multi-step predictions.

Which region is expected to post the highest growth rate?

Asia-Pacific is set to expand at a 10.67% CAGR, propelled by China's cross-border e-commerce, India's distribution digitization, and Japan's automation initiatives.

Page last updated on: