Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

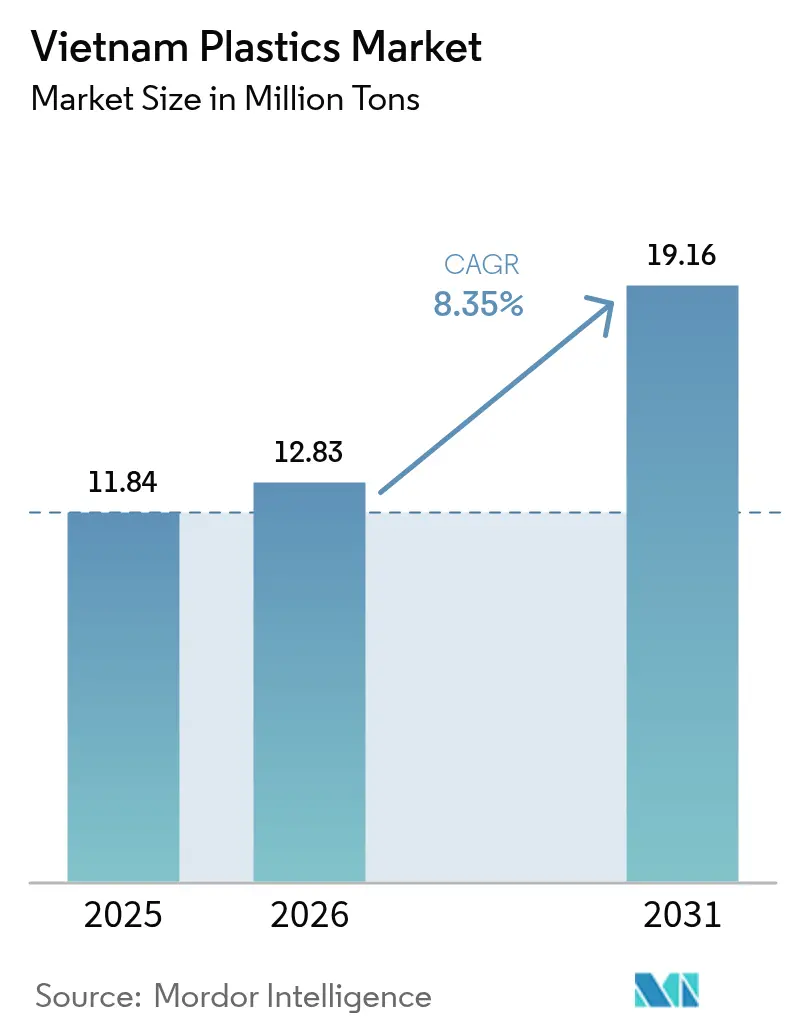

| Base Year Market Size (2025) | 11.84 Million tons |

| Market Volume (2026) | 12.83 Million tons |

| Market Volume (2031) | 19.16 Million tons |

| Growth Rate (2026 - 2031) | 8.35% CAGR |

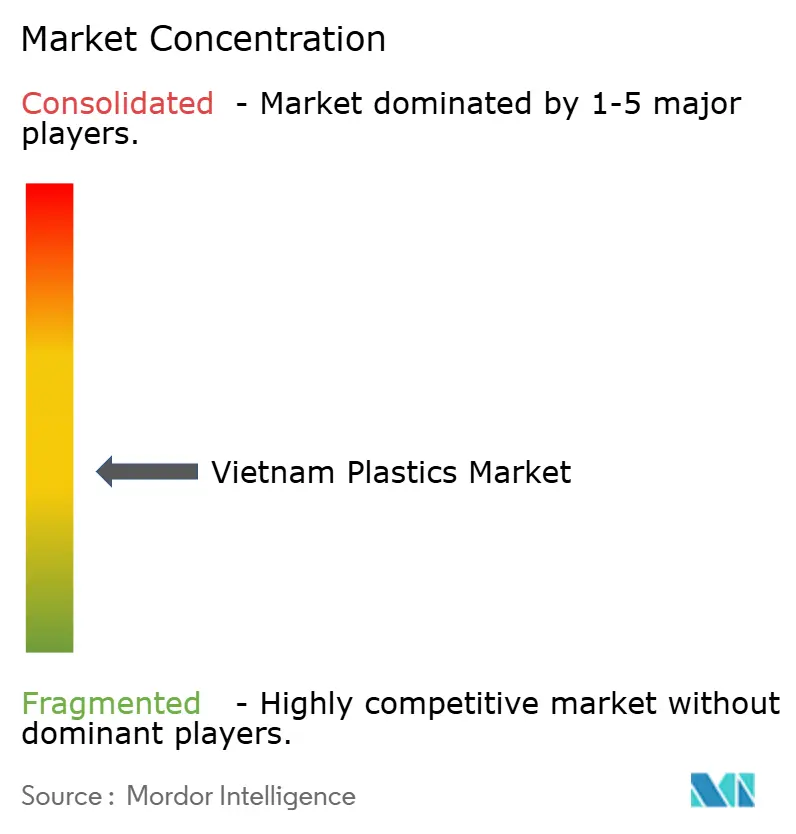

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Plastics Market Analysis by Mordor Intelligence

Vietnam Plastics Market size in 2026 is estimated at 12.83 million tons, growing from 2025 value of 11.84 million tons with 2031 projections showing 19.16 million tons, growing at 8.35% CAGR over 2026-2031. Robust foreign direct investment, aggressive infrastructure outlays, and decisive regulatory modernization converge to position Vietnam as Southeast Asia’s fastest-growing plastics hub. Manufacturing relocation from China continues to swell downstream consumption, while construction investments—up 40% year over year in H1 2025—channel steady demand for pipes, profiles, and insulation materials. Local converters prioritize throughput over experimentation, scaling extrusion lines to meet surging orders. Simultaneously, sustainability mandates accelerate bioplastics adoption, nudging resin suppliers to diversify feedstocks and recycle content even as imported naphtha and propylene remain cost-sensitive inputs.

Key Report Takeaways

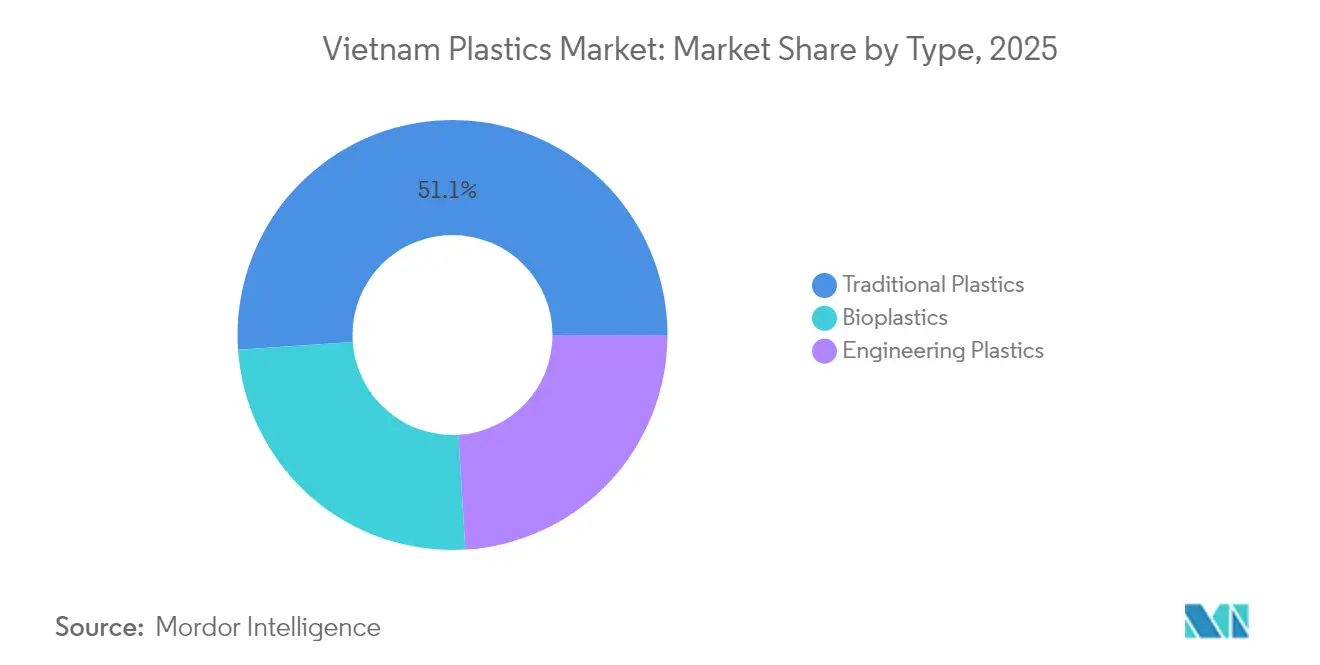

- By type, traditional plastics command 51.10% market share in 2025; however, bioplastics are forecast to expand at a 12.55% CAGR through 2031.

- By technology, extrusion held 61.35% of the Vietnam plastics market share in 2025. Extrusion is also projected to post the fastest 10.12% CAGR through 2031.

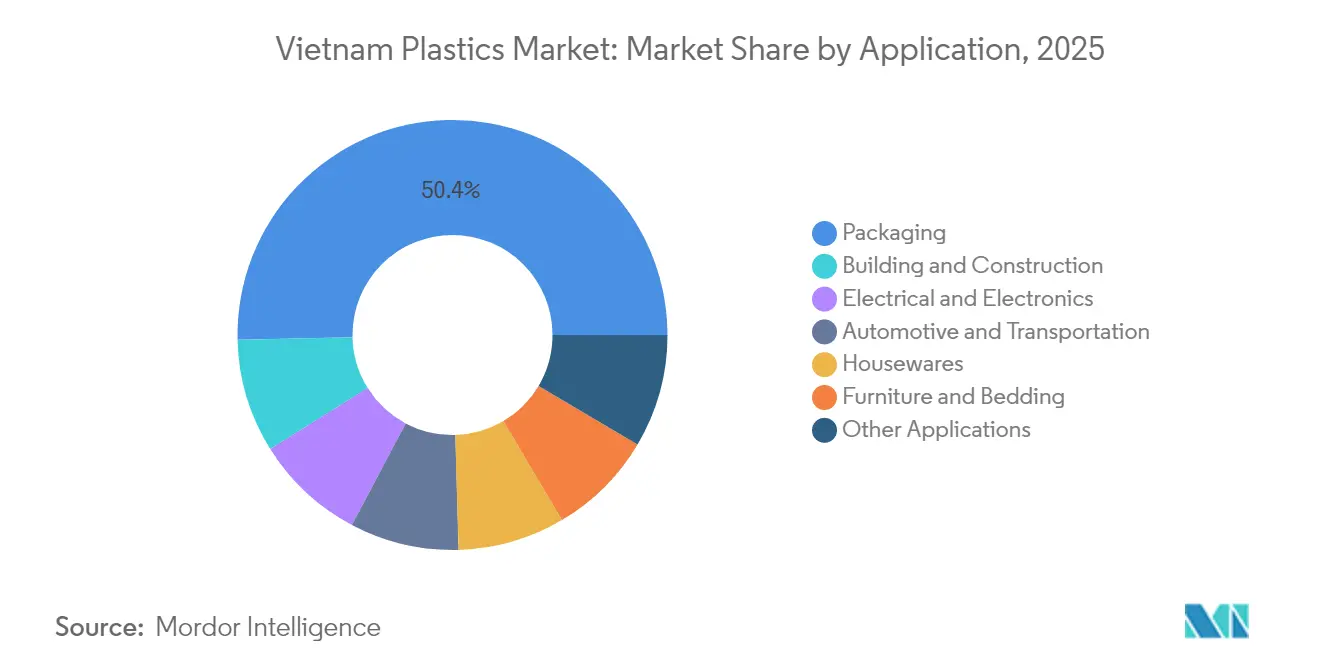

- By application, packaging accounted for 50.35% of the Vietnam plastics market size in 2025 and is projected to rise at an 8.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Plastics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust Growth in Domestic Construction Projects | +2.1% | National, with concentration in Ho Chi Minh City, Hanoi, Da Nang | Medium term (2-4 years) |

| Booming Food-grade & E-commerce Packaging Demand | +1.8% | National, with spillover to ASEAN export markets | Short term (≤ 2 years) |

| Rising Foreign Direct Investment in Downstream Resin Conversion | +2.3% | Northern provinces (Bac Ninh, Hung Yen), Southern industrial zones | Long term (≥ 4 years) |

| Surge in Automotive & Electronics Relocation to Vietnam | +1.9% | Regional clusters in Bac Ninh, Quang Ninh, Ba Ria-Vung Tau | Medium term (2-4 years) |

| Government Incentives for Recycled-content Resins | +0.3% | National, with pilot programs in major cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Robust Growth in Domestic Construction Projects

Infrastructure spending climbed 40% year over year in H1 2025 after disbursement timelines were cut from weeks to 1-3 days[1]Vietnam Chamber of Commerce and Industry, “Infrastructure Investment Report H1 2025,” vcci.vn. Demand for PVC pipes, insulation boards, and flame-retardant cable trays has soared, reflecting Vietnam’s status as a cost-competitive construction center with costs still 60%-65% below Singapore levels. Data center projects outpace factory builds, elevating requirements for halogen-free compounds and heat-resistant engineered resins. Circular 10/2024/TT-BXD mandates quality checks on imported building materials, a policy that favors local converters able to document compliance. Together, these trends funnel volume and value growth into the Vietnam plastics market.

Booming Food-grade & E-commerce Packaging Demand

Vietnam’s food processing output reached USD 79.3 billion in 2024, up 7.4%, just as e-commerce adoption leapt across urban centers. As a result, converters face parallel requirements for barrier films that prolong shelf life and lightweight mailers that cut shipping costs. Protective cushioning for electronics—imports of components rose 29.3% through March 2025—adds further pull for cushioning foams and molded inserts. Government preference programs that spotlight locally made packaging tilt procurement toward domestic suppliers, encouraging capital upgrades in printing, lamination, and multilayer extrusion lines.

Rising Foreign Direct Investment in Downstream Resin Conversion

Foreign direct investment surged 32% in H1 2025, with multinationals building component plants rather than importing finished parts. Samsung Display’s USD 1.8 billion OLED module line in Bac Ninh lifts demand for optical films and precision housings, while Foxconn’s USD 287.2 million console facility in Quang Ninh will need high-impact polystyrene and ABS grades for casings[2]CafeF, “Samsung Display Expands OLED Capacity in Vietnam,” cafef.vn . Local converters gain from contract manufacturing volumes and technology transfer, locking in long-run orders that underpin capacity expansion plans.

Surge in Automotive & Electronics Relocation to Vietnam

Vietnamese vehicle plants now hit local-content thresholds above 40%, unlocking zero-tariff ASEAN exports that require durable under-hood components, acoustic insulation, and lightweight trim. Electronics assemblers join the migration, stirring orders for connector housings and Electromagnetic Induction (EMI)-shielded enclosures as imports of parts swell. Combined, these sectors diversify demand and help insulate converters from single-industry downturns.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heavy Dependence on Imported Naphtha and Propylene | -1.40% | National, with concentration in petrochemical complexes | Short term (≤ 2 years) |

| Escalating Environmental Activism Against Single-use Plastics | -0.80% | Urban centers, with policy spillover nationwide | Medium term (2-4 years) |

| Rising Competition from Bio-based Substitutes in FMCG | -0.60% | Consumer goods segments, concentrated in Ho Chi Minh City and Hanoi | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Heavy Dependence on Imported Naphtha and Propylene

Vietnam imported more than 5.5 million tons of plastic feedstock in the first 7 months of 2025, largely from China, South Korea, and Taiwan. SCG’s Long Son complex came online in August 2025 with a 1.4 million tons capacity, yet it still covers only a slice of domestic demand. Feedstock expenses, 60%-70% of output cost, remain tethered to global oil swings, eroding price competitiveness when crude spikes. Planned ethane upgrades worth USD 700 million will narrow the gap, but cost parity with gas-advantaged Gulf producers remains elusive.

Escalating Environmental Activism Against Single-use Plastics

The Law on Environmental Protection bans non-biodegradable plastic bags under 50×50 cm from January 2026 and orders a complete phase-out of single-use plastic manufacture by December 2030. Required recycling targets and producer fees add operating costs that weigh most heavily on small converters. Urban consumers increasingly choose reusable options, trimming sales of traditional packaging even as bioplastic film lines face a 20%-40% cost premium over commodity grades. While the shift unlocks premium niches for compostable resins, it crimps short-run volume across mass-market applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Traditional Plastics Anchor Market Foundation

Traditional plastics retained 51.10% of the Vietnam Plastics market share in 2025, anchored by polyethylene and polypropylene grades used in everyday packaging, pipes, and molded parts. These products benefit from mature supply chains and low unit costs, ensuring continued volume leadership. Engineering plastics, including polycarbonate and polyamide, are gaining traction in electronics lines that ship high-brightness OLED(Organic Light Emitting Diode) displays and optical modules. Polyurethanes ride the construction boom, serving sandwich panels and furniture cushioning.

Bioplastics, though still a niche, are set to grow at a 12.55% CAGR through 2031 as brand owners chase sustainability targets and new regulations unlock demand. Agricultural residues supply potential starch inputs, yet scaling remains hindered by certification hurdles and premium pricing. Still, pilot programs led by international apparel groups showcase Vietnam as a future biopolymer production site, signaling a possible inflection after 2027.

By Technology: Extrusion Dominance Reflects Scale Economics

Extrusion claimed 61.35% of the Vietnam Plastics market share in 2025 and is expected to rise at a 10.12% CAGR through 2031. Converters expand multilayer film lines for food packaging and corrugated pipes for drainage networks, choosing proven equipment that assures uptime. Blow molding fills beverage, household, and lubricant bottle demand but stays capacity-constrained relative to extrusion. Injection molding thrives on demand for precision connectors and cosmetic closures, yet its growth lags extrusion because of higher tooling investments per SKU. Emerging processes such as 3D printing remain experimental, cushioned by government research and development (R&D) credits that encourage limited prototyping rather than mass scale.

By Application: Packaging Leadership Drives Market Expansion

Packaging captured 50.35% of the Vietnam Plastics market size in 2025 and is forecast to grow 8.78% by 2031. Food processors need barrier pouches that block oxygen and moisture, while e-commerce sellers demand tamper-evident, lightweight solutions that navigate last-mile delivery bruises. Electronics packaging volumes climb with component imports, boosting demand for antistatic films and thermoformed trays. Building and construction uses PVC and polyethylene in conduit, profiles, and waterproofing membranes, tapping the 40% surge in infrastructure spending.

Automotive and transportation applications gain impetus from rising export-ready vehicle production, lifting requirements for lightweight structural plastics that displace metal. Household and furniture items close the loop, especially as Vietnam scales furniture exports to North America. Diversified demand across these segments mitigates cyclical risk, anchoring resilient growth in the Vietnam plastics market.

Geography Analysis

Northern clusters such as Bac Ninh and Hung Yen host display, mobile, and semiconductor assembly, creating dense demand for high-performance plastic films and housings. Southern provinces, notably Ba Ria-Vung Tau, house petrochemical complexes and port assets that feed Ho Chi Minh City converters. Import reliance exposes manufacturers to swings in regional supply, with China supplying 32%, South Korea 17.2%, and Japan 6.5% of raw plastics through July 2026. Yet the same geography affords short transit lanes that keep inventory cycles lean. Clusters benefit from provincial incentives—land-lease discounts, utility subsidies, and expedited licensing—that draw additional investment. Inland freight corridors linking Hanoi to Haiphong and the southern North-South expressway shave logistics costs, further cementing Vietnam’s competitiveness against ASEAN peers with higher operating costs.

Value Chain Analysis

Vietnam's plastics value chain begins with upstream feedstock supply (naphtha, propylene, and polymer pellets), where the country remains import-dependent, and domestic production is estimated to cover only about 20-25% of total raw-material requirements. Imports are handled through major port-linked industrial corridors and then converted into commodity resins and compounds. Integrated capacity such as SCG's Long Son Petrochemicals (LSP) complex in Ba Ria-Vung Tau produces key polyolefins (HDPE, LLDPE, and PP), which should help dampen exposure to external resin cycles.

Midstream, thousands of fragmented converters, concentrated around Ho Chi Minh City and northern electronics clusters, process resins mainly via extrusion, injection molding, and blow molding into films, pipes, profiles, housings, and molded packaging. Downstream demand is shaped by packaging, construction, and electronics manufacturing supply chains, where procurement increasingly relies on documented quality and sustainability requirements. Post-consumer collection and recycling remain a structural bottleneck, with informal recyclers under pressure from compliance tightening. Formal recyclers and brand-led circular partnerships are taking a larger role in securing consistent recycled-resin supply under Extended Producer Responsibility (EPR) obligations.

Competitive Landscape

The Vietnam Plastics Market is moderately fragmented as foreign and domestic players vie for share. SCG commands upstream strength via Long Son Petrochemicals, while local giants such as Binh Minh Plastic leverage nationwide pipe distribution. Samsung Display’s vertically integrated campus locks in demand for optical films, and Foxconn’s console plant heralds specialty ABS and HIPS orders for casings. Automation partners supply turnkey injection lines, improving finished-part tolerances and lowering labor dependence. Informal recyclers process hundreds of tons daily but face regulatory tightening that favors larger, capital-rich recyclers capable of meeting environmental norms. Competitive advantage is shifting from cost to compliance and supply-chain proximity, especially as Extended Producer Responsibility fees reshape packaging economics.

Vietnam Plastics Industry Leaders

Vietnam Oil and Gas Group

SCG Chemicals Public Company Limited

NSRP LLC

LyondellBasell Industries Holdings B.V.

Vinaplast

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Circular plastics-related opportunities are expanding as EPR implementation increases the need for traceable recycled content in packaging supply chains. Decree No. 110/2026/ND-CP (effective May 25, 2026) sets out more detailed requirements for producer and importer responsibility, which encourages brand owners and converters to contract with compliant collectors and recyclers or contribute to the Vietnam Environmental Protection Fund. This regulatory pull shows up in investment and collaboration, including Norfund's February 2026 equity investment to scale CPC Vietnam's industrial PET recycling operations in the Ho Chi Minh City area, and in converter-brand partnerships that prioritize higher recycled-content packaging formats.

A second opportunity is feedstock localization and the move toward higher-spec materials that support Vietnam's export manufacturing base. Vietnam still relies on imported raw materials for about 70% of inputs as of 2026, leaving room for local resin supply, compounding, and application development aligned with electronics, automotive parts, and construction standards. The government's Supporting Industries Development Program for 2026-2035 reinforces localization as a policy priority, while upstream efforts such as LSP's 1.4 million-ton polyolefins capacity and ongoing enhancements create pathways for tighter domestic integration between resin producers and converters. In parallel, biodegradable materials projects, including PBAT capacity being built in Hai Phong by SK-linked entities, support premium packaging niches where compliance and certification capabilities can differentiate suppliers.

Recent Industry Developments

- June 2026: Duy Tan Plastics Manufacturing Corporation expanded a circular packaging initiative with DUYTAN Recycling and Y&B Corporation (Cocoon brand) to develop cosmetic packaging made from 100% recycled plastic. The collaboration strengthens demand signals for consistent, high-quality recycled resin and pushes converters toward closed-loop sourcing and design-for-recycling practices.

- April 2026: Long Son Petrochemicals (LSP) awarded Technip Energies an engineering and procurement scope for the Long Son Petrochemicals Enhancement (LSPE) project to convert the steam cracker from naphtha to ethane feedstock. The project supports feedstock diversification and cost competitiveness for domestic polymer output, with downstream implications for converter margins and supply stability.

- May 2024: Ecovance Vietnam (SKC Group) committed about USD 100 million to build a biodegradable PBAT plant in the Dinh Vu Industrial Zone, Hai Phong, with planned annual capacity of 70,000 tons. This investment adds domestic capability in biodegradable materials and broadens the local supply base for compliant packaging solutions as restrictions on conventional single-use plastics tighten.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers plastics consumption in Vietnam measured in volume, across major polymer families and the main processing technologies used to convert resin into plastic products for end users.

Scope exclusions: We exclude rubber, textiles, metals, glass, and paper-based substitutes, and we do not count non-plastic additives unless they are part of the finished plastic volume.

Segmentation Overview

- By Type

- Traditional Plastics

- Polyethylene

- Polypropylene

- Polystyrene

- Poly Vinyl Chloride

- Engineering Plastics

- Polyurethanes

- Fluoropolymers

- Polyamides

- Polycarbonates

- Styrene Copolymers (ABS and SAN)

- Thermoplastic Polyesters

- Other Engineering Plastics

- Bioplastics

- Traditional Plastics

- By Technology

- Blow Molding

- Extrusion

- Injection Molding

- Other Technologies

- By Application

- Packaging

- Electrical and Electronics

- Building and Construction

- Automotive and Transportation

- Housewares

- Furniture and Bedding

- Other Applications

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with collecting Vietnam-level demand signals that can be tied back to plastic use in packaging, construction, automotive, and electrical and electronics. We leaned on public sources such as Vietnam General Statistics Office releases, Vietnam Customs trade statistics, Ministry of Industry and Trade publications, and UN Comtrade and World Bank indicators to map import dependence and end-use momentum.

To keep assumptions grounded, we also reviewed company annual reports, investor presentations, and industry association updates (such as plastics and packaging bodies) to understand capacity additions, utilization direction, and product mix shifts. When needed, paid subscriptions were used only for company financials and news screening, import and export shipment-level checks, and patent lookups to confirm technology direction. These examples are not exhaustive, and other public sources were also referenced for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test the desk assumptions, especially around conversion yields, scrap rates, recycled content adoption, and pricing behavior by polymer family. We spoke with a mix of resin distributors, converters, and large end users, and then cross-checked views across APAC, EMEA, and the Americas to avoid over-weighting one trade flow or one customer set.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 21% | |

| Mid tier: 41% | Functional/Unit leaders: 23% | |

| Smaller Players: 21% | Managers: 56% |

Market-Sizing & Forecasting

Our sizing starts with a top-down demand pool build that reconstructs plastics consumption using Vietnam manufacturing output, construction activity, packaged goods throughput, and net trade direction for key polymers, which are then converted into application-level volume shares. Once this first pass is built, the totals are corroborated with selective bottom-up approximations like sampled converter throughput, resin distribution channel checks, and implied volume from average selling price ranges where price signals were consistent.

Inputs that mattered most included Vietnam polymer import dependency, capacity and utilization changes at major conversion hubs, packaging intensity per unit of consumer output, building and construction pipeline indicators, and shifts in the share of engineering plastics driven by electronics and transport demand. Where bottom-up gaps appeared (for example, small converter volumes and informal recycling streams), we used conservative fill factors that were later checked again with interviewees. Forecasts were developed using scenario analysis, where resin price direction, export-led manufacturing growth, and substitution toward recycled content were varied, then aligned to the consensus range coming from expert calls.

Data Validation & Update Cycle

Totals were triangulated by comparing the modeled volume with independent signals such as trade balances for key polymer families, large end-use production trends, and observed price-volume behavior over time. Outliers were flagged, revisited, and adjusted only after the driver was identified, and then a second analyst review was completed before sign-off.

The work is refreshed annually, and we also do interim checks when material events occur, such as sudden policy changes on waste imports, major capacity start-ups, or sharp resin price moves. Before delivery, a final pass is completed so clients receive the most current view available at the time.

Mordor Intelligence's Vietnam Plastics Market Size Versus Other Published Estimates

Published market sizes for Vietnam plastics often do not match because the unit of measure is not always the same, and the scope can shift between resin in primary forms, converted plastic products, or only selected end uses like packaging. Timing also matters because some figures are updated faster when resin prices swing or when trade flows change.

Key gaps usually come from how recycled volumes are treated, how imports and re-exports are netted, and whether conversion scrap is counted inside consumption. Some sources also lean more on revenue-style assumptions, where average selling price choices can move totals quickly, while others stick to physical volume tracking and then validate it against manufacturing and trade signals, a choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 11.84 M (2025) | |

| Industry Research Group A | USD 11.13 M (2025) | Uses a different polymer and application split, and its conversion assumptions (including scrap and recycled share treatment) appear to be set more uniformly across end uses, which can compress the total volume. |

| Trade Journal B | USD 17.75 M (2030) | Presents a forward-year point estimate and may apply a single high-growth trajectory across end uses, without clearly separating net trade effects and price-driven volume shifts year by year. |

The table shows that the spread is mostly explained by scope choices and how conversion realities like scrap and recycled content are handled, followed by timing and forecasting stance. By keeping the model tied to repeatable demand indicators and then validating them with channel checks, the final size stays traceable to clear steps that can be revisited as new data arrives.

Key Questions Answered in the Report

How big is the Vietnam Plastics market in 2026?

The Vietnam Plastics market size is 12.83 million tons in 2026 and is projected to reach 19.16 million tons by 2031.

Which segment holds the largest share of plastics demand in Vietnam?

Packaging leads with 50.35% of demand in 2025, driven by food processing and e-commerce fulfillment.

What is the growth outlook for bioplastics in Vietnam?

Bioplastics are expected to expand at a 12.55% CAGR through 2031, the fastest among all resin categories.

How dependent is Vietnam on imported plastic feedstock?

More than 5.5 million tons of raw plastic materials were imported in the first seven months of 2026, underscoring high reliance on external supply.

What policy measures influence recycling in Vietnam?

Extended Producer Responsibility rules introduce mandatory recycling targets and fees, incentivizing use of recycled-content resins and formalizing waste streams.

Page last updated on: