Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

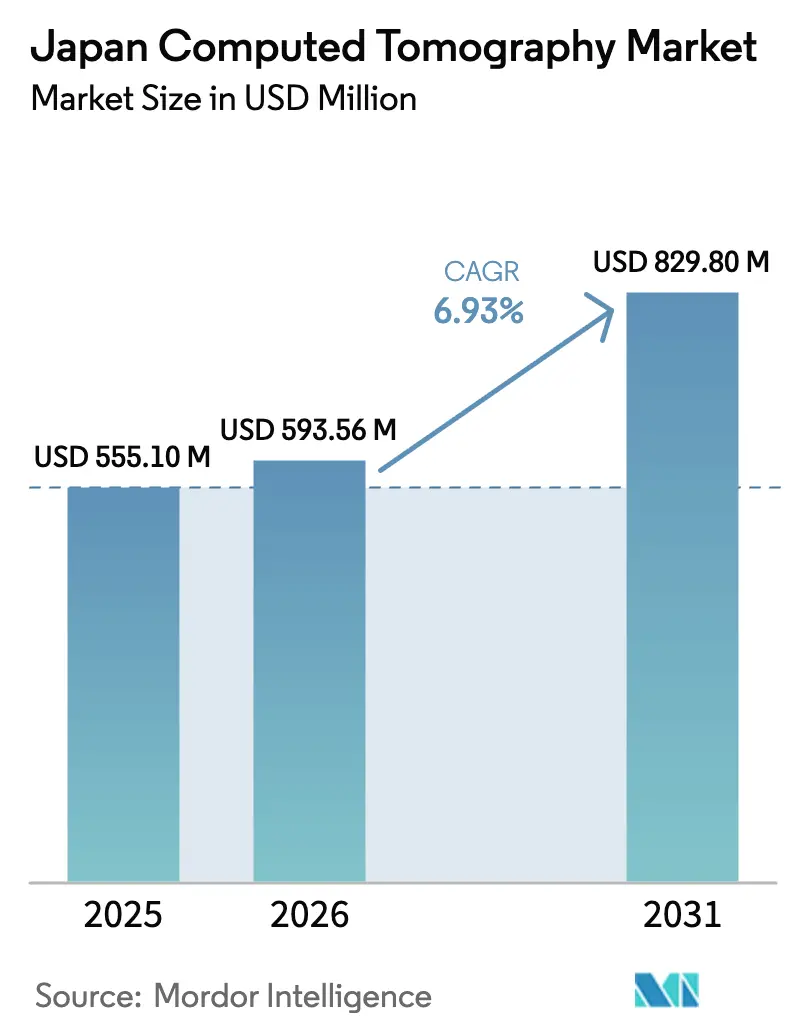

| Base Year Market Size (2025) | USD 555.1 Million |

| Market Size (2026) | USD 593.56 Million |

| Market Size (2031) | USD 829.8 Million |

| Growth Rate (2026 - 2031) | 6.93% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Japan Computed Tomography Market Analysis by Mordor Intelligence

The Japan computed tomography market size in 2026 is estimated at USD 593.56 million, growing from 2025 value of USD 555.1 million with 2031 projections showing USD 829.8 million, growing at 6.93% CAGR over 2026-2031. The expansion is fueled by the country’s super-aged demographic profile, steady oncology screening volumes, and the rollout of photon-counting systems that permit dose-efficient spectral imaging. Vendors capitalize on reimbursement incentives for AI-enabled low-dose protocols and on disaster-preparedness budgets that underwrite mobile fleets. The convergence of these factors shelters pricing power even as scan-fee revisions trend downward. Competitive dynamics remain moderate because four multinational manufacturers control most installed bases, yet white-space opportunities persist in portable architectures and AI retrofit kits that augment legacy scanners without full-system replacement.

Key Report Takeaways

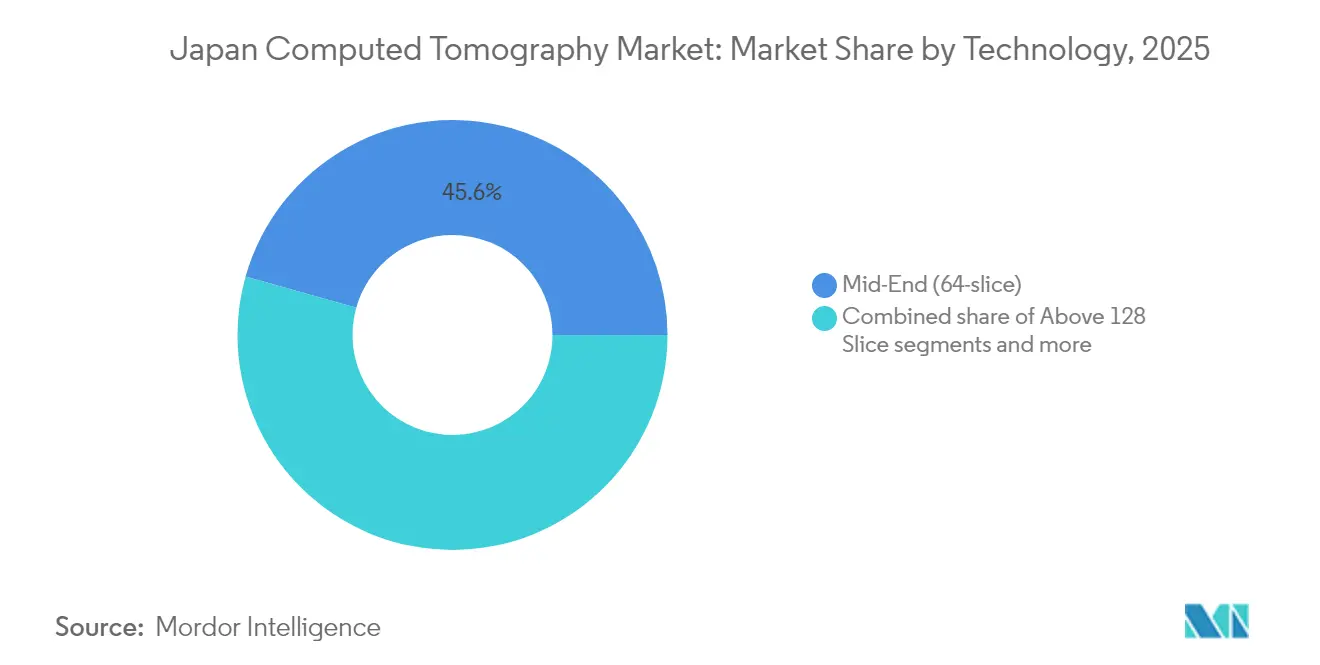

- By technology, Mid-End 64-slice systems accounted for 45.62% of the Japan computed tomography market share in 2025, while Above 128-slice platforms are projected to post a 6.12% CAGR through 2031.

- By product type, Stationary scanners commanded 91.05% revenue in 2025; Portable scanners are forecast to expand at a 6.72% CAGR to 2031.

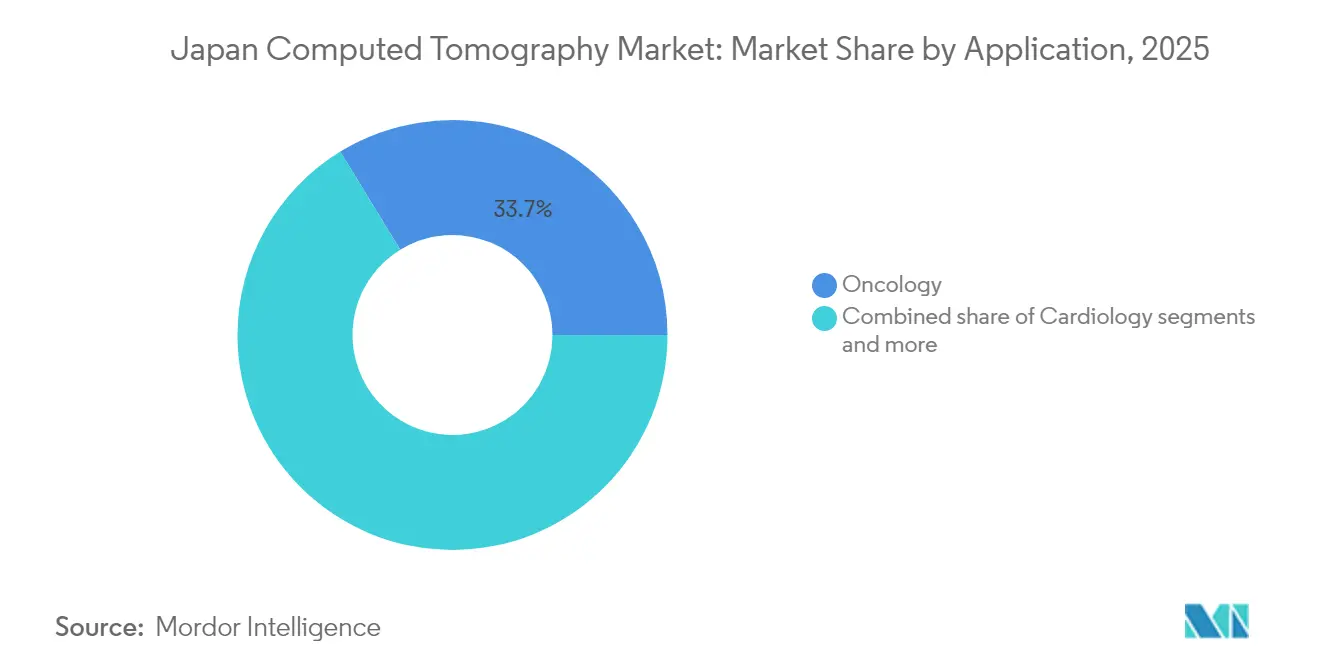

- By application, Oncology held 33.74% of the Japan computed tomography market size in 2025, and Cardiology is tracking the fastest CAGR at 6.53% through 2031.

- By end-user, Hospitals led with a 57.62% share in 2025, whereas Private Hospitals are slated to deliver a 6.15% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Computed Tomography Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of photon-counting CT in academic centers | +1.2% | Japan core, spillover to APAC | Medium term (2-4 years) |

| Ageing population-driven oncologic imaging demand | +2.1% | National, concentrated in metropolitan areas | Long term (≥ 4 years) |

| Disaster-preparedness funding for mobile CT fleets | +0.8% | Japan national, rural prefectures priority | Short term (≤ 2 years) |

| Reimbursement incentives for AI-enabled low-dose protocols | +1.5% | National, early adoption in university hospitals | Medium term (2-4 years) |

| Precision-oncology integration of CT radiomics | +0.9% | Japan core, academic medical centers | Long term (≥ 4 years) |

| OEM–AI start-up retro-fit collaborations lowering upgrade cost | +0.7% | Global, Japan early adopter market | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid adoption of photon-counting CT in academic centers

Academic hospitals validate photon-counting CT by showcasing sub-0.2 mm isotropic resolution and intrinsic spectral outputs that elevate lung-nodule characterization and coronary-plaque analysis. Early adopters such as Osaka University leverage the Siemens NAEOTOM Alpha platform to publish peer-reviewed evidence supporting radiation-dose cuts of 30-40% while sustaining diagnostic confidence. Local R&D partnerships accelerate domestic prototypes using cadmium-zinc-telluride detectors that address national supply-chain resilience priorities. As clinical protocols mature, procurement committees in tertiary hospitals replicate these benchmarks, expanding addressable volumes across the Japan computed tomography market.

Ageing population-driven oncologic imaging demand

Cancer incidence peaks in the seventh and eighth decades, mirroring Japan’s demographic curve. National CT-based lung-cancer screening iterations are entrenched and collectively deliver several hundred-thousand annual examinations that anchor one-third of total scan volume. AI-reconstruction algorithms lower dose per scan, mitigating cumulative exposure anxieties among older patients. Health-economic models demonstrate system-wide savings when early detection defers late-stage chemotherapy costs, ensuring durable policy backing.

Disaster-preparedness funding for mobile CT fleets

Government relief appropriations mandate deployable imaging capacity following seismic events. The latest truck-mounted CT units integrate battery-buffered power and automated leveling, enabling on-site neuro assessments within 20 minutes of arrival. These specifications align with rural-prefecture resilience plans, underpinning the 6.94% CAGR registered by portable scanners.

Reimbursement incentives for AI-enabled low-dose protocols

Once PMDA clears an AI reconstruction algorithm, universal coverage guidelines tag a differentiated scan code that reimburses 3–5% above standard fees, offsetting upgrade costs for institutions adopting certified software. University hospitals spearhead rollout, creating reference centers that disseminate best-practice dose-optimization pathways nationwide.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital outlay amid declining scan fees | -1.8% | National, affecting smaller hospitals disproportionately | Medium term (2-4 years) |

| Shortage of radiologic technologists in rural prefectures | -1.3% | Rural Japan, spillover to suburban areas | Long term (≥ 4 years) |

| Stricter national diagnostic reference levels on dose | -0.6% | National, uniform implementation | Short term (≤ 2 years) |

| Slow PMDA approvals for next-gen detector technologies | -0.9% | Japan specific, affecting global vendors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High capital outlay amid declining scan fees

List prices range from USD 300,000 for 16-slice models to beyond USD 5 million for photon-counting flagships, straining budgets when Social Insurance Medical Council updates have trimmed CT scan tariffs by 2% annually since 2024. Smaller community hospitals therefore favor leasing or pay-per-scan agreements, moderating total equipment revenue growth.

Shortage of radiologic technologists in rural prefectures

Vacancy rates for technologists stand at 18.1%, with the shortfall most acute outside metropolitan areas RSNA.ORG. Unfilled shifts limit scanner utilization below the economic breakeven of 12–15 studies per day, tempering procurement appetites despite clinical need.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Mid-Slice Platforms Anchor Clinical Volume

Mid-End 64-slice scanners retained 45.62% of 2025 revenue because they satisfy bread-and-butter oncology and trauma protocols at manageable ownership costs. The Japan computed tomography market size for this tier is projected to expand at 5.05% through 2031 as iterative reconstruction keeps them dose-competitive. High-slice (>128) installations, while only 18% of unit shipments in 2024, capture the prestige segment and are forecast to add USD 97 million by 2031, reflecting a 6.12% CAGR tied to photon-counting launches. Vendor roadmaps indicate detector-module backward-compatibility that lets facilities upgrade piecemeal, elongating replacement cycles yet boosting software revenue streams.

Clinical consensus increasingly favors spectral capabilities, nudging even mid-slice buyers to consider dual-energy add-ons. Canon’s 1024-matrix reconstruction upgrade delivered 0.4 mm airway visualization on existing 320-row Aquilion installations, blurring performance gaps with high-slice peers. Consequently, manufacturers package AI-based metal-artifact reduction and calcium-scoring automation as subscription layers, reinforcing multi-year annuity models across the Japan computed tomography market.

By Product Type: Stationary Dominance, Portable Momentum

Stationary scanners accounted for 91.05% of units in 2025, underscoring entrenched hospital work-flows and lead-lining requirements. Their throughput advantage bolsters ROI in facilities exceeding 40 patients per day, explaining continued procurement despite space constraints. Portable scanners, though a modest 8.95% slice, are advancing at a 6.72% CAGR on the back of disaster-resilience legislation that subsidizes two mobile units per prefecture. Field hospitals also deploy compact 32-row variants for neuro triage, dovetailing with population-aging policies that emphasize home-and-community care.

Technological cross-pollination lifts both segments. Photon-counting detector miniaturization allows vendors to ship battery-powered units without compromising spectral resolution, broadening clinical eligibility beyond head CT into thoracic and vascular indications. The shift accelerates revenue diversification across the Japan computed tomography market.

By Application: Oncology Leads, Cardiology Accelerates

Oncology generated 33.74% of 2025 revenue after lung-cancer screening volumes rebounded to pre-pandemic levels. Program expansion in Kanagawa and Hokkaido prefectures will amplify scan counts by an estimated 11% over 2025-2027. Cardiology remains the fastest-gaining application, logging a 6.53% CAGR as expanded coronary CT angiography guidelines recommend non-invasive imaging before catheterization in intermediate-risk cohorts. The Japan computed tomography market size for cardiac exams is forecast to reach USD 166.1 million in 2031, up from USD 113.8 million in 2025.

Neurology scans hold steady due to stroke-code adherence, while vascular and musculoskeletal niches see incremental lift from dose-efficient spectral scans that cut contrast volumes by 25%. AI triage software that flags pulmonary embolism and intracranial bleeds keeps radiologist workloads manageable, sustaining demand even amid staffing shortages.

By End-User: Hospital Backbone, Private-Sector Upshift

Hospitals controlled 57.62% of 2025 spending, reflecting their gatekeeper role in universal coverage. Public institutions focus on mid-slice replacements, whereas private hospitals pursue differentiation via photon-counting systems and AI co-pilots, supporting a 6.15% CAGR. Diagnostic imaging centers are expanding in suburbs where aging populations prefer outpatient convenience, translating to tailored service contracts that bundle scanner, PACS, and cloud analytics.

Academic institutes, though <5% of unit volume, punch above their weight in innovation adoption, serving as reference sites that catalyze nationwide rollouts. Veterinary and dental clinics remain niche but profitable add-ons, often buying compact cone-beam units assembled locally.

Geography Analysis

Metropolitan prefectures, Tokyo, Osaka, and Aichi, house 52% of scanners, driven by population density, tertiary centers, and stronger capital budgets. Urban facilities cycle equipment every 6-7 years, sustaining high-slice demand. In contrast, rural prefectures own aging fleets approaching a 10-year median age, prompting government grants for mobile units and AI retrofits rather than outright replacements.

Seismic risk shapes procurement in the Pacific coastal belt, where hospitals embed CT suites with earthquake-resistant mounts and maintain trailer-based backups parked off-site. Post-disaster deployment drills executed in 2024 demonstrated full diagnostic uptime within 48 hours of simulated infrastructure failure, validating policy investments.

Universal coverage guarantees identical scan-fee schedules nationwide, yet income disparities influence out-of-pocket extras such as expedited reporting. Tele-radiology networks connect Hokkaido’s rural clinics to Tokyo reading hubs, compressing turnaround from 48 hours to 6 hours and justifying new scanner acquisitions where local staffing is thin

Competitive Landscape

Four multinationals—Siemens Healthineers, GE HealthCare, Canon Medical Systems, and Philips—command significant 2024 revenue, indicating moderate concentration. Siemens leads in photon-counting patents, GE leverages radiopharmaceutical integration after buying Nihon Medi-Physics for USD 183 million, Canon benefits from domestic supply-chain goodwill, and Philips differentiates with iterative AI recon software.

Strategic cooperation is intensifying. Siemens and Sectra integrated spectral post-processing into mainstream PACS, eliminating workstation silos and speeding physician adoption. Canon and Olympus co-develop ultrasound-CT fusion imaging, signaling convergence plays that broaden modality ecosystems.

Start-ups focus on AI triage and radiation-dose tracking, often signing non-exclusive distribution deals with incumbents. The resulting value-chain interlock fosters service bundling—hardware, software, and isotope supply—creating sticky relationships that raise switching costs across the Japan computed tomography market.

Japan Computed Tomography Industry Leaders

-

GE Healthcare

-

Koninklijke Philips N.V.

-

Canon Medical Systems

-

Siemens Healthineers

-

Fujifilm Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: GE HealthCare completed acquisition of Nihon Medi-Physics for USD 183 million, integrating radiopharmaceuticals with CT workflows.

- April 2023: Canon Inc. announced that Canon and the National Cancer Center Japan (NCC) have begun clinical research employing a next-generation X-ray CT system with photon-counting computed tomography (photon-counting CT, PCCT).

Japan Computed Tomography Market Report Scope

As per the report's scope, computed tomography (CT) is an imaging process that customizes special X-ray equipment to generate a sequence of exhaustive images or scans of areas inside the body. Japan Computed Tomography (CT) Market is Segmented by Type (Low Slice, Medium Slice, and High Slice), Application (Oncology, Neurology, Cardiovascular, Musculoskeletal, and Other Applications), End User (Hospitals, Diagnostic Centers, and Other End-Users). The report offers the value (in USD) for the above segments.

By Technology (Slice Count)

| Low-slice (<64) |

| Mid-slice (64) |

| High-slice (128–256) |

By Product Type

| Stationary CT Scanners |

| Portable / Mobile CT Scanners |

By Application

| Oncology | Lung Cancer Screening |

| Head & Neck Oncology | |

| Colorectal Oncology | |

| Other Oncology | |

| Cardiology | Coronary CT Angiography |

| Calcium Scoring | |

| Structural Heart Disease | |

| Neurology | Stroke Assessment |

| Brain Trauma | |

| Vascular | Peripheral Vascular Disease |

| Pulmonary Angiography | |

| Musculoskeletal | Orthopedic Trauma |

| Sports Injuries | |

| Dental & Maxillofacial | |

| Trauma & Emergency | |

| Other Applications |

By End-User

| Hospitals | Public Hospitals |

| Private Hospitals | |

| Diagnostic Imaging Centers | |

| Dental Clinics | |

| Veterinary Clinics & Hospitals | |

| Academic & Research Institutes |

| By Technology (Slice Count) | Low-slice (<64) | |

| Mid-slice (64) | ||

| High-slice (128–256) | ||

| By Product Type | Stationary CT Scanners | |

| Portable / Mobile CT Scanners | ||

| By Application | Oncology | Lung Cancer Screening |

| Head & Neck Oncology | ||

| Colorectal Oncology | ||

| Other Oncology | ||

| Cardiology | Coronary CT Angiography | |

| Calcium Scoring | ||

| Structural Heart Disease | ||

| Neurology | Stroke Assessment | |

| Brain Trauma | ||

| Vascular | Peripheral Vascular Disease | |

| Pulmonary Angiography | ||

| Musculoskeletal | Orthopedic Trauma | |

| Sports Injuries | ||

| Dental & Maxillofacial | ||

| Trauma & Emergency | ||

| Other Applications | ||

| By End-User | Hospitals | Public Hospitals |

| Private Hospitals | ||

| Diagnostic Imaging Centers | ||

| Dental Clinics | ||

| Veterinary Clinics & Hospitals | ||

| Academic & Research Institutes | ||

Key Questions Answered in the Report

How big is the Japan Computed Tomography Market?

The Japan Computed Tomography Market size is expected to reach USD 593.56 million in 2026 and grow at a CAGR of 6.93% to reach USD 829.8 million by 2031.

What is the current Japan Computed Tomography Market size?

In 2026, the Japan Computed Tomography Market size is expected to reach USD 593.56 million.

Who are the key players in Japan Computed Tomography Market?

GE Healthcare, Koninklijke Philips N.V., Canon Medical Systems, Siemens Healthineers and Fujifilm Holdings Corporation are the major companies operating in the Japan Computed Tomography Market.

What years does this Japan Computed Tomography Market cover, and what was the market size in 2025?

In 2025, the Japan Computed Tomography Market size was estimated at USD 555.1 million. The report covers the Japan Computed Tomography Market historical market size for years: 2019, 2020, 2021, 2022, 2023, 2024 and 2025. The report also forecasts the Japan Computed Tomography Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: