Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.79 Billion |

| Market Size (2026) | USD 3.94 Billion |

| Market Size (2031) | USD 4.75 Billion |

| Growth Rate (2026 - 2031) | 3.85% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Japan Cosmetic Products Market Analysis by Mordor Intelligence

The Japanese cosmetic products market size was valued at USD 3.79 billion in 2025 and estimated to grow from USD 3.94 billion in 2026 to reach USD 4.75 billion by 2031, at a CAGR of 3.85% during the forecast period (2026-2031). In the Japanese cosmetic products market, a subtle headline expansion hints at a shift toward efficacy-driven, quasi-drug formulations. This shift, coupled with a trend of trading up to premium products and the use of sustainable biotech actives, is redefining the competitive landscape. Functional medicated cosmetics now make up about 40% of domestic shipments. Premium lines are outpacing their mass-market counterparts, buoyed by a 3% nominal wage increase and strong household purchasing power. E-commerce is booming, with Shiseido aiming to triple its online presence and Cosme boasting 16.6 million monthly users. This surge is expanding digital platforms for both established brands and emerging indie players. Meanwhile, Korean imports, which represent 39.3% of lip-product inflows, are influencing preferences in color cosmetics. This trend highlights how global retail dynamics are reshaping brand hierarchies in Japan's cosmetic market.

Key Report Takeaways

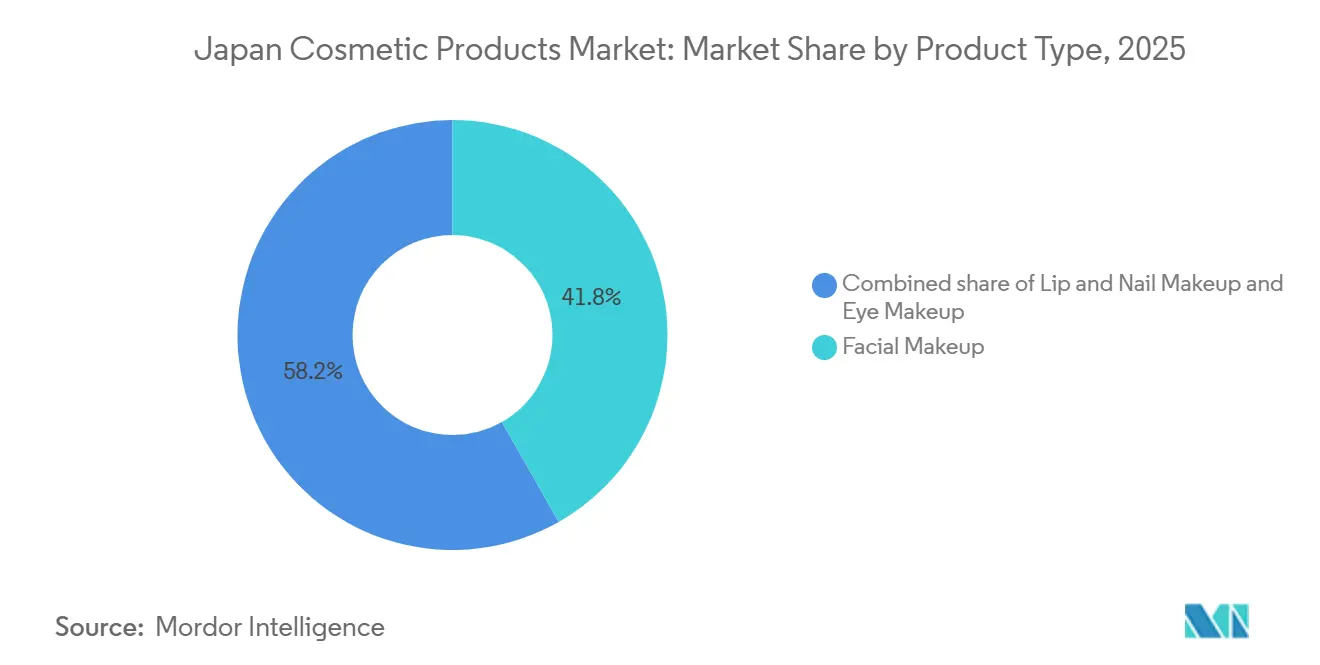

- By product type, facial make-up dominated with a 41.78% Japan cosmetic products market share in 2025, while lip make-up is forecast to expand at a 4.31% CAGR through 2031.

- By nature, conventional formulations held a 73.58% share in 2025; organic and natural alternatives are set to grow at a 4.12% CAGR.

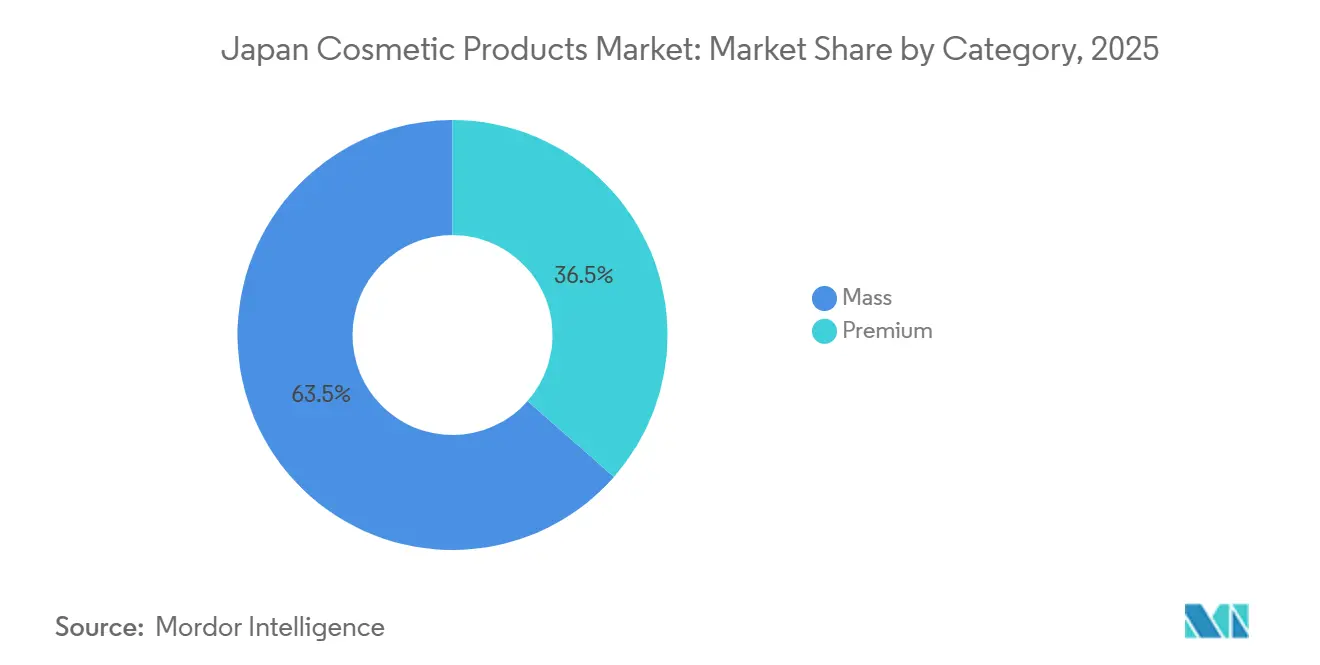

- By category, premium offerings captured a 36.48% share in 2025 and are projected to advance at a 5.72% CAGR.

- By distribution channel, health and beauty stores commanded a 46.35% share in 2025, yet online retail will record the fastest growth at a 4.48% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Cosmetic Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population drives anti-aging and dermocosmetics | 0.8% | National, concentrated in urban prefectures (Tokyo, Osaka, Aichi) | Long term (≥ 4 years) |

| Male grooming acceptance boosts color cosmetics for men | 0.5% | National, with early gains in metropolitan areas | Medium term (2-4 years) |

| Premiumization underpinned by high disposable income | 0.9% | National, strongest in Tokyo, Kanagawa, and duty-free hubs | Short term (≤ 2 years) |

| Clean-label dermatological actives from biotech fermentation | 0.4% | National, led by research and development clusters in Kanto and Kansai | Medium term (2-4 years) |

| Solid/water-free formats gain traction for sustainability | 0.3% | National, early adoption in eco-conscious urban segments | Medium term (2-4 years) |

| Cross-border e-commerce inflow of niche foreign brands | 0.6% | National, amplified by digital platforms and duty-free channels | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging population drives anti-aging and dermo cosmetics

Japan’s aging population plays a significant role in driving this trend, as the World Bank reported in 2024 that 30% of the country’s population is aged 65 or older[2]Source: World Bank, "Population ages 65 and above (% of total population) - Japan", worldbank.org. As a result, there's been a noticeable shift in demand towards solutions addressing wrinkles, pigmentation, and skin elasticity. These are now being formulated as quasi-drugs, allowing them to legally assert their efficacy. Notably, these medicated variants already account for 40% of Japan's domestic cosmetic shipments. With a life expectancy of 84.9 years, product-use cycles are extended. This suggests that growth in the market is more reliant on increased per-capita spending than on volume expansion. Ingredient innovation is taking center stage, with exosomes and iPS-derived actives making waves at Cosme Tokyo 2024, highlighting the intersection of biomedical advancements and Japan's cosmetic market. While the aging population drives a surge in premium spending, formulators face a challenge: securing quasi-drug approval. This six-month review process can slow down their speed to market.

Male grooming acceptance boosts color cosmetics for men

In recent years, male grooming sales in Japan have grown significantly, showing a strong upward trend. This growth is driven by social media's increasing promotion of products like tinted moisturizers and brow definers for men, which are becoming more normalized in male grooming routines. Mandom leads the market, holding a dominant position in men's hair-styling and men's cosmetics, supported by its extensive product portfolio and strong brand recognition. Meanwhile, Shiseido's men's line has seen a remarkable surge in sales during the current fiscal year, reflecting the growing acceptance of male-specific cosmetic products. Thanks to the absence of gender-specific hurdles in MHLW regulations, brands are efficiently repurposing existing quasi-drug dossiers for male SKUs, significantly shortening development cycles and reducing time-to-market. Yet, penetration of male cosmetics lags behind their female counterparts, indicating untapped potential and a substantial growth opportunity in Japan's cosmetic products market as consumer preferences continue to evolve.

Premiumization underpinned by high disposable income

In 2023, Japanese households reported a significant increase in monthly disposable income, reflecting improved economic conditions and wage growth. Full-time wages experienced a notable rise, driven by a stronger labor market, while part-time earnings also showed considerable growth, supported by increased demand for flexible work arrangements. Despite modest CPI inflation, consumers demonstrated a preference for premium cosmetics, particularly lipsticks and serums, indicating a shift towards higher-quality products. This consumer behavior has propelled the premium cosmetics sector to a strong growth trajectory, highlighting the resilience of the market even amidst economic fluctuations. Duty-free boutiques at Haneda and Narita airports, along with the Cosme flagship in Tokyo’s Ginza district, have emerged as key growth nodes. These locations capitalize on the “lipstick effect” psychology, where consumers indulge in affordable luxuries during uncertain times, translating into heightened basket values. However, Shiseido’s projected net loss for FY 2024 serves as a stark reminder of the volatility premium portfolios can encounter, whether due to inventory write-downs, external shocks, or shifts in consumer preferences.

Clean-label dermatological actives from biotech fermentation

Biotech fermentation is gaining ground over petrochemical extraction, thanks to its traceability and eco-friendly credentials. Kao's launch of gallic acid in January 2024, alongside Shiseido's USD 7 million microalgae collaboration with CHITOSE in May 2025, highlights a significant shift in research and development budgets towards lab-grown, nature-identical molecules. These advancements reflect the industry's growing focus on sustainable and innovative solutions to meet consumer demands. While ISO 16128 guidelines remain voluntary, they provide marketers in Japan's cosmetic products market a numeric benchmark for "natural origin," shaping label claims and enhancing transparency. Furthermore, ensuring supply certainty and controlling allergens not only addresses past issues, like the Rhododenol-induced leukoderma crisis, but also bolsters consumer trust in biotech actives, paving the way for broader adoption of these technologies in the cosmetics sector.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shrinking working-age population limits volume growth | -0.5% | National, acute in rural prefectures (Akita, Shimane, Kochi) | Long term (≥ 4 years) |

| Stringent functional-claim approval delays time-to-market | -0.3% | National, governed by PMDA/MHLW frameworks | Medium term (2-4 years) |

| Consumer allergy concerns raise preservative scrutiny | -0.2% | National, heightened in urban centers with high awareness | Short term (≤ 2 years) |

| Highly saturated retail shelf space restricts new listings | -0.4% | National, most intense in Tokyo, Osaka, Nagoya metropolitan areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shrinking working-age population limits volume growth

In 2023, Japan's working-age population (ages 15-64) made up 59.5% of the total demographic, but projections indicate a drop to 51.4% by 2050, according to the Statistics Bureau of Japan. This shift, highlighted by the Statistics Bureau of Japan, is largely due to the exit of the baby-boom cohort from the labor force, resulting in millions fewer in absolute numbers. The United Nations has also chimed in, predicting a 14% contraction in Japan's population from 2024 to 2054. This demographic shift is set to shrink the core consumer base for daily-use cosmetics. While spending per capita on premium and anti-aging products might see an uptick, the overall volume sales are grappling with structural challenges. The Bank of Japan, observing the trends in 2023-2024, pointed out a dip in cosmetics production within the chemicals sector, linking it to a lackluster domestic demand. In response, companies are pivoting towards high-margin, low-volume SKUs and are broadening their export horizons, targeting Southeast Asia and China, where the working-age demographic is more robust. However, this demographic crunch isn't just affecting sales; it's also tightening the labor supply in retail and manufacturing sectors, leading to increased wage costs and slimmer operating margins.

Stringent functional-claim approval delays time-to-market

Under the Ministry of Health, Labour and Welfare (MHLW), the Pharmaceuticals and Medical Devices Agency (PMDA) mandates pre-approval for quasi-drug formulations touting benefits like whitening or anti-acne effects. Dossier reviews can stretch up to six months, causing product launch delays. This window allows quicker competitors from Korea and China to seize shelf space with similar offerings, marketed as conventional cosmetics, according to Maven Regulatory Consultancy. While amendments to the Pharmaceutical and Medical Device Act (PMD Act) are slated for early 2025, aiming to introduce conditional approvals and ease access, the timeline for these changes remains ambiguous, as noted by MHLW. This regulatory maze poses challenges, especially for smaller brands without dedicated regulatory teams, further entrenching the market dominance of established players like Shiseido, Kao, and Kosé. Past safety incidents, such as the Glupearl wheat-allergy outbreak affecting 2,111 individuals and the Rhododenol leukoderma crisis with 19,609 cases, have made regulators more cautious, emphasizing consumer safety over rapid market entry, highlighted by the Japanese Cosmetic Science Society.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Lip Makeup Outpaces Facial Dominance

In 2025, facial makeup dominated Japan's cosmetic products market, seizing a 41.78% share. This leadership stems from the rising allure of base products, promising flawless and poreless finishes. Highlighting a trend towards functional infusion, Shiseido unveiled its Foundation Serum in May 2024, merging skincare benefits with cosmetic coverage. The increasing consumer preference for multi-functional products that combine beauty and skincare benefits has significantly contributed to the growth of this segment. Meanwhile, eye makeup is adopting "skinification," integrating peptides and hyaluronic acid for enhanced skin health. This approach aligns with the broader consumer demand for products that not only enhance appearance but also provide long-term skin benefits. In response to dermatitis concerns, nail products are shifting towards safer formulations, reflecting a growing emphasis on product safety and consumer well-being.

On the other hand, the lip sub-segment is emerging as the fastest-growing category in color cosmetics, boasting a projected CAGR of 4.31% through 2031. This surge is driven by a preference for glossy "mucosal" lip aesthetics and the competitive pricing of Korean brands, which resonate with younger consumers. The affordability and trend-driven appeal of these products have made them particularly popular among Gen Z and millennial demographics. Even in the face of economic challenges, this robust demand underscores a desire for affordable self-expression, cementing the lip segment's status as a pivotal growth area in Japan's color cosmetics landscape. The segment's growth also highlights the importance of innovation and accessibility in capturing consumer interest in a competitive market.

By Nature: Conventional Leads, Organic Gains Momentum

In 2025, conventional cosmetic products commanded a dominant 73.58% value share of Japan's cosmetic market, thanks to their affordability and extended shelf life. This segment is primarily driven by skin-care and hair-care formulations leveraging biotech “nature-identical” actives for enhanced stability and scalability, which allow manufacturers to meet consumer demands for effective and reliable products. As of March 31, 2023, the Japan Cosmetic Industry Association (JCIA) reported 4,243 marketing license holders and 4,222 manufacturing license holders in the cosmetics industry, showcasing a strong infrastructure for product development and supply.While ISO 16128 provides a voluntary framework for organic claims, the absence of mandatory certification heightens the risk of greenwashing. This lack of regulation has led to growing consumer skepticism, prompting many to favor brands with transparent supply chains and verified sustainability practices.

Yet, the organic and natural segment is on a steady rise, boasting a CAGR of 4.12%, largely driven by eco-conscious millennials and Gen Z. This growth in Japan's organic and natural cosmetics market underscores a burgeoning demand for sustainable and health-oriented beauty products. Social media platforms have amplified awareness of eco-friendly lifestyles, influencing purchasing decisions and encouraging consumers to seek products aligned with their values. Within this niche, natural and organic skin-care not only dominates but is also set for significant growth, as consumers increasingly prioritize clean ingredients and environmentally responsible production methods. Even as the organic segment flourishes, conventional products anchor the market, leveraging their cost-effectiveness and longevity to maintain a central role in Japan's cosmetic scene.

By Category: Premium Surges Amid Mass Maturity

In 2025, mass brands dominated Japan's cosmetics market, capturing 63.52% of retail value. Their widespread presence spans 23,041 drugstores nationwide. These brands, known for their affordability and extended shelf life, cater to a broad consumer base, even amidst modest inflation. Highlighting the competitive stakes, Shiseido's FY 2024 restructuring, with its SKU rationalization and emphasis on eight core brands, aims to rebound from a significant billion-dollar net loss. This solidified stance ensures mass products remain central to the market, even as dynamics evolve.

Meanwhile, the premium segment is set for the fastest growth at a 5.72% CAGR. This trend underscores a continued appetite for aspirational spending, even in inflationary climates. Duty-free outlets, especially at major hubs like Narita Airport, steer global travelers towards prestige counters, bolstering the allure of premium products. Shiseido's focus on SKU optimization and brand consolidation underscores its drive to enhance profitability after recent losses. Simultaneously, Kosé is banking on its high-end brands, Decorté and Albion, to counterbalance declines in the mass segment and fuel its revenue goals. With such momentum, the premium tier emerges as the primary growth driver in Japan's cosmetics arena.

By Distribution Channel: Health Stores Dominate, Online Accelerates

In 2025, health and beauty stores in Japan command a significant 46.35% share of the cosmetics distribution turnover. Their widespread presence and convenience make them primary gatekeepers for mass-market purchases. In 2023, major chains like Welcia, Tsuruha, and Matsukiyo added over 300 outlets, intensifying competition and crowding shelf space in an already saturated market. While supermarkets and convenience stores showcase mass brands, they struggle when shoppers seek personalized counseling or a wider assortment. Despite facing diminishing returns from over-expansion, drugstores continue to play a pivotal role in everyday beauty access. As saturation challenges mount, chains are pivoting towards efficiency to maintain their leadership position.

Online channels are poised for the fastest growth, projected at a 4.48% CAGR through 2031. Data-rich platforms, such as cosme and various brand sites, are driving personalized gains. E-commerce giants like Rakuten and Amazon are enhancing user experience with features like virtual try-ons and same-day delivery, catering to a tech-savvy audience. Omnichannel strategies are gaining traction, with Kao’s Raku-raku Switch highlighting the importance of logistics in bridging in-store and e-commerce fulfillment. While convenience stores and supermarkets facilitate impulse purchases, they fall short in depth, underscoring the online channel's advantage in capturing incremental sales. This evolving landscape not only complements traditional retail but also reshapes the broader market dynamics.

Geography Analysis

Japan stands as the sole focus for this market, with no regional breakdowns indicated in the Table of Contents. The domestic market's projected 3.85% CAGR through 2031 underscores Japan's status as a mature, high-income economy grappling with demographic challenges and evolving consumer behaviors. The prefectures of Tokyo, Kanagawa, Osaka, and Aichi, buoyed by higher disposable incomes and a dense retail landscape, dominate purchasing power. Duty-free outlets at Haneda and Narita airports play pivotal roles, catering to both inbound tourists and Japanese shoppers eyeing premium imports. Notably, in 2023, Korean cosmetics seized 39.3% of Japan's lip-product imports, outpacing their French counterparts in total value. Meanwhile, rural prefectures like Akita, Shimane, and Kochi grapple with a pronounced demographic decline, witnessing a faster shrinkage of their working-age populations compared to the national average. This trend compresses local demand, compelling retailers to either consolidate or exit the market.

Shiseido's FY2024 report highlights Japan's significance, accounting for 28.6% of its global sales. The domestic market enjoyed a high-single-digit growth in January 2024, but this momentum waned in Q4, attributed to a more cautious consumer sentiment. In response to raw-material inflation, Shiseido enacted a price hike in April 2024. This strategy was also adopted by rivals Kao and Kosé. However, with real wage growth being modest, the room for further price adjustments appears limited. While inbound tourism, a significant driver before the pandemic, saw a partial rebound in 2024, purchases at duty-free stores by Chinese and Southeast Asian visitors fell short of 2019's peak volumes. For instance, By May 2025, Japan had welcomed 18.14 million visitors, as reported by Japan National Tourism Organization (JNTO), and in 2024, tourists spent a record JPY 8.14 trillion, emphasizing the strong link between retail and travel experiences. Looking ahead, the Japan External Trade Organization (JETRO) anticipates a surge in cross-border e-commerce, noting that Japanese consumers are increasingly procuring niche foreign brands directly from international platforms, sidestepping local distributors.

Product approvals in Japan are overseen by the Ministry of Health, Labour and Welfare (MHLW) and the Pharmaceuticals and Medical Devices Agency (PMDA). Notably, quasi-drug formulations necessitate pre-approval dossiers, with a review period extending up to 6 months. In a bid to expedite this process, amendments to the Pharmaceutical and Medical Device Act (PMD Act) are slated for early 2025, aiming to streamline conditional approvals. However, the timeline for these changes remains ambiguous. Sustainability is also a focal point, with Japan's Plastic Resource Circulation Act, enforced by the Ministry of the Environment (MOE), pushing for design-for-recycling and extended producer responsibility. This drive has birthed innovations like Kao's Raku-raku Switch eco-refill (set to debut in September 2025) and Shiseido's award-winning LiquiForm refillable containers (garnering the WorldStar Award in June 2024). Such mandates are not only reshaping packaging strategies but also offering competitive edges to proactive players.

Competitive Landscape

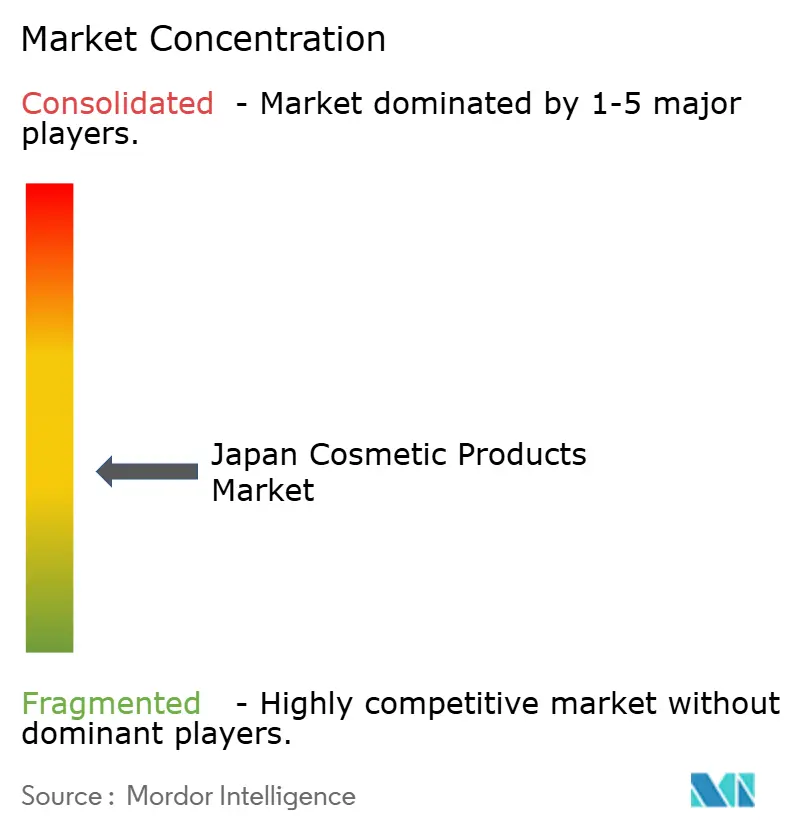

Japan's cosmetic products market is characterized by fragmentation, with the top three firms collectively holding less than a 40% share, resulting in a concentration score of 5. Shiseido, while leading in scale, faced its first loss in four years, amounting to JPY 52.0 billion in FY 2024. In response, the company launched "SHIFT 2025 and Beyond," a strategy aimed at cutting 1,500 jobs and streamlining its product offerings to improve operational efficiency and profitability. Kao's cosmetics division, benefiting from biotech innovations and refillable packaging solutions, reported sales of JPY 244.1 billion. The company has effectively leveraged its group research and development synergies to enhance product quality and sustainability, aligning with evolving consumer preferences.

Kosé is targeting JPY 336 billion in FY 2025, with hopes that its Decorté line will bolster its premium image and drive revenue growth. Meanwhile, niche players are making their mark: Mandom dominates the men's hair styling segment with a 55% share, showcasing its stronghold in a specialized category, and Fancl is pushing its refill infrastructure to achieve 100% 4R compliance by FY 2030, reflecting its commitment to environmental sustainability and innovation in packaging.

Digital platforms are becoming increasingly influential; istyle's @cosme boasts 16.6 million monthly users and 410,000 SKUs, providing it with significant data-driven leverage to negotiate with brands and retailers. Korean brands, leveraging influencer marketing and cost advantages, are making inroads into the Japanese market, as evidenced by Romand's successful 300,000-unit drop at Lawson, which highlighted the growing consumer demand for trendy and affordable products. With challenges like quasi-drug lead times and stringent plastic-waste regulations adding complexity to operations, only those brands that can swiftly innovate, maintain research and development momentum, and adeptly navigate multiple sales channels will thrive in Japan's evolving cosmetic landscape.

Japan Cosmetic Products Industry Leaders

-

L'Oreal S.A.

-

Shiseido Co Ltd

-

Kao Corporation

-

Pols Orbis Holdings Inc

-

Kose Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Kao introduced the Raku-raku Switch pump with eco-refills for its Bioré line, achieving a 50% reduction in plastic use per unit. This initiative received validation from METI and MOE collection schemes.

- June 2025: Kao Corporation broadened the reach of KATE, a leading Japanese makeup brand, aiming to bolster its global footprint, especially in Asia. In collaboration with Universal Studios Japan, KATE is curating distinctive experiences. These initiatives, underscoring individuality and confidence, align with Kao's "Global Sharp Top" cosmetics vision. Backed by substantial investments, the focus remains on immersive brand experiences and deep cultural connections.

- May 2025: Shiseido, through its fibona open innovation program, launched the Sengan Serum. This innovative beauty serum, leveraging Droplet Membrane Emulsification Technology, effortlessly merges with water. This unique feature not only hydrates during cleansing but also purges unwanted impurities, leaving the skin rejuvenated and soft.

- January 2025: SUQQU unveiled two new lipstick shades: 02 Kouboku and 08 Seishuku. The 02 Kouboku shade, a refined rose-pink, exudes mature elegance, while the 08 Seishuku, a subtle reddish-brown, complements both formal and casual attire.

Japan Cosmetic Products Market Report Scope

Cosmetic products are substances or mixtures used on external body parts, to modify appearance without altering body structure or functions.

By Type

| Facial Make-up Products |

| Eye Make-up Products |

| Lip and Nail Make-up Products |

By Nature

| Conventional |

| Organic/Natural |

By Category

| Mass |

| Premium |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Health and Beauty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| By Type | Facial Make-up Products |

| Eye Make-up Products | |

| Lip and Nail Make-up Products | |

| By Nature | Conventional |

| Organic/Natural | |

| By Category | Mass |

| Premium | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Health and Beauty Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

Key Questions Answered in the Report

How large is the Japan cosmetic products market in 2026?

The industry is worth USD 3.94 billion in 2026 and is projected to reach USD 4.75 billion by 2031.

Which product segment is expected to grow fastest through 2031?

Lip make-up leads with a 4.31% forecast CAGR, outpacing facial and eye categories.

What drives premium cosmetics spending in Japan?

Rising disposable incomes, duty-free tourism, and a “lipstick effect” that favors affordable luxury fuel a 5.72% CAGR for premium lines.

How significant are online channels for beauty sales?

Online retail is projected to post a 4.48% CAGR, propelled by platforms such as @cosme and brand-owned e-commerce sites.

Page last updated on: