Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

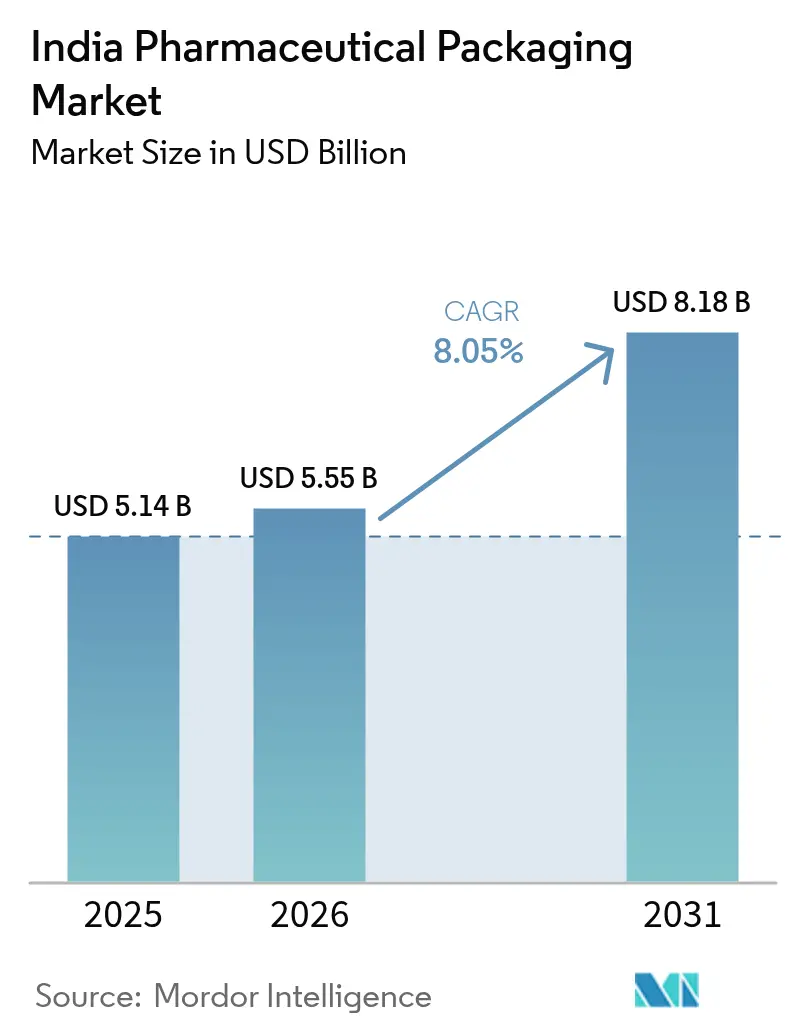

| Base Year Market Size (2025) | USD 5.14 Billion |

| Market Size (2026) | USD 5.55 Billion |

| Market Size (2031) | USD 8.18 Billion |

| Growth Rate (2026 - 2031) | 8.05% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Pharmaceutical Packaging Market Analysis by Mordor Intelligence

The India pharmaceutical packaging market size was valued at USD 5.14 billion in 2025 and estimated to grow from USD 5.55 billion in 2026 to reach USD 8.18 billion by 2031, at a CAGR of 8.05% during the forecast period (2026-2031). Heightened demand emerges from production-linked incentive outlays, digital therapeutics adoption, and rigorous sustainability regulations. Capacity additions at export-oriented plants are boosting uptake of good-manufacturing-practice compliant containers and closures, while e-pharmacy growth accelerates orders for tamper-evident flexible packs. Sustainability mandates compelling 30% recycled content in rigid formats are shaping material choices, with recycled polyethylene terephthalate and post-consumer-recycled resins gaining validation. Simultaneously, biologics fill-finish expansion encourages cold-chain compatible vials, syringes, and high-barrier films, and ongoing polymer price volatility is prompting converters to streamline sourcing and adopt digital cost controls.

Key Report Takeaways

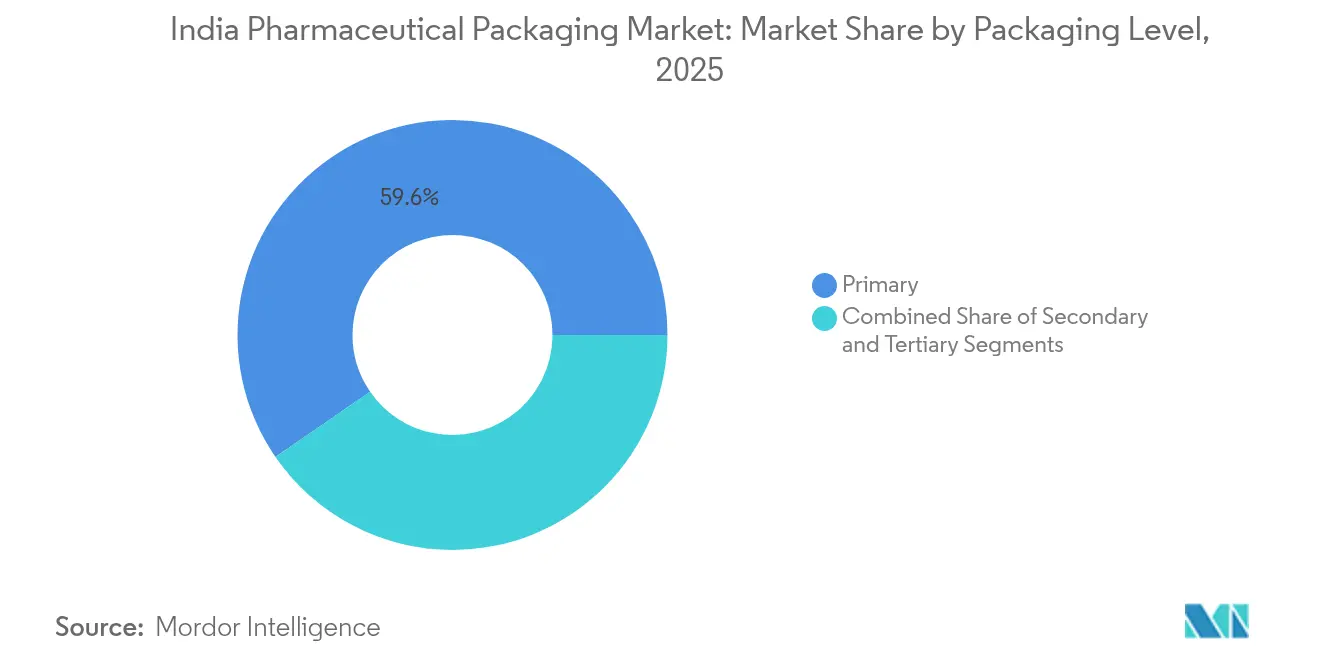

- By material type, primary packaging held 59.60% of the India pharmaceutical packaging market share in 2025 and is forecast to grow at a 8.78% CAGR through 2031.

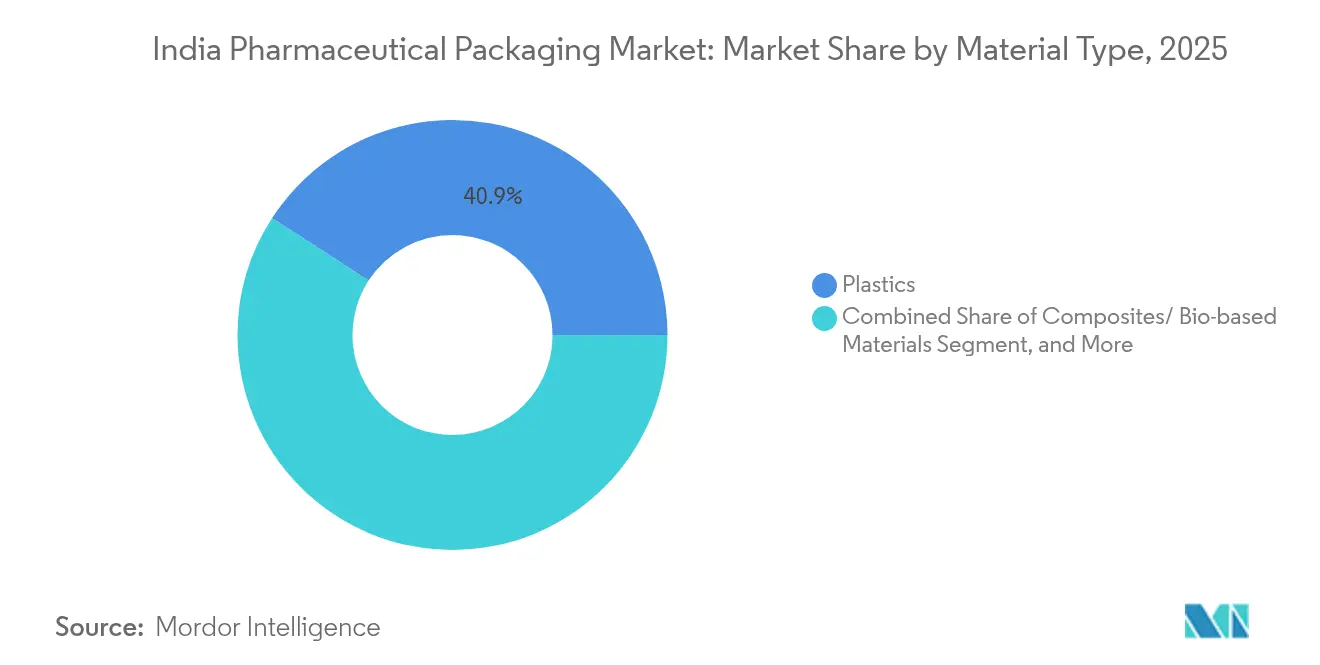

- By product type, plastics remained dominant with 40.85% 2025 revenue share, although composites and bio-based resins recorded 9.65% CAGR 2031, the fastest among all materials.

- By packaging level, bottles led with 21.05% contribution in 2025, while pouches and bags posted the strongest 9.1% CAGR 2031 among products.

- By end-user industry, pharmaceutical manufacturers retained the largest 49.20% 2025 end-user share during and contract packaging organizations expanded at a 9.55% CAGR 2031 .

- By gujarat accounted for roughly one-third of national drug output in 2024, underpinning clustering benefits for converters and logistics efficiencies.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Pharmaceutical Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated shift to pre-fillable formats | +1.8% | Gujarat, Maharashtra | Medium term (2-4 years) |

| Expansion of India's vaccine and biologics fill-finish capacity | +2.1% | Major pharma hubs nationwide | Long term (≥ 4 years) |

| Government PLI and GMP upgrades for export-oriented pharma | +2.3% | SEZ and export zones | Medium term (2-4 years) |

| E-pharmacy boom driving tamper-evident, home-delivery packs | +1.6% | Urban centers, Tier-2 rollout | Short term (≤ 2 years) |

| Sustainability mandates pushing rPET and PCR rigid plastics | +1.2% | Metro areas, national scope | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of India's Vaccine and Biologics Fill-Finish Capacity

India’s ambition to become a global biologics hub is fueling specialized containment demand. Ongoing investments, including Lonza’s gelatin capsule line in Rewari, require high-barrier films that withstand sterilization and maintain sub-zero stability across extended logistics chains. Growth in cold-chain packaging with integrated temperature indicators is enabling uninterrupted product integrity from plant to patient. Biologic developers also favor tamper-evident seals and unit-level serialization for supply chain visibility, encouraging converters to scale ISO-8 clean-room production.

Government PLI and GMP Upgrades for Export-Oriented Pharma

The Production-Linked Incentive scheme earmarked INR 2,444.93 crore (USD 293 million) for FY 2025-26, driving systematic upgrades in packaging infrastructure and supporting simultaneous compliance with FDA 21 CFR 211.132 and EU FMD serialisation requirements. Subsidy applicants must meet ambitious export targets, which translate into orders for premium laminated foils, tamper-proof closures, and cloud-connected vision inspection units. The December 2025 GMP upgrade deadline compels facilities to install ISO-8 compatible lines, raising recurring demand for validated primary packs and cleanroom consumables.

E-Pharmacy Boom Driving Tamper-Evident, Home-Delivery Packs

Direct-to-consumer medicine delivery grew swiftly across metropolitan markets, with mobile apps integrating AI dosage reminders. Packages must endure multiple courier handoffs and still assure authenticity, prompting the adoption of serialized QR-codes and break-away seals.[1]Elisabeth Cuneo, “Three Trends Shaping Pharmaceutical Packaging Today,” healthcarepackaging.com Flexible pouches sized for chronic-care regimens improve portability, and moisture-barrier sachets cater to personalized dosing. Automated dispensing warehouses favor stackable mailers that streamline pick-and-pack robotics, reinforcing demand for lightweight yet puncture-resistant laminates.

Sustainability Mandates Pushing rPET and PCR Rigid Plastics

Extended Producer Responsibility rules mandate 30% recycled content in 2024-25, escalating to 60% by 2027-28, compelling converters to validate recycled resins for pharmaceutical use. UFlex has commercialized a 90% PCR biaxially-oriented polyester film, demonstrating regulatory-approved recycled content in blister webs. Converters are investing in traceable waste-feedstock procurement and in-house pelletizing to guarantee supply continuity. Sustainable moves dovetail with brand differentiation as exporters preference carbon-reduced packs for regulated markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in medical-grade polymer and glass input costs | -1.4% | Import-dependent regions | Short term (≤ 2 years) |

| Single-use-plastic EPR and recycling logistics gaps | -0.9% | Tier-2/3 cities | Medium term (2-4 years) |

| High cap-ex for ISO-8 clean-room packaging lines | -1.1% | Gujarat, Maharashtra, Tamil Nadu | Long term (≥ 4 years) |

| Fragmented downstream distribution inflating unit pack costs | -0.8% | Rural networks in rural distribution networks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Medical-Grade Polymer and Glass Input Costs

Polypropylene fluctuated between USD 970-990 per metric ton CFR India in 2025, eroding converter margins and complicating contract pricing. Glass container makers face rising energy tariffs and silica sand shortages, adding pass-through costs for high-value vials. Overall EBITDA margins for flexible packaging dipped to 8% in FY 2024-25 amid resin oversupply and lukewarm export demand. These factors force packaging firms to hedge raw materials and optimize formulations to cushion profitability.

Single-Use-Plastic EPR and Recycling Logistics Gaps

While mandatory recycled-content thresholds are clear, collection infrastructure for contaminated pharmaceutical plastics lags, particularly beyond primary cities. Separate handling protocols and traceability requirements inflate reverse-logistics expenses, and uneven state-level enforcement breeds compliance uncertainty. Producers are piloting take-back programs, yet commercial scale remains limited, constraining availability of pharmaceutical-grade PCR feedstock and delaying broader circular-economy benefits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Sustainable Alternatives Gain Momentum

In 2025, plastics led with 40.85% revenue, yet composites and bio-based resins surged at a 9.65% CAGR, the highest among all materials. Stringent Extended Producer Responsibility norms are spurring trials of recycled PET inserts and sugarcane-based HDPE lines. Pharmaceutical buyers insist on full extractable-leachable validation, prompting converters to build application labs and secure regulatory master files. India's pharmaceutical packaging market size for bio-based materials is set to expand quickly as contract packers market greener credentials to multinational sponsors. Parallel investments in enzymatic delamination promise recovery of aluminum layers from aseptic cartons, illustrating innovation depth. Future growth depends on a robust supply chain for high-purity recycled feedstock and harmonized national testing standards.

Sustainability themes also reshape glass and metal demand. Borosilicate vials retain relevance for biologics owing to inertness, yet lightweight coated glass variants target energy reductions during melt. Aluminum collapsible tubes find use in topical formulations where zero-leach barriers and recyclability offer dual appeal. Paperboard is regaining favor for secondary cartons as water-based coatings achieve 95% humidity resistance, satisfying patient safety while enabling fiber recovery. Collectively these shifts reflect heightened material stewardship across the India pharmaceutical packaging market.

By Product Type: Flexible Formats Drive Innovation

Bottles commanded 21.05% of 2025 revenue, yet pouches and bags logged a 9.1% CAGR, the fastest among all categories, fueled by e-pharmacy parcel shipping. India's pharmaceutical packaging market share for prefilled syringes is climbing as biologic therapies proliferate, demanding silicon-oil-free plungers and tight particulate controls. Meanwhile, blister-pack upgrades focus on child-resistant push-through lidding and NFC tags that connect patients to refill portals. Smart features migrate into flexible sachets, embedding humidity sensors for at-home adherence monitoring.

Downstream, rapid swab kits and nasal sprays push demand for snap-fit caps, integrated droppers, and low-dead-volume valves. Converters offering turnkey molding plus pulsed-light sterilization win contracts where lean supply chains are pivotal. India pharmaceutical packaging market size for adaptive closures is projected to widen as personalized therapy packs and micro-dosing devices multiply. The resulting SKU complexity rewards firms capable of short-run digital printing and agile changeovers.

By Packaging Level: Primary Packaging Dominance Continues

Primary formats captured 59.60% revenue in 2025, reflecting direct contact requirements that elevate regulatory scrutiny and capital intensity. Serialization imprints at the dose level improve anti-counterfeit control and allow remote batch recalls, aligning with National Drug Authentication plans. Future primary pack trends center on built-in RFID for cold-chain visibility and laser-etched variable data replacing paper inserts. Secondary and tertiary packs, while smaller contributors, embrace recycled fiber content and right-sized cushioning to shrink deadweight in ecommerce parcels.

Multi-layer compatibility between primary vials, nested tubs, and shippers influences barrier design. High-density polyethylene blow-fill-seal bottles bring sterile barrier integrity and shorten validation cycles, attracting oral-liquid generics. India's pharmaceutical packaging market size, attributed to blow-fill-seal, will benefit from track-and-trace mandates at the bottle level. Automated vision cameras combined with AI detect 10 micron particulates, cutting inspection labor and elevating batch throughput for export-grade packing houses.

By End-User Industry: Contract Packaging Organizations Accelerate

Pharmaceutical manufacturers retained 49.20% 2025 spending, yet contract packaging organizations (CPOs) advanced at a 9.55% CAGR as innovators outsource non-core activities. CPOs leverage scale procurement and dedicated compliance teams to satisfy multi-jurisdiction audits, positioning themselves as growth engines within the India pharmaceutical packaging market. Many add formulation and analytic labs to become one-stop CDMOs, aligning with global sponsor preference for integrated supply chains.

Retail and institutional pharmacies now favor shelf-ready packs featuring scannable lids and recyclable trays that speed dispensing. Hospital demand for ready-to-administer injector cartridges spurs CPO investment in barrier isolators and high-speed plunger insertion. Meanwhile, healthcare startups seek tiny batch runs for orphan drugs, prompting contract packers to deploy modular lines that can switch between nested vials and pump sprays in under an hour. This agility cements CPOs as pivotal stakeholders through 2030.

Geography Analysis

Gujarat generated roughly one-third of national pharmaceutical output in 2024, reinforcing the state’s anchor role in the India pharmaceutical packaging market. Ports at Mundra and Pipavav enable swift resin imports and finished-pack exports, while a dense vendor base shortens lead times for ISO-certified tooling. State government incentives further entice converters to locate extrusion, printing, and sterilization units adjacent to large drug plants, compressing supply cycles and lowering logistics carbon footprint.

Maharashtra and Tamil Nadu follow as regional focal points, particularly for complex biologics and hormone therapies that demand clean-room vial washing and cold-storage warehouses. Recent industrial parks near Pune and Chennai integrate common effluent treatment and centralized utility corridors, easing GMP compliance for packaging producers. India pharmaceutical packaging market size, attributed to southern clusters, grows as multinational sponsors award long-term fill-finish projects conditioned on proximity to international airports.

Emerging northeastern corridors benefit from freight subsidies yet grapple with container shortages and limited specialty-film supply. Converters establishing satellite depots in Assam and Meghalaya gain first-mover advantage but must invest in on-site quality testing and redundant power to assure consistency. National highway upgrades under Bharatmala Phase-I unlock road transit to northern drug depots, balancing distribution across hinterlands and positioning the India pharmaceutical packaging market for broader geographic diversification.

Value Chain Analysis

The value chain starts with upstream feedstocks and substrates, including medical-grade polymers (PP, HDPE/LDPE, PET), glass tubing and molded glass for vials and ampoules, aluminum foils and lidding, paperboard, inks, adhesives, and coatings. Packaging converters and component makers convert these inputs into primary packs (bottles, vials, ampoules, blisters, prefilled devices, closures), then secondary and tertiary formats (cartons, labels, inserts, shippers), with quality systems aligned to drug makers' supplier-qualification expectations under Schedule M of the Drugs Rules, 1945. In India, standards and test methods, including Indian Standards for plastics such as IS 12252 for PET and IPC guidance on primary packaging, affect resin selection, extractables and leachables programs, and the documentation package needed for regulated product supply.

Midstream manufacturing is increasingly characterized by cleanroom-capable operations (ISO-8 where required), in-line inspection, and variable-data printing for serialization and authentication, which links packaging lines to data capture and traceability workflows. Distribution runs from converters to pharmaceutical manufacturers and contract packaging organizations, then through domestic wholesale and retail channels as well as export lanes supported by western logistics infrastructure, such as Gujarat production clusters backed by ports like Mundra and Pipavav. A near-term inflection for the chain is enhanced oversight of printed packaging material suppliers. In June 2026, CDSCO initiated a plan to bring printed pharmaceutical packaging material manufacturers (cartons, labels, foils, inserts) under a registration framework, increasing the weight of auditable supplier documentation, traceability controls, and compliant print/VDP capacity.

Competitive Landscape

The competitive field features multinational specialists, diversified Indian conglomerates, and nimble regional firms, creating a moderately fragmented structure. No single company exceeds a 15% revenue share across the India pharmaceutical packaging market, though some dominate niches such as polymer films or glass ampoules. Technology differentiation, particularly in digital serialization and in-line vision systems, is the chief contract-winning lever; converters with proven data-integrity frameworks and cyber-secure cloud dashboards gain insurer and regulator confidence.

UFlex extends vertical reach from PET resin extrusion to finished blister foils, leveraging in-house ink and coating chemistries that accelerate custom barrier solutions.[3]UFlex Limited, “UFlex News and Insights,” uflexltd.com Gerresheimer’s acquisition of Bormioli Pharma strengthens glass vial capacity, giving global vaccine makers dual-source risk mitigation. Domestic newcomer Mold-Tek Packaging deploys in-mold labeling for high-definition graphics, lowering copy-cat risk for over-the-counter brands. Polymerupdate-reported raw material swings push converters to secure long-term resin contracts, leading some to consider backward integration into polypropylene compounding.

White-space opportunities revolve around smart packaging, with start-ups embedding NFC chips in child-safe caps for dose reminders. Sustainability continues as a battleground: firms first-certified for 60% PCR rigid bottles are likely to lock in supply agreements with multinational generic majors looking to meet EU Green Deal provisions. Collaborations with cloud analytics vendors to create predictive maintenance for form-fill-seal lines illustrate the convergence of packaging and Industry 4.0, sharpening the competitive divide between digital leaders and laggards.

India Pharmaceutical Packaging Industry Leaders

Medipack Innovations Private Limited

N S Industries

A S Packers

North East Pharmapack Pvt Ltd

Packtime Innovations Pvt Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Two whitespace areas are taking shape around compliance-grade traceability and sustainability execution at scale. On the compliance side, tighter oversight of printed packaging materials, including CDSCO deliberations around formal registration and unique identifiers for printed packaging manufacturers, is raising demand for qualified partners that can support secure variable-data printing, controlled artwork change management, and data integrity across cartons, labels, foils, and inserts. This is also driving investments that pair packaging with inspection and traceability. Amcor commissioned an expansion at its Sira, Karnataka, healthcare packaging facility in June 2026, highlighting high-performance formats and automated vision systems, which points to continued pull for higher-spec manufacturing and QA capabilities within India.

On the sustainability side, EPR-linked recycled-content requirements and circularity pilots are opening opportunities in pharmaceutical-grade recycled-material validation, traceable feedstock procurement, and take-back logistics tailored to contaminated healthcare plastics. A real-life example is the April 2026 launch of a pharma-led pilot Deposit Return System (DRS) project by VINSAK, Pravesha, and Recykal, which shows collection and reverse logistics models moving beyond concept work. Converters that can deliver validated PCR/rPET structures while maintaining barrier, seal integrity, and regulatory documentation are positioned to win programs from exporters and organized channels, especially when packaging must support tamper-evidence, child resistance, and authentication for e-pharmacy distribution.

Recent Industry Developments

- July 2026: Mankind Pharma disclosed in its FY 2025-26 annual report that Medipack Innovations Private Limited is a 51% subsidiary and North East Pharma Pack is a 57.50% subsidiary. The disclosure reinforces a tighter linkage between drug manufacturing and packaging capabilities, supporting better control over quality systems and supply continuity for packaging components used in commercial distribution.

- September 2025: Mankind Pharma partnered with OpenAI to deploy predictive AI quality analytics across packaging and distribution workflows, targeting faster batch-release cycles. The initiative highlights growing adoption of data-driven inspection and release controls, raising competitive expectations for converters and packers to provide cleaner data capture and more consistent pack quality.

- December 2024: Gerresheimer completed the acquisition of Bormioli Pharma, adding capacity and breadth across glass vials and related containment formats used in regulated pharmaceuticals. For India-focused exporters and biologics programs, the combination strengthens access to high-spec primary packaging supply and encourages dual-sourcing strategies across global and local supply chains.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenue earned from packaging products and materials used to pack pharmaceutical products in India, across primary, secondary, and tertiary packaging formats.

Scope exclusions: It excludes the value of the packaged drug itself and also excludes packaging machinery and plant-level services that are not part of packaging product sales.

Segmentation Overview

- By Material Type

- Plastic

- High-Density Polyethylene (HDPE)

- Low-Density Polyethylene (LDPE)

- Polyethylene Terephthalate (PET)

- Other Plastics

- Glass

- Metal

- Paper and Paperboard

- Composites/ Bio-based Materials

- Plastic

- By Product Type

- Bottles

- Vials and Ampoules

- Blister Packs

- Prefilled Syringes and Cartridges

- Tubes

- Caps and Closures

- Pouches and Bags

- Labels

- Other Product Types

- By Packaging Level

- Primary

- Secondary

- Tertiary

- By End-user Industry

- Pharmaceutical Manufacturing Companies

- Contract Packaging Organizations

- Retail and Institutional Pharmacies

- Hospitals and Clinics

- Other End-user Industries

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the fact base and make sure our market model starts from realistic demand and supply signals. We referred to public sources such as Ministry of Commerce and Industry trade statistics, Central Drugs Standard Control Organization (CDSCO) updates, National Pharmaceutical Pricing Authority (NPPA) notifications, and the Reserve Bank of India (RBI) for macro indicators and currency context.

Alongside this, we reviewed annual reports, investor presentations, and regulatory filings of listed packaging and pharma-related companies to understand product mix and revenue exposure to pharma packaging. We also used patent databases to pick up direction of change in materials, closures, and barrier requirements, and we complemented this with shipment-level import and export databases where relevant for pack material flows. The desk sources cited here are illustrative only, and additional public and paid references were used for data collection, clarification, and cross-checking.

Primary Interviews and Surveys

Primary work was done through expert interviews and structured surveys with packaging converters, component suppliers, pharma manufacturers, and contract packaging participants, so gaps from public data could be narrowed. We also tested assumptions on pack type adoption, material shifts, and pricing behavior across major manufacturing corridors, and then the feedback was used to align the model with what buyers and suppliers are seeing on the ground.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 15% | |

| Mid tier: 42% | Functional/Unit leaders: 41% | |

| Smaller Players: 20% | Managers: 44% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up approach, where the top-down layer reconstructs the demand pool from pharma output and trade indicators, and then it is translated into packaging spend by format and material. To keep the numbers practical, we track inputs such as domestic pharma production and export momentum, dosage form mix shifts (solid versus liquid and injectables), blister and bottle penetration, share of cold-chain sensitive packs, and observed price movement in plastics and glass packaging components.

After that, the totals were corroborated using selective bottom-up approximations, such as sampled supplier revenue splits to pharma packaging, channel checks on volumes, and ASP times volume sanity checks for high-use formats like blister packs, bottles, and vials. When bottom-up visibility was incomplete, the gaps were handled using conservative penetration and price bands that were validated through interviews, before final totals were adjusted.

For forecasting, we relied on scenario analysis supported by short-run trend smoothing for the key drivers, since demand and pricing can move quickly with export orders and material costs. The forward view was then tightened by what experts expect on material substitution, sustainability-driven redesign, and compliance-led shifts in pack formats.

Data Validation & Update Cycle

Validation was done through multiple checks so that one data stream did not dominate the final number. Model outputs were compared with independent signals like trade flows for relevant packaging inputs, pharma manufacturing momentum, and observed pricing trends, and then large variances were reviewed and corrected if the assumptions did not hold.

Before sign-off, the work goes through step-by-step analyst review, where calculations, unit logic, and year-on-year movements are rechecked for anomalies. When a new policy update, major capacity change, or unusual raw material swing is detected, the team re-contacts sources to confirm what changed and how it should be reflected. Reports are refreshed annually, and material events trigger interim updates, followed by a final pre-delivery pass to ensure clients receive the latest view.

Mordor Intelligence's India Pharmaceutical Packaging Market Sizing Compared With Other Published Estimates

Published market sizes for India pharmaceutical packaging can differ even when the topic sounds identical, because firms pick different packaging levels, product inclusions, and pricing assumptions. Timing also matters, since a study anchored to a different base year or conversion rate can shift the reported USD value.

The main gap comes from how tertiary packaging and adjacent packaging services are counted, where Mordor Intelligence treats the market as revenue from packaging products sold into pharma use (primary, secondary, and tertiary) and keeps machinery and non-product service value outside the total, which changes the comparable size versus sources that blend wider packaging spend.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.14 B (2025) | |

| Industry Publisher A | USD 2.02 B (2025) | Uses a narrower spend pool in practice, which can occur when parts of secondary and tertiary packaging value are treated inconsistently, and when pricing is averaged across fewer pack formats. |

| Packaging Insights Desk B | USD 4.79 B (2024) | Anchors the market to a different base year and a longer projection window, and the scope language is broader, which can bring in mixed application buckets and faster assumed price progression. |

Looking at the spread, the biggest differences come from what is counted as packaging value and how base year and pricing are set. Our approach stays traceable, since each total is tied back to visible demand indicators, validated pack-type assumptions, and repeatable checks on pricing and format mix.

Key Questions Answered in the Report

What value will pharmaceutical packaging in India reach by 2031?

It is projected to touch USD 8.18 billion by 2031, rising from USD 5.14 billion in 2025 and USD 5.55 billion in 2026.

Which packaging level contributes the most revenue in India?

Primary formats account for 59.60% of 2025 revenue thanks to direct drug-contact requirements and serialisation rules.

Why are contract packaging organizations gaining share?

Pharmaceutical firms are outsourcing to specialized CPOs that offer compliance expertise and flexible capacity, leading to a 9.55% CAGR for the segment.

How are sustainability mandates influencing material choices?

Extended Producer Responsibility rules require 30% recycled content now and 60% by 2027-28, spurring adoption of PCR rigid bottles and recycled PET films.

Which Indian state is the primary hub for pharmaceutical packaging?

Gujarat hosts roughly one-third of national drug output and anchors a dense cluster of packaging suppliers, aided by deep-sea ports and policy incentives.

Page last updated on: