Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Italy Data Center Rack Market is Segmented by Rack Size (Quartely Rack, Half Rack, Full Rack), Rack Height (42U, 45U and More), Rack Type (Cabinet (Closed) Racks, Open-Frame Racks, Wall-Mount Racks), Data Center Type (Colocation Facilities, Hyperscale and Cloud Service Provider DCs, Enterprise and Edge), Material (Steel, Aluminum, Other Alloys and Composites). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

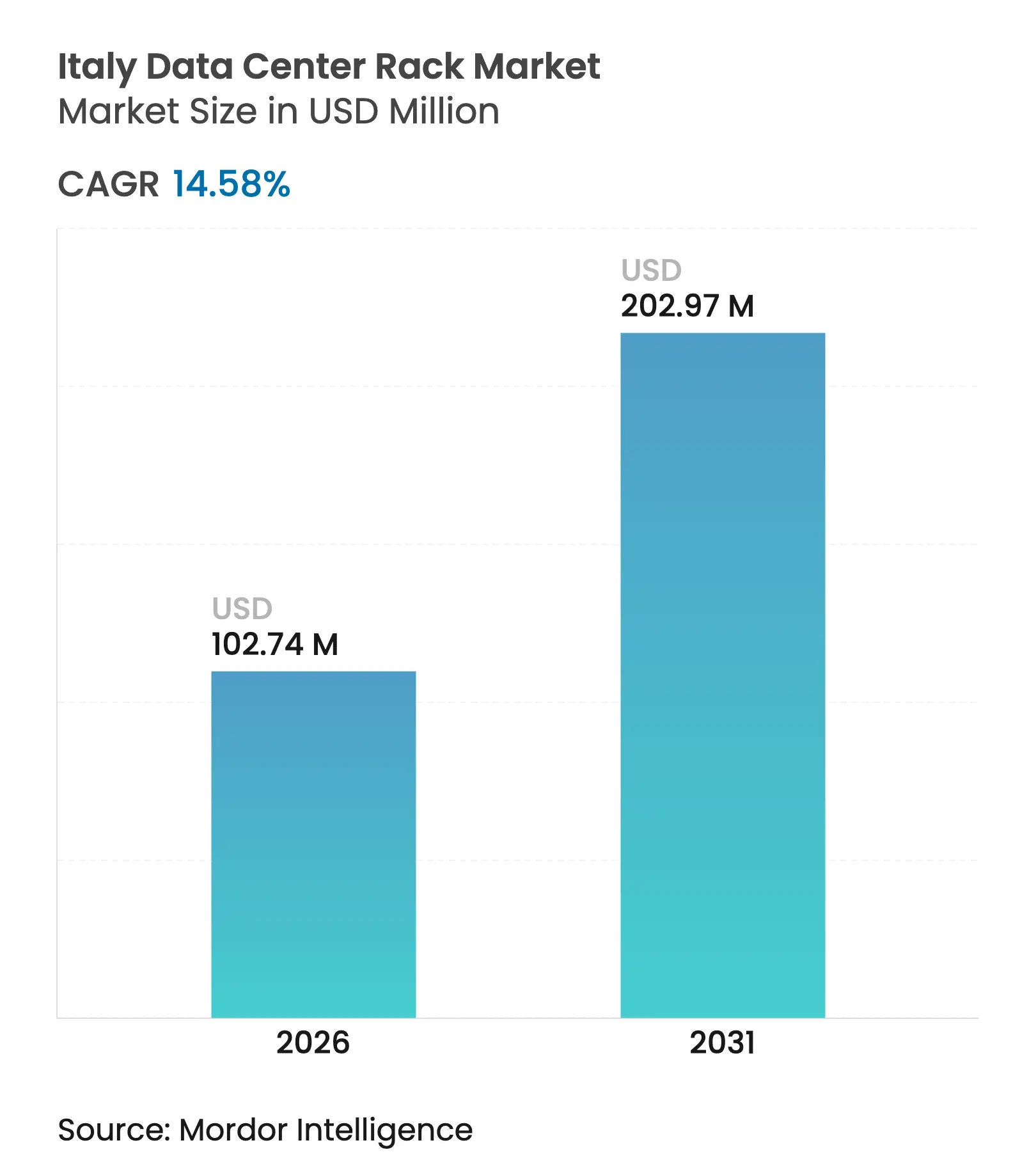

| Market Size (2026) | USD 102.74 Million |

| Market Size (2031) | USD 202.97 Million |

| Growth Rate (2026 - 2031) | 14.58 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Italy data center rack market size in 2026 is estimated at USD 102.74 million, growing from 2025 value of USD 89.68 million with 2031 projections showing USD 202.97 million, growing at 14.58% CAGR over 2026-2031. Sustained capital commitments of more than EUR 6 billion (USD 6.90 billion) from Microsoft, AWS, and Data4, combined with Italy’s cloud-first public-sector mandate, are the primary catalysts. Power-connection requests already total 42 GW, a level that signals a decisive shift from 5-10 kW legacy deployments to 80-100 kW racks engineered for AI workloads. Edge roll-outs led by national telcos and a sharp rise in ESG-linked financing for liquid-cooled architectures further reinforce demand. Competitive dynamics favour suppliers that can combine racks, cooling, and power distribution in one integrated offer as energy prices remain 40% higher than Spanish averages, squeezing operating margins.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Aggressive cloud-first policies of Italian public sector

Aggressive cloud-first policies of Italian public sector

| +2.8% | National, concentrated in Rome administrative hub | Medium term (2-4 years) | (~)% Impact on CAGR Forecast:

+2.8%

|

Geographic Relevance

:

National, concentrated in Rome administrative hub

|

Impact Timeline

:

Medium term (2-4 years)

|

Surge in hyperscale investments around Milan & Rome

availability zones

Surge in hyperscale investments around Milan & Rome

availability zones

| +3.2% | Northern Italy (Milan) and Central Italy (Rome) | Short term (≤ 2 years) | |||

Acceleration of edge-network roll-outs by Italian telcos

(5G & FTTH backhaul)

Acceleration of edge-network roll-outs by Italian telcos

(5G & FTTH backhaul)

| +1.9% | National, with priority in metropolitan areas | Medium term (2-4 years) | |||

Stringent latency SLAs pushed by e-commerce & fintech

platforms

Stringent latency SLAs pushed by e-commerce & fintech

platforms

| +1.4% | Milan financial district, Rome e-government corridor | Short term (≤ 2 years) | |||

Growth of AI/ML workloads demanding high-density (40-52

kW) racks

Growth of AI/ML workloads demanding high-density (40-52

kW) racks

| +3.8% | Milan-Rome corridor, expanding to Turin and Naples | Long term (≥ 4 years) | |||

ESG-linked financing rewarding liquid-cooled rack

deployments

ESG-linked financing rewarding liquid-cooled rack

deployments

| +1.5% | National, with emphasis on renewable energy regions | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Aggressive cloud-first policies of the Italian public sector

The National Recovery and Resilience Plan (PNRR) allocates EUR 194.4 billion (USD 223.81 billion) to modernize public infrastructure, and the 2024-2026 Triennial Plan requires 75% of agency workloads to migrate to cloud platforms.[1]Agenzia per l’Italia Digitale, “Piano Triennale per l’Informatica 2024-2026,” agid.gov.itStandardized racks that meet the Public Connectivity System’s interoperability rules are now mandatory for new deployments. Sovereign-hosting rules further tilt purchasing toward domestic supply sources, boosting demand for secure 42U cabinets in Rome’s government corridors.

Surge in hyperscale investments around Milan & Rome availability zones

Microsoft’s EUR 4.3 billion (USD 4.95 billion) build-out in Northern Italy, AWS’s EUR 1.2 billion (USD 1.38 billion) Milan expansion, and Data4’s EUR 1 billion (USD 1.15 billion) campus jointly anchor a hyperscale cluster that requires consistent, OCP-compatible 48U racks engineered for GPU-dense nodes.[2]Amazon Corporate, “AWS announces EUR 1.2 billion investment in Italy,” aboutamazon.comThe clustering effect compresses delivery timelines and elevates local technical-support requirements, favouring vendors with on-the-ground assembly and service hubs.

Acceleration of edge-network roll-outs by Italian telcos

Fastweb, TIM and WindTre have earmarked more than EUR 3.4 billion for nationwide 5G and FTTH backbones, generating fresh demand for wall-mount and compact racks that integrate with telecommunication cabinets. Edge sites in smaller municipalities require ruggedized enclosures, tight thermal envelopes and rapid-install designs, widening the product mix beyond traditional full-height cabinets.

Growth of AI/ML workloads demanding high-density racks

Italy’s 2024-2026 AI Strategy has lifted enterprise AI adoption to 8.2% of companies. iGenius and Vertiv unveiled a sovereign AI data center featuring racks able to dissipate 500-1000 kW per row, highlighting how liquid cooling, busbar power feeds and 48U vertical density coalesce into a new specification baseline.[3]Vertiv Corporate, “Vertiv launches PowerDirect and SmartRun,” vertiv.comLegacy rack vendors are pivoting to integrated solutions that bundle cooling manifolds and high-amp power panels.

Restraints Impact Analysis

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Lengthy building-permit cycles for new colocation sites

Lengthy building-permit cycles for new colocation sites

| -1.8% | National, with acute delays in Northern Italy | Medium term (2-4 years) | (~)% Impact on CAGR Forecast:

-1.8%

|

Geographic Relevance

:

National, with acute delays in Northern Italy

|

Impact Timeline

:

Medium term (2-4 years)

|

Rising electricity spot-prices versus long-term PPA

availability

Rising electricity spot-prices versus long-term PPA

availability

| -2.3% | National, with highest impact in Southern Italy | Short term (≤ 2 years) | |||

Limited skilled labour pool for high-density O&M in

Tier 3+ facilities

Limited skilled labour pool for high-density O&M in

Tier 3+ facilities

| -1.2% | Northern Italy (Milan-Turin corridor) | Long term (≥ 4 years) | |||

Tightened national cybersecurity law (Perimetro di

Sicurezza Nazionale Cibernetica) complicating equipment sourcing

Tightened national cybersecurity law (Perimetro di

Sicurezza Nazionale Cibernetica) complicating equipment sourcing

| -0.9% | National, with emphasis on critical infrastructure | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Lengthy building-permit cycles for new colocation sites

Italian law lacks dedicated data-center regulations, forcing developers to navigate commercial-building codes and environmental reviews that stretch approvals to 18-24 months, double northern-European norms . These delays channel demand toward operators with proven local permitting expertise, skewing early-stage orders in their favour.

Rising electricity spot prices versus limited PPA option

Wholesale electricity costs climbed 24% in 2025, placing Italy 40% above Spain. With few long-term PPAs available, operators rely on volatile spot markets, prompting a faster shift to liquid cooling and higher-efficiency rack designs to control power bills.

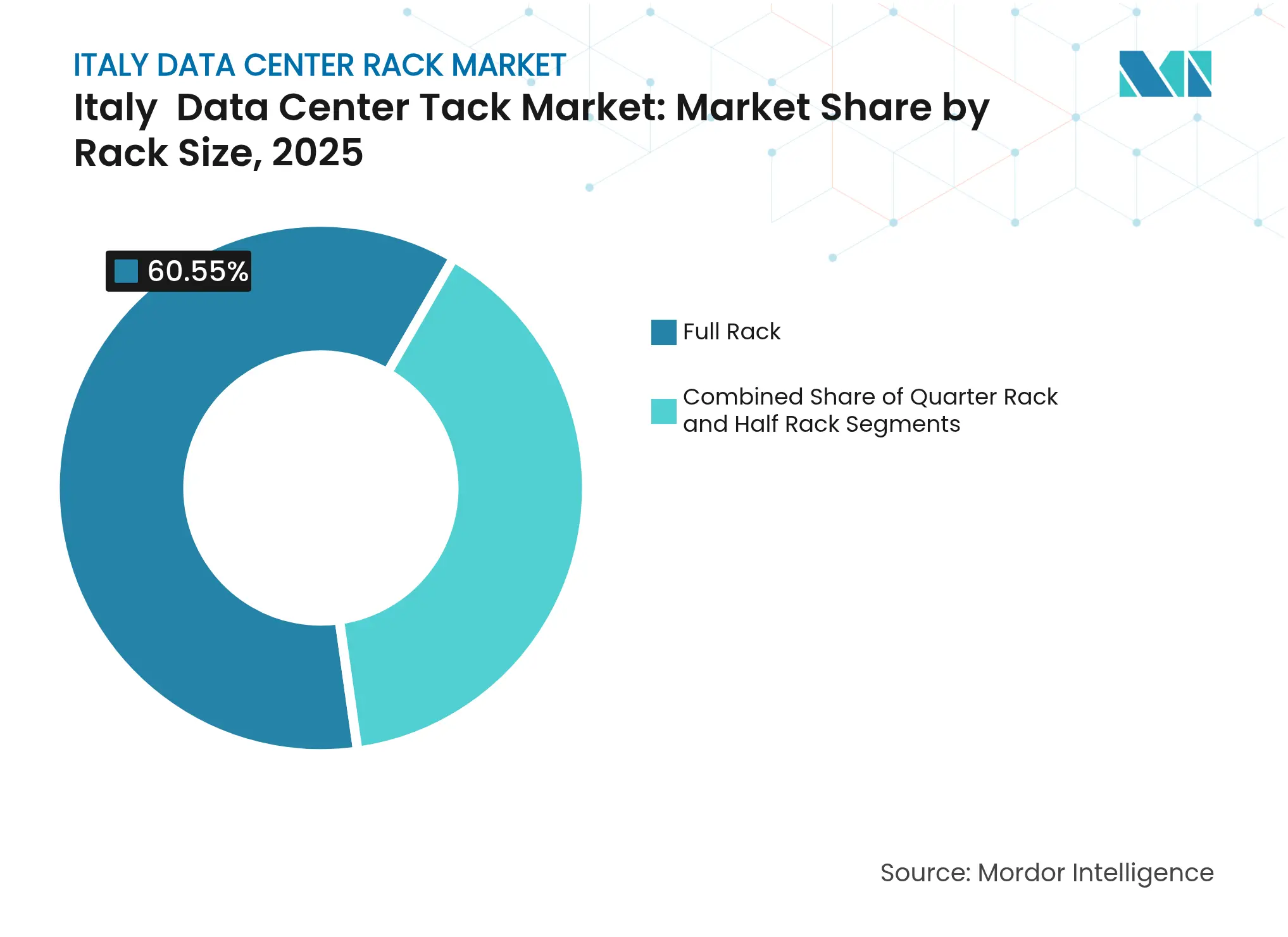

By Rack Size: Full-rack standardization enables hyperscale scale-out

Full Rack units captured 60.55% of 2025 revenue as hyperscalers seek identical footprints that accelerate automated installation. The Italy data center rack market size for Full Rack solutions is on track for a 14.68% CAGR to 2031, helped by Microsoft’s uniform deployment blueprints in Lombardy. Smaller Quarter and Half Rack formats remain relevant for edge and enterprise micro-sites, yet their share will erode as cloud providers expand sovereign zones. OCP-driven interchangeability raises order volumes for suppliers able to ship pre-configured ecosystems.

Ongoing conversions from mixed cabinet estates to fully standardized 52U or 48U profiles lift ancillary demand for busway power, in-rack battery back-ups and monitoring modules. This convergence underpins cross-selling opportunities across thermal, power and physical-security categories, reshaping vendor scorecards toward ecosystem depth

Note: Segment shares of all individual segments available upon report purchase

By Rack Height: 48U emerges as the AI-era default

While 42U frames held 51.80% of 2025 shipments, 48U designs are rising fastest at 15.12% CAGR as operators squeeze more servers into each footprint. Google’s fifth-generation cooling distribution unit, added to the OCP repository, is calibrated specifically for 48U, forging an ecosystem that reinforces the format. The Italy data center rack market now grades bids on vertical capacity alongside thermal ceilings, pushing cabinet makers to redesign load-bearing rails and cable-management planes.

Larger vertical envelopes support denser power shelves and direct-to-chip liquid loops, yet still allow technicians safe access for hot-swap maintenance. Progressive operators in Lombardy are testing custom 52U shells for ultradense AI clusters, but 48U offers a pragmatic midpoint that balances serviceability with space efficiency.

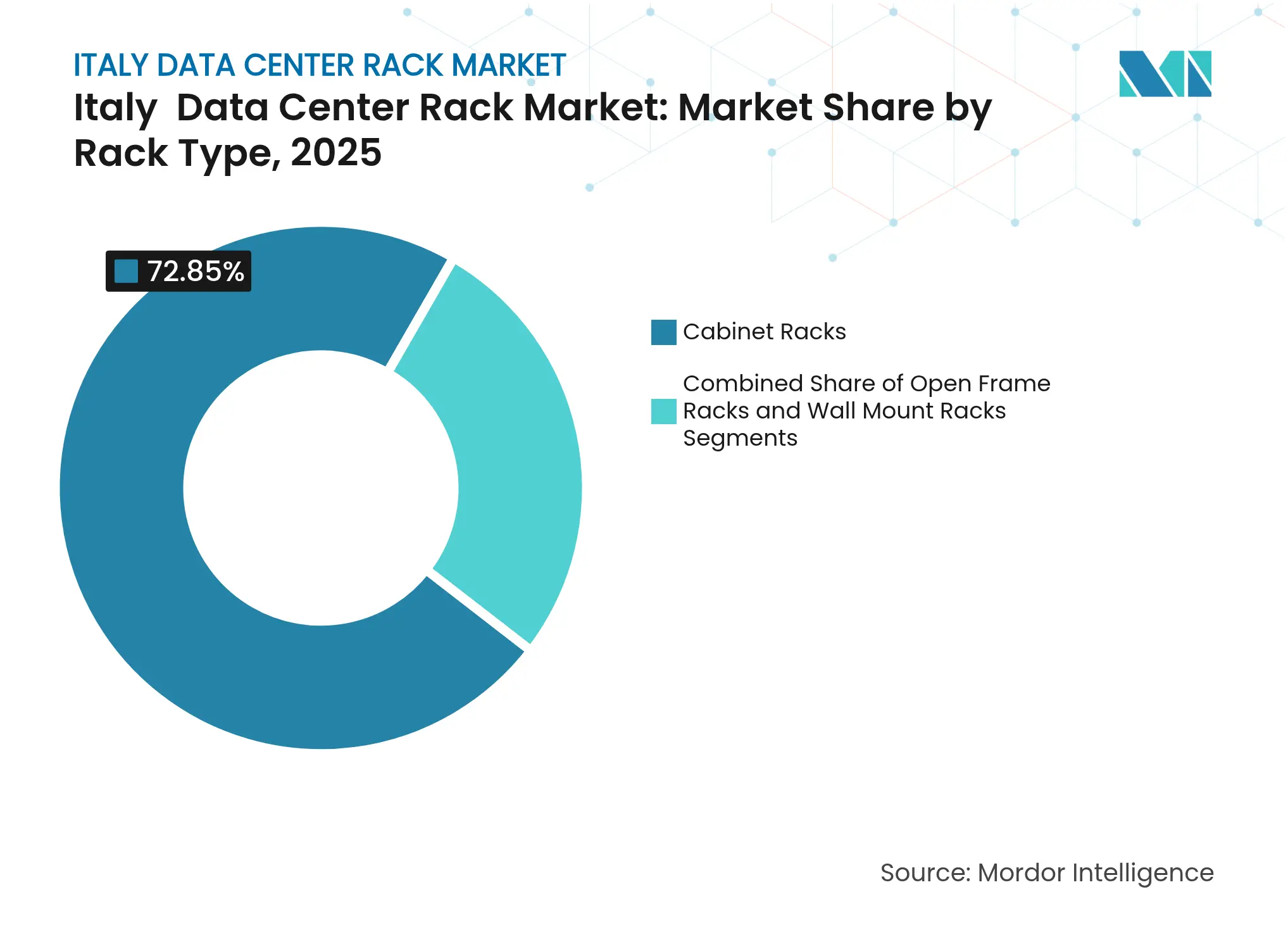

By Rack Type: Cabinet leadership underscores security needs

Cabinet (closed) racks commanded 72.85% of revenue in 2025 on the back of colocation contracts that prize customer isolation, airflow containment and compliance with Italy’s cybersecurity perimeter rules. The segment will compound at 15.96% annually to 2031 as enterprise tenants rent high-density footprints within third-party facilities. Open-frame racks retain a role inside sealed hyperscale halls where physical segregation is unnecessary, yet the enclosure premium is shrinking.

Cabinet manufacturers are embedding IP-rated cable apertures, biometric door handles and in-rack suppression systems that meet evolving Perimetro di Sicurezza requirements. Integration elevates switching-cost barriers, compelling operators to standardize on a single mechanical family across sites to streamline spares and maintenance.

Note: Segment shares of all individual segments available upon report purchase

By Data Center Type: Hyperscalers redefine procurement criteria

Colocation facilities still claimed 52.10% of 2025 spending, but hyperscaler and cloud service provider builds will outpace every other segment at a 16.85% CAGR to 2031. The Italy data center rack market share held by hyper-scale operators is projected to widen as sovereign AI workloads mature inside ring-fenced Milan and Rome regions. Edge nodes attached to 5G towers pull through wall-mount and micro cabinets that address remote-operation constraints.

Hyperscale buyers insist on automated factory testing, serial-number traceability and logistics that sync with building-shell completion schedules. Vendors with modular, pre-engineered racks that integrate power and cooling are best placed to win multi-site, multi-megawatt frame agreements.

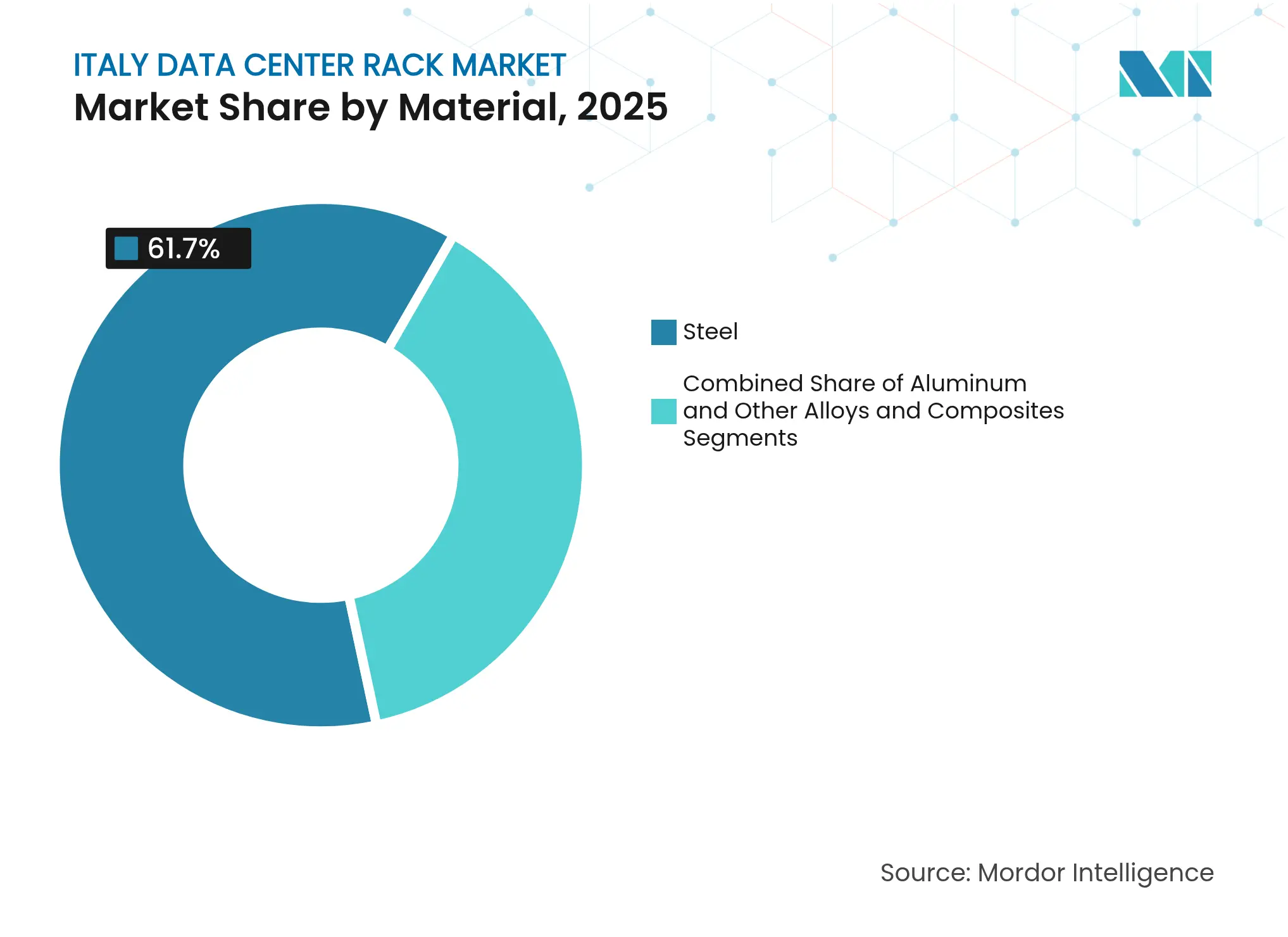

By Material: Aluminum uptake accelerates in the high-density era

Steel still constitutes 61.70% of 2025 shipments thanks to favourable cost and proven rigidity. Yet, Aluminum is expanding at a 14.92% CAGR as operators value its lighter weight for high-density row designs. The Italy data center rack market size for Aluminum enclosures will rise notably in facilities pursuing 500-1000 kW per row, where lighter frames simplify floor loading calculations. Hybrid chassis that pair steel cores with aluminum doors or cross-members are gaining traction as a midpoint between cost and performance.

Thermal conductivity advantages also allow Aluminum doors to act as passive heat sinks, easing the job of liquid loops attached to GPUs. Suppliers that master multi-material welding and powder-coat finishing stand to capture premium margins in this segment.

Note: Segment shares of all individual segments available upon report purchase

Rome as the administrative nucleus, fuelling orders for compliance-centric cabinets that support the PNRR’s cloud-migration targets. Concentrated activity compresses installer capacity, prompting operators to secure multi-year service contracts to guarantee skilled labour availability near these zones.

Central regions, including Tuscany and Emilia-Romagna, now court second-wave deployments that leverage renewable energy quotas and emerging fibre routes. The shift to zonal power pricing encourages smaller municipalities to market low-carbon energy mixes to colocation investors, yet limited last-mile connectivity still tempers immediate take-up. Projects such as the subterranean Trento facility illustrate how unconventional sites can exploit natural cooling to offset power premiums.

Market Concentration

Competition is moderate, with global incumbents every bit as active as regional specialists. Eaton, Schneider Electric, Vertiv and Rittal leverage extensive Italian service networks to deliver integrated rack-power-cooling bundles. Their portfolios now embed liquid-cooling manifolds, rear-door heat exchangers and busbar power rails aligned to 48U and 52U chassis. New entrants emphasise AI-ready platforms; for example, Vertiv and NVIDIA co-developed a reference design that marries 132 kW racks to direct-to-chip cooling across the GB200 platform.

M&A is reshaping the landscape. Legrand acquired four data-center-focused firms in 2024, broadening its rack ecosystem with smart PDUs and cable-management suites. Domestic manufacturers such as Tecnosteel differentiate through rapid customisation and proximity manufacturing, an advantage when hyperscalers demand sub-eight-week lead times. Meanwhile, ABB and Cisco bundle power or networking gear with chassis pitches to boost attach rates and lock in larger share-of-wallet per hall.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE and GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES and FUTURE OUTLOOK

Market Definitions and Key Coverage

According to Mordor Intelligence, the Italy data center rack market captures every newly manufactured open-frame, cabinet, and wall-mount rack (19- or 23-inch) installed in colocation, hyperscale, enterprise, and edge facilities across the country, valued at the actual transaction prices paid for the rack itself. The study tracks volume in rack units and relates density in kilowatts per rack to spending.

Scope exclusion: Our analysts exclude second-hand racks, modular container shells, and standalone accessories such as patch panels or power strips.

Segmentation Overview

Detailed Research Methodology and Data Validation

Primary Research

Conversations with Milan and Rome-based colocation managers, hyperscaler facility engineers, domestic rack fabricators, and procurement leads let us verify density trends, price spreads, and build-out timetables. Follow-up surveys across edge-site owners refined the energy-adjustment factors and confirmed adoption intentions for half-rack micro-PODs.

Desk Research

Our desk work began with ISTAT production indices, the Ministry of Enterprises building-permit bulletins, GSE power-tariff files, and customs line items 9403.20 and 8517.62 that flag rack inflows. Trade bodies such as the European Data Centre Association, Open Compute Project, and AI-on-GPU consortium reports helped us understand the nationwide shift toward 48U liquid-ready frames.

We then enriched these signals with D&B Hoovers supplier revenues, Dow Jones Factiva news on facility pipelines, and Questel patent filings that highlight cooling innovations, while company filings and credible press releases clarified average selling prices. This list is illustrative, not exhaustive, of the sources reviewed.

Market-Sizing & Forecasting

We begin with a top-down reconstruction that multiplies forecast white-space square meters by racks-per-megawatt ratios and staggered utilization curves. We then cross-check the totals with sampled manufacturer sales and distributor channel checks. Key variables include announced IT-load additions, average rack power draw, rack-height mix, flat-rolled steel prices, and the public-cloud share of new capacity. A multivariate regression linking these drivers to historical rack shipments yields the forecast, and a bottom-up roll-up of sampled ASP × volume validates the curve.

Data Validation & Update Cycle

Mordor analysts compare each model run with import statistics, project trackers, and quarterly vendor earnings; variances above three percent trigger a re-examination before sign-off. Reports refresh annually, while a mid-cycle update is issued for material investment events, and a final analyst pass ensures clients receive the latest view.

Why Mordor's Italy Data Center Rack Baseline Commands Reliability

Benchmark comparison

Published estimates differ, and we acknowledge that openly. Divergences typically arise from scope choices, currency conversions, refresh cadence, and density assumptions for AI clusters.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 89.68 million (2025) | Mordor Intelligence | Anonymized source:Mordor Intelligence | Primary gap driver: | |

USD 83.4 million (2023) | Regional Consultancy A | Excludes edge and telecom micro-sites, applies conservative digital-adoption multipliers | ||

USD 330 million (2025) | Trade Journal B | Combines racks with broader mechanical enclosures, applies list pricing | ||

USD 365 million (2023) | Industry Association C | Values installed base, includes pre-owned units |

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.