London Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

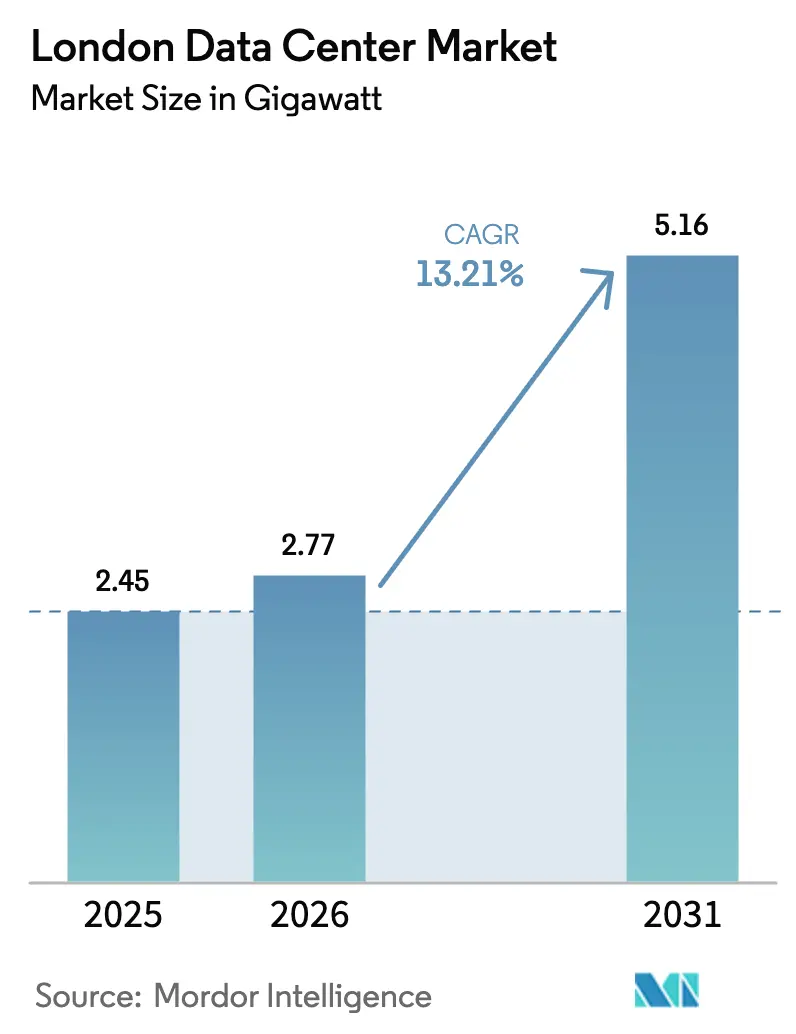

| Base Year Market Size (2025) | 2.45 gigawatt |

| Market Volume (2026) | 2.77 gigawatt |

| Market Volume (2031) | 5.16 gigawatt |

| Growth Rate (2026 - 2031) | 13.21% CAGR |

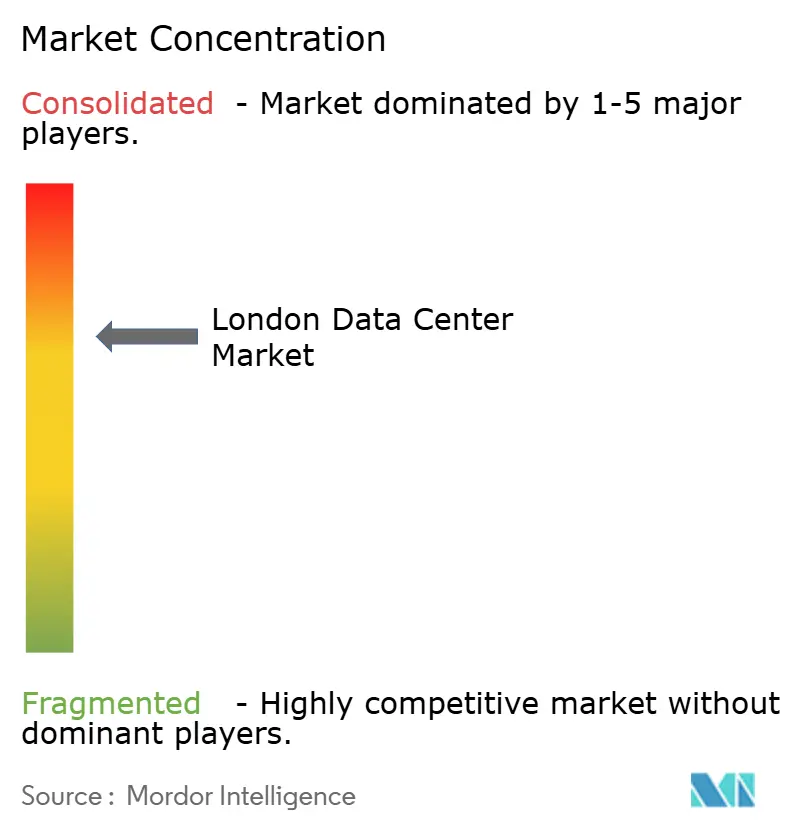

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

London Data Center Market Analysis by Mordor Intelligence

London data center market size in 2026 is estimated at 2.77 GW, growing from 2025 value of 2.45 GW with 2031 projections showing 5.16 GW, growing at 13.21% CAGR over 2026-2031. Growth is propelled by hyperscaler demand for AI-ready capacity, sustained enterprise migration to hybrid architectures, and London’s unmatched global connectivity. Operators are redesigning facilities to support 40-140 kW rack densities, embracing liquid and river-water cooling, and adopting 24/7 carbon-free power procurement. Intensifying grid constraints in West London have nudged new builds eastward, while the UK government’s AI Growth Zones and Critical National Infrastructure designation create a clearer policy runway. Market participants are now balancing soaring AI-driven power requirements against tightening energy-efficiency mandates, catalyzing investments in renewable PPAs, district-cooling schemes, and waste-heat recovery. Competitive pressure remains sharp as Equinix, Digital Realty, and NTT protect incumbency, yet agile specialists such as Kao Data capture premium AI workloads.

Key Report Takeaways

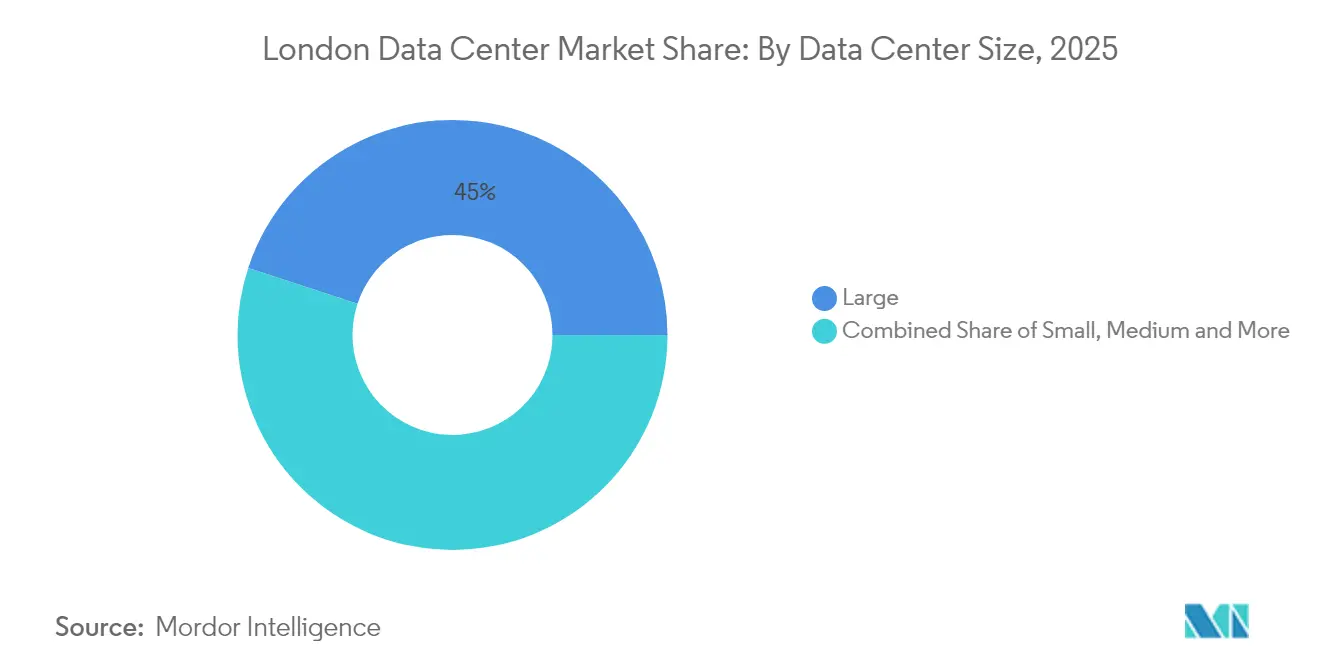

- By data-center size, Large facilities (10-20 MW) led with 44.95% of London data center market share in 2025, while Mega facilities (>40 MW) are poised for the fastest 27.60% CAGR through 2031.

- By tier type, Tier 3 sites held 84.35% revenue share in 2025; Tier 4 is projected to expand at 36.10% CAGR, the quickest among all tiers.

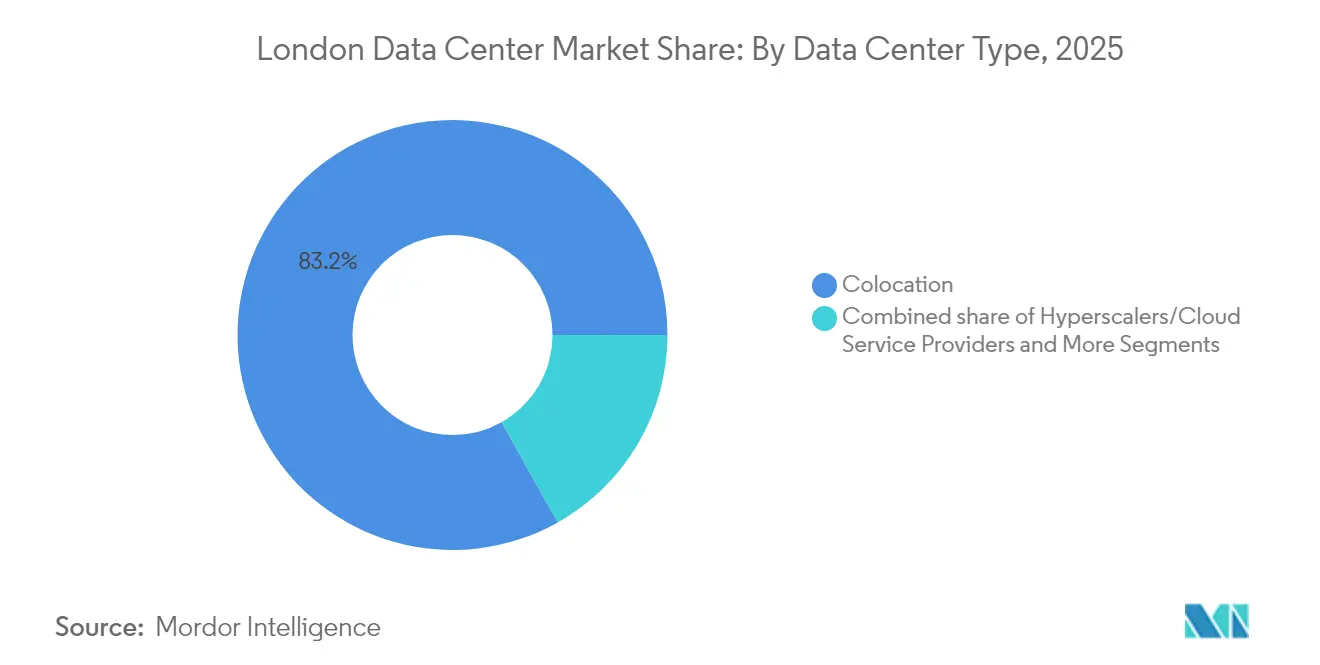

- By facility type, colocation captured 83.15% share of the London data center market in 2025; hyperscalers are projected to record a 14.55% CAGR to 2031.

- By end user, cloud & IT services commanded 22.10% of the London data center market size in 2025; government workloads exhibit the highest 22.40% CAGR outlook.

- By geography, West London retained close to half of installed capacity in 2025, but East London is forecast to outpace at 18.95% CAGR on new power availability.

- Equinix, Digital Realty, and NTT collectively controlled more than 44.20% of the London data center market size in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

London Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscaler cloud expansion demand | +5.2% | Slough, Docklands, East London | Medium term (2-4 years) |

| AI / GPU-driven high-density compute requirements | +4.8% | Financial district, wider metropolitan area | Medium term (2-4 years) |

| Sub-sea cable and metro-fiber ecosystem depth | +1.8% | London core and adjacent counties | Long term (≥ 4 years) |

| Renewable-energy PPAs and net-zero mandates | +1.3% | UK-wide with London as early adopter | Long term (≥ 4 years) |

| London Underground fiber right-of-way for edge DCs | +0.6% | Central city extending to outer zones | Medium term (2-4 years) |

| Thames River district-cooling schemes | +0.4% | Docklands and riverside developments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hyperscaler Cloud Expansion Driving Market Growth

Hyperscalers continue to underwrite the London data center market, committing multi-billion-pound budgets to AI-ready builds and retrofit programs. January 2025 saw a UK government announcement of GBP 14 billion in data-center projects aimed at AI infrastructure, redirecting new capacity toward designated AI Growth Zones. CoreWeave’s GBP 1 billion entry underscores the capital depth backing GPU-accelerated environments. Slough’s historic dominance is waning as power caps squeeze new requests; Ada Infrastructure’s 210 MW Royal Docks campus illustrates the eastward realignment. Community benefit packages—on-site skills academies, public green space, and district-heating interfaces—have become standard as developers secure faster approvals.

AI-Driven Compute Density Transforming Facility Design

The arrival of 40-140 kW racks has reset design norms across the London data center market. Kao Data’s deployment of Nvidia H200 GPUs in March 2025 demonstrated the operational leap, integrating closed-loop rear-door heat exchangers and 100% renewable energy feeds. Power draw per AI server now runs 4-5 times that of legacy workloads, forcing new revenue models that blend power, space, and cooling metrics. Financial-services tenants—whose algorithmic trading and risk simulations thrive on GPU clusters—accept higher colocation rates in exchange for latency-sensitive compute near the City. Facility blueprints increasingly adopt slab-to-slab clear heights above 6 m, dual 132 kV feeds, and modular cooling blocks that can swing from air-to-liquid without extended downtime.

Sub-sea Cable Ecosystem Enhancing London’s Connectivity Value

Low-latency trans-Atlantic links remain a marquee lure for the London data center market. Equinix’s LD4 and LD5 nodes in Slough anchor the Hibernia Express cable, sustaining sub-59 ms round-trip latency to New York, critical for high-frequency trading.[1]Equinix, “London Data Centers | Premium Colocation Provider and Internet Exchange Point,” equinix.com Hyperscalers’ direct ownership of new cables is reshaping carrier economics, routing fresh landings to purpose-built hyperscale campuses. This vertical integration deepens London’s role as a cloud region while heightening physical-security diligence; industry consortia have urged new European standards for cable protection, reflecting concerns over geopolitical disruption.

Renewable Energy PPAs Becoming Operational Imperative

For operators competing on ESG credentials, 24/7 carbon-free supply has replaced annual RECs. Kao Data’s Harlow campus exemplifies the shift, locking multi-year renewable PPAs that track hourly consumption. UK policy revisions tightening minimum energy-performance benchmarks spur similar commitments across the London data center market. Sophisticated energy-management software now arbitrages grid, battery, and onsite generation in real time, smoothing volatility from offshore wind. District-heating exports, such as Queen Mary University’s January 2025 heat-reuse rollout, demonstrate monetizable sustainability pathways.[2]UK Government, “Thousands of homes to be kept warm by waste heat from computer data centres in UK first,” gov.uk

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-power allocation shortages in West London | -2.1% | Ealing, Hillingdon, Hounslow | Short term (≤ 2 years) |

| High land and business-rate costs + planning delays | -1.4% | Greater London, acutest in central zones | Medium term (2-4 years) |

| Waste-heat reuse obligations tightening CAPEX | -0.9% | City-wide with priority on new builds | Medium term (2-4 years) |

| HV commissioning-engineer scarcity | -0.5% | London-wide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Grid-Power Allocation Creating Critical Development Bottleneck

Pending grid requests topping 400 GW in West London have triggered a pause on new connections, compelling developers to fund sub-station upgrades or migrate projects east of the city.[3]Greater London Authority, “West London Electricity Capacity Constraints,” london.gov.uk Some proposals have been rejected outright on power-availability grounds, pushing operators toward hybrid on-site generation and battery solutions. Government deliberations on connection-queue reform and vessel-to-grid pilots on the Thames hint at near-term relief, yet risk persists for schemes banking on 100 MW-plus blocks in constrained boroughs.

High Land Costs and Planning Complexities Impeding Growth

Land in Slough, Docklands, and Central London ranks among Europe’s most expensive parcels, elevating entry thresholds for new players. A more rigorous planning environment further elongates timelines; local councils now insist on clear community benefits and demonstrable emissions reductions. The national reclassification of data centers as significant infrastructure promises streamlined approvals above 50 MW, but smaller schemes still navigate borough-specific variances. Savvy developers now embed pre-application community sessions and transparent sustainability dashboards to secure buy-in.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Size: Mega facilities capturing AI-driven growth

Large sites between 10 MW and 20 MW led capacity in 2025, contributing 44.95% to the London data center market. The dominance reflected their sweet spot in balancing build costs and proximity to key fiber routes. Momentum is shifting, however, toward Mega campuses exceeding 40 MW, projected to gallop ahead at a 27.60% CAGR between 2026 and 2031. Ada Infrastructure’s 210 MW Royal Docks project illustrates the blueprint: three 70 MW halls configured for liquid-cooled GPU clusters and supplemented by district-cooling tie-ins. Such projects exploit economies of scale in power procurement and on-site sub-station build-outs, giving operators tariff leverage with distribution network operators. Smaller facilities under 5 MW are repurposed into edge nodes that trim latency for IoT and fintech applications, extending the London data center market footprint into suburban exchange buildings and underground fiber vaults.

The growth trajectory reinforces consolidation pressures. Mega campus investors bundle multiple data halls into a single planning envelope, reducing per-MW capital expenditure and shortening time-to-revenue. Enterprises gravitate toward these scale facilities for predictable expansion paths and richer interconnection fabrics. Conversely, medium-sized assets now face capex upgrades to chase rising rack densities. Operators unable to retrofit to 30 kW racks may see occupancy taper as AI workloads bypass them, driving mergers or asset sales. The London data center market size for Mega facilities is forecast to double, lifting their revenue contribution above one-third of the total by decade’s end.

By Tier Type: Tier 4 facilities surging on resilience demands

Tier 3 halls supplied 84.35% of the London data center market in 2025, valued for concurrent maintainability and cost discipline. Yet Tier 4 facilities, while a niche today, are racing ahead at 36.10% CAGR through 2031 as AI model-training jobs, financial clearing, and regulated workloads seek fault tolerance. Tier 4’s 99.99% uptime and 2N+1 redundancy shield high-value computations from costly resets—outages can erase days of training cycles or stall multi-billion-pound trades. Operators price Tier 4 footprints at a 25-40% premium over Tier 3; demand still outstrips supply, signaling headroom for new greenfield builds.

Regulation tightens the narrative. The EU’s Digital Operational Resilience Act pushes financial entities toward demonstrable infrastructure redundancy, channelling fresh requirements into London data center market contracts. Some hyperscalers are blending Tiers—hosting latency-sensitive front ends in Tier 4 zones and relegating batch processing to Tier 3 wings within the same campus. Over time, hybrid architectures could erode the stark pricing differentials, but for now, Tier 4 remains the favoured badge for mission-critical deployments.

By Data Center Type: Hyperscalers driving next wave of expansion

Colocation retained an 83.15% share of the London data center market in 2025, answering enterprises’ appetite for elasticity without capex burden. Within colocation, hyperscale-focused formats held 41.60%, themselves advancing at 23.90% CAGR. Parallel to this, hyperscalers’ self-built campuses are projected to outstrip every other archetype at 14.55% CAGR, reflecting surging AI inference and sovereign-cloud workloads. Sovereign requirements from UK public-sector agencies favour in-country zones, attracting AWS, Microsoft, and Google to earmark land for dual-region availability pairs.

Edge-compute footprints grow incrementally as 5G rollouts press latency expectations below 5 ms for fintech and augmented-reality use cases. Small carrier-neutral sites inside Tube stations and roadside cabinets emerge as new endpoints. Meanwhile, enterprise-owned on-premises suites decline, with CFOs reallocating budgets toward cloud architectures and GPU-as-a-service consumption. The London data center industry thus migrates toward a tri-layer stack—mega-scale cores, suburban edge pods, and metro micro-nodes—each commanding its own economics and power-density profile.

Geography Analysis

West London’s historic cluster, anchored by Slough Trading Estate, still hosts nearly half of installed capacity in the London data center market. Superior fiber routes to the City and primary liquidity venues made it the early default for colocation builds. Yet grid-power caps have frozen large new connections, and available land now trades at premium rates. Developers report lead times surpassing 60 months for 100 MW sub-station slots, prompting some operators to pivot expansions north toward Hemel Hempstead or Reading where grid headroom persists.

East London’s Royal Docks district is rapidly emerging as the new powerhouse. Ada Infrastructure’s 210 MW campus has become the bellwether, validated by planning approval that integrated community skills hubs and river-water cooling. Proximity to Docklands fiber paths maintains the low-latency link cherished by financial services; relative land affordability underpins project economics. Over the next five years, East London’s share of the London data center market size is projected to climb from single digits to mid-teens, lifting overall capacity resilience for the metro.

The Docklands area itself, despite spatial constraints, remains London’s interconnection heart, home to the London Internet Exchange. Telehouse is expanding legacy sites vertically, employing multi-story data halls and direct-to-chip liquid cooling to unlock incremental megawatts. Peripheral towns beyond the M25—such as Basingstoke and Didcot—now court hyperscale builds, bundling renewable-energy proximity and quicker grid hookups. This geographic dispersion ensures the London data center market retains growth momentum even as core boroughs face planning headwinds.

Competitive Landscape

Equinix, Digital Realty, and NTT hold dominant interconnected campuses and collectively exceed 45% of installed MW, giving the London data center market a moderate concentration profile. Equinix leverages its neutral interconnection fabric, drawing cloud-on-ramp demand from financial and media firms. Digital Realty’s July 2024 Slough acquisition advanced its metro footprint to 14 facilities, boosting cross-campus capacity planning. NTT’s May 2025 land purchase for LON2 signals a continued multi-GW global expansion plan that positions London as its EMEA flagship.

Niche specialists add competitive nuance. Kao Data’s AI-optimized campus became the first UK site to host Nvidia H200 GPUs, winning workloads with tailored liquid-cooling and 100% renewable supply. Telehouse reinforces its position by anchoring subsea routes and maintaining sub-5 ms metro round-trips, a critical feature for financial exchanges.

Sustainability is now a visible battleground. Operators publish hourly carbon-intensity dashboards and commit to heat-reuse partnerships with municipal housing. Early movers secure planning goodwill and long-term PPAs at favourable tariffs, differentiating beyond megawatt scale alone. With capital inflows chasing AI capacity and policy tightening around emissions, consolidation may accelerate, especially for mid-tier players lacking liquidity for efficiency retrofits.

London Data Center Industry Leaders

Equinix, Inc.

Digital Realty Trust, Inc.

Telehouse (KDDI)

Global Switch

VIRTUS Data Centres

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: NTT DATA secured 26.3 acres for its LON2 site, bolstering its London portfolio and supporting a USD 10 billion global expansion plan.

- April 2025: UK Power Networks launched “Electric Thames,” testing floating battery barges to alleviate riverside grid strain.

- March 2025: Ori installed Nvidia H200 GPUs at Kao Data’s Harlow campus, marking the first UK deployment.

- January 2025: Queen Mary University began heating campus buildings with data-center waste heat, showcasing circular-energy viability.

- January 2025: The UK government unveiled GBP 14 billion of AI-aligned data-center projects within its AI Opportunities Action Plan.

- July 2024: Digital Realty purchased a Slough data-center site for USD 200 million, expanding its metro footprint to 14 facilities.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study frames the London data center market as the aggregate installed IT-load capacity hosted inside professionally built, multi-tenant colocation, hyperscale cloud, or enterprise facilities located within Greater London's metropolitan ring. Capacity is tracked in megawatts (MW) and gigawatts (GW) of critical IT load that is commercially contracted or owner-operated.

Scope exclusions: Small on-premise server rooms below 250 kW and disaster-recovery pop-sites positioned outside the M25 are not counted.

Segmentation Overview

- By Data Center Size

- Small

- Medium

- Large

- Massive

- Mega

- By Tier Type

- Tier 1 and 2

- Tier 3

- Tier 4

- By Data Center Type

- Hyperscalers/Cloud Service Providers

- Enterprise and Edge

- Colocation

- Utilized

- Colocation Type

- Retail

- Wholesale

- Hyperscale

- End User

- Cloud and IT

- Telecom

- Media and Entertainment

- Government

- BFSI

- Manufacturing

- E-Commerce

- Other End User

- Colocation Type

- Utilized

- Non-Utilized

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview data-center developers, electrical engineers, real-estate brokers, and cloud procurement managers across the UK, continental Europe, and North America. These discussions validate live versus commissioned power, average sell-through rates, and achievable price per kW, filling gaps that secondary data alone cannot resolve.

Desk Research

We start with verifiable public datasets such as Ofgem's sub-regional electricity allocation files, HM Land Registry price indices for industrial plots, and the Greater London Authority's planning portal, which tell us where power and land are truly available. Trade bodies like techUK and the Uptime Institute supply annual inventory audits, while Statista and DC Byte dashboards help us benchmark vacancy and under-construction pipelines. Company filings, investor decks, and press releases provide announced MW additions, and subscription tools including D&B Hoovers and Dow Jones Factiva let us cross-check operator revenues and contract wins. This list is illustrative; many other sources feed our desk research.

Market-Sizing & Forecasting

A top-down reconstruction of installed and pipeline IT load begins with National Grid connection data, land-bank disclosures, and planning approvals, which are then adjusted for average capacity utilization ramps. Select bottom-up checks, such as sampled rack counts and hyperscaler campus roll-ups, fine-tune totals before finalization. Key variables shaping the model include substation energization timelines, average rack density (kW per rack), vacancy absorption velocity, wholesale colocation pricing, renewable energy mix, and planned GPU-ready high-density halls. Forecasts apply multivariate regression on these variables and are stress tested through scenario analysis shared with interviewees, ensuring realistic CAGR paths.

Data Validation & Update Cycle

Triangulation against independent indicators (electric equipment shipments, fiber trench permits, and cloud CAPEX disclosures) surfaces anomalies that trigger re-checks. Each model passes a senior peer review, and reports refresh annually; material events such as megawatt-scale M&A or large grid allocation awards prompt interim updates so clients receive the newest view.

Why Mordor's London Data Center Baseline Stands Dependable

Published market values often diverge because firms select different geographic cut-offs, treat pipeline capacity unevenly, or convert currencies at mismatched dates.

Our disciplined scope, quarterly grid connection tracking, and yearly refresh cadence limit those distortions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 2.45 GW IT load | Mordor Intelligence | - |

| 1.30 GW | Global Consultancy A | Excludes pre-leased halls and downgrades pipeline beyond 12 months |

| 1.56 GW | Industry Association B | Counts live capacity only and omits enterprise self-build campuses |

The comparison shows that once future-dated capacity and self-operated hyperscale sites are rightly included, Mordor's baseline presents the fullest, most transparent picture, giving decision makers a dependable starting point for strategy.

Key Questions Answered in the Report

What is the current size of the London data center market?

The London data center market stands at 2.77 GW of installed IT power in 2026.

How fast is the London data center market expected to grow?

Capacity is projected to advance to 5.16 GW by 2031, translating to a 13.21% CAGR.

Why are Mega data centers gaining prominence in London?

AI workloads demand high rack densities and economies of scale, propelling Mega campuses (>40 MW) toward a 27.60% CAGR-the quickest among all size categories.

Which geographic area of London is attracting new data center investments?

East London’s Royal Docks is emerging as the preferred zone thanks to better grid access and lower land costs, exemplified by Ada Infrastructure’s 210 MW campus.

How are operators addressing power-grid constraints in West London?

Strategies include relocating builds eastward, funding sub-station upgrades, exploring vessel-to-grid battery projects on the Thames, and signing renewable-energy PPAs.

What regulatory trend most affects new data-center builds in London?

Tighter energy-efficiency and 24/7 carbon-free requirements are reshaping facility design and siting decisions, making sustainability credentials crucial for planning approval.

Page last updated on: