Size and Share of Europe Semiconductor Device Market In Consumer Industry

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

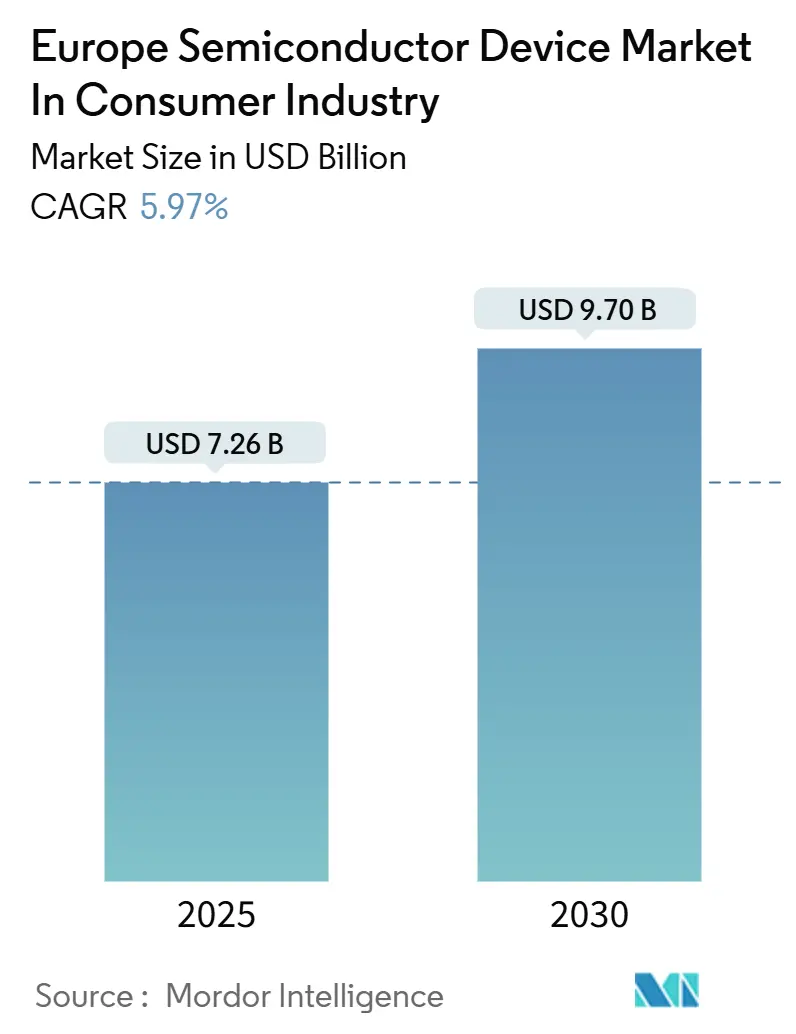

| Base Year Market Size (2025) | USD 7.26 Billion |

| Market Size (2025) | USD 7.26 Billion |

| Market Size (2030) | USD 9.70 Billion |

| Growth Rate (2025 - 2030) | 5.97% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Analysis of Europe Semiconductor Device Market In Consumer Industry by Mordor Intelligence

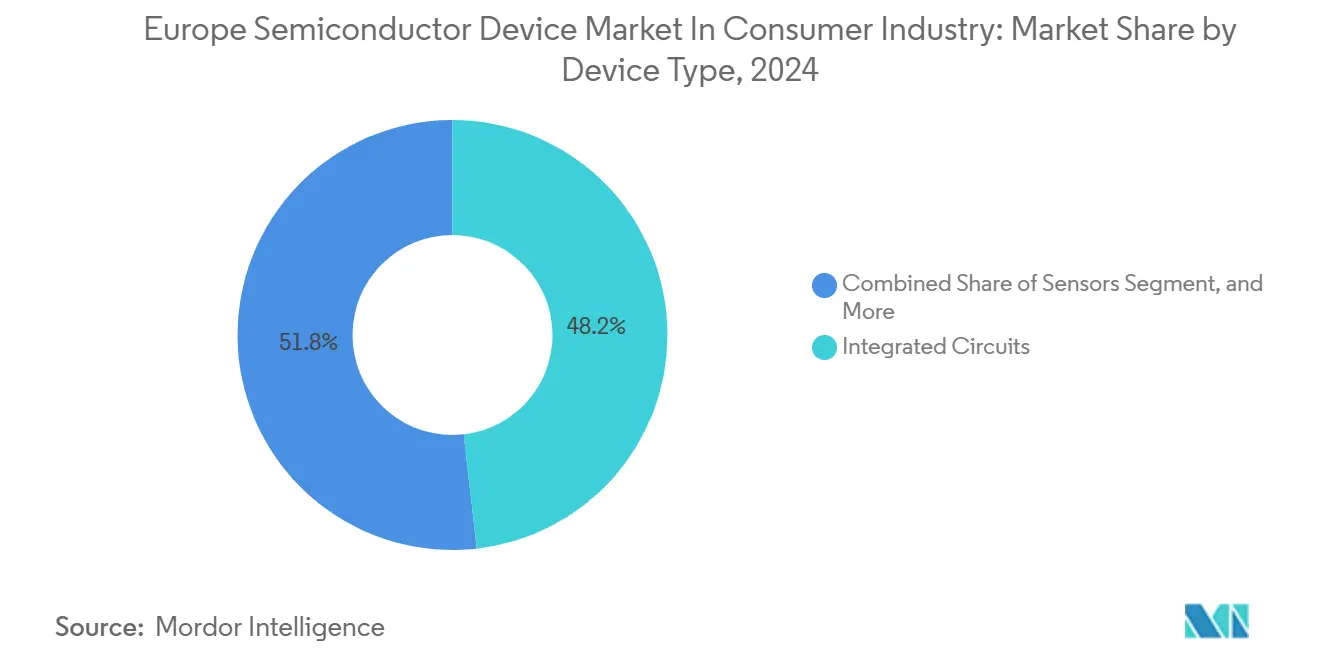

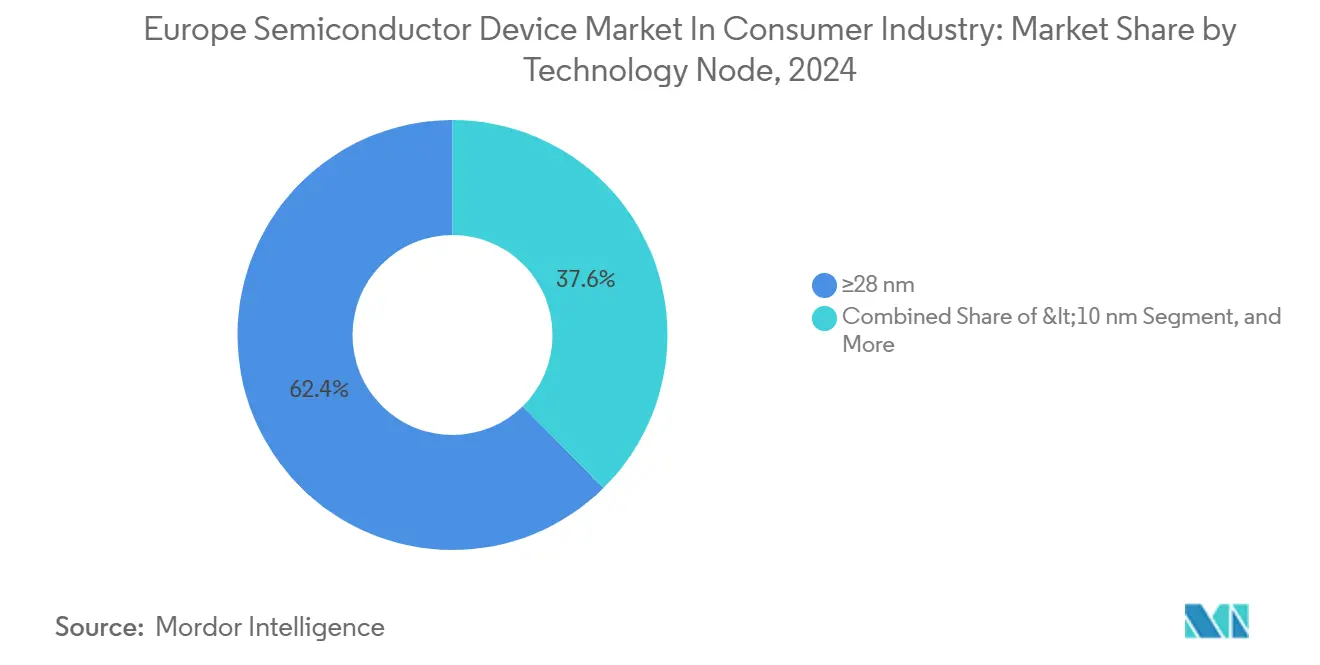

The Europe semiconductor device market size in the consumer segment reached USD 7.26 billion in 2025 and is projected to touch USD 9.70 billion by 2030, translating into a 5.97% CAGR over 2025-2030. Edge-intelligence workloads, energy-constrained architectures and tighter Ecodesign requirements are steering demand toward sensors, ultra-low-power microcontrollers and gallium-nitride power devices. Integrated circuits kept the revenue lead in 2024, yet sensors are outpacing all other categories as wearables, smart-home hubs and environmental monitors proliferate. Smartphones and tablets still dominate application revenue, but wearables are scaling faster helped by Bluetooth Low Energy SoCs that extend battery life to multiday use cases. Germany remains the largest national market on the back of automotive-grade fabs now cross-selling into consumer IoT, while France is the growth front-runner thanks to STMicroelectronics’ EUR 5 billion Crolles build-out. Mature 28 nm-plus nodes hold volume share because of cost-sensitive appliances, whereas sub-10 nm processors for flagship phones and game consoles are the technology node growth engine.

Key Report Takeaways

- By device type, integrated circuits captured 48.20% of 2024 revenue, while sensors are set to expand at a 6.28% CAGR through 2030.

- By application, smartphones and tablets accounted for 35.70% of the 2024 value, whereas wearables led growth at a 7.01% CAGR through 2030.

- By technology node, ≥28 nm processes accounted for 62.40% of 2024 output, yet <10 nm devices are forecast to climb at a 6.38% CAGR.

- By material, silicon supplied 70.10% of the 2024 volume, but gallium nitride is projected to rise at a 6.12% CAGR through 2030.

- By geography, Germany delivered 28.30% of 2024 demand, while France is poised for a 7.42% CAGR over the outlook.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global valuation is built by aggregating outputs from multiple regions, with Europe forming one of the important contributors. Mordor Intelligence's global consumer electronics semiconductor market size report represents that cumulative total.

Insights and Trends of Europe Semiconductor Device Market In Consumer Industry

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Consumer Electronics Products | 1.20% | Europe-wide, strongest in Germany, France, Italy, and Spain | Short term (≤ 2 years) |

| Growing Adoption of Consumer IoT Devices | 1.00% | Europe-wide, with high penetration in Nordic countries, Germany, and the Netherlands | Medium term (2-4 years) |

| Proliferation of 5G-Enabled Smartphones and Wearables | 0.90% | Europe-wide, led by Western European smartphone markets | Short term (≤ 2 years) |

| Accelerated Shift Toward Smart Home Ecosystems | 0.80% | Europe-wide, particularly in Germany, the UK, France, and the Netherlands | Medium term (2-4 years) |

| Emergence of Chiplet-Based Modular Architectures in Low-Power Consumer Devices | 0.60% | Europe, concentrated in advanced semiconductor design and R&D hubs | Long term (≥ 4 years) |

| EU Ecodesign Regulations Driving Demand for Ultra-Low-Standby Power ICs | 0.50% | European Union, driven by EU member states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation Of 5G-Enabled Smartphones And Wearables

European operators had built 5G standalone cores that covered 87% of city populations by mid-2024, prompting rapid refresh of radio-frequency front-end modules in smartphones and smartwatches. Mid-band allocations at 3.4–3.8 GHz favor gallium-nitride power amplifiers and silicon-on-insulator switches that lower cost per watt by 18%. Wearables with sub-300 mAh batteries now rely on envelope-tracking PMICs, extending talk time by 22%. Nordic Semiconductor’s nRF91 secured 14 design wins in 2024, proving that integrated cellular plus Cortex-M33 logic displaces discrete basebands. Cyber-security clauses in the 2025 Radio Equipment Directive mandate secure boot and firmware attestation, which lifts demand for embedded secure elements from NXP and STMicroelectronics.

Accelerated Shift Toward Smart-Home Ecosystems

Matter 1.2 unified Thread, Zigbee and Wi-Fi 6 under one application layer in 2024, letting gateway makers collapse discrete radios into single-die solutions. Silicon Labs and Nordic Semiconductor SoCs captured 60% of Matter-certified launches, trimming bill-of-materials by 12%. Far-field voice-assistant speakers now embed STMicroelectronics MEMS microphones that respect the 0.3 W Ecodesign standby ceiling through duty-cycled wake-word detection. Certified KNX smart-home installations climbed 31% year-on-year, stimulating MCU shipments for lighting and HVAC nodes. Shared 802.15.4 PHY layers let chip vendors reuse RF blocks, spreading design cost over larger volumes and accelerating penetration into mid-tier appliances.

Emergence Of Chiplet-Based Modular Architectures

The Grenoble APEC pilot line displayed 22 nm logic chiplets bonded to 130 nm analog dies on silicon interposers for smart-speaker use cases. Partitioning trimmed average power 34% versus monolithic SoCs by gating high-performance compute most of the time. STMicroelectronics confirmed 18-point gross-margin uplift from chiplet audio processors because partially defective dies can be salvaged and matched with known-good analog tiles. The Universal Chiplet Interconnect Express standard specifies 16 Gbps links at 2 pJ/bit, enabling European fabless firms to source compute dies from Asia while retaining analog and PMIC dies locally. Faster derivative development is pivotal in consumer sectors where product life cycles barely exceed 18 months.

EU Ecodesign Regulations For Ultra-Low-Standby Power ICs

The July 2024 Sustainable Products Regulation enforces sub-0.3 W standby and sub-2 W networked-standby ceilings. Appliance vendors are replacing linear regulators with 92%-efficient synchronous bucks that hold efficiency down to 10 mA load. Dialog’s DA9063 PMIC draws only 8 µA in always-on state, letting smart thermostats stay connected without breaching the Ecodesign limit. German environment-agency testing showed 73% of certified devices now use leakage-suppression techniques such as body biasing and power gating. The phased roll-out through 2027 accelerates adoption of fully depleted SOI at 22 nm, boosting demand for Soitec substrates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Semiconductor Supply Chain Disruptions | -0.6% | Global, acute in advanced packaging and substrate supply to Europe | Short term (≤ 2 years) |

| High Capital Intensity of Advanced Node Fabrication in Europe | -0.8% | France, Germany, Netherlands | Long term (≥ 4 years) |

| Fragmented Consumer OEM Design Cycles Increasing NRE Cost Volatility | -0.4% | Pan-European, affecting fabless and integrated-device manufacturers | Medium term (2-4 years) |

| Stricter EU Chemicals Restriction (PFAS Ban) Complicating Lithography Materials | -0.5% | EU-wide, concentrated in advanced-node fabs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Intensity Of Advanced-Node Fabrication

Building a 5 nm-class fab in Europe now costs beyond EUR 15 billion(USD 17.47 billion), and no local IDM has earmarked that sum exclusively for consumer workloads. Crolles focuses on 18 nm FD-SOI, Dresden on 28-40 nm power devices, leaving phone and tablet processors to Asian foundries.[1]“CoolGaN 600 V Transistors,” Infineon Technologies, infineon.com Chips Act grants prioritize automotive and defense, sidelining commodity consumer ICs. Consequently, European brands depend on Taiwan and Korea for advanced logic, fragmenting supply chains and extending lead times by four to six months. Lack of proximal advanced nodes also hinders co-optimization of design and process for regional fabless firms.

Stricter EU Chemicals Restriction (PFAS Ban)

The January 2025 PFAS restriction under REACH Annex XVII eliminates many legacy photoresists.[2]“REACH Annex XVII PFAS Restrictions,” European Chemicals Agency, echa.europa.eu PFAS-free EUV resists exhibit 12% higher line-edge roughness, resulting in a 6% reduction in wafer throughput. European customers have requested 11-week qualification extensions, which will delay 3-nm tape-outs. One local fabless company experienced a 23% increase in mask-revision cycles in 2024, eroding its NRE budgets. Registration dossiers add EUR 1.8-3.2 million per new chemistry, costs that smaller suppliers struggle to absorb, thus consolidating the materials landscape around large Asian incumbents.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Sensors Capture Wearable And Smart-Home Telemetry Surge

Sensors’ 6.28% CAGR through 2030 outflanks all other device categories even though integrated circuits owned 48.20% of 2024 revenue. The Europe semiconductor device market size for sensors is buoyed by environmental, inertial and biometric arrays that extend edge intelligence into fitness trackers, smart speakers and air-quality monitors. STMicroelectronics’ LSM6DSV16X inertial module executes gesture-recognition on-chip, cutting MCU wake events 47% and adding two days to smartwatch battery life. Bosch Sensortec shipped 180 million MEMS devices in 2024, with barometric and gas sensors underpinning ambient-intelligence use cases. Optoelectronics command share in smartphone OLED drivers, while discrete GaN transistors are replacing silicon MOSFETs in fast-charge adapters due to 30% lower heat dissipation.

Parallel cost-sensitive appliance MCUs remain entrenched at 130 nm, but sensors benefit from tighter integration at 40 nm and 22 nm FD-SOI, where reduced leakage prolongs coin-cell life. The Europe semiconductor device market share for integrated circuits will decline modestly as power-management units, image sensors and logic controllers migrate into multi-chip modules dominated by sensor-driven architectural choices. Suppliers that bundle sensor, connectivity and PMIC reference designs stand to capture bigger platform wins in Matter and KNX deployments.

By Application: Wearables Ascend On Ultra-Low-Power System Integration

Smartphones and tablets owned 35.70% of 2024 revenue, yet wearables are growing at 7.01% CAGR on the back of health telemetry cleared under EU MDR. The Europe semiconductor device market size for wearables will strengthen further as dual-core Bluetooth SoCs such as Nordic’s nRF5340 trim continuous heart-rate monitoring current to sub-5 mA. Smart-home appliances also climb due to Matter standardization and retrofits in Germany’s KNX base, driving demand for multi-protocol microcontrollers. Gaming and AR/VR, a smaller slice, still require high-bandwidth graphics processors whose advanced packaging may soon be performed in TSMC’s Dresden facility, cutting logistics lag.

Wearables’ reliance on ultra-low-leakage FD-SOI processes positions European substrate providers favorably. Meanwhile, smartphones will keep absorbing the largest silicon area per unit, sustaining node migration toward 3 nm and below. Brands that harmonize phone, watch and smart-home processor roadmaps can leverage shared die-to-die interconnects to time-slice R&D spend and improve bill-of-materials across devices.

By Technology Node: Sub-10 nm Nodes Gain As Flagship Processors Anchor Demand

Nodes ≥28 nm contributed 62.40% of 2024 shipments because appliance MCUs and PMICs prioritize cost over density. Yet the Europe semiconductor device market share for <10 nm logic will swell given 6.38% CAGR driven by Qualcomm, Apple and MediaTek flagships now packaging in Poland, Czechia and Hungary. Mid-tier 14-22 nm FD-SOI offers a leakage-optimized path for always-on voice processors that need higher performance than 40 nm but cannot stomach 3 nm mask complexity. TSMC’s upcoming Dresden advanced-packaging plant will catalyze European co-design by shortening tape-out-to-ramp timelines.

Supply-chain duality persists: leading-edge wafers are still fabbed in Asia, but final test and system-in-package assembly are shifting local. Vendors able to co-optimize thermal and RF performance at the package level will differentiate in gaming consoles and high-refresh-rate tablets.

By Material: Gallium Nitride Penetrates Fast-Charging Segments

Silicon remained the workhorse with 70.10% share in 2024, yet gallium-nitride’s 6.12% CAGR will carve a bigger slice in chargers above 60 W. The Europe semiconductor device market size for GaN transistors is underpinned by CoolGaN 600 V devices that achieve 98.5% efficiency in totem-pole PFC topologies. Silicon carbide currently plays a minor role in the consumer market, but it could potentially infiltrate wireless power transmitters operating at 6.78 MHz once coil designs mature. Indium-phosphide photodiodes support AR-glasses proximity sensors as designers push immersion fidelity. EU raw-materials policy now classifies gallium as strategic, spurring Soitec to pilot 15% recycling at its Bernin site by 2027.

Material choice is increasingly application-specific. Mobile chargers transition to GaN due to power-density mandates, while sensors remain on silicon for cost reasons. Vendors offering package-level co-integration of GaN power and silicon controllers can capture OEM roadmaps that aim to collapse external FETs into single-module designs.

Geography Analysis

Germany’s 28.30% 2024 share flows from automotive-qualified fabs repurposing capacity for consumer IoT devices that require the same functional-safety pedigree. Infineon’s Villach and Dresden lines now allocate more wafer starts to smart-speaker MCUs. Bosch Sensortec’s Reutlingen base shipped 180 million MEMS units into European wearables in 2024, underlining Germany’s sensor leadership. Silicon Saxony’s 70-company cluster accelerates chiplet and advanced packaging knowledge transfer, providing regional OEMs with early access to heterogeneous integration techniques.

France will grow at the fastest rate, with a 7.42% CAGR, as STMicroelectronics’ Crolles extension adds 18 nm FD-SOI wafers tailored for imaging sensors and PMICs in phones, watches, and smart-home nodes. The France 2030 plan allocates EUR 2.5 billion (USD 2.91billion) to semiconductor R&D, with Grenoble’s APEC pilot line already demonstrating 34% power savings in chiplet smart-speaker processors. Soitec’s recycled GaN wafer program complements the push for strategic-materials autonomy.

The United Kingdom, Spain, Italy, and the rest of Europe combined held 43.50% of the 2024 value. Arm’s Cambridge design hub anchors MCU IP, while Dialog’s Swindon teams refine power-management ICs for EU Ecodesign compliance. Spain’s compound-semiconductor institutes research III-V photonics for AR-VR optics, and Italy’s Catania Fab scales silicon-carbide discretes that also spill over into high-wattage laptop chargers. Nordic Semiconductors in Oslo dominated BLE design wins, showcasing the Nordics’ impact on connectivity silicon.

Coverage of the consumer electronics semiconductor market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Asia Pacific, alongside detailed country-level intelligence for Japan, each shaped by local operating conditions.

Competitive Landscape

Integrated-device manufacturers leverage vertical stacks: ST’s STM32 ecosystem secured 23 smart-home appliance wins in 2024, bundling Matter stacks that compress platform schedules by months. Fabless specialists Nordic and Dialog (Renesas) capture the wearables market with ultra-low-power SoCs that integrate radios, PMICs, and machine-learning accelerators, reducing board area by 35%.

White-space opens around chiplet-enabled Ecodesign compliance suppliers that partition always-on domain logic, stand to meet sub-0.3 W standby, and win smart-speaker sockets. TSMC’s EUR 4.5 billion (USD 5.24 billion) Dresden packaging plant, scheduled for 2027, will further blur the lines as European brands gain local access to chip-on-wafer capabilities. Disruptors include X-FAB for SiC and Soitec for FD-SOI substrates, both of which provide ultra-low-leakage MCU roadmaps.

ST acquired NFC IP house Panthronics, Infineon partnered with Arm on PMICs for Cortex-M85 hubs, and NXP added BLE to EdgeLock secure elements for wearable payments.[3]“EdgeLock SE051W Brief,” NXP Semiconductors, nxp.com The coming Radio Equipment Directive cyber-rules raise entry barriers for suppliers lacking cryptographic IP.

Leaders of Europe Semiconductor Device Market In Consumer Industry

-

STMicroelectronics N.V.

-

NXP Semiconductors N.V.

-

Dialog Semiconductor Plc (Renesas Electronics Corporation)

-

AMS-OSRAM AG

-

X-FAB Silicon Foundries SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Dialog Semiconductor (Renesas) gained MDR clearance for its DA14706 BLE SoC enabling continuous glucose monitoring wearables.

- November 2024: TSMC committed EUR 4.5 billion (USD 5.24 billion) to Dresden advanced-packaging, operational in 2027.

- October 2024: STMicroelectronics rolled out STM32H7R/S MCUs with integrated graphics for smart-home displays.

- September 2024: Nordic launched nRF54H20 multi-protocol SoC, securing 18 smart-home platform wins.

Scope of Report on Europe Semiconductor Device Market In Consumer Industry

The Europe semiconductor device market in the consumer industry encompasses the production and deployment of semiconductor components such as discrete devices, sensors, optoelectronics, and integrated circuits used in a wide range of consumer electronics. This market supports technologies in smartphones, wearables, smart home appliances, gaming systems, and AR/VR devices, leveraging advanced and emerging process nodes and materials. Overall, it focuses on enabling high performance, energy efficiency, and intelligent functionality across Europe’s consumer electronics ecosystem.

The Europe Semiconductor Device Market in Consumer Industry Report is Segmented by Device Type (Discrete Semiconductors, Optoelectronics, Sensors, Integrated Circuits including Analog, Logic, Memory, and Micro comprising Microprocessor, Microcontroller, Digital Signal Processors), Application (Smartphones and Tablets, Wearables, Smart Home Appliances, Gaming Consoles and AR-VR Devices), Technology Node (≥28 nm, 14-22 nm, <10 nm), Material (Silicon, Silicon Carbide, Gallium Nitride, Other Compound Semiconductors), and Geography (United Kingdom, Germany, France, Spain, Italy, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| Discrete Semiconductors | ||

| Optoelectronics | ||

| Sensors | ||

| Integrated Circuits | Analog | |

| Logic | ||

| Memory | ||

| Micro | Microprocessor | |

| Microcontroller | ||

| Digital Signal Processors | ||

| Smartphones and Tablets |

| Wearables |

| Smart Home Appliances |

| Gaming Consoles and AR-VR Devices |

| ≥28 nm |

| 14-22 nm |

| <10 nm |

| Silicon |

| Silicon Carbide |

| Gallium Nitride |

| Other Compound Semiconductors |

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| Rest of Europe |

| By Device Type | Discrete Semiconductors | ||

| Optoelectronics | |||

| Sensors | |||

| Integrated Circuits | Analog | ||

| Logic | |||

| Memory | |||

| Micro | Microprocessor | ||

| Microcontroller | |||

| Digital Signal Processors | |||

| By Application | Smartphones and Tablets | ||

| Wearables | |||

| Smart Home Appliances | |||

| Gaming Consoles and AR-VR Devices | |||

| By Technology Node | ≥28 nm | ||

| 14-22 nm | |||

| <10 nm | |||

| By Material | Silicon | ||

| Silicon Carbide | |||

| Gallium Nitride | |||

| Other Compound Semiconductors | |||

| By Country | United Kingdom | ||

| Germany | |||

| France | |||

| Spain | |||

| Italy | |||

| Rest of Europe | |||

Key Questions Answered in the Report

What is the current value of the Europe semiconductor device market in consumer electronics?

The market was valued at USD 7.26 billion in 2025 and is forecast to reach USD 9.70 billion by 2030.

Which device category is growing fastest in European consumer applications?

Sensors lead growth with a 6.28% CAGR, fueled by wearables and smart-home telemetry.

Why is France the fastest-growing national market?

STMicroelectronics Crolles expansion, France 2030 subsidies and chiplet pilot lines in Grenoble are accelerating domestic output.

How will EU Ecodesign rules affect semiconductor demand?

They mandate sub-0.3 W standby, driving adoption of ultra-low-leakage microcontrollers and efficient PMICs.

What role will gallium nitride play in European chargers?

GaN transistors enable >98% efficiency and higher power density, expanding at a 6.12% CAGR through 2030.

How concentrated is supplier power in the region?

The top five vendors hold 42% revenue share, indicating moderate concentration with room for emerging specialists.

Page last updated on: