KYC Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

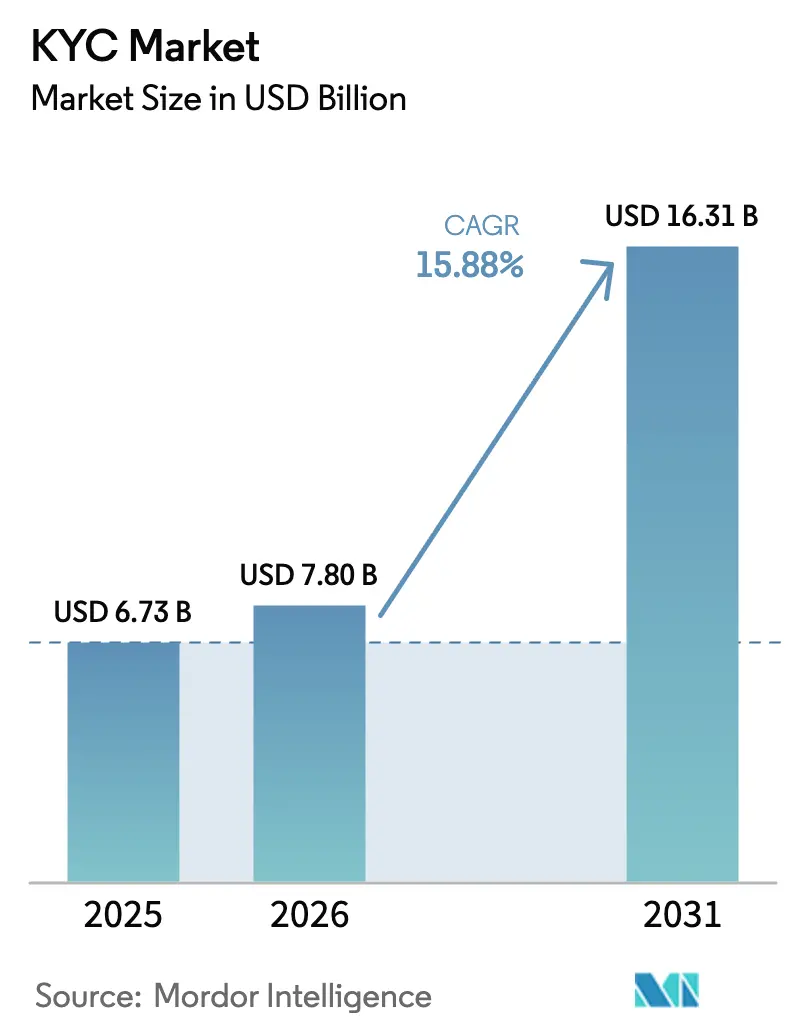

| Market Size (2026) | USD 7.8 Billion |

| Market Size (2031) | USD 16.31 Billion |

| Growth Rate (2026 - 2031) | 15.88% CAGR |

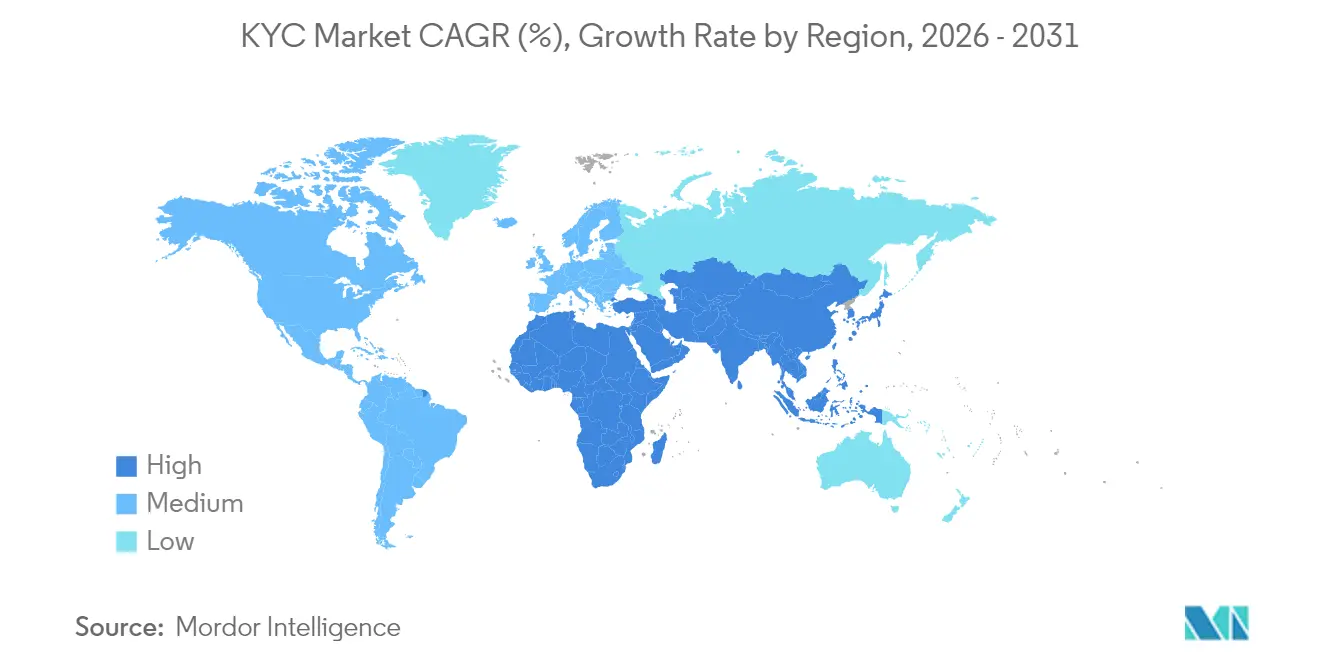

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

KYC Market Analysis by Mordor Intelligence

The KYC market size is expected to grow from USD 6.73 billion in 2025 to USD 7.8 billion in 2026 and is forecast to reach USD 16.31 billion by 2031 at 15.88% CAGR over 2026-2031. Its expansion is powered by stricter enforcement actions such as TD Bank’s USD 3 billion anti-money-laundering fine and Binance’s USD 4.3 billion settlement, which have pushed financial institutions to replace manual checks with real-time, AI-driven verification. Cloud deployment now underpins 64.60% of all identity-verification workloads, reflecting the shift toward elastic, API-based infrastructures that complete millions of checks in seconds. Regional growth remains bifurcated: North America commands 34.50% revenue today, while Asia-Pacific grows fastest at an 18.60% CAGR on the back of mass fintech adoption and regulatory catch-up. Consolidation is speeding up as established vendors buy AI-native specialists to secure sub-second decisioning and 99%-plus accuracy levels.

Key Report Takeaways

- By component, solutions retained 69.92% of the KYC market share in 2025; services are projected to expand at a 22.35% CAGR through 2031.

- By deployment mode, cloud accounted for 64.85% of the KYC market size in 2025 and is advancing at a 20.15% CAGR to 2031.

- By enterprise size, large enterprises held 60.35% of the KYC market share in 2025, while SMEs post the fastest growth at 19.95% CAGR.

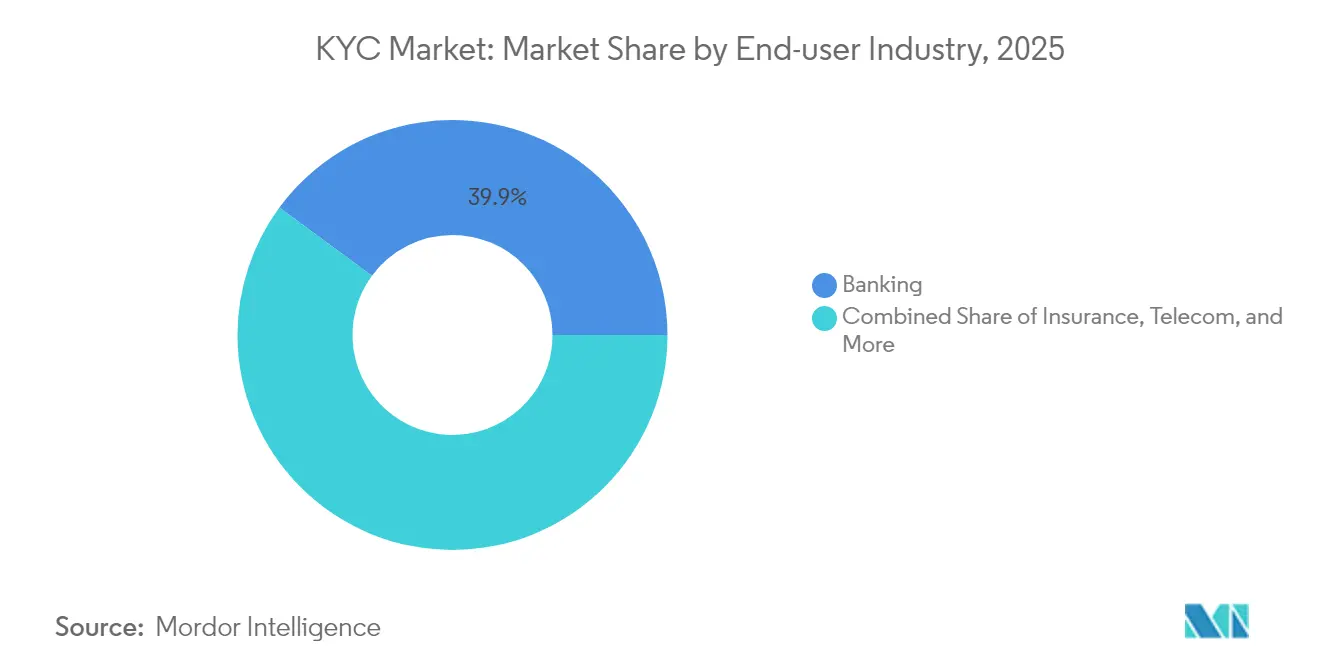

- By industry, banking led with 39.90% of 2025 revenue; fintech and payment-service providers are forecast to expand at a 21.40% CAGR.

- By verification technology, biometrics contributed 44.85% of the KYC market size in 2025 and is forecast to grow at a 23.05% CAGR.

- By geography, North America secured 34.10% revenue in 2025; Asia-Pacific is expected to post the highest 18.05% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global KYC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising regulatory penalties for non-compliance | +2.8% | Global, highest in North America and EU | Short term (≤ 2 years) |

| Surge in remote digital onboarding | +3.2% | Global, led by Asia-Pacific | Medium term (2-4 years) |

| AI/ML-driven false-positive reduction | +2.1% | North America and EU core | Medium term (2-4 years) |

| DeFi on-ramp compliance needs | +1.4% | Crypto-friendly jurisdictions | Long term (≥ 4 years) |

| Reusable digital-ID wallets (eIDAS 2.0) | +1.8% | EU primary | Long term (≥ 4 years) |

| ISO 20022 real-time cross-border payments | +1.3% | Global rollout | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising regulatory penalties for non-compliance

Record fines such as the USD 3 billion assessment against TD Bank in 2024 have elevated non-compliance from an operational cost to an existential threat, prompting banks to fund automated verification projects that eliminate manual backlogs and reduce investigative cycles from weeks to seconds[1]U.S. Department of Justice, “Justice Department Announces TD Bank Penalty,” justice.gov. FinCEN’s 2026 AML/CFT rules will extend customer-identification obligations to investment advisers, further enlarging addressable demand. In Europe, eIDAS 2.0 obliges every member state to accept interoperable digital-ID wallets by 2026, widening the remit of KYC obligations beyond banking into ecommerce and telecom. Together these measures can push annual non-compliance costs above USD 100 million for a single global institution, making advanced KYC technologies a risk-mitigation staple rather than discretionary spend.

Surge in remote digital onboarding

Traditional onboarding lost 67% of prospects in 2024, which spurred firms to deploy AI engines that complete identity checks in under two seconds while holding 99%-plus accuracy. The pandemic embedded digital-first habits, and embedded-finance operators now demand low-friction KYC modules that slot directly into existing customer journeys. Regulators have responded: the FFIEC explicitly endorsed fully digital processes that still meet enhanced due-diligence thresholds, removing a major adoption barrier. As embedded finance spreads to non-bank brands, digital onboarding capability has become a baseline competitive requirement.

AI/ML-driven false-positive reduction

Rule-based tools historically buried compliance teams in duplicate alerts; AI platforms that blend document forensics, behavioral biometrics and NLP now suppress false positives by up to 90%, freeing staff capacity for genuine risk investigation. Large-language-model pipelines ingest external data—including sanctions news and social posts—to enrich real-time customer risk profiles, while deepfake-detection models counter synthetic-ID attacks rising alongside generative-AI adoption. The combination elevates both compliance performance and customer experience by stripping out redundant verification steps.

DeFi on-ramp compliance needs

IRS regulations effective January 2025 classify many DeFi operators as brokers, requiring them to perform traditional customer-reporting duties. Zero-knowledge-proof toolkits from vendors such as RISC Zero enable privacy-preserving checks that validate users without revealing personal data on-chain, aligning crypto ethos with regulator expectations. Institutional entry into tokenized markets is accelerating demand for enterprise-grade KYC stacks that reconcile pseudonymity with legal accountability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy regulation fragmentation | -1.9% | Global, peak in EU and California | Medium term (2-4 years) |

| Legacy-system integration complexity | -2.3% | North America and EU incumbents | Short term (≤ 2 years) |

| Privacy-preserving ID (ZK-proof) adoption | -1.1% | Global, concentrated in crypto-friendly jurisdictions | Long term (≥ 4 years) |

| Analytics-talent shortage in emerging markets | -1.4% | Asia-Pacific emerging markets, MEA, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-privacy regulation fragmentation

Conflicting mandates—GDPR, CCPA and 20-plus emerging frameworks—create a patchwork of data-localization and consent rules that often clash with AML record-keeping requirements [2]European Commission, “Regulation (EU) 2024/0000 on European Digital Identity,” europa.eu. Global KYC platforms must therefore build costly privacy-by-design architectures featuring encryption, data-minimization and automated-deletion functions. Banks hesitate to commit capital as looming revisions can invalidate deployed solutions, stretching procurement cycles and stalling adoption.

Legacy-system integration complexity

Many core-banking systems pre-date the internet and store customer records in proprietary formats, leading to multi-year KYC-modernization projects that overrun budgets by 50-100% once middleware and parallel-run costs surface. Compliance deadlines do not pause during migration, forcing institutions to operate duplicate stacks—raising operational risk and sapping return on investment. Although ISO 20022 offers a unifying data model, the 2025 deadline intensifies pressure on already-strained IT teams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Drive Market Foundation

Solutions generated 69.92% of 2025 revenue, confirming that end-to-end platforms sit at the heart of the KYC market. Institutional buyers demand single-API suites that merge biometric authentication, document forensics and real-time risk scoring, allowing 94% automated decisions and cutting manual review queues to hours . Services, however, post a 22.35% CAGR as firms lean on system integrators for multi-jurisdiction rollouts and perpetual-KYC tuning. Managed offerings appeal to SMEs that lack the talent or capital to run advanced stacks in-house, steering vendors toward compliance-as-a-service business models.

The services boom extends vendor stickiness beyond initial license fees. Professional teams translate changing statutes into rule updates, refine ML models against fresh fraud typologies and support zero-knowledge-proof pilots. As perpetual KYC transitions from optional to mainstream, continuous-monitoring subscriptions will contribute an ever-larger slice of overall KYC market revenue.

By Deployment Mode: Cloud Transformation Accelerates

Cloud already holds 64.85% of the KYC market share and is compounding at 20.15% annually as institutions retire hardware-bound verification nodes. Elastic infrastructure absorbs onboarding spikes—often millions of checks per day—without procurement lead-times. Vendor roadmaps now put SOC 2 controls, data-residency zoning and sovereign-cloud options at the center, persuading regulators that risk can be lower in the cloud than on-prem. Consequently, the KYC market size attributable to cloud instances is slated for double-digit gains through 2031.

On-prem solutions persist for defense and public-sector segments with absolute sovereignty mandates, but hybrid architectures bridge the two worlds. Edge-computing containers keep high-risk checks local yet dispatch low-risk data to the cloud for bulk processing and analytics. Multi-cloud strategies are becoming standard, driving demand for orchestration layers that abstract away underlying infrastructure.

By End-user Enterprise Size: SME Growth Outpaces Enterprise

Large enterprises still anchor 60.35% of 2025 spending, leveraging deep budgets to adopt the latest biometrics and predictive analytics. These institutions increasingly favor unified vendor ecosystems capable of merging KYC, AML and fraud control into a shared graph, eliminating data silos and supporting perpetual-KYC ambitions. For SMEs, subscription-priced, zero-coding KYC modules level the compliance playing field. Their 19.95% CAGR trajectory underlines how democratized tooling widens the addressable KYC market.

Rapid fintech formation amplifies SME demand: challenger banks, pay-by-instalment providers and micro-lenders must satisfy the same onboarding rules as tier-1 banks but with lighter staffing. Turnkey KYC APIs that drop into existing checkout flows therefore unlock immediate go-live, keeping compliance from blocking growth.

By End-user Industry: FinTech Disruption Reshapes Banking Dominance

Banking maintained 39.90% revenue in 2025, yet fintech and payment-service providers grow at 21.40% CAGR as real-time payments and embedded finance proliferate. Fintechs treat frictionless onboarding as a brand promise; hence they over-index on AI-led KYC innovations ranging from multi-modal biometrics to behavioral analytics. Banks, in turn, deploy perpetual-KYC engines that monitor news, sanctions and transaction patterns to update risk scores continuously, slashing remediation cycles and audit exposure.

Beyond finance, telecom, healthcare and gaming increasingly fall under stringent identity-verification requirements, swelling total addressable demand. DeFi platforms and crypto exchanges are a special case: pending broker-reporting rules push them toward privacy-preserving verification—an emerging sub-vertical where zero-knowledge techniques could prove decisive.

By Verification Technology: Biometrics Lead Anti-Fraud Innovation

Biometrics captured 44.85% of 2025 spend and will grow at 23.05% CAGR, owing to escalating deepfake and synthetic-identity threats. Vendors combine facial recognition with voice and behavioral signals for layered defences, and advanced liveness tests screen out AI-generated spoofing. In parallel, document-authentication engines now inspect holograms, microprint and UV reactions to flag forgeries invisible to human reviewers, pushing overall KYC market accuracy beyond 99%.

Blockchain-anchored identity credentials represent a promising frontier. Decentralized storage grants users data control while furnishing tamper-proof attestations to relying parties. Early pilots suggest that cross-vendor interoperability could compress integration timelines and unlock reusable identity models, cutting total compliance costs by double-digit percentages.

Geography Analysis

North America remains the epicenter with 34.10% revenue in 2025, underpinned by well-funded banks and an active venture-capital universe that poured more than USD 6 billion into ID-tech startups. FinCEN’s expanded AML program will add thousands of investment advisers to the mandatory-KYC roster in 2026, reinforcing demand for cloud-native verific¬ation suites. Canada’s 2025 AML overhaul, including tighter controls on white-label ATMs, further enlarges the regional opportunity set.

Asia-Pacific posts the strongest growth at 18.05% CAGR as mobile-first consumers flock to super-apps and digital wallets. Government identity frameworks such as India’s Aadhaar Pay and Singapore’s Singpass Pay prove that national e-ID rails can accelerate financial inclusion and lower onboarding cost. With hundreds of millions still unbanked, scalable KYC modules that can process mass onboarding in vernacular languages stand to capture outsized growth.

Europe’s trajectory hinges on eIDAS 2.0. Universal acceptance of EU Digital Identity Wallets by 2026 will standardize verification workflows, giving European providers a home-field advantage in privacy-preserving KYC. GDPR compliance also forces vendors to build highly granular consent and deletion mechanisms, turning data protection into a competitive differentiator. Middle East and Africa trail in absolute terms but display rising deal activity: the UAE launched a national KYC platform in 2024 to streamline fintech licensing, signaling government commitment to digital compliance.

Competitive Landscape

The KYC market is semi-consolidated, driven by the presence of major players. Keyy players employ strategies such as mergers, acquisitions, and product innovations to maintain a competitive edge and broaden their global footprint. Key player include EQUINITI KYC Solutions B.V., Truth Technologies, Inc., ACTICO GmbH and others.

The demand for KYC solutions is poised for significant growth as organizations increasingly recognize the importance of effective identity verification processes in mitigating risks associated with fraud and regulatory non-compliance. With substantial revenue projections driven by regulatory demands, technological advancements, and the shift towards digital services, stakeholders must navigate challenges such as integration complexity while capitalizing on emerging opportunities within this dynamic market landscape. The future looks promising for KYC solutions as they continue to evolve to meet the demands of modern businesses across various sectors globally.

KYC Industry Leaders

GB Group plc

Fenergo Group Holdings Ltd.

LexisNexis Risk Solutions Inc.

Jumio Corporation

Trulioo Information Services Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Capgemini acquires Delta Capita to strengthen European KYC services.

- February 2025: Fenergo launches AI-powered KYC and onboarding suite with a Trader Request Portal for the energy and commodities sector.

- February 2025: LexisNexis Risk Solutions buys IDVerse to bolster deepfake-resistant document authentication.

- January 2025: iCapital acquires Parallel Markets, adding reusable investor passports for private-market onboarding.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Know-Your-Customer (KYC) market as all software and managed-service solutions that verify and continuously monitor customer identity to satisfy anti-money-laundering, counter-terror finance, and sanctions regulations across regulated industries. This includes document and biometric verification engines, watch-list screening, risk scoring dashboards, and workflow orchestration layers deployed on-premise or in the cloud.

Scope Exclusions: Stand-alone fraud analytics tools that do not perform regulated identity checks and generic customer-relationship-management suites are excluded.

Segmentation Overview

- By Component

- Solutions

- Services

- By Deployment Mode

- Cloud

- On-Premises

- Hybrid

- By End-user Enterprise Size

- Small and Medium Enterprises

- Large Enterprises

- By End-user Industry

- Banking

- FinTech and Payment Service Providers

- Insurance

- Telecom

- Government and Public Sector

- Healthcare

- Gaming and iGaming

- Others

- By Verification Technology

- Biometrics

- Document Authentication

- Database/API-based

- Liveness and Anti-spoofing

- Blockchain-based KYC

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed compliance heads at tier-1 and challenger banks, fintech operations officers, regional regulators, and reg-tech product leads across North America, Europe, and Asia-Pacific. These discussions validated spending ranges, emerging biometric preferences, and regional onboarding pain points, which we then layered onto the desk research evidence to resolve data gaps.

Desk Research

We began with public data sets that anchor compliance activity, such as FATF mutual-evaluation reports, FinCEN civil-penalty statistics, the European Banking Authority's risk indicators, and World Bank Findex adoption rates. Trade groups (for example, the American Bankers Association), peer-reviewed journals on digital identity, and company 10-Ks filled foundational gaps. To size vendor revenues, we accessed D&B Hoovers, Dow Jones Factiva, and select import shipment logs showing ID scanners. This menu is illustrative; numerous additional sources informed our evidence base.

Market-Sizing & Forecasting

A top-down model started with the global count of regulated financial and high-risk non-financial entities, mapped against average KYC spend per onboarded customer. Results were stress-tested through bottom-up checks, sampled vendor revenues and cloud-based verification volumes, before reconciliation. Key variables include digital account-opening volumes, regulatory fine trends, smartphone penetration, uptake of reusable digital IDs, and average verification cost curves. A multivariate-regression forecast projects these drivers to 2030; scenario analysis adjusted for enforcement-intensity swings. Where vendor disclosures were partial, cost-per-check benchmarks from primary interviews bridged gaps.

Data Validation & Update Cycle

Outputs pass variance checks against external penalty and onboarding datasets, followed by senior-analyst review and a second pass before sign-off. We refresh the model annually and trigger interim updates when material events, such as a megafine or major rule change, occur.

Why Mordor's KYC Baseline Commands Reliability

Published figures often diverge because firms vary scope, refresh cadence, and underlying cost assumptions.

Key gap drivers include limited inclusion of managed services, older base years, and omission of biometric or perpetual-KYC modules, whereas Mordor's scope captures the full lifecycle spend and is updated yearly.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.73 B (2025) | Mordor Intelligence | - |

| USD 3.81 B (2025) | Regional Consultancy A | Focuses on software licenses, excludes outsourced screening services |

| USD 3.49 B (2022) | Global Consultancy B | Relies on pre-pandemic baseline and omits biometric verification spend |

| USD 2.67 B (2024) | Industry Journal C | Limits geography to North America and Europe and counts only SaaS subscriptions |

The comparison shows how narrower scopes or older baselines compress market value, while Mordor's disciplined variable selection and annual refresh deliver a balanced, transparent foundation decision-makers can trust.

Key Questions Answered in the Report

What is driving the rapid growth of the KYC market?

Rising regulatory penalties, digital-only customer onboarding and AI-powered fraud-detection breakthroughs are pushing global revenue from USD 7.8 billion in 2026 toward USD 16.31 billion by 2031 at a 15.88% CAGR.

Which region is growing fastest in the KYC market?

Asia-Pacific leads with an 18.05% CAGR through 2031 thanks to explosive fintech adoption and supportive national digital-ID schemes.

Why are cloud deployments dominating new KYC projects?

Cloud platforms process millions of verifications without hardware limits, now accounting for 64.85% of spending and expanding at 20.15% CAGR as regulators accept their security posture.

How are perpetual KYC models changing compliance operations?

Continuous monitoring replaces periodic reviews, cutting remediation timelines to seconds and reducing operational costs by up to 60%.

What role do biometrics play in combating fraud?

Biometrics hold 44.85% revenue share and grow at 23.05% CAGR by layering facial, voice and behavioral signals with live-ness checks to defeat deepfakes and synthetic IDs.

Are SMEs investing in KYC solutions?

Yes. Affordable, subscription-based KYC-as-a-Service platforms fuel a 19.95% CAGR among SMEs, widening market participation beyond large banks.

Page last updated on: