Non-stick Coatings Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2 Billion |

| Market Size (2031) | USD 2.38 Billion |

| Growth Rate (2026 - 2031) | 3.56% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Non-stick Coatings Market Analysis by Mordor Intelligence

The Non-stick Coatings Market size is projected to expand from USD 1.93 billion in 2025 and USD 2 billion in 2026 to USD 2.38 billion by 2031, registering a CAGR of 3.56% between 2026 to 2031. Continuing migration toward PFOA-free ceramics, widening industrial machinery adoption, and fresh capacity additions in water-based fluoropolymers are sustaining steady volume growth even as raw-material inflation trims margins at leading suppliers. Asia-Pacific maintains its demand edge on the back of Chinese appliance exports and India’s pharmaceutical equipment roll-outs, while Europe and North America pivot to low-VOC chemistries in response to tightening air-quality rules. Global feedstock pressures stemming from fluorspar constraints in Mongolia and Mexico have raised costs by two to three percentage points for fluoropolymer producers, yet market participants continue to prioritize performance niches, electronics, medical devices, and precision-engineered machinery, where switching costs are high. Competitive dynamics remain moderate; the five largest vendors command roughly 60% of installed capacity, leaving room for regional ceramic and sol-gel specialists to gain share through faster product cycles and lower entry prices.

Key Report Takeaways

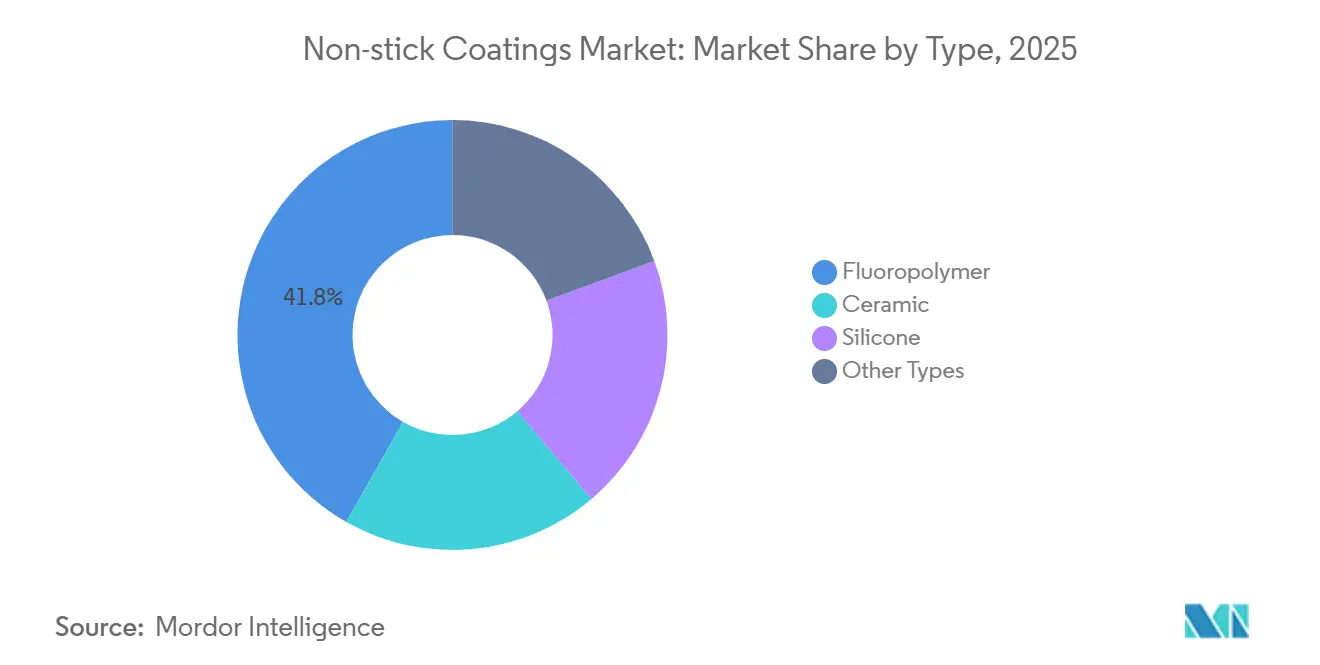

- By type, fluoropolymers led the non-stick coatings market with 41.78% of the market share in 2025. By type, ceramic coatings are projected to log the fastest 3.71% CAGR during the forecast period (2026-2031).

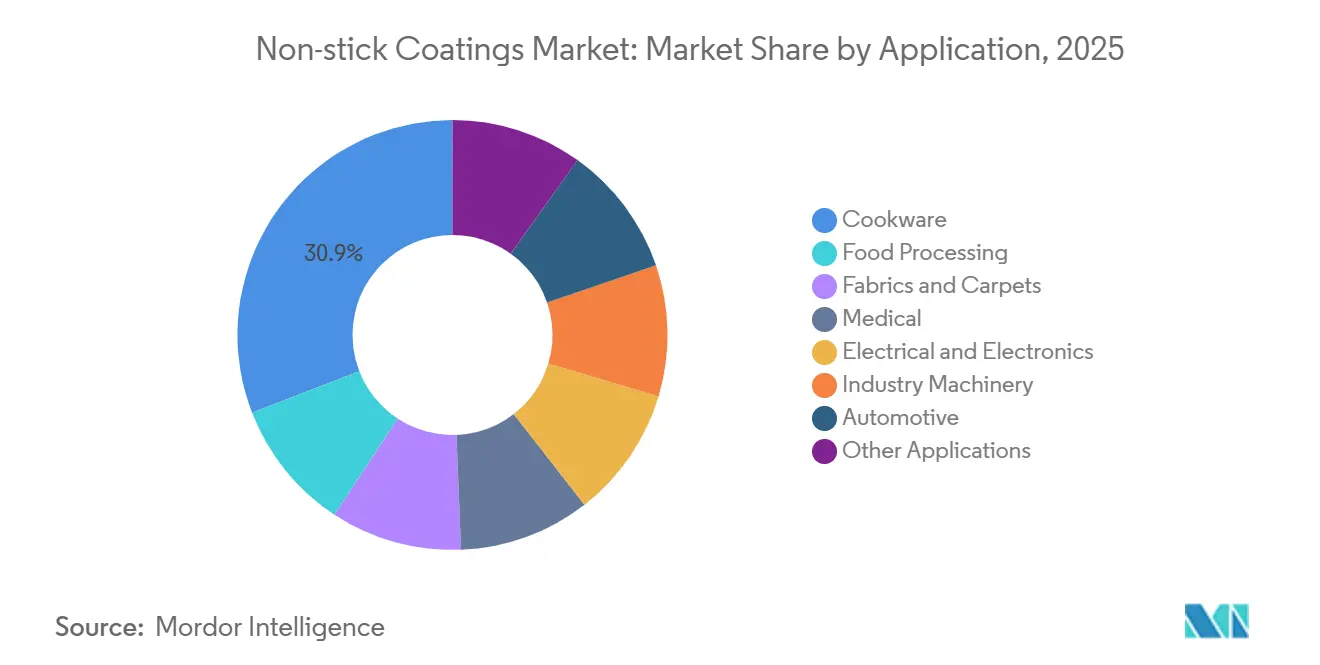

- By application, cookware captured 30.89% share of the non-stick coatings market size in 2025, whereas industrial machinery is set to expand at a 3.82% CAGR during the forecast period (2026-2031).

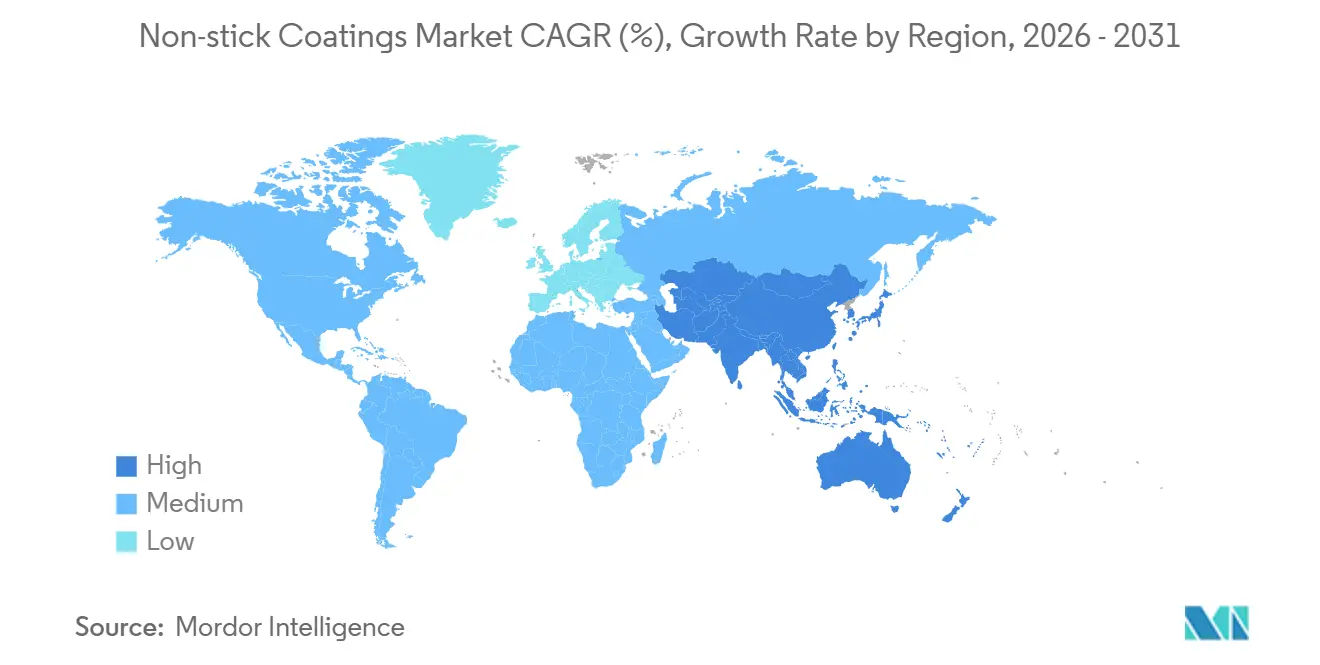

- By geography, the Asia-Pacific region commanded a 50.12% revenue share in 2025 and is also anticipated to post the highest CAGR of 3.62% during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Non-stick Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Industrial machinery and food-processing uptake | +0.8% | Global, with concentration in APAC and North America | Medium term (2-4 years) |

| Regulation-driven shift to PFOA-free ceramics | +0.7% | Europe and North America, spillover to APAC | Short term (≤ 2 years) |

| Electronics and medical-device adoption (precision coatings) | +0.6% | APAC core (Taiwan, South Korea, Japan), North America | Medium term (2-4 years) |

| Water-based low-VOC fluoropolymer dispersions | +0.5% | North America and Europe, early adoption in China | Long term (≥ 4 years) |

| Emerging nano-textured omniphobic top-coats | +0.4% | Global, led by industrial and medical segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Industrial Machinery and Food-Processing Uptake

Demand from food-processing equipment is elevating the industrial machinery slice of the non-stick coatings market at a 3.82% annual pace through 2031, as dairy plants in the Netherlands and U.S. meat processors retrofit stainless-steel conveyors with ceramic matrices that tolerate caustic wash cycles up to pH 12[1]PPG Industries, “Annual Report 2025,” ppg.com. Textile calendering lines in India and Vietnam now specify fluoropolymer-silicone hybrids to counter fabric adhesion during heat-setting, a need amplified by higher surface energy in recycled polyester blends. Pharmaceutical tooling is another pull factor; Daikin logged a 40% year-over-year rise in PTFE release-coating orders during 2025 from Indian tablet-press OEMs aiming to raise throughput without excipient reformulations. Chemours commissioned a USD 35 million PTFE dispersion line in Corpus Christi, Texas, in early 2026 to capture these food-contact and industrial accounts. Higher average selling prices, three to five percentage points above cookware grades, continue to attract incremental capacity investment across APAC and North America.

Regulation-Driven Shift to PFOA-Free Ceramics

Europe’s REACH roadmap and the US EPA’s hazardous-substance listing for long-chain PFAS in 2024 have accelerated ceramic and sol-gel trials that remove fluorine entirely. Germany’s Federal Institute for Risk Assessment advised cookware brands in late 2025 to phase out all long-chain PFAS by 2028, spurring retailers such as IKEA and Carrefour to delist PTFE-coated pans across European hubs. Ceramic offerings anchored in silicon dioxide and aluminum oxide are winning cookware share at a 3.71% CAGR, yet dishwasher shock induces failure rates two to three times higher than PTFE benchmarks, underscoring a durability gap. Solvay responded with a EUR 20 million pilot plant in Lyon to engineer ceramic formulations that mimic fluoropolymer release without fluorine. Compliance frameworks, ISO 21067 and FDA 21 CFR 175.300, are shaping R&D timelines as firms seek to avoid the costs that accompanied the prior PFOA withdrawal.

Electronics and Medical-Device Adoption (Precision Coatings)

Semiconductor packaging houses in Taiwan specify Chemours’ FEP dispersions for 5G heat spreaders that face thermal swings from -40°C to 150°C, conditions under which ceramic coatings delaminate[2]The Chemours Company, “Press Release October 2025,” chemours.com. Medical-device OEMs in Germany and the United States deploy sub-10 μm PTFE coatings on catheter guidewires, exploiting friction coefficients below 0.1 to minimize tissue trauma. Showa Denko’s nano-textured omniphobic layer, launched in mid-2025, achieved water and oil contact angles above 150°C, reducing biofilm adhesion by 60% in endoscope channels versus uncoated stainless steel. Precision coatings sell at price premiums of three to five times cookware grades, yet FDA 510(k) registrations add 12-18 months to commercialization cycles, extending payback horizons. Suppliers willing to navigate the regulatory gauntlet secure long-term margins insulated from commodity price swings.

Water-Based Low-VOC Fluoropolymer Dispersions

California’s 50 g/L VOC cap and parallel EU directives are channeling demand toward aqueous fluoropolymer systems. AGC boosted Fluon ETFE dispersion output by 30% at its Chiba site in 2025, targeting automotive underbodies that must blend corrosion protection with solvent-free compliance. 3M reformulated its Dyneon PTFE line with non-ionic surfactants that hold colloidal stability from pH 6 to 11, slicing customer defect claims by 40% in 2025. Water-based chemistries trim solvent costs yet introduce dispersion-stability challenges that raise spray-line rejection rates, cutting one to two points from supplier gross margins. Still, environmental permit advantages open doors across China’s Yangtze River Delta, where solvent systems were barred from new food-processing plants starting January 2025.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Micro-plastic and micro-fragment health perception | -0.5% | Europe and North America, emerging in APAC | Short term (≤ 2 years) |

| Fluorspar-supply and price shocks | -0.4% | Global, acute in fluoropolymer supply chains | Medium term (2-4 years) |

| Low-cost sol-gel entrants intensifying price competition | -0.3% | Europe and China, limited in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Micro-Plastic and Micro-Fragment Health Perception

Public unease about micro-particle shedding from aged cookware lifted US web searches for “PFAS-free cookware” by 180% year-over-year in 2025. A German study detected 1-50 μm fluoropolymer fragments in dishwasher effluent, prompting retailers in Germany and the Netherlands to require third-party abrasion testing that limits shedding to below 5 mg per 1,000 wash cycles. Ceramic suppliers emphasize inorganic safety profiles, yet consumer watchdogs have confirmed comparable aluminum-oxide particle release when ceramic surfaces face high-abrasion cleaning regimes. Regulatory bodies have not set exposure limits, leaving perception rather than policy to drive brand decisions in the non-stick coatings market. The concern skews toward consumer cookware, leaving B2B industrial and medical channels relatively insulated from near-term volume impact.

Fluorspar-Supply and Price Shocks

Acid-grade fluorspar spot prices climbed from USD 450 per metric ton in early 2024 to USD 720 by mid-2025 after mine closures in Mongolia and Chinese export quotas tightened supply. Chemours disclosed a USD 18 million cost hit in Q3 2025, implementing a 6% price rise on PTFE dispersions that flowed through to downstream buyers. Mexican mines raised output 12% during 2025, yet logistics bottlenecks and lower ore grade blunted the offset benefits. Daikin moved early in 2026, locking in a five-year offtake at USD 580 per ton with a Mongolian supplier, shielding its chain against future spikes. Persistent feedstock uncertainty nudges low-temperature food-contact users toward ceramics or sol-gels, but mission-critical electronic and medical segments continue to tolerate higher fluoropolymer prices given performance imperatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Fluoropolymers Anchor Value, Ceramics Capture Growth

Fluoropolymers held 41.78% of the non-stick coatings market in 2025, sustained by industrial, electronics, and medical users that require thermal stability beyond 260°C and chemical inertness against aggressive media. Ceramic variants are climbing at a 3.71% CAGR during the forecast period (2026-2031) as cookware brands seek PFOA-free solutions to align with European and US consumer sentiment. Silicone matrices occupy a niche in bakeware and textile applications owing to flexible cure profiles, but lack the abrasion endurance needed for high-throughput food-processing lines. Sol-gel hybrids and polyimide films are making inroads into aerospace fasteners and wafer-handling tools, pairing non-stick traits with tolerance for vacuum or extreme cycling.

Daikin’s ceramic-reinforced PTFE composite, launched in 2025, aims to bridge performance gaps by embedding ceramic particulates in a PTFE backbone, lifting wear life without sacrificing low friction. Ceramic layers, though fluorine-free, still face brittle-fracture risks under dishwasher thermal shock, prompting some retailers to recommend hand-wash care labels. Silicone offerings remain limited to bakeware temperatures below 200°C and soften under continuous high heat, curbing uptake in industrial ovens. Sol-gel pilot lines in Spain and Italy advertise 20-30% lower cost positions but must close adhesion gaps, now 25% under PTFE controls in accelerated corrosion tests, before large-scale industrial deployment.

By Application: Industrial Machinery Outpaces Cookware

Cookware delivered a 30.89% share of the non-stick coatings market size in 2025, but industrial machinery is advancing at a 3.82% CAGR during the forecast period (2026-2031) as food-processing and pharmaceutical tooling retrofit toward FDA-compliant release surfaces. Food processors in the Netherlands and the US Midwest integrate ceramic matrices on conveyors that endure alkaline cleaning above pH 12, while Indian and Vietnamese textile calenders shift to fluoropolymer-silicone hybrids to reduce polyester sticking. Medical devices deploy ultra-thin PTFE layers under 10 μm to secure friction coefficients below 0.1, aiding minimally invasive procedures. Electronics demand surges as 5G base-station heat sinks require dielectric coatings with thermal conductivity over 0.25 W/m·K, specifications that ceramic alternatives cannot yet meet.

Automotive underbody adoption of water-based ETFE dispersions is climbing in response to 50 g/L VOC ceilings, though lightweighting toward aluminum narrows coated surface area. Aerospace fasteners and laboratory equipment explore omniphobic nano-textures that cut cleaning chemical consumption by half in high-fat processing lines. Chemours posted a 40% year-over-year rise in PTFE orders from Indian tablet-press OEMs in 2025, underscoring superior margins, three to five points above cookware, within the industrial slice of the non-stick coatings market.

Geography Analysis

Asia-Pacific captured a 50.12% share in 2025 and is widening at 3.62% to 2031 as Chinese appliance exports, Indian pharmaceutical equipment, and Japanese semiconductor packaging spur specialized coating demand. China’s Yangtze River Delta banned solvent-based coatings in new food-processing projects from January 2025, accelerating water-based PTFE and ceramic uptake that dovetails with regional environmental goals. India’s generic-drug expansion raised Daikin’s PTFE tooling orders by 40% in 2025, reflecting throughput priorities across contract manufacturing organizations. Japanese fabs in Kyushu turn to high-purity FEP dispersions for 5G modules, where delamination can cripple thermal pathways.

North America confronts PFOA phase-outs and stringent VOC limits simultaneously. US cookware brands pilot ceramic lines, while industrial users qualify water-based dispersions that bypass solvent permits. Fluorspar output gains of 12% in Mexican mines could not fully offset Chinese quota-driven shortages, leaving fluoropolymer raw materials elevated through 2025. Dairy and meat processors retrofit ceramic matrices on stainless conveyors to meet caustic cleaning regimes, pushing equipment OEMs to retool spray lines for ceramic compatibility.

Europe leads PFAS-free reformulation after ECHA’s blanket PFAS restriction proposal in February 2025. Retailer delistings in Germany and France forced cookware suppliers to accelerate ceramic adoption, while Solvay’s EUR 20 million Lyon pilot plant focuses on matching PTFE release in fluorine-free matrices. Spain and Italy emerge as sol-gel hubs thanks to lower-temperature cure ovens and EU sustainability incentives, though adhesion deficits remain under accelerated corrosion tests. Nordic wind-turbine OEMs test omniphobic coatings to deflect ice and salt accumulation, a high-value niche with performance-based pricing power.

South America and Middle East-Africa contribute smaller but rising volumes. Brazil’s food-processing complexes adopt non-stick coatings on mixers to reduce lubricant migration, while UAE pharmaceutical plants specify FDA-grade PTFE releases for tablet presses. Argentina’s textile mills weigh silicone release layers but face currency swings that curb capital spend. Saudi Arabia’s Vision 2030 industrial diversification pushes demand for corrosion-resistant fluoropolymers in petrochemical assets, yet reliance on imported dispersions exposes buyers to freight volatility.

Competitive Landscape

The Non-Stick Coatings Market is moderately concentrated. Regional challengers intensify price pressure. Zhejiang Pfluon Technology exports sol-gel-coated pans under USD 20, cutting into incumbent shelf space across Southeast Asia and the Middle East. Technology upgrades provide defense levers: AGC’s aqueous ETFE capacity uplift and 3M’s surfactant overhaul trimmed defect rates, improving bid win ratios in automotive and industrial machinery contracts. Emerging omniphobic nano-textures offer a premium niche, but scaling costs remain high, leaving incumbents with capital breadth positioned to absorb early investment curves and preserve profitability within the non-stick coatings market.

Non-stick Coatings Industry Leaders

The Chemours Company

PPG Industries, Inc.

DAIKIN INDUSTRIES, Ltd.

3M

Solvay

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Stahl introduced Artisan Schild, featuring PEEK technology that revolutionizes non-stick cooking for modern Indian homes. Stahl’s Artisan Schild cookware features a next-generation, nearly indestructible non-stick coating with exceptional hardness and scratch resistance.

- May 2024: IKEA launched HEMKOMST, MIDDAGSMAT, and HUSKNUT, new products in the cookware range, including pans and pots, with a ceramic non-stick coating called sol-gel. Sol-gel consists mostly of silica and is created by applying a gel-like solution to the product and drying it in an oven to a hard, glossy surface with non-stick properties.

Global Non-stick Coatings Market Report Scope

Non-stick coatings are a type of coating that is applied to various surfaces to reduce the adherence between the surface and other materials. These coatings reduce the ability of other materials to stick to the engineered surface where the non-stick coating has been applied. The product is extensively used across various applications, including cookware, food processing, textiles, medical, and automotive.

The non-stick coatings market is segmented by type, application, and geography. By type, the market is segmented into fluoropolymer, ceramic, silicone, and other types (PTFE, quartz, eclipse, and others). By application, the market is segmented into cookware, food processing, fabrics and carpets, medical, electrical and electronics, industrial machinery, automotive, and other applications (textiles, aerospace, and others). The report also covers the market size and forecasts for the non-stick coatings market in 20 countries across major regions, such as Asia-Pacific, North America, Europe, South America, the Middle East, and Africa. For each segment, the market sizing and forecasts have been done based on value (USD).

| Fluoropolymer |

| Ceramic |

| Silicone |

| Other Types |

| Cookware |

| Food Processing |

| Fabrics and Carpets |

| Medical |

| Electrical and Electronics |

| Industry Machinery |

| Automotive |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordic | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| Turkey | |

| UAE | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Fluoropolymer | |

| Ceramic | ||

| Silicone | ||

| Other Types | ||

| By Application | Cookware | |

| Food Processing | ||

| Fabrics and Carpets | ||

| Medical | ||

| Electrical and Electronics | ||

| Industry Machinery | ||

| Automotive | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordic | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| Turkey | ||

| UAE | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected global value for non-stick coatings in 2031?

The non-stick coatings market is forecast to reach USD 2.38 billion by 2031.

Which formulation currently leads worldwide demand?

Fluoropolymers held 41.78% of global demand in 2025, making them the leading formulation type.

Which application segment is expanding fastest through 2031?

Industrial machinery coatings are growing at a 3.82% CAGR thanks to food-processing, pharmaceutical, and textile equipment retrofits.

Why are ceramic coatings gaining ground in cookware?

Retailer delistings of PFAS-based pans and European REACH proposals are steering cookware brands toward PFOA-free ceramic alternatives.

How are supply shortages influencing fluoropolymer pricing?

Tight fluorspar availability lifted acid-grade feedstock prices to USD 720/ton in 2025, prompting fluoropolymer suppliers to pass through 6% price increases.

Page last updated on: