Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

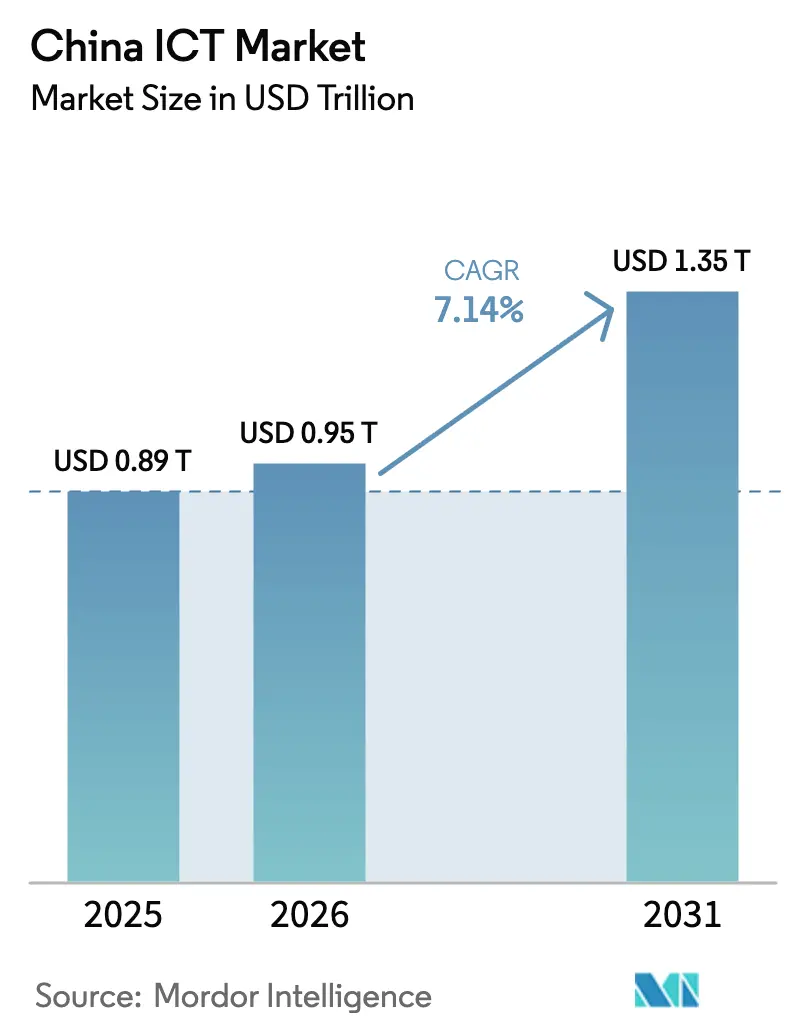

| Base Year Market Size (2025) | USD 0.89 Trillion |

| Market Size (2026) | USD 0.95 Trillion |

| Market Size (2031) | USD 1.35 Trillion |

| Growth Rate (2026 - 2031) | 7.14% CAGR |

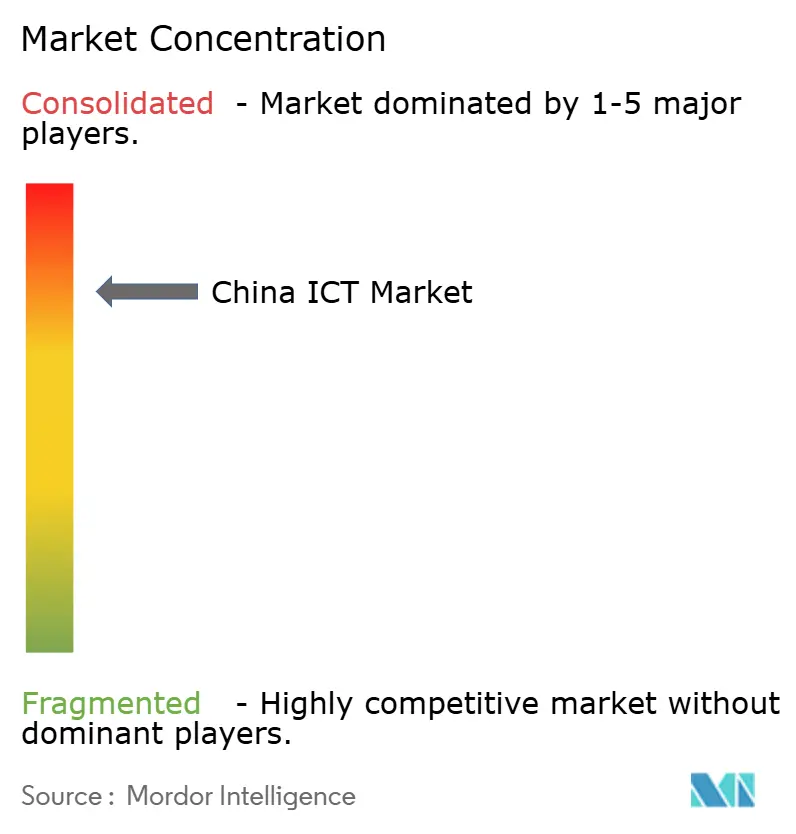

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China ICT Market Analysis by Mordor Intelligence

The China ICT Market size is expected to grow from USD 0.89 trillion in 2025 to USD 0.95 trillion in 2026 and is forecast to reach USD 1.35 trillion by 2031 at 7.14% CAGR over 2026-2031. Hardware infrastructure continues to underpin spending, yet software and platform services record the quickest gains as enterprises shift toward cloud-native operating models. Government programs under the “Digital China” banner align fiscal incentives, data-center construction, and preferential procurement to accelerate domestic technology uptake. Persistent US export controls amplify import substitution, deepening the local component ecosystem and reinforcing long-term resilience. The China ICT market also benefits from surging 5G adoption, which raises demand for edge processing and IoT solutions, while artificial intelligence integration increases per-user value across retail, manufacturing, and public services.

Key Report Takeaways

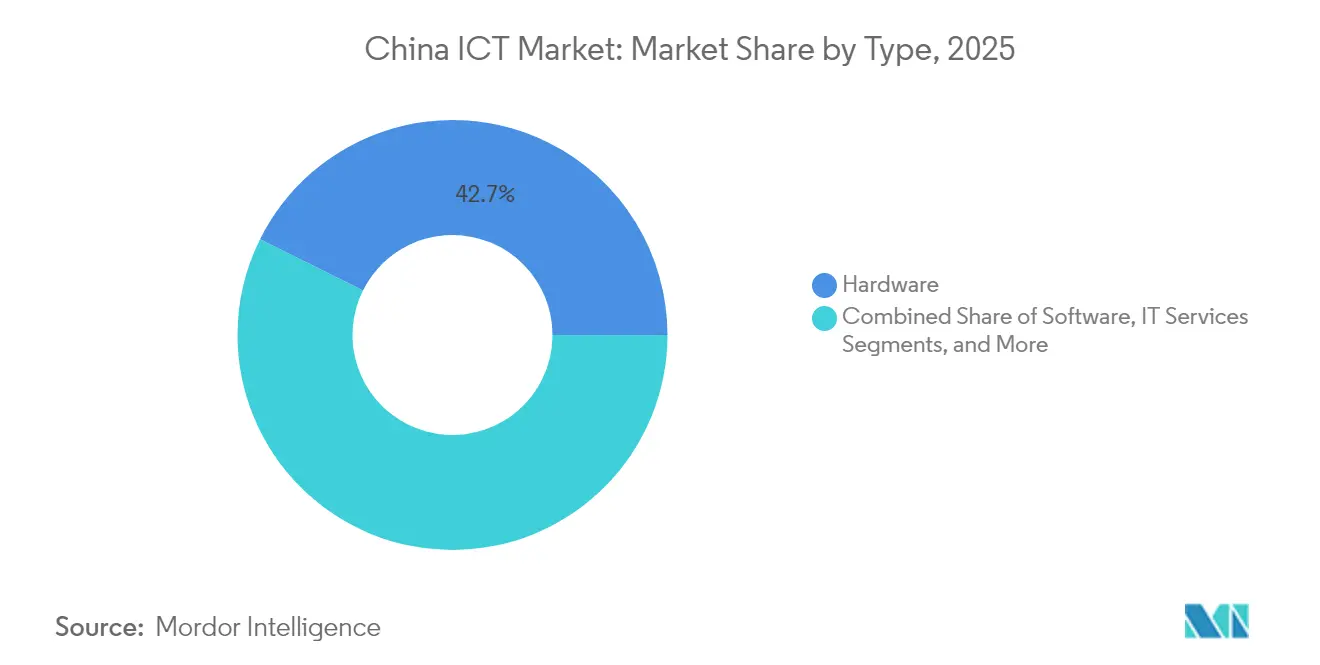

- By type, hardware led with 42.65% revenue share of the China ICT market in 2025, whereas software is projected to advance at a 10.09% CAGR through 2031.

- By enterprise size, large enterprises captured 63.55% of China's ICT market share in 2025; small and medium enterprises are expanding at a 10.32% CAGR to 2031.

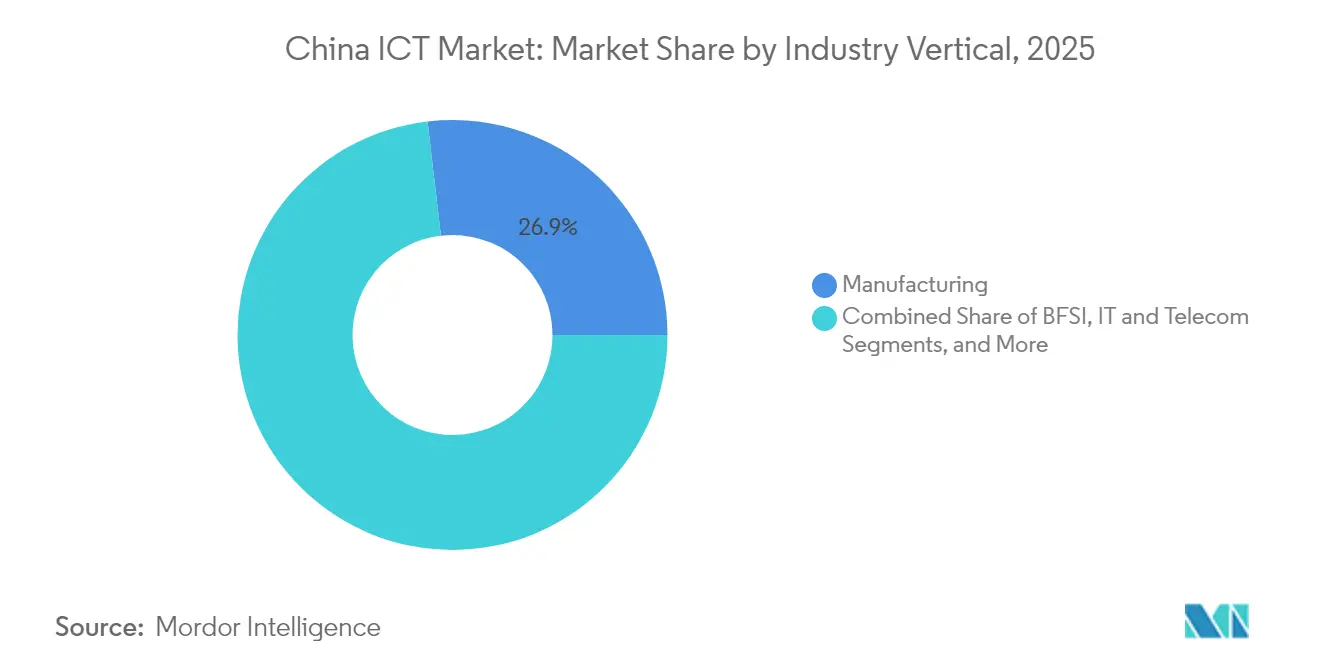

- By industry vertical, manufacturing controlled 26.85% of the China ICT market size in 2025, while retail and e-commerce are poised for 11.02% CAGR growth to 2031.

- By technology domain, cloud computing accounted for 30.35% of China's ICT market size in 2025; artificial intelligence shows the fastest trajectory at a 11.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising internet and 5G penetration | +1.5% | National, early gains in East and South | Medium term (2-4 years) |

| Government “Digital China” and 14th Five-Year ICT plan | +1.2% | National, tier-1 cities | Long term (≥4 years) |

| Accelerated enterprise cloud migration | +0.8% | East and South China | Short term (≤2 years) |

| AI-driven productivity gains | +1.1% | East China, spill-over to Central | Medium term (2-4 years) |

| “Xinjiang” localization push | +0.9% | National, strongest in manufacturing | Long term (≥4 years) |

| Carbon-informatization mandates | +0.7% | National, led by East and South China | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Internet and 5G Penetration

Nationwide 5G rollout exceeded 101.4 million subscribers in 2024, lifting mobile internet usage to 78.6%. [1]National Bureau of Statistics of China, “Statistical Communiqué of the People’s Republic of China on the 2024 National Economic and Social Development,” stats.gov.cn Industrial parks adopt private 5G networks to enable real-time quality control and autonomous guided vehicles. Each additional base station multiplies data traffic, increasing the addressable workload for edge servers and IoT gateways. Pricing models evolve from bandwidth metering toward outcome-based arrangements that link service fees to measured productivity uplifts. The China ICT market, therefore, captures both subscription revenues and high-margin integration services as enterprises redesign processes around low-latency connectivity.

Government “Digital China” and 14th Five-Year ICT Plan

Central planning sets explicit digital-economy targets, including a 45% GDP contribution by 2030. [2]Fujian Provincial Government, “Outline of the 14th Five-Year Plan (2021-2025) for National Economic and Social Development and Vision 2035,” fujian.gov.cn Unified technical standards lower integration costs for smart-city, telemedicine, and e-government platforms. Provincial grants funnel workloads westward under the “Eastern Data, Western Computing” program, cutting energy expenses and balancing regional capacity. Mandatory preference for local suppliers expands market access for domestic chip, server, and middleware vendors. The China ICT market thus gains both volume and value as policy support creates predictable demand cycles.

Accelerated Enterprise Cloud Migration

State-owned and private enterprises shift capital budgets toward operating-expense-based cloud subscriptions to conserve cash and boost agility. Hybrid deployments combine domestic clouds for regulated data with global providers for overseas operations, complicating integration and raising demand for professional services. Large retailers demonstrate AI-assisted supply-chain systems that cut fulfillment costs and improve delivery predictability. Small firms gain access to the same toolsets without building on-premises stacks, narrowing the technology gap with market leaders. Cloud-native development frameworks shorten product cycles, cementing the platform model as the de facto innovation backbone of the Chinese ICT market.

AI-Driven Productivity Gains Across Sectors

AI training capacity expanded to 23,000 PetaFLOPS with SenseTime’s SenseNova 5.5 platform release in 2025. Manufacturers report downtime reductions of up to 30% after deploying predictive-maintenance algorithms, while banks improve fraud detection accuracy with real-time models. Healthcare pilots use AI imaging to triage cases, lowering specialist workloads. The growing availability of domain-specific datasets lifts model quality, driving faster ROI and encouraging repeat investment. As AI workloads often run on domestic clouds, each new application anchors clients deeper into incumbent ecosystems, enlarging the China ICT market service revenue pool.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy IT complexity in state-owned enterprises | -0.6% | National, industrial regions | Medium term (2-4 years) |

| Escalating cybersecurity / data-sovereignty risk | -0.4% | National, heightened in border provinces | Short term (≤2 years) |

| US export controls on advanced semiconductors | -0.8% | National, severe in coastal tech hubs | Long term (≥4 years) |

| Fragmented provincial procurement processes | -0.3% | Central and West China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Legacy IT Complexity in State-Owned Enterprises

Many state actors still depend on proprietary mainframe environments installed over decades. Integrating cloud applications with these systems requires middleware and custom connectors that increase project timelines and costs. Procurement frameworks emphasize vendor track record, restricting market entry for emerging software firms. Workforce retraining adds an organizational challenge because digital workflows often conflict with established operating procedures. This inertia slows the overall pace at which the Chinese ICT market can penetrate heavy-industry value chains.

Escalating Cybersecurity and Data-Sovereignty Risk

The Cybersecurity Law and Personal Information Protection Law mandate domestic storage of sensitive datasets, forcing multinationals to duplicate infrastructure. Financial institutions must segment networks to comply with regulator audits, fragmenting architectures and raising the total cost of ownership. Threat actors increasingly target industrial control systems, prompting double-digit budget reallocation toward detection and response tools. Approved security vendors are limited, creating lock-in and supply concentration. As compliance burdens grow, discretionary funds for innovation shrink, tempering some potential expansion of the China ICT market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Hardware Foundation Enables Software Innovation

The hardware segment accounted for 42.65% of China's ICT market revenue in 2025. Investments in 5G base stations, high-density servers, and edge gateways form the indispensable substrate for nationwide digitalization. Procurement linked to smart-city, transportation, and manufacturing projects guarantees a steady equipment refresh cycle. Datacenter operators prioritize domestic chips and switch gear to mitigate export risk, anchoring value locally.

Software, though smaller today, is forecast to post a 10.09% CAGR, making it the fastest-growing component of the China ICT market. Platform-as-a-Service offerings accelerate code deployment, while low-code tools let non-technical staff prototype customer-facing applications. System-infrastructure software rides the cloud wave as enterprises modernize legacy workloads. The convergence of hardware and software yields integrated stacks, allowing vendors such as Huawei to monetize silicon, operating systems, and cloud services in a single contract.

By Enterprise Size: SME Digitalization Drives Growth

Large organizations retained 63.55% of the China ICT market share in 2025 due to sizable ERP, SCM, and CRM deployments that require bespoke integration. Their digital-transformation roadmaps span core production, finance, and distribution functions, locking in high consulting demand. Procurement cycles are lengthy yet produce multi-year recurring revenue streams once relationships mature.

SMEs log the fastest expansion at 10.32% CAGR, adding fresh addressable volume to the China ICT market size. Fiscal incentives, including tax rebates on qualifying software purchases, lower adoption barriers. Subscription-based cloud suites grant access to AI analytics, cybersecurity, and e-commerce modules without up-front hardware spend. Peer-to-peer knowledge sharing boosts confidence, and local service partners offer affordable customization. As SME digital intensity rises, overall productivity gains per USD invested often exceed those of larger rivals, reinforcing the structural importance of this customer layer.

By Industry Vertical: Manufacturing Leads Digital Transformation

Manufacturing generated 26.85% of China's ICT market revenue in 2025, reflecting government backing for smart-factory rollouts under “Made in China 2025.” IoT sensors supply granular data on machine health, enabling predictive repairs that cut downtime and scrap. Additive manufacturing and machine-vision tools increase product complexity while preserving unit economics.

Retail and e-commerce register an 11.02% CAGR to 2031, the fastest among tracked verticals. Livestreaming commerce platforms combine AI-driven personalization with real-time payment settlement to heighten consumer engagement. Logistics firms deploy route-optimization algorithms that shave delivery times, strengthening omnichannel propositions. BFSI, health, and public services also deepen digitization to meet compliance and citizen-service targets, collectively broadening the China ICT market footprint.

By Technology Domain: AI Transforms Cloud Computing

Cloud computing maintained 30.35% of the China ICT market size in 2025 as the central orchestration layer for enterprise workloads. Providers differentiate by bundling databases, middleware, and AI frameworks to drive higher average revenue per user. Interoperability standards mature, easing migration between clouds and minimizing lock-in concerns.

Artificial intelligence is projected to grow at a 11.74% CAGR to 2031, gaining from expanding data availability and improved neural-network efficiencies. Pre-trained large language models enable natural-language interfaces for internal applications, trimming employee training requirements. Edge AI supports computer-vision tasks in inspection lines and autonomous vehicles. Together, AI and cloud offerings create flywheel effects: each new AI service lifts utilization of base compute, enlarging the total China ICT market.

Geography Analysis

East China commands the largest slice of the Chinese ICT market because Shanghai, Hangzhou, and Nanjing host dense clusters of software firms, data centers, and venture funding. Regional governments commit capital to 5G macro-cell expansion and AI research institutes, stimulating corporate demand for managed infrastructure. Superior logistics links let manufacturers execute just-in-time strategies, further driving system integration spend.

South China benefits from adjacency to Hong Kong and global trade lanes. Shenzhen’s smart-city blueprint pilots sensor-rich traffic systems, digital citizen IDs, and green-energy microgrids that require real-time analytics. Semiconductor design houses in Guangdong draw on cross-border talent, reinforcing the local innovation pipeline. The combination of hardware engineering and fintech experimentation elevates the region’s share of the Chinese ICT market.

Central and Western provinces capture increasing workloads as “Eastern Data, Western Computing” incentives steer hyperscale data centers toward lower-cost inland sites. Cooler climates reduce cooling expenses, and renewable-energy availability aligns with carbon-reduction mandates. Improved rail and fiber corridors lower latency to coastal consumers, permitting national-scale services to run from interior locations. These shifts spread the China ICT market’s economic impact while narrowing historical development gaps.

Competitive Landscape

The vendor field shows medium concentration. Three local hyperscalers—Alibaba Cloud, Tencent Cloud, and Huawei Cloud—command the bulk of infrastructure services revenue, each scaling user communities through bundled AI, payments, and messaging extensions. Cybersecurity, enterprise software, and edge hardware markets remain fragmented, with scores of specialist firms targeting regulatory niches or vertical workflows.

Domestic firms accelerate proprietary chip design to sidestep export controls. Huawei’s system-on-chip roadmap illustrates vertical integration that shields supply continuity and differentiates performance for telecom and cloud workloads. [4]UC Institute on Global Conflict and Cooperation, “Huawei is Quietly Dominating China’s Semiconductor Supply Chain,” ucigcc.org Platform strategy dominates: ecosystem lock-in via developer toolkits and marketplace incentives discourages multicloud substitution. Proprietary APIs embed services deep in customer operations, raising switching costs and inflating customer lifetime value.

International intellectual-property licensors such as InterDigital adapt by signing portfolio deals that bundle 5G, video, and Wi-Fi patents, monetizing standards compliance without competing on end-user services. Foreign hyperscalers serve joint-venture customers but face data-localization barriers, cementing domestic providers’ dominance. Overall, the China ICT market balances scale benefits with innovation churn, giving agile newcomers room while rewarding incumbents that refresh technology stacks rapidly.

China ICT Industry Leaders

Alibaba Group Holding Ltd.

Huawei Technologies Co Ltd.

Tencent Holdings Ltd.

China Mobile Communications Group Co. Ltd.

Lenovo Group Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Huawei accelerated 5G infrastructure investment and semiconductor self-sufficiency initiatives, reinforcing its leadership in global telecom standards.

- April 2025: SenseTime Group launched the SenseNova 5.5 large-model system, reaching 23,000 PetaFLOPS computing power.

- April 2025: InterDigital signed 14 new licensing agreements, including OPPO and Lenovo, generating USD 869 million in revenue.

- March 2025: Baidu’s Form 20-F disclosed that variable-interest-entity transactions delivered 44% of total revenue in 2024.

- February 2025: The National Bureau of Statistics reported software and IT services revenue of CNY 13,727.6 billion, a 10% rise year on year.

- December 2024: CITI evaluation showed 86% of Chinese ICT firms committed to green supply-chain development.

- October 2024: Ningbo Municipal Government unveiled a digital-economy collaboration plan to foster regional growth.

- September 2024: UNESCO awarded the King Hamad Bin Isa Al-Khalifa Prize to China’s Smart Education platform for expanding digital resources.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines China's ICT market as the total annual spend inside mainland China on digital hardware, system and application software, IT services, and fixed and mobile telecommunication services that enable the creation, storage, transmission, and use of data across consumer and enterprise environments.

Devices whose primary purpose is analog broadcasting or non-digital entertainment are outside our scope.

Segmentation Overview

- By Type

- Hardware

- Computing Devices

- Network Equipment

- Datacentre Infrastructure

- Software

- System Infrastructure

- Enterprise Applications

- IT Services

- Consulting and Integration

- Managed Services

- Telecommunication Services

- Mobile Services

- Fixed-Line and Broadband

- Hardware

- By Enterprise Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By Industry Vertical

- BFSI

- IT and Telecom

- Government and Public

- Retail and E-commerce

- Manufacturing

- Energy and Utilities

- Healthcare

- Education

- Transportation and Logistics

- Other Industry Verticals

- By Technology Domain

- Cloud Computing

- Artificial Intelligence

- Cybersecurity

- Digital Services (SaaS, PaaS)

- Edge Computing

- Internet of Things

- Blockchain

- By Region

- East China

- South China

- North and Northeast China

- Central China

- West and North-west China

Detailed Research Methodology and Data Validation

Primary Research

We supplemented desk work with structured interviews and online surveys involving CIOs of manufacturers, bank technology heads, telecom carrier planners, regional system integrators, and SME digital-service resellers across East, South, Central, and Western China. These conversations tested price-volume assumptions, clarified emerging demand pools (edge AI, private 5G), and confirmed short-term sentiment that our models later incorporated.

Desk Research

Our analysts first mapped the revenue universe through publicly available tier-1 sources such as the Ministry of Industry and Information Technology, National Bureau of Statistics, International Telecommunication Union, OECD digital-economy dashboards, and peer-reviewed journals that track cloud and AI uptake. Company filings, investor presentations, reputable press, and curated news from Dow Jones Factiva and D&B Hoovers then supplied granular vendor and pricing clues. A spectrum of trade-association white papers plus customs statistics helped us capture import-heavy hardware niches. The sources listed here illustrate the breadth consulted; many additional references were reviewed to validate facts and close data gaps.

Market-Sizing and Forecasting

A top-down build started with MIIT revenue lines, carrier service income, and hardware production plus trade data, which were then reconciled with selective bottom-up checks such as sampled average selling price multiplied by smartphone shipments and supplier roll-ups for servers. Key variables driving the model include 5G base-station stock, enterprise cloud spend, SaaS ARPU, GDP growth, and annual device replacement intervals. Multivariate regression, supported by ARIMA overlays for cyclical hardware swings, projects values through 2030. Where SME spending evidence was thin, weightings derived from primary-research penetration rates bridged the gap.

Data Validation and Update Cycle

Outputs pass anomaly screens, variance checks against independent indices, and a two-step peer review before sign-off. Reports refresh yearly, with interim revisions when policy shifts or large acquisitions materially alter the baseline. Before each client delivery, an analyst re-runs the latest data sweep, ensuring users receive a timely view.

Why Our China ICT Baseline Earns Trust

Published figures often diverge because firms use different scopes, refresh cadences, and untested assumptions. Our disciplined boundary setting, twice-validated inputs, and annual recalibration keep Mordor's number dependable when decisions must be made quickly.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.89 trillion (2025) | Mordor Intelligence | - |

| USD 651 billion (2024) | Regional Consultancy A | Excludes telecom services and consumer device turnover |

| USD 691.5 billion (2028) | Industry Association B | Focuses on enterprise outlays only, no consumer hardware reconciliation |

| USD 1.5 trillion (2023) | Global Consultancy C | Combines carrier capex with historical sales, last full update two years old |

The comparison shows that when scope is narrow or updates lag, totals shrink or swell unpredictably. By grounding estimates in current, clearly delineated revenue streams and verifying them through field intelligence, Mordor delivers a balanced, transparent baseline clients can rely on.

Key Questions Answered in the Report

What is the value of China’s ICT market today and in 2031?

The market is valued at USD 0.95 trillion in 2026 and is forecast to reach USD 1.35 trillion by 2031, growing at a 7.14% CAGR.

Which component of spending is expanding the fastest?

Software is the quickest-growing segment with a 10.09% CAGR through 2031, reflecting a shift toward platform services and recurring revenue models.

How do government policies shape industry growth?

“Digital China” programs and the 14th Five-Year ICT Plan direct investment, set procurement preferences for domestic suppliers, and target a 45% digital-economy share of GDP by 2030, creating predictable demand cycles.

Why is artificial intelligence so important to Chinese enterprises?

AI workloads improve productivity—manufacturers report up to 30% fewer equipment outages—while SenseTime’s SenseNova 5.5 brings 23,000 PetaFLOPS of compute to market, enabling rapid deployment without building in-house models.

Which region contributes the largest share of ICT spending?

East China leads due to dense clusters of technology firms and datacenters in Shanghai, Hangzhou, and Nanjing, supported by strong logistics and policy incentives.

What restraints could slow market expansion?

Legacy IT systems in state-owned enterprises, tighter data-sovereignty rules, and ongoing US export controls on advanced chips each subtract from potential growth by adding complexity, cost, or supply risk.

Page last updated on: