Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

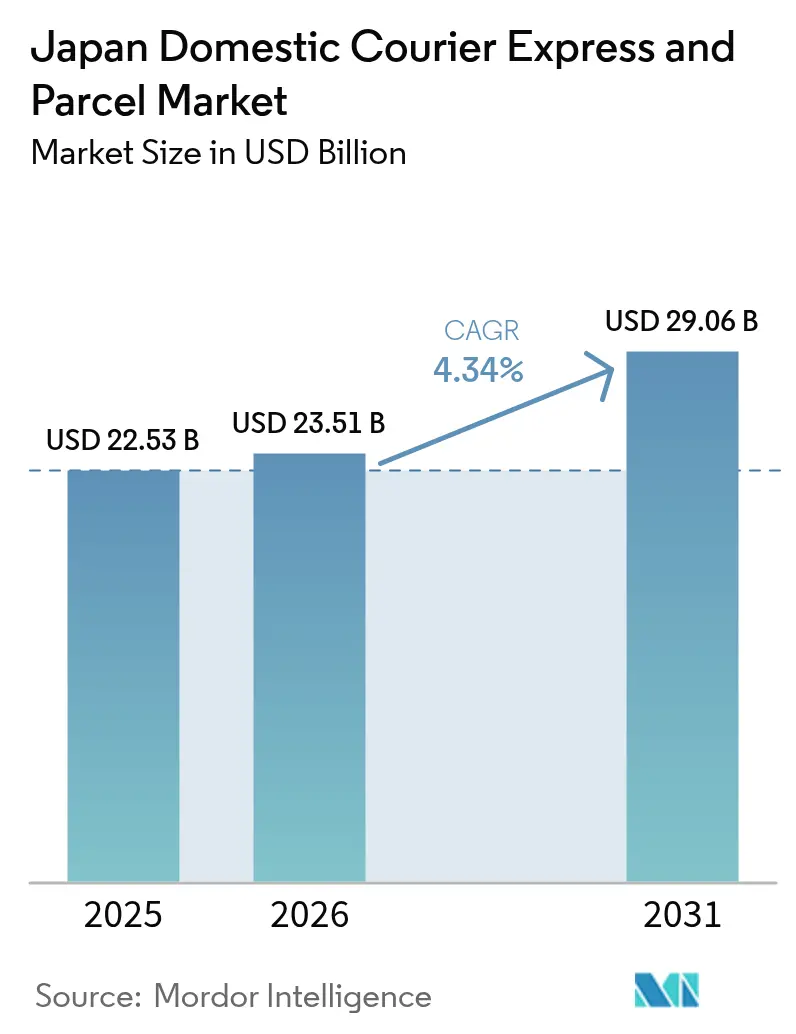

| Base Year Market Size (2025) | USD 22.53 Billion |

| Market Size (2026) | USD 23.51 Billion |

| Market Size (2031) | USD 29.06 Billion |

| Growth Rate (2026 - 2031) | 4.34% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Domestic Courier Express And Parcel Market Analysis by Mordor Intelligence

The Japan Domestic Courier Express And Parcel Market size was valued at USD 22.53 billion in 2025 and estimated to grow from USD 23.51 billion in 2026 to reach USD 29.06 billion by 2031, at a CAGR of 4.34% during the forecast period (2026-2031). Steady e-commerce demand, demographic aging, and tighter service-level expectations underpin this trajectory. Carriers offset slowing volume growth through premium, value-added services and targeted surcharges that lift revenue per shipment. Structural driver shortages caused by the 2024 overtime cap motivate accelerated automation, electric-vehicle rollouts, and micro-hub networks that lift fleet productivity. Heightened environmental regulation and voluntary net-zero pledges also push operators to modernize assets while differentiating on sustainable delivery credentials. Competitive pressure from gig-economy platforms remains intense, yet established firms retain an edge through nationwide coverage, convenience-store alliances, and trusted handling of regulated goods.

Key Report Takeaways

- By speed of delivery, non-express services held 75.40% of the Japan domestic courier market share in 2025; express services are projected to grow the fastest at a 4.98% CAGR between 2026-2031.

- By shipment weight, light weight shipments accounted for 72.10% of the Japan domestic courier market size in 2025, but medium weight shipments are forecast to expand at 4.45% CAGR between 2026-2031.

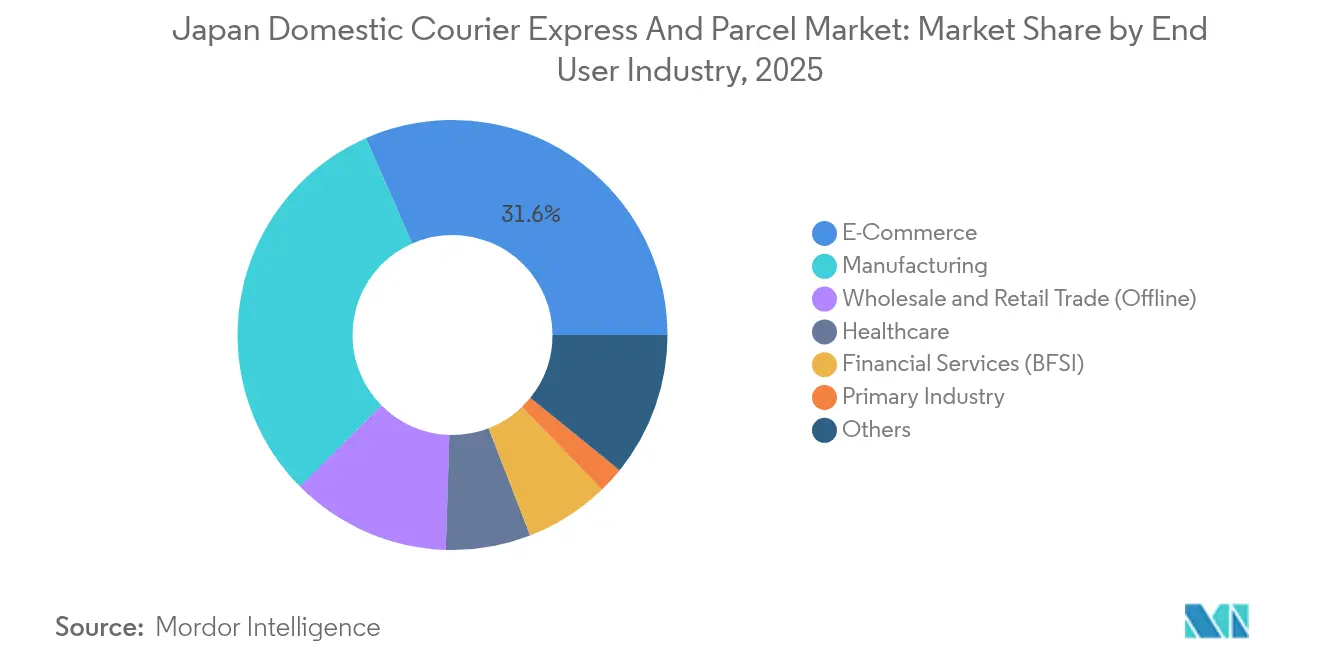

- By end user industry, E-Commerce commanded 31.60% revenue share in 2025, while manufacturing is expected to record the highest segment CAGR at 4.55% between 2026-2031.

- By model, the business-to-consumer (B2C) segment represented 42.95% of the Japan domestic courier market share in 2025; the business-to-business (B2B) segment is predicted to advance at 5.60% CAGR between 2026-2031.

- By mode of transport, road transport retained 49.10% revenue in 2025, whereas air transport is projected to post a 4.96% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Domestic Courier Express And Parcel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth in B2C parcel volumes driven by E-commerce purchases | +1.2% | National, Tokyo–Osaka corridor | Short term (≤ 2 years) |

| Accelerating adoption of same-day delivery services and quick-commerce models | +0.8% | Major cities | Medium term (2-4 years) |

| Increasing deployment of electric and alternative-fuel vehicles reduces operating costs and emissions | +0.6% | Nationwide metro first | Long term (≥ 4 years) |

| Ageing population drives higher demand for home healthcare parcel deliveries | +0.7% | Nationwide, rural skew | Medium term (2-4 years) |

| Expanding convenience-store pickup and drop-off networks improve delivery efficiency | +0.5% | Nationwide | Short term (≤ 2 years) |

| Rising cross-border small-parcel inflows via Narita and Kansai airports feed domestic deliveries | +0.4% | Airport hinterlands | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth in Business-to-Consumer (B2C) Parcel Volumes Driven by E-Commerce Purchases

E-commerce gross merchandise value (GMV) rose from USD 176.50 billion in 2024 to USD 201.40 billion in 2025, pushing the Japan domestic courier market toward denser residential delivery rounds[1]Ministry of Economy, Trade and Industry, “FY2023 E-Commerce Market Survey,” meti.go.jp. Smaller, more frequent orders reduce average parcel weight and strain hub capacity, prompting the rapid rollout of micro-sortation facilities inside urban boundaries. Cross-border marketplaces such as Temu add customs-clearance complexity that established carriers monetize through brokerage fees. Food and beverage online sales climbed to USD 48.46 billion in 2025, stimulating chilled-parcel lanes that command premium tariffs yet require additional handling infrastructure. Live-streaming flash sales create unpredictable peaks, leading operators to blend gig-worker fleets with fixed resources for surge coverage. Large platforms, notably Amazon Japan and Rakuten, wield buying leverage that compresses headline rates, so couriers emphasise service reliability and flexible delivery windows.

Accelerating Adoption of Same-Day Delivery Services and Quick-Commerce Models

Same-day fulfillment has shifted from an optional feature to a baseline expectation, as 7-Eleven’s 7NOW service targets USD 1 billion sales through 20,000 outlets in 2025. Quick-commerce dark stores support 20-minute urban drop-offs, bypassing regional depots and placing inventory within five kilometers of consumers. Lawson and Uber Eats introduced sidewalk robots carrying 30 kg payloads on fixed routes, mitigating labor limits during peak shifts. Tele-pharmacy pilots in Osaka enable patients to receive prescriptions the same day, blending medical compliance with express logistics. Artificial-intelligence route engines shrink arrival windows from forty to ten minutes, improving asset utilization without proportional headcount growth. However, only 10% of shoppers select express tiers, and willingness to pay offsets higher cost per stop, preserving margins in premium subsegments.

Increasing Deployment of Electric and Alternative-Fuel Vehicles Reduces Operating Costs and Emissions

Yamato obtained approval to mass-produce conversion kits that electrify existing light trucks at one-third the price of new EVs[2]Yamato Mobility & Mfg., “EV Conversion Kit Mass Production Approval,” prtimes.jp. SBS Holdings already runs 72 electric vans and plans 20 more in 2025, demonstrating fleet-wide scalability. Diesel averaged USD 1.11 per liter in 2024, elevating the cost advantage of stable-priced electricity. Refrigerated EV trucks supplied by Konoike Transport for Aeon stores prove cold-chain viability over 120 km routes. FamilyMart’s machine-learning dispatcher cut CO₂ by 12.8% versus 2017 baselines through smarter route sequencing. A new sustainable aviation fuel agreement between Sagawa Express and DHL lowers the greenhouse-gas intensity of express air consignments by 10%[3]Sagawa Express, “Sustainable Aviation Fuel Agreement with DHL,” prtimes.jp.

Ageing Population Drives Higher Demand for Home Healthcare Parcel Deliveries

Citizens aged 65 or above will reach 29% of Japan’s population in 2025, spurring growth in prescription and device shipments that require temperature control and chain-of-custody proof. Market value for healthcare delivery services is projected at JPY 1.76 billion (USD 0.012 billion) in 2025. Drone lanes piloted by Alfresa move medicine to remote clinics, reducing lead times during disaster events. Same-day pharmacy-to-home integrations in metropolitan areas bundle tele-consultation with last-mile fulfillment, creating combined service revenue streams. Declines in postal mail create capacity gaps that private couriers now fill for rural medical replenishment. Long-term care reforms anchor stable contract volumes, making healthcare a defensive growth pocket within the Japan domestic courier market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor shortages intensified by overtime cap inflate delivery costs | -1.1% | Nationwide, rural acute | Short term (≤ 2 years) |

| Introduction of urban congestion pricing increases per-parcel surcharges in major cities | -0.4% | Tokyo, Osaka, Nagoya | Medium term (2-4 years) |

| Price competition from gig-economy couriers erodes margins in same-day segment | -0.6% | Dense urban districts | Medium term (2-4 years) |

| Delayed regulatory approvals for drones and sidewalk robots postpone automation savings | -0.3% | Pilot test areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Labor Shortages Intensified by Overtime Cap Inflate Delivery Costs

Japan’s 2024 rule capping truck-driver overtime at 960 hours triggers immediate productivity loss, with 30% of firms still reporting non-compliance after twelve months[4]NHK, “Driver Overtime Regulation Compliance Survey,” nhk.or.jp. Surveys show 46.8% of shippers pay higher freight rates, while 41.2% cannot secure enough drivers, pushing wages up and raising per-parcel expenditure. Small haulers possess limited capacity to absorb surcharges due to scale limitations. Enforcement strength rose in 2025 when regulators revoked licenses for 2,500 Japan Post vehicles following health-check lapses, signaling tougher industry policing. Government draft guidelines on subcontractor remuneration may lift baseline freight tariffs, squeezing margins for operators tied to fixed-price e-commerce contracts.

Price Competition From Gig-Economy Couriers Erodes Margins in Same-Day Segment

App-based networks such as Uber Direct and Amazon Flex mobilize flexible driver pools that undercut conventional pricing, especially on short urban hops. Lawson stores integrate with Uber robots, blending autonomous hardware and gig riders to maintain low overheads. AnyCarry’s platform extends similar cost structures to corporate accounts, challenging traditional rate cards. Established carriers thus confront a margin squeeze, balancing service reliability against customers’ appetite for lower fees. New-entrant claims of “logistics that never refuse” set fresh service benchmarks that raise consumer expectations. Pending legislation on gig-worker status could alter the cost hierarchy, yet uncertainty persists over enforcement timelines and benefit obligations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User Industry: Manufacturing Ups the Growth Pace

Manufacturing climbs fastest at a 4.55% CAGR (2026-2031) as smart-factory rollouts shrink batch sizes and raise shipment frequency. Direct-to-plant supply contracts require tight delivery windows and real-time visibility. Carriers integrate API feeds with shop-floor systems, embedding themselves into replenishment cycles. The e-commerce sector stays the largest at 31.60% share of 2025 revenue, driven by sustained uptake of digital shopping and cross-border marketplace transactions.

Healthcare gains strategic importance despite small absolute volume. Regulatory tracking and cold-chain mandates support premium rates that cushion overall yields for operators with certified facilities. Financial services and legal firms continue to use secure courier hand-offs for critical documents, though absolute growth remains modest. Retailers with legacy store networks adopt ship-from-store schemes, blurring lines between pure digital and bricks-plus-clicks fulfillment.

By Speed of Delivery: Express Services Expand on Premium Demand

Express services generated the fastest sub-segment growth, advancing at 4.98% CAGR between 2026-2031. Although Non-Express retains revenue leadership with 75.40% share in 2025, mounting customer preference for guaranteed delivery windows fuels express lane upgrades across the Japan domestic courier market. Same-day and next-day expectations once associated exclusively with premium tiers are migrating toward mainstream offerings as omnichannel retailers race to match instant-gratification benchmarks. Investments in autonomous sidewalk robots and AI routing compress transit times at competitive cost, reshaping the boundary between classic Express and standard parcels.

Express carriers leverage value-added options, temperature control, secure ID verification, and late-night slots to justify pricing premiums. The restrained competitive set limits price erosion and sustains above-average yields. Meanwhile, Non-Express networks innovate via parcel lockers, neighborhood pick-up counters, and data-driven load pooling that shorten actual arrival times without formal service-level upgrades. Over the forecast period, carriers are expected to calibrate service menus that align price points with finely segmented delivery urgency, preserving revenue diversity within the Japan domestic courier market.

By Model: Business-to-Business (B2B) Shipments Gather Momentum

The business-to-business (B2B) sub-segment outpaces the market at a 5.60% CAGR between 2026-2031, mirroring lean-inventory moves and the growth of small-batch supplier relationships. Predictable order cycles enable route consolidation that boosts vehicle fill and reduces delivery cost per kg. Unified dashboards give corporate clients continuous status feeds, embedding courier performance into procurement metrics.

Business-to-consumer (B2C) maintains leadership at 42.95% revenue share in 2025, but faces rising service-quality expectations coupled with price resistance. Subscription commerce and automatic replenishment services may temper growth variability by smoothing volume peaks. Consumer-to-consumer (C2C) remains a steady avenue for recommerce and peer-to-peer exchanges, benefiting from platform-provided labels and simplified returns.

By Shipment Weight: Medium Weight Shipments Rebound

Light weight shipments (less than 5 Kg) dominate the Japan domestic courier market size, securing 72.10% revenue share in 2025, a direct outcome of online retail’s cadence of small-basket orders. Profitability pressures arise as cubic-volume revenue lags handling frequency growth. Electric-conversion light trucks help reclaim margin by cutting propulsion and maintenance costs. The medium weight shipments band between 5 kg and 31.5 kg posts a 4.45% CAGR between 2026-2031, powered by manufacturers shipping components direct to plant lines and SMEs executing drop-shipment models.

Industrial digitalization encourages higher-value parcelization, with on-demand spare-part dispatch replacing pallet moves. Carriers that equip depots for forklift-assisted parcel lanes and deploy weight-profiling sorters tap this rebound. Heavy shipments above 31.5 kg remain niche yet stable, serving construction and capital-equipment after-sales. Specialized handling competency and lift-gate fleets preserve competitive insulation for providers that commit to safety and compliance.

By Mode of Transport: Air Cargo Expands Within a Road-Heavy Network

Road transport captured 49.10% of 2025 revenue, reflecting Japan’s dense expressway grid and the flexibility of truck-based last-mile. Nevertheless, the 4.34% Japan domestic courier market CAGR (2026-2031), combined with driver scarcity, accelerates modal diversification. Domestic air consignments rise at 4.96% CAGR (2026-2031) as Narita and Kansai airport expansions elevate belly-hold capacity and shorten cut-off times for overnight lanes.

Rail and coastal shipping stay limited to niche applications owing to transload requirements. Looking forward, government trials of conveyor-belt freight corridors and highway platooning could realign modal economics by reducing dependency on human drivers, reshaping long-haul portions of the Japan domestic courier market.

Geography Analysis

Metropolitan prefectures stretching from Tokyo through Kanagawa, Aichi, and Osaka concentrate the lion’s share of parcel origin and destination flows, underpinning route density that supports advanced automation rollouts. Same-day delivery demand thrives here, assisted by dense convenience-store networks and multi-tenant micro-fulfilment nodes. Urban congestion schemes proposed for central Tokyo may levy access fees that raise per-stop costs, nudging carriers toward sidewalk robots and bicycle couriers for inner-city hops.

Second-tier regional cities such as Fukuoka and Sapporo exhibit rising online retail penetration but present softer density, requiring hybrid drop-off options to maintain economics. Rural prefectures face sharper demographic aging, with healthcare deliveries and government document logistics forming core demand in these zones. Drone trials over mountainous terrain aim to compensate for long road detours and limited driver availability, promising to extend service coverage without continuous human presence.

International gateway regions enjoy spill-over parcel inflows from inbound cross-border e-commerce. Cargo-friendly customs regimes at Narita and Kansai accelerate domestic transfer, making surrounding prefectures attractive for sortation investment. Climate initiatives influence routing strategy nationwide; FamilyMart’s 12.8% CO₂ drop arose from algorithms calibrated to specific regional traffic patterns, suggesting further gains by localizing route logics.

Competitive Landscape

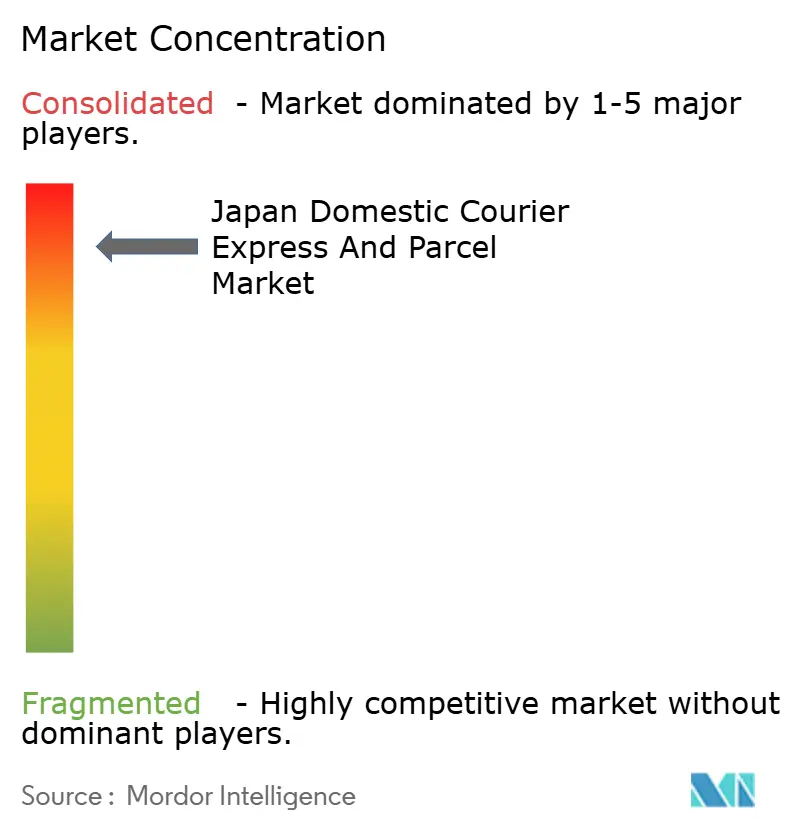

Three incumbents, Yamato Holdings, Sagawa Express (SG Holdings), and Japan Post Group, anchor the Japan domestic courier industry by virtue of nationwide depots, branded fleets, and customer trust. Their combined coverage secures enterprise accounts and regulated-goods contracts. Yet, regulatory scrutiny tightened when authorities revoked 2,500 Japan Post vehicle permits in June 2025, demonstrating reputational risk tied to compliance lapses.

Incumbents invest heavily in electrification and robotics to stabilize cost bases. Yamato’s conversion-kit approval yields capital-light fleet renewal, while Sagawa pairs with DHL on sustainable aviation fuel to differentiate international offerings. Medium-sized challengers pursue specialization, medical, temperature-controlled, or reverse logistics to build defensible niches. Gig-economy aggregators disrupt pricing in high-density urban districts by mobilizing flexible labor and autonomous rigs. anyCarry, Uber Direct, and Amazon Flex extend capacity without owning trucks, accelerating price discovery toward variable on-demand tariffs. Small local carriers grapple with rising compliance and technology investment thresholds, prompting partnerships or acquisitions by scale-seeking networks.

Convenience-store alliances form a critical competitive lever. 7-Eleven, Lawson, and FamilyMart integrate pick-up counters and micro-fulfillment space, offering exclusive access to tens of thousands of storefronts. Carriers unable to secure such tie-ups risk higher last-mile costs and weaker consumer brand presence. Over the forecast horizon, inorganic consolidation and technology joint ventures are set to redraw market shares as players strive to attain the scale needed to invest in electrification, AI, and automation.

Japan Domestic Courier Express And Parcel Industry Leaders

Yamato Holdings Co., Ltd.

SG Holdings Co., Ltd. (Sagawa Express)

Japan Post Holdings Co., Ltd.

Nippon Express Holdings

Seino Holdings Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Japan Post Holdings faced permit cancellation for 2,500 postal trucks due to improper driver health-check procedures, disrupting nationwide network capacity.

- April 2025: Yamato Mobility & Mfg. received mass-production approval for electric conversion kits that lower fleet upgrade costs by two-thirds.

- April 2025: SG Holdings’ Sagawa Express signed a sustainable aviation fuel partnership with DHL Japan, targeting a 10% emissions reduction on international routes.

- September 2024: Nippon Express Holdings launched the “NX Universal Harmonious Work Warehouse” pilot integrating mobility robots to mitigate labor shortages.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, our study treats the Japan domestic courier, express, and parcel (CEP) market as all revenue generated inside the country from the pickup, transport, and final hand-off of small consignments up to 30 kg that move on scheduled parcel networks by road or domestic air shuttle.

Scope Exclusion: Cross-border export or import flows handled under international waybills fall outside this definition.

Segmentation Overview

- Speed of Delivery

- Express

- Non-Express

- Shipment Weight

- Heavy Weight Shipments

- Light Weight Shipments

- Medium Weight Shipments

- End User Industry

- E-Commerce

- Financial Services (BFSI)

- Healthcare

- Manufacturing

- Primary Industry

- Wholesale and Retail Trade (Offline)

- Others

- Model

- Business-to-Business (B2B)

- Business-to-Consumer (B2C)

- Consumer-to-Consumer (C2C)

- Mode of Transport

- Road

- Air

- Others

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed fleet managers, third-party logistics executives, union representatives, and technology vendors across Kanto, Kansai, and Kyushu. These discussions confirmed redelivery ratios, overtime impacts, and average stop densities that refine desk-based assumptions.

Desk Research

We start by compiling time-series parcel volume, traffic, and vehicle statistics released by the Ministry of Land, Infrastructure, Transport and Tourism and the Japan Post annual postal review, alongside e-commerce gross merchandise value from the Ministry of Economy, Trade and Industry. Company filings, tariff notices, and investor presentations map carrier pricing drift. Paid platforms such as D&B Hoovers and Dow Jones Factiva support financial validation and news tracking, while Questel patents highlight automation intensity and Volza shipment data anchor domestic versus inbound flows. This list is illustrative, and many other public datasets and trade bulletins aided data collection and clarification.

Market-Sizing & Forecasting

We first derive the baseline value through a top-down rebuild that links MLIT parcel counts with sampled average revenue per parcel, reconstructed by weight band and delivery speed. Select bottom-up checks, such as carrier revenue roll-ups and B2C shipment audits, calibrate the totals. Key variables feeding the model include e-commerce GMV, parcel redelivery rate, fuel cost index, driver vacancy rate, and urban population density. A multivariate regression projects each driver to 2030, and scenario analysis stress tests labor and fuel shocks. Gaps in bottom-up data, especially for micro couriers, are bridged using modeled penetration factors benchmarked through expert calls.

Data Validation & Update Cycle

Outputs undergo a two-step analyst review. Outliers are flagged against carrier quarterly sales and MLIT monthly volumes, and we re-contact sources when swings exceed preset bands. The model refreshes each year, with interim updates after material regulatory or wage shifts.

Why Our Japan Domestic CEP Baseline Earns Trust

Published estimates often diverge because firms slice the market differently or apply untested price multipliers. One external study pegs 2024 domestic CEP at USD 24.90 billion, while another stretches to USD 33 billion. These gaps arise from scope creep into cross-border flows and from uniform average-price assumptions that ignore Japan's heavy mix of sub-5 kg parcels.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 22.53 B (2025) | Mordor Intelligence | - |

| USD 24.90 B (2024) | Global Consultancy A | Includes international parcels and applies straight-line e-commerce extrapolation |

| USD 33.00 B (2024) | Regional Consultancy B | Blends trucking freight revenue with parcel earnings and uses single ASP across weight bands |

The comparison shows that Mordor's disciplined scoping, variable-level adjustments, and annual refresh provide a balanced, transparent baseline that decision-makers can trace and replicate with confidence.

Key Questions Answered in the Report

What is the current size of the Japan domestic courier market?

The market is valued at USD 23.51 billion in 2026 and is projected to grow to USD 29.06 billion by 2031.

How fast is the Japan domestic courier market expected to grow?

It is forecast to register a 4.34% CAGR from 2026 to 2031.

Which segment is growing the quickest within the Japan domestic courier market?

Express delivery services lead growth with a projected 4.98% CAGR between 2026-2031.

How are labor shortages being addressed by courier companies?

Carriers accelerate automation, deploy electric vehicles, and add autonomous robots to boost productivity while reducing reliance on human drivers.

Why is healthcare delivery a strategic focus?

Japan’s aging population and expanding tele-medicine adoption create specialized, higher-margin shipment demand for pharmaceuticals and medical equipment.

What role do convenience stores play in courier logistics?

Over 55,000 convenience stores act as pick-up and drop-off points and micro-fulfillment hubs, improving last-mile efficiency and consumer accessibility.

Page last updated on: