Middle East And Africa Plant-based Meat And Dairy Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

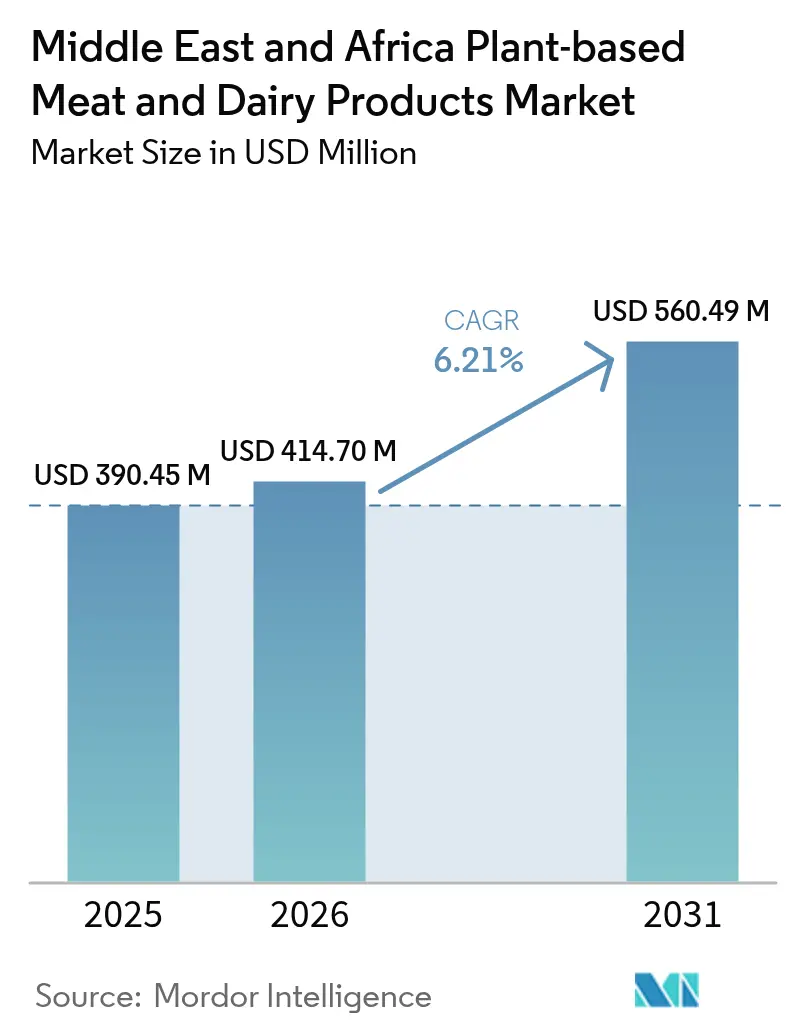

| Base Year Market Size (2025) | USD 390.45 Million |

| Market Size (2026) | USD 414.7 Million |

| Market Size (2031) | USD 560.49 Million |

| Growth Rate (2026 - 2031) | 6.21% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle East And Africa Plant-based Meat And Dairy Products Market Analysis by Mordor Intelligence

The Middle East and Africa plant-based meat and dairy products market size in 2026 is estimated at USD 414.7 million, growing from 2025 value of USD 390.45 million with 2031 projections showing USD 560.49 million, growing at 6.21% CAGR over 2026-2031. Current growth is propelled by sovereign food-security programs that treat alternative proteins as strategic infrastructure, not niche trends. Government-backed initiatives such as the UAE’s Future Food Foundry are channeling capital into precision fermentation, while Saudi regulators have fast-tracked approvals for microbial proteins. Consumer behavior is evolving in parallel: health-driven shoppers, expanding flexitarian segments, and rising lactose intolerance rates are steering demand toward fortified dairy alternatives. Meanwhile, supply-chain pressures linked to grain imports and shipping costs are nudging producers toward vertical integration and local crop substitution, reshaping sourcing and pricing dynamics within the Middle East and Africa plant-based meat and dairy products market.

Key Report Takeaways

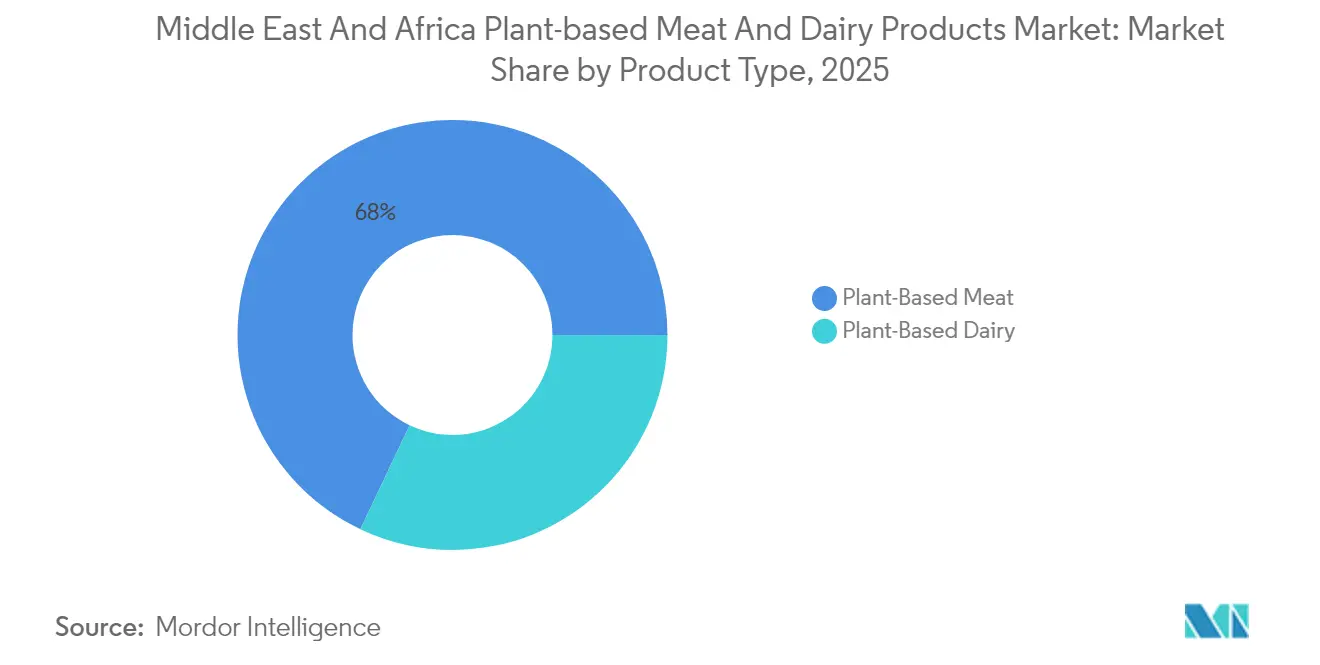

- By product type, plant-based meat led with 67.95% revenue share in 2025; plant-based dairy is forecast to expand at a 7.21% CAGR through 2031.

- By protein source, soy commanded 41.86% of the Middle East and Africa plant-based meat and dairy products market share in 2025, while pea protein is set to grow at 7.55% CAGR to 2031.

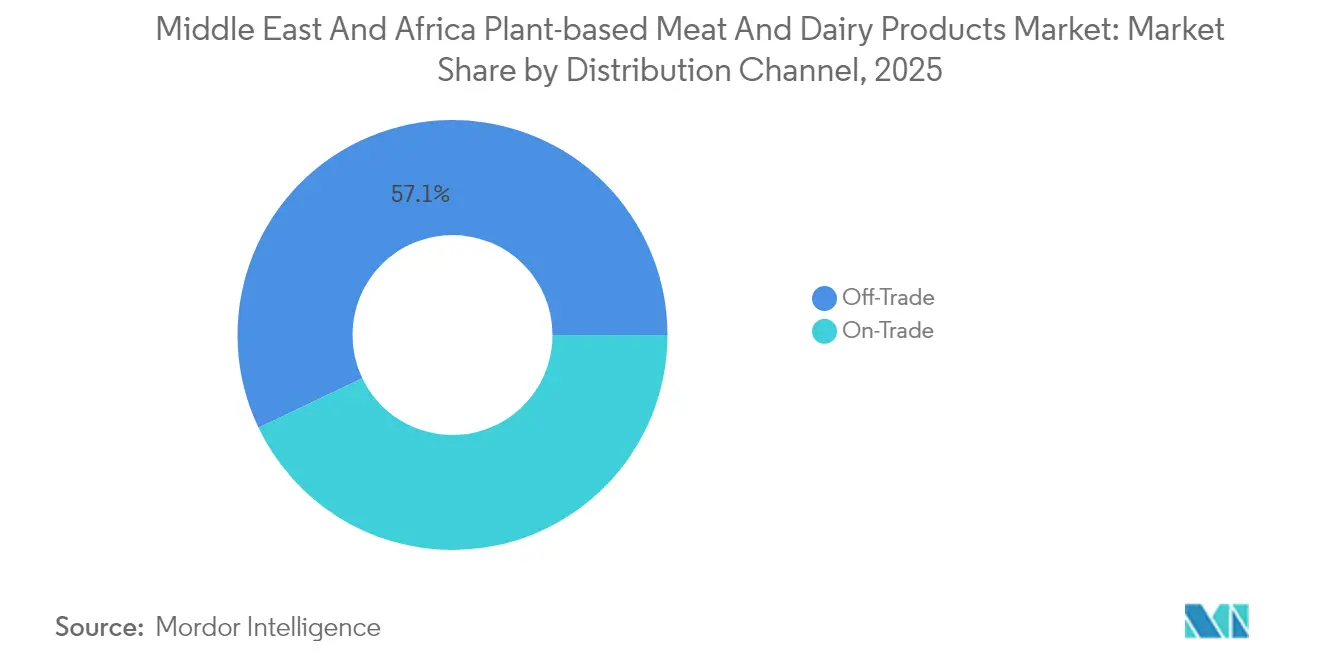

- By distribution channel, off-trade formats held 57.10% share of the Middle East and Africa plant-based meat and dairy products market size in 2025; on-trade channels record the fastest trajectory at 6.88% CAGR to 2031.

- By geography, South Africa captured 29.75% of regional sales in 2025; Saudi Arabia shows the highest growth outlook at 7.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Plant-based Meat And Dairy Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer awareness about health benefits of plant-based diets | +1.2% | Regional, with stronger penetration in United Arab Emirates, South Africa | Medium term (2-4 years) |

| Rising prevalence of lactose intolerance and dairy allergies in the region | +0.8% | Middle East core markets, spillover to North Africa | Long term (≥ 4 years) |

| Expansion of vegan and flexitarian populations in urban areas | +1.0% | Urban centers in United Arab Emirates, Saudi Arabia, South Africa | Medium term (2-4 years) |

| Government initiatives and favorable regulations promoting sustainable and alternative protein sources | +1.5% | United Arab Emirates, Saudi Arabia, South Africa with regulatory leadership | Short term (≤ 2 years) |

| Growing investments by major companies in product innovation and portfolio expansion | +1.3% | Regional hubs in United Arab Emirates, Saudi Arabia, expanding to Egypt, Morocco | Medium term (2-4 years) |

| Rising demand for ethical and animal welfare-friendly food products | +0.7% | Urban markets across the Region, concentrated in higher-income segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing consumer awareness about health benefits of plant-based diets

Growing consumer awareness about the health benefits of plant-based diets is a key driver of the Middle East and Africa (MEA) plant-based meat and dairy products market. This trend is further reinforced by the rising prevalence of lifestyle diseases such as diabetes in the region, which is creating a strong demand for healthier dietary alternatives. According to the International Diabetes Federation, in 2024, around 85 million adults aged 20 to 79 in the Middle East and North Africa (MENA) region were diagnosed with diabetes, representing one of the highest regional diabetes burdens globally [1]Source: International Diabetes Federation, "Diabetes in MENA 2024", idf.org. The increasing incidence of diabetes and related health concerns is encouraging consumers to adopt plant-based meat and dairy options, which are perceived to be lower in cholesterol, saturated fats, and better suited for managing such chronic conditions. Consequently, this health-driven dietary shift, combined with rising disposable incomes and urbanization, is propelling the growth of the MEA plant-based meat and dairy market significantly.

Rising prevalence of lactose intolerance and dairy allergies in the region

In North Africa, about 70% of adults are genetically predisposed to lactose intolerance. This widespread condition not only highlights a significant market for dairy alternatives but also underscores their medical necessity. Healthcare providers in the region are increasingly reporting a rise in diagnoses related to dairy-induced digestive issues, such as bloating, diarrhea, and abdominal pain. This trend is especially pronounced in urban areas, where there's been a surge in processed dairy consumption due to changing dietary habits and increased availability of packaged foods [2]Source: Egyptian Ministry of Health, "Certification of vaccinations issued by the Preventive Administration", www.mohp.gov.eg. Such physiological needs foster a consistent demand for dairy alternatives, one that's notably less influenced by price fluctuations than mere preference. Furthermore, the medical validation of plant-based dairy substitutes positions them as viable solutions for individuals with lactose intolerance. This validation opens opportunities for endorsements from the healthcare system and considerations for insurance coverage, both of which could significantly hasten their acceptance and integration into mainstream markets.

Expansion of vegan and flexitarian populations in urban areas

Urban demographic shifts are creating concentrated demand clusters, facilitating efficient distribution and marketing strategies for plant-based products. In Dubai, where expatriates make up over 85% of the population, the presence of diverse dietary preferences is driving the normalization of plant-based consumption patterns [3]Source: Dubai Statistics Center, "Expatriate Population", www.dsc.gov.ae. This trend is further supported by the growing awareness of health, environmental sustainability, and ethical considerations associated with plant-based diets. Major cities like Johannesburg, Cairo, and Riyadh are experiencing a notable rise in flexitarian adoption, primarily fueled by younger demographics who are increasingly prioritizing dietary flexibility and exploring alternatives to traditional protein sources. These younger consumers are also influenced by global trends and social media, which promote plant-based lifestyles as modern and progressive. This urban concentration provides companies with an opportunity to penetrate the market effectively through targeted retail partnerships and foodservice integration, enabling them to establish a strong foothold.

Government initiatives and favorable regulations promoting sustainable and alternative protein sources

Government initiatives and favorable regulations are significantly promoting sustainable and alternative protein sources in the Middle East and Africa (MEA), driving growth in the plant-based meat and dairy products market. Recognizing the pressing challenges of climate change, food security, and resource scarcity, governments in the region are increasingly adopting policies that support innovation and investment in alternative proteins such as plant-based, cultivated meat, and protein from microbial fermentation. For example, Saudi Arabia is advancing projects to produce protein using cutting-edge biotechnology and local resources to reduce environmental stress and boost food self-sufficiency. Regulatory frameworks are being developed to ensure the safety and market access of novel protein products, while public investment and partnerships are encouraged to foster research and commercialization. These initiatives not only aim to provide sustainable protein options but also create economic opportunities and align with global climate goals, thus accelerating the adoption of alternative proteins across MEA markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High price premium of plant-based meat and dairy compared to conventional products | -1.8% | Regional impact with strongest effect in price-sensitive markets like Egypt, Morocco | Short term (≤ 2 years) |

| Supply chain complexities and sourcing of raw plant-based ingredients | -1.2% | Import-dependent markets including United Arab Emirates, Saudi Arabia, with spillover effects | Medium term (2-4 years) |

| Limited awareness and acceptance of plant-based products among certain population segments | -0.9% | Rural and traditional communities across the region | Long term (≥ 4 years) |

| Cultural and religious dietary preferences influencing consumer choices | -0.6% | Conservative communities with traditional dietary practices | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High price premium of plant-based meat and dairy compared to conventional products

The high price premium of plant-based meat and dairy products compared to conventional animal-based products acts as a significant restraint for the Middle East and Africa (MEA) plant-based meat and dairy market. Despite growing consumer interest driven by health and environmental concerns, the relatively higher production costs associated with plant-based alternatives—stemming from expensive raw materials, advanced processing technologies, and supply chain complexities—result in higher retail prices. This price differential limits accessibility, especially in price-sensitive segments and developing countries within the region, where conventional meat and dairy remain more affordable. While premium pricing appeals to affluent and urban consumers, broader market penetration requires strategies to reduce costs through innovation, economies of scale, and localized production to make plant-based options more competitively priced. The challenge of balancing cost and consumer demand is critical for sustained growth and mainstream adoption in the MEA market.

Supply chain complexities and sourcing of raw plant-based ingredients

The Middle East and Africa plant-based meat and dairy products market faces notable supply chain complexities and challenges in sourcing raw plant-based ingredients, which act as a significant market restraint. The region relies heavily on imports for key raw materials and finished plant-based products, predominantly from countries like India, the United Kingdom, United States, and various European nations, leading to vulnerability in supply continuity and higher costs. Limited local production infrastructure and underdeveloped supply chains impede the scalability and affordability of plant-based alternatives. Additionally, logistical hurdles such as transportation, storage, and distribution inefficiencies exacerbate these supply challenges, especially in countries with less advanced food supply systems. These factors collectively restrict market growth by impacting product availability and causing price premiums, which can deter wider consumer adoption. Addressing supply chain resilience and boosting local ingredient sourcing is essential to overcome these bottlenecks and enable sustainable expansion of the plant-based market in MEA.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Meat Alternatives Drive Market Leadership

The plant-based meat segment holds the largest market share in the Middle East and Africa plant-based meat and dairy products market, commanding approximately 67.95% of the market in 2025. This dominant position is driven by strategic positioning of plant-based meat products as direct substitutes for conventional protein sources rather than niche or specialty items. Consumers in the region are increasingly adopting flexitarian and meat-reducing diets, which has led to widespread availability of plant-based meat products like burger patties, sausages, and meatballs in mainstream retail outlets. The success of the segment is reinforced by continuous product innovation aimed at replicating the taste, texture, and nutritional benefits of traditional meat. Key markets such as the UAE and South Africa are particularly instrumental in driving demand, fueled by rising health awareness and environmental concerns. Retailers and manufacturers in these countries have expanded their plant-based meat portfolios to cater to diverse consumer preferences and dietary requirements.

In contrast, the plant-based dairy segment is the fastest-growing segment within the Middle East and Africa market, projected to grow at a CAGR of 7.21% through 2031. This strong growth trajectory is driven primarily by increasing consumer demand for functional plant-based dairy applications, especially in coffee culture and dessert preparations, which have gained substantial popularity in urban centers. The rise in lactose intolerance cases and a growing interest in vegan and vegetarian lifestyles are key factors propelling this segment. Manufacturers are responding with innovative products derived from various plant sources like soy, almond, and coconut, including vegan cheeses and plant-based milks. These products have started to penetrate mainstream retail channels more deeply, becoming a staple in cafes and dessert shops across metropolitan areas. Enhanced product development efforts focusing on taste, nutritional value, and texture continue to strengthen the appeal of plant-based dairy alternatives, making this segment a significant growth driver in the overall market.

By Protein Source: Soy Dominance Faces Diversification Pressure

Soy protein holds the largest market share of 41.86% in the Middle East and Africa plant-based meat and dairy products market in 2025. This dominance is underpinned by its well-established supply chains and proven functionality across a variety of product applications. Soy protein is widely recognized for its complete amino acid profile and versatility, making it a preferred ingredient in meat alternatives, dairy substitutes, and nutritional supplements. The extensive adoption of soy protein is supported by robust production infrastructure and consumer awareness about its health benefits. It is extensively used in both conventional and organic forms, facilitating its integration into multiple food products including beverages, bakery items, and processed foods. Moreover, soy protein benefits from economies of scale and competitive pricing, further solidifying its market leadership in the region.

Conversely, pea protein represents the fastest-growing segment in the market, with a compelling CAGR of 7.55% projected through 2031, signaling a trend towards diversification in plant-based protein sources. Pea protein's growth is driven by rising consumer concerns over soy's potential hormonal impacts and genetic modification issues, encouraging a shift to allergen-friendly and non-GMO alternatives. It offers exceptional adaptability to local cultivation conditions, which benefits supply chains and sustainability considerations, especially in varying Middle Eastern and African climates. The increasing preference for clean-label products and plant-based protein options free from common allergens is fueling demand. Innovations in pea protein processing and formulation are expanding its use across meat analogs, dairy-free products, and nutritional supplements. This trend highlights a strategic market shift toward inclusivity and health-conscious consumption patterns, broadening the plant-based protein landscape in the Middle East and Africa.

By Distribution Channel: Retail Infrastructure Shapes Market Access

In the Middle East and Africa plant-based meat and dairy products market, off-trade channels hold the largest market share at 57.10% in 2025. This reflects the critical importance of retail infrastructure, such as supermarkets, hypermarkets, and convenience stores, in driving consumer trial and repeat purchase behavior. These channels provide consumers with wide product variety, competitive pricing, and convenient access, which promotes greater adoption of plant-based alternatives. Retailers are increasingly dedicating shelf space to plant-based products and utilizing strategic product placements and promotions to enhance visibility. The established retail network ensures a one-stop shopping experience for consumers looking to incorporate plant-based options into their diets. This extensive reach and accessibility have established off-trade channels as the primary driver of market penetration in the region.

On the other hand, on-trade channels, which include restaurants, cafes, and foodservice outlets, are the fastest-growing segment within this market, showing a CAGR of 6.88% through 2031. This growth indicates an increasing integration of plant-based products into foodservice menus to meet the rising demand for diverse dietary options. The acceleration is driven by consumer interest in healthier, environmentally friendly, and allergen-conscious food choices available outside the home. Foodservice establishments are expanding their plant-based offerings, reflecting evolving consumer preferences and dietary requirements. This trend not only increases market consumption but also raises consumer awareness and acceptance through experiential tasting and meal occasions. As plant-based foods become more normalized in dining out scenarios, on-trade channels are expected to play an increasingly important role in market growth and diversification.

Geography Analysis

The Middle East and Africa Plant-based Meat and Dairy Products Market showcases significant geographical dynamics, with South Africa leading regional development in 2025 by capturing a 29.75% market share. The country leverages its robust food processing infrastructure and supportive regulatory frameworks to drive product innovation and facilitate market entry. Notably, South Africa's investments in precision fermentation, highlighted by the launch of its first public funding initiative in 2024, position it as a technological hub for alternative protein development. Urban centers such as Johannesburg and Cape Town exhibit consumer acceptance rates that surpass regional averages, fueled by health-conscious and diverse dietary preferences among affluent populations.

Saudi Arabia is emerging as the fastest-growing geography in the region, with a projected CAGR of 7.34% through 2031. This growth is underpinned by government initiatives that prioritize alternative proteins as strategic assets for food security. The kingdom's Vision 2030 sustainability goals provide strong policy support for plant-based alternatives, while the Saudi Food and Drug Authority's (SFDA) streamlined regulatory approvals for microbial proteins facilitate smoother market entry. These efforts reflect Saudi Arabia's commitment to fostering a sustainable and secure food ecosystem, driving the adoption of plant-based products across the country.

The UAE serves as a critical innovation and distribution hub within the region, driven by Dubai's diverse expatriate population, which generates demand for international plant-based brands and products. Government-backed initiatives such as the Future Food Foundry and Food Tech Valley highlight the UAE's dedication to advancing alternative protein development. Premium retail chains like Spinneys provide international brands with market access, while the integration of plant-based offerings in hotels and restaurants enhances consumer exposure. Meanwhile, emerging markets such as Egypt, Morocco, Nigeria, and Turkey exhibit substantial growth potential. However, challenges such as infrastructure limitations and price sensitivity necessitate the adoption of localized strategies and tailored product formulations to overcome barriers and unlock market opportunities.

Competitive Landscape

The competitive landscape of the Middle East and Africa Plant-based Meat and Dairy Products Market reflects moderate fragmentation, with a concentration score of 4. This indicates a balanced environment where both multinational corporations and regional specialists can establish competitive positions. Global players such as Danone, Nestlé, and Oatly are leveraging their international brand recognition, extensive supply chain networks, and expertise to penetrate premium market segments. These companies are focusing on catering to the growing demand for high-quality plant-based alternatives, which aligns with the increasing consumer preference for sustainable and health-conscious products. On the other hand, regional companies like SADAFCO and Almarai are utilizing their well-established distribution networks and strong consumer trust to expand into the plant-based category.

Competitive strategies in the market are evolving significantly, moving beyond traditional product development to emphasize vertical integration and supply chain control. Companies are increasingly recognizing the importance of cost competitiveness and supply security in maintaining their market positions. Vertical integration allows firms to streamline operations, reduce costs, and ensure a steady supply of raw materials, which is critical in a market where input costs and supply chain disruptions can significantly impact profitability. Additionally, supply chain control is becoming a focal point as companies aim to mitigate risks associated with import dependencies and currency fluctuations. This strategic shift highlights the growing need for operational efficiency and resilience in the face of global economic uncertainties.

Investment patterns in the Middle East and Africa Plant-based Meat and Dairy Products Market further underscore the emphasis on local manufacturing capabilities. Companies are increasingly establishing regional production facilities to reduce reliance on imports and minimize exposure to currency risks. These facilities not only help in lowering production costs but also enable companies to respond more swiftly to local market demands. By investing in local infrastructure, firms can enhance their supply chain efficiency and strengthen their presence in the region. This approach also aligns with the broader trend of promoting sustainability and reducing the carbon footprint associated with long-distance transportation. As the market continues to grow, these strategic investments are expected to play a pivotal role in shaping the competitive dynamics of the region.

Middle East And Africa Plant-based Meat And Dairy Products Industry Leaders

-

Blue Diamond Growers

-

Beyond Meat Inc.

-

Al Islami Foods

-

Saudi Dairy & Food Stuff Co.

-

Danone S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2022: Saudi Dairy and Food Stuff Company launched Saudia oat milk, claiming it is the Kingdom's first locally produced oat-based milk.

- May 2025: UAE-based meat alternatives producer Switch Foods has teamed up with Malak Al Tawouk to unveil a fresh lineup of plant-based chicken dishes. This collaboration aims to cater to the growing demand for sustainable and healthier food options, offering consumers a variety of innovative menu items that align with evolving dietary preferences.

- December 2024: Almarai Company announced USD 4.8 billion investment in domestic dairy production facilities across Saudi Arabia, with plans to integrate plant-based alternatives into existing manufacturing infrastructure. This strategic expansion positions the company to leverage established distribution networks for alternative protein market entry while maintaining supply chain control.

- June 2023: IFFCO Group, in a move aligned with Saudi Vision 2030's emphasis on sustainable food security, has introduced THRYVE™, its entirely plant-based meat brand, to the Saudi Arabian market. THRYVE™ offers a range of products, from mince and burgers to koftas, all infused with Middle Eastern flavors to resonate with local palates. These products are now accessible through major retailers across Saudi Arabia.

Middle East And Africa Plant-based Meat And Dairy Products Market Report Scope

Plant-based meat and dairy refer to products made from plant materials that are designed to mimic meat in every way, from taste, texture, smell, and appearance.

The Middle East and Africa plant-based meat and dairy products market is segmented by product type, distribution channel, and geography. Based on product type, the market studied is segmented into plant-based meat and plant-based dairy. Plant-based meat is further segmented into burger patties, sausages, strips and nuggets, meatballs, and other plant-based meats. Also, plant-based dairy is further segmented into milk, yogurt, butter and cheese, and other plant-based dairy products. By distribution channel, the market studied is segmented into supermarkets/hypermarkets, convenience stores, online retail channels, and other distribution channels. By geography, the market studied is segmented into South Africa, the United Arab Emirates, Saudi Arabia, Egypt, and the Rest of Middle-East and Africa.

For each segment, the market sizing and forecasts have been done on the basis of value (USD million).

| Plant-Based Meat | Burger Patties |

| Sausages | |

| Strips and Nuggets | |

| Meatballs | |

| Minced Meat | |

| Other Plant-based Meats | |

| Plant-Based Dairy | Milk |

| Yogurt | |

| Butter and Cheese | |

| Creamers | |

| Other Plant-based Dairy |

| Soy |

| Pea |

| Wheat |

| Almond |

| Others |

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Specialty Health Stores | |

| Online Retailers | |

| Other Distribution Channel |

| South Africa |

| Saudi Arabia |

| United Arab Emirates |

| Nigeria |

| Egypt |

| Morocco |

| Turkey |

| Rest of Middle East and Africa |

| By Product Type | Plant-Based Meat | Burger Patties |

| Sausages | ||

| Strips and Nuggets | ||

| Meatballs | ||

| Minced Meat | ||

| Other Plant-based Meats | ||

| Plant-Based Dairy | Milk | |

| Yogurt | ||

| Butter and Cheese | ||

| Creamers | ||

| Other Plant-based Dairy | ||

| By Protein Source | Soy | |

| Pea | ||

| Wheat | ||

| Almond | ||

| Others | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Specialty Health Stores | ||

| Online Retailers | ||

| Other Distribution Channel | ||

| By Geography | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the Middle East and Africa plant-based meat and dairy products market?

The market stands at USD 414.7 million in 2026.

How fast is the category expected to grow?

It is projected to expand at a 6.21% CAGR to reach USD 560.49 million by 2031.

Which country holds the largest regional share?

South Africa leads with 29.75% of 2025 sales.

Which product segment is growing fastest?

Plant-based dairy shows the highest CAGR at 7.21%.

What role do government initiatives play?

Policies in the UAE and Saudi Arabia fast-track regulatory approvals and fund precision-fermentation facilities, accelerating innovation and local production.

Page last updated on: