Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

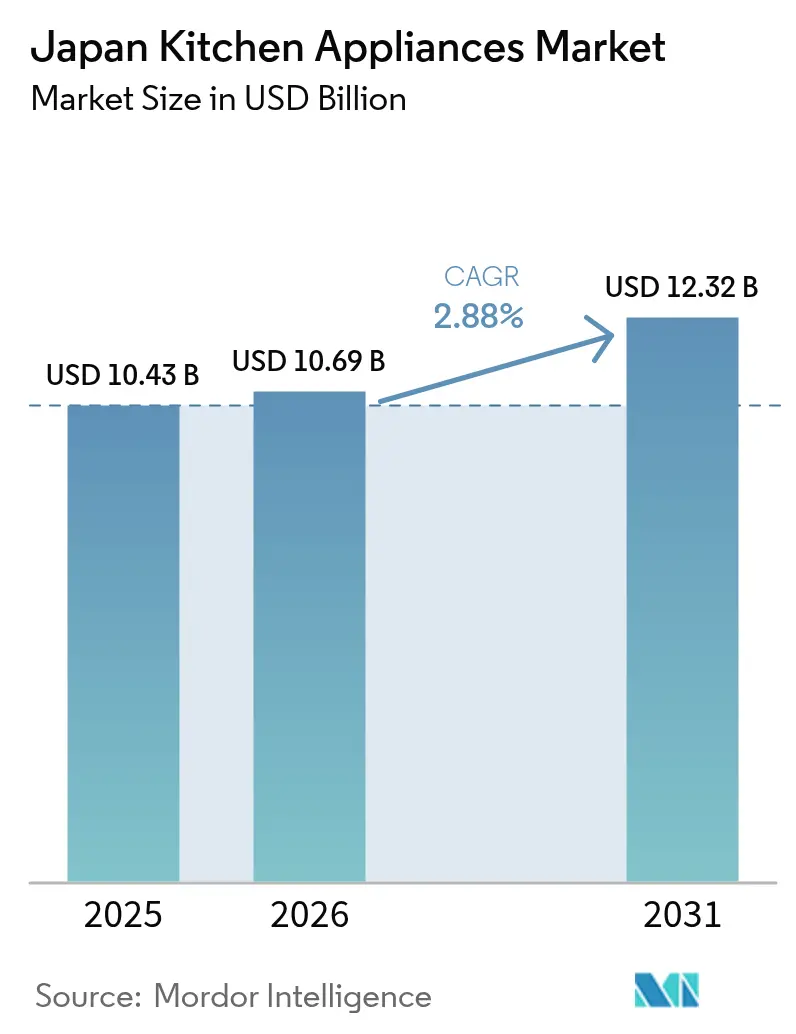

| Base Year Market Size (2025) | USD 10.43 Billion |

| Market Size (2026) | USD 10.69 Billion |

| Market Size (2031) | USD 12.32 Billion |

| Growth Rate (2026 - 2031) | 2.88% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Kitchen Appliances Market Analysis by Mordor Intelligence

The Japan kitchen appliances market size reached USD 10.43 billion in 2025, is expected to be USD 10.69 billion in 2026, and is projected to reach USD 12.32 billion by 2031 at a 2.88% CAGR. Near-term growth reflects a release of replacement demand supported by the Top Runner energy-efficiency framework that is extended through 2030 and by rebate programs that reimburse a significant share of the price premium on efficient models. A sizable senior population that reduces new household formation sits in tension with premiumization cycles and higher online penetration, which lifts average selling prices even as unit volumes stay steady[1]. E-commerce already accounts for a large slice of appliance purchases and continues to grow faster than store-based channels, reshaping discovery, fulfillment, and after-sales routines. Regional dynamics support uneven momentum, with Kanto sustaining the largest base and Kansai recording the fastest trajectory on the back of tourism and renovation-linked demand.

Key Report Takeaways

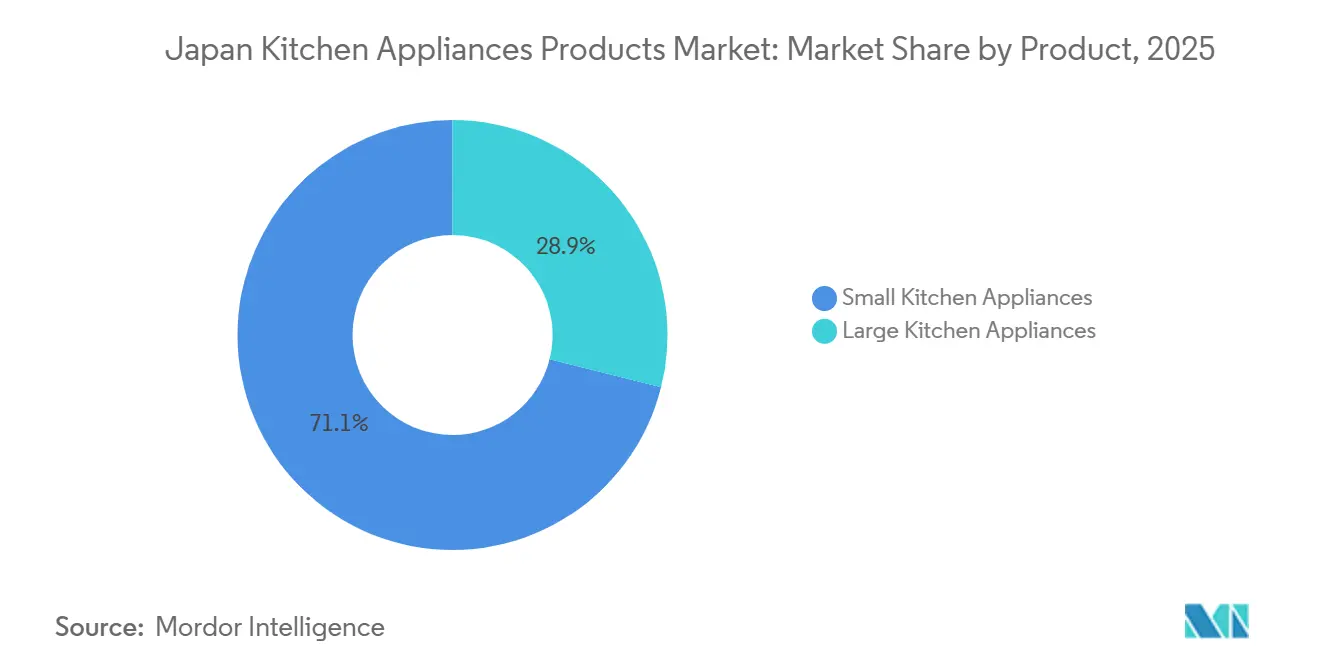

- By product, large kitchen appliances led with 28.97% of Japan kitchen appliances market share in 2025, while small kitchen appliances are forecast to expand at a 4.52% CAGR through 2031.

- By end-user, the Residential segment held 87.25% of Japan kitchen appliances market share in 2025, while Commercial recorded a 3.83% projected CAGR through 2031.

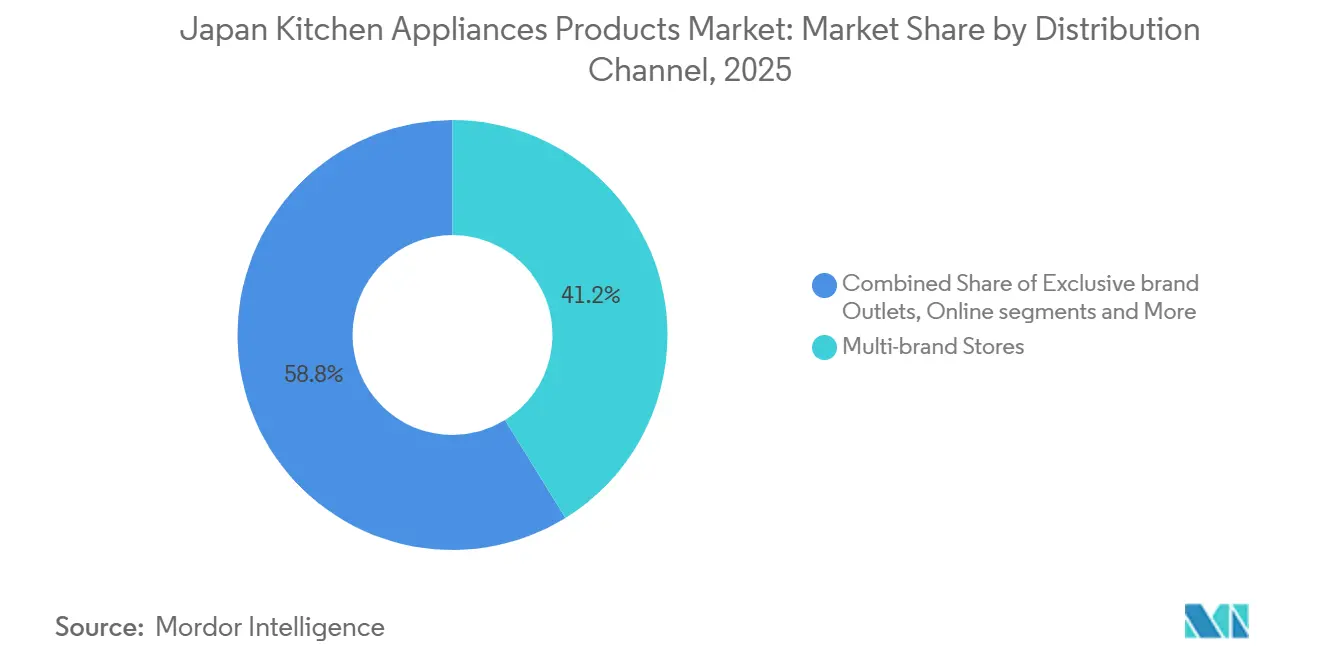

- By distribution channel, Multi-Brand Stores accounted for 41.25% of Japan kitchen appliances market share in 2025, and Online Channels are projected to grow at a 5.12% CAGR through 2031.

- By geography, Kanto captured 33.65% of Japan kitchen appliances market share in 2025, and Kansai is projected to grow at a 4.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Kitchen Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce penetration accelerates appliance uptake | +0.8% | National, strongest in Kanto and Kansai urban cores | Medium term (2-4 years) |

| Energy-efficiency standards drive replacement demand | +0.7% | National; Top Runner rules apply uniformly | Long term (≥ 4 years) |

| Premiumization and smart upgrades in urban households | +0.5% | Kanto, Kansai, and Chubu metropolitan areas | Medium term (2-4 years) |

| Urban micro-living boosts compact multi-function devices | +0.4% | Tokyo, Osaka, Nagoya | Short term (≤ 2 years) |

| Utility-led IH cooktop electrification expands the addressable base | +0.3% | National, early gains in Tokyo, Osaka, Nagoya | Long term (≥ 4 years) |

| Hospitality and rental housing upgrades spur built-in suites | +0.3% | Kansai, secondary spill to Kanto, Chubu | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

E-commerce Penetration Accelerates Appliance Uptake

E-commerce has achieved critical mass for appliances in Japan, with online channels accounting for 42.88% of appliance sales in 2024, second only to books and media within retail categories. Store-based multi-brand specialists still held 41.25% in 2025, yet online channels are projected to outpace them with a 5.12% CAGR through 2031 as buyers favor integrated discovery, payment, delivery, and installation flows. A blended approach defines the channel shift since leading chains coordinate inventory visibility and flexible pickup to reduce friction for time-pressed and senior shoppers. Japanet Takata illustrates this behavior by aggregating trade-in processing and white-glove installation for a base of 18.35 million users, which improves conversion among buyers who favor guided experiences. Manufacturers add augmented reality previews and live demonstrations that close the tactile gap that once anchored showroom visits. The revision of packaging recycling rules in 2025 has also pushed online sellers to disclose materials and offer eco-pack options, which aligns sustainability goals with digital convenience for the Japan kitchen appliances market[2]Ministry of Economy, Trade and Industry, “Packaging and Recycling Policy Updates,” METI, meti.go.jp .

Energy-Efficiency Standards Drive Replacement Demand

The Top Runner Programme governs efficiency benchmarks across major home appliances and requires models sold to meet or exceed weighted-average targets, which makes compliance a structural driver for replacements and upgrades. The program is in effect through 2030 and spans refrigerators, rice cookers, microwave ovens, and gas cooking appliances, thus covering most of the household electricity load. Consumer rebates under national and local schemes reimburse a meaningful share of the premium for compliant models, which shortens payback periods and shifts preferences toward inverter-based and high-insulation designs. Japan’s 7th Strategic Energy Plan targets deep reductions in energy-related emissions and raises the role of renewables by 2040, which steadily raises the performance baseline that appliance makers must meet. Utility bill increases in early 2026 further sharpened the consumer focus on high-efficiency refrigerators and IH cooktops, which helps sustain upgrade cycles even when volumes are stable. This policy-and-cost alignment supports a steady replacement rhythm that underpins the Japan kitchen appliances market through 2031.

Premiumization and Smart Upgrades in Urban Households

Premium connected products now anchor many urban upgrades, as buyers look for performance, ease, and ecosystem fit in smaller kitchens. Panasonic’s HomeCHEF Connect 4-in-1 multi-Oven integrates microwave, air fry, convection bake, and broil functions and syncs with the Panasonic Kitchen+ app and Fresco to automate settings, which offer convenience and versatility in a compact footprint. Sharp’s 2026 Celerity High-Speed Oven uses a Golden Heater and inverter control to compress cook times for full meals, which appeals to time-pressed professionals willing to pay for speed. Vendor-side pricing discipline and inventory return arrangements also reduce markdown risk and support stable retail pricing, which contributed to operating-profit uplift for leading brands during 2022–2024. Hitachi’s large-capacity refrigerator with a built-in camera and shelf-wide precision cooling showcases how connectivity extends value beyond the core hardware and into the broader smart-home context. As the average household size has declined, more buyers pick compact, high-spec models and attach service plans or supplies, which deepens lifetime value in the Japan kitchen appliances market.

Urban micro-kitchen trend spurring compact multi-function devices

The average apartment size in Tokyo has declined to 55 m², while single-person households now represent 38.1% of the national total[3]Cabinet Office of Japan, “Public Opinion Survey on Household Concerns,” Cabinet Office, cao.go.jp. Space scarcity propels demand for slim combination ovens, stackable air-fryer-toaster hybrids, and collapsible hot plates introduced by home-furnishing leader Nitori. Panasonic’s 6.7 kg Auto Cooker integrates sauté, stew, and bake functions within a 4.2-liter footprint, signaling how engineering advances condense versatility into countertop form factors. Compactness no longer sacrifices performance; instead, premium compact appliances command higher price-to-volume ratios. The wave of multifunctional designs keeps the Japan kitchen appliances market vibrant even as floor areas contract.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging demographics and stagnant household formation | -0.6% | National; acute in rural prefectures outside Kanto/Kansai | Long term (≥ 4 years) |

| Elevated electricity costs dampen discretionary upgrades | -0.4% | National, with a heavier burden on Hokkaido, Tohoku (cold-climate regions) | Medium term (2-4 years) |

| Yen depreciation raises import component costs | -0.3% | National; affects importers of European/North American brands | Short term (≤ 2 years) |

| Space-constrained kitchens limit large built-in adoption | -0.2% | Tokyo, Osaka metropolitan cores (average 55 m² apartments) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Demographics and Stagnant Household Formation

Japan’s aging profile reduces the pool of first-time buyers and tilts spending toward smaller, simpler devices that extend replacement cycles. Seniors account for a high share of households, and many buyers prefer voice control and ergonomic designs that reduce physical strain, which alters product mixes and lengthens refresh intervals. Smaller average household size also reduces the need for very large-capacity refrigerators or multi-burner ranges, a shift that directs innovation toward compact multi-function units and retrofit-friendly form factors. In this context, vendors focus more on replacement triggers tied to energy costs and convenience rather than on unit growth fueled by new household formation. Financial caution remains visible among seniors, with survey evidence pointing to inflation as a top concern, which constrains upgrades to premium tiers unless payback is clear. The net effect is a stable but selective demand profile that favors efficiency, user-friendly features, and service-backed offerings within the Japan kitchen appliances market.

Elevated Electricity Costs Dampen Discretionary Upgrades

Nine of ten regional utilities raised household tariffs in February 2026, and average household bills at Tokyo Electric Power Company rose to JPY 7,497 (USD 51.3) for the month, which elevated sensitivity to the running costs of high-consumption appliances. Wholesale spot prices spiked to JPY 13.37 per kWh (USD 0.09) on January 21, 2026, as heavy snow curbed solar output and LNG stocks tightened, reinforcing the push toward efficient models to mitigate bills. Wholesale power prices in the first half of 2025 averaged USD 76 per MWh, and futures pricing for 2026 pointed higher, which implies sustained operating cost focus for households and small businesses. Forecasts to fiscal 2034 indicate modest electricity-demand growth, yet capacity tightness could linger and keep upward pressure on prices, which tempers discretionary appliance refresh where payback is unclear. Real wages fell in late 2025, and the policy rate increased to 0.75% in December 2025, adding to financing costs, which together softened the appetite for non-essential big-ticket items. Government energy-bill relief remains temporary, and scheduled phase-outs risk renewed increases that may delay replacement of functioning legacy units within the Japan kitchen appliances market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Small Multi-Function Units Outpace Bulky Standalones

Large Kitchen Appliances accounted for 28.97% of revenue in 2025, while Small Kitchen Appliances are projected to post a 4.52% CAGR through 2031 as compact, versatile devices align with urban living constraints. Refrigerators, ovens, cooktops, range hoods, and dishwashers dominate the large segment, and replacements rise as efficiency rules tighten and subsidies improve payback for higher-spec models. Cooktops continue shifting toward induction heating as buyers pursue safety, cleanliness, and electrification compatibility that link to demand-response programs and local incentive schemes. The most resilient pockets of large-format demand reflect compliance-led refresh cycles and commercial spillover linked to tourism and hospitality upgrades, which sustain procurement even as household volumes remain steady. Compact and counter-depth introductions meet retrofit needs in older buildings, while quiet operation and better insulation expand appeal among seniors and small families.

The small-appliance cluster remains the bright spot for the Japan kitchen appliances market as single-person households and micro-living sharpen preferences for multi-function countertop devices. Panasonic’s 4-in-1 HomeCHEF Connect demonstrates the value of combining microwave, convection, air fry, and broil into one connected unit that fits modern use patterns[4]Panasonic Corporation, “HomeCHEF Connect Product Page,” Panasonic, panasonic.com . Design-first brands sustain premium willingness to pay where compactness does not mean compromise, as seen in Balmuda’s temperature-stable grills that double as statement pieces. Electric cookers and rice cookers retain cultural relevance, with leading models adding PFAS-free surfaces and smarter controls to meet wellness and sustainability expectations. Retail innovation at value price points, including foldable or stowable appliances, continues to attract urban renters who lack space for full-size gear but still seek variety in home cooking.

By End-User: Residential Dominates, Commercial Accelerates via Expo and Tourism

Residential installations held 87.25% of revenue in 2025, supported by entrenched cooking-at-home patterns and by product features that match aging-in-place needs such as voice-control and ergonomic layouts. Senior-led households have a high presence, which keeps a strong focus on usability, while urban dual-income buyers pull demand into connected, premium refrigeration and cooking suites. The extension of the Top Runner Programme and the availability of rebates compress payback windows for high-efficiency units and sustain the cadence of replacements as utility costs climb. Developers of rental housing are also bundling efficient built-ins to hit energy standards and market differentiation goals, which ensures a steady base of B2B residential demand beyond retail channels. Together, these currents support stable to modest growth in the Japan kitchen appliances market, even as household formation slows.

Commercial demand, while a smaller portion of the base, is projected to advance at 3.83% CAGR through 2031 as tourism recovers and event-driven upgrades lift hotel, restaurant, and institutional kitchens. Predictive maintenance or IoT-enabled diagnostics shorten downtime for dishwashers and cooking lines in busy operations, an important factor during peak occupancy or seasonal surges. Compliance with HACCP food safety and energy-management frameworks refreshes older fleets that no longer meet hygiene and efficiency thresholds, which channels capital toward modern, efficient equipment. Forward-looking pilots that explore hydrogen-based cooking show a willingness to test future energy vectors, even if near-term adoption remains limited to electrified solutions that meet current standards. These elements add a durable non-residential pillar to the Japan kitchen appliances market as hospitality and foodservice pursue productivity and energy control.

By Distribution Channel: Online Gains Outpace Brick-and-Mortar Incumbents

Multi-Brand Stores accounted for 41.25% of sales in 2025, but Online Channels are projected to grow at a 5.12% CAGR to 2031 as consumers favor full-service digital journeys that bundle trade-in, delivery, and installation. Specialty platforms with large user communities strengthen performance marketing and lifetime service attachment, which in turn improves economics for connected small appliances that benefit from digital engagement. Manufacturer-run brand outlets retain a role for shoppers who seek guidance across a full ecosystem, while department and home-center channels concentrate more in regional markets where online fulfillment is less optimized. The Japan kitchen appliances market is therefore moving toward a hybrid equilibrium in which physical stores and online channels reinforce each other at different stages of the journey.

B2B direct-from-manufacturer procurement remains important in build-to-rent and hospitality projects, which prize standardized specifications, bulk pricing, and streamlined installation. Component security has become a competitive lever in this channel, as seen in vertical integration moves to stabilize inputs for water heaters and built-in suites. Revised packaging and recycling guidelines that took effect in 2025 also influence retail operations and fulfillment, with new disclosure requirements shaping packaging choices and reverse logistics practices. As digital product visualization matures, customer education is shifting toward immersive assets, which further improves the conversion of compact and retrofit lines suited to apartments and smaller homes. This blend of retail and direct channels secures a broad reach for the Japan kitchen appliances market and keeps price competition in check through service differentiation.

Geography Analysis

Kanto commanded 33.65% of sales in 2025, anchored by Tokyo’s density and higher household incomes that support premium upgrades and omnichannel fulfillment at scale. Space constraints, such as a 55-square-meter average apartment size, push the adoption of compact counter-depth refrigerators and multi-function ovens that secure utility without large footprints. Specialty retail hubs strengthen discovery and service attachment, while connected features and efficiency rebates keep replacement demand steady for refrigerators and IH cooktops. The region’s mature base means growth is moderate, but absolute gains remain large given the starting scale of the Japan kitchen appliances market in Kanto.

Kansai is projected to lead regional growth with a 4.05% CAGR through 2031 on renovation cycles tied to tourism and hospitality upgrades, which lift both commercial equipment and premium residential built-ins. Refits near event venues expand installation of efficient dishwashers, combi-ovens, and induction ranges, and this momentum spills into residential projects as contractors standardize specifications for multi-unit developments. Product localization and brand investment also contribute, with global challengers building share through targeted campaigns and SKUs tailored to local preferences. This activity combines with the rising demand for retrofit-friendly compact units as younger renters concentrate on urban cars and favor multi-function appliances. As a result, the Japan kitchen appliances market in Kansai blends hospitality-driven capex with steady residential upgrades into a sustained growth profile.

Beyond the two largest regions, the rest of Japan shows slower growth due to older demographics, lower rates of new household formation, and higher sensitivity to energy costs in colder climates. Households in Hokkaido and Tohoku face larger winter energy burdens, which magnified the bite of early 2026 tariff increases and reinforced the case for high-efficiency appliances. Rural markets rely more on home centers and cooperatives for distribution, which shapes assortment and price points in favor of durable, efficient models that minimize long-term operating costs. Uniform packaging and recycling rules apply nationwide, and centralized e-commerce logistics help standardize compliance even where store networks are sparse. Tourism-focused zones such as resort areas still generate pockets of commercial equipment demand, which balances softer replacement cycles in aging communities. Together, these differences underscore a two-speed Japan kitchen appliances market in which urban regions sustain premiumization while regional markets center on efficiency and reliability.

Competitive Landscape

The Japan kitchen appliances market is moderately concentrated, with the top five domestic incumbents holding slightly over half of the combined share, while many niche brands and foreign entrants add competitive pressure. AQUA by Haier reached a significant share in freezers by volume in H1 2025, which demonstrates that focused category strategies can break through even in mature segments. Incumbents emphasize ecosystem breadth, efficient production, and pricing discipline to protect profitability, while design-led challengers and compact specialists explore premium niches and faster innovation cycles. Moves in component security and channel agreements aim to stabilize supply and retail execution, which reduces markdown risk and smooths sell-through across cycles. Investment in North American and European capacity tied to heat pumps and compressors also strengthens cross-category technology spillovers that influence kitchen platforms such as IH cooktops and inverter refrigeration.

Product strategies now center on compactness, connectivity, and premium finishes that suit urban kitchens. Panasonic’s HomeCHEF Connect integrates app control and recipe automation, which increases lifetime value through content and service attachment within the Japan kitchen appliances products market. Hitachi’s camera-enabled large-capacity refrigerator points to expanding roles for vision and sensing in everyday food management. Materials advances, such as Mitsubishi Electric’s Full-SiC and Hybrid-SiC power modules for appliances, promise lower losses and thinner form factors that benefit countertop designs and refrigeration. Compliance with evolving zero-energy and efficiency standards increases certification costs, which advantages larger players that amortize these expenses across multiple product families. Launch cadence remains brisk as vendors address retrofit needs with 24-inch formats, quiet operation, and flexible installation options.

Portfolio realignment and M&A continue to reshape competitive positions. In August 2025, Bosch acquired 100% of the Johnson Controls–Hitachi air-conditioning joint venture for about USD 8 billion, and Hitachi received JPY 211 billion (USD 1.46 billion) for its 40% stake, which freed capital to refocus on connected appliances and industrial IoT. Panasonic expanded European air-to-water heat pump capacity and partnered with tado°, which supports energy-service integration strategies that can extend into connected kitchens over time. Toshiba Lifestyle celebrated its 95th anniversary and opened a Tokyo Design Center to anchor user-centered innovation close to core markets. Vertical integration and supplier acquisitions, including in pumps and other critical components, help reduce volatility and ensure quality for built-in suites in both residential and commercial projects. Altogether, these steps reflect a steady push toward efficiency-led performance, connected experiences, and reliable fulfillment within the Japan kitchen appliances market.

Japan Kitchen Appliances Industry Leaders

Panasonic Corporation

Sharp Corporation

Hitachi Global Life Solutions, Inc.

Toshiba Lifestyle Products & Services Corporation

Mitsubishi Electric Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Sharp unveiled more than twenty new products at KBIS 2026, including the Celerity High-Speed Oven, a 24-inch Counter-Depth French Door Refrigerator, a 24-inch Wall Oven, Microwave Drawer Deco Series, a 3-in-1 Countertop Microwave, and quiet dishwashers, targeting retrofit-friendly installations in space-constrained apartments.

- February 2026: Rinnai introduced five new water-heating solutions at IBS 2026, including the RHPC Heat Pump Companion Kit, RECT Series Commercial Electric Tank, SENSEI RX Gas Tankless, REHP Electric Heat Pump, and I-SERIES Plus Condensing Gas Boiler.

- December 2025: Toshiba Lifestyle marked its 95th anniversary and highlighted the opening of its Tokyo Design Center, reinforcing its commitment to user-centered innovation in Asia-Pacific.

- November 2025: Noritz resolved to acquire Ogihara Mfg. Co. Ltd, a miniature-pump manufacturer, as a wholly owned subsidiary to secure component supply and enhance quality control for water-heater systems.

Japan Kitchen Appliances Market Report Scope

The Japan kitchen appliances market includes both large built-in or freestanding appliances used for primary cooking and food storage, as well as small countertop appliances used for preparation and convenience cooking. A complete background analysis of the market, including the analysis of market size and forecast, market shares, industry trends, growth drivers, and vendors, is provided.

The Japan Kitchen Appliances Market is segmented by Product, End User, Distribution Channel, and Geography. By product, the market is divided into Large Kitchen Appliances and Small Kitchen Appliances. By end user, the market is categorized into Residential and Commercial segments. By distribution channel, the market is segmented into B2C/Retail and B2B channels. The B2C/Retail segment is further divided into multi-brand stores, exclusive brand outlets, and online channels. Geographically, the market analysis covers Kanto, Kansai, Chubu, and the Rest of Japan. The report provides market size and forecasts for the Japan kitchen appliances market in value (USD) across all the above segments.

By Product

| Large Kitchen Appliances | Refrigerators & Freezers |

| Dishwashers | |

| Range Hoods | |

| Cooktops | |

| Ovens | |

| Other Large Kitchen Appliances | |

| Small Kitchen Appliances | Food Processors |

| Juicers and Blenders | |

| Grills and Roasters | |

| Air Fryers | |

| Coffee Makers | |

| Electric Cookers | |

| Toasters | |

| Electric Kettles | |

| Countertop Ovens | |

| Other Small Kitchen Appliances (bread makers, waffle makers, egg cookers, etc.) |

By End-User

| Residential |

| Commercial |

By Distribution Channel

| B2C/Retail | Multi-brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| B2B (directly from the manufacturers) |

By Geography

| Kanto |

| Kansai |

| Chubu |

| Rest of Japan |

| By Product | Large Kitchen Appliances | Refrigerators & Freezers |

| Dishwashers | ||

| Range Hoods | ||

| Cooktops | ||

| Ovens | ||

| Other Large Kitchen Appliances | ||

| Small Kitchen Appliances | Food Processors | |

| Juicers and Blenders | ||

| Grills and Roasters | ||

| Air Fryers | ||

| Coffee Makers | ||

| Electric Cookers | ||

| Toasters | ||

| Electric Kettles | ||

| Countertop Ovens | ||

| Other Small Kitchen Appliances (bread makers, waffle makers, egg cookers, etc.) | ||

| By End-User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail | Multi-brand Stores |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| B2B (directly from the manufacturers) | ||

| By Geography | Kanto | |

| Kansai | ||

| Chubu | ||

| Rest of Japan | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the Japan kitchen appliances market?

The Japan kitchen appliances products market size is USD 10.43 billion in 2025, is expected to be USD 10.69 billion in 2026, and is projected to reach USD 12.32 billion by 2031 at a 2.88% CAGR.

Which product categories are leading and growing fastest in Japan?

Large Kitchen Appliances led in 2025 with 28.97% revenue share, while Small Kitchen Appliances is the fastest-growing, projected at a 4.52% CAGR to 2031.

What are the main drivers supporting upgrades and replacements?

Tighter efficiency standards under the Top Runner Programme and rebate schemes that offset premium prices are pushing replacements for refrigerators, cooktops, and other appliances.

Which regions matter most for growth?

Kanto held 33.65% of 2025 sales, while Kansai is projected to be the fastest-growing region at 4.05% CAGR through 2031.

Who are the key competitors in Japan, and how concentrated is the space?

The top five domestic players hold slightly over half of the combined share, while challengers such as AQUA by Haier have made gains, including a significant share in freezers by volume in H1 2025.

Page last updated on: