India Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2031 |

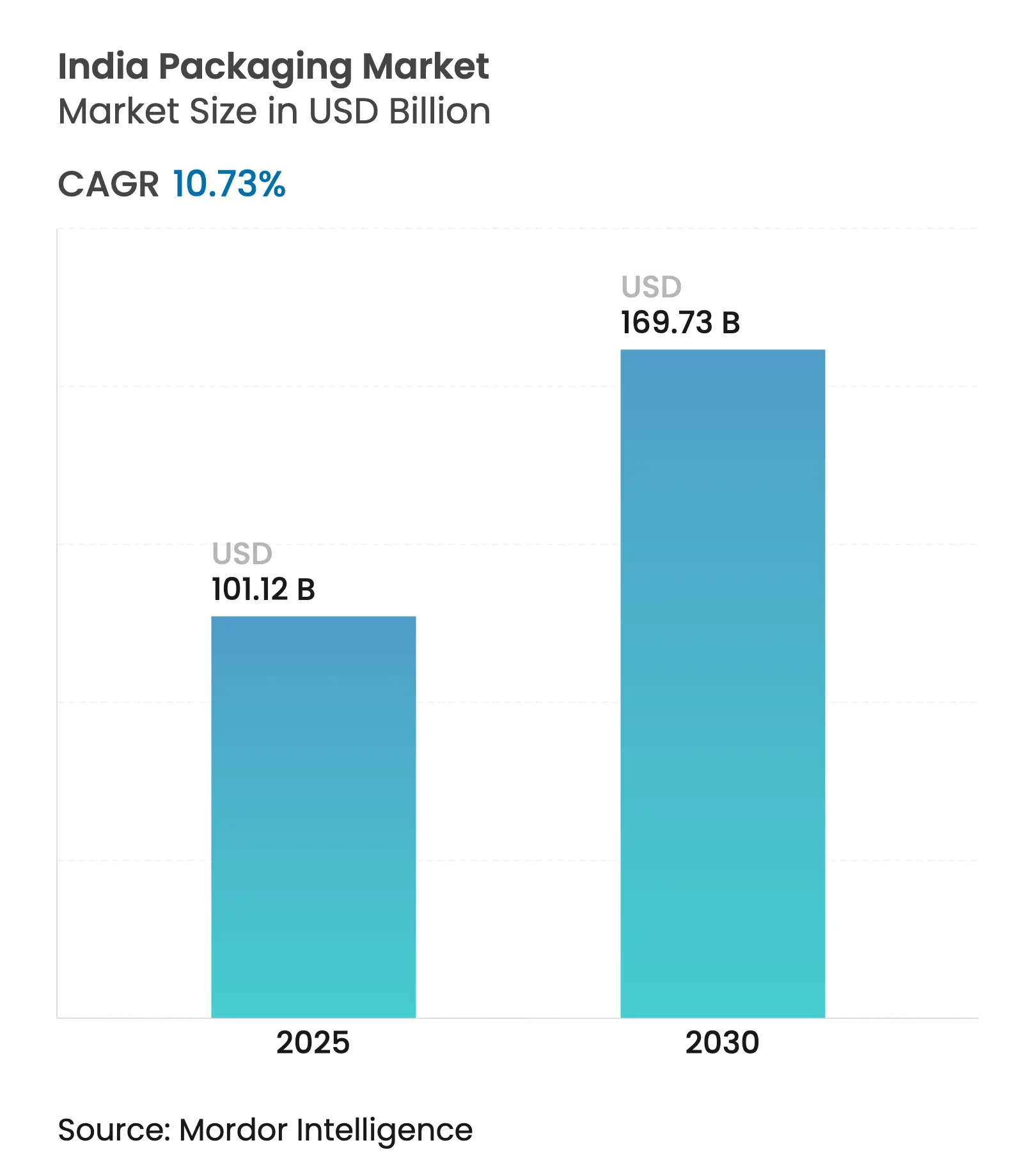

| Market Size (2025) | USD 101.12 Billion |

| Market Size (2030) | USD 169.73 Billion |

| Growth Rate (2025 - 2030) | 10.73 % CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

India Packaging Market Analysis by Mordor Intelligence

The India packaging market size is valued at USD 101.12 billion in 2025 and is forecast to reach USD 169.73 billion by 2030, advancing at a 10.73% CAGR. The India packaging market is shifting from commodity containers to technology-enabled solutions as Extended Producer Responsibility (EPR) rules demand 30% recycled content in rigid plastics by 2025 and 60% by 2029. Quick-commerce operators in tier-1 cities, rising exports of generic medicines, and consumer preference for sustainably sourced materials are expanding the India packaging market into new substrates, barrier coatings, and distribution models. Capital flows are accelerating as private equity groups finance consolidations that help converters fund automation, closed-loop recycling, and advanced analytics. Paperboard and compostable films are winning share as multinationals align procurement with global decarbonization targets, while domestic brands adapt pack formats for rural cold-chain gaps and multilingual labelling. Competition is also intensifying in bottle-to-bottle PET where joint ventures between global resin majors and local recyclers are scaling facilities close to Western and Southern manufacturing hubs.

Key Report Takeaways

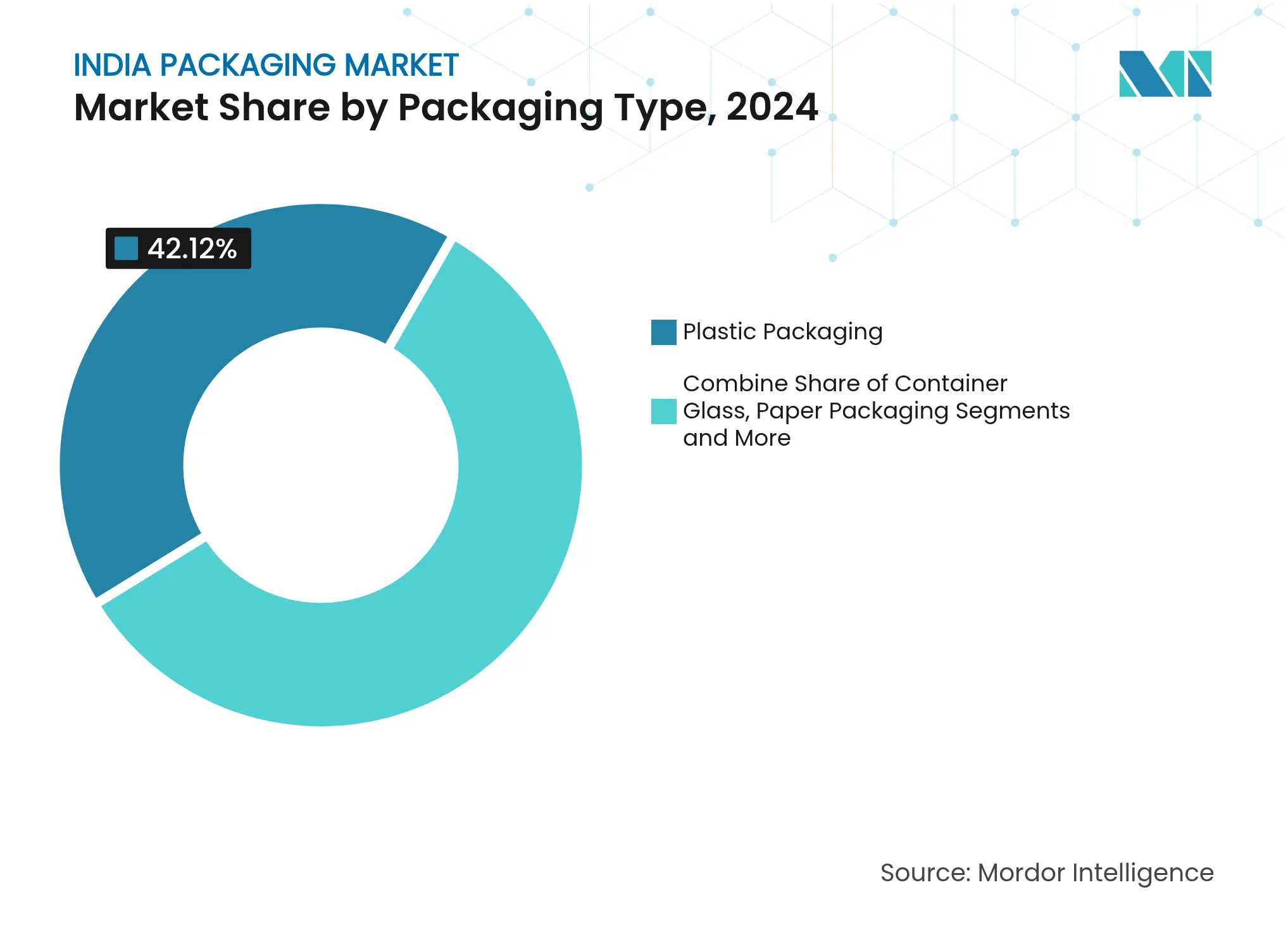

- By packaging type, plastic held 42.12% of India packaging market share in 2024, while paperboard grew at the fastest 12.21% CAGR through 2030.

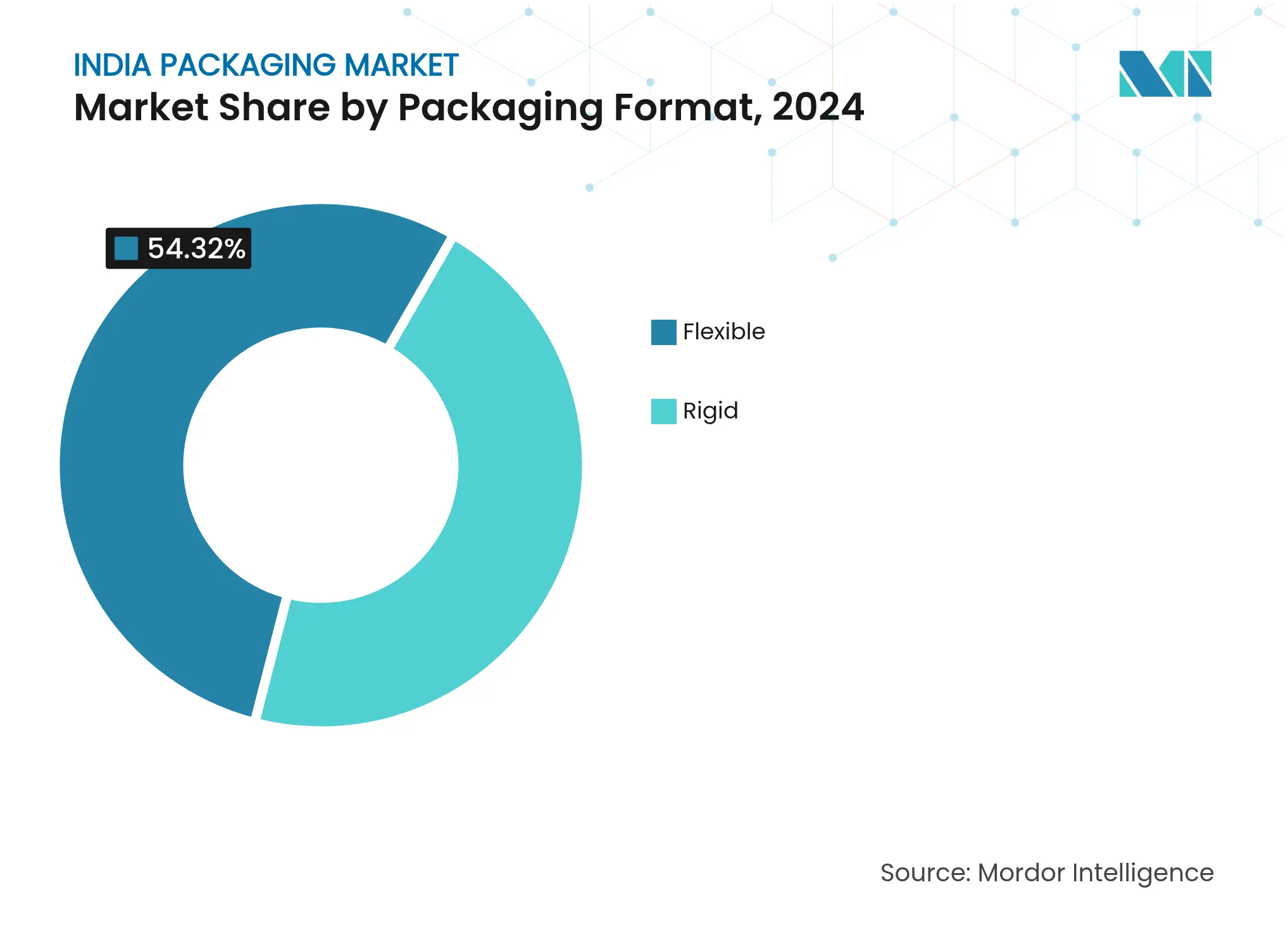

- By packaging format, flexible solutions led with 54.32% of the India packaging market size in 2024 and expanded at an 11.51% CAGR.

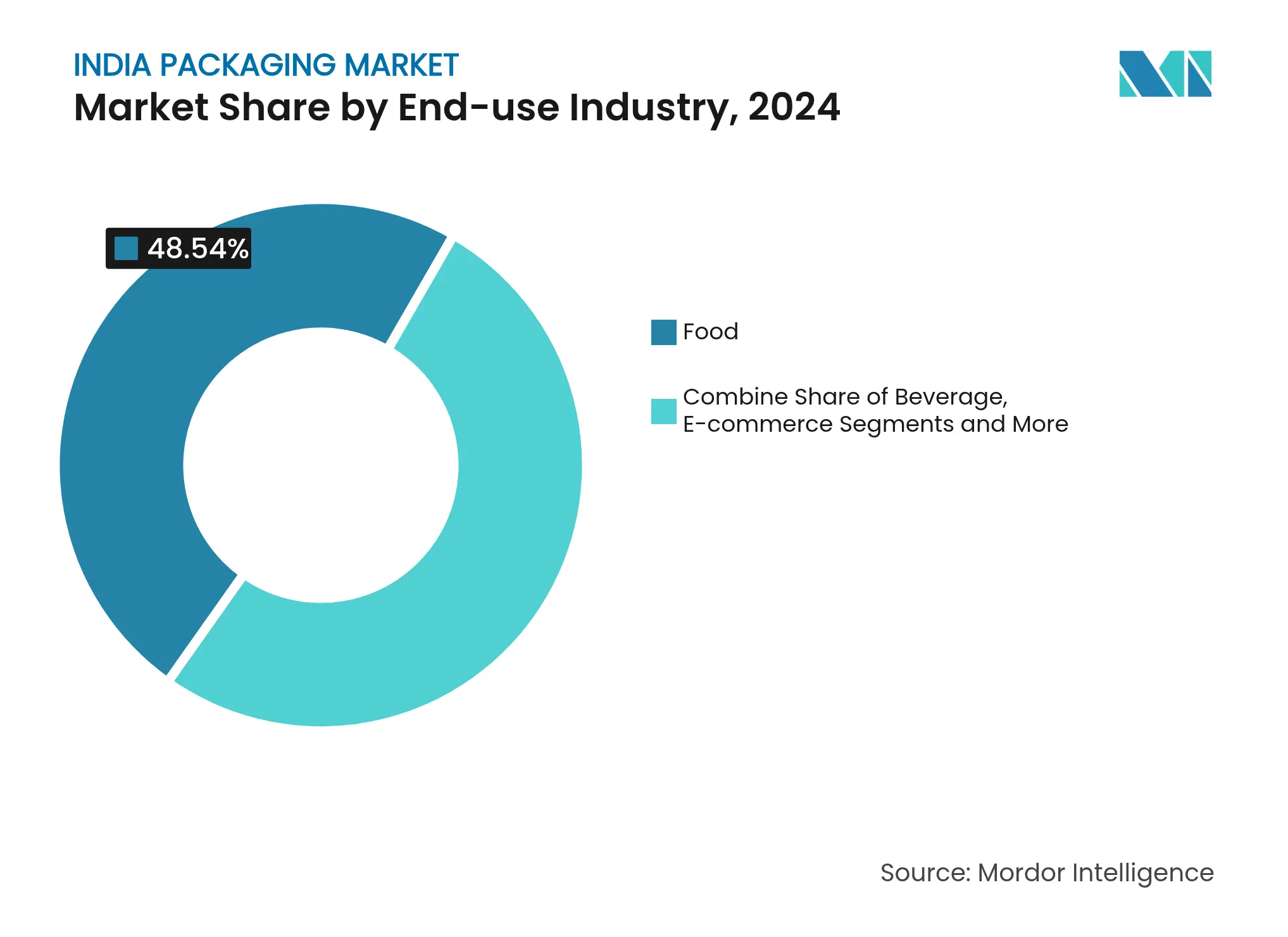

- By end-use industry, food accounted for 48.54% of India packaging market size in 2024, whereas e-commerce packaging is projected to grow at 15.1% CAGR to 2030.

- By business activity, over 900 paper mills collectively supplied less than one-third of national demand, highlighting consolidation potential encouraged by PAG’s USD 1.2 billion series of acquisitions.

India Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Surge in Quick-Commerce Fulfilment Demands from Tier-1 Indian Cities Surge in Quick-Commerce Fulfilment Demands from Tier-1 Indian Cities | +2.1% | Tier-1 cities with spillover to Tier-2 urban centers | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:+2.1% | Geographic Relevance:Tier-1 cities with spillover to Tier-2 urban centers | Impact Timeline:Short term (≤ 2 years) |

Government EPR Mandate Accelerating Recycled-Content Adoption Government EPR Mandate Accelerating Recycled-Content Adoption | +1.8% | National, with early compliance in Maharashtra, Gujarat, Tamil Nadu | Medium term (2-4 years) | |||

Rapid Capacity Addition in PET Bottle-to-Bottle Recycling Facilities Rapid Capacity Addition in PET Bottle-to-Bottle Recycling Facilities | +1.4% | Western and Southern India manufacturing hubs | Medium term (2-4 years) | |||

Ready-to-Eat Food Penetration in Rural Markets Boosting Flexible Pouches Ready-to-Eat Food Penetration in Rural Markets Boosting Flexible Pouches | +1.2% | Rural markets across North and Central India | Long term (≥ 4 years) | |||

Rise of 100% Compostable Agro-Residue Mailers among D2C Brands Rise of 100% Compostable Agro-Residue Mailers among D2C Brands | +0.9% | Urban centers with D2C concentration | Short term (≤ 2 years) | |||

Record Pharma Export Growth Requiring Sterile Vial & Ampoule Supply Record Pharma Export Growth Requiring Sterile Vial & Ampoule Supply | +1.5% | Export-oriented pharmaceutical clusters in Hyderabad, Ahmedabad | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Surge in Quick-Commerce Fulfilment Demands from Tier-1 Indian Cities

Quick-commerce promises delivery in 10-30 minutes, pushing the India packaging market toward hybrid materials that cushion, insulate, and prove tamper evidence within densely packed rider bags. Corrugated mini-shippers are replacing conventional mailers to reduce scuffing across multiple hand-offs, while micro-perforated polymer windows regulate moisture for fresh produce. Temperature stability is critical for last-mile pharmacy and dairy packs; hence converters promote phase-change gel liners compatible with municipal recycling streams. UFlex noted early rural adoption of these designs, hinting that scale benefits will soon reach tier-2 cities as last-mile networks densify. [1]UFlex Limited, “Q4 FY24 Investor Presentation,” uflexltd.comInvestors view the segment as a gateway to double-digit growth because high-velocity SKUs deliver repeat volumes that offset the cost of premium substrates, reinforcing the India packaging market’s shift toward performance-driven value propositions.

Government EPR Mandate Accelerating Recycled-Content Adoption

The April 2025 deadline for 30% post-consumer resin in rigid plastics forces producers to redesign packs and secure food-grade rPET in a supply-constrained environment. Only five licensed Indian recyclers can supply compliant material, so beverage and dairy brands are vertically integrating or locking multi-year contracts to guarantee feedstock. Investments exceeding INR 10,000 crore since 2022 have upgraded wash lines, extruders, and de-contamination units, making recycling capacity a competitive moat rather than a statutory burden. As the target ratchets to 60% by 2029, the India packaging market anticipates accelerated mergers between resin suppliers and fillers, establishing integrated ecosystems that lower reverse logistics costs and buoy margins through extended producer credits.

Rapid Capacity Addition in PET Bottle-to-Bottle Recycling Facilities

Ganesha Ecopet tripled its bottle-grade rPET output to 42,000 tpa using Starlinger systems, positioning to capture 25% of national PET waste by 2026. Parallel ventures by Indorama Ventures, Dhunseri, and Varun Beverages will add 100 kt by 2025, clustering plants near port-proximate Maharashtra and Tamil Nadu for export flexibility. [2]Indorama Ventures, “Joint Venture Plans Multiple Recycling Facilities,” indoramaventures.com Concentrated hubs shorten bale haul distances, cut greenhouse emissions, and enable traceability through digital bale tags. These efficiencies anchor the India packaging market’s circular economy trajectory, enticing global CPGs to pre-book recycled resin quotas for ASEAN and Middle-East supply chains handled from India.

Ready-to-Eat Food Penetration in Rural Markets Boosting Flexible Pouches

Rising disposable income and all-weather rural roads are broadening the addressable base for ambient snacks, millet mixes, and fortified dairy drinks. Flexible pouches thrive because they deliver gas and light barriers at low gram-weight and fit “sachet economics” that encourage trial purchases. Amul’s organic line and ITC’s multigrain launches rely on retort-ready laminates compatible with kerbside collection programs. Pakka’s agro-residue compostable films add biodegradability, enabling direct field compost when municipal services lag. Over the long term, the India packaging market will see value migrate toward flexible pack innovators who balance performance, affordability, and certified compostability.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Intermittent Moratoriums on Single-Use Plastics Intermittent Moratoriums on Single-Use Plastics | -1.3% | National, with varying enforcement across states | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-1.3% | Geographic Relevance:National, with varying enforcement across states | Impact Timeline:Short term (≤ 2 years) |

Volatile Kraft Paper Prices on Imported Waste-Paper Disruptions Volatile Kraft Paper Prices on Imported Waste-Paper Disruptions | -0.8% | Paper manufacturing clusters in Odisha, Andhra Pradesh, Karnataka | Medium term (2-4 years) | |||

Limited Cold-Chain Infrastructure Constraining Active Packaging Limited Cold-Chain Infrastructure Constraining Active Packaging | -0.6% | Rural markets and Tier-2/3 cities with infrastructure gaps | Long term (≥ 4 years) | |||

Fragmented Converter Base Curtailing Automation Investments Fragmented Converter Base Curtailing Automation Investments | -0.9% | National, particularly affecting small-scale converters | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Intermittent Moratoriums on Single-Use Plastics

Disparate state bans on straws, stirrers, and certain bags regulate roughly 11% of India’s single-use output, leaving producers juggling dual production lines and inventory buffers. Because enforcement vacillates, small converters hesitate to finance new molds, lowering capacity utilization and inflating unit costs. Exclusions covering multi-layered food wraps and beverage bottles distort competitive parity between flexible and rigid formats, injecting uncertainty into the India packaging market’s capital-planning cycles. Brands hedge by designing mono-material structures that could meet future bans yet stay price competitive, but uncertain policy cadence still compresses ROI horizons.

Volatile Kraft Paper Prices on Imported Waste-Paper Disruptions

Shipping surcharges and supply gaps for recovered fiber from Europe and North America trigger double-digit swings in kraft prices. Domestic mills lobby for anti-dumping tariffs on virgin board imports, adding another variable for converters. Margin pressure slows paper substitution despite sustainability targets.

Segment Analysis

By Packaging Type: Plastic Dominance Faces Sustainable Disruption

Plastic retained 42.12% share of the India packaging market in 2024 thanks to unmatched versatility in food, pharma, and industrial chains. Paperboard, though smaller, expanded fastest at a 12.21% CAGR through 2030 as e-commerce, QSRs, and government procurement teams demanded visibly recyclable options. Container glass held niche strength in premium spirits and parenteral drugs, while metal cans secured longer shelf life for processed foods under rural ambient temperatures. The plastic segment’s shift toward recycled content is redefining supply contracts, with UFlex recycling 6,600 t of post-consumer PET in FY 2024 as part of its backward integration plan. ITC earmarked 30-35% of its INR 20,000 crore capex to paperboards and packaging, reinforcing the trajectory toward fiber-based alternatives.

The India packaging market size for rigid plastics linked to beverages and household cleaning is projected to grow alongside recycled-content mandates that encourage stable offtake agreements for rHDPE and rPP pellets. Conversely, virgin multilayer laminates face down-trades toward paper-poly hybrid wraps that can delaminate in mainstream recycling. The India packaging industry continues to pilot enzymatic depolymerization and solvent purification to push recycled-content ceilings above 70% without compromising food contact safety. Firms that integrate mechanical and chemical recycling at scale are expected to command a premium, shifting competitive advantage from extrusion throughput to resin reclamation proficiency.

Note: Segment shares of all individual segments available upon report purchase

By Packaging Format: Flexible Solutions Drive Market Evolution

Flexible packs captured 54.32% share of the India packaging market in 2024 and advanced at an 11.51% CAGR as converters substituted rigid tubs with lightweight pouches that cut freight costs by up to 70%. Demand surged from ready-to-eat grains, nutraceutical sachets, and single-dose agrochemicals, each benefitting from hermetic seals and easy tear-open features. Mono-material PE-PE and PP-PP laminates are gaining traction under design-for-recycling protocols, while EVOH barriers extend shelf life for retorted products without aluminium foils. Innovations such as digital watermarks allow automatic sortation in material recovery facilities, enhancing circularity credentials.

Rigid formats still dominate carbonated beverages, detergents, and premium skincare, where rigidity, drop resistance, and shelf impact outweigh weight penalties. Growth opportunities persist in thin-wall injection-molded PP tubs fortified with talc fillers that enable 20% weight savings. Aseptic cartons received a boost when SIG invested EUR 90 million in an Ahmedabad plant able to supply 4 billion packs annually, reflecting confidence that the India packaging market will accelerate the shift from open pouches to shelf-stable milk systems. Overall, converters are recalibrating machinery portfolios, hedging between flexographic presses for high-mix SKUs and injection lines configured for post-consumer resin blends.

By End-Use Industry: Food Sector Leadership Amid E-commerce Disruption

The food industry held 48.54% share of the India packaging market in 2024, driven by consumption of packaged snacks, staples, and dairy products that require controlled-atmosphere seals. Urban nuclear households favor portioned packs, pushing brands toward stand-up pouches with re-closable zippers. Rural uptake of fortified staples positions flexible laminates as the preferred choice due to their moisture and pest resistance during long transits. The beverage sector straddles PET and glass, but premium craft spirits increasingly deploy anodized aluminium tins to reinforce brand narratives around sustainability.

E-commerce packaging, expanding at a 15.1% CAGR, is reshaping designs around dimensional weight pricing and returns-ready constructions. Paper-based void fillers and corrugated B-flute shippers are replacing bubble wrap, but brands remain cautious about paper dust contamination for electronics and cosmetics. Pharmaceutical exports demand Type I borosilicate glass vials, clean-room molded HDPE bottles, and tamper-evident closures, all of which command higher margins and strict certification. Industrial bulk packs, from IBCs to woven PP FIBCs, rely on UV-stabilized films suited to tropical outdoor storage. Segment diversification underscores the India packaging industry’s need for modular production lines that pivot quickly across downstream categories without incurring prolonged changeover downtime.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Western and Southern India dominate the India packaging market thanks to integrated petrochemical complexes, port access, and agri-processing clusters. Maharashtra, Gujarat, and Tamil Nadu host multilayer film lines, recycled-PET pelletizers, and corrugated mega-plants that leverage export-oriented logistics. These states also rolled out EPR registries early, giving local converters a head start in certifying traceability and reclaim rates. Joint ventures, such as Varun Beverages–Indorama, chose industrial estates near Ahmedabad for proximity to bottle-grade resin buyers.

Northern and Eastern corridors, while historically under-served, are emerging opportunity nodes. Government-backed industrial zones in Uttar Pradesh and West Bengal provide tax incentives for flexible pouch and folding carton units targeting horticulture and aquaculture value chains. Cold-chain deficiencies still inhibit active packaging adoption, but rising smartphone penetration fuels demand for tamper-evident e-commerce cartons in tier-2 towns. The India packaging market expects these regions to absorb capacity overflow from Western clusters, balancing the national footprint and easing freight bottlenecks.

Export-centric pharma hubs in Hyderabad and Visakhapatnam amplify demand for Type I glass ampoules and coated aluminium blisters that meet EU and US Pharmacopeia. SGD Pharma’s collaboration with Corning to produce Velocity Vials in Telangana exemplifies how regional specialization secures compliant supply for high-value biologics. Across zones, municipal policies on plastic waste segregation vary, influencing feedstock availability for localized recycling plants and shaping supply-chain resilience for the India packaging market.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

Market Concentration

The India packaging market is fragmented. PAG’s USD 1.2 billion spree, including stakes in Manjushree Technopack and Pravesha Industries, signals an ongoing roll-up strategy targeting high-margin pharma and food niches. Consolidators prioritize assets with in-house recycling, sterile molding capacity, and multi-color flexo presses to serve diversified FMCG and healthcare pipelines. Smaller units, often family-run paper mills, find it difficult to finance AI-equipped inspection systems or robotic palletizers, widening the productivity gap.

Sustainability anchoring drives technology races: UFlex integrates AI for predictive maintenance, waste-heat recovery, and needle-sharp register control on gravure lines to cut ink wastage. [3]UFlex Limited, “Latest News & Insights,” uflexltd.comStart-ups such as Bambrew switch bamboo and bagasse into molded mailers, having displaced more than 1,000 t of plastic while serving 170 enterprise clients. International suppliers respond by localizing; SIG’s new aseptic carton plant reduces lead times for dairy co-ops shifting to shelf-stable packs. Meanwhile, ITC leverages forestry stewardship to secure virgin fiber, balancing commodity risk with certified paperboard used in growing quick-service channels. Strategic alliances that pair design labs with material scientists will likely decide future leadership in the India packaging market.

India Packaging Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: SIG opened its first Indian aseptic carton plant in Ahmedabad, investing EUR 90 million with 4 billion-pack capacity and earmarking another EUR 50 million for an extrusion line by 2027.

- February 2025: Ganesha Ecopet lifted bottle-grade rPET capacity to 42,000 tpa through two Starlinger systems, aiming to recycle 25% of national PET bottle waste by 2026.

- January 2025: PAG acquired Pravesha Industries at an enterprise value of INR 1,700 crore, strengthening its position in sterile pharma packaging.

- January 2025: Canpac Trends purchased Saptagiri Packagings’ Silvassa facility, adding blister backer cards to its consumer portfolio.

Table of Contents for India Packaging Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Surge in Quick-Commerce Fulfilment Demands from Tier-1 Indian Cities

- 4.2.2Government EPR Mandate Accelerating Recycled-Content Adoption

- 4.2.3Rapid Capacity Addition in PET Bottle-to-Bottle Recycling Facilities

- 4.2.4Ready-to-Eat Food Penetration in Rural Markets Boosting Flexible Pouches

- 4.2.5Rise of 100 % Compostable Agro-Residue Mailers among D2C Brands

- 4.2.6Record Pharma Export Growth Requiring Sterile Vial and Ampoule Supply

- 4.3Market Restraints

- 4.3.1Intermittent Moratoriums on Single-Use Plastics

- 4.3.2Volatile Kraft Paper Prices on Imported Waste-Paper Disruptions

- 4.3.3Limited Cold-Chain Infrastructure Constraining Active Packaging

- 4.3.4Fragmented Converter Base Curtailing Automation Investments

- 4.4Supply-Chain Analysis

- 4.5Trade Scenario Analysis (under relevant HS codes)

- 4.6Routes to Entry into the Indian Packaging Sector

- 4.7Technological Outlook

- 4.8Regulatory Outlook

- 4.9Current Recycling Trends in India

- 4.10Key Industry Themes

- 4.10.1Sustainability Imperatives in FandB Packaging

- 4.10.2Closed-Loop Solutions Emerging in Organised Retail

- 4.11Porter's Five Forces

- 4.11.1Bargaining Power of Suppliers

- 4.11.2Bargaining Power of Buyers

- 4.11.3Threat of New Entrants

- 4.11.4Threat of Substitutes

- 4.11.5Competitive Rivalry

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1By Packaging Type

- 5.1.1Plastic Packaging

- 5.1.1.1By Type

- 5.1.1.1.1Rigid Plastic Packaging

- 5.1.1.1.1.1By Material Type

- 5.1.1.1.1.1.1Polyethylene (PE)

- 5.1.1.1.1.1.2Polypropylene (PP)

- 5.1.1.1.1.1.3Polyethylene Terephthalate (PET)

- 5.1.1.1.1.1.4Polyvinyl Chloride (PVC)

- 5.1.1.1.1.1.5Polystyrene (PS) and Expanded Polystyrene (EPS)

- 5.1.1.1.1.1.6Other Material Types

- 5.1.1.1.1.2By Product Type

- 5.1.1.1.1.2.1Bottles and Jars

- 5.1.1.1.1.2.2Caps and Closures

- 5.1.1.1.1.2.3Trays and Containers

- 5.1.1.1.1.2.4Other Product Types

- 5.1.1.1.1.3By End-use Industry

- 5.1.1.1.1.3.1Food

- 5.1.1.1.1.3.2Beverage

- 5.1.1.1.1.3.3Pharmaceutical

- 5.1.1.1.1.3.4Cosmetics and Personal Care

- 5.1.1.1.1.3.5Industrial

- 5.1.1.1.1.3.6Other End-use Industry

- 5.1.1.1.2Flexible Plastic Packaging

- 5.1.1.1.2.1By Material Type

- 5.1.1.1.2.1.1Polyethylene (PE)

- 5.1.1.1.2.1.2Biaxially Oriented Polypropylene (BOPP)

- 5.1.1.1.2.1.3Cast Polypropylene (CPP)

- 5.1.1.1.2.1.4Other Material Types

- 5.1.1.1.2.2By Product Type

- 5.1.1.1.2.2.1Pouches and Bags

- 5.1.1.1.2.2.2Films and Wraps

- 5.1.1.1.2.2.3Other Product Types

- 5.1.1.1.2.3By End-use Industry

- 5.1.1.1.2.3.1Food

- 5.1.1.1.2.3.2Beverage

- 5.1.1.1.2.3.3Pharmaceutical

- 5.1.1.1.2.3.4Cosmetics and Personal Care

- 5.1.1.1.2.3.5Industrial

- 5.1.1.1.2.3.6Other End-use Industry

- 5.1.1.2By Product Type

- 5.1.1.2.1Bottles and Jars

- 5.1.1.2.2Pouches and Bags

- 5.1.1.2.3Bulk-Grade Products

- 5.1.1.2.4Other Product Types

- 5.1.1.3By End-use Industry

- 5.1.1.3.1Food

- 5.1.1.3.2Beverages

- 5.1.1.3.3Cosmetics and Personal Care

- 5.1.1.3.4Pharamceuticals

- 5.1.1.3.5Industrial

- 5.1.1.3.6Other End-use Industry

- 5.1.2Paper Packaging

- 5.1.2.1By Product Type

- 5.1.2.1.1Folding Carton

- 5.1.2.1.2Corrugated Boxes

- 5.1.2.1.3Liquid Paperboard

- 5.1.2.1.4Other Product Type

- 5.1.2.2By End-use Industry

- 5.1.2.2.1Food

- 5.1.2.2.2Beverages

- 5.1.2.2.3E-commerce

- 5.1.2.2.4Other End-use Industry

- 5.1.3Container Glass

- 5.1.3.1By Color

- 5.1.3.1.1Green

- 5.1.3.1.2Amber

- 5.1.3.1.3Flint

- 5.1.3.1.4Other Colors

- 5.1.3.2By End-use Industry

- 5.1.3.2.1Food

- 5.1.3.2.2Beverage

- 5.1.3.2.2.1Alcoholic

- 5.1.3.2.2.2Non-Alcoholic

- 5.1.3.2.3Personal Care and Cosmetics

- 5.1.3.2.4Pharmaceuticals (excluding Vials and Ampoules)

- 5.1.3.2.5Perfumery

- 5.1.4Metal Cans and Containers

- 5.1.4.1By Material Type

- 5.1.4.1.1Steel

- 5.1.4.1.2Aluminum

- 5.1.4.2By Product Type

- 5.1.4.2.1Cans

- 5.1.4.2.2Drums and Barrels

- 5.1.4.2.3Caps and Closures

- 5.1.4.2.4Other Product Type

- 5.1.4.3By End-use Industry

- 5.1.4.3.1Food

- 5.1.4.3.2Beverage

- 5.1.4.3.3Chemicals and Petroleum

- 5.1.4.3.4Industrial

- 5.1.4.3.5Paints and coatings

- 5.1.4.3.6Other End-use Industry

- 5.2By Packaging Format

- 5.2.1Flexible

- 5.2.2Rigid

- 5.3By End-use Industry

- 5.3.1Food

- 5.3.2Beverage

- 5.3.3Pharmaceuticals and Healthcare

- 5.3.4Personal Care and Cosmetics

- 5.3.5Industrial

- 5.3.6E-commerce

- 5.3.7Other End-use Industry

6. COMPETITIVE LANDSCAPE

- 6.1Strategic Moves

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1Gerresheimer AG

- 6.3.2AGI Glaspac

- 6.3.3PGP Glass Private Limited

- 6.3.4Hindusthan National Glass & Industries Ltd.

- 6.3.5ITC Limited (Packaging Division)

- 6.3.6JK Paper Ltd.

- 6.3.7CANPACK INDIA PVT. LTD

- 6.3.8Velpack Pvt. Ltd.

- 6.3.9Smurfit WestRock

- 6.3.10Oji India Packaging Pvt Ltd

- 6.3.11KCL Limited

- 6.3.12Trident Paper Box Industries

- 6.3.13Packman Packaging Pvt. Ltd.

- 6.3.14Hitech Corporation Limited

- 6.3.15AptarGroup, Inc.

- 6.3.16Manjushree Technopack Ltd.

- 6.3.17JPFL Films Private Limited

- 6.3.18TCPL Packaging Limited

- 6.3.19UFlex Limited

- 6.3.20Polyplex Corporation Ltd.

- 6.3.21Cosmo First Limited

- 6.3.22Hindustan Tin Works Ltd

- 6.3.23Ball Corporation

- 6.3.24ZENITH TINS PVT. LTD.

- 6.3.25Kaira Can Company Ltd.

- 6.3.26Tetra Pak International S.A.

- 6.3.27Megaplast India Pvt Ltd

- 6.3.28The Bag Smiths

- 6.3.29Amcor Plc

- 6.3.30HUHTAMAKI INDIA LTD

- 6.3.31Sealed Air Corporation

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1White-space and Unmet-Need Assessment

India Packaging Market Report Scope

Packaging is defined as the process of providing a protective and informative covering to the product such that it protects the product during material handling, storage, and movement and also provides useful information to all the related supply chain partners about the content of the package. Its application can extend from primary, secondary, and tertiary to ancillary packaging.

The Indian packaging market is segmented by material (plastic, paper, container glass, metal can, and container) and end users (food and beverage, retail and e-commerce, paints and chemicals, industrial, personal care and cosmetics, and other end users). The market sizes and forecasts regarding value (USD) for all the above segments are provided.