Japan Residential Construction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

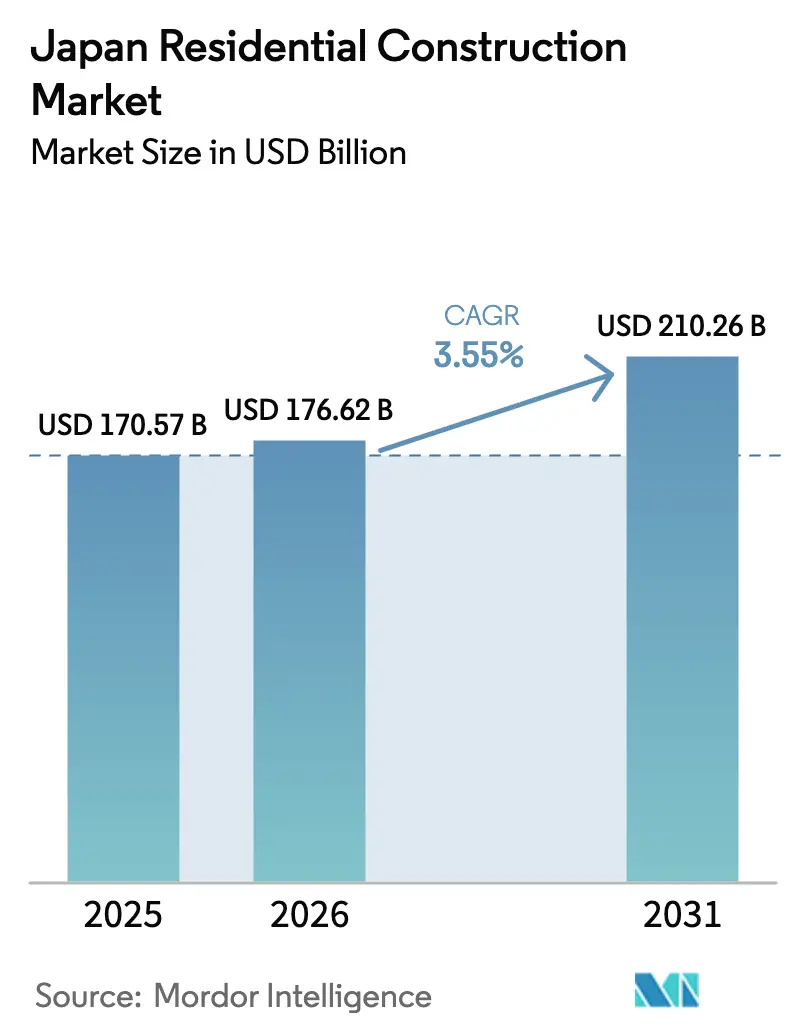

| Base Year Market Size (2025) | USD 170.57 Billion |

| Market Size (2026) | USD 176.62 Billion |

| Market Size (2031) | USD 210.26 Billion |

| Growth Rate (2026 - 2031) | 3.55% CAGR |

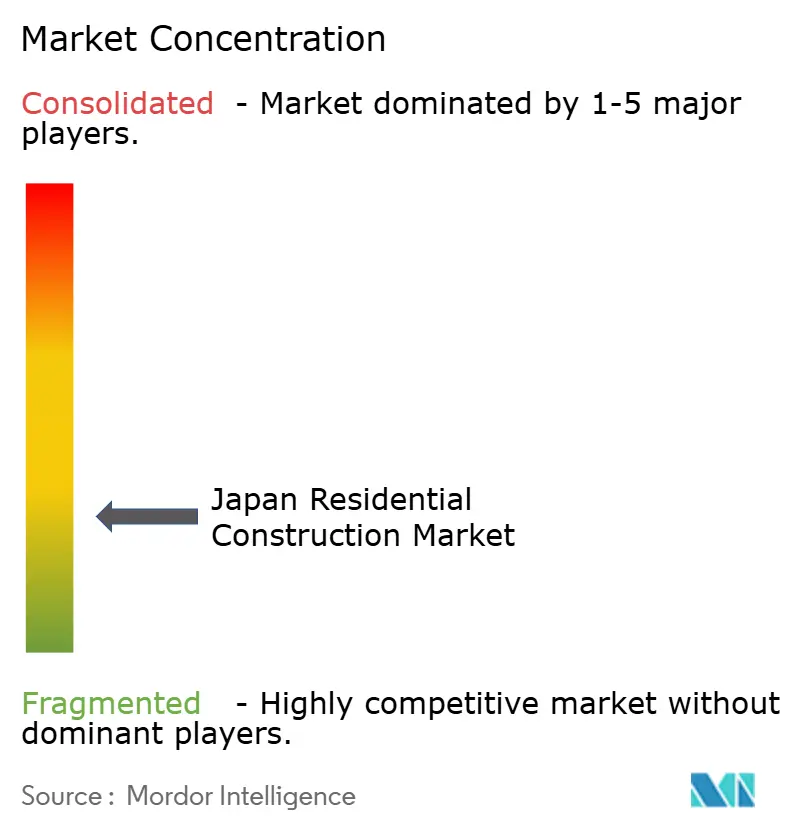

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Residential Construction Market Analysis by Mordor Intelligence

The Japan residential construction market size was valued at USD 170.57 billion in 2025 and estimated to grow from USD 176.62 billion in 2026 to reach USD 210.26 billion by 2031, at a CAGR of 3.55% during the forecast period (2026-2031). Growth rests on energy-efficiency mandates that propel renovation spending, persistent urbanization that tightens apartment demand, and technology advances that shorten build times. Digital mortgages are making finance faster, while foreign-currency buyers—buoyed by a weak yen—drive premium condominium absorption. At the same time, labor shortages and materials volatility continue to pressure margins, pushing firms toward modern methods of construction and long-term supplier contracts. The overall outlook signals measured expansion, yet players that align products with shrinking household sizes and regulatory upgrades remain best positioned to capture value in the Japan residential construction market.

Key Report Takeaways

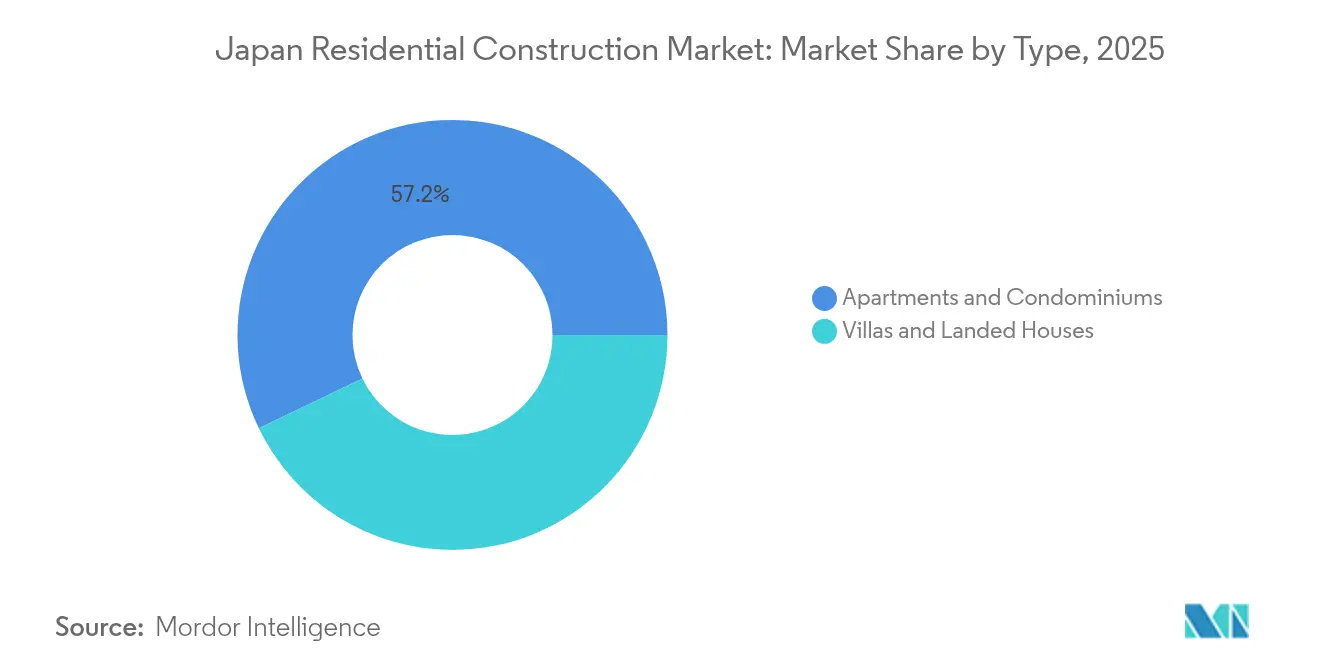

- By type, apartments and condominiums led with 57.15% of the Japan residential construction market share in 2025, whereas villas and landed houses are forecast to expand at a 3.86% CAGR to 2031.

- By construction type, new construction accounted for 64.55% of the Japan residential construction market size in 2025; renovation is advancing at a 3.74% CAGR through 2031.

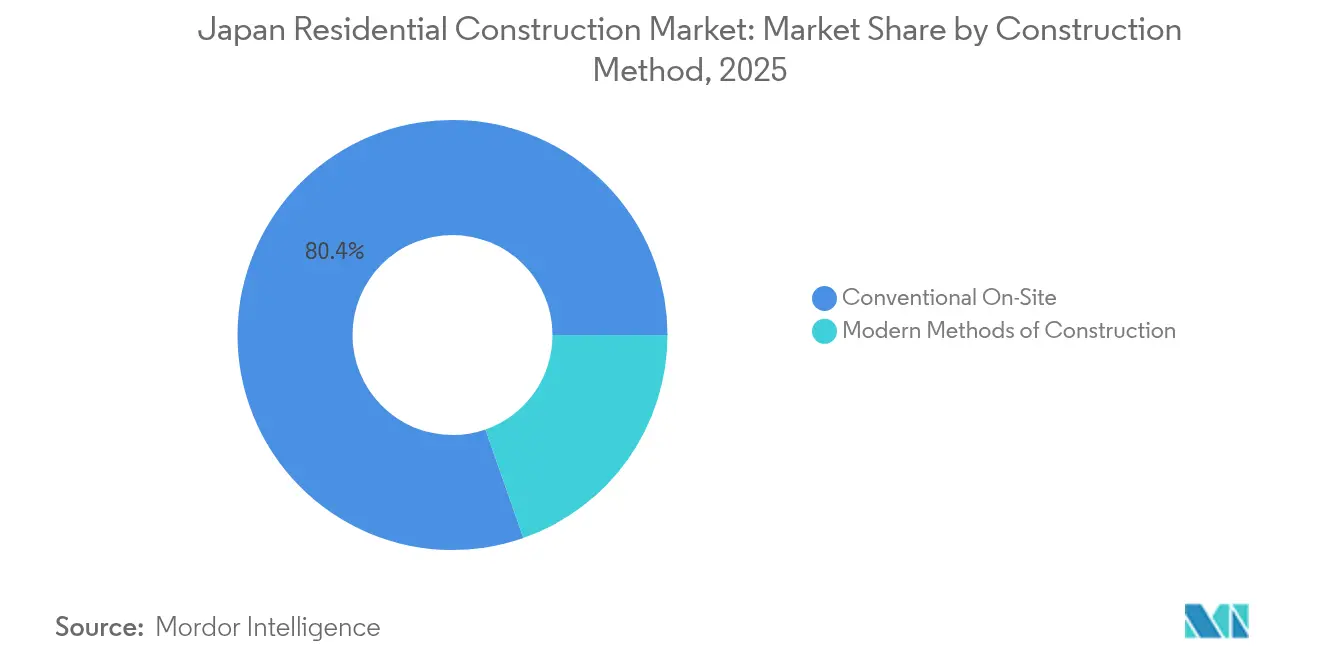

- By construction method, conventional on-site building retained an 80.35% share of the Japan residential construction market size in 2025, while modern methods of construction exhibit the fastest 4.68% CAGR.

- By investment source, private capital held 72.85% of funding in 2025, yet public investment is the faster-growing stream at 4.29% CAGR on the back of seismic-retrofit and energy-subsidy programs.

- By geography, Tokyo commanded 35.85% of the Japan residential construction market share in 2025; Osaka is set to grow at a 4.22% CAGR as Expo 2025 infrastructure fuels demand.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Residential Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory 2025 energy-efficiency codes accelerate renovation activity | +1.2% | National, with early gains in Tokyo, Osaka | Short term (≤ 2 years) |

| Shrinking household size fuels demand for compact urban apartments | +0.8% | Tokyo, Osaka, Nagoya metropolitan areas | Medium term (2-4 years) |

| High-precision off-site fabrication cuts build time by up to 30% | +0.7% | National, led by major metropolitan areas | Long term (≥ 4 years) |

| Government seismic-retrofit grants for older homes | +0.6% | National, concentrated in earthquake-prone regions | Long term (≥ 4 years) |

| Foreign-currency buyers exploiting weak yen in premium condo segment | +0.5% | Tokyo, Osaka premium districts | Short term (≤ 2 years) |

| Digital mortgage platforms shorten approval cycles, boosting starts | +0.4% | Urban centers, expanding to regional markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shrinking Household Size Fuels Demand for Compact Urban Apartments

Japan’s average household size continues to fall, spurring a lasting appetite for smaller, well-designed urban dwellings. One- and two-person households dominate metropolitan areas, prompting developers to optimize space via modular layouts that fit within tight footprints. The preference for convenience and proximity to transit is reshaping project design toward maintenance-free buildings with integrated community services. Prefabricated compact modules enable faster delivery and customization, aligning with lifestyle choices that favor rental flexibility over ownership permanence. These dynamics keep apartment absorption resilient even as the overall population declines[1]Statistics Bureau of Japan, “Household Projections for Japan, 2025–2040,” Statistics Bureau of Japan, stat.go.jp.

Mandatory 2025 Energy-Efficiency Codes Accelerate Renovation Activity

Amendments to the Building Energy Efficiency Act compel every new residential build to meet stringent consumption benchmarks by 2025. Thousands of existing homes now require insulation, window, and HVAC upgrades to preserve asset values, energizing a nationwide retrofit wave. Contractors have pivoted to specialized energy-retrofit packages, and property owners are rushing projects to avoid compliance penalties. The compressed timeline expands renovation backlogs, raising the Japan residential construction market size tied to retrofits and reinforcing demand for high-performance materials.

Digital Mortgage Platforms Shorten Approval Cycles, Boosting Starts

Automated underwriting and e-document verification have trimmed mortgage approvals from weeks to days. Faster credit decisions improve cash-flow planning for developers and empower smaller builders to compete against established conglomerates. Transparency in lending terms intensifies price competition among banks, resulting in wider borrower choice. Integration between digital mortgage tools and project-management software further synchronizes drawdowns with on-site milestones, minimizing financing bottlenecks in the Japan residential construction market.

Government Seismic-Retrofit Grants for Older Homes

Subsidies covering up to 50% of diagnostic and retrofit costs make structural reinforcement financially viable for millions of pre-1981 buildings that sit below today’s seismic codes. Installation of energy-efficient elements often accompanies reinforcement, creating dual compliance benefits. Rural communities benefit from the grants as lower property values previously deterred investment. With funding horizons extending beyond 2030, specialist contractors enjoy predictable demand streams and invest in standardized retrofit systems that cut site time and waste.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid labour-cost inflation and 2024 overtime cap | -1.1% | National, most severe in metropolitan areas | Short term (≤ 2 years) |

| Demographic decline creating long-term oversupply risk | -0.9% | Rural areas, spreading to secondary cities | Long term (≥ 4 years) |

| Materials price volatility post-Ukraine conflict | -0.6% | National, with regional supply chain variations | Medium term (2-4 years) |

| Complex land-title laws delaying site assembly | -0.4% | National, particularly acute in rural areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Labour-Cost Inflation and 2024 Overtime Cap

Overtime restrictions now cap weekly hours, forcing contractors to maintain larger workforces amid already scarce skilled labour. Wage rates have climbed quickly as firms poach experienced hands, squeezing profit margins and causing smaller builders to exit the market. Pressure is most acute in the Tokyo and Osaka areas, where project pipelines remain busy. Automation and off-site fabrication adoption rise as rational countermeasures, yet implementation requires capital beyond many smaller players’ reach.

Demographic Decline Creating Long-Term Oversupply Risk

Japan’s population has contracted by more than 2 million since 2008, and forecasts show a sustained decline. Rural prefectures report 8.5 million vacant houses, equal to 13% of stock, dragging local prices lower. Developers now scrutinize household-formation projections before green-lighting projects outside major metros, shifting capital toward renovation of existing assets rather than speculative new builds.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Compact Living Drives Urban Density

Apartments and condominiums captured 57.15% of the Japan residential construction market in 2025, a testament to enduring urban concentration and shrinking average household size. Developers rely on high-rise formats to optimize scarce land and employ prefabricated modules for speed, quality, and energy compliance. High-performance windows, smart meters, and co-living amenities meet buyer priorities for efficiency and community. Villas and landed houses remain niche yet fast-moving, forecast to grow at 3.86% CAGR as affluent locals and foreign buyers chase larger footprints and garden space. Luxury builders such as Sekisui House tailor these detached units with solar roofing and seismic isolation to justify premium pricing.

Urban apartment schemes also benefit from scale economics; common mechanical systems and shared services compress per-unit operating costs, supporting competitive rents. Developers partner with prop-tech firms to integrate keyless entry and energy dashboards that appeal to digital-native tenants. Conversely, spacious landed properties attract overseas purchasers capitalizing on yen weakness, particularly in Tokyo’s western suburbs and resort locales. Builders pursue mass-customization strategies—factory-built shells paired with bespoke interiors—to keep margins healthy without stretching timelines. Such flexibility allows the Japan residential construction market to satisfy distinctly different lifestyle segments while keeping capacity utilization high.

By Construction Type: Renovation Gains Momentum

New construction represented 64.55% of the Japan residential construction market size in 2025, reflecting sustained demand for code-compliant housing. However, renovation is growing at 3.74% CAGR as energy mandates and seismic grants reshape spending priorities. Tokyo condominium boards schedule window retrofits and insulation upgrades to lock in subsidies, while detached-home owners pursue envelope improvements that raise resale prospects. Construction firms now offer bundled refurbishment packages, including heat-pump installation and structural bracing, to capture the rising retrofit wallet share.

New-build projects continue to thrive where land consolidation succeeds, enabling smart-city precincts with district-level energy systems and 5G connectivity. Prefabricated platform houses from Daiwa House hit the site in days, satisfying buyers eager for rapid occupancy. Yet capital allocation is gradually rebalancing toward existing stock, where asset uplift is often more predictable and avoids title consolidation headaches. As renovation depth intensifies, material suppliers expand ranges of thin-profile insulation, triple-glazed sash, and low-VOC finishes suited to occupied retrofits, broadening the solution set available to the Japan residential construction market.

By Construction Method: Technology Transforms Traditional Practices

Conventional on-site methods still held 80.35% of the 2025 output, given their adaptability to irregular sites and custom architecture. Nevertheless, modern methods of construction (MMC) are scaling at a 4.68% CAGR, driven by labour scarcity and productivity goals. Firms like Kajima deploy autonomous bulldozers and drone-guided surveys that slash earthworks duration, while Sekisui House’s Smart Heim factories deliver volumetric units pre-fitted with mechanicals. These MMC approaches provide measured tolerances, lower waste, and consistent thermal performance that ease regulatory compliance.

Traditional builders respond by integrating partial off-site components—such as panelized façades and bathroom pods—to offset job-site overtime constraints. Hybrid workflows preserve architectural flexibility yet capture manufacturing gains. Financial institutions recognise the risk mitigation benefits of MMC’s predictable timelines, leading some lenders to offer preferential terms for factory-based projects. As robotic capability matures, the Japan residential construction market anticipates a gradual shift from hand-built processes to automated assembly lines without abruptly sidelining the artisanal craftsmanship prized in niche luxury segments.

By Investment Source: Private Capital Leads Market Development

Private investors supplied 72.85% of project funding in 2025, underscoring Japan’s market-centric housing system. Developers access low-interest loans and increasingly tap REIT structures to recycle capital into new pipelines. Homebuyers leverage historically low mortgage rates, amplified by digital underwriting, to secure units quickly. Public investment, although just 27.15% of total funding, is advancing 4.29% annually thanks to seismic-retrofit and climate-resilience allocations in national budgets.

Private capital thrives on quick-turn condominium projects in central business districts where presales secure debt coverage ratios early. Meanwhile, public funds target social and environmental objectives: grants cover half the diagnostic cost of quake upgrades and offer USD 4,000 equivalent per dwelling for high-spec insulation. This catalytic role pulls in matching private outlays, multiplying total sector stimulus. The blended finance environment reinforces stability across the Japan residential construction market while allowing competitive dynamics to steer project selection and execution efficiency.

Geography Analysis

Tokyo captured 35.85% of the Japan residential construction market share in 2025, sustained by dense employment hubs, premium schooling, and global connectivity that underpin continuous in-migration. Foreign investors exploiting the weak yen accounted for one-fifth of luxury condominium transactions, nudging price points upward. Developers respond with high-rise towers engineered for net-zero energy and vertical greening, features that align with metropolitan carbon-reduction agendas. Land scarcity pushes design toward micro-units and multi-purpose communal areas, optimizing every square meter and keeping per-unit pricing within reach of younger professionals.

Osaka registers the fastest 4.22% CAGR through 2031 as Expo 2025 infrastructure augments transit corridors and waterfront regeneration. The event’s projected USD 19.4 billion ripple boosts job creation, stimulating new household formation and temporary worker accommodation demand. Regional banks extend construction credit to capitalize on tourism-driven rental prospects. Local authorities fast-track permitting for mixed-use districts that upgrade seafront resilience and integrate smart waste systems. The transformation elevates Osaka’s profile as an affordable alternative to Tokyo, encouraging inter-city migration and overseas investor diversification.

Beyond the major metros, Nagoya benefits from stable manufacturing payrolls anchored by automotive and aerospace clusters, supporting balanced construction pipelines. Nevertheless, many regional cities grapple with shrinking populations and vacant housing. Government-backed “compact city” policies consolidate services around transit nodes, incentivizing teardown of dilapidated stock and redevelopment into energy-efficient mid-rise apartments. Construction firms specializing in demolition and brownfield remediation find opportunity in these localized renewal schemes, preserving activity breadth across the Japan residential construction market even as national demographics soften.

Competitive Landscape

The Japan residential construction market is quite fragmented. Fragmentation defines competition, with roughly 20 key firms each holding single-digit shares yet separated by technology capabilities rather than scale alone. Daiwa House and Sekisui House dominate the prefabricated segment through proprietary steel-frame and modular wood systems, while Sumitomo Forestry leverages sustainable timber platforms to attract eco-conscious buyers. These leaders funnel R&D into autonomous assembly and integrated energy storage, setting performance benchmarks that smaller regional builders struggle to match. Market share gaps remain moderate, sustaining customer choice and pricing tension.

Strategic moves increasingly feature overseas expansion that hedges domestic demographic risk. Daiwa House’s 35% stake in Alliance Residential deepens its US multifamily pipeline, and Sekisui House targets 20,000 annual US home deliveries by 2031, exporting Japanese quality systems abroad. At home, firms invest in AI-enabled design configurators that customize layouts at low marginal cost, differentiating offers without compromising factory throughput. Energy-as-a-service packages bundled with rooftop solar and storage systems surface as newer revenue streams, tying buyers into long-term maintenance contracts[3]Japan Federation of Housing Organizations, “Prefabricated Housing Market Share Survey 2024,” Japan Federation of Housing Organizations, jfoh.jp.

Labour regulation and input volatility accelerate consolidation among mid-tier contractors that lack the capital to adopt MMC or buffer material shocks. Larger players snap up niche specialists in seismic retrofitting and insulation to bolt capabilities onto integrated platforms. Financial robustness enables tier-one builders to lock multi-year steel contracts or forward-purchase land, stabilizing supply in turbulent markets. These defensive and offensive maneuvers collectively sustain a dynamic yet disciplined competitive environment in the Japan residential construction market.

Japan Residential Construction Industry Leaders

Daiwa House

Sekisui House

Sumitomo Forestry

Panasonic Homes

Asahi Kasei Homes

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Panasonic Corporation rolled out its OASYS residential central air-conditioning system in the United States, touting energy cuts of more than 50% versus legacy HVAC units. The move extends Panasonic’s premium, high-efficiency product line into a market that values reduced operating costs.

- November 2024: Daiwa House Industry closed on a 35% equity stake in U.S. multifamily specialist Alliance Residential, securing an immediate pipeline of large-scale rental projects. The deal diversifies Daiwa’s earnings base while leveraging its modular building know-how overseas.

- June 2024: Sekisui House unveiled a U.S. growth blueprint targeting annual deliveries of 20,000 homes by FY 2031, backed by its acquisition of M.D.C. Holdings. The plan anchors revenue expansion on exporting Japanese off-site construction and sustainability standards.

- April 2024: Sumitomo Forestry announced it will lift U.S. rental housing output to at least 10,000 units a year through 2027, up 25% from 2023 levels. Management cited surging American rental demand amid higher mortgage rates as the catalyst for scaling operations.

Japan Residential Construction Market Report Scope

Residential construction includes construction on single-family or two-family dwellings that are occupied or used or are intended to be occupied or used, primarily for residential purposes. One in which the architect uses materials to construct the complete structure according to customers' tastes and choices before selling it to the buyers at a profit. The Japanese residential construction market is segmented by type (apartments & condominiums, villas, and other types) and by construction type (new construction and renovation). The report offers market size and forecasts for Japan's residential construction market in value (USD billion) for all the above segments.

| Apartments & Condominiums |

| Villas and Landed Houses |

| New Construction |

| Renovation |

| Conventional On-Site |

| Modern Methods of Construction |

| Public |

| Private |

| Tokyo |

| Osaka |

| Nagoya |

| Rest of Japan |

| By Type | Apartments & Condominiums |

| Villas and Landed Houses | |

| By Construction Type | New Construction |

| Renovation | |

| By Construction Method | Conventional On-Site |

| Modern Methods of Construction | |

| By Investment Source | Public |

| Private | |

| By Region | Tokyo |

| Osaka | |

| Nagoya | |

| Rest of Japan |

Key Questions Answered in the Report

What is the current size of the Japan residential construction market?

The Japan residential construction market stands at USD 176.62 billion in 2026 and is expected to reach USD 210.26 billion by 2031.

Which housing type dominates new projects?

Apartments and condominiums lead with 57.15% share of activity in 2025, reflecting strong urban demand for compact living.

How fast is renovation spending growing?

Renovation work is expanding at a 3.74% CAGR through 2031, driven by energy-efficiency mandates and seismic-retrofit subsidies.

Why are modern methods of construction gaining traction?

Labour shortages and overtime limits push builders toward factory-built modules that cut on-site time by up to 30% while ensuring code compliance.

Which city is the fastest-growing regional market?

Osaka posts the quickest 4.22% CAGR, supported by Expo 2025 infrastructure and waterfront redevelopment.

How do foreign buyers influence premium condominium demand?

A weak yen lets overseas investors purchase high-end Tokyo and Osaka units at perceived discounts, making up roughly 20% of luxury transactions and spurring tailored amenities.

Page last updated on: