Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.35 Billion |

| Market Size (2026) | USD 4.57 Billion |

| Market Size (2031) | USD 5.87 Billion |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

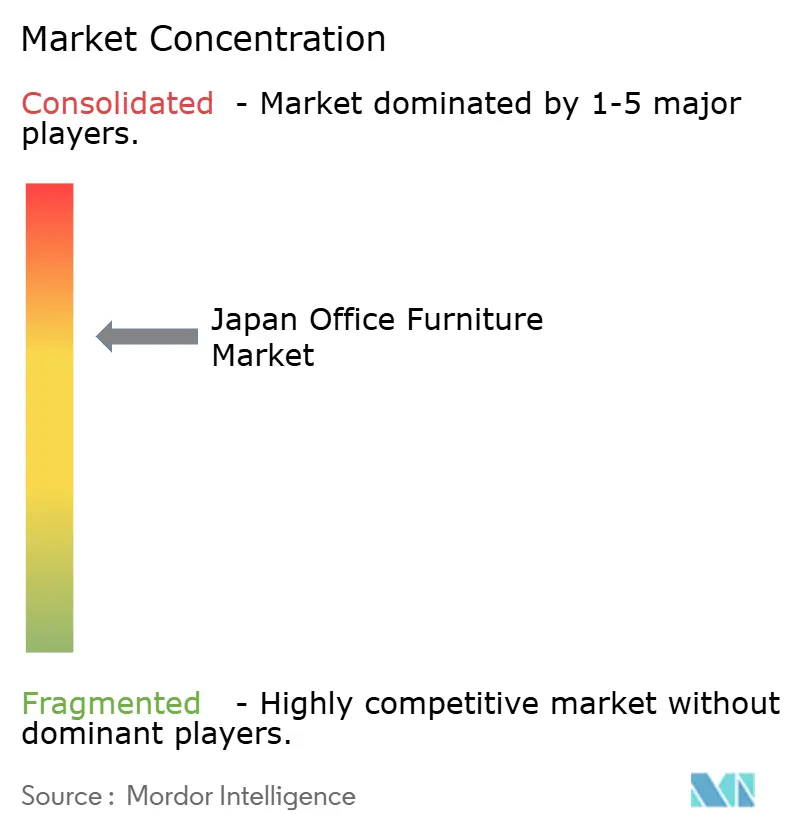

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Office Furniture Market Analysis by Mordor Intelligence

Japan Office Furniture Market size in 2026 is estimated at USD 4.57 billion, growing from 2025 value of USD 4.35 billion with 2031 projections showing USD 5.87 billion, growing at 5.12% CAGR over 2026-2031.

Hybrid work models, government telework incentives, and activity-based working (ABW) layouts are reshaping purchasing criteria toward flexible, technology-enabled furnishings that improve well-being and space efficiency. Renovation cycles that were deferred during the pandemic have restarted as corporate balance sheets stabilize and as landlords compete through premium amenity upgrades. Kanto’s dominance anchors national demand, yet rapid growth in Kyushu–Okinawa signals geographic diversification of corporate expansions. High market concentration enables incumbents to scale R&D on sensor-fitted furniture, though it also limits price competition for mid-sized buyers.

Key Report Takeaways

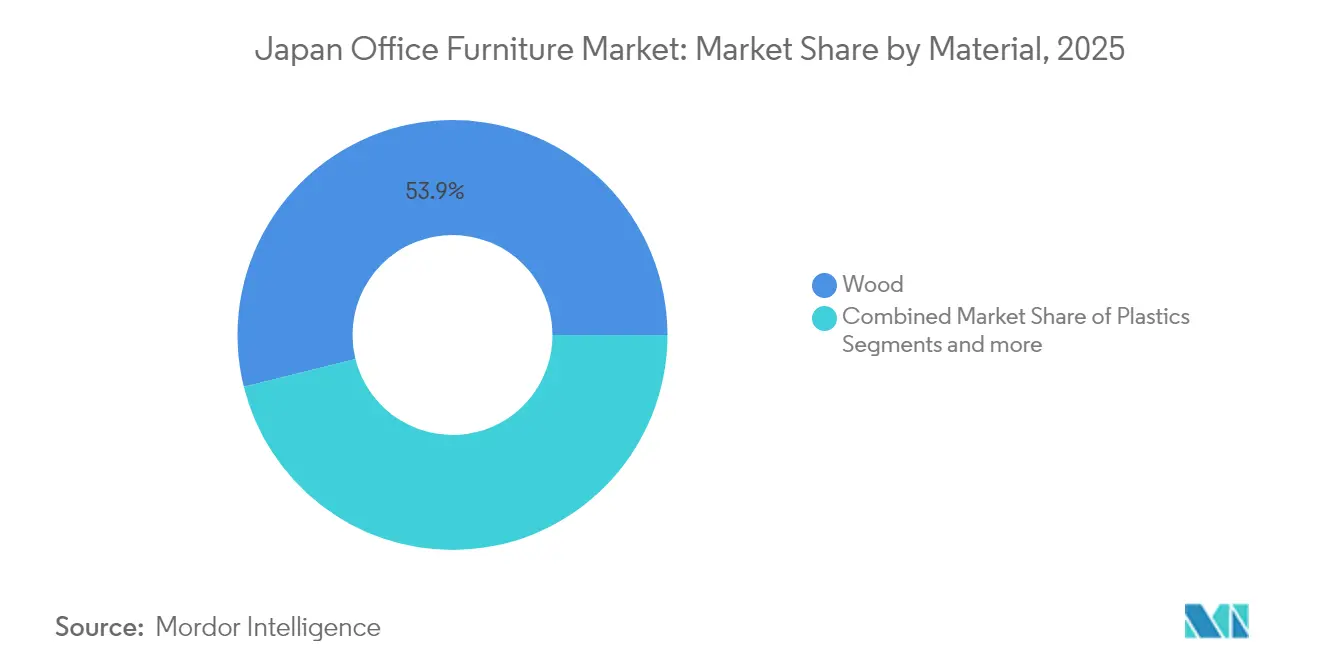

By material, wood captured 54.34% of Japan office furniture market share in 2024, while plastics is projected to expand at a 7.87% CAGR through 2030.

By product, desks held 26.26% of the Japan office furniture market size in 2024, and smart desks are growing at a 9.76% CAGR to 2030.

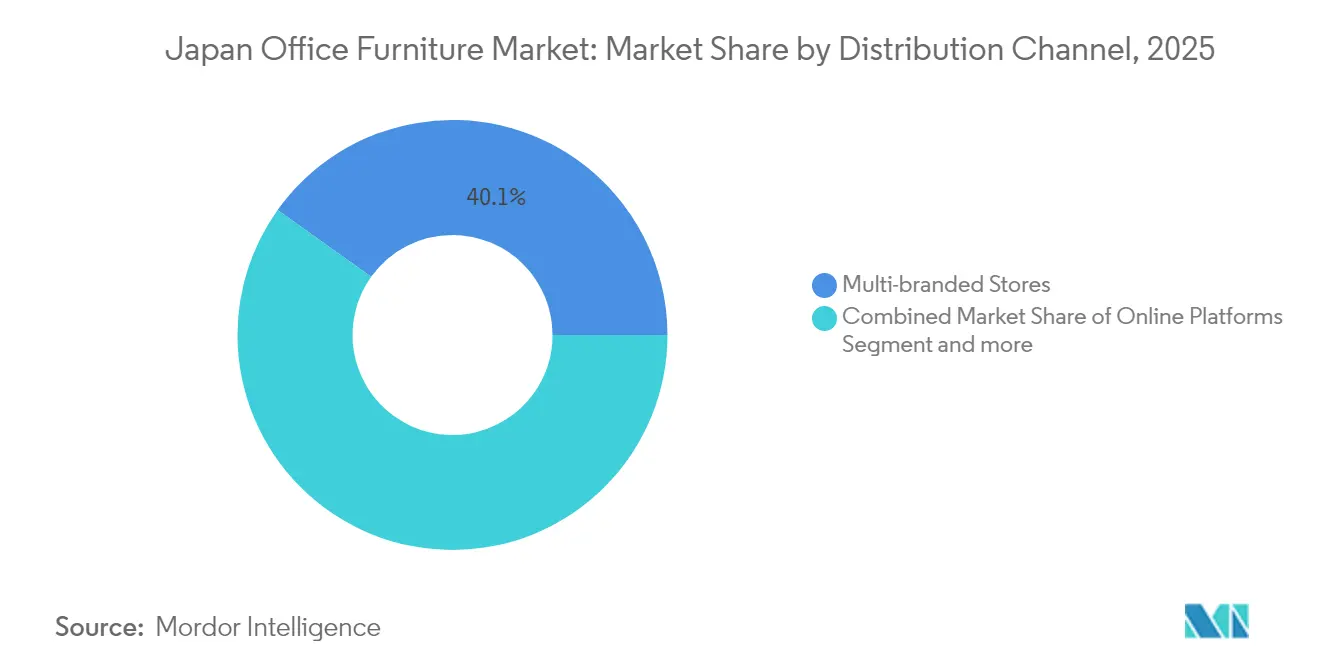

By distribution channel, multi-branded stores commanded 40.85% share of the Japan office furniture market size in 2024, but online platforms recorded the fastest growth at 12.76% CAGR.

By geography, Kanto led with 49.34% Japan office furniture market share in 2024, whereas Kyushu–Okinawa is advancing at a 6.33% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Office Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renovation cycles rebound post-COVID | +1.2% | Tokyo, Osaka, Nagoya | Medium term (2-4 years) |

| Corporate shift to ABW layouts | +1.5% | Major metros, regional roll-out | Long term (≥4 years) |

| Telework-linked tax incentives | +0.8% | Nationwide, urban uptake | Short term (≤2 years) |

| Ergonomic health regulations | +0.6% | Nationwide | Medium term (2-4 years) |

| Export lift for reused furniture | +0.4% | Asia-Pacific routes | Long term (≥4 years) |

| AI-based space analytics | +0.8% | Tech hubs, national spread | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Stagnant GDP-linked renovation cycles rebounding post-COVID

The stabilization of GDP in 2024 facilitated the release of capital budgets that had been restricted during the pandemic. This development allowed property owners and tenants to address deferred investments in workspace enhancements, reflecting a renewed focus on improving operational efficiency and meeting evolving workplace demands. Flexible desks, acoustic pods, and IoT-ready seating form the core of these upgrade packages, rewarding suppliers that bundle traditional craftsmanship with embedded connectivity. Fiscal-year 2025 budgets earmark larger allocations for workplace modernization, accelerating order volumes for modular fittings that cut installation time. Compliance with newer MHLW safety guidelines further shortens furniture life cycles within large corporates.

Corporate demand for activity-based working (ABW) layouts

Large enterprises are abandoning fixed seating in favour of zones dedicated to focus, collaboration, and relaxation, a shift proven to lift creative performance in peer-reviewed studies. Modular tables, lightweight partitions, and locker-based storage allow rapid reconfiguration as teams fluctuate between onsite and remote. Employee satisfaction surveys show 90% approval rates for ABW workstyles, enabling procurement teams to justify premium prices for specialized furniture. Manufacturers respond with quick-lock casters, stackable power rails, and upholstery options that dampen open-office noise without sacrificing visual openness. As hybrid attendance patterns normalize, ABW’s emphasis on spatial adaptability positions it as a long-run growth engine for the Japan office furniture market.

Government tax incentives for telework-supportive furniture

Since 2024, companies can deduct up to 100% of qualifying furniture that facilitates hybrid work. Height-adjustable desks, ergonomic chairs, and integrated charging hubs dominate corporate wish lists because tax treatment sharply improves their total cost of ownership. SMEs, which account for 99.7% of Japanese firms, are particularly sensitive to these savings and have shortened replacement cycles from seven to four years. Procurement teams track productivity metrics to validate incentive claims, thereby boosting demand for sensor-equipped models that generate usage data. The policy dovetails with national digital-transformation goals and channels steady orders toward domestic OEMs with certified telework lines.

Ergonomic-related occupational-health regulations

Revised MHLW rules require companies with more than 50 employees to provide lumbar-support seating and adjustable desks, or face fines that exceed the cost of compliance[1]Ministry of Health, Labour and Welfare, “Telework Model Regulations,” mhlw.go.jp . Technology and finance tenants, where screen-time intensity is highest, represent the early adopters, replacing chairs and task lighting ahead of inspection deadlines. International brands tailor catalogues to Japanese Industrial Standards, while local firms leverage cultural insights on sitting postures to refine cushion angles and breathable fabrics. Compliance software now checkpoints furniture specifications during lease renewals, guaranteeing recurring demand for certified models. Ergonomic mandates thus create a protective revenue stream within the Japan office furniture market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shrinking white-collar workforce | −1.8% | Nationwide, rural severity | Long term (≥4 years) |

| High urban rents temper refurbishments | −1.1% | Tokyo, Osaka | Medium term (2-4 years) |

| Engineered-wood cost volatility | −0.7% | Nationwide | Short term (≤2 years) |

| Slow IoT protocol standardization | −0.5% | Early adopters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Declining white-collar workforce due to aging demographics

Japan’s working-age population continues to contract as retirements outpace new entrants, trimming aggregate desk demand[2]Ministry of Internal Affairs and Communications, “Workforce Demographics,” soumu.go.jp . Leading corporations are strategically reducing their office footprints, as evidenced by the adoption of desk-sharing models and the downsizing of headquarters. This shift is particularly evident in manufacturing-centric regions, where corporate consolidations have resulted in an increased availability of office space. In urban centres, the inflow of foreign labour has mitigated some of the impacts of these changes; however, suburban suppliers are experiencing a decline in order volumes due to reduced demand. The hybrid work model has partially supported the furniture market by driving higher ergonomic standards for home offices. Nevertheless, the overall growth in furniture unit sales is projected to decelerate over the long term, reflecting a broader adjustment in market dynamics.

High urban rents are limiting large office refurbishments

Tokyo's Grade A office rents have reached an unprecedented level of JPY 37,012 (USD 252) per m², significantly impacting budget allocations for interior renovations. Small and medium-sized enterprises (SMEs) are deferring comprehensive floor refurbishments, instead opting for cost-effective alternatives such as upholstery and hardware refreshes, which are less expensive than new installations. Rising vacancy rates in secondary locations are prompting businesses to prioritize capital investment in retaining these spaces over furniture upgrades. Corporations are increasingly implementing "space-compression" strategies, including the adoption of benching systems and fold-away tables, to optimize functionality within constrained office areas. Suppliers specializing in multi-purpose furniture designs are gaining market share; however, overall revenue growth in the sector remains subdued, constrained by persistent rental inflation. A recovery in growth is anticipated only when rental pressures begin to ease.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Wood Dominance Faces Sustainability Pressures

Wood retained 53.86% Japan office furniture market share in 2025, sustained by cultural affinity for natural aesthetics and traditional joinery. Import dependence, however, exposes costs to global timber volatility, pushing buyers to experiment with recycled and bio-based composites that lower carbon footprints. Plastics segment accelerates at 7.74% CAGR, fuelled by advances in post-consumer resin blends that satisfy ESG audits without sacrificing structural integrity. Metal frames remain indispensable for sit-stand desks where durability and motorized actuation require steel or aluminium substructures.

Plastics’ growth also stems from their compatibility with embedded sensors, because moulded cavities simplify housing for IoT modules. Domestic OEMs trial biomass-derived polypropylene while international brands test ocean-bound plastics for chair shells aimed at environmentally sensitive procurement teams. Meanwhile, wood suppliers pursue chain-of-custody certification to preserve their premium positioning. Pilot projects using domestic cedar have raised utilization rates marginally above 40%, yet volume scale-up awaits mechanized drying and lamination upgrades in rural mills. Against this backdrop, circular models such as Kokuyo–ChopValue’s chopstick-based panels hint at a hybrid future where waste streams supply next-generation wood composites.

By Product: Smart Desks Revolutionize Traditional Categories

Desks led with 25.98% share of the Japan office furniture market size in 2025, underpinned by enterprise spending on height-adjustable models that mitigate sedentary health risks. Smart desks grow 9.58% CAGR, integrating wireless chargers, posture alerts, and ambient-light sensors that feed workplace analytics dashboards. Seating innovations are keeping pace with Kokuyo’s “ingCloud” chair auto-calibrates via a 3D Ultra Auto Fit mechanism and transmits anonymized usage data for predictive maintenance.

Category crossover blurs lines between tables and storage as modular pods combine power trunks, whiteboard surfaces, and lockable compartments. Lounge furniture adopts acoustic fabrics that double as sound panels, supporting video-conference clarity in hybrid meeting zones. Swivel chairs integrate dual lumbar supports tailored to Japanese anthropometrics, a feature co-developed by Officecom and SIHOO. Large corporates increasingly quantify ROI through reduced sick days and elevated employee-engagement scores, validating premium expenditures on sensor-rich models.

By Distribution Channel: Digital Transformation Accelerates Online Growth

Multi-branded showrooms held a 40.12% share in 2025 because tactile evaluation remains essential for high-involvement purchases. Nonetheless, online platforms surge 12.43% CAGR as 3D configurators, augmented reality (AR) placement tools, and procurement-workflow APIs shrink buyer friction. Corporates now shortlists products virtually, then dispatches facility managers to in-store “experience centres” for final verification. Specialty stores retain relevance by curating ergonomic or design-icon ranges not widely available elsewhere, while leasing programs align with circular-economy objectives by bundling maintenance and take-back services.

E-commerce operators invest in AI chatbots that parse building layouts to recommend SKU bundles, effectively serving as digital specifiers. Integration with enterprise resource planning (ERP) systems speeds bulk orders, cutting purchase-order cycles from weeks to days. Yet last-mile delivery for fully assembled items still requires local logistics, leading to omnichannel alliances between pure-play online retailers and regional warehouse networks. The outcome is a hybrid landscape where digital discovery and physical fulfilment coexist, each amplifying the other.

Geography Analysis

Kanto sustained 48.88% Japan office furniture market share in 2025 on the strength of Tokyo’s concentration of headquarters, ministries, and global finance. Grade A rent escalation reinforces demand for high-value, space-efficient solutions such as compact sit-stand stations and modular collaboration hubs. Kansai’s steady inflows from Osaka finance and Kobe tech parks support replacement cycles centred on ergonomic upgrades rather than full renovations.

Kyushu–Okinawa posts the fastest 6.21% CAGR to 2031, propelled by Fukuoka’s push to attract start-ups through favourable office-conversion grants that stipulate modern, flexible interiors. Chubu benefits from automotive R&D clusters that favour specialized drafting benches and vibration-isolated worktables. Tohoku and Hokkaido capture modest growth as regional revitalization policies encourage satellite offices in lower-cost cities, stimulating purchases of modular kits that can traverse narrow stairwells common in older buildings. Chugoku–Shikoku sees incremental gains linked to logistics and shipbuilding firms upgrading control rooms with integrated consoles. Nationwide, furniture suppliers establish decentralized service depots to shorten installation times and meet the service-level agreements demanded by corporate customers executing multi-site rollouts. Geography thus shapes logistics strategy as much as demand, reinforcing the need for agile distribution footprints.

Competitive Landscape

The top-five players controlled a significant share of 2024 revenue, giving the Japan office furniture market a pronounced oligopolistic profile. Kokuyo, Okamura, and Itoki lead with full-stack offerings that span design consulting, manufacturing, and after-sales services, leveraging vertical integration to accelerate product refresh cycles. Kokuyo is allocating a significant portion of its revenue toward research and development, focusing on advancements in IoT sensors, the integration of recycled materials, and the development of software dashboards. These initiatives aim to transform traditional furniture offerings into comprehensive service platforms, aligning with the company's strategic innovation objectives.

International entrants such as Herman Miller localize flagship lines through partnerships with Japanese distributors, often adding compact footprints and seismic-resistant features to suit domestic building codes. Chinese brand SIHOO co-develops ergonomic chairs with Officecom, signalling cross-border collaboration around price-competitive innovation. Disruptive start-ups target circular economy niches, offering subscription models that bundle maintenance and refurbishment, which appeal to CSR-minded corporates.

Private-equity interest in the broader workspace ecosystem is rising, illustrated by EQT’s USD 2.7 billion acquisition of elevator supplier Fujitec, a move that underscores confidence in Japan’s office-infrastructure outlook. Consolidation abroad also reverberates locally as HNI’s planned USD 2.2 billion buyout of Steelcase may spawn a larger global rival capable of contesting domestic incumbents on project tenders[4]AInvest, “HNI to Buy Steelcase,” ainvest.com .

Japan Office Furniture Industry Leaders

Kokuyo Co., Ltd.

Itoki Corporation

Okamura Corporation

Plus Corporation

Uchida Yoko Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Itoki launched “Opacity” high dividers for hybrid zones with controllable transparency.

- July 2025: EQT, a European investment firm, announced the acquisition of Japan's Fujitec for USD 2.7 billion, marking significant foreign investment in Japan's office infrastructure sector.

- July 2025: Kokuyo Corporation announced the general release of its "ingCloud" office chair featuring a 3D Ultra Auto Fit mechanism, set for winter 2025 launch on the company's official e-commerce platform after winning the Grand Prix at Orgatec Tokyo 2025 Kokuyo Corporation.

- April 2025: Kokuyo partnered with ChopValue Japan to commercialize chopstick-recycled panels.

Japan Office Furniture Market Report Scope

The term 'office furniture' encompasses products and services catering to the furnishing needs of diverse work environments, including offices, healthcare facilities, educational institutions, and hospitality venues.

The Japanese office furniture market is segmented by material, product, and distribution channel. By material, the market is segmented into wood, metal, plastic, and other materials. By product, the market is segmented into meeting chairs, lounge chairs, swivel chairs, office tables, storage cabinets, and desks. By distribution channel, the market is segmented into multi-branded stores, specialty stores, online platforms, and other distribution channels. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Material

| Wood |

| Metal |

| Plastics |

| Other Materials |

By Product

| Meeting Chairs |

| Lounge Chairs |

| Swivel Chairs |

| Office Tables |

| Storage Cabinets |

| Desks |

By Distribution Channel

| Multi-branded Stores |

| Specialty Stores |

| Online Platforms |

| Other Distribution Channels |

By Geography

| Kanto |

| Kansai |

| Chubu |

| Kyushu–Okinawa |

| Tohoku |

| Hokkaido |

| Chugoku–Shikoku |

| By Material | Wood |

| Metal | |

| Plastics | |

| Other Materials | |

| By Product | Meeting Chairs |

| Lounge Chairs | |

| Swivel Chairs | |

| Office Tables | |

| Storage Cabinets | |

| Desks | |

| By Distribution Channel | Multi-branded Stores |

| Specialty Stores | |

| Online Platforms | |

| Other Distribution Channels | |

| By Geography | Kanto |

| Kansai | |

| Chubu | |

| Kyushu–Okinawa | |

| Tohoku | |

| Hokkaido | |

| Chugoku–Shikoku |

Key Questions Answered in the Report

What is the projected value of the Japan office furniture market by 2031?

Forecasts place the market at USD 5.87 billion by 2031.

Which material segment is growing fastest in Japan’s office furniture sector?

Plastics lead with a 7.74% CAGR, driven by recycled and sensor-friendly resins.

How fast are online sales channels expanding?

Online platforms are advancing at a 12.43% CAGR through 2031.

Which region shows the highest growth rate?

Kyushu–Okinawa registers the fastest 6.21% CAGR to 2031.

Why are smart desks gaining traction?

They integrate sensors and height-adjustment features that enhance ergonomics and supply space-utilization data, supporting hybrid work strategies.

Which companies dominate the Japan office furniture sector?

Kokuyo, Okamura, Itoki, Plus and Kurogane together controlled a significant share of 2024 sales, giving them outsized influence over pricing and product innovation.

Page last updated on: