Brazil Mobile Virtual Network Operator (MVNO) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

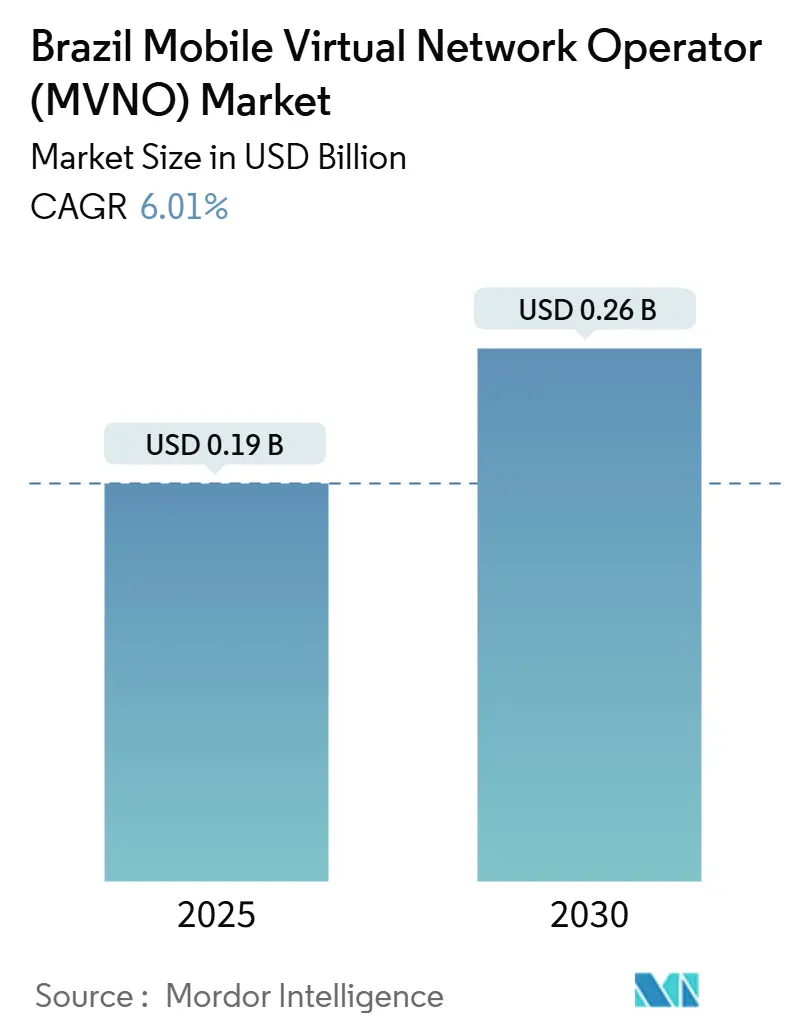

| Market Size (2025) | USD 0.19 Billion |

| Market Size (2030) | USD 0.26 Billion |

| Growth Rate (2025 - 2030) | 6.01% CAGR |

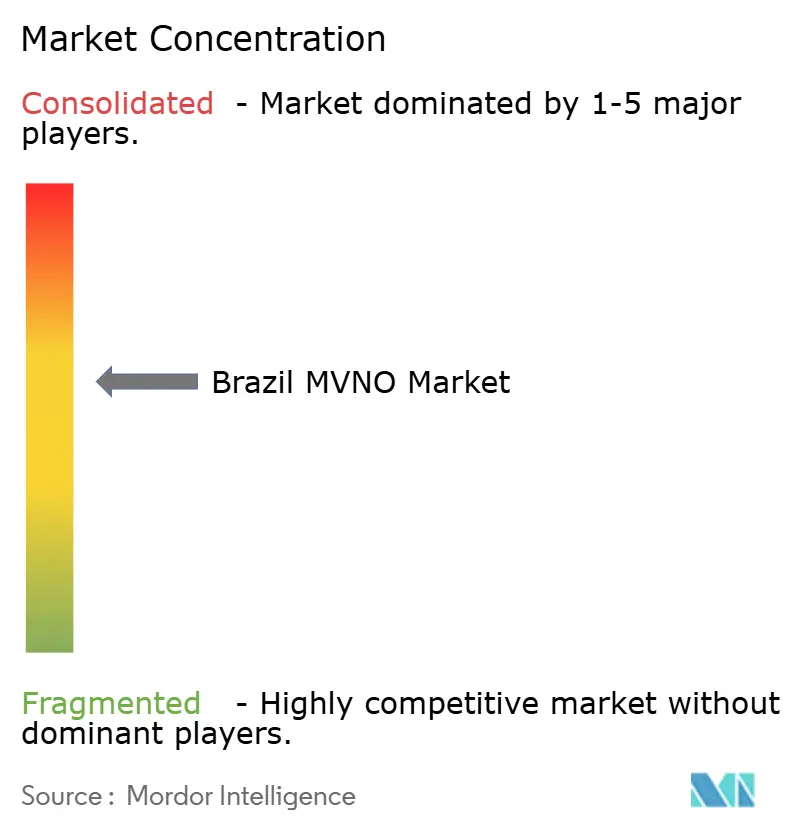

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Mobile Virtual Network Operator (MVNO) Market Analysis by Mordor Intelligence

The Brazil MVNO Market size is estimated at USD 0.19 billion in 2025, and is expected to reach USD 0.26 billion by 2030, at a CAGR of 6.01% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 7.14 million Subscribers in 2025 to 9.19 million Subscribers by 2030, at a CAGR of 5.17% during the forecast period (2025-2030). Demand is shifting from discount voice and data propositions toward bundled connectivity-plus-service offers, enabled by sweeping regulatory reforms that resolved long-standing licensing bottlenecks [1]ANATEL Board, “Resolução Anatel nº 777,” informacoes.anatel.gov.br. The continued rollout of fiber broadband and the introduction of 5G network-slicing wholesale agreements allow virtual operators to launch enterprise-grade private networks without building physical infrastructure. Fintech-led co-branded services such as Nubank’s NuCel demonstrate how embedded financial ecosystems can slash acquisition costs and push subscriber growth in major metropolitan areas. Meanwhile, specialized MVNOs targeting industrial IoT applications are gaining traction in agribusiness hubs, supported by Brazil’s USD 400 million rural-connectivity investment pipeline.

Key Report Takeaways

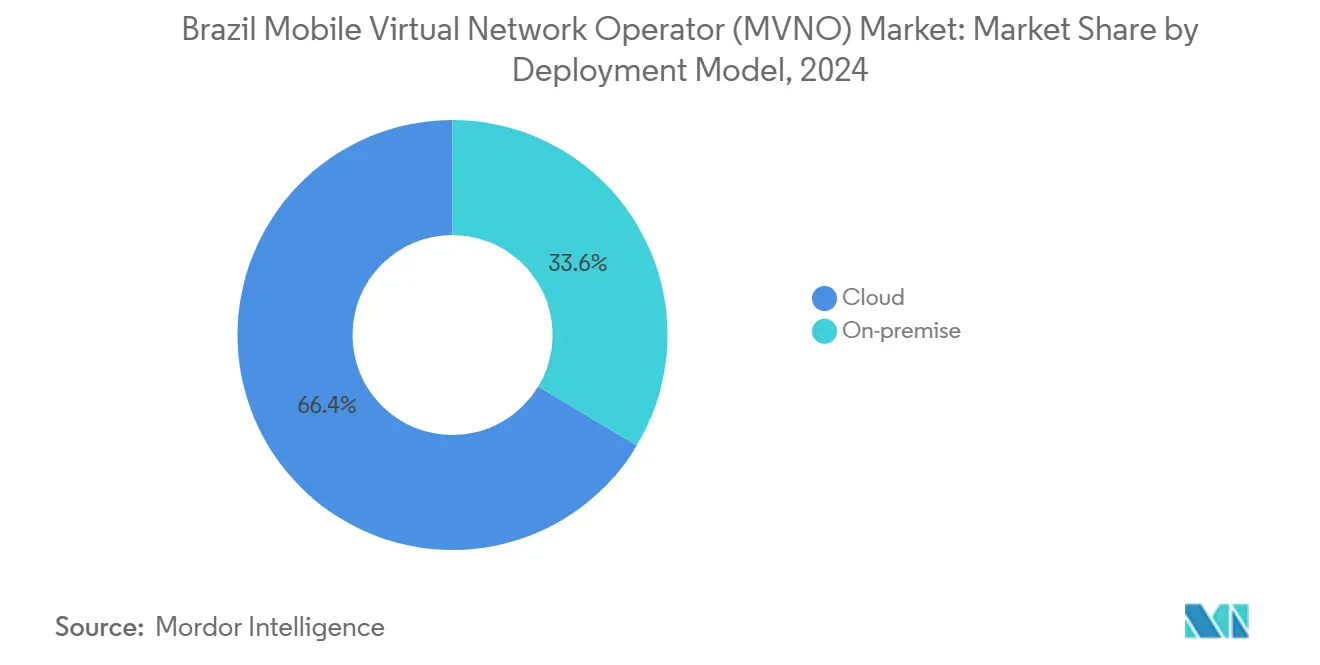

- By deployment model, cloud infrastructure led with 66.40% of the Brazil MVNO market share in 2024, and it is expanding at a CAGR of 11.52% through 2030.

- By operational mode, reseller/light/brand MVNOs held 62.68% of the Brazil MVNO market size in 2024; full MVNO operations are expanding at a 19.97% CAGR through 2030 as enterprise clients demand end-to-end control.

- By subscriber type, consumer accounts captured 86.92% of the Brazil MVNO market in 2024, whereas IoT-specific subscriptions are advancing at a 33.52% CAGR to 2030.

- By application, discount services controlled 44.72% revenue in 2024; cellular M2M solutions are forecast to climb at a 32.62% CAGR as industrial digitization accelerates.

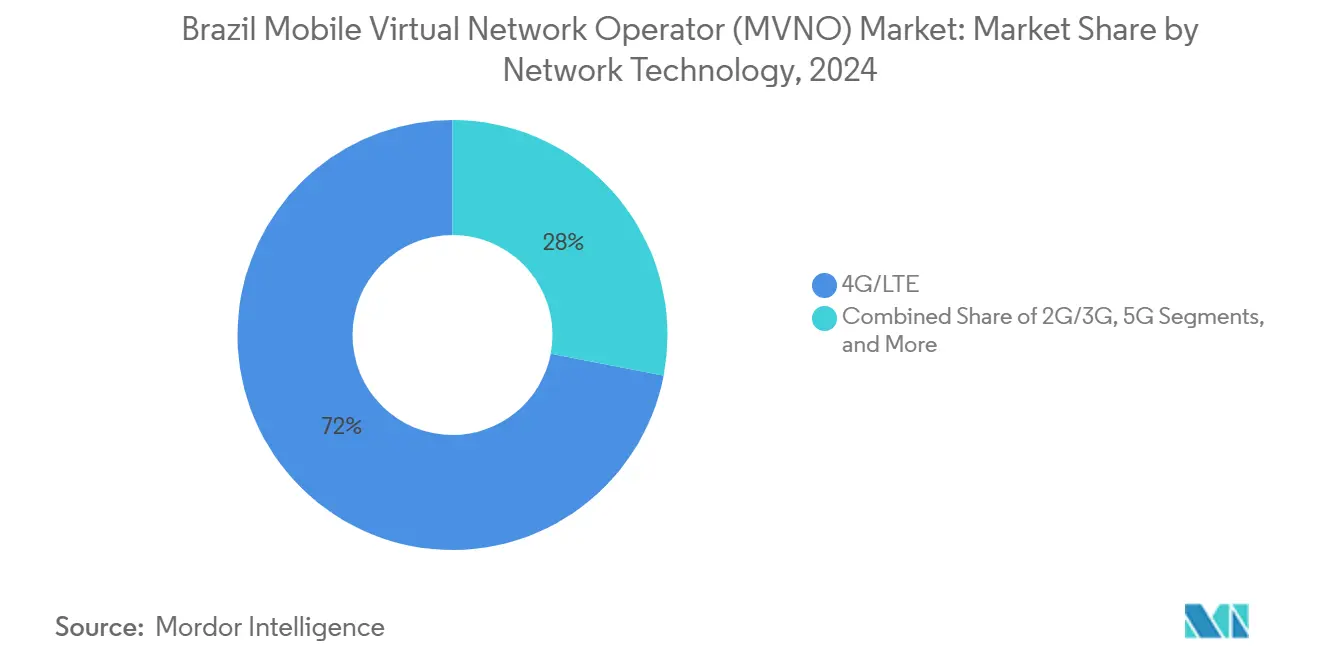

- By network technology, 4G/LTE represented 71.99% of the base in 2024, but satellite/NTN connections are set for a 101.81% CAGR as remote-area coverage improves.

- By distribution channel, online/digital-only sales captured 52.38% in 2024 and are projected to rise at a 10.07% CAGR, outpacing store-based channels as activation shifts to app models.

Brazil Mobile Virtual Network Operator (MVNO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory reforms unlocking MVNO licensing | +1.8% | National; early gains in São Paulo, Rio de Janeiro, Brasília | Short term (≤ 2 years) |

| Massive expansion of fiber broadband | +1.5% | National; concentrated in Southeast and South | Medium term (2-4 years) |

| Fintech-led co-branded mobile propositions | +1.2% | National; urban concentration | Short term (≤ 2 years) |

| Corporate demand for private LTE/5G | +0.9% | Industrial clusters in São Paulo, Minas Gerais, Rio Grande do Sul | Medium term (2-4 years) |

| 5G network-slicing wholesale agreements | +0.4% | State capitals prioritized for 5G rollout | Long term (≥ 4 years) |

| Rising IoT connections in agribusiness | +0.3% | Rural Mato Grosso, Goiás, Paraná | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Reforms Unlocking MVNO Licensing

ANATEL’s Resolution 777 modernized service rules in 2025, replacing lengthy application cycles with a streamlined online portal that cuts approval times from months to weeks. The change opened doors for fintech partnerships such as Nubank-Claro, which gained clearance despite exclusivity clauses once viewed skeptically by regulators. By licensing both Authorized and Accredited models, ANATEL now accommodates ventures that own frequency blocks and those leasing wholesale capacity. Flexible rules around wholesale negotiation let MVNOs craft bespoke service terms instead of accepting rigid tariffs, enabling competitive differentiation. Consumer-protection requirements remain in force through Resolution 765, ensuring quality metrics are met while still granting operators freedom to tailor pricing tiers.

Massive Expansion of Fiber Broadband Enabling Bundled Offers

Fixed fiber lines exceeded 52.9 million accesses by mid-2025, providing a high-capacity backbone that MVNOs can bundle with mobile plans. Regional ISPs, already controlling 52% of those connections, seek to attach mobile service as a loyalty extension, fueling wholesale demand from host networks. América Móvil’s USD 7.7 billion pledge to bolster Claro’s fiber footprint through 2029 amplifies passive infrastructure available for virtual entrants [2]América Economía desk, “América Móvil to Invest USD 7.7 Billion in Claro Brasil,” americaeconomia.com. In underserved interior towns, fiber often arrives before high-capacity LTE, allowing MVNOs to market converged packages that leapfrog patchy mobile-only coverage. The broadened footprint also supports backhaul for satellite-to-cellphone pilots, further eroding geographic barriers.

Surge of Fintech-Led Co-Branded Mobile Propositions

Nubank added 44,400 NuCel lines within weeks of its October 2024 debut, validating the thesis that embedded banking ecosystems lower acquisition costs and churn [3]Nubank newsroom, “Nubank Launches NuCel,” international.nubank.com.br. Fintech MVNOs leverage real-time customer analytics to personalize data top-ups, extend interest-free credit, and integrate PIX payments inside their apps. The model dovetails with Brazil’s emerging central-bank digital currency, Drex, promising frictionless micro-payments that traditional telecom billing cannot match. Financial institutions also enjoy reduced credit-risk exposure when connectivity fees are bundled with daily banking transactions. Success stories have prompted Banco Inter and C6 Bank to outline similar mobile entries, indicating that financial-telecom convergence is now a mainstream play rather than a niche experiment.

Corporate Demand for Private LTE/5G via MVNO Models

Enterprises facing Industry 4.0 mandates increasingly favor private networks delivered through MVNO intermediaries instead of direct MNO contracts, a service line rising at 21.1% annual spend through 2028 [4]Valor Econômico reporters, “Rede Privativa Apoia a Expansão da Conectividade,” valor.globo.com . Vivo’s 30-site Ambev roll-out shows how wholesale slicing can isolate bandwidth for mission-critical factory automation. MVNOs customize SLAs and integrate with cloud orchestration tools to give manufacturers dashboard-level visibility, something harder to secure from retail MNO lines. Agricultural conglomerates deploy IoT sensors over MVNO-managed slices to monitor soil moisture and optimize fertilizer use, cutting OpEx and meeting sustainability metrics. Because MVNOs bear none of the radio-access capital load, they can price dedicated capacity sharply below bespoke MNO enterprise offers, spurring adoption across logistics, energy, and mining segments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High wholesale rate floor from MNO oligopoly | -1.9% | Competitive urban markets nationwide | Short term (≤ 2 years) |

| Complex SIM registration and data privacy | -0.8% | Nationwide; disparate state enforcement | Medium term (2-4 years) |

| Slow uptake outside Tier-1 cities | -0.6% | Northeast and North rural corridors | Long term (≥ 4 years) |

| Scarcity of eSIM platforms with local pay | -0.4% | Urban centers where eSIM interest peaks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Wholesale Rate Floor from Limited MNO Competition

Vivo, Claro, and TIM collectively own 95.5% of active mobile lines, enabling them to set interconnect and wholesale fees that erode MVNO margins. Volume-based discounts favor large-scale players like Surf Telecom, leaving smaller regional entrants unable to price competitively. Minimum-traffic clauses lock MVNOs into multi-year commitments that limit tariff flexibility and slow pivot strategies when market dynamics shift. Although ANATEL publicly encourages voluntary rate transparency, it has refrained from imposing a mandated wholesale ceiling, citing a desire to maintain investment incentives. Until alternative wholesale capacity arrives, price pressure will remain the most acute restraint on short-term profitability.

Complex SIM Registration and Data-Privacy Compliance

Brazil mandates multi-factor ID verification under Resolution 717, requiring passports, biometric data, or tax ID numbers for each activation. MVNOs must integrate with national fraud-prevention databases and maintain auditable logs for a minimum of five years, driving up back-office costs. Parallel LGPD requirements impose strict consent sequencing and data-storage localization, complicating fully automated e-commerce onboarding flows. For IoT operators managing hundreds of thousands of sensors, the rules set can cripple deployment timelines because each device technically counts as a “subscriber” needing registration. Larger, capitalized entities mitigate the drag by outsourcing compliance to specialist SaaS platforms, whereas start-ups face a regulatory cost that can dwarf marketing expenditures during early growth phases.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Architecture Redefines Scale

Cloud platforms dominated the Brazil MVNO market in 2024 with a 66.40% revenue share as operators pursued asset-light expansion paths that circumvent terrestrial switching hubs. The segment is set to register an 11.52% CAGR to 2030, far outpacing on-premise facilities that remain tethered to legacy hardware cycles. Public cloud zones in São Paulo, Rio Grande do Sul, and Bahia enable nationwide service rollout within hours, shrinking time-to-market for regional promotions. Bare-metal functions, from HLR to PCRF, are now containerized, allowing continuous integration updates without service disruption.

On-premise deployments persist in defense, banking, and energy verticals where data sovereignty rules dictate local processing. However, integration vendors increasingly offer hybrid orchestration layers so sensitive workloads stay stateside while signaling nodes reside in the cloud. As a result, the Brazil MVNO market continues to tilt toward SaaS-driven core networks, leaving rack-based installations to niche enterprise builds. The trend aligns with government cloud-first procurement guidelines, propelling the Brazil MVNO market toward a predominantly virtualized future.

By Operational Mode: Full MVNO Control Gains Ground

Reseller/light/brand formats retained 62.68% revenue in 2024, capitalizing on quick brand launches that rely entirely on host operator infrastructure. Yet the full MVNO model, posting a robust 19.97% CAGR, is emerging as the default choice for corporate-oriented entrants needing granular policy control and differentiated quality of service. Full operators own core voice and data elements, issue their own SIMs, and craft unique roaming agreements, allowing value creation beyond price competition.

The Brazil MVNO market size for full-control operations is projected to double by 2030 as industrial IoT projects require programmable network slices unattainable under reseller frameworks. Conversely, light MVNOs remain critical for marketing-driven fintech tie-ins because they avoid hardware capex. This dual-track evolution illustrates the flexibility embedded in Brazil’s licensing framework, ensuring the Brazil MVNO market accommodates both mass-consumer plays and enterprise specialists under distinct cost structures.

By Subscriber Type: IoT Ascends as Next Growth Engine

Consumer lines still captured 86.92% revenue in 2024, reflecting Brazil’s 200-million-plus population attraction for price-sensitive voice-and-data bundles. However, the IoT-specific segment, showing a 33.52% CAGR, is on track to chip away at consumer dominance by 2030. Agricultural telemetry, smart-grid meters, and logistics asset tracking generate smaller ARPU but high-volume SIM orders that create scale economics.

Within the Brazil MVNO industry, enterprises now view virtual operators as systems-integration partners rather than mere bandwidth resellers. For example, pest-monitoring sensors from TIM transmit field data every 30 minutes over low-band NB-IoT, yielding massive packet volume without straining network capacity. This trajectory suggests the Brazil MVNO market will transition to a mixed user base where device connections eventually outnumber handsets in certain verticals.

By Application: M2M Solutions Eclipse Discount Roots

Discount positioning initially elevated MVNO uptake, controlling 44.72% revenue in 2024 through aggressive pricing on bulk data packages. Yet cellular M2M applications are growing at a 32.62% CAGR, outstripping all other use cases as industries automate supply chains. Predictive-maintenance sensors, remote health-care monitors, and smart-city lighting are quickly dwarfing person-to-person traffic volumes.

Consequently, the Brazil MVNO market share for discount services is forecast to erode gradually, even as absolute revenues remain stable. Operators now integrate SIM management APIs directly into enterprise dashboards, letting technicians set usage thresholds and trigger top-ups programmatically. This shift underscores the Brazil MVNO market size opportunity tied to service orchestration rather than voice minutes, accelerating ecosystem migration away from pure price wars.

By Network Technology: Satellite Renaissance Reshapes Coverage

4G/LTE provided 71.99% of active connections in 2024, a figure expected to plateau as terrestrial densification reaches cost limits in remote Amazon and Pantanal regions. Satellite/NTN lines, posting a 101.81% CAGR, unlock nationwide ubiquity when paired with low-earth-orbit constellations. Direct-to-cell pilots run by Claro show latency below 50 ms, enabling standard handset access without special hardware.

As regulatory clearance broadens, MVNOs will bundle hybrid KU-band and cellular plans, using adaptive routing to shift traffic onto satellite backhaul only when terrestrial service degrades. The Brazil MVNO industry, therefore, stands at a technological inflection where radio-agnostic billing engines decide packet pathways, delivering unheard-of resiliency for logistics, mining, and telemedicine. The coming sunset of 2G and 3G networks, which will impose USD 1.6 billion in transition costs, further accelerates investment toward LTE-and-above solutions.

By Distribution Channel: Digital-Only Strategies Lead Acquisition

Online channels accounted for 52.38% activations in 2024, benefiting from instant e-KYC workflows embedded in banking and e-commerce apps. The segment is set to register a 10.07% CAGR to 2030. App-based provisioning eliminates physical SIM dispatch by supporting remote eSIM QR-code downloads, cutting acquisition cost by up to 40%. Meanwhile, brick-and-mortar retail endures in lower-income districts where cash payments prevail.

The Brazil MVNO market size tied to digital-only channels is projected to reach USD 0.15 billion by 2030, equal to 58% penetration, as smartphone ownership nears 91%. Carrier sub-brand kiosks act as hybrid points of presence for troubleshooting complex port-in requests, preserving service perception while still leaning on app-centric self-care. Overall, the Brazil MVNO market remains committed to omnichannel experiences but clearly prioritizes self-service tech to gain marginal-cost advantages against MNO incumbents.

Geography Analysis

Greater São Paulo anchors roughly one-third of Brazil's MVNO market revenue, underpinned by high income levels and a 100% LTE population-coverage footprint that supports premium fintech bundles. Rio de Janeiro and Brasília follow, where converged broadband-plus-mobile packages resonate with professional service workers. In these metros, full MVNOs negotiate differentiated quality of service guarantees to court data-heavy subscribers who demand seamless video streaming during long commutes.

The Brazil MVNO market is rapidly extending into South and Southeast interior cities such as Campinas and Curitiba, leveraging fiber backhaul to counter patchy macrocell coverage. Here, regional ISPs with entrenched customer relationships parlay fixed-line contracts into mobile add-ons, stimulating cross-sell penetration. Meanwhile, agribusiness corridors in Mato Grosso and Goiás underpin the fastest subscriber growth as IoT devices multiply across irrigation sites and cattle-management systems.

In the North and Northeast, adoption remains tempered by affordability constraints and coverage perception gaps, yet policy programs that subsidize rural satellite links are expected to catalyze uptake. The Brazil MVNO market, therefore, displays a dual-speed geographic pattern: urban hubs drive ARPU expansion through premium bundles, while interior provinces propel unit growth via IoT and hybrid satellite plays.

Competitive Landscape

The Brazil MVNO market supports more than 60 authorized brands, yet remains semi-consolidated because Surf Telecom alone carries 1.1 million lines, positioning it as the sixth-largest mobile operator overall. Nubank exploits banking customer reach to monetize telecom add-ons with minimal marketing spend, while Plintron follows an enablement model that supplies core network services to dozens of niche labels.

Strategic moves increasingly center on vertical specialization. emnify partners with global logistics firms to bundle Brazilian multi-network access inside a single IoT SIM, sidestepping roaming penalties. At the same time, telecommunications arms of energy conglomerates such as Petrobras evaluate MVNO licenses to support offshore platform connectivity, indicating that corporate self-provisioning is no longer hypothetical.

Investment flows highlight cloud over physical assets: Pareteum extended its hosted core agreement to encompass 5G standalone features, granting smaller MVNOs early access to slicing. Competitive intensity is amplified by oligopolistic wholesale pricing from the Big Three MNOs, but regulatory openness to exclusive partnerships now lets MVNOs secure favorable economics in exchange for ecosystem stickiness.

Brazil Mobile Virtual Network Operator (MVNO) Industry Leaders

Correios Celular

Veek Tecnologia S/A

Fluke Telecomunicações Ltda

Datora Telecomunicações Ltda

Surf Telecom (EUTV S.A.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: ANATEL authorized exclusive partnership between Nubank and Claro for NuCel service, cementing fintech-telecom convergence.

- April 2025: ANATEL approved expansion of Starlink operations, broadening satellite wholesale capacity for rural-focused MVNOs.

- March 2025: Claro launched direct satellite-to-cell trials, paving the way for nationwide handset interoperability without extra hardware.

- October 2024: Nubank introduced NuCel with three prepaid plans covering 93% of the population via Claro’s network, enrolling 44,400 users quickly.

- September 2024: Emnify rolled out a single-SIM nationwide solution through a Claro agreement, enhancing enterprise IoT options.

- August 2024: Nokia and TIM inked a deal to extend 5G coverage in 15 states by 2025, strengthening wholesale slicing opportunities.

- February 2024: Algar debuted “Nomo by Algar” in Porto Alegre and adjacent cities after acquiring the brand’s MVNO rights.

Brazil Mobile Virtual Network Operator (MVNO) Market Report Scope

| Cloud |

| On-premise |

| Reseller / Light / Brand MVNO |

| Service Operator |

| Full MVNO |

| Consumer |

| Enterprise |

| IoT-specific |

| Discount |

| Business |

| Cellular M2M |

| Others |

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

| Online/Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party/Wholesale |

| By Deployment Model | Cloud |

| On-premise | |

| By Operational Mode | Reseller / Light / Brand MVNO |

| Service Operator | |

| Full MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Others | |

| By Network Technology | 2G/3G |

| 4G/LTE | |

| 5G | |

| Satellite/NTN | |

| By Distribution Channel | Online/Digital-only |

| Traditional Retail Stores | |

| Carrier Sub-brand Stores | |

| Third-Party/Wholesale |

Key Questions Answered in the Report

What is the current value of the Brazil MVNO market?

The Brazil MVNO market size was USD 0.19 billion in 2025 and is forecast to reach USD 0.26 billion by 2030.

Which segment is growing fastest among Brazil’s virtual operators?

IoT-specific subscriptions are expanding at a 33.52% CAGR as agriculture, logistics, and smart-city projects deploy connected devices.

How concentrated is wholesale supply for virtual operators?

Three MNOs, such as Vivo, Claro, and TIM, control more than 95% of retail mobile lines, giving them strong leverage over MVNO wholesale rates.

What technology is set to disrupt 4G dominance in remote areas?

Satellite/NTN links are forecast to grow at a 101.81% CAGR through 2030, enabling handset-level connectivity in regions lacking cellular coverage.

Why are fintech companies launching MVNOs in Brazil?

Fintechs leverage existing banking apps and user data to lower acquisition costs, embed telecom services seamlessly, and create sticky multi-service ecosystems.

How does regulatory reform support MVNO growth?

ANATEL’s Resolution 777 streamlined licensing, letting new entrants secure approval within weeks and negotiate flexible wholesale terms.

Page last updated on: