Precast Concrete Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 149.52 Billion |

| Market Size (2031) | USD 186.08 Billion |

| Growth Rate (2026 - 2031) | 4.47% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Precast Concrete Market Analysis by Mordor Intelligence

Precast Concrete market size in 2026 is estimated at USD 149.52 billion, growing from 2025 value of USD 143.12 billion with 2031 projections showing USD 186.08 billion, growing at 4.47% CAGR over 2026-2031. Robust public-sector pipelines, labor shortages in conventional construction, and sustainability mandates collectively accelerate industrialized building adoption. Developers favor standardized, factory-made components that shorten schedules, reduce site risks, and generate verifiable carbon savings. Sovereign infrastructure funds in Asia-Pacific and the Gulf States sustain demand visibility, while insurance incentives of up to 55% premium reductions for resilient precast buildings strengthen project economics. Competition pivots on the ability to orchestrate efficient logistics for oversized elements and to certify low-carbon production processes, positioning vertically integrated suppliers for strategic advantage.

Key Report Takeaways

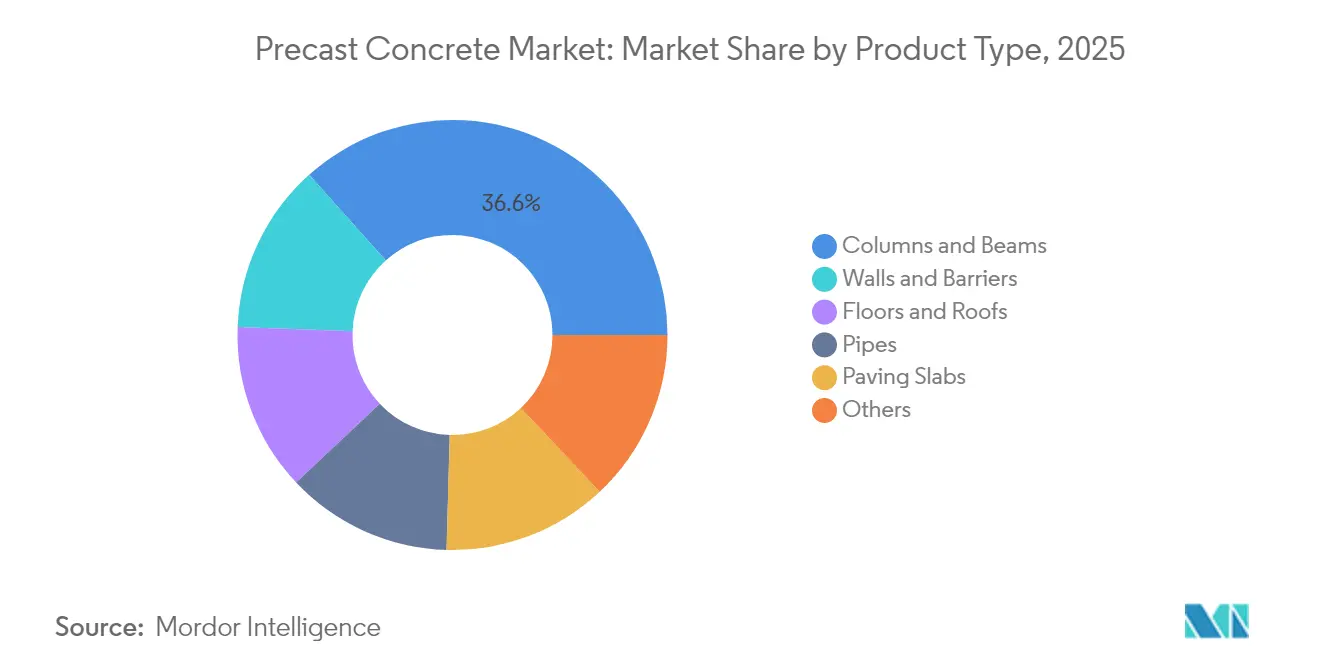

- By product type, columns and beams led with 36.62% of the precast concrete market share in 2025; walls and barriers are projected to advance at a 5.07% CAGR through 2031.

- By end-use industry, infrastructure commanded a 31.78% share of the precast concrete market size in 2025, while residential construction posts the fastest growth at a 4.69% CAGR to 2031.

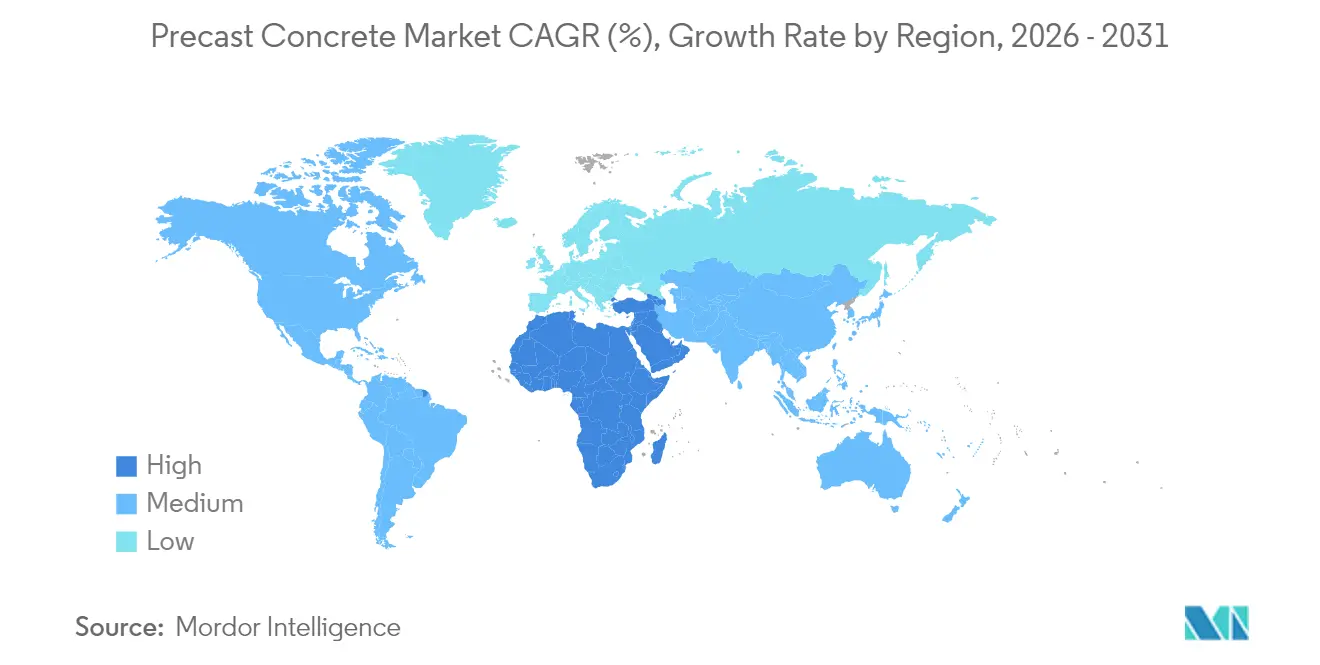

- By geography, Asia-Pacific accounted for a 39.12% precast concrete market share in 2025; the Middle East and Africa regions are set to expand at a 4.83% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Precast Concrete Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-led megaproject pipelines | +1.20% | Global, with concentration in APAC and MEA | Medium term (2-4 years) |

| Housing-for-All mandates in emerging economies | +0.80% | APAC core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Shift to off-site manufacturing amid skilled-labor scarcity | +0.70% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| Embodied-carbon credits monetisation | +0.60% | Europe and North America, expanding to APAC | Medium term (2-4 years) |

| Insurance-premium discounts for resilient precast structures | +0.40% | North America, Gulf States, disaster-prone regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government-led Megaproject Pipelines

National infrastructure programs funnel predictable volumes to the precast concrete market by standardizing designs and front-loading component procurement. The USD 1.2 trillion U.S. Infrastructure Investment and Jobs Act, the European Green Deal’s low-carbon build targets, and China’s mandate that 30% of new urban buildings employ prefabrication collectively underpin a multiyear demand base. Tasmania’s Bridgewater Bridge replacement documented a 40% schedule reduction versus cast-in-place options[1]Australian Government Department of Infrastructure, “Bridgewater Bridge Project Update,” infrastructure.gov.au . Scale procurement compresses unit costs and assures cross-project quality consistency. Suppliers with regional hub plants and modular formwork systems capture early-stage package awards, reinforcing first-mover advantages.

Housing-for-All Mandates in Emerging Economies

Affordable-housing blueprints elevate precast adoption by tying subsidy disbursements to rapid, standardized delivery within the precast concrete industry. India’s Pradhan Mantri Awas Yojana targets 20 million units and reports 50% faster build cycles plus 15% direct cost savings with precast walls, slabs, and stair cores[2]. Indonesia relocates portable factories across its archipelago, proving that mobile batch plants overcome geographic fragmentation. Predictable volume unlocks investments in automated carousel lines that triple hourly output compared with conventional yards. Latin American social-housing ministries increasingly require factory-molded panels to meet hurricane-load codes, illustrating the alignment between cost, speed, and resilience objectives.

Shift to Off-site Manufacturing Amid Skilled-Labor Scarcity

Developed economies confront labor gaps of more than 430,000 craft workers, prompting contractors in the precast concrete industry to pivot toward plant-based production. Robotics now places reinforcement, cast, and finish elements with 60% lower manual input than bench fabrication. Digital twins monitor concrete hydration, enabling precision curing and real-time quality control. All-weather factory operations stabilize material flow and working hours, smoothing revenue peaks for both builders and suppliers. Integration of logistics platforms further synchronizes just-in-time trucking with on-site crane windows, trimming idle-time penalties and carbon emissions.

Embodied-Carbon Credits Monetization

Carbon-pricing frameworks convert emissions savings into revenue, pushing producers to redesign mixes using slag, fly ash, and captured CO₂. Controlled dosing cuts cement volumes by 10-15% without strength loss, generating credits valued at EUR 80–100 per ton across the European Union. Blockchain tracking authenticates cradle-to-gate carbon data, commanding premium bids in green public-procurement tenders. Durability gains stretch service life, reducing replacement cycles and reinforcing the net-zero case for precast concrete market adoption among institutional asset owners.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High logistics cost of oversize elements | -0.50% | Global, particularly regions with limited transport infrastructure | Short term (≤ 2 years) |

| Competition from self-healing in-situ concretes | -0.30% | North America and Europe, expanding to APAC | Medium term (2-4 years) |

| Regional code fragmentation | -0.40% | Global, particularly North America, Europe, and emerging markets with evolving standards | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Logistics Cost of Oversize Elements

Hauling girders longer than 30 meters can add 15–25% to delivered component cost , especially beyond 100 km from the plant[3]. Limited bridge clearances and weight caps force circuitous routes that inflate fuel usage and permit fees. Urban congestion magnifies crane staging and road-closure requirements, compressing allowable delivery windows and raising overtime premiums. Remote project sites endure elevated escort-vehicle expenses, occasionally offsetting factory productivity benefits in the precast concrete industry. Suppliers mitigate exposure by deploying satellite yards or designing splice-ready segments, yet capex for mobile forms and batch setups restrains near-term scalability.

Competition from Self-Healing In-situ Concretes

Microencapsulated agents, bacterial admixtures, and shape-memory polymers enable poured-in-place mixes to self-seal cracks, challenging precast durability leadership in the precast concrete industry. Rapid-setting formulations narrow schedule advantages as slabs reach design strength within 24 hours. Architects value the geometry freedom of cast-in-place methods, which self-healing technology now extends to aggressive exposure classes. While material premiums remain high and field data are limited, ongoing pilot projects across European bridges suggest broader uptake by 2028. Precast suppliers respond by embedding self-healing capsules during factory casting, aiming to retain their quality-control edge.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Structural Elements Drive Volume Growth

Columns and beams anchored the precast concrete market size, accounting for 36.62% share in 2025. Robust demand stems from high-rise, bridge, and industrial frameworks where load-bearing precision necessitates controlled factory casting. Walls and barriers are poised to expand at a 5.07% CAGR to 2031 as governments tighten perimeter-security codes and modular housing kits proliferate. Floors and roofs benefit from open-plan preferences, leveraging long-span hollow-core slabs that cut on-site shoring time. Pipe segments track water-infrastructure funding cycles, while paving slabs serve steady streetscape renewal programs.

Automation reshapes all product lines: robotized cages trim labor by 40–60% across the precast concrete industry; laser projection ensures formwork accuracy, and 3D-printed molds facilitate custom architectural textures. Integrated insulation and conduit chases elevate walls and barriers from commodity panels to turnkey envelope systems, supporting premium pricing. Standardized connection hardware accelerates job-site assembly, embedding speed advantages directly into component design. Earthquake zones demand ductile joint details, reinforcing the regional tailoring of product portfolios.

By End-use Industry: Residential Momentum Builds

Infrastructure retained leadership with 31.78% of the precast concrete market share in 2025, buoyed by bridge, tunnel, and desalination contracts. Residential construction, however, records the highest 4.69% CAGR toward 2031 as governments and developers pivot to mass-housing solutions. Multi-family towers adopt full-frame precast packages that compress schedule risk, enabling developers to secure earlier drawdowns and occupancy certificates. Commercial demand remains cyclical yet stable, underpinned by precast parking decks and mixed-use podiums prioritizing speed-to-revenue. Institutional buyers favor factory-made units for laboratories and hospitals, given stringent cleanliness and vibration criteria.

Residential acceleration aligns with government subsidy frameworks that reward modular completion timelines. Integrated panel systems pre-route plumbing, electrical, and HVAC, slashing follow-on trades by as much as 30% in the precast concrete industry. Developers cite enhanced mortgage securitization prospects when delivery certainty rises, further channeling volume to precast suppliers. Industrial warehouse growth, powered by e-commerce logistics realignment, complements the residential surge, keeping plant utilization rates high across product lines.

Geography Analysis

Asia-Pacific held a 39.12% share of the precast concrete market in 2025, with China enforcing 30% prefabrication quotas across new urban projects and India subsidizing low-income housing starts. Regional manufacturers capitalize on scale economies and local cement supplies, driving export of standardized formwork technology to Vietnam and the Philippines. Japan and South Korea pioneer seismic-grade precast frames, while Australia integrates high-durability marine mixes for coastal infrastructure.

The Middle East and Africa register the fastest 4.83% CAGR to 2031. Gulf sovereign wealth funds channel capital into smart-city platforms such as Saudi Arabia’s NEOM, which specifies factory-finished facades for thermal efficiency. Qatar’s World Cup build-out left a legacy of yard capacity now redeployed for metro and desalination projects. African metros like Nairobi and Lagos trial modular schools and hospitals, yet road-haul limits and crane shortages temper immediate scalability.

North America and Europe exhibit mature yet innovation-driven demand profiles within the precast concrete industry. U.S. insurers’ resilience discounts spur uptake in hurricane corridors, while Canada’s carbon-tax schedule incentivizes low-cement precast mixes. European tender specifications increasingly weight cradle-to-gate CO₂ declarations, pushing suppliers to adopt clinker-reduced cements and renewable-energy curing kilns. Market access hinges on meeting evolving EN and ASTM standards alongside locally calibrated environmental product declarations.

Competitive Landscape

The precast concrete market is highly fragmented. Automation investments top strategic agendas: Elematic’s digital-twin platform reduces rework incidents by 30% and extends mold life cycles. Progressive Gulf producers incorporate solar rooftops and battery storage to stabilize energy costs and meet green-procurement thresholds.

Acquisition momentum persists Molins’ EUR 100 million Concremat purchase secures Portuguese market entry and funds a robotic Spain plant plus a U.S. urban-landscaping factory. CRH’s USD 2.1 billion Texas asset buy expands Southwest yard density, enabling next-day delivery within a 400 km radius. Technology entrants experiment with gantry-based 3D printing of reinforcement-free walls, posing medium-term disruption threats, particularly for non-load-bearing applications in the precast concrete industry.

Competitive differentiation increasingly revolves around whole-building solutions that integrate structure, envelope, and MEP pathways. Providers bundling design-for-manufacture consultancy with low-carbon certification command specification preference in public tenders. The race to decarbonize also triggers alliances with admixture specialists and startup carbon-capture firms, reinforcing cross-industry convergence trends within the precast concrete market.

Precast Concrete Industry Leaders

Holcim

CEMEX S.A.B. de C.V.

CRH

Forterra Building Products Limited

Boral Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Molins is investing EUR 100m in the acquisition of Concremat, a leading precast concrete firm in Portugal. The investment also includes the development of a new robotic plant in central Spain and a new U.S. factory for its urban landscaping division, Escofet. This acquisition strengthens Molins' precast concrete business and marks its entry into the Portuguese market.

- February 2024: CRH has acquired Texas-based concrete operations for USD 2.1 billion, enhancing its precast manufacturing capacity across the southwestern United States and strengthening its position in infrastructure markets. This acquisition is expected to boost the precast concrete market by accelerating regional growth and meeting rising demand efficiently.

Global Precast Concrete Market Report Scope

Precast concrete is a type of concrete that is manufactured in a controlled factory environment rather than being cast on-site. This prefabricated concrete product is shaped using molds or forms and subsequently transported to construction sites for assembly and installation.

The precast concrete market is segmented by product type, end-user industry, and geography. By product type, the market is segmented into beams & columns, paving slabs, floors & roofs, pipes, walls & barriers, and others. By end-user industry, the market is segmented into residential, infrastructure, commercial, industrial, and institutional. The report also covers the market sizes and forecasts for the global precast concrete market in 27 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Columns and Beams |

| Walls and Barriers |

| Floors and Roofs |

| Pipes |

| Paving Slabs |

| Others |

| Residential |

| Commercial |

| Infrastructure |

| Industrial and Institutional |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Russia | |

| Spain | |

| Turkey | |

| Nordic Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Egypt | |

| Nigeria | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Columns and Beams | |

| Walls and Barriers | ||

| Floors and Roofs | ||

| Pipes | ||

| Paving Slabs | ||

| Others | ||

| By End-use Industry | Residential | |

| Commercial | ||

| Infrastructure | ||

| Industrial and Institutional | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Russia | ||

| Spain | ||

| Turkey | ||

| Nordic Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Egypt | ||

| Nigeria | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the global precast concrete market value in 2026?

The precast concrete market size stands at USD 149.52 billion in 2026.

How fast is demand expected to grow over the next five years?

The market is projected to record a 4.47% CAGR, lifting value to USD 186.08 billion by 2031.

Which region leads consumption of factory-made concrete elements?

Asia-Pacific holds 39.12% of global demand, driven by China’s industrialized-construction policies.

What segment will expand the quickest through 2031?

Walls and barriers are forecast to grow at 5.07% CAGR, reflecting rising modular-housing and security needs.

How are producers addressing carbon-reduction mandates?

Plants substitute low-clinker binders and capture CO₂, monetizing 10–15% cement savings via carbon credits.

Page last updated on: