Hong Kong Data Center Networking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

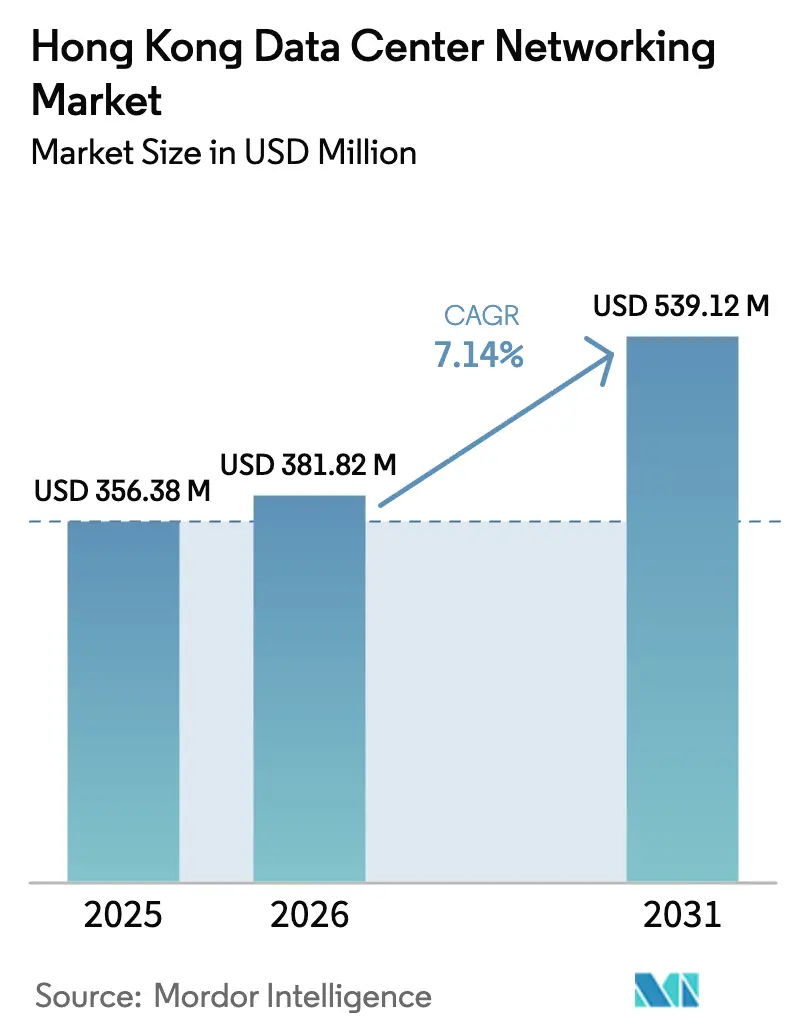

| Base Year Market Size (2025) | USD 356.38 Million |

| Market Size (2026) | USD 381.82 Million |

| Market Size (2031) | USD 539.12 Million |

| Growth Rate (2026 - 2031) | 7.14% CAGR |

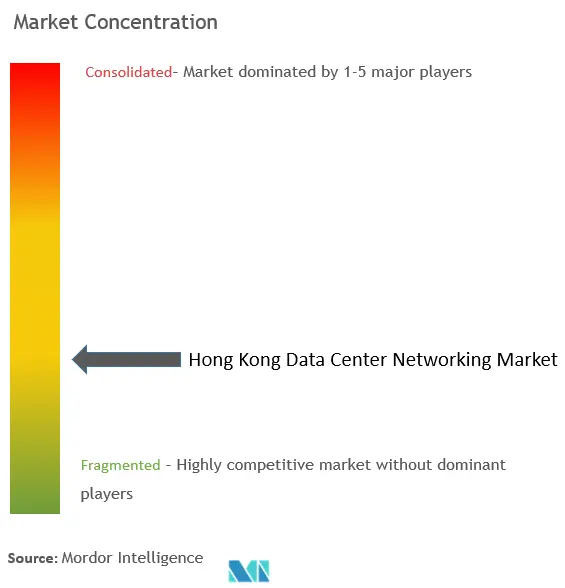

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hong Kong Data Center Networking Market Analysis by Mordor Intelligence

The Hong Kong data center networking market size was valued at USD 356.38 million in 2025 and estimated to grow from USD 381.82 million in 2026 to reach USD 539.12 million by 2031, at a CAGR of 7.14% during the forecast period (2026-2031). Momentum is fueled by hyperscale capital expenditure, aggressive cloud-service uptake, and 5G-enabled edge traffic that together reinforce the territory’s role as a digital gateway connecting mainland China with the rest of the world. Service providers are modernising switching fabrics to support AI-driven workloads, while sustainability mandates are accelerating retrofits of legacy hardware with energy-efficient, software-defined alternatives. Land and power scarcity raise operating costs and have triggered vertical designs that prioritise high-density networking and efficient cooling. More than 581 MW of operational capacity existed in 2024, and capacity is on track to double by 2030, intensifying demand for high-bandwidth optics able to scale beyond 100 GbE.

Key Report Takeaways

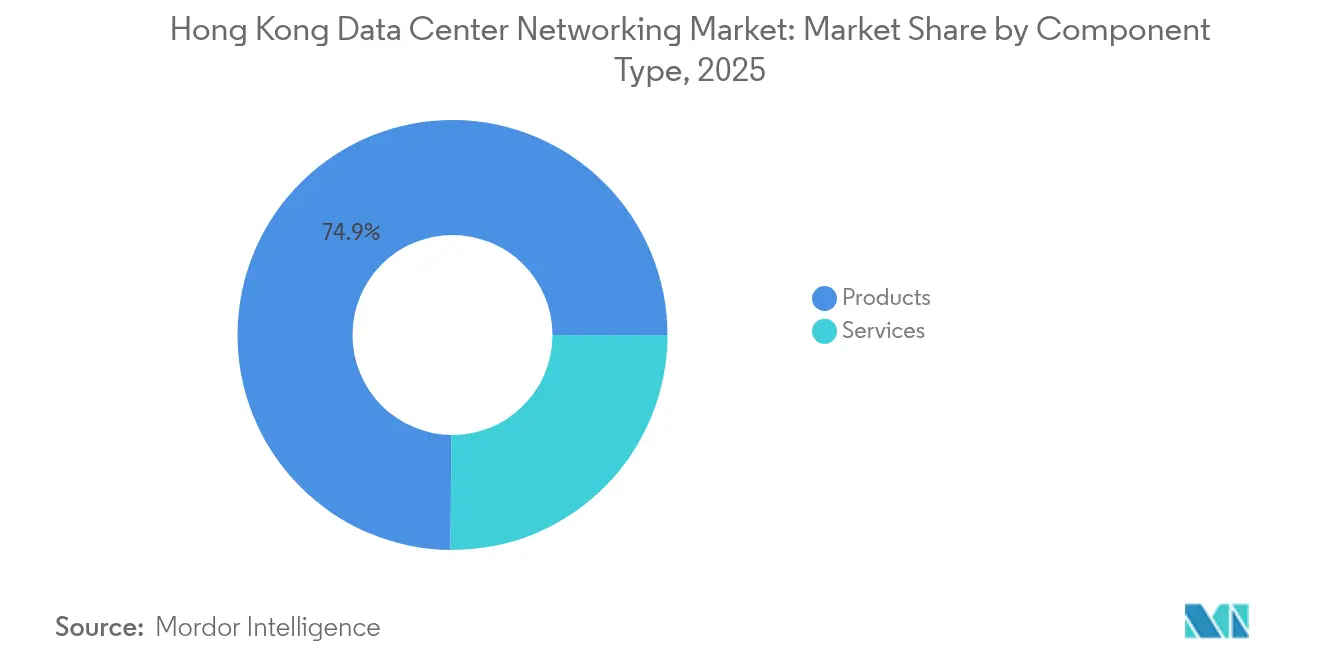

- By component, products led with 74.85% revenue share in 2025; services recorded the fastest CAGR at 9.89% through 2031.

- By end-user, IT & telecommunications held 36.65% of the Hong Kong data center networking market share in 2025, while manufacturing and industrial applications are expanding at 11.05% CAGR to 2031.

- By data-center type, colocation accounted for 51.62% of the Hong Kong data center networking market size in 2025; hyperscalers and cloud service providers post the top CAGR at 11.92% during the outlook period.

- By bandwidth, the 50-100 GbE segment commanded a 34.88% share of the Hong Kong data center networking market size in 2025; greater than 100 GbE is advancing at an 11.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

No country-level or regional dataset alone defines global value; it is assembled from all contributing countries and geographies, including Hong kong. Our global data center networking market size reflects this full aggregation.

Hong Kong Data Center Networking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-service adoption surge | +2.1% | Hong Kong, Greater Bay Area | Medium term (2-4 years) |

| Hyperscale and colocation capex boom | +1.8% | Hong Kong core | Short term (≤2 years) |

| 5G-enabled edge traffic growth | +1.5% | Territory-wide | Medium term (2-4 years) |

| Sustainability-driven network retrofits | +0.9% | Territory-wide | Long term (≥4 years) |

| Government tax incentives for DC upgrades | +0.6% | Domestic | Short term (≤2 years) |

| Greater Bay Area low-latency demand | +1.3% | Hong Kong-Shenzhen-Guangzhou | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Cloud-service adoption surge

Enterprises are retiring on-premises systems in favour of hybrid architectures that lean on hyperscale cloud nodes in Hong Kong. Equinix invested USD 124 million in its HK6 facility, designed for liquid-cooled AI racks, underlining the territory’s pull for capital-intensive cloud builds[1]Equinix, “Equinix to Invest US$124 Million in New Hong Kong Data Center,” equinix.com. Mobile penetration has topped 320% and peak connection speeds average 1,261.9 Mbps, ensuring sufficient access bandwidth for latency-sensitive SaaS workloads. Software-defined networking (SDN) adoption is rising because programmable fabrics allow multitenant isolation and rapid bandwidth allocation. Growing reliance on public cloud is therefore a durable catalyst for high-capacity, policy-driven switching platforms.

Hyperscale and colocation capex boom

BDx secured financing for a purpose-built hyperscale site in Kwai Chung that showcases high-density automation and energy optimisation. SUNeVision already supports around 15,000 interconnections in its carrier-neutral campuses, illustrating the scale of east-west traffic handled within a single metro.[2]Data Center Knowledge, “SUNeVision Hits 15,000 Interconnections,” datacenterknowledge.com Such density pressures vendors to supply high-radix switches and optical transport able to collapse tiered topologies into flatter fabrics that cut latency.

5G-enabled edge traffic growth

Private 5G pilots by NTT and others provide ultra-low-latency connectivity for smart-city use cases, fuelling micro-data-center rollouts across hospitals, campuses, and transport nodes. CUHK Medical Centre streams 4K medical video over HKT’s 5G backbone, demanding deterministic performance at the edge. Vendors are shipping compact, ruggedised switches that host compute modules, enabling local processing while maintaining a pathway to core clouds.

Sustainability-driven network retrofits

The Green Data Centres Practice Guide has tied equipment procurement to measurable energy performance.[3]Government of the Hong Kong SAR, “Green Data Centres Practice Guide,” gov.hk Equinix joined with CLP Power and PolyU to codify best practices, including eco-mode power supplies in top-of-rack switches and dynamic fan-speed control. ESR’s USD 205 million green loan underscores how access to capital now hinges on sustainability metrics. Operators thus refresh older 10/25 GbE equipment sooner and adopt ASICs fabricated on sub-7 nm processes to lower watt-per-gigabit ratios.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex for 100-800 GbE optics | -1.2% | Territory-wide | Short term (≤2 years) |

| Land and power supply scarcity | -0.8% | Core districts | Long term (≥4 years) |

| Geopolitical compliance uncertainty | -0.6% | Cross-border ops | Medium term (2-4 years) |

| Local SDN talent shortage | -0.4% | Territory-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High capex for 100-800 GbE optics

Operators migrating to 400 GbE coherent links face list prices that can exceed USD 10,000 per module. Chip shortages worsened the squeeze through early 2025. Many firms stage upgrades in phases, mixing 100 GbE leaf layers with 400 GbE spines to balance spend against scale needs, yet sticker-shock continues to delay full-fabric refresh cycles.

Land and power supply scarcity

Only a handful of government parcels remain earmarked for data center use, and new sites compete with logistics and residential projects. Power-allocation caps in Tseung Kwan O and Tsuen Wan keep energy budgets tight, leading to capacity auctions that lift rack rental rates. Constrained footprints motivate stacked server halls and, by extension, dense vertical cabling schemes that complicate network design.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Dominance Amid Service Acceleration

Products generated 74.85% of all Hong Kong data center networking market revenue in 2025, thanks to one-off capital outlays for switching, routing, and optical gear. Ethernet switches form the bulk of spend as enterprises refresh 10/25 GbE ports to 50/100 GbE leaf-spine fabrics. Robust router demand stems from cross-border traffic engineering and 5G backhaul. Storage-area-network interfaces ride the same bandwidth curve as AI training clusters. In security, application-delivery controllers and network-firewall appliances grow rapidly following the Critical Infrastructure Bill’s tougher mandates.

Services, while smaller, are scaling at 9.89% CAGR through 2031. Managed network services see uptake among banks and OTT platforms that outsource operations. Integration consultancies thrive on complex SDN rollouts, and training providers benefit from a persistent skills gap. Support contracts shift from break-fix to subscription models as software takes a larger share of functionality.

By End-User: IT Sector Leadership with Manufacturing Momentum

The IT and telecommunications vertical held 36.65% of the Hong Kong data center networking market size in 2025. Telcos refit legacy MPLS cores with SR-enabled IP fabrics to deliver network slicing for SME cloud connectivity, while cloud providers overlay programmable policies to orchestrate thousands of tenant VPCs.

Manufacturing and industrial customers, although smaller today, lead growth at 11.05% CAGR. Hong Kong’s re-industrialisation strategy plans advanced R&D labs that need deterministic low-latency links for robotics and real-time analytics. Smart-factory pilots in Tseung Kwan O rely on ruggedised switches that support Time Sensitive Networking (TSN). Healthcare and life-sciences adoption accelerates under the Science Park’s new digital health ecosystem program, requiring HIPAA-grade network segmentation.

By Data-Center Type: Colocation Stability Versus Hyperscaler Acceleration

Carrier-neutral colocation retained 51.62% revenue in 2025 because financial services, gaming, and CDN tenants value cross-connect density. Nine intra-Asian subsea cables land inside these facilities, reinforcing their hub status.

Hyperscale and cloud-service providers, though presently smaller, post the fastest 11.92% CAGR. Global players build dedicated campuses like BDx’s Kwai Chung site, optimised for AI liquid cooling and 100 GbE+ fabrics. Edge and micro sites emerge near stadiums, hospitals and transport hubs to shave latency for AR/VR and tele-surgery applications, embedding small-footprint routers and front-end caches tied via 400 ZR coherent optics.

By Bandwidth: High-Speed Migration Accelerates

The 50-100 GbE segment controls 34.88% revenue, the practical standard for most enterprise refresh cycles in 2025. Yet the >100 GbE class posts an 11.22% CAGR, pushed by AI clusters requiring 400 GbE leaf-spine pairs. Ciena’s 400 GbE coherent optics validated metro-reach economics for such pipes

Sub-10 GbE share declines as support contracts lapse. 25-40 GbE gear serves budget-constrained SMEs but is viewed as a stepping-stone. FlexE and 800 GbE roadmaps from Microchip and Broadcom are on watchlists as customers future-proof cable trays without expanding physical port counts

Geography Analysis

Hong Kong sits at the confluence of 11 intra-Asian subsea cables, nine of which terminate within the territory’s carrier-neutral campuses, anchoring it as a traffic exchange for North-South and East-West routes. Tseung Kwan O, Tsuen Wan and Kwai Chung host the bulk of the 581 MW live capacity logged in 2024, and fresh supply of roughly 700 MW is permitted or under construction, positioning the metro for a near-doubling by 2030.

Government roadmaps such as Smart City Blueprint 2.0 incentivise digital services that rely on low-latency backbones, including autonomous-bus pilots and e-government platforms. Tax deductions for energy-saving retrofits spur demand for high-efficiency switches.

Cross-border data co-operation initiatives let Hong Kong-based operators host mainland enterprise traffic under clarified compliance, though geopolitical tensions force multi-vendor strategies to mitigate sourcing risk. Vacancy tightened to 21% in late 2024, pushing rack rates higher and accelerating adoption of ultra-dense optical transceivers to wring capacity from existing shells. Average peak internet speeds of 1,261.9 Mbps and mobile penetration above 320% ensure last-mile readiness for cloud and OTT workloads.

The data center networking market is assessed by Mordor Intelligence through a multi-layered geographic lens, covering other regions such as Asia, Africa, and North America, along with detailed country-level analysis for Taiwan, China, Nigeria, United States, Sweden, and Austria.

Competitive Landscape

Competition is moderate, with the top five switch and router suppliers collectively holding an estimated majority, yet leaving room for SDN-focused disruptors. Incumbents Cisco, Juniper, and Huawei pivot toward disaggregated operating systems that decouple hardware from control planes. Arista posted USD 7 billion in 2024 revenue and launched its Etherlink-AI platform optimised for GPU clusters, bundling leaf-spine designs with workload-aware telemetry.

Partnership ecosystems grow: Equinix integrates Nvidia’s Spectrum-X in HK6 to offer bare-metal AI fabric. Schneider Electric and Vertiv co-develop prefabricated power-network pods to shorten hyperscale build times. Political scrutiny over equipment provenance drives many operators to insist on multi-vendor fabrics blending Western ASICs with open-source NOS, benefiting companies like Arrcus and DriveNets that specialise in cloud-native routing stacks.

Energy efficiency is a clear differentiator. H3C markets silicon-photonic transceivers rated below 4 W per 400 GbE port. Juniper’s Apstra intent-based software automates under-load power throttling, cutting switch-floor consumption by up to 20%. As AI training clusters balloon, vendors able to guarantee deterministic micro-burst handling at sub-five-microsecond latency command a pricing premium. The Hong Kong data center networking market concentration score is assessed at 6, reflecting share dominance by a handful of global OEMs yet notable growth of niche SDN players.

Hong Kong Data Center Networking Industry Leaders

Cisco Systems Inc.

Arista Networks Inc.

Huawei Technologies Co. Ltd.

Juniper Networks Inc.

Dell Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Thales Group published guidance for Hong Kong’s Critical Infrastructure Bill preparation, outlining cybersecurity requirements for data centers and networking systems.

- May 2025: BDx Data Centers secured project financing from Clifford Capital, UOB and SMBC for its first dedicated hyperscale facility in Kwai Chung.

- February 2025: Cushman & Wakefield reported that operational capacity reached 581 MW and is projected to double within five years.

- October 2024: Equinix launched its Digital Super-connector Program in Hong Kong following a HK$1 billion investment in HK6.

- October 2024: Hong Kong Science and Technology Parks Corporation partnered with 12 organisations to develop an international digital health ecosystem.

- August 2024: Equinix announced a USD 124 million investment for its HK6 data center, designed for liquid-cooled AI racks.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Hong Kong data-center networking market as the annual value generated by switches, routers, optical interconnects, security appliances, software-defined networking stacks, and related professional services that knit together servers and storage inside colocation, hyperscale, and edge facilities. The figure captures fresh hardware shipments and recurring support fees that keep racks online at five-nines availability.

Scope exclusion: telecom backhaul equipment serving public 5G or fixed broadband access sits outside this sizing.

Segmentation Overview

- By Component

- Products

- Ethernet Switches

- Routers

- Storage Area Network (SAN)

- Application Delivery Controllers (ADC)

- Network Security Appliances

- Software-Defined Networking (SDN) Controllers

- Optical Interconnects

- Services

- Installation and Integration

- Training and Consulting

- Support and Maintenance

- Managed Network Services

- Products

- By End-User

- IT and Telecommunications

- Banking, Financial Services and Insurance (BFSI)

- Government and Defense

- Media and Entertainment

- Healthcare and Life Sciences

- Manufacturing and Industrial

- Other End-Users

- By Data-Center Type

- Colocation

- Hyperscalers/Cloud Service Providers

- Edge/Micro Data Centers

- By Bandwidth

- Less Than equals to 10 GbE

- 25–40 GbE

- 50–100 GbE

- Greater Than 100 GbE

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed data-center operators, regional network architects, and optics distributors across Tseung Kwan O, Kwai Chung, and Central. Discussions validated ASP shifts toward 100 GbE optics, confirmed lead times on 400 GbE leaf-spine deployments, and highlighted how fintech latency requirements reshape switch purchase timing.

Desk Research

We began with open data from the Hong Kong Census & Statistics Department, the Office of the Communications Authority, and the Innovation and Technology Commission to map fiber density, rack counts, and cloud adoption rates. Trade association portals such as the Submarine Cable Map, the Hong Kong Internet Exchange, and the Asia Cloud Computing Association provided traffic benchmarks and latency corridors that influence port-speed mix. Company filings, investor decks, and local press helped benchmark capex per megawatt and annual port refresh cycles. Paid databases, including D&B Hoovers for operator financials and Dow Jones Factiva for deal tracking, added depth. This list is illustrative, not exhaustive; many additional sources informed cross-checks and clarifications.

Market-Sizing & Forecasting

A top-down model reconstructs demand from installed rack totals, average switch ports per rack, and prevailing ASPs, which are then validated through selective bottom-up checks on shipment volumes collected from channel partners. Key inputs include submarine-cable landing growth, vacancy rates, hyperscale capex announcements, port-speed migration curves, and power capacity additions. Multivariate regression links these drivers to historical spend and projects value through the forecast period. Gaps in operator disclosures are bridged with sampled ASP × volume pairs and adjusted for equipment life cycles before final reconciliation.

Data Validation & Update Cycle

Outputs undergo anomaly screening, peer review, and a senior analyst sign-off. We refresh the model each year, with interim updates triggered by material events such as a new cable landing or change in land policy. Clients receive numbers that reflect the latest market signals.

Credibility of Mordor's Hong Kong Data Center Networking Baseline

Published estimates often diverge because firms choose different equipment mixes, bandwidth cut-offs, and currency bases.

Key gap drivers include variation in whether professional services are counted, dissimilar ASP progression methods, and contrasting refresh cadences.

Mordor reports a balanced base case that matches on-the-ground rack density with realistic port-upgrade timelines.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 356 M | Mordor Intelligence | - |

| USD 255 M | Regional Consultancy A | Excludes security appliances and services, uses conservative ASPs |

| USD 10.32 Bn | Trade Journal B | Aggregates broader cloud networking and mixes enterprise LAN spend |

Taken together, the comparison shows that Mordor's disciplined scope selection and annual refresh cadence yield a dependable baseline that decision-makers can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the forecast size of the Hong Kong data center networking market by 2031?

The Hong Kong data center networking market is projected to reach USD 539.12 million in 2031, expanding at a 7.14% CAGR from 2026.

Which end-user vertical is growing fastest and why?

Manufacturing and industrial applications are advancing at an 11.05% CAGR as smart-factory and Industrial IoT initiatives demand low-latency, high-reliability connectivity.

How are land and power constraints influencing network design?

Scarcity of land and tight power-allocation caps push operators toward vertical, high-density builds that rely on energy-efficient switches and compact optical transport systems to maximise capacity.

Why is Greater Than 100 GbE adoption accelerating in Hong Kong?

AI and real-time analytics workloads require leaf-spine fabrics capable of 400 GbE or higher throughput, driving the >100 GbE segment to grow at an 11.22% CAGR through 2031.

What government policies are shaping procurement decisions?

The Green Data Centres Practice Guide links equipment selection to energy-efficiency benchmarks, while the forthcoming Critical Infrastructure Bill mandates security-by-design networking solutions.

How is 5G deployment affecting edge networking demand?

Private 5G projects for smart-city and healthcare use cases create distributed traffic that necessitates edge-optimised switches and routers able to process data locally while maintaining cloud connectivity.

Page last updated on: