Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

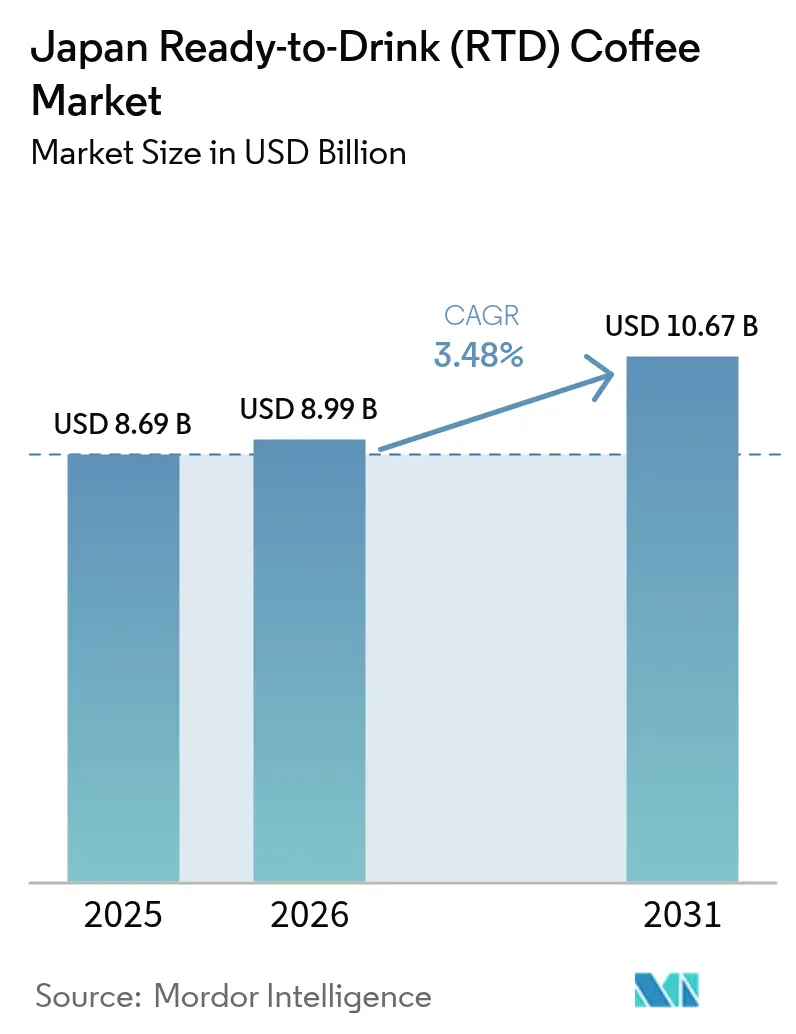

| Base Year Market Size (2025) | USD 8.69 Billion |

| Market Size (2026) | USD 8.99 Billion |

| Market Size (2031) | USD 10.67 Billion |

| Growth Rate (2026 - 2031) | 3.48% CAGR |

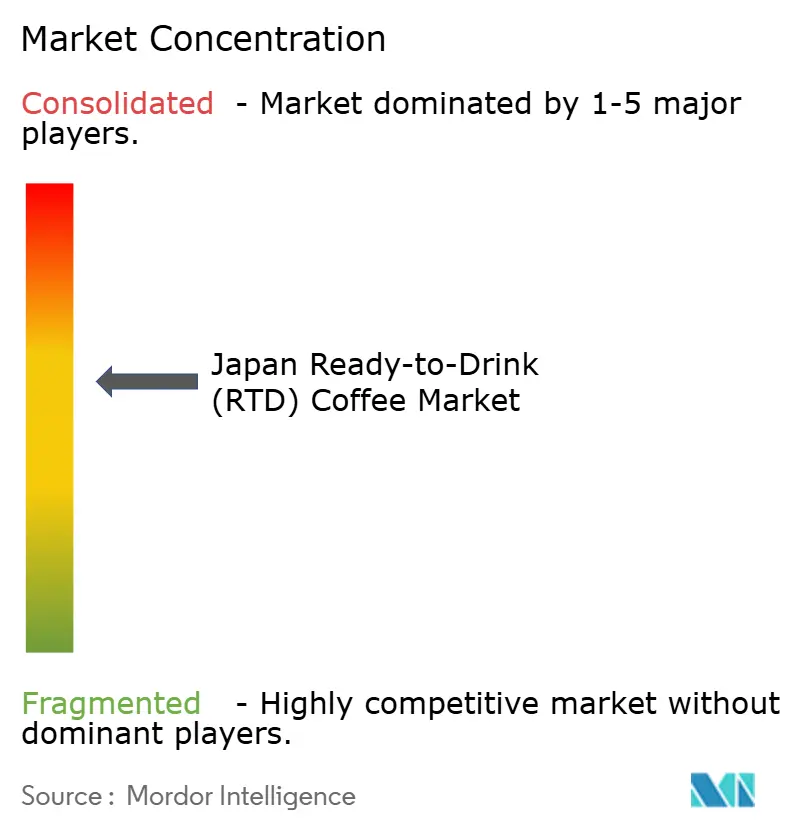

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Japan Ready-to-Drink (RTD) Coffee Market Analysis by Mordor Intelligence

The Japanese Ready-to-Drink (RTD) Coffee market size is expected to grow from USD 8.69 billion in 2025 to USD 8.99 billion in 2026 and is forecast to reach USD 10.67 billion by 2031 at 3.48% CAGR over 2026-2031. The moderate growth trajectory reflects market maturity in a country where canned coffee has been deeply embedded in daily consumer routines for over five decades. However, the market's sustained performance is underpinned by rapid urbanization, Japan's unparalleled vending machine infrastructure, and persistent product innovation. Additionally, consumer preferences are transforming due to heightened health awareness and increasing demand for premium offerings. Significant market developments include the transition to convenient resealable PET bottles, the proliferation of cold-brew varieties, and diversification into plant-based alternatives. Despite intense market competition, established manufacturers maintain their market positions through innovative flavor combinations, enhanced functional benefits, and optimized distribution strategies.

Key Report Takeaways

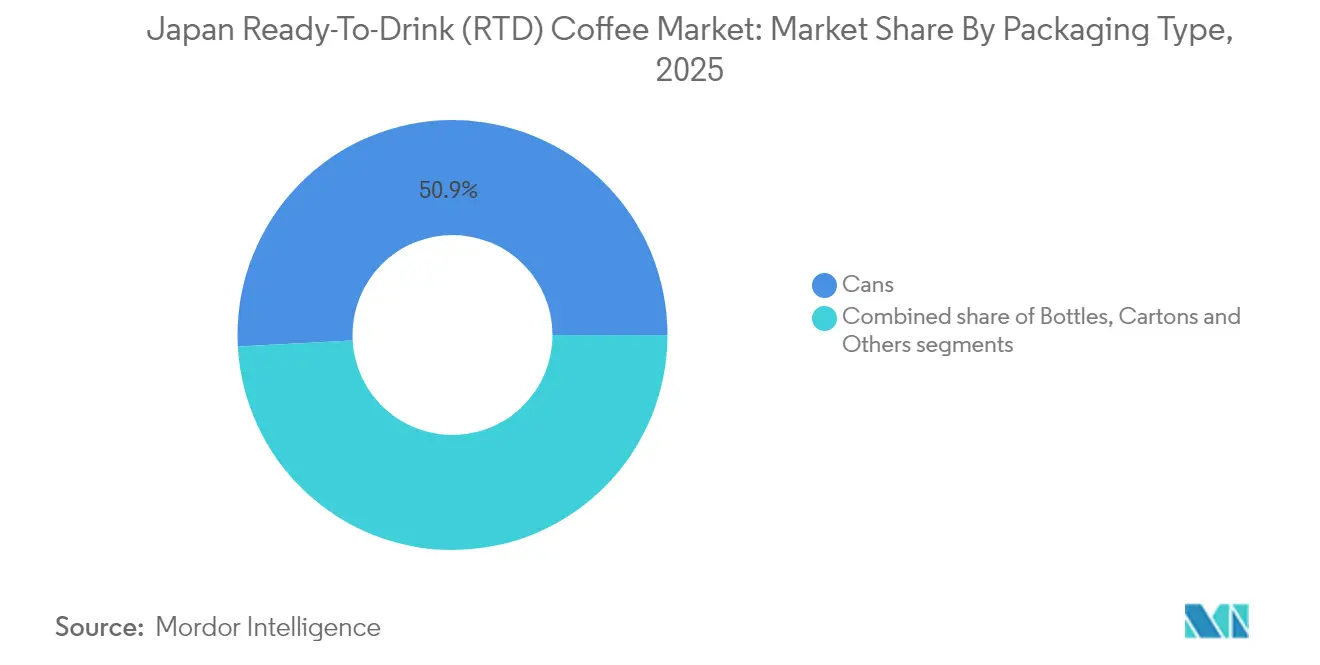

- By packaging type, cans led with 50.86% of the Ready-to-Drink Coffee market share in 2025, while bottles (PET + glass) are projected to post the fastest 4.98% CAGR through 2031.

- By product type, iced latte/cappuccino captured 54.25% of the Ready-to-Drink Coffee market size in 2025; cold brew is forecast to expand at a 5.62% CAGR to 2031.

- By flavor profile, plain/classic coffee captured 61.05% share in 2025; flavored variants are set to log the highest 6.15% CAGR over the same period.

- By ingredient base, dairy formats dominated with an 79.35% share in 2025, whereas plant-based alternatives are advancing at an 8.17% CAGR to 2031.

- By price positioning, mass-market SKUs accounted for 69.65% of sales in 2025, with premium lines growing at a 6.04% CAGR to 2031.

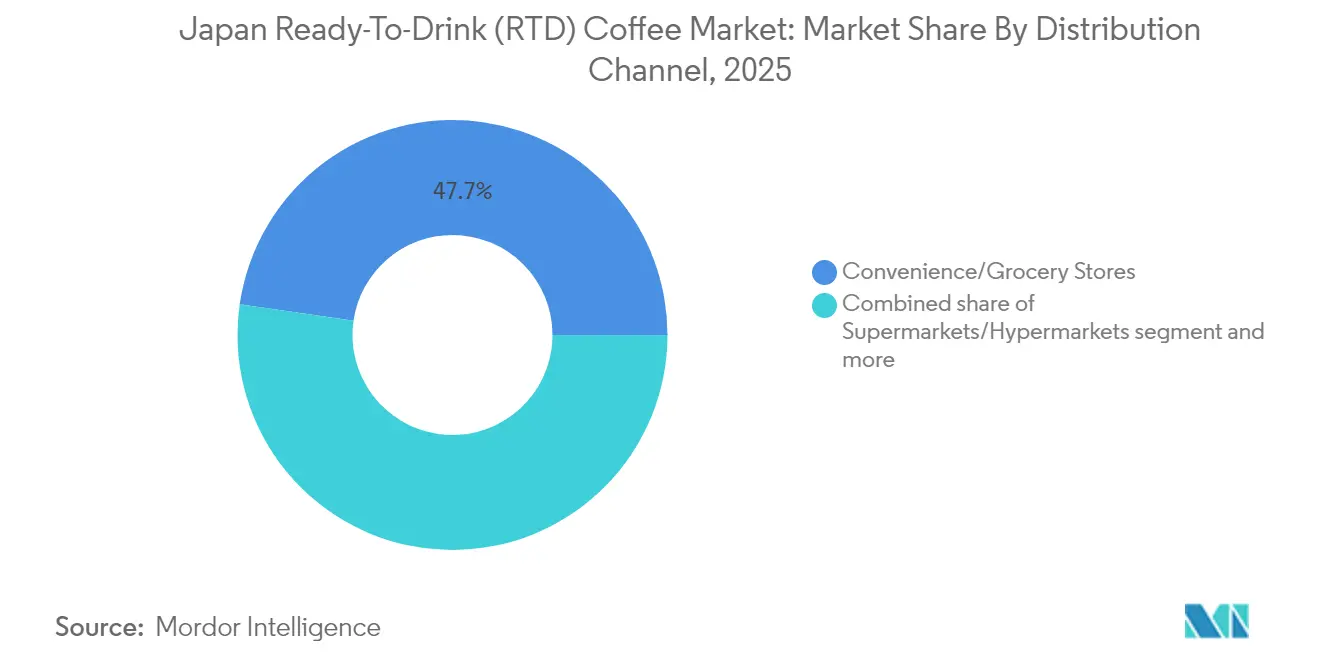

- By distribution channel, convenience/grocery stores delivered 47.72% of 2025 sales; online retail is rising at an 8.03% CAGR through 2031.

- By prefecture, Tokyo contributed 18.10% of national revenue in 2025, while Kanagawa is the fastest-growing area at a 4.16% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Ready-to-Drink (RTD) Coffee Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Convenience and On-the-Go Consumption on the Rise | +1.2% | National, with particular relevance in urban centers of Tokyo, Osaka, and Kanagawa | Short term (≤ 2 years) |

| Health Trends Spotting in RTD Coffee Beverages | +0.8% | National, with early adoption in Tokyo metropolitan area | Medium term (2-4 years) |

| Augmented Expenditure on Advertising and Promotional Activities | +0.5% | National, with concentration in major urban centers | Short term (≤ 2 years) |

| Product Innovation Experiences Notable Surge | +0.9% | National, serving as the domestic innovation hub | Medium term (2-4 years) |

| Established Coffee Culture Supports Market Expansion | +0.4% | National, with stronger impact in urban prefectures | Long term (≥ 4 years) |

| Workplace Consumption Boosts Market Demand | +0.3% | Tokyo, Osaka, Nagoya, and other business centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Convenience and On-the-Go Consumption on the Rise

Japan's RTD coffee market thrives due to a large and active workforce, approximately 69.6 million people in 2024, as reported by the Ministry of Internal Affairs and Communication (Japan) [1]Official Statistics of Japan, "Labour Force Survey 2024", e-stat.go.jp/, many of whom operate in fast-paced urban environments like Tokyo. In Tokyo's prominent business districts, notably Shinjuku and Marunouchi, office workers depend on canned or bottled coffee during work breaks, capitalizing on immediate availability and streamlined service. This labor force fuels demand for quick caffeine fixes, especially through the country’s dense vending machine network, which offers 24/7 access to hot and cold coffee. With one vending machine for every 23 people, Japan ensures unparalleled RTD availability, perfectly suited to its long-working-hour culture. The consistent year-round consumption of RTD coffee further highlights the entrenched role RTD beverages play in Japan’s daily lifestyle.

Health Trends Spotting in RTD Coffee Beverages

Japanese consumers are demonstrating a significant shift toward RTD coffee products with health benefits, compelling manufacturers to develop innovative formulations with reduced sugar content and enhanced functional ingredients. This trend aligns with Japan's comprehensive focus on wellness and preventive health, particularly resonating among busy office workers and health-conscious older consumers. The substantial increase in demand for unsweetened black coffee, prominently featured by major brands like Suntory's BOSS and Asahi's Wonda, reflects a decisive movement toward healthier, low-calorie alternatives. The market is experiencing robust growth in functional RTD coffees enriched with essential nutrients, including protein, vitamins, collagen, and probiotics. Meiji's strategic April 2025 launch of a whole oats RTD coffee beverage, featuring 12 grams of whole grain oats per bottle and delivering beneficial dietary fiber with heart-healthy beta-glucan, exemplifies this innovative approach. These enhanced beverages effectively bridge the gap between nutritional requirements and convenience, catering to consumers seeking wholesome options in their daily routines.

Augmented Expenditure on Advertising and Promotional Activities

Japanese RTD coffee manufacturers have significantly increased their marketing investments to differentiate themselves in the highly competitive market. Suntory's BOSS brand campaigns, featuring the Pride of BOSS commemorative can and Craft BOSS PET bottle series, generated substantial sales growth despite market deceleration. The Craft BOSS series achieved remarkable success through strategic market positioning and targeted consumer engagement. Companies are extensively utilizing digital platforms and social media channels to connect with younger consumers, focusing on sophisticated visual product design and packaging innovations. Additionally, cold brew products have particularly benefited from this digital-first approach, as their aesthetic appeal drives significant social media engagement and sharing among Gen Z consumers.

Product Innovation Experiences Notable Surge

The Japanese ready-to-drink (RTD) coffee market is undergoing extensive product innovation, as manufacturers develop sophisticated brewing methods, diverse flavor profiles, and advanced packaging solutions. UCC's launch of "water-brewed coffee" in June 2025 represents a breakthrough in cold extraction technology, delivering enhanced smoothness and aromatic complexity specifically designed for younger consumer preferences. The market evolution includes premium nitro-infused canned coffees and specialized functional RTD coffee beverages incorporating adaptogens and nootropics. Moreover, in a significant packaging advancement, SIG's implementation of aseptic carton packs at Moriyama's Kanagawa Prefecture plant demonstrates technological innovation while reinforcing environmental sustainability commitments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Amout of HFSS Sugar Limiting Iced Coffee Growth | -0.7% | National, particularly affecting health-conscious urban consumers | Medium term (2-4 years) |

| Arabica Cost Volatility Post-Brexit Tariffs | -0.5% | National, influencing domestic importers and manufacturers | Short term (≤ 2 years) |

| RTD Coffee Faces Stiff Competition for Shelf Space from Emerging Alternatives | -0.4% | National, with stronger impact in urban retail environments | Medium term (2-4 years) |

| Caffeine Concerns Curbing RTD Coffee | -0.3% | National, with particular relevance among younger and elderly demographics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Amout of HFSS Sugar Limiting Iced Coffee Growth

The elevated sugar content in ready-to-drink (RTD) coffee beverages continues to deter health-conscious Japanese consumers, particularly amid growing awareness of high fat, salt, and sugar (HFSS) content. This concern is especially prominent among urban professionals and younger consumers who demand nutritional transparency in their beverage choices. The intensifying focus on health has accelerated the shift toward reduced-sugar options across the market. Manufacturers face the critical challenge of maintaining appealing flavor profiles while reducing sugar content, as traditional RTD coffee products typically contain significant levels of added sugars. This limitation particularly impacts the iced latte/cappuccino segment, where sweetened formulations have traditionally dominated consumer preferences. In response to this market evolution, major companies like Suntory and Asahi are actively developing and introducing innovative lower-sugar alternatives to address this growth constraint.

Arabica Cost Volatility Post-Brexit Tariffs

The fluctuating prices of Arabica coffee beans, combined with post-Brexit tariff changes, have significantly increased operational costs for Japanese ready-to-drink (RTD) coffee manufacturers. Japan's substantial dependence on European trading networks for premium coffee beans has made procurement increasingly complex under the new tariff structure. These mounting cost pressures directly impact production expenses and profit margins, particularly for premium RTD coffee products that require high-quality Arabica beans. In response, companies are actively developing alternative sourcing strategies and conducting comprehensive evaluations of coffee blend modifications to optimize costs. Smaller manufacturers, constrained by limited purchasing power, face intensifying challenges in maintaining market competitiveness against large companies that possess greater financial resources to absorb price fluctuations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Cans Maintain Dominance While Bottles Gain Momentum

Cans dominate Japan's RTD coffee market with a commanding 50.86% share in 2025, continuing their legacy since UCC's groundbreaking introduction of canned coffee in 1969. Japan's network of approximately 3.93 million vending machines, as reported by the Japan Vending Machine Manufacturers Association in 2023, enables consumers to purchase hot and cold coffee throughout the year . Japanese consumers demonstrate strong loyalty to canned coffee, purchasing an average of 100 units annually through vending machines and convenience stores, underscoring the format's deep-rooted position in daily consumption patterns.

The bottle segment (PET and glass) demonstrates robust growth potential with a projected 4.98% CAGR from 2026 to 2031, driven by increasing consumer demand for resealable packaging that ensures product freshness and flexibility in consumption. Besides, glass bottles have established a strong presence in the premium segment, particularly for cold brew and specialty coffee offerings, capturing the attention of discerning consumers who value superior quality and sophisticated packaging presentation.

By Product Type: Cold Brew Challenges Iced Latte Dominance

Iced latte and cappuccino products dominate 54.25% of the RTD coffee market share in 2025. These beverages capture mainstream consumer interest through their well-established taste profiles and premium milk-based formulations. The segment's market leadership reflects Japanese consumers' strong preference for creamy, balanced coffee beverages that minimize bitterness while delivering optimal caffeine benefits. Industry leaders BOSS Coffee (Suntory) and Georgia (Coca-Cola Japan) maintain substantial market presence through continuous product innovation and strategic marketing investments.

Cold brew RTD coffee exhibits exceptional growth at 5.62% CAGR (2026-2031). This expansion is primarily driven by younger consumers who value its distinctive, smooth, less acidic profile and enhanced caffeine content. The segment's market success is amplified by its established health advantages, including significantly reduced acidity and clean ingredient composition.

By Flavor Profile: Flavored Variants Disrupt Classic Dominance

Plain/classic coffee flavors dominate the Japanese market with a 61.05% share in 2025, underscoring the nation's deep-rooted appreciation for authentic coffee experiences. This significant market presence stems from Japan's sophisticated coffee culture, where consumers place high value on quality, craftsmanship, and traditional brewing methods. Black unsweetened varieties have gained substantial momentum, particularly among health-conscious consumers and coffee connoisseurs who seek pure, unaltered flavor experiences.

The flavored ready-to-drink (RTD) coffee segment demonstrates robust growth potential with a projected CAGR of 6.15% from 2026 to 2031. This expansion is fueled by younger demographics actively seeking diverse taste experiences, coupled with manufacturers' continuous investment in flavor innovation. The segment's evolution encompasses carefully curated seasonal limited editions and sophisticated fusion flavors that harmoniously blend coffee with complementary taste elements. Advanced flavor technology enables manufacturers to develop more refined and authentic taste profiles, while the strategic integration of local and international flavor trends allows companies to establish unique market positions in this dynamic segment.

By Ingredient Base: Plant-based Alternatives Challenge Dairy Dominance

Dairy-based RTD coffee products dominate the Japanese market with an 79.35% share in 2025. This dominance reflects established consumer preferences and Japan's extensive dairy processing infrastructure. The combination of rich texture and coffee flavor enhancement through dairy remains appealing to consumers, particularly in traditional formats like café au lait and milk coffee available in vending machines and convenience stores. Major companies like Georgia (Coca-Cola Japan) and BOSS (Suntory) have established their core product lines around dairy-based varieties, strengthening consumer confidence in this segment.

Plant-based milk alternatives in the RTD coffee segment are witnessing significant growth, with a projected CAGR of 8.17% from 2026 to 2031. This momentum is fueled by a rising focus on health and wellness, increasing rates of lactose intolerance, and growing consumer awareness of environmental sustainability. Technological advancements in emulsification and flavor-masking have played a key role in improving the taste and texture of plant-based RTD coffees, making them more appealing to mainstream consumers. Among the various alternatives, oat milk stands out due to its naturally creamy mouthfeel and neutral flavor profile, which harmonizes well with coffee. The expanding availability of plant-based offerings across convenience stores and e-commerce platforms further supports their integration into daily consumption habits.

By Distribution Channel: Online Retail Disrupts Traditional Channels

Convenience/grocery store retailers dominate RTD coffee distribution, capturing 47.72% market share in 2025. In Japan, convenience stores function as the primary distribution channel for RTD coffee, offering both refrigerated and ambient products that meet consumer demand for mobility and accessibility. According to the Ministry of Economy, Trade and Industry, Japan had over 56 thousand convenience stores in 2023 . These retail outlets operate as strategic distribution points for RTD coffee, implementing seasonal variants and store-specific products to maintain customer retention and stimulate product experimentation.

Additionally, online retail emerges as the fastest-growing distribution channel, achieving an 8.03% CAGR from 2026 to 2031, propelled by fundamental shifts in consumer purchasing behavior and accelerating digital adoption rates. E-commerce platforms deliver unprecedented access to an extensive range of RTD coffee products, encompassing both mainstream and premium offerings unavailable in traditional retail environments. Subscription-based RTD coffee delivery services are gaining significant momentum, particularly resonating with urban millennials who prioritize convenience and product exploration. Major manufacturers are strategically expanding their direct-to-consumer capabilities while simultaneously developing robust partnerships with established e-commerce platforms to maximize market penetration and capitalize on emerging growth opportunities.

By Price Positioning: Premium Segment Outpaces Mass Market Growth

Mass-market RTD coffee products dominate with 69.65% of sales in 2025, offering cost-effective options for daily consumption. This segment maintains its market leadership through robust distribution networks, particularly through strategically placed vending machines and convenience stores, ensuring maximum consumer reach. Major manufacturers, including Asahi, Suntory, and Coca-Cola Japan, engage in intense market competition through strategic pricing, targeted promotional campaigns, and continuous product innovations.

Premium RTD coffee demonstrates strong growth potential with a 6.04% CAGR (2026-2031), fueled by increasing consumer preferences for superior quality, distinctive flavor profiles, and enhanced functional benefits. The segment shows significant expansion in specialty coffee variants, carefully selected single-origin offerings, and products featuring clean label certifications. Rising disposable incomes and a sophisticated coffee culture among Japanese consumers continue to drive market growth. Manufacturers are investing in premium product portfolios, emphasizing sustainable sourcing practices, innovative brewing technologies, and premium packaging solutions to meet evolving consumer demands.

Geography Analysis

Tokyo dominates Japan's RTD coffee market with an 18.10% share in 2025, driven by its strategic advantages in population density, comprehensive vending machine networks, and concentration of office workers. The prefecture's fast-paced urban environment generates substantial demand for convenient caffeine solutions, particularly among time-conscious commuters and professionals. As a market trendsetter, Tokyo significantly influences national consumption patterns, with manufacturers prioritizing the capital for new product launches to capitalize on its sophisticated consumer preferences. The prefecture's extensive convenience store infrastructure, encompassing major chains like Lawson, FamilyMart, and 7-Eleven, forms a robust distribution network alongside vending machines. The market continues to evolve with innovative offerings, including premium single-origin selections and functional RTD coffee variants designed for health-conscious urban professionals.

Kanagawa prefecture demonstrates exceptional market potential with a projected 4.16% CAGR from 2026 to 2031, leveraging its strategic location near Tokyo and demographically advantageous younger population base. The ongoing development of urban infrastructure and expansion of business districts in Yokohama create multiple consumption opportunities across various channels. The prefecture's manufacturing capabilities are exemplified by Moriyama's advanced facility, which utilizes SIG's cutting-edge filling technology for premium RTD products, including organic coffee in aseptic carton packaging. Kanagawa's competitive living costs relative to Tokyo attract a younger consumer demographic, driving demand for innovative RTD coffee formats. The prefecture's distinctive coastal setting and popular recreational destinations generate significant seasonal demand for cold RTD coffee products, particularly during the summer tourism peak, contributing to sustained market growth.

Moreover, Osaka's RTD coffee market demonstrates consistent demand, primarily through convenience stores and train station retail locations serving urban professionals and students. Lawson's store-exclusive "UCC Black" canned coffee maintains strong sales performance during peak commuting hours, indicating consumer adoption of convenient beverage options. The city's comprehensive transit infrastructure facilitates RTD coffee distribution through these strategic retail points.

Competitive Landscape

The Japan RTD coffee market is moderately consolidated, with a few key players like Coca-Cola Japan (Georgia), Suntory, Asahi, and Kirin holding significant market shares. These companies leverage deep distribution networks, strong brand equity, and frequent product innovation to maintain their competitive positions. For instance, Suntory's BOSS brand maintains a significant market share in Japan's ready-to-drink coffee segment, distributing products ranging from low-sugar formulations to premium latte varieties through its vending machine infrastructure. UCC, the original manufacturer of canned coffee in Japan, sustains its market presence through product innovations that address evolving consumer demands.

While niche and regional brands continue to emerge, the dominance of established players in vending machines and convenience stores limits their overall impact. The market exhibits high entry barriers due to logistics, vending infrastructure, and consumer loyalty to legacy brands. As a result, competition is active but largely concentrated within a core group of large firms.

Moreover, digital technology integration and premium product development influence market dynamics. Nestlé Japan implements connected machines and digital loyalty programs for personalized solutions. Market demand for café-style beverages drives manufacturers to produce premium ready-to-drink lattes and cold brews. Companies adjust product formulations and distribution strategies to meet consumer preferences in Japan's ready-to-drink coffee market.

Japan Ready-to-Drink (RTD) Coffee Industry Leaders

-

Asahi Group Holdings, Ltd.

-

The Coco-Cola Company

-

Suntory Holdings Limited

-

UCC Ueshima Coffee Co., Ltd.

-

Nestlé S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Meiji expanded its beverage portfolio by launching a ready-to-drink (RTD) coffee beverage with whole oats under its Meiji Marugoto Oats product line. The formulation incorporates 6% whole oat flour and 12 g of whole grain oats per unit, delivering dietary fiber and beta-glucan content. The product is available in 200 ml cartons at JPY 162.

- September 2024: Starbucks Japan launched a ready-to-drink Pumpkin Spice Latte variant in 200 ml chilled cups through its convenience store distribution network nationwide. The product, priced at JPY 219, represents a strategic collaboration with Suntory that incorporates the traditional pumpkin and spice flavor profile. This seasonal product extension enables market penetration beyond Starbucks retail outlets.

- August 2024: Costa Coffee, the UK's largest café chain operator, established operations in Japan through a joint venture (JV) with Sojitz Royal Café. The partnership intends to position Costa Coffee as Japan's dominant café chain. The expansion of retail locations is expected to drive sales growth across the company's ready-to-drink (RTD) coffee beverages, coffee beans, and coffee pods segments.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

In our study, Mordor Intelligence defines Japan's ready-to-drink coffee market as every packaged beverage that is brewed, cooled, and sealed in cans, PET or glass bottles, or aseptic cartons so it can be consumed immediately without additional preparation. All shelf-stable and chilled variants, whether plain, flavored, dairy, or plant-based, are included.

Scope exclusion: single-serve coffee pods and freshly brewed beverages sold through cafés lie outside our remit.

Segmentation Overview

-

By Packaging Type

-

Bottles

- Glass Bottles

- PET Bottles

- Cans

- Cartons

- Others

-

Bottles

-

By Product Type

- Cold Brew RTD Coffee

- Iced Latte/Cappuccino

- Nitro RTD Coffee

- Functional / Protein-Enhanced RTD Coffee

-

By Flavor Profile

- Plain/Classic

- Flavored

-

By Ingredient Base

- Dairy-Based

- Plant-Based Milk

-

By Price Positioning

- Mass

- Premium

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenienc/Grocery Stores

- Online Retail Stores

- Others (Vending Machine, Forecourt Stores, etc)

-

By Prefecture

- Tokyo

- Kanagawa

- Osaka

- Aichi

- Saitama

- Other Prefectures

Detailed Research Methodology and Data Validation

Primary Research

We then interviewed buying managers at convenience chains, beverage formulators, packaging suppliers, and import brokers across Kanto, Kansai, and Kyushu, and ran consumer pulse surveys in Tokyo and Osaka. These conversations clarified actual case volumes, vending price ladders, and flavor shifts, allowing us to refine base-year assumptions and narrow forecast ranges.

Desk Research

Our analysts began with broad desk work, pulling production and trade statistics from the Ministry of Finance customs portal, vending-machine counts from the Japan Vending Machine Manufacturers Association, beverage sales tables from the All Japan Coffee Association, consumer-spend data issued by the Statistics Bureau, and labeling rules from the Consumer Affairs Agency. Company filings, press releases, and news archived in Dow Jones Factiva, together with D&B Hoovers financial traces, helped us cross-check brand-level trends and price corridors.

A second sweep captured patent activity through Questel, prefecture-level retail audits shared by convenience-store bodies, and food-science journals discussing cold-brew shelf life, which sharpened our view on technology adoption and innovation intensity. The sources cited here are only illustrative; many additional references were reviewed to collect, validate, and clarify data.

Market-Sizing & Forecasting

A top-down reconstruction starts from national beverage spend, which we filter for coffee share and RTD penetration before layering channel mix and average selling prices. Select bottom-up checks, annual output reported by leading fillers and sampled wholesale invoices, anchor the totals. Key inputs include vending-machine density, per-capita coffee intake, import cost of green beans, PET versus can share, and the pace of premium launches. Forecasts rely on multivariate regression allied to scenario analysis, with vending-footprint growth and consumer-spend elasticity driving variance. Gaps in supplier disclosures are bridged with anchored ratios agreed during interviews.

Data Validation & Update Cycle

Every draft model passes two analyst reviews; variance thresholds trigger extra calls, and outputs are benchmarked against monthly retail-scanner signals. Mordor refreshes the study yearly, while material regulatory or M&A events prompt interim updates, ensuring clients receive the latest view.

Why Mordor's Japan RTD Coffee Baseline Inspires Confidence

Published estimates often diverge because firms adopt different inclusion rules, price bases, and refresh cadences, and this market is no exception.

Key gap drivers include some studies folding RTD tea into coffee totals, others freezing average prices at historic exchange rates, and a few extrapolating global growth rates without vending-machine context. Mordor isolates coffee only, applies rolling yen-to-dollar averages, and updates variables after each channel check, yielding a more dependable baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.69 B (2025) | Mordor Intelligence | - |

| USD 8.10 B (2023) | Regional Consultancy A | older base year, static pricing |

| USD 2.30 B (2024) | Industry Analytics Firm B | limited channel coverage |

| USD 1.11 B (2024) | Global Consultancy C | excludes chilled PET sales |

These comparisons show that when variables are fully aligned and transparently disclosed, Mordor's disciplined, clearly traceable process delivers a balanced figure that decision-makers can trust.

Key Questions Answered in the Report

What is the current Ready-to-Drink Coffee market size in Japan?

The Ready-to-Drink Coffee market size stands at USD 8.99 billion in 2026 and is projected to reach USD 10.67 billion by 2031.

Which product type is growing fastest in Japan’s Ready-to-Drink Coffee market?

Cold brew RTD coffee is forecast to register the highest 5.62% CAGR between 2026 and 2031, driven by demand for smoother taste and higher caffeine content.

Why are plant-based RTD coffees gaining popularity?

The plant-based alternatives market is experiencing an 8.17% CAGR, propelled by heightened consumer health awareness, increased recognition of lactose intolerance, and growing environmental considerations.

Which prefecture shows the strongest growth outlook?

Kanagawa Prefecture anticipates a 4.16% CAGR through 2031 in the RTD coffee market. The growth stems from the prefecture's young population demographics, urban infrastructure development, and manufacturing capital investments in RTD coffee production.

Page last updated on: