Legal Process Outsourcing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

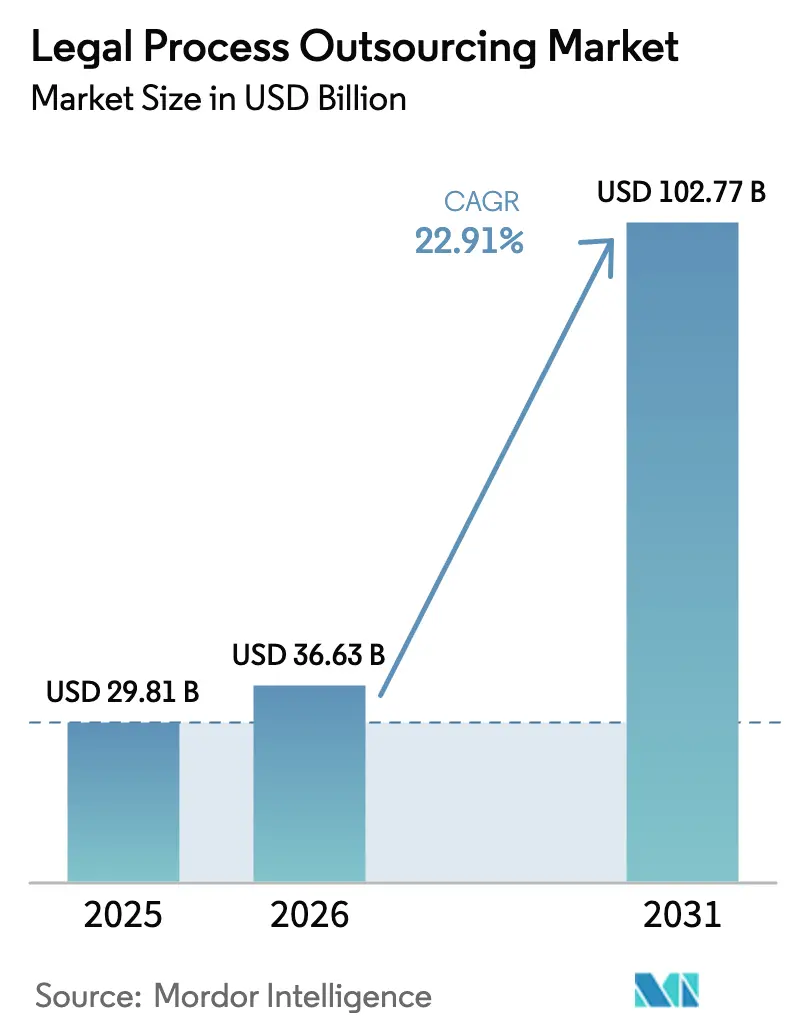

| Market Size (2026) | USD 36.63 Billion |

| Market Size (2031) | USD 102.77 Billion |

| Growth Rate (2026 - 2031) | 22.91% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Legal Process Outsourcing Market Analysis by Mordor Intelligence

Legal process outsourcing market size in 2026 is estimated at USD 36.63 billion, growing from 2025 value of USD 29.81 billion with 2031 projections showing USD 102.77 billion, growing at 22.91% CAGR over 2026-2031. Strong demand arises as 43% of chief legal officers intend to send more work outside their organizations in 2025, 17 percentage points above 2024 levels. Digital-first delivery, regulatory complexity, and AI-enabled process automation collectively push buyers toward external experts, while service providers re-engineer offerings around technology and flexible pricing. North America still dominates revenue, but Asia-Pacific’s faster scaling base, supportive policy frameworks, and cost benefits reshape global supply lines. Within services, e-discovery keeps the largest slice, yet its AI-enabled variant grows the quickest, confirming that automation eclipses manual review. Growth differentials among enterprise sizes, delivery models, and geographic clusters underline a market in transition rather than one driven purely by cost savings.

Key Report Takeaways

- By service, e-discovery led with 27.12% of the Legal process outsourcing market share in 2025; AI-enabled e-discovery is advancing at a 27.24% CAGR through 2031.

- By end-user, corporate legal departments posted the fastest 32.40% CAGR, while law firms retained a 47.90% share of the Legal process outsourcing market size in 2025.

- By enterprise size, SMEs are expanding at a 31.60% CAGR, whereas large enterprises commanded 64.05% of spending in 2025.

- By delivery model, third-party vendors held 69.60% of the Legal process outsourcing market share in 2025; captive centers, however, are rising at a 24.98% CAGR.

- By geography, North America recorded a 41.10% revenue share in 2025; Asia-Pacific is forecast to climb at a 29.10% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Legal Process Outsourcing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Focus on core competencies | +4.2% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Cost-reduction pressures | +5.8% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Integration of AI and automation | +6.1% | North America and Europe leading, rapid Asia-Pacific use | Long term (≥ 4 years) |

| Expanding e-discovery data volumes | +3.4% | North America and Europe primary, Asia-Pacific rising | Medium term (2-4 years) |

| Post-pandemic virtual litigation support | +2.7% | Global, advanced markets lead | Short term (≤ 2 years) |

| ESG-driven contract outsourcing | +1.3% | Europe and North America, emerging Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Integration of AI and automation into legal workflows

Generative AI adoption is quickening 82% of UK lawyers either use or plan to deploy the technology. Large law firms already run AI research tools that cut analysis time by up to 50%. Providers showcasing platforms such as Epiq’s AI Discovery Assistant, which automates 80% of classic review tasks, win new mandates.[1]“Epiq Launches AI Discovery Assistant,” Epiq Global, epiqglobal.com Buyers now value technological maturity above rate cards, realigning competitive dynamics toward data science capabilities and away from headcount-led scale.

Cost-reduction pressures among legal departments and law firms

Even as 61% of general counsels anticipate larger overall budgets for 2025, most aim to optimize spending through outcome-based external engagements.[2]Ashish Walia, “Legal Department Budget Trends 2025,” Lawtrades, lawtrades.com Litigation outlays grow amid regulatory scrutiny, encouraging selective outsourcing of specialist work. AI can shave 20% off routine labor, forcing traditional firms to revisit billable-hour models and partner with alternative legal service providers.

Focus on core competencies

Three-quarters of legal teams are revisiting sourcing mixes so that in-house lawyers devote time to strategic risk and stakeholder matters while providers take repetitive tasks. Contract lifecycle platforms now underpin this shift, letting in-house units emphasize negotiation and compliance oversight rather than document management. Demand therefore rises for niche suppliers in areas like cross-border regulation and intellectual property.

Expanding e-discovery data volumes

Remote work and cloud adoption multiplied data sources, and advanced review engines can scan 500,000 documents per hour, a throughput internal teams rarely match. Varied privacy rules across jurisdictions further complicate evidence handling, pushing organizations toward specialist outsourcing partners with global data-sovereignty know-how.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data security and confidentiality concerns | −2.8% | Global, sharp in regulated industries | Short term (≤ 2 years) |

| Cross-border regulatory and data-sovereignty gaps | −1.9% | Global, intensity varies by jurisdiction | Medium term (2-4 years) |

| In-house AI tools reduce outsourcing need | −1.4% | North America and Europe, Asia-Pacific emerging | Long term (≥ 4 years) |

| Offshore talent wage inflation | −1.1% | India and Philippines | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data security and confidentiality concerns

GDPR-style rules raise direct liability for breaches, while the Financial Stability Board urges stronger oversight of third-party arrangements during crises.[3]“Third-Party Risk Guidance,” Financial Stability Board, fsb.org Clients therefore scrutinize encryption, audit trails, and data-center certifications. Elevated compliance costs can even erode the traditional labor-cost saving enjoyed in offshore deals.

Cross-border regulatory and data-sovereignty barriers

Separate localization rules in the EU, HIPAA mandates in the US, and a rise in digital-nationalism policies amplify legal complexity. Counsel must track conflicting privilege and privacy duties when files move across borders, occasionally limiting the scope of work suitable for remote jurisdictions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

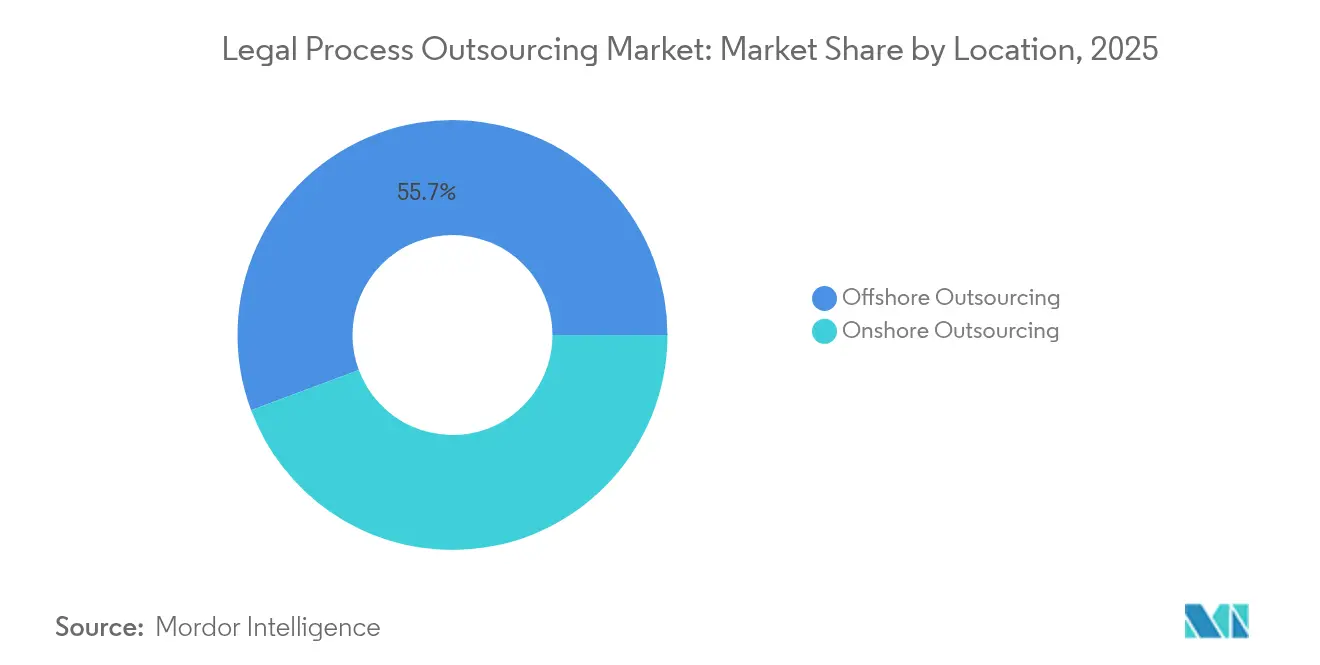

By Location: Offshore Dominance Faces Nearshore Challenge

Offshore hubs accounted for 55.70% of the Legal process outsourcing market in 2025, buoyed by India and the Philippines’ long-standing scale advantages. At the same time, onshore and nearshore alternatives are projected to climb 25.95% CAGR to 2031 as buyers weigh time-zone alignment, data-sovereignty comfort, and rising wage costs abroad. The Legal process outsourcing market size for nearshore services is on course to outstrip early expectations should currency shifts narrow the cost gap.

Talent scarcity and salary inflation in legacy offshore venues encourage diversification toward Mexico, Colombia, and Brazil, all offering cultural proximity to US clients. Governments in those countries tout IP-protection reforms that mirror US standards, improving buyer confidence. While offshore teams still deliver process scale, providers increasingly add local-country “front offices” for high-sensitivity matters.

By Service: AI-Enabled E-discovery Disrupts Traditional Models

Classic e-discovery retained 27.12% of the Legal process outsourcing market share in 2025, but AI-enabled e-discovery is forecast to expand at a 27.24% CAGR. That shift stems from machine-learning engines achieving 75-90% predictive accuracy, slashing manual review hours and reducing error rates. The Legal process outsourcing market size tied to AI-based review is rising in tandem with global litigation data volumes.

Contract drafting, patent support, and compliance work benefit from similar automation. Providers embed generative tools such as ContractPodAi’s Leah into managed-service offerings, positioning themselves as technology partners rather than labor substitutes. Growth opportunities also emerge in contract lifecycle management as ESG clauses, cyber-risk terms, and AI-governance language proliferate within corporate agreements.

By End-user Enterprise Size: SMEs Drive Aggressive Adoption

SMEs are set to post a 31.60% CAGR between 2026 and 2031, outpacing their larger counterparts even though enterprises above the 1,000-employee mark still represent 64.05% of 2025 spending. Flexible subscription models, cloud delivery, and lower minimum spend thresholds let smaller firms tap sophisticated advisory, leveling competitive disparities.

Large organizations meanwhile pivot to hybrid delivery—retaining strategic counsel in-house while outsourcing workflows like global e-billing or mass contract review. AI tools delivered through multi-tenant platforms distribute costs, supporting wide SME uptake without compromising functionality.

By End-user: Corporate Legal Departments Accelerate Outsourcing

Corporate legal departments, growing at 32.40% CAGR, now prioritize outsourcing for cybersecurity, privacy, and ESG matters that require niche know-how. Their adoption pace eclipses that of law firms, which still held a 47.90% revenue share in 2025 due to entrenched relationships and litigation volumes. The Legal process outsourcing market sees corporates driving multiyear managed-service deals that shift provider revenue toward predictable annuity streams.

Government uptake remains nascent; however, budget constraints and digital-first policy drives may spur future outsourcing to address backlog in e-discovery for public-records requests. Law firms themselves increasingly face capacity limits and partner with providers for overflow or technology augmentation.

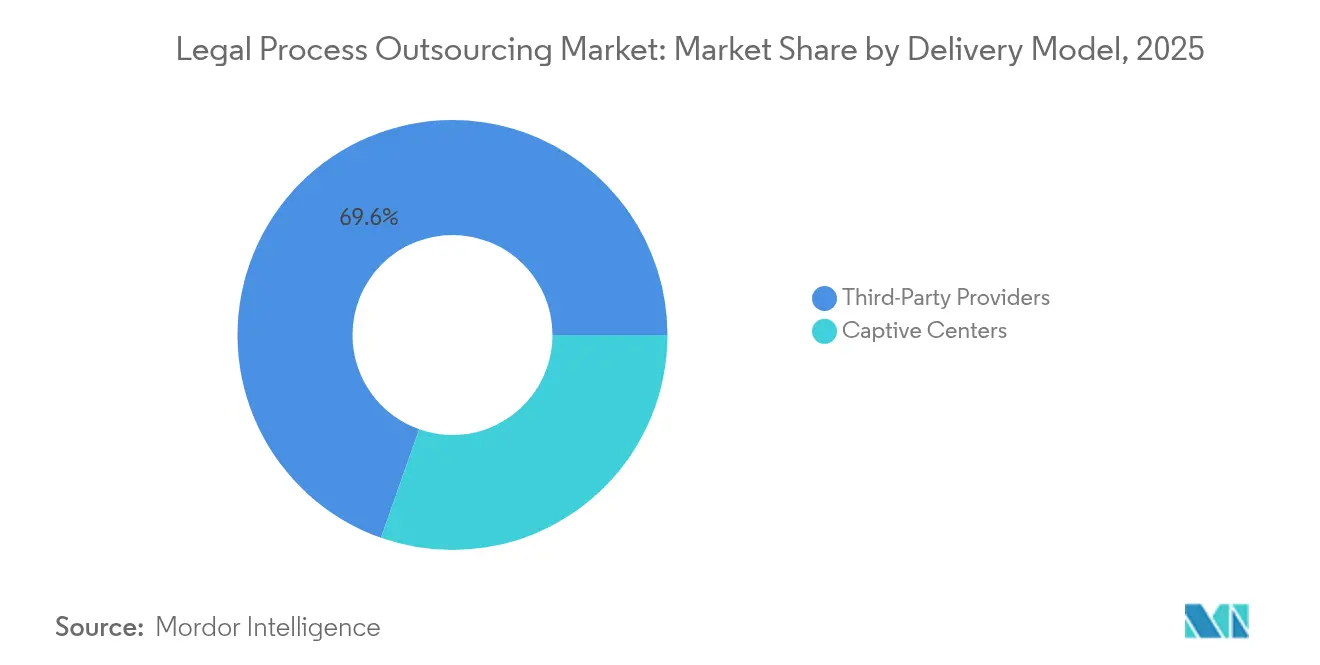

By Delivery Model: Captive Centers Challenge Third-Party Dominance

Third-party vendors retained 69.60% revenue in 2025, yet corporates and Am Law 100 firms are scaling proprietary captive centers at a 24.98% CAGR. Intellectual-property protection and process control rank among the main catalysts. Still, upfront investment and operational complexity keep the captive path viable chiefly for large entities with sustained volume.

Hybrid structures blend both models and critical workflows sit in captives, while variable or innovation-led projects continue with external specialists. Providers adjust by offering “build-operate-transfer” options, easing the switch from third-party to captive where appropriate.

By Technology Adoption: AI Revolution Transforms Service Delivery

Traditional labor-centric models made up 84.90% of 2025 revenue, but AI-enabled offerings increased at a 32.78% CAGR, marking an inflection in 2026 when many new tenders require a technology roadmap as a precondition. Consequently, the Legal process outsourcing market features widening performance gaps, providers emphasizing R&D secure higher-margin mandates, whereas slow adopters confront pricing pressure.

Intelligent document analysis, predictive analytics for litigation outcomes, and automated redlining of contracts are now baseline expectations for large buyers. Service lines combine human insight with machine speed, fostering outcome-based pricing that decouples provider earnings from the time spent on hourly effort.

Geography Analysis

North America captured 41.10% of 2025 revenue thanks to a sophisticated buyer base, but its growth is moderating as procurement priorities migrate toward value-added advisory services over pure labor arbitrage. The United States generates the bulk of spend given its complex regulatory environment, while Canada leverages common-law congruence and bilingual talent. Mexico’s ascent as a nearshore node provides cost-efficient Spanish-plus-English support, helping some US corporates rebalance offshore exposure. Notably, 43% of chief legal officers in the region plan to increase outsourced volumes in 2025.

Asia-Pacific is the fastest-growing theatre, set to advance at a 29.10% CAGR. India and the Philippines remain cornerstones, yet favorable regulatory reforms, including 100% foreign ownership allowances in select public services, entice additional law-firm investment. China delivers AI engineering capabilities, while Australia and New Zealand act as regional hubs for complex English-language matters. Rising wages and talent shortages may temper cost advantages but reinforce the need for technology-led scale.

Europe shows stable mid-single-digit growth, driven by ESG reporting rules and GDPR-level data mandates that spur demand for compliance support. The United Kingdom upholds its global legal-services status post-Brexit, leveraging deep capital-markets expertise. Germany and France draw on large manufacturing and technology client bases that require cross-border contract support. Eastern European countries provide nearshore capacity to Western Europe, though data-localization laws and divergent privilege doctrines necessitate careful engagement structures. The Middle East and Africa, while smaller, present fresh opportunities as Gulf states diversify economies through megaprojects needing robust contract management.

Competitive Landscape

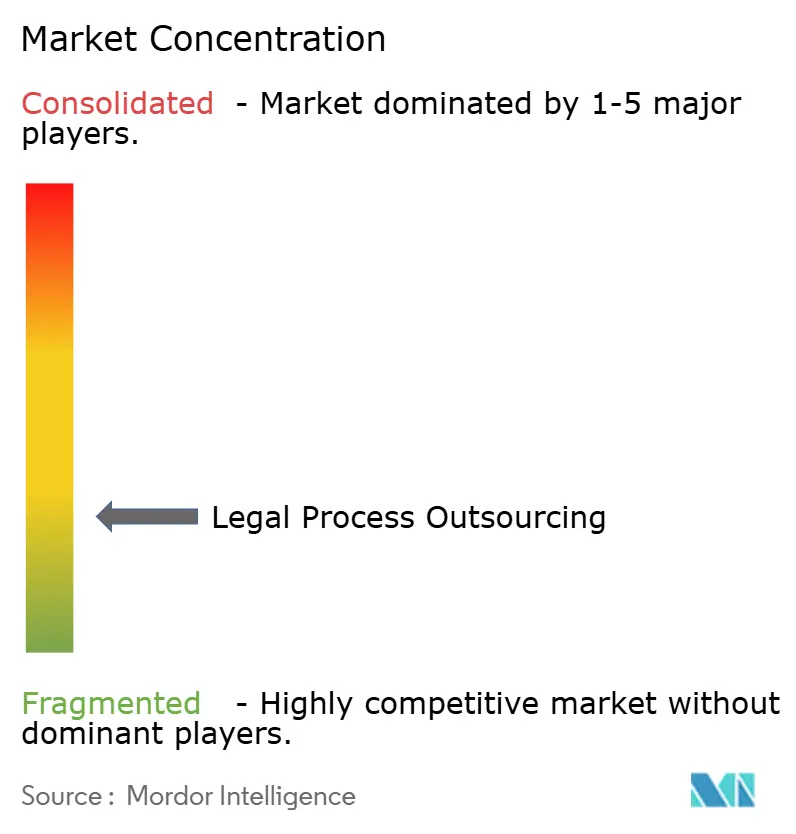

The Legal process outsourcing market remains moderately fragmented, with top third-party players accounting for roughly 30% of total revenue, while the remainder splits across mid-tier specialists and emerging AI-first entrants. Providers such as Epiq deploy proprietary AI Discovery Assistant modules that automate up to 80% of document review. Professional-services brands form alliances, PwC partnered with Integreon to bolster its AI-powered ALSP portfolio.

Captive units inside 35% of Am Law 100 firms blur competitive lines, turning erstwhile buyers into rivals. UnitedLex and Integreon illustrate the scale tier, generating USD 300 million and USD 750 million annually, respectively. Technology-centric disruptors pursue cloud-native architectures and usage-based fees, appealing to SMEs. MandA activity remains lively as investors bet on AI capabilities and global footprints. Specialized whitespace persists in ESG compliance, cyberlaw, and AI governance, where regulatory novelty outpaces incumbent service catalogs.

Legal Process Outsourcing Industry Leaders

Integreon Managed Solutions, Inc.

Elevate Services, Inc.

QuisLex, Inc.

Epiq Global, Inc.

Axiom Law Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: RELX posted 2024 revenue of GBP 9,434 million (USD 11,780 million), with 83% derived from electronic formats.

- November 2024: Thomson Reuters reported an 8% year-on-year rise in its Legal Professionals segment to USD 745 million revenue.

- August 2024: Morae Global and ContractPodAi integrated the Leah generative-AI engine into managed contract solutions.

- March 2024: CS Disco logged USD 36.7 million Q1 2025 revenue and launched new AI features in its legal-automation suite.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the legal process outsourcing (LPO) market as the spend generated when law firms or corporate legal departments contract external providers to perform legal support activities such as e-discovery, contract drafting and review, litigation support, patent services, compliance management, due diligence, and legal research, whether these tasks are delivered from offshore, near-shore, or on-shore centers. The valuation tracks fee-based revenues earned by third-party or captive providers and is expressed in nominal US dollars for the calendar year.

Scope Exclusions: Internal legal spend retained in-house, stand-alone legal technology licensing, and wider knowledge-process outsourcing tasks that fall outside legal work are not counted in our market size.

Segmentation Overview

- By Location

- Offshore Outsourcing

- Onshore Outsourcing

- By Service

- Contract Drafting

- Review and Contract Management

- e-Discovery

- Litigation Support

- Patent Support

- Compliance Management

- Due Diligence and Legal Research

- Other Services

- By Enterprise Size

- SMEs

- Large Enterprises

- By End-user

- Law Firms

- Corporate Legal Departments

- Government and Public Sector

- Other End-user

- By Delivery Model

- Captive Centers

- Third-Party Providers

- By Technology Adoption

- AI-Enabled Services

- Traditional Services

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Southeast Asia

- Rest of Asia Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted structured interviews and short surveys with managing partners at law firms, corporate counsels in BFSI, technology, and healthcare verticals, plus executives at offshore LPO centers across India, the Philippines, South Africa, and Latin America. The conversations confirmed current pricing bands, utilization rates, AI adoption levels, and regional capacity constraints, allowing us to reconcile desk findings and refine key assumptions.

Desk Research

We began by mapping the addressable demand using publicly available statistics such as United States Bureau of Labor Statistics employment files, Indian Ministry of Commerce service-export tables, U.K. Office for National Statistics professional-service turnover series, and filings compiled by bar associations across major jurisdictions. Complementary insights were drawn from peer-reviewed journals, country-level judiciary annual reports, and reputable trade publications that track e-discovery volumes. Where company-level intelligence or press coverage was required, analysts accessed Dow Jones Factiva and D&B Hoovers to verify provider revenues and client footprints.

These sources illustrate hiring cycles, offshore wage differentials, case filings, and cross-border service receipts that together ground the demand pool. The lists above are illustrative; many additional data points were assessed to corroborate trends and sanity-check anomalies.

Market-Sizing & Forecasting

A blended top-down and bottom-up model underpins the numbers. First, we reconstruct global legal services expenditure and apply penetration ratios for each LPO service line, adjusting for outsourcing propensity by region and enterprise size. These outputs are then cross-checked against sampled supplier roll-ups (average selling price × estimated volumes) and channel checks with sourcing advisors, which help flag under- or over-counts. Variables such as hourly offshore wage gaps, litigation case filings, cross-border service exports, AI tool adoption, and regulatory data-protection pressures feed our multivariate regression forecast. Scenario analysis captures shifts in legal tech automation and exchange-rate moves, while data gaps in provider disclosures are bridged through conservative interpolation anchored to verified trend proxies.

Data Validation & Update Cycle

Before sign-off, every model passes a senior analyst review that reruns variance, growth-rate, and currency checks. We refresh the dataset annually, and we trigger interim revisions if material events, such as major regulation, large mergers, or currency shocks, alter our baseline. A final pre-publication sweep ensures clients receive the most current view.

Why Mordor's Legal Process Outsourcing Baseline Earns Trust

Published estimates often differ because firms choose distinct service baskets, geographic spans, and forecast cadences. By stating exactly which revenue streams we include and by refreshing our inputs each year, we offer buyers a figure that mirrors real spend rather than theoretical potential.

Key gap drivers versus other publishers involve: (a) some count adjacent ALSP or KPO activities that inflate totals, (b) others limit coverage to offshore delivery or extrapolate growth from small historical samples, and (c) several roll forward historical CAGRs without stress-testing wage inflation or technology substitution. Our approach, grounded in validated demand drivers and provider-side checks, avoids these pitfalls.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 29.81 B (2025) | Mordor Intelligence | - |

| USD 22.16 B (2025) | Regional Consultancy A | Narrower service scope and limited country set cause lower base |

| USD 38.32 B (2025) | Global Analytics B | Includes broader KPO and legal tech revenues and relies on macro ratios without supplier cross-checks |

In short, the disciplined scope definition, transparent variable selection, and yearly refresh cycle mean users can rely on Mordor's numbers as a balanced, defensible baseline for strategic and budgeting decisions.

Key Questions Answered in the Report

What is the current value of the legal process outsourcing market?

The Legal process outsourcing market size is USD 36.63 billion in 2026.

How fast is the market expected to grow?

It is projected to register a 22.91% CAGR and reach USD 102.77 billion by 2031.

Which region will record the highest growth?

Asia-Pacific is forecast to progress at a 29.10% CAGR, making it the prime growth engine through 2031.

Why are AI-enabled services gaining traction in legal outsourcing?

Generative AI reduces document-review time by up to 80% and improves accuracy, prompting buyers to favor technology-rich providers.

Which service segment accounts for the largest revenue share?

Traditional e-discovery held 27.12% of 2025 revenue, though AI-enabled e-discovery is the fastest-expanding niche.

Page last updated on: