Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

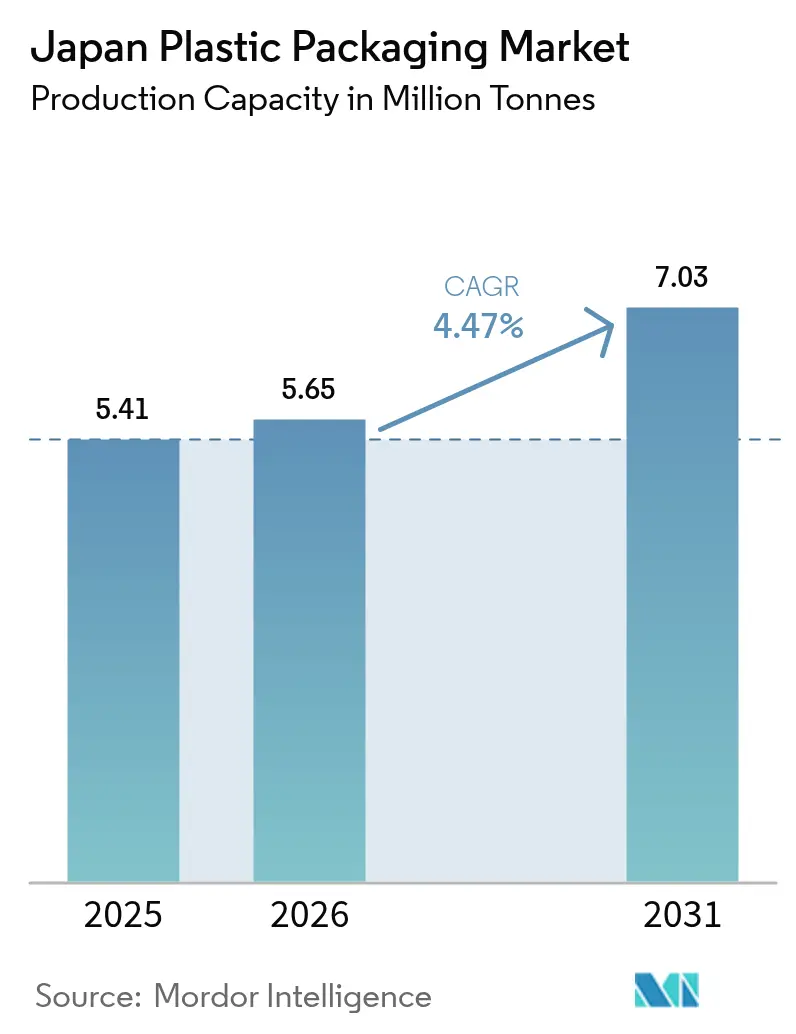

| Base Year Market Size (2025) | 5.41 Million tonnes |

| Market Volume (2026) | 5.65 Million tonnes |

| Market Volume (2031) | 7.03 Million tonnes |

| Growth Rate (2026 - 2031) | 4.47% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Plastic Packaging Market Analysis by Mordor Intelligence

The Japan plastic packaging market size was valued at 5.41 million tonnes in 2025 and estimated to grow from 5.65 million tonnes in 2026 to reach 7.03 million tonnes by 2031, at a CAGR of 4.47% during the forecast period (2026-2031). Persistent demand from e-commerce fulfillment centers, rising pharmaceutical consumption among older citizens, and brand owner commitments to circular-economy goals underpin this growth trajectory.[1]Plastic Waste Management Institute, “Plastics recycling in Japan,” pwmi.or.jp Flexible film converters capitalize on the boom in online grocery and specialty retail, while resin suppliers gain from lightweight bottle programs that stabilize PET volumes despite material-reduction targets. National subsidies for chemical-recycling pilots broaden feedstock options, yet sweeping Extended Producer Responsibility (EPR) fees intensify cost control across the value chain. Tight labor markets accelerate automation, nudging small converters toward mergers with integrated groups that can fund robotics and data-driven quality systems.

Key Report Takeaways

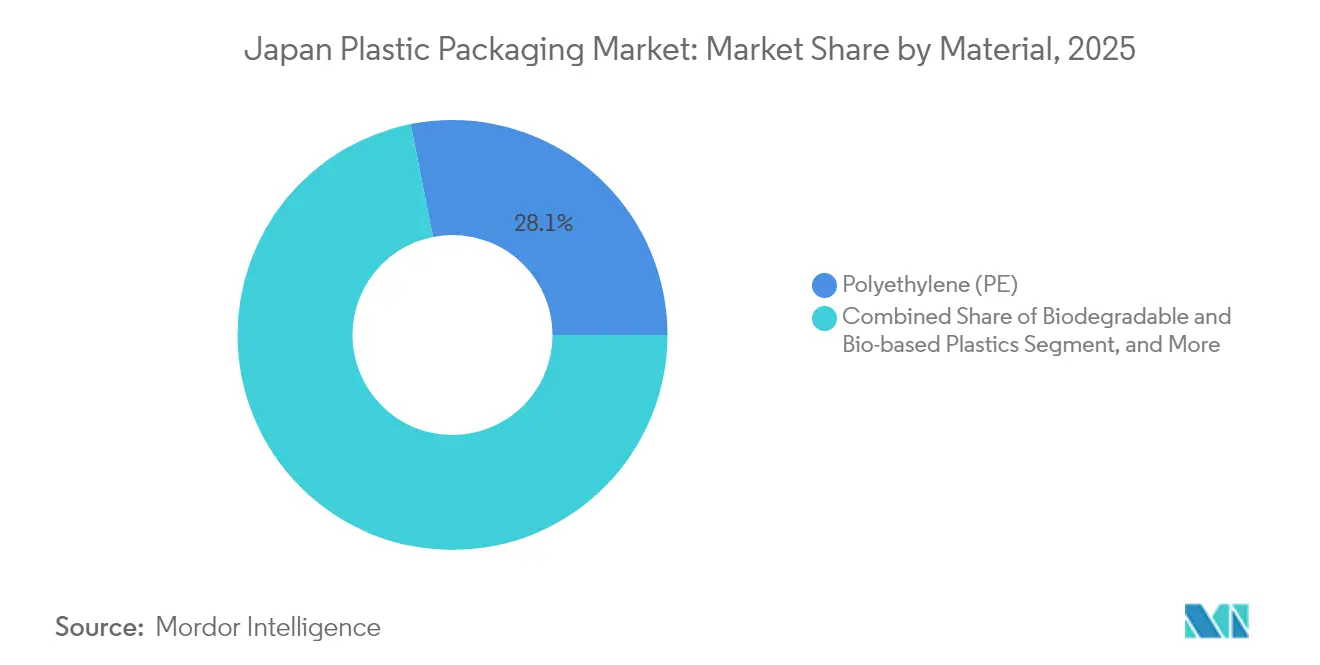

- By material, polyethylene held 28.12% of the Japan plastic packaging market share in 2025, bio-based plastics, though under 5% of tonnage today, post the fastest 4.93% CAGR through 2031.

- By type, the flexible segment accounted for 53.85% of the Japan plastic packaging market size in 2025, leads forecast growth at 5.84% CAGR through 2031.

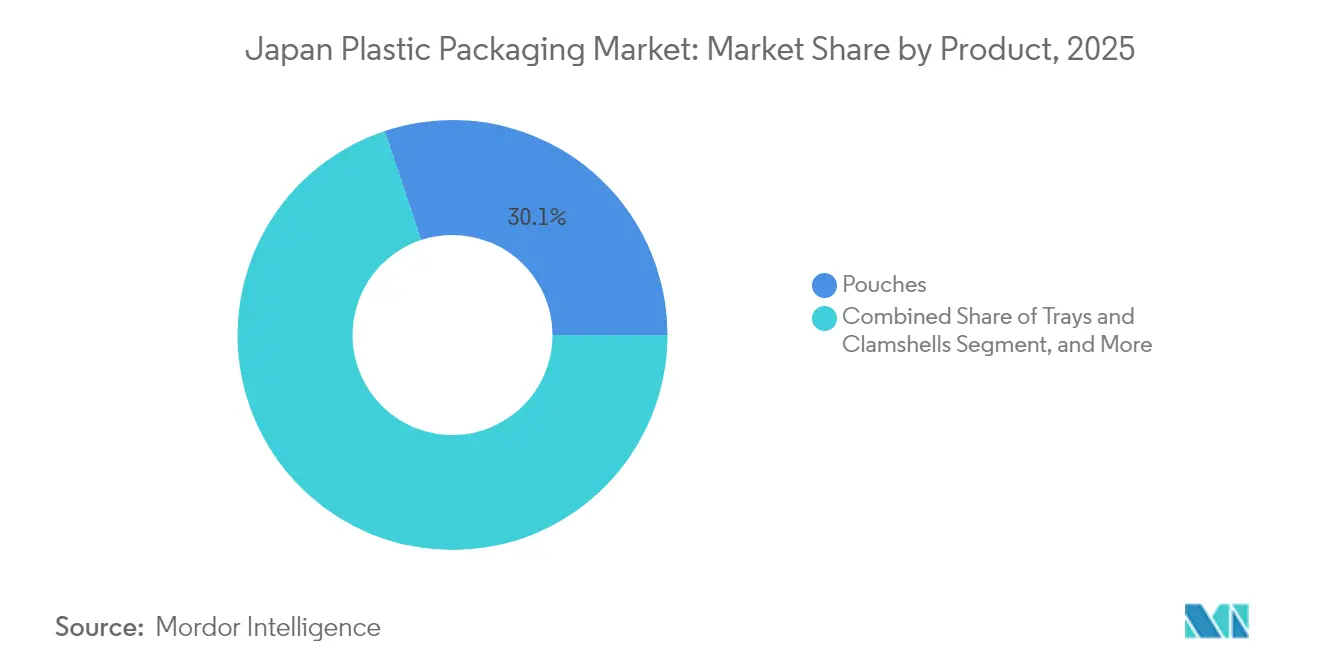

- By product, pouches led with 30.10% of the Japan plastic packaging market size in 2025, grow fastest at 5.21% CAGR through 2031.

- By end-user, food applications captured 29.10% of the Japan plastic packaging market share in 2025, personal care registers the highest 6.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Plastic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of e-commerce driving demand for high-barrier flexible packs | +0.8% | Nationwide, strongest in Tokyo–Osaka corridor | Medium term (2-4 years) |

| Ageing population escalating demand for pharma blister and pouch formats | +0.6% | Nationwide, higher in rural prefectures | Long term (≥ 4 years) |

| Beverage PET bottle lightweighting lowering cost and boosting volumes | +0.4% | Nationwide, PET hubs in Kansai and Kanto | Short term (≤ 2 years) |

| Convenience food boom raising use of retort pouches | +0.5% | Large urban areas | Medium term (2-4 years) |

| Government subsidies for chemical-recycling pilot plants | +0.3% | Chiba, Mizushima, Osaka complexes | Long term (≥ 4 years) |

| Spread of plasma-coated mono-material films for 2030 recyclability goals | +0.2% | R&D centers nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth of E-commerce Driving Demand for High-Barrier Flexible Packs

Parcel volumes handled by Japan Post and private couriers continue to set records, prompting online retailers to specify packaging that withstands multistep distribution without overpacking. Film producers answer with multi-layer structures combining EVOH and mLLDPE that deliver oxygen-barrier performance at reduced gauge, thereby trimming logistics emissions and freight cost per unit.[2]EY Japan, “Sustainable flexible plastic packaging strategy,” ey.com The result is steady volume gains for converters specialized in lamination and digital printing, solidifying the e-commerce channel as the single largest new demand node for the Japan plastic packaging market.

Ageing Population Escalating Demand for Pharma Blister and Pouch Formats

Citizens aged 65 and older now represent more than 29% of Japan’s population, lifting prescription volumes and over-the-counter supplement usage. Pharma packagers report double-digit volume growth for push-through blisters with tactile cues and easy-tear pouches that aid seniors with reduced grip strength. Regulatory reforms that encourage home-based care intensify the need for unit-dose compliance packaging, a trend that injects resilient demand into the Japan plastic packaging market.

Beverage PET Bottle Lightweighting Lowering Cost and Boosting Volumes

Domestic beverage leaders have shaved average bottle weight by roughly 20% since 2020 while maintaining shelf stability. Material savings create room for price promotions that defend market share against aluminum cans and glass. Converters benefit because unit sales climb even as resin per bottle falls, holding aggregate PET consumption roughly flat. The Japan plastic packaging market, therefore, enjoys volume insulation despite sustainability targets that emphasize material reduction.

Convenience Food Boom Raising Use of Retort Pouches

Urban consumers with busy schedules increasingly favor heat-and-eat meals from convenience stores. Retort pouches extend shelf life up to 18 months without refrigeration, freeing retailers from cold-chain space constraints. Producers adopt all-polypropylene constructions that survive 121 °C sterilization while qualifying for mono-material recycling streams. Retort demand secures an above-market growth rate for pouches, reinforcing flexible packaging leadership within the Japan plastic packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter Extended Producer Responsibility fees on single-use plastics | -0.7% | All municipalities, highest in Tokyo wards | Short term (≤ 2 years) |

| Consumer shift toward paper and glass alternatives | -0.4% | Premium retail in major cities | Medium term (2-4 years) |

| Corporate zero-plastic pledges by FMCG majors | -0.3% | Nationwide | Medium term (2-4 years) |

| Volatility in naphtha prices disrupting resin cost economics | -0.5% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stricter Extended Producer Responsibility Fees on Single-Use Plastics

Japan’s EPR law now requires brand owners to finance collection and recycling, lifting compliance outlays by up to 60% for single-use categories. As invoices arrive, food manufacturers labor to redesign packs that cut gram-weight or move toward reusable containers. The near-term burden trims profit margins and tempers volume expansion in the Japan plastic packaging market.

Consumer Shift Toward Paper and Glass Alternatives

Perception outruns science as city-center shoppers equate non-plastic with eco-friendlier. Several premium tea and confectionery brands have switched to paper pouches lined with bio-resin coatings, accepting shorter shelf life in exchange for marketing gains. While plastic remains indispensable for high-barrier needs, the shift siphons demand away from commodity film grades and forces converters to update product portfolios within the Japan plastic packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: PE Retains Scale While Bio-Based Grades Accelerate

Polyethylene held a 28.12% share of the Japan plastic packaging market size in 2025, buoyed by versatility across grocery films and industrial liners. Cost advantages and mature processing infrastructure sustain its dominance, yet decarbonization pledges push brand owners to trial drop-in bio-PE made from sugarcane ethanol. Bio-based plastics, though under 5% of tonnage today, post the fastest 4.93% CAGR and attract subsidies that close price gaps with fossil grades.

R&D groups tap cellulose nanofibers from forestry residues to engineer resins that match HDPE stiffness while offering landfill biodegradability. Resin majors aim for 20,000 tonnes of bioethanol-derived output by 2027, positioning Japan to meet the national 2 million-tonne bio-plastic target by 2030. These initiatives introduce fresh feedstocks into the Japan plastic packaging market, diversifying material supply and mitigating crude-derived volatility.

By Type: Flexible Formats Command Volume and Innovation

Flexible packaging captured 53.85% of the Japan plastic packaging market share in 2025 and leads forecast growth at 5.84% CAGR. Material-efficient films minimize freight emissions and storage space, critical for e-commerce parcel density. Advances in solvent-free lamination and digital presses shorten artwork changeovers, letting converters cater to limited-edition SKUs without costly inventory. Rigid categories such as jars and tubs soldier on in ambient staples, yet their growth trails flexible peers given higher resin intensity.

Patented layer-separation films allow post-consumer peel-off that feeds single-polymer streams, eroding recyclability disadvantages historically linked to multi-layer pouches. As national recycling targets tighten, the shift bolsters the flexible segment’s share in the Japan plastic packaging market while containing lifecycle impacts.

By Product: Pouches Outperform on Convenience and Sustainability

Pouches represented 30.10% of the Japan plastic packaging market size in 2025 and grew fastest at a 5.21% CAGR. Stand-up and spouted formats displace rigid bottles in sauces and detergents, delivering 70% lighter pack weight and 80% lower truckload CO₂ emissions. For seniors, easy-tear notches and wide openings facilitate meal preparation, tying demographic shifts to pouch adoption.

Brand owners deploy mono-PP retort pouches that survive high-temperature sterilization and flow seamlessly into material recovery facilities. Smart labels embedded in high-value pharmaceutical pouches monitor humidity, turning packaging into an active quality-control node. These attributes entrench pouches as the lead innovation engine inside the Japan plastic packaging market.

By End-User Industry: Food Dominates, Personal Care Rises

Food applications held 29.10% of the Japan plastic packaging market share in 2025, anchored by strict hygiene codes and a vibrant convenience-store ecosystem. Portion-controlled servings cater to shrinking household sizes, sustaining demand for multilayer films with gas barriers that preserve flavor without refrigeration.

Personal care registers the highest 6.18% CAGR through 2031 as cosmetics groups roll out refill pouches and airless pump packs that promise 50% plastic reduction per use. High-clarity PET jars with recycled content bolster premium positioning while meeting eco-label criteria. These gains reposition personal care from a niche to a growth locomotive in the Japan plastic packaging market.

Geography Analysis

Manufacturing of plastic packaging clusters along the Tokyo-Osaka corridor, where 70% of GDP is generated, enabling converters to tap integrated petrochemical hubs in Chiba and Mizushima for resin feedstock. Efficient Shinkansen freight and expressway arteries ensure one-day delivery to 85% of retail outlets, reducing warehousing requirements and letting brand owners run lean inventories.

Kansai hosts beverage and chemical majors that collaborate on closed-loop PET recycling, with Osaka’s plant-scale depolymerization unit targeted to process 60,000 tonnes annually by 2027. Kyushu’s government offers up to JPY 300 million investment grants (USD 2.0 million) for sustainable packaging ventures, luring dehydrated food processors that export to Southeast Asia.

Uniform national food-contact standards simplify multi-site production, yet local EPR fee schedules vary, compelling brand owners to track municipal ordinances. Inbound raw-material logistics rely on coastal petrochemical terminals, creating exposure to typhoon disruptions, which firms mitigate through dual-sourcing strategies. These geographic dynamics collectively shape supply resilience in the Japan plastic packaging market.

Competitive Landscape

The top five suppliers collectively account for roughly 42% of volume, yielding a moderately concentrated arena where scale coexists with niche specialization. Large groups such as TOPPAN, Toyo Seikan, Amcor Japan, and Toppan Printing leverage integrated extrusion, coating, and converting lines to offer one-stop solutions. Mid-tier firms carve out niches in cosmetics, sampling sachets, or high-shrink labels.

TOPPAN’s USD 1.8 billion purchase of Sonoco’s TFP division in April 2025 vaulted the firm into the global top-three flexible players and deepened high-barrier film capacity.[3]TOPPAN Holdings, “Completion of Sonoco Flexible acquisition,” toppan.com Resin makers tie up with recyclers in chemical-loop consortia, locking in feedstock and meeting Scope 3 emission targets. Strategic priorities converge on automation, with robotics trimming headcount by up to 30% at new pouch lines while boosting traceability.

Intellectual-property battles intensify around oxygen-scavenger additives and plasma coatings that enable mono-material structures. Firms co-develop voluntary carbon-footprint protocols to pre-empt regulatory mandates, turning sustainability compliance into a competitive moat within the Japan plastic packaging market.

Japan Plastic Packaging Industry Leaders

Toyo Seikan Group Holdings, Ltd.

Takemoto Yohki Co. Ltd.

Takigawa Corporation

Amcor Group

Toppan Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Bio-X and Anipitaru formed an equity partnership to deploy heat-resistant PLA for veterinary medical tools and pet accessories.

- April 2025: TOPPAN concluded its USD 1.8 billion acquisition of Sonoco’s TFP business, expanding high-barrier film output across Asia and Europe.

- March 2025: Idemitsu Kosan and Mitsui Chemicals began studying consolidation of one Chiba ethylene unit to uplift asset utilization and curb CO₂ emissions by 15%.

- February 2025: Resonac secured JPY 8 billion (USD 54 million) from NEDO’s Green Innovation Fund to scale chemical recycling of mixed-plastic waste.

Japan Plastic Packaging Market Report Scope

Lightweight plastic cuts down on transportation costs and energy consumption. Its durability safeguards products from damage during shipping and handling. By forming a barrier against moisture, air, and contaminants, plastic packaging not only keeps food and other items fresh but also extends their shelf life. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

Japan Plastic Packaging Market is Segmented by Type (Rigid Plastic, Flexible Plastic), by End-User Industry (Food, Beverage, Healthcare, Personal Care and Household), and by Products (Bottles, Jars, Pouches, Trays, Containers, Bags, Films, Wraps). The Market Sizes and Forecasts are Provided in Terms of Volume (Tonnes) for all the Above Segments.

By Material

| Polyethylene Terephthalate (PET) | |

| Polyethylene (PE) | High-Density Polyethylene (HDPE) |

| Low-Density and Linear-LDPE | |

| Linear Low-Density Polyethylene (LLDPE) | |

| Polypropylene (PP) | |

| Bio-based Plastics | |

| Other Materials |

By Type

| Rigid Plastic |

| Flexible Plastic |

By Product

| Bottles and Jars |

| Cans |

| Pouches |

| Trays and Clamshells |

| Caps and Closures |

| Other Products |

By End-User Industry

| Food |

| Beverage |

| Healthcare and Pharmaceuticals |

| Retail and E-commerce |

| Industrial Manufacturing |

| Personal Care and Household |

| Other End-User Industries |

| By Material | Polyethylene Terephthalate (PET) | |

| Polyethylene (PE) | High-Density Polyethylene (HDPE) | |

| Low-Density and Linear-LDPE | ||

| Linear Low-Density Polyethylene (LLDPE) | ||

| Polypropylene (PP) | ||

| Bio-based Plastics | ||

| Other Materials | ||

| By Type | Rigid Plastic | |

| Flexible Plastic | ||

| By Product | Bottles and Jars | |

| Cans | ||

| Pouches | ||

| Trays and Clamshells | ||

| Caps and Closures | ||

| Other Products | ||

| By End-User Industry | Food | |

| Beverage | ||

| Healthcare and Pharmaceuticals | ||

| Retail and E-commerce | ||

| Industrial Manufacturing | ||

| Personal Care and Household | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

What is the current volume of the Japan plastic packaging market?

The market totals 5.65 million tonnes in 2026.

How fast will the sector grow through 2031?

Forecast calls for a 4.47% CAGR, taking volumes to 7.03 million tonnes.

Which packaging type is expanding quickest?

Flexible formats lead at a 5.84% CAGR owing to e-commerce and convenience-food demand.

Why are pouches gaining popularity among brand owners?

They reduce pack weight by 70%, cut logistics emissions, and now offer mono-material recyclability.

How do EPR fees influence material choice?

Higher fees on single-use plastics push companies to down-gauge films or shift to reusable and recyclable formats.

Page last updated on: