Italy Fixed Wireless Access (FWA) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

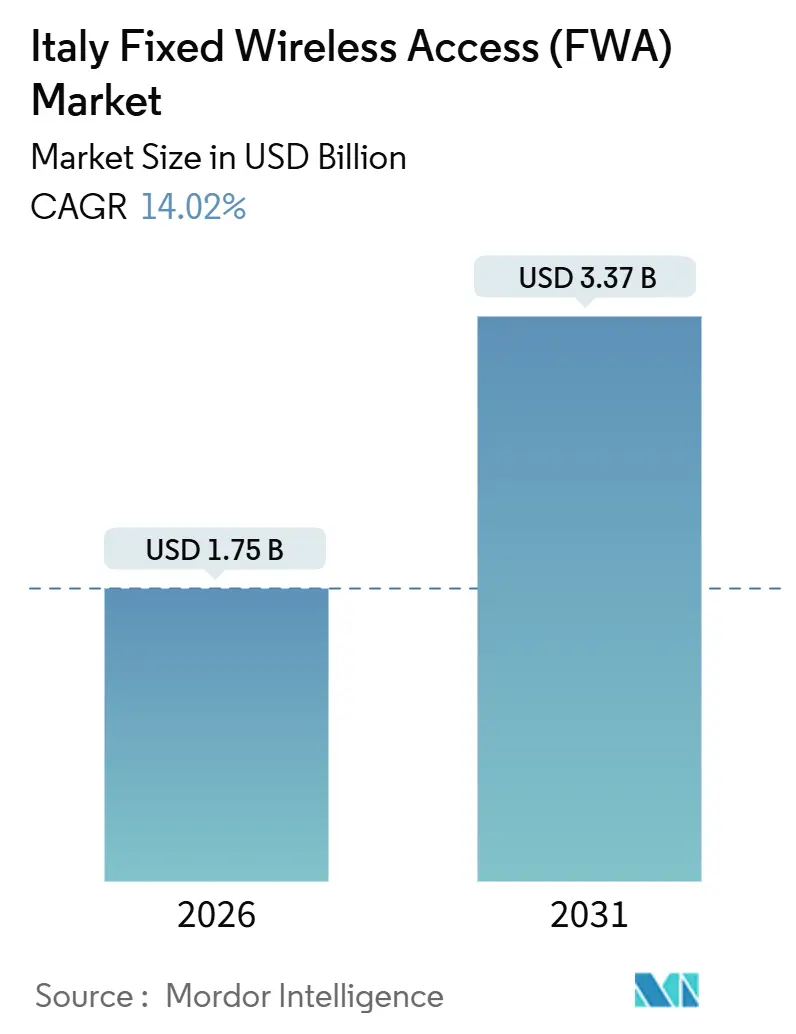

| Market Size (2026) | USD 1.75 Billion |

| Market Size (2031) | USD 3.37 Billion |

| Growth Rate (2026 - 2031) | 14.02% CAGR |

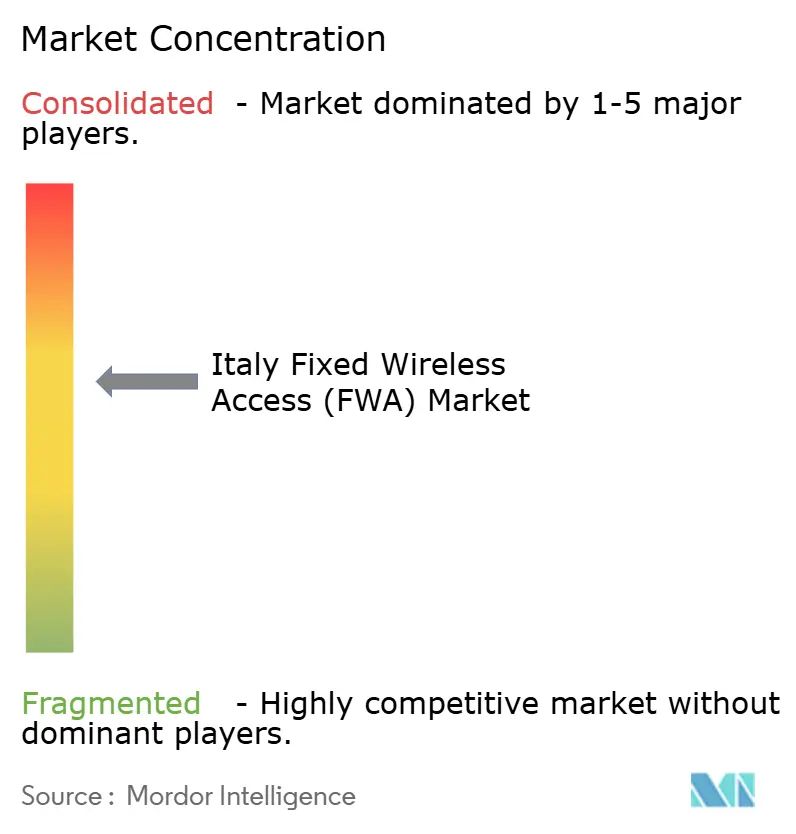

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Fixed Wireless Access (FWA) Market Analysis by Mordor Intelligence

The Italy fixed wireless access market size reached USD 1.75 billion in 2026, and it is projected to climb to USD 3.37 billion by 2031, reflecting a robust 14.02% CAGR. Rapid 5G site densification, continued delays in fiber trenching, and spectrum-sharing incentives have combined to make fixed wireless a mainstream broadband option across urban, suburban, and rural zones. Operators are capitalizing by bundling home internet with mobile SIMs, reducing churn, and lifting average revenue per user. Hardware still accounts for most outlays, though recurring subscription income is expanding faster as managed Wi-Fi, static IP, and security add-ons gain traction. Mid-band 3.6 GHz channels dominate suburban builds, while newly clarified 26 GHz rules unlock dense urban hotspots and lift premium speed tiers, sharpening competition in the Italy fixed wireless access market.

Key Report Takeaways

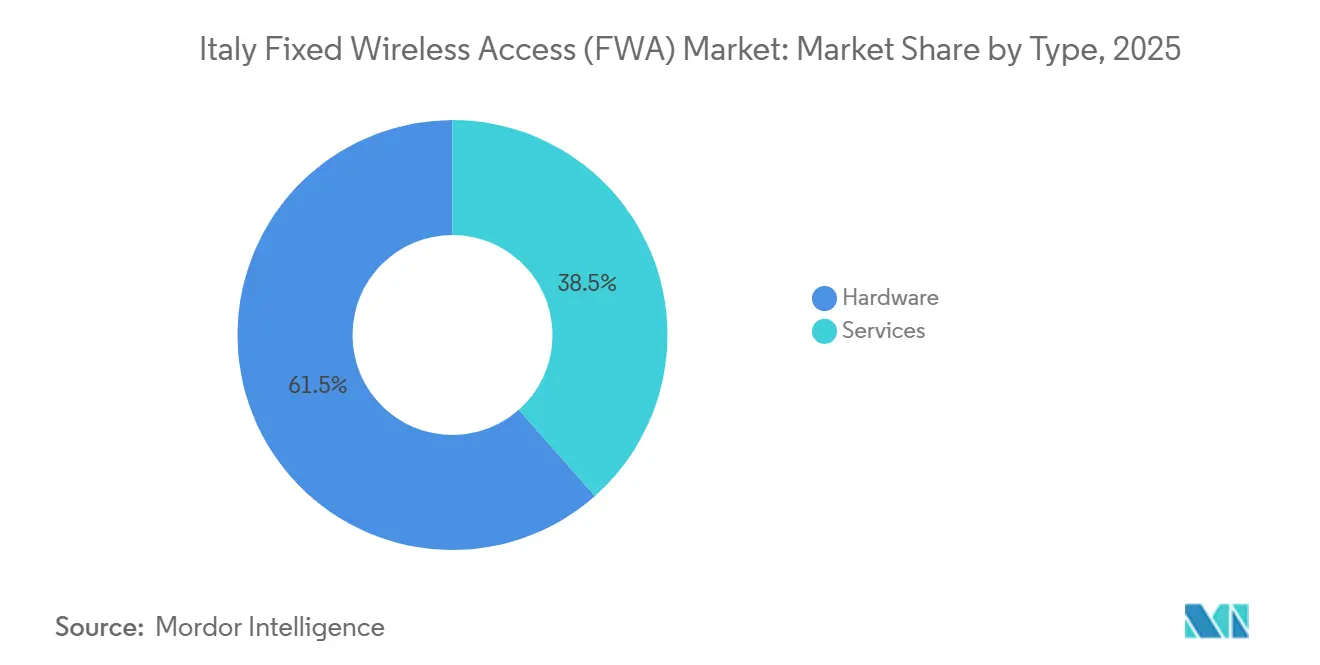

- By type, hardware captured 61.54% of Italy fixed wireless access market share in 2025, while services are growing at a 15.62% CAGR through 2031.

- By application, residential connections held 54.64% of the Italy fixed wireless access market size in 2025, whereas commercial usage is advancing at a 15.46% CAGR to 2031.

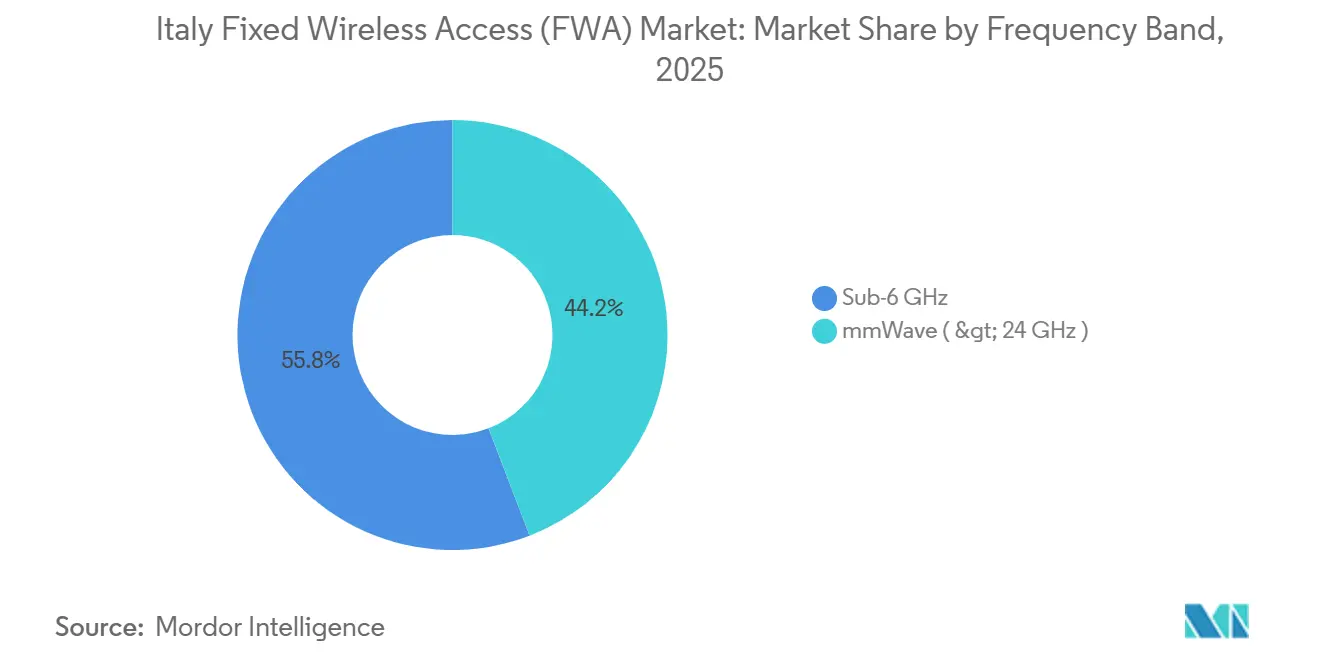

- By frequency band, sub-6 GHz accounted for 55.84% of revenue in 2025, and mmWave is set to expand at a 15.78% CAGR through 2031.

- By deployment mode, indoor CPE represented 60.42% of installations in 2025, while outdoor CPE is rising at a 15.39% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Italy Fixed Wireless Access (FWA) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for High-Speed Data Connectivity | +3.5% | National, with concentration in Lombardy, Lazio, Emilia-Romagna | Medium term (2-4 years) |

| Strategic Collaborations Across 5G Ecosystem | +2.8% | National, particularly in low-density provinces | Medium term (2-4 years) |

| Government Incentives for Rural Broadband in Italy | +2.5% | White and grey areas (Calabria, Basilicata, Molise, Abruzzo) | Long term (≥ 4 years) |

| Expansion of 26 GHz Spectrum for 5G FWA | +2.2% | Urban centers (Milan, Rome, Turin, Naples) and suburban corridors | Short term (≤ 2 years) |

| Rising Smart Home Adoption Driving Bandwidth Needs | +1.8% | National, with higher penetration in northern regions | Medium term (2-4 years) |

| Infrastructure Sharing Agreements Lower Deployment Costs | +1.5% | Low-density municipalities and mountainous areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand For High-Speed Data Connectivity

Average monthly data consumption has surged as households stream 4K video, game online, and run cloud workspaces, widening the gap between user needs and the capacity of legacy copper links. Operators fill that void by positioning the Italy fixed wireless access market as a fiber-like substitute that activates in days instead of months.[1]Ericsson, “Ericsson Mobility Report,” ericsson.com EOLO’s October 2025 1 Gbps tier at EUR 34.90 (USD 39.49) across more than 300 municipalities demonstrates that an attractive price-performance ratio can unlock latent rural and suburban demand. EOLO booked EUR 140 million EBITDA on EUR 245 million revenue in fiscal 2025, highlighting margin parity with fiber when acquisition costs stay modest. Qualcomm’s Snapdragon X75 silicon, integrated in new CPE, aggregates sub-6 GHz and mmWave bands to deliver multi-gigabit service, reinforcing consumer expectations for faster tiers. As video adoption spreads, bandwidth growth sustains high utilization rates across existing radio assets, lifting returns on every deployed site.[2]Qualcomm, “Snapdragon X75 5G Modem-RF System,” qualcomm.com

Strategic Collaborations Across The 5G Ecosystem

Co-tenancy and asset-sharing models are reshaping cost curves. The January 2026 RAN-sharing deal linking TIM, Fastweb, and Vodafone Italia pools towers, radios, and backhaul in sparsely populated municipalities, trimming site economics and speeding 5G reach. Wind Tre and Iliad validated this template earlier via a rural joint venture that already covers over one-quarter of Italian residents. Tower specialist INWIT reported EUR 1.036 billion revenue in 2024, crediting fixed wireless tenants for a tenancy ratio now above 2.2 and rising. Neutral-host models invite regional Internet service providers into the Italy fixed wireless access market without the burden of owning every mast, thereby intensifying competition. Meanwhile, shared spectrum rules let operators carve out mid-band slivers for pop-up deployments, ensuring that coverage grows even when capital is scarce.

Government Incentives For Rural Broadband In Italy

Under Italia Domani, EUR 5.29 billion (USD 5.98 billion) is earmarked for ultra-fast networks, complemented by a EUR 2.02 billion (USD 2.28 billion) 5G fund targeting towns under 5,000 residents. Although most money flows to fiber backbone builds, funded backhaul fibers and new towers are open to wholesale, lowering incremental costs for last-mile radio operators. AGCOM’s club-use license structure in the 26 GHz band lets dormant blocks be reused by neighbors, while a “use-it-or-lease-it” rule in 3.6-3.8 GHz forces incumbents to share idle spectrum. Together, subsidies and spectrum pooling enable smaller firms to boot-strap service in Calabria, Basilicata, Molise, and Abruzzo, shrinking Italy’s persistent north-south digital divide. The more projects advance, the more funding milestones unlock, creating a virtuous cycle of public-private investment in the Italy fixed wireless access market.

Expansion Of 26 GHz Spectrum For 5G FWA

AGCOM ended three years of uncertainty in October 2025 by publishing technical rules that unlock 1 GHz of 26 GHz airwaves, clarifying interference thresholds and handset-to-tower requirements. Each national operator already owns a 200 MHz slice, and the club-use clause allows spectrum pooling in zones where licensees are inactive, boosting spectral efficiency. TIM and Ericsson previously demonstrated 1 Gbps downlink over a 6.5 km rural link, debunking the myth that mmWave only works at street-lamp range. The GSMA estimates 150-700 MHz suffices for dense areas at 30% penetration, indicating that Italy’s allocation supports near-term growth, though additional releases could be needed as adoption scales.[3]GSMA, “5G mmWave Deployment Best Practices,” gsma.com Early movers now trial rooftop CPE in Milan’s San Babila and Rome’s EUR districts, creating premium tiers that siphon high-end users from congested fiber nodes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dependence on Spectrum Allocation Policies | -1.2% | National, with heightened sensitivity in regions awaiting 3.6 GHz renewals | Medium term (2-4 years) |

| Cost and Environmental Challenges of mmWave Deployment | -1.5% | Dense urban centers (Milan, Rome, Turin) and industrial zones | Short term (≤ 2 years) |

| Competitive Pressure from Fiber Rollout Acceleration | -2.0% | Northern regions (Lombardy, Veneto, Piedmont) with higher FTTH availability | Long term (≥ 4 years) |

| Community Opposition to 5G Tower Installations | -0.8% | Localized in smaller municipalities with active environmental advocacy groups | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Dependence On Spectrum Allocation Policies

Key 3.6-3.8 GHz licenses expire soon, yet renewal terms remain undefined, complicating multi-year investment plans. Radio hardware tuned for mid-band frequencies has limited reuse if operators are forced to migrate bands, upping financial risk. Small Internet service providers depend on leasing frameworks mandated by AGCOM; any postponement or shift in policy could strand equipment or trigger expensive retunes. Municipal approval windows for microwave backhaul also vary, adding localized uncertainty. Until policymakers provide clear timelines and fee structures, the Italy fixed wireless access market must price regulatory risk into every tower and CPE purchase.

Cost And Environmental Challenges Of mmWave Deployment

Millimeter-wave promises vast capacity yet demands tight cell grids and high-gain outdoor CPE, driving capital cost per subscriber higher than mid-band solutions. Politecnico di Milano field tests measured outdoor-to-indoor losses above 14 dB through dual-pane glass, making professionally mounted antennas mandatory in most buildings. Urban boards often apply stricter exposure limits than federal standards, extending permit cycles and raising compliance costs. The European Court of Auditors cautioned in 2022 that divergent local rules inflate the expense of marginal sites by millions of euros, reducing returns on small-cell clusters. Environmental groups have used these concerns to stall projects in Tuscany’s hill towns and along Liguria’s coast, forcing operators to reroute coverage plans and delaying revenue accrual in affected districts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Services Gain Revenue Momentum

Hardware spending led with 61.54% of revenue in 2025, reflecting upfront tower builds, antennas, and customer premises equipment required to blanket mountainous and coastal regions. However, services revenue is advancing at a 15.62% CAGR because operators now bundle managed Wi-Fi, cybersecurity, and static IP products into monthly bills, lifting the Italy fixed wireless access market size portion tied to recurring cash flows. EOLO, TIM, Wind Tre, and the Fastweb-Vodafone duo all price CPE rentals into subscription fees, reducing installation friction. Nokia’s FastMile Gateway 4 uses Wi-Fi 7 and Qualcomm’s X75 modem to deliver multi-gigabit throughput without specialist installs, helping lower acquisition costs. At the network edge, operators add femtocells and micro-antennas that upgrade capacity without large site leases, compressing payback periods.

A second momentum shift is automation. EOLO’s eSIM provisioning cuts truck rolls, while cloud orchestration lets a single technician monitor thousands of radios at once. Such efficiencies shrink operating expenses and allow operators to reinvest in spectrum and densification, sustaining hardware demand even as services outpace growth. By 2031, the services share of the Italy fixed wireless access market size is expected to surpass hardware, signaling a transition toward asset-light revenue streams that resemble cable or FTTH business models.

By Application: Commercial Uptake Accelerates

Residential lines dominated at 54.64% in 2025 because the largest fiber gaps remain among households in grey and white areas. Yet commercial links are projected to grow at a 15.46% CAGR as logistics depots, vineyards, and boutique hotels seek rapid broadband without trenching delays. Enterprises value guaranteed service levels and symmetric upload speeds that support cloud backups and video conferences, accepting premiums that enhance operator margins. Fastweb’s wholesale pact with Linkem enables each brand to reuse the other’s radio footprint, extending addressable business sites without duplicative capital.

Industrial campuses, ports, and smart farms are smaller today but gaining ground as 5G Standalone’s low latency supports robotics and sensor data. TIM’s WiFi Casa product defends residential market share in non-fiber zones, while Wind Tre leverages OpNet’s 3,000 acquired base stations to court suburban merchants left out of FTTH rollouts. Altogether, rising commercial adoption widens the Italy fixed wireless access market footprint beyond homes, diversifying revenue and cushioning seasonal churn in tourist districts.

By Frequency Band: Mid-Band Dominates, mmWave Finds Premium Niche

Sub-6 GHz channels accounted for 55.84% of 2025 revenue because stronger propagation supports broad coverage with fewer towers, perfect for rolling terrain across Piedmont and Veneto. The Italy fixed wireless access market relies on this band for baseline service tiers, exploiting a favorable mix of range and capacity. mmWave revenue, meanwhile, is projected to grow at a 15.78% CAGR through 2031 as AGCOM’s 26 GHz framework green-lights city-center rollouts. TIM’s 4 Gbps live demo using 400 MHz aggregated blocks validated mmWave’s headline speeds, generating marketing buzz that tilts affluent users toward premium plans.

Operators must lease unused MHz to rivals, ensuring high network utilization. Operators balance mid-band for blanket coverage with mmWave for gigabit hotspots in Milan’s Porta Nuova or Rome’s EUR quarter. This balance maximizes capacity and protects margins, anchoring long-term growth in the Italy fixed wireless access market.

By Deployment Mode: Outdoor CPE Poised To Expand

Indoor routers made up 60.42% of installed units in 2025, favored for simple self-install packages that minimize technician visits. Outdoor units, however, are surging at a 15.39% CAGR as operators tackle valleys, coastal cliffs, and mountain hamlets where exterior antennas boost signal-to-noise ratios. Zyxel’s NR7305 outdoor router offers 7.01 Gbps peak downlink with IP66 weather sealing and 802.3at power over Ethernet, ideal for Sardinian salt-spray or Alpine snow. EOLO’s October 2025 gigabit launch hinged on rooftop installs that carry line-of-sight traffic up to 6 km, unlocking subscribers unreachable with window-mounted gear.

Self-install indoor gateways retain popularity in dense neighborhoods where signal strength is ample, particularly after Wi-Fi 7 chips reduce internal congestion. Yet outdoor CPE is indispensable for grey zones, pushing the Italy fixed wireless access market toward a hybrid install model that balances cost and performance. As operators automate provisioning and remote diagnostics, professional outdoor installs become more scalable, furthering rural coverage goals.

Geography Analysis

Northern Italy commands the largest slice of revenue because dense populations and high GDP per capita translate into robust take-rates. Lombardy and Emilia-Romagna supply the bulk of subscriptions, where 3.6 GHz clusters fill historic city centers too narrow for easy trenching. Here, outdoor CPE sits on terracotta rooftops, meeting landlord rules while delivering 300-600 Mbps service. Operators use shared tower grids to cut rents, ensuring competitive tariffs and stiff rivalry in the Italy fixed wireless access market.

Central regions such as Tuscany, Umbria, and Lazio show mid-level penetration but brisk growth. The October 2025 release of 26 GHz technical rules spurred trials in Rome’s suburbs, relieving evening congestion on FTTH links and boosting average speeds. Vineyards in Chianti deploy outdoor routers to stream agronomic data and facilitate agritourism bookings, illustrating diverse commercial use cases. Municipal councils in these provinces leverage Italia Domani funding to backhaul towers, narrowing the urban-rural digital divide.

Southern regions and islands remain under-served yet carry the highest forecast CAGR as public subsidies de-risk buildouts. Calabria and Basilicata are early beneficiaries of government vouchers that discount installation fees, raising household adoption. In Sicily and Sardinia, seasonal tourism peaks motivate hotel chains to adopt gigabit wireless for temporary capacity boosts, an application ill-suited to unmanaged fiber lines. Overall, the mix of subsidy, shared infrastructure, and outdoor CPE flexibility positions the Italy fixed wireless access market for especially strong growth south of Rome.

Competitive Landscape

EOLO leads with 27.9% of subscribers, leveraging proprietary wireless backhaul and rural focus to dominate white areas. TIM follows at 19.5%, pairing nationwide mobile assets with bundled fixed plans that deepen customer stickiness. The December 2024 Fastweb-Vodafone merger, backed by Swisscom, assembled mobile, FTTH, and mid-band spectrum into a converged challenger holding 14.9%, enabling quad-play offers at scale. Together these top suppliers account for 62.3% of the Italy fixed wireless access market share, indicating moderate concentration.

Wind Tre’s August 2024 purchase of OpNet injected 3,000 base stations and valuable 3.5 GHz holdings, helping it court suburban families left out of fiber deployments. Tiscali and a cadre of regional ISPs occupy niche footholds, accessing mid-band airwaves via AGCOM’s lease-or-lose rules. EOLO deploys autonomous network automation to provision new lines in minutes, while Nokia’s new Wi-Fi 7 gateways allow rivals to promise fiber-like speeds without truck rolls.

Tower companies such as INWIT and Cellnex profit from this multi-operator environment, boasting tenancy ratios above 2.0 and pipeline commitments for another 3,500 towers by 2030. Regulators keep hoarding in check, mandating wholesale mmWave access and strict build deadlines. Consequently, price competition stays fierce, but differentiation through reliability, bundled content, and guaranteed service levels remains viable. The Italy fixed wireless access market rewards agile operators that blend shared assets, smart spectrum use, and customer-centric packaging.

Italy Fixed Wireless Access (FWA) Industry Leaders

Telecom Italia S.p.A.

Vodafone Italia S.p.A.

Fastweb S.p.A.

Linkem S.p.A.

EOLO S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: TIM, Fastweb, and Vodafone Italia executed a RAN-sharing pact covering passive and active infrastructure in low-density municipalities, reducing site costs and accelerating 5G reach.

- December 2025: Zyxel unveiled the NR5313 indoor 5G router with Wi-Fi 7 and 6.47 Gbps peak downlink for self-install consumer deployments.

- October 2025: AGCOM published final 26 GHz technical rules, enabling operators to commercialize dormant mmWave blocks.

- October 2025: EOLO launched a 1 Gbps 5G fixed wireless plan at EUR 34.90 (USD 39.49) across more than 300 municipalities.

Italy Fixed Wireless Access (FWA) Market Report Scope

Fixed wireless technology connects two fixed locations, such as buildings or towers, using wireless links like radio waves or laser bridges. Typically integrated into a wireless LAN infrastructure, fixed wireless links facilitate data communication between sites. Moreover, Fixed Wireless Data (FWD) links often serve as a cost-effective substitute for leasing fiber or installing cables between buildings.

The Italy Fixed Wireless Access (FWA) Market Report is Segmented by Type (Hardware, and Services), Application (Residential, Commercial, and Industrial), Frequency Band (Sub-6 GHz, and mmWave above 24 GHz), and Deployment Mode (Indoor CPE, and Outdoor CPE). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware | Consumer Premises Equipment (CPE) |

| Access Units (Femto and Picocells) | |

| Services |

| Residential |

| Commercial |

| Industrial |

| Sub-6 GHz |

| mmWave ( > 24 GHz ) |

| Indoor CPE |

| Outdoor CPE |

| By Type | Hardware | Consumer Premises Equipment (CPE) |

| Access Units (Femto and Picocells) | ||

| Services | ||

| By Application | Residential | |

| Commercial | ||

| Industrial | ||

| By Frequency Band | Sub-6 GHz | |

| mmWave ( > 24 GHz ) | ||

| By Deployment Mode | Indoor CPE | |

| Outdoor CPE |

Key Questions Answered in the Report

What is the current value of the Italy fixed wireless access market?

The Italy fixed wireless access market size stands at USD 1.75 billion in 2026.

How fast is revenue growing?

Market revenue is forecast to expand at a 14.02% CAGR, reaching USD 3.37 billion by 2031.

Which service type is increasing fastest?

Subscription services, including managed Wi-Fi and static IP bundles, are advancing at a 15.62% CAGR through 2031.

Why are operators eager to use 26 GHz spectrum?

AGCOM rules clarified in October 2025 allow multi-gigabit links in dense cities, unlocking premium tiers for capacity-hungry users.

How does fixed wireless compare with fiber in rural Italy?

In many white and grey zones, fixed wireless offers quicker deployment and comparable speeds, bridging gaps where fiber trenching is uneconomic.

Who leads the competitive field?

EOLO, TIM, and the merged Fastweb-Vodafone group together command just over 60% of subscriptions, with Wind Tre and Tiscali following.

Page last updated on: