Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 43.46 Billion |

| Market Size (2031) | USD 209.13 Billion |

| Growth Rate (2026 - 2031) | 36.92% CAGR |

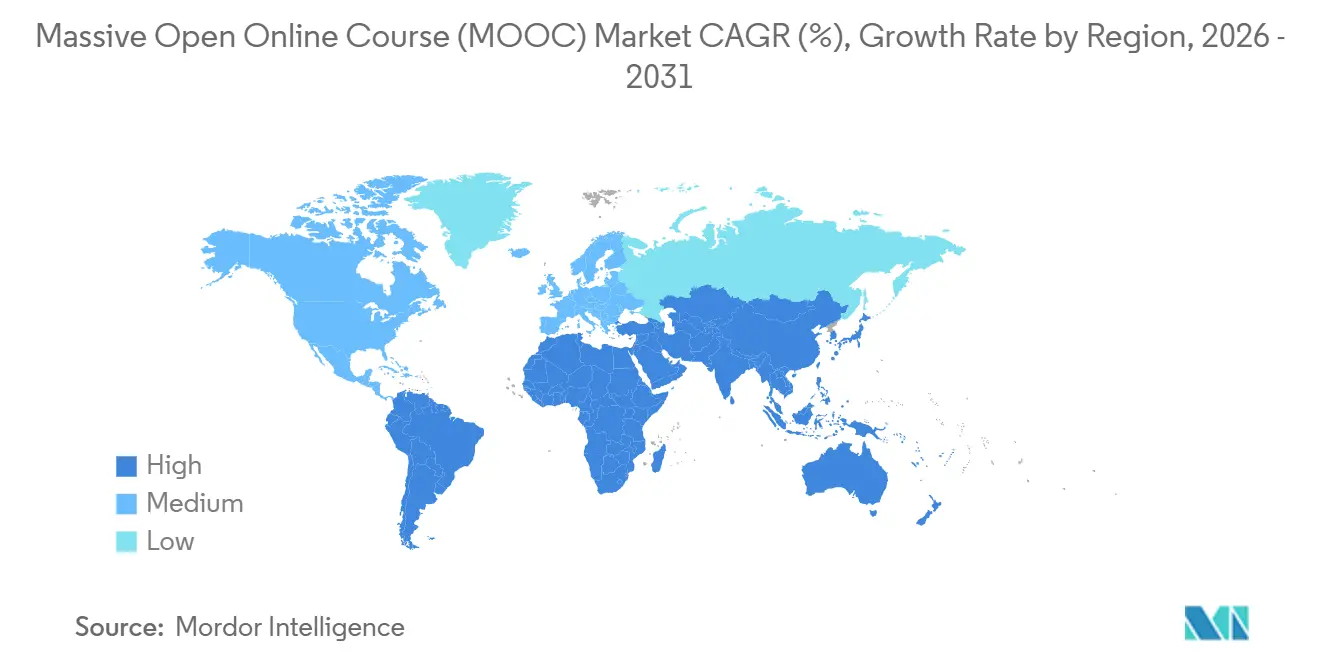

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Massive Open Online Course (MOOC) Market Analysis by Mordor Intelligence

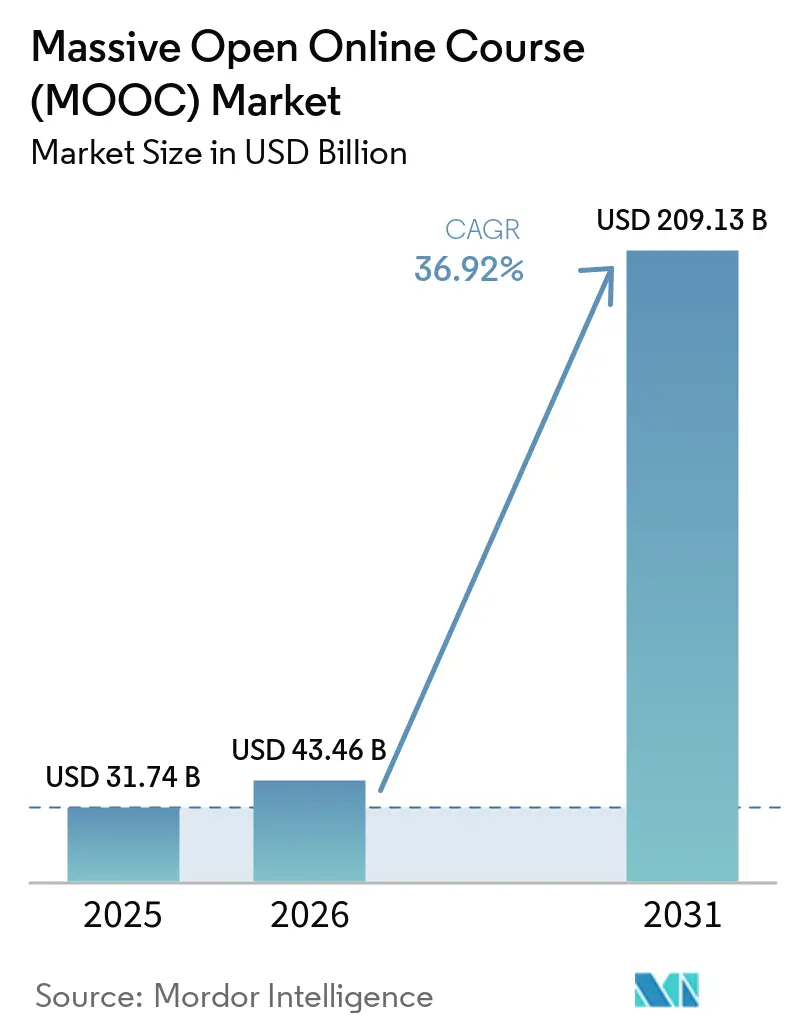

The Massive Open Online Course (MOOC) market size was valued at USD 31.74 billion in 2025 and estimated to grow from USD 43.46 billion in 2026 to reach USD 209.13 billion by 2031, at a CAGR of 36.92% during the forecast period (2026-2031). Soaring enterprise reskilling budgets, government-funded digital education programs, and rapid deployment of AI-driven adaptive learning engines underpin this expansion. The Massive Open Online Course market size stood at USD 31.74 billion in 2025 and is projected to reach USD 165.87 billion by 2030, translating into a 39.2% CAGR over the forecast period. Soaring enterprise reskilling budgets, government-funded digital education programs, and rapid deployment of AI-driven adaptive learning engines underpin this expansion.

Key Report Takeaways

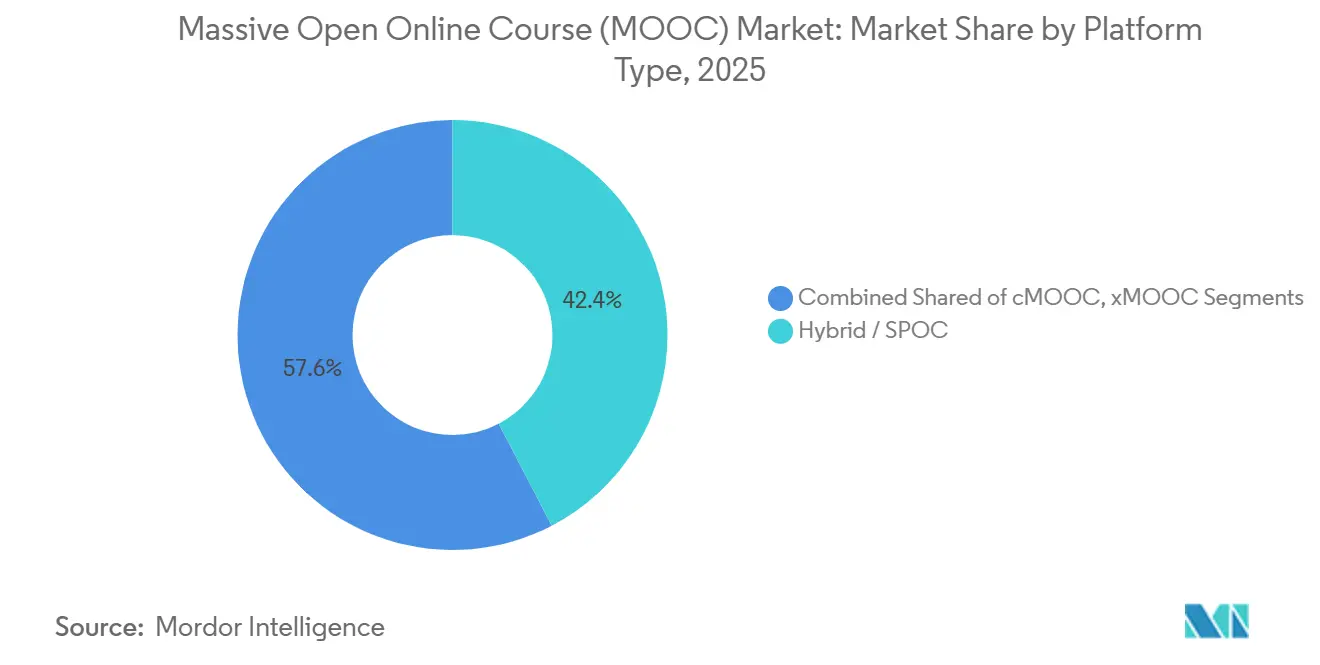

- By platform type, xMOOC captured 48.76% of the Massive Open Online Course market share in 2025.

- Hybrid/SPOC is forecast to advance at a 40.11% CAGR through 2031.

- By subject area, Technology and Computer Science led with 32.52% revenue share in 2025, while Language Learning is projected to expand at a 37.68% CAGR to 2031.

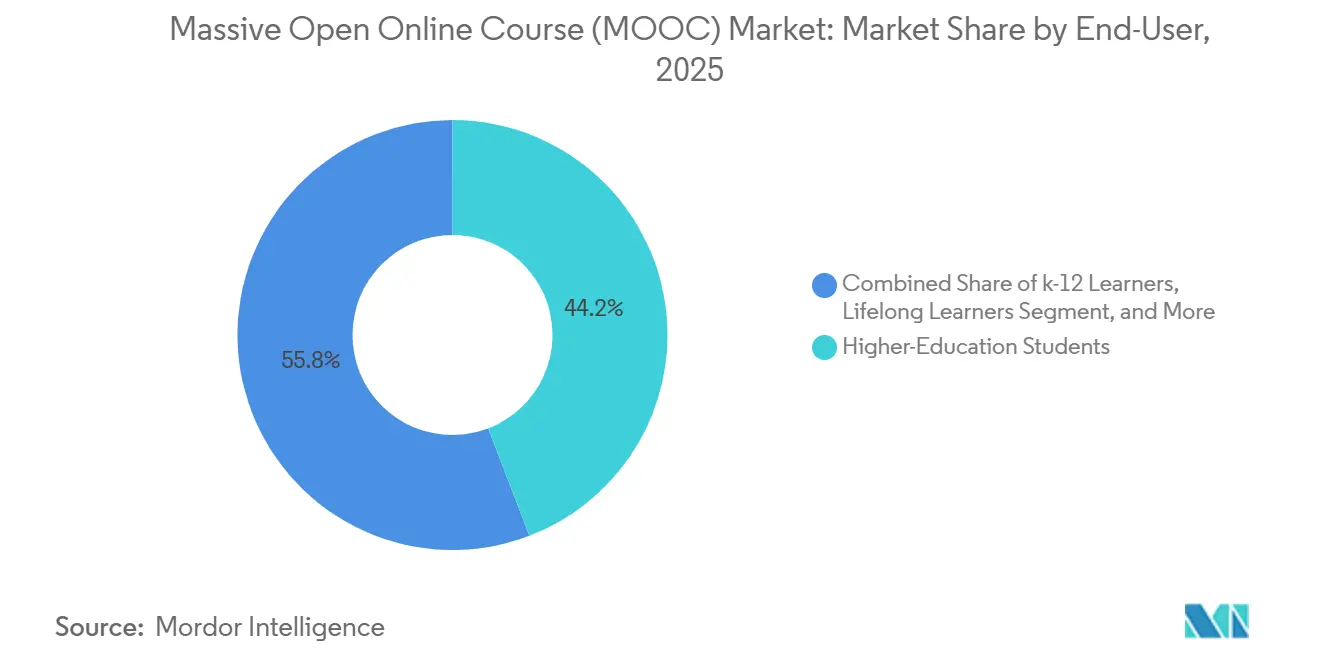

- By end user, higher-education students accounted for 44.18% of the Massive Open Online Course market size in 2025, and working professionals are climbing at a 37.41% CAGR between 2026-2031.

- By revenue model, freemium held 38.21% share of the Massive Open Online Course market size in 2025; subscription B2C is the most dynamic at a 37.92% CAGR over the same period.

- North America retained 31.65% of the Massive Open Online Course market share in 2025, whereas Asia-Pacific is set to post a 37.25% CAGR through 2031.

- Accenture, Coursera, and Udacity together controlled roughly 27% of 2024 global revenue, reflecting a moderately fragmented arena.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Massive Open Online Course (MOOC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for cost-effective flexible learning | +8.5% | Global, with stronger adoption in emerging markets | Medium term (2-4 years) |

| Corporate upskilling & reskilling mandates | +12.3% | North America & Europe core, expanding to APAC | Short term (≤ 2 years) |

| Smartphone & broadband proliferation | +6.8% | APAC core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Government push for micro-credentials & funding | +7.2% | Global, policy-driven in developed markets | Medium term (2-4 years) |

| AI-driven adaptive learning breakthroughs | +9.1% | North America & APAC leading, Europe following | Short term (≤ 2 years) |

| Global employer consortiums validating MOOC badges | +4.6% | Enterprise concentration in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Corporate upskilling mandates drive enterprise adoption

Enterprise learning budgets surpassed USD 350 billion in 2025 as employers tied competitive advantage to continuous skill renewal. FPT Corporation’s alliance with Udemy illustrates this momentum: the firm invested VND 187.3 billion (USD 7.6 million) to train staff across Japan and Korea, embedding curated MOOCs into its performance framework [1].FPT Corporation, “FPT and Udemy Forge Partnership to Enhance Human Resources Development,” fpt.com Similar talent-centric investments from Skillsoft and Accenture’s LearnVantage accelerate platform demand by connecting verified certificates to internal career ladders.

Government funding accelerates digital education infrastructure

Canada earmarked CAD 39.2 million (USD 29.1 million) for the CanCode program’s AI track, Australia allocated AUD 436.4 million (USD 291.6 million) to Skills for Education and Employment, and the EU’s Digital Europe Programme injected EUR 108 million (USD 117.7 million) into advanced digital skills. These grants subsidize content development, subsidize micro-credential recognition, and upgrade broadband capacity, positioning MOOCs as critical national competitiveness infrastructure[2].European Commission, “Digital Europe Programme: Calls for Artificial Intelligence and Advanced Digital Skills,” europa.eu

AI-driven personalization transforms learning outcomes

Generative AI course enrollments in Asia-Pacific rose 1,270% year on year in 2024. Major platforms now deploy real-time adaptive pathways, intelligent tutoring bots, and predictive analytics that flag at-risk learners before disengagement. Coursera’s Skills Benchmarking suite, for instance, calibrates lesson difficulty to prior assessment results, reducing early-stage drop-off and boosting verified-certificate completion to 21% on select cohorts.

Blockchain credentials gain enterprise recognition

Immutable credentialing gained traction as Hong Kong Polytechnic University issued blockchain-sealed certificates through its ACVP.hk portal, allowing employers to verify qualifications in seconds. The American Council on Education’s blockchain pilots in the United States further standardize digital wallets for academic records.. Survey data show 95% of employers perceive stackable blockchain badges as at least equal to traditional transcripts, shortening hiring cycles and raising MOOC credibility.

Restraints Impact Analysis*

| Restraint | ( ~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistently low completion and engagement rates | −6.8% | Global, higher in consumer segments | Medium term (2-4 years) |

| Quality-assurance / accreditation gaps | −4.3% | Regulatory variations worldwide | Long term (≥ 4 years) |

| Stricter data-privacy rules limiting analytics | −3.2% | Europe and North America core, expanding globally | Short term (≤ 2 years) |

| Post-pandemic digital fatigue dampening screen time | −2.9% | Higher impact in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Completion rates remain critically low despite innovation

Average course completion hovers between 5% and 15% on major platforms, and even MIT-Harvard joint MOOCs close at a 3.13% rate. India’s SWAYAM registers sub-4% completions despite government credit recognition, underscoring a persistent motivation gap. Research links early dropout to limited digital literacy, while later attrition correlates with time-management and academic skill mismatches. Platforms experiment with cohort mentors, micro-learning formats, and gamified milestones to mitigate attrition, yet material improvement remains elusive.

Data-privacy regulations constrain personalization capabilities

GDPR, CPRA, and other privacy regimes mandate opt-in consent, granular data rights management, and encryption standards that complicate real-time learning analytics. Engineering resources shift from feature innovation to compliance tooling such as robust audit logs and automated data-subject-access workflows. Smaller providers struggle to fund these upgrades, creating a competitive moat for incumbents with enterprise-grade security stacks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform Type: Hybrid models accelerate employee engagement

Hybrid/SPOC solutions captured 40.11% CAGR potential through 2031 as employers seek structured cohorts that blend asynchronous video with live coaching. xMOOCs still hold 48.76% of 2025 revenue, buoyed by university partnerships and well-defined curricula that address compliance and accreditation requirements. cMOOC offerings continue to serve collaborative knowledge communities but command limited scale.

Enterprises integrate Hybrid/SPOC platforms directly into learning-management systems to embed bite-sized virtual sessions into the workday. Real Madrid University School’s Coursera tie-up delivers 12 sports-industry courses that combine peer projects and faculty webinars to global cohorts. These structured experiences improve social presence and accountability, elevating feedback cycles and completion metrics compared with self-paced xMOOCs.

By Subject Area: Tech leadership meets surging language demand

Technology and Computer Science retained 32.52% of the Massive Open Online Course market share in 2025 by catering to relentless demand for programming, AI, and cybersecurity competencies. Massive Open Online Course market size in language learning is rising fastest, expanding at a 37.68% CAGR as remote work multiplies multilingual communication needs. Business and Management and Science and Engineering segments post steady gains but face competitive saturation.

Duolingo’s USD 748 million 2024 revenue validates consumer enthusiasm for gamified language apps that transition seamlessly into enterprise offerings. Simultaneously, 101 Blockchains collaborates with Accredible to issue digital certificates for over 30,000 professionals, demonstrating convergence between advanced tech content and credential innovation.

By End User: Working professionals reshape demand cycles

Higher-education students generated 44.18% of 2025 sales, leveraging MOOC credit pathways to accelerate degree timelines. However, working professionals register the strongest momentum at 37.41% CAGR, reflecting employer mandates that tie promotions and pay raises to verified skill milestones. The Massive Open Online Course market size generated by corporate learners is primed for outsized growth through 2031.

Udemy’s enterprise division earned USD 494.5 million in 2024 with 18% year-over-year expansion, contrasting a shrinking consumer segment. The University of Pretoria’s online programs through Higher Ed Partners South Africa demonstrate how academic institutions reposition to meet mid-career demand while preserving academic rigor.

By Revenue Model: Subscription momentum outpaces freemium

Freemium offerings attracted 38.21% of 2025 users by lowering entry barriers yet struggled with monetization. Subscription B2C services exhibit a 37.92% CAGR as enterprises favor predictable per-seat pricing that includes analytics dashboards and curated learning paths. Massive Open Online Course market size tied to pay-per-course sales remains resilient in credential-intensive niches such as advanced data science.

Coursera’s Q1 2025 revenue reached USD 179.3 million, propelled by its Coursera Plus subscription for enterprises. The Corporate Governance Institute’s credit-rated diplomas with Glasgow Caledonian University show how bundled subscriptions can mesh academic credit, professional recognition, and ongoing mentor support.

Geography Analysis

North America retained 31.65% of the Massive Open Online Course (MOOC) market share in 2025, anchored by robust venture-capital flows, deep corporate learning budgets, and early regulatory clarity on micro-credentials. The United States accounts for the lion’s share, with Accenture’s USD 1 billion Udacity acquisition underscoring confidence in platform economics. Canada’s CanCode funding embeds AI curricula into K-12 pipelines, while Mexico’s near-shoring boom fuels bilingual upskilling demand.

Asia-Pacific is the fastest-growing territory, expanding at a 37.25% CAGR. India’s SWAYAM and China’s domestic MOOC ecosystems tap colossal learner bases and government sponsorship that recognize MOOCs as scalable answers to higher-education capacity constraints. Australia’s AUD 436.4 million Skills for Education and Employment initiative reinforces regional public-private collaboration, and FPT-Udemy training illustrates cross-border enterprise learning synergies spanning Japan, Korea, and Vietnam.

Europe, the Middle East, and Africa show steady uptake moderated by regulatory and infrastructure diversity. The EU’s Digital Europe grants foster coordinated credential standards and fund advanced digital-skills content, while the University of Surrey’s AR/VR course portfolio illustrates an academic push toward immersive learning. In the Middle East, IHG Academy’s Arabic-language hospitality MOOC addresses local workforce needs. Sub-Saharan Africa leverages mobile-first delivery to mitigate campus capacity gaps, while South America advances through Brazil and Argentina’s ed-tech investment climates.

Competitive Landscape

The Massive Open Online Course (MOOC) market features a moderate degree of fragmentation. Coursera, Udemy, EdX, and LinkedIn Learning anchor the global tier, together holding roughly 27% of 2024 revenue. Scale provides superior AI-training data, regulatory compliance head-starts, and bargaining power with enterprise clients.

Strategic differentiation increasingly revolves around credential verification, analytics depth, and integration APIs rather than sheer course count. Hong Kong Polytechnic University’s blockchain certificates and TheBadge’s decentralized verification layer highlight new trust architectures. At the same time, universities such as the University of London partner with platforms on VR development content to deliver immersive experiences without building proprietary tech stacks[4]University of London, “Virtual Reality – 3D Models,” london.ac.uk ..

M&A accelerates as incumbents seek technical advantages and geographic reach. Accenture’s LearnVantage bet on Udacity, 2U’s strategic review, and regional acquisitions across Latin America underscore a buyer’s market for distressed yet content-rich portals. Compliance burdens tied to data privacy and accessibility rules further pressure small providers, pushing them toward niche specializations or partnership networks.

Massive Open Online Course (MOOC) Industry Leaders

Coursera Inc.

edX Inc. (2U)

Udacity Inc. (Accenture)

Udemy Inc.

Canvas Networks Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: University of Central Florida launched a 10-week XR Development course with Circuit Stream, including live sessions and premium community access.

- March 2024: IHG Academy partnered with Queen Rania Foundation and Edraak to launch an Arabic-language “Careers in Hospitality” MOOC for Jordanian learners.

- March 2025: University of North Texas broadened its Coursera agreement to cover 3,800 non-credit courses for all students and staff.

- January 2025: Hong Kong Polytechnic University expanded its ACVP.hk electronic certification system, issuing QR-code-enabled diplomas.

- December 2024: upGrad expanded university alliances to reach 10 million learners across 100 countries.

Global Massive Open Online Course (MOOC) Market Report Scope

A massive open online course (MOOC) is a web-based distance learning program designed for the participation of large numbers of geographically dispersed students. Courses related to subjects such as technology, business, and science are considered under the report's scope. Technology includes computer science, IT, data analytics, and statistics; the business comprises finance, marketing, entrepreneurship, leadership, and strategy. The science segment includes electronics, physics, chemistry, life sciences, and engineering. Apart from the mentioned segments, the rest are covered under other subject types.

The massive open online course (MOOC) market is segmented by type (cMOOC and XMOOC), subject type (technology, business, science, and other subject types), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

By Platform Type

| cMOOC |

| xMOOC |

| Hybrid / SPOC |

By Subject Area

| Technology and Computer Science |

| Business and Management |

| Science and Engineering |

| Arts and Humanities |

| Language Learning |

By End User

| Higher-Education Students |

| K-12 Learners |

| Working Professionals / Corporate |

| Lifelong Learners |

By Revenue Model

| Free (Audit-only) |

| Freemium |

| Subscription (B2C) |

| Pay-per-course / Certificate |

| Enterprise Licensing (B2B) |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Platform Type | cMOOC | ||

| xMOOC | |||

| Hybrid / SPOC | |||

| By Subject Area | Technology and Computer Science | ||

| Business and Management | |||

| Science and Engineering | |||

| Arts and Humanities | |||

| Language Learning | |||

| By End User | Higher-Education Students | ||

| K-12 Learners | |||

| Working Professionals / Corporate | |||

| Lifelong Learners | |||

| By Revenue Model | Free (Audit-only) | ||

| Freemium | |||

| Subscription (B2C) | |||

| Pay-per-course / Certificate | |||

| Enterprise Licensing (B2B) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the projected value of the Massive Open Online Course market by 2031?

The market is forecast to reach USD 209.13 billion by 2031, growing at a 36.92% CAGR.

Which platform type is expanding fastest?

Hybrid/SPOC models are expected to post a 40.11% CAGR between 2026 and 2031 thanks to structured cohort formats.

Why are subscription models gaining traction?

Enterprises favor all-inclusive subscriptions that bundle analytics and credential support, driving a 37.92% CAGR for this revenue model.

Which region will grow the quickest through 2031?

Asia-Pacific will advance at a 37.25% CAGR owing to widescale government digitization and AI-skills demand.

How are employers validating MOOC credentials?

Blockchain-based verification, such as Hong Kong Polytechnic University’s ACVP.hk platform, enables instant tamper-proof certificate checks.

Page last updated on: