Knowledge Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

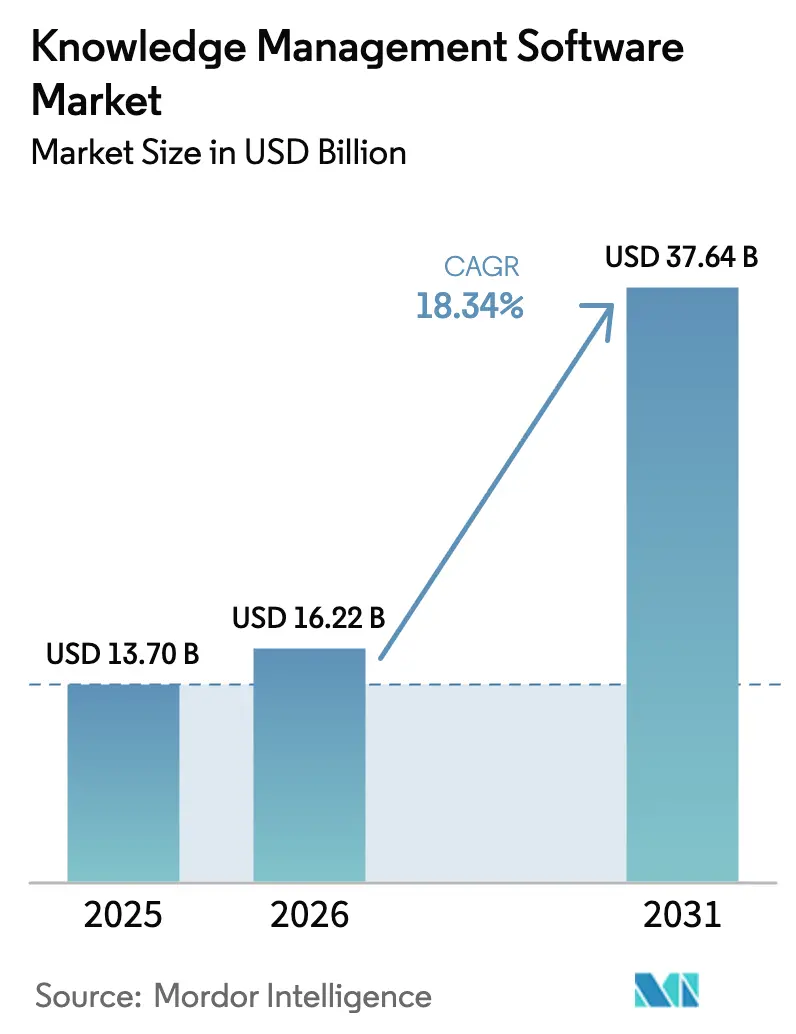

| Market Size (2026) | USD 16.22 Billion |

| Market Size (2031) | USD 37.64 Billion |

| Growth Rate (2026 - 2031) | 18.34% CAGR |

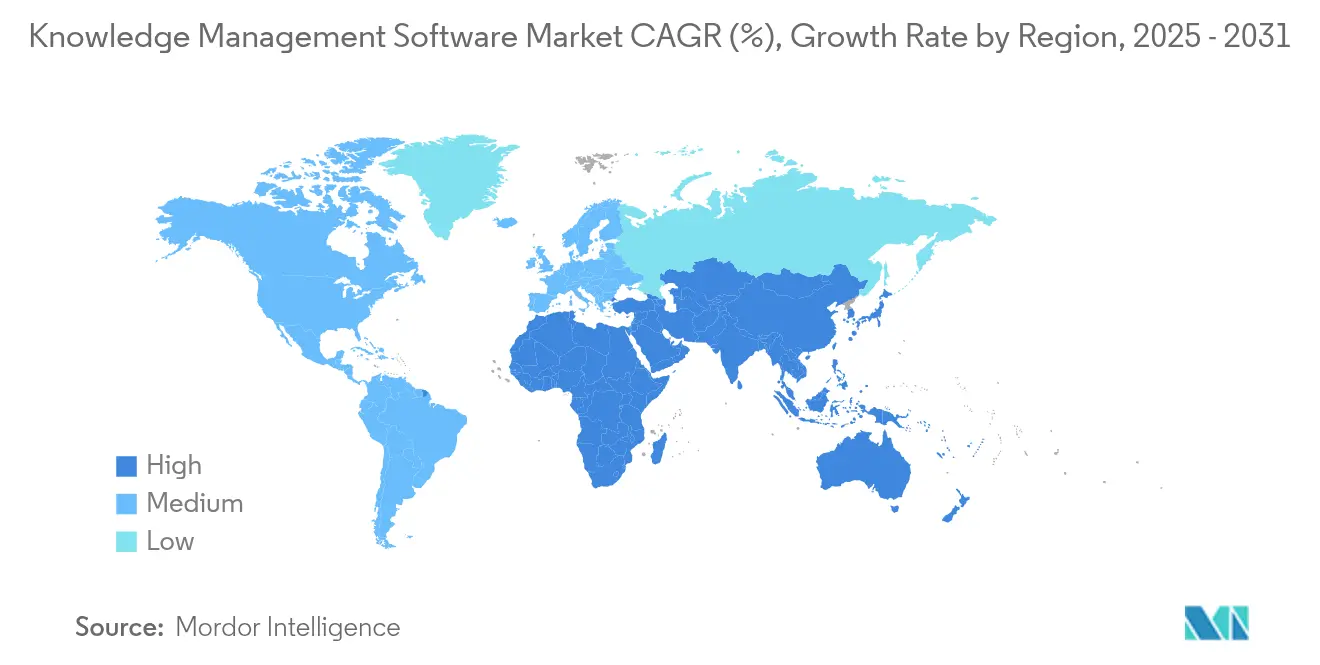

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Knowledge Management Software Market Analysis by Mordor Intelligence

The knowledge management software market size is expected to grow from USD 13.70 billion in 2025 to USD 16.22 billion in 2026 and is forecast to reach USD 37.64 billion by 2031 at 18.34% CAGR over 2026-2031. This expansion reflects enterprises’ urgency to organize corporate know-how as a differentiator while embedding generative-AI tools that capture, process, and activate intellectual assets at scale. Rapid cloud adoption, continuous AI investment by large vendors, and rising regulatory pressures on data governance are reinforcing demand. At the same time, a fragmented provider landscape and persistent security concerns temper growth, compelling vendors to fuse knowledge suites with identity management, governance, and low-code workflow tools. Rising SME participation, Asia-Pacific’s digital acceleration, and industry-specific knowledge graphs together expand the total addressable opportunity for the knowledge management software market.

Key Report Takeaways

- By deployment, the cloud segment dominated with 62.18% of knowledge management software market share in 2025 and is forecast to grow at a 19.68% CAGR to 2031.

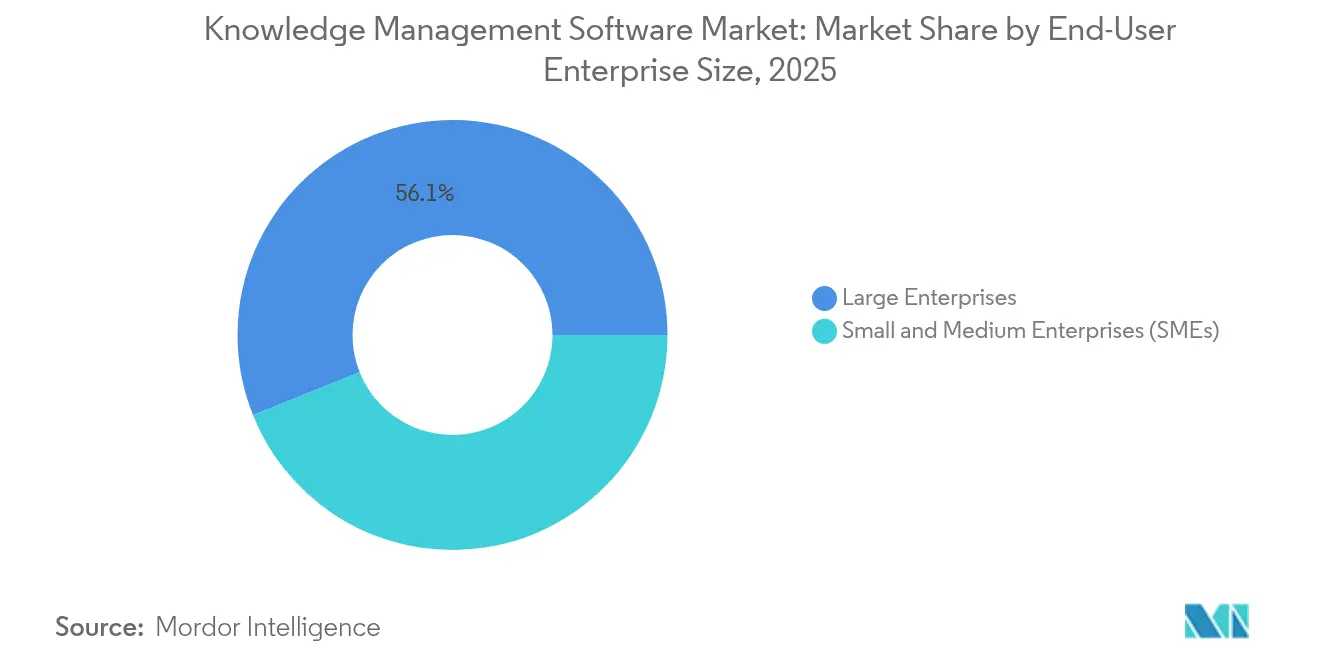

- By organization size, large enterprises led with 56.08% share of the knowledge management software market size in 2025, while SMEs record the highest projected CAGR at 19.02% through 2031.

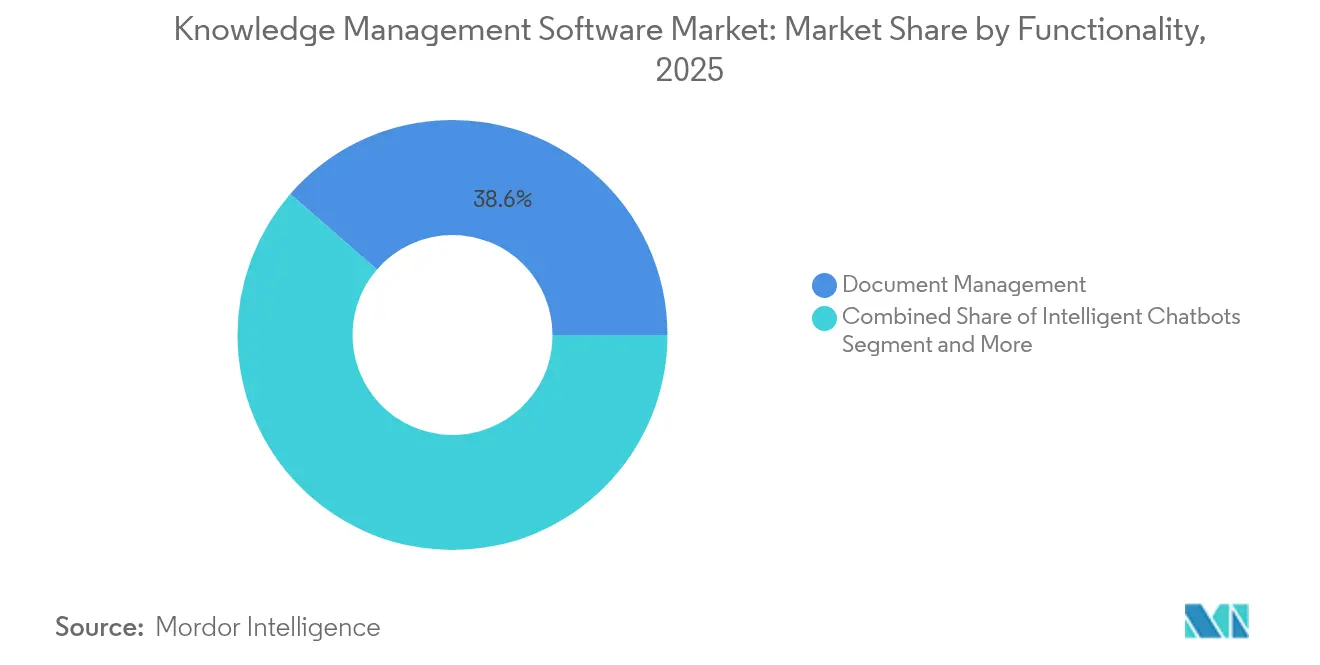

- By functionality, document management accounted for 38.61% of the knowledge management software market share in 2025, whereas intelligent chatbots and virtual agents exhibit the fastest growth at 21.88% CAGR to 2031.

- By end-user industry, IT and telecom captured 23.87% revenue share in 2025; healthcare is set to expand at a 20.74% CAGR to 2031.

- By geography, North America held 38.08% of the knowledge management software market share in 2025, yet Asia-Pacific is advancing at a 22.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Knowledge Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising investment in AI and automation | +4.2% | Global, Asia-Pacific leadership | Medium term (2-4 years) |

| Growing importance of data and knowledge sharing | +3.8% | North America and Europe | Long term (≥ 4 years) |

| Expansion of remote/hybrid work models | +3.1% | Developed markets | Short term (≤ 2 years) |

| Rapid adoption of cloud-native KM suites | +2.9% | Global enterprise focus | Medium term (2-4 years) |

| Generative-AI knowledge automation wave | +2.7% | Asia-Pacific core, spill-over to North America | Short term (≤ 2 years) |

| Vertical-specific knowledge graph monetization | +1.3% | North America and EU | Long term (≥ 4 years) |

| Rising investment in AI and automation | +4.2% | Global, Asia-Pacific leadership | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising investment in AI and automation

IBM’s generative-AI revenue reached USD 6 billion in Q1 2025, and its software segment advanced 9% year-over-year, underscoring the link between AI spending and robust knowledge systems that underpin model training and deployment. Microsoft added USD 8.5 billion of productivity-and-business-processes revenue in FY24 Q4 as AI-enabled Office 365 features boosted adoption, demonstrating how enriched knowledge repositories accelerate upsell potential.[1]Microsoft Investor Relations, “FY24 Q4 Results,” microsoft.com Cognizant earmarked USD 1 billion for generative AI and deployed 25,000 Microsoft 365 Copilot seats, signaling that consulting firms now regard enterprise knowledge assets as prerequisites for scaled AI value creation.[2]Cognizant, “Generative AI Investment Announcement,” cognizant.com Such investments strengthen the knowledge management software market by channeling budget to platforms that structure data for AI workloads.

Growing importance of data and knowledge sharing

Atlassian surpassed USD 5 billion in annualized revenue by positioning Confluence and related tools as hubs that dissolve departmental silos. Georgia-Pacific’s ‘ChatGP’ project with AWS captures retiree know-how into a central AI-driven knowledge base, illustrating how heavy-industry players institutionalize experiential insights for plant-wide reuse. These examples show that organizations gain speed and innovation agility when institutional knowledge flows freely, bolstering the knowledge management software market.

Expansion of remote/hybrid work models

TCS consolidated 500+ repositories into its Adaptive Knowledge Bank, improving customer experience by 15% and cutting support handling time 40% after applying natural-language search. ServiceNow’s integration of Now Assist with Microsoft 365 lets distributed employees retrieve policies and file tickets via conversational prompts, addressing collaboration gaps inherent in hybrid workplaces.[3]ServiceNow Newsroom, “ServiceNow to Acquire data.world,” servicenow.com As knowledge workers become more dispersed, firms require unified yet context-aware knowledge access, further scaling the knowledge management software market.

Rapid adoption of cloud-native KM suites

SAP grew Q1 2025 cloud revenue 27% to EUR 4.993 billion (USD 5.4 billion) and launched Business Data Cloud, embedding knowledge graphs that feed AI agents with cross-domain context. OpenText’s FY2024 cloud revenue rose to USD 1.8 billion, reflecting the shift of traditional content-management workloads into subscription-based, AI-ready stacks. Cloud models supply elastic compute that AI-centric knowledge mining demands, reinforcing the knowledge management software market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial cost and implementation complexity | −2.1% | Global, SME focus | Short term (≤ 2 years) |

| Data-security and privacy concerns | −1.8% | EU and North America | Medium term (2-4 years) |

| End-user trust deficit in AI-generated knowledge | −1.4% | Industry-dependent | Medium term (2-4 years) |

| Shortage of knowledge-engineering talent | −1.2% | Developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High initial cost and implementation complexity

Comprehensive roll-outs entail data migration, taxonomy design, and user training that often span 6–12 months. Although cloud subscriptions lower capex, organizations still face integration with ERP, CRM, and identity platforms, raising change-management overhead. Vendors are mitigating the barrier through pre-built connectors and low-code setup wizards, yet the constraint temporarily slows the knowledge management software market’s penetration among resource-pressed SMEs.

Data-security and privacy concerns

Enterprises deploying large language models inside knowledge systems demand granular permissions, audit trails, and region-specific data residency. Microsoft Copilot pilots exposed over-permissioned content access, prompting enterprises to implement continuous monitoring before full rollout. Regulations such as GDPR and CCPA compel providers to deliver fine-grained retention and anonymization features. These safeguards increase total cost of ownership and elongate procurement cycles, restraining short-term adoption while pushing the knowledge management software market toward secure-by-design architectures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Functionality: Document Management Dominance Faces AI Disruption

Document management retained 38.61% of knowledge management software market share in 2025, affirming that organized repositories remain foundational to digital work. However, the segment’s growth is overshadowed by intelligent chatbots and virtual agents rising at 21.88% CAGR to 2031. Organizations blend traditional libraries with conversational front-ends so users can retrieve contextually relevant excerpts rather than sift through folders.

Knowledge discovery and search modules connect static documents to AI engines that parse unstructured text via machine learning, while analytics dashboards surface usage gaps, guiding content curation. LG CNS, for instance, cut retrieval time by more than 50% after integrating Elastic search into its KeyLook platform, raising search relevance 95%. As generative models rewrite or summarize content on demand, formerly siloed document archives transform into interactive knowledge assets, sustaining momentum within the knowledge management software market.

By Deployment: Cloud Transformation Accelerates Enterprise Adoption

Cloud deployment captured 62.18% of knowledge management software market share in 2025 and is set for 19.68% CAGR through 2031. Hyperscalers equip tenants with auto-scaling GPUs and pre-integrated AI APIs, enabling knowledge extraction, summarization, and semantic search without on-premise hardware. ServiceNow’s 2025 purchase of data.world embeds lineage-rich data catalogs into its SaaS workflow fabric, positioning its cloud stack as the default knowledge backbone for cross-department use cases.

On-premise deployments persist in defense, healthcare, and finance owing to sovereignty mandates, yet even these sectors pilot hybrid topologies that route non-sensitive analytics to public cloud. Subscription pricing further entices SMEs, democratizing enterprise-grade capability and expanding knowledge management software market size among first-time buyers. The convergence of workload portability, continuous feature delivery, and AI accelerators cements cloud as the dominant delivery model.

By End-User Enterprise Size: SME Growth Challenges Enterprise Incumbency

Large organizations controlled 56.08% of knowledge management software market share in 2025, reflecting decades of content-management investment. Their adoption centers on complex use cases—regulatory e-discovery, multilingual taxonomies, and integration with DevOps pipelines—that require enterprise-class governance. Atlassian now counts more than 500 customers spending USD 1 million or more annually on its collaboration stack, illustrating sustained enterprise appetite.

SMEs, however, are accelerating at a 19.02% CAGR, drawn by plug-and-play SaaS suites bundled with workflow and generative write-assist tools. With limited IT staff, these firms prioritize rapid onboarding and ROI, turning to templated knowledge wikis that extend existing productivity suites. The resulting influx of net-new accounts invigorates overall knowledge management software market growth while pressuring vendors to streamline UX and support multi-tier pricing.

By End-user Industry: Healthcare Acceleration Outpaces IT Leadership

IT and telecom retained a 23.87% revenue share in 2025 as early digital adopters enhanced developer-support portals and incident-response playbooks. Yet healthcare climbs at a 20.74% CAGR because clinical decision support, patient-safety mandates, and electronic health record interoperability hinge on real-time, evidence-based knowledge delivery. Hospitals deploy AI-tagged repositories that surface treatment protocols and research summaries at the bedside, directly shaping patient outcomes.

BFSI firms integrate knowledge hubs with risk-modelling engines, while manufacturers digitize legacy standard-operating procedures to counter retiring-workforce brain drain. Retailers embed knowledge bases into chatbots for omnichannel customer service. Each vertical imposes domain-specific taxonomies and compliance filters, spurring vendors to launch pre-configured industry packs and driving segmentation within the broader knowledge management software market.

Geography Analysis

North America accounted for 38.08% of knowledge management software market share in 2025. The region’s technology incumbents both supply and consume advanced suites, reinforcing a virtuous cycle of product enhancement. Microsoft’s productivity portfolio alone added USD 8.5 billion year-over-year, highlighting mature yet growing demand for AI-infused knowledge services. Regulatory scrutiny around AI governance prompts providers to embed auditability and role-based controls geared to U.S. and Canadian privacy statutes, shaping product roadmaps.

Asia-Pacific advances at a 22.98% CAGR, acting as the growth engine for the knowledge management software market. National digital-transformation programs, mobile-first workforces, and aggressive AI skilling initiatives foster fertile ground. Hitachi’s multi-billion-dollar partnership with Microsoft illustrates how regional conglomerates scale generative-AI-ready knowledge platforms to support smart-city and industrial-IoT rollouts. Cloud availability zones across India, Japan, and Southeast Asia further reduce latency and improve compliance alignment, catalyzing adoption.

Europe shows steady expansion underpinned by GDPR-driven demand for metadata lineage, retention controls, and on-premise options. Enterprises invest in semantic graph layers that enforce fine-grained consent and enable multilingual search across complex corporate archives. Meanwhile, Latin America, the Middle East, and Africa emerge as green-field territories where SaaS knowledge hubs leapfrog legacy ECM investments, with public-sector e-government projects acting as anchor tenants and widening the knowledge management software market’s global footprint.

Competitive Landscape

The knowledge management software market remains moderately fragmented. Microsoft, IBM, and Atlassian integrate knowledge functions across productivity, cloud, and DevOps ecosystems, leveraging scale advantages. IBM enriches Watsonx with curated enterprise ontologies to attract AI-heavy workloads; Microsoft bundles Copilot inside Microsoft 365 to turn ordinary documents into interactive knowledge nodes.

Specialized vendors such as Bloomfire and Guru emphasize ease of use and frontline engagement, carving space in customer-experience-focused enterprises. ServiceNow fuses workflow automation with embedded knowledge graphs, and its data.world acquisition boosts metadata governance depth. Graphwise, the result of Semantic Web Company and Ontotext’s merger, tightens competition by uniting knowledge-engineering expertise with a high-performance graph database.

Strategic alliances proliferate as players vie to combine vertical expertise, AI accelerators, and low-code orchestration. Hyperscalers court consulting majors to bundle generative agents that draw on institutional content, reshaping value propositions from standalone repositories to end-to-end process platforms. The upshot is heightened innovation but also a buyer’s market where offerings converge around AI capabilities, accelerating adoption and enlarging the knowledge management software market.

Knowledge Management Software Industry Leaders

Atlassian Corporation

Microsoft Corporation

IBM Corporation

Salesforce

ServiceNow

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: ServiceNow acquired data.world to enrich its Workflow Data Fabric with cataloging and governance functions critical for scaling AI agents.

- March 2025: Adobe introduced Adobe Marketing Agent and Adobe Express Agent for Microsoft 365 Copilot to generate assets and insights directly inside productivity suites.

- January 2025: ServiceNow and Microsoft deepened their alliance, enabling employees to access ServiceNow knowledge bases through Microsoft 365 conversational interfaces.

- October 2024: Semantic Web Company and Ontotext merged to form Graphwise, combining semantic AI and graph database technologies for integrated enterprise knowledge graphs.

Global Knowledge Management Software Market Report Scope

Knowledge management software is an application tailored for organizations to efficiently capture, store, organize, share, and manage their knowledge and information resources. KMS aims to enhance decision-making, collaboration, and innovation by facilitating easy access to, sharing of, and contributing to knowledge among employees.

The study tracks the revenue accrued through the sale of knowledge management software by various players across the globe. It also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The knowledge management software market is segmented by functionality (document management, knowledge discovery, and collaboration), deployment (on-premise and cloud), and geography (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America). The market sizes and forecasts regarding value (USD) for all the above segments are provided.

| Document Management |

| Knowledge Discovery and Search |

| Collaboration / Social KM |

| Intelligent Chatbots and Virtual Agents |

| Analytics and Insight Engines |

| On-Premise |

| Cloud |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| BFSI |

| Healthcare and Life Sciences |

| IT and Telecom |

| Manufacturing |

| Retail and E-commerce |

| Government and Public Sector |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Functionality | Document Management | ||

| Knowledge Discovery and Search | |||

| Collaboration / Social KM | |||

| Intelligent Chatbots and Virtual Agents | |||

| Analytics and Insight Engines | |||

| By Deployment | On-Premise | ||

| Cloud | |||

| By End-User Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By End-user Industry | BFSI | ||

| Healthcare and Life Sciences | |||

| IT and Telecom | |||

| Manufacturing | |||

| Retail and E-commerce | |||

| Government and Public Sector | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Southeast Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the knowledge management software market?

The knowledge management software market is worth USD 16.22 billion in 2026 and is set to grow to USD 37.64 billion by 2031.

Which deployment model leads the market?

Cloud deployment commands 62.18% market share and is projected to rise at a 19.68% CAGR through 2031, reflecting enterprises’ preference for scalable, AI-ready platforms.

Which functionality segment is expanding fastest?

Intelligent chatbots and virtual agents are the fastest-growing functionality, advancing at a 21.88% CAGR as firms embed conversational AI into knowledge workflows.

Which region is expected to grow the quickest?

Asia-Pacific is forecast to register a 22.98% CAGR to 2031 due to aggressive digital-transformation programs and high AI adoption.

Why is healthcare a high-growth end-user segment?

Healthcare systems adopt knowledge platforms to meet regulatory requirements and improve patient safety, driving a 20.74% CAGR within the sector.

Page last updated on: