Australia Warehousing And Storage Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

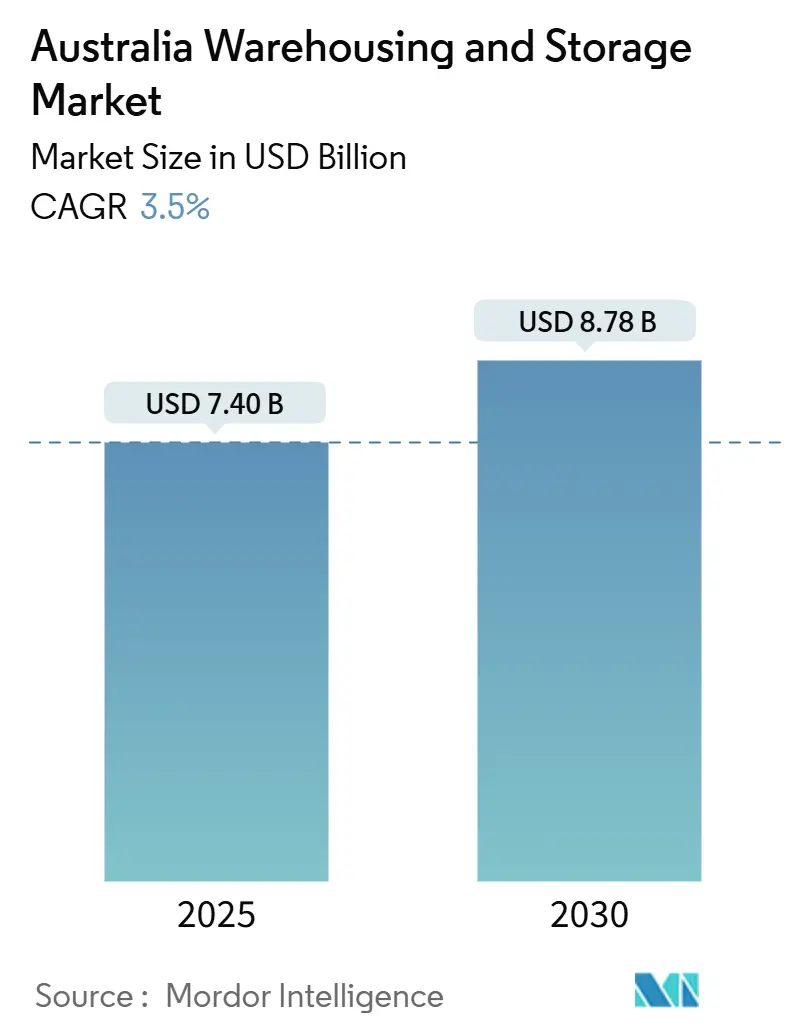

| Market Size (2025) | USD 7.40 Billion |

| Market Size (2030) | USD 8.78 Billion |

| Growth Rate (2025 - 2030) | 3.50% CAGR |

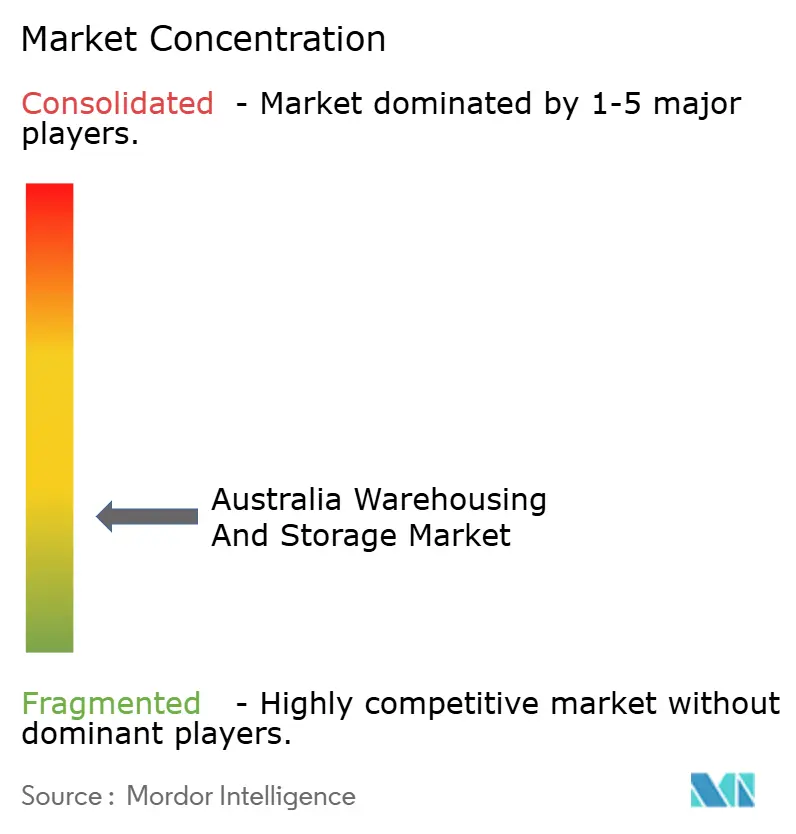

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Warehousing And Storage Market Analysis by Mordor Intelligence

The Australia Warehousing And Storage Market size is estimated at USD 7.40 billion in 2025, and is expected to reach USD 8.78 billion by 2030, at a CAGR of 3.5% during the forecast period (2025-2030).

The measured growth trajectory reflects a mature logistics landscape where e-commerce fulfillment, cold-chain expansion, and government-backed infrastructure projects fuel incremental gains while industrial land scarcity and labor shortages temper headline acceleration. Same-day delivery expectations are pulling inventory into micro-fulfillment centers inside metropolitan rings, cold-chain nodes are multiplying around ports and pharmaceutical hubs, and the Inland Rail corridor is spawning inland intermodal parks that re-route long-haul flows. Competition hinges on automation depth, with early adopters squeezing 25% productivity gains from robotics, while insurers’ climate-risk repricing pushes resilience upgrades to the top of capital budgets. Fragmentation persists, yet capitalized players able to pair prime sites with high-throughput technology capture outsize value in the Australia warehousing and storage market.

Key Report Takeaways

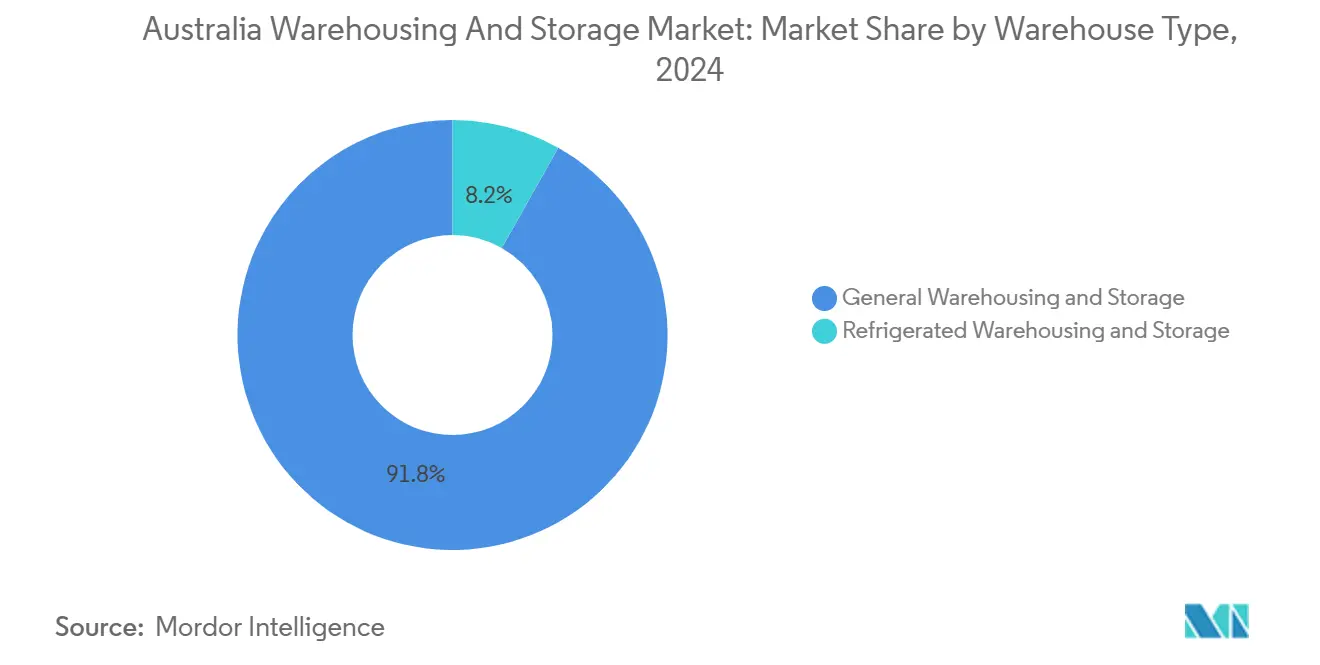

- By warehouse type, general storage led with 91.81% revenue share in 2024; refrigerated warehousing is projected to expand at a 3.73% CAGR to 2030.

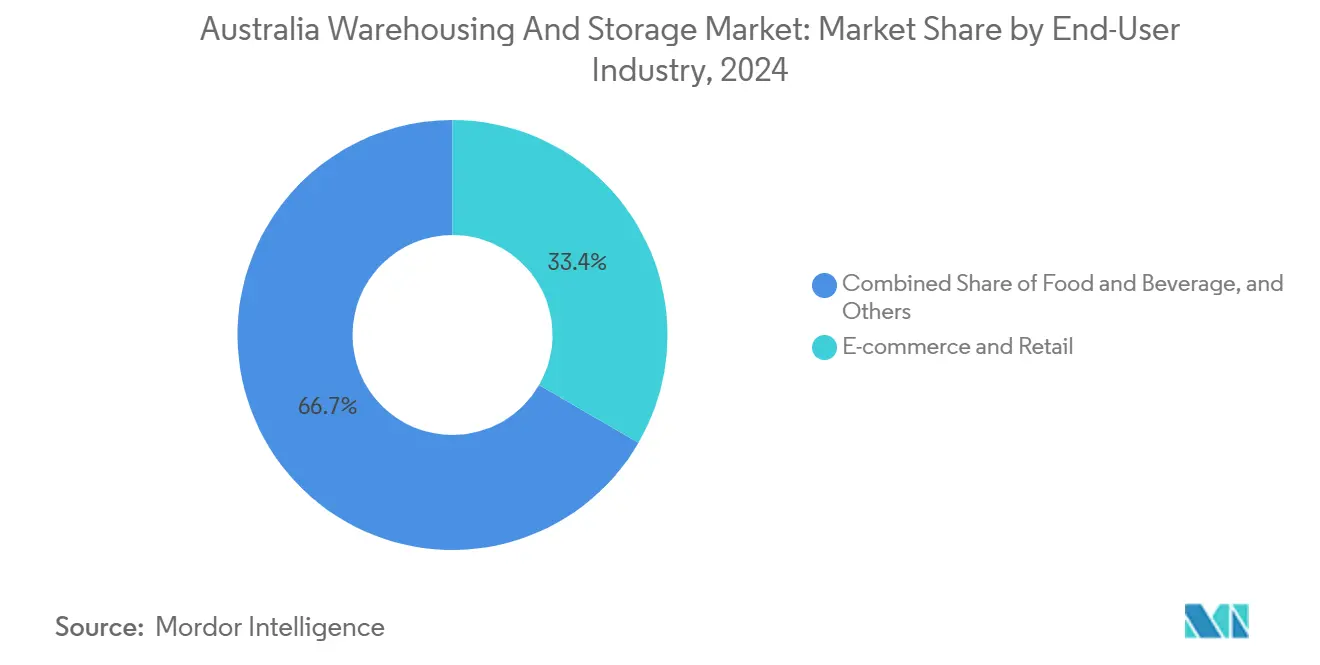

- By end-user industry, e-commerce and retail accounted for 33.35% of the Australia warehousing and storage market share in 2024, while healthcare, pharmaceuticals, and life sciences is forecast to grow at 4.63% CAGR through 2030.

Australia Warehousing And Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming e-commerce demand for last-mile fulfillment | +0.8% | Sydney, Melbourne, Brisbane metropolitan rings | Short term (≤ 2 years) |

| Growth of cold-chain logistics | +0.6% | Sydney, Melbourne, Adelaide corridors | Medium term (2-4 years) |

| Government infrastructure investments | +0.5% | Melbourne–Brisbane Inland Rail spine | Long term (≥ 4 years) |

| Warehouse automation and robotics adoption | +0.4% | Major industrial precincts nationwide | Medium term (2-4 years) |

| Mandatory stockpiling of critical medical supplies | +0.3% | National strategic hubs | Short term (≤ 2 years) |

| Expansion of defense-sector supply hubs | +0.2% | South Australia, Western Australia, New South Wales | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Booming E-commerce Demand for Last-Mile Fulfillment

Online retail spend hit AUD 69 billion (USD 46 billion) in 2024, a 12% jump that forced retailers to abandon single-node models for micro-fulfillment centers within 50 km of population clusters. Facilities ranging 5,000-15,000 m² now dominate lease inquiries, and Amazon’s six-site rollout added 200,000 m² of capacity during 2024, signaling sustained demand for urban infill warehouses. Inventory turns of 12-15× annually versus 4-6× in legacy retail distribution intensify the need for high-clearance buildings equipped for robotics, pushing premiums on power-dense sites. These shifts anchor the Australia warehousing and storage market near consumption centers rather than ports[1]“Inland Rail Project Overview,” Australian Rail Track Corporation, ARTC.COM.AU .

Growth of Cold-Chain Logistics (F&B, Pharma)

Australia maintains just 0.4 m³ of cold storage per urban resident against 0.6 m³ in the United States, leaving a structural deficit of 2.5 million m³. Pharmaceutical biologics and vaccine flows require 2-8 °C storage, commanding rents 40-60% above ambient space. NewCold’s AUD 180 million (USD 112.10 million) automated site in Melbourne with 45,000 pallet positions illustrates the capital intensity behind this expansion. Dual-certified facilities meeting FSANZ and TGA standards emerge as a preferred model, especially for exporters chasing premium Asian food markets[2]“National Robotics Strategy,” Department of Industry, Science and Resources, INDUSTRY.GOV.AU .

Government Infrastructure Investments (Ports, Inland Rail)

The AUD 15 billion (USD 9.34 billion) Inland Rail is reshaping freight economics by slashing unit costs 30-40% on corridors over 500 km. Moorebank Intermodal Terminal’s 1.7 million TEU capacity stimulated 200,000 m² of adjacent warehousing within a year, proving the pull effect of rail-port nodes. Port of Melbourne’s 8 million TEU 2030 target and National Reconstruction Fund incentives amplify industrial land demand within 20 km port radii where rents already carry 25-30% premiums.

Warehouse Automation and Robotics Adoption

National Robotics Strategy goals of 25% productivity gains push operators toward automated guided vehicles, goods-to-person systems, and AI-driven warehouse management software. Implementation costs are falling 20% per year, and Coles’ Witron center recoups its capex in 3-4 years on AUD 40,000-60,000 labor savings per full-time equivalent. Accuracy rates rising to 99.8% reduce returns and raise throughput, strengthening margins despite wage inflation.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity and cost of prime industrial land | -0.7% | Sydney, Melbourne, Brisbane cores | Short term (≤ 2 years) |

| Labour shortages and rising wages | -0.4% | Nationwide, acute in regional centers | Medium term (2-4 years) |

| ESG retrofit capital pressures | -0.3% | Older precincts nationwide | Medium term (2-4 years) |

| Rising insurance premiums | -0.2% | Bushfire- and flood-exposed zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Scarcity and Cost of Prime Industrial Land

Sydney prime sites fetch over AUD 1,000/m² and Melbourne vacancies sit at 1.1%, forcing users into outer rings that add 15-25% to last-mile costs. Developers answer with multi-story designs up to 40 m high, but build costs climb 30-40%, lengthening payback windows. Goodman Group’s 2,000 ha land bank underscores how institutional control perpetuates scarcity[3]“2024 Climate Report,” Commonwealth Bank of Australia, COMMBANK.COM.AU.

Labour Shortages and Rising Wages

The logistics sector carried 47,000 vacancies in 2024, with warehouse roles accounting for a 12% shortfall and wages running 8% ahead of national averages. Technical skill premiums widen as automation spreads, inflating payrolls for mechatronics talent and pressuring margins until efficiency gains materialize[4]“National Accounts: State Accounts,” Australian Bureau of Statistics, ABS.GOV.AU.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Warehouse Type: General Storage Holds Scale as Cold Chain Advances

General warehousing commands 91.81% of the Australia warehousing and storage market size in 2024, a reflection of broad-based distribution requirements spanning consumer electronics to machinery. Stable demand allows operators to amortize technology investments across large footprints, preserving cost leadership. Cold-chain facilities, though a smaller slice, post a 3.73% CAGR to 2030 on pharmaceutical biologics and premium food exports. Australia warehousing and storage market share in refrigerated space rises as multi-zone sites mix ambient, chilled, and frozen chambers, optimizing scarce land. Capital intensity remains high, yet rental premiums of 40-60% sustain attractive yields for investors willing to fund automated high-bay builds such as NewCold Melbourne.

Operators retrofit ambient boxes with HVAC and insulated panels, but purpose-built designs with automated shuttles deliver superior energy efficiency. Utilities sourcing renewable power win tenants facing Scope 3 emissions targets, supporting the cold-chain’s appeal. New health regulations require serialized pharma tracking, elevating compliance costs but locking in longer leases with life-science tenants. Consequently, diversified providers that balance general storage scale with refrigerated nodes hedge demand cycles in the Australia warehousing and storage market.

By End-User Industry: E-commerce Leads, Healthcare Rises

E-commerce and retail captured 33.35% share of the Australia warehousing and storage market size in 2024, propelled by double-digit online sales growth. Peak-season surges demand flexible space, leading retailers to pre-commit to speculative builds near major highways. Healthcare, pharmaceuticals, and life sciences, however, is the fastest climber at 4.63% CAGR, underpinned by sovereign stockpile mandates and on-shoring of advanced therapies. Temperature control, security, and regulatory rigour enable premium rents that outpace ambient yields.

Automotive and broader manufacturing segments maintain steady throughput, supporting specialized racking for bulky parts. Food and beverage flows increase on Asia-bound protein exports, demanding near-port cold-chain capacity. Chemicals and specialty materials remain niche, yet the hazardous-goods premiums enhance profitability for compliant operators. Overall, tenant diversification reduces cyclical risk and supports sustained absorption in the Australia warehousing and storage market.

Geography Analysis

New South Wales and Victoria account for about 60% of national capacity, anchored by Sydney’s consumption density and Melbourne’s manufacturing base. Sydney prime rents hover at record highs amid land prices topping AUD 1,000/m², while Melbourne leverages Inland Rail access to draw interstate freight into its western precincts. Queensland’s Brisbane hub grows on agricultural exports and Pacific trade, with cold-chain nodes proliferating near the Port of Brisbane.

Western Australia’s mining sector needs heavy-lift depots for spares and consumables, and Perth precincts add warehouses serving lithium battery supply chains. South Australia rides AUKUS-driven defense logistics, elevating demand for secure, access-controlled facilities. Regional terminals such as Toowoomba and Parkes gain prominence as Inland Rail brings double-stack trains inland, where land costs sit 40-50% below metropolitan averages.

Northern Territory and Tasmania, though smaller, record fastest percentage growth as Darwin and Hobart plug into Asia-centric seafood exports. The Western Sydney International Airport cargo precinct, with 75,000 m² of 24/7 warehousing, exemplifies how air-freight integration reshapes site selection. These dynamics keep absorption robust nationwide, even as the Australia warehousing and storage market grapples with supply constraints.

Competitive Landscape

The Australia warehousing and storage market remains fragmented. Domestic giants Linfox and Toll Group lead in scale, yet global entrants DHL, CEVA, DP World expand through acquisitions such as DP World’s 2024 purchase of Silk Logistics. Institutional investment hit AUD 9.8 billion (USD 6.10 billion) in 2024 industrial deals, with 52% of volumes from funds seeking stable, inflation-hedged yields.

Differentiation increasingly rests on automation density, ESG credentials, and specialized capabilities like pharma-grade cold storage. Vertical warehouses and urban micro-fulfillment sites open niches where tech-enabled startups compete on flexibility. Defense-sector secure storage, regional cold-chain gaps, and circular-economy depots for reverse logistics stand out as white-space opportunities. Consolidation is expected as smaller operators struggle with capital requirements for robotics and sustainability retrofits.

Australia Warehousing And Storage Industry Leaders

Linfox

Toll Group

Qube Holdings

DHL Group

Mainfreight

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Rohlig Logistics opened a 19,000 m² Melbourne Airport warehouse with 17,500 pallet positions and renewable energy systems.

- October 2024: Qantas pre-committed to a 24,000 m² facility at Western Sydney International Airport’s cargo precinct.

- August 2024: DP World acquired Silk Logistics for AUD 174.5 million (USD 108.67 million), expanding national warehousing coverage.

- April 2024: Mainfreight opened a 55,865 m² warehouse at Moorebank Intermodal Terminal, bringing 66,000 pallet positions online.

Australia Warehousing And Storage Market Report Scope

| General Warehousing and Storage |

| Refrigerated Warehousing and Storage |

| E-commerce and Retail |

| Food and Beverage |

| Manufacturing and Automotive |

| Healthcare, Pharmaceuticals, and Life Sciences |

| Chemicals and Specialty Materials |

| Others |

| By Warehouse Type | General Warehousing and Storage |

| Refrigerated Warehousing and Storage | |

| By End User Industry | E-commerce and Retail |

| Food and Beverage | |

| Manufacturing and Automotive | |

| Healthcare, Pharmaceuticals, and Life Sciences | |

| Chemicals and Specialty Materials | |

| Others |

Key Questions Answered in the Report

What is the current value of the Australia warehousing and storage market?

The market is valued at USD 7.40 billion in 2025.

How fast is the market expected to grow through 2030?

It is projected to advance at a 3.5% CAGR, reaching USD 8.78 billion.

Which warehouse type is expanding the quickest?

Refrigerated warehousing leads growth with a 3.73% CAGR, driven by pharma and premium food logistics.

Why are automation investments accelerating?

Robotics and AI trim labor costs by up to AUD 60,000 per FTE and raise order accuracy to 99.8%, supporting rapid payback.

How does the Inland Rail project influence warehousing demand?

It shifts long-haul freight to rail, spurring warehouses around new inland terminals along the Melbourne–Brisbane corridor.

Which end-user industry is forecast to grow fastest?

Healthcare, pharmaceuticals, and life sciences are set to expand at 4.63% CAGR owing to sovereign stockpiles and on-shoring of advanced therapies.

Page last updated on: