Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

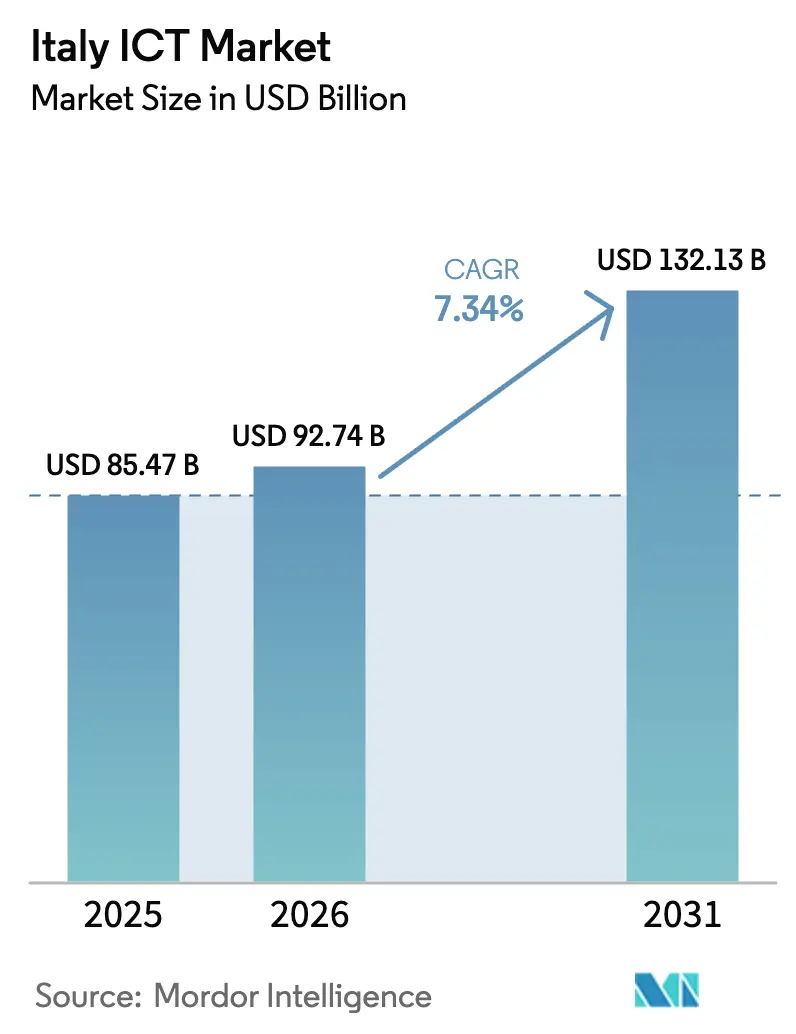

| Base Year Market Size (2025) | USD 85.47 Billion |

| Market Size (2026) | USD 92.74 Billion |

| Market Size (2031) | USD 132.13 Billion |

| Growth Rate (2026 - 2031) | 7.34% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy ICT Market Analysis by Mordor Intelligence

The Italy ICT Market size is projected to expand from USD 85.47 billion in 2025 and USD 92.74 billion in 2026 to USD 132.13 billion by 2031, registering a CAGR of 7.34% between 2026 to 2031. Accelerated public funding under Mission 1 of the National Recovery and Resilience Plan, which earmarked EUR 41.34 billion (USD 46.3 billion) for nationwide digitalization, provides a long-run demand floor as ministries, regions, and municipalities shift workloads to the cloud, automate back-office workflows, and roll out citizen-facing e-services. Continued fiber-to-the-premises build-outs, now at 59.6% national coverage, raise baseline bandwidth, enabling low-latency SaaS adoption in manufacturing, banking, and health care. Multi-cloud strategies are proliferating as risk-averse enterprises pair domestic hyperscale regions with sovereign cloud nodes to meet data-residency requirements under the NIS2 Directive, enacted locally in 2024. Meanwhile, tax credits under Transition 4.0 reduce upfront costs for connected machinery, IoT sensors, and digital twin software, steering industrial buyers toward predictive analytics and remote maintenance use cases.

Key Report Takeaways

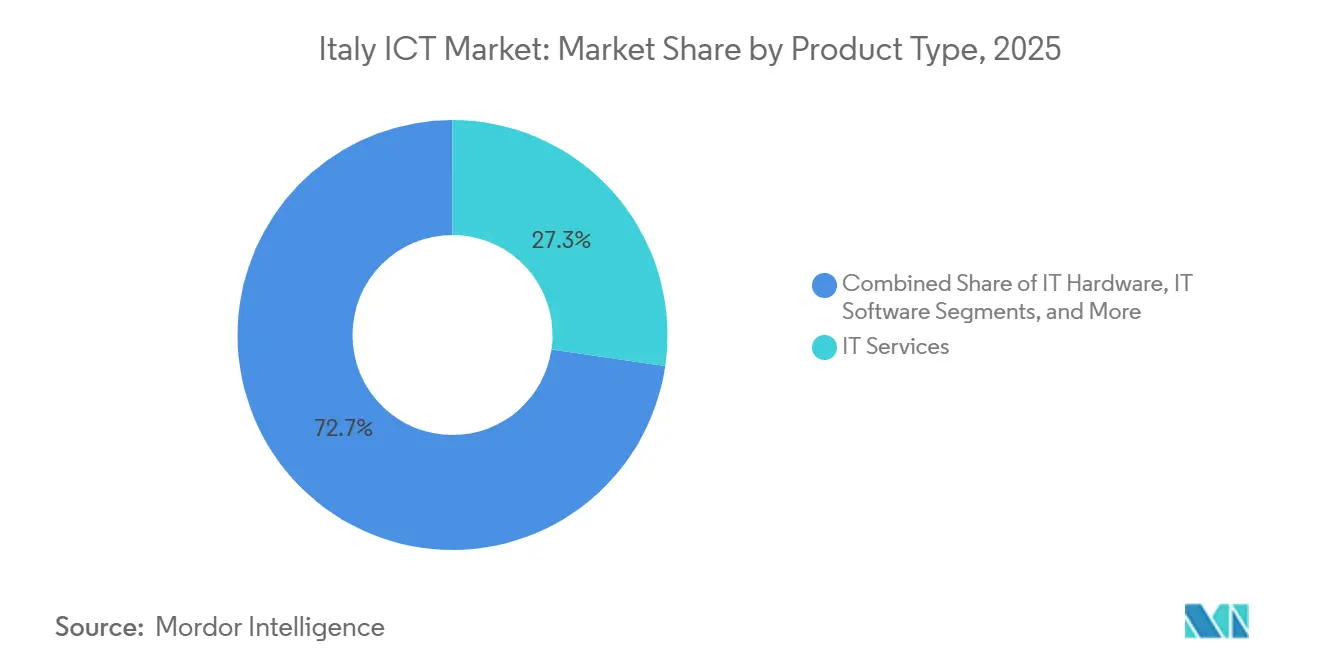

- By product type, IT Services led with 27.31% revenue share in 2025 while Cloud and Platform Services are forecast to grow at an 8.46% CAGR to 2031.

- By enterprise size, large enterprises accounted for 64.68% of the Italy ICT market share in 2025, whereas SMEs record the fastest trajectory at an 8.27% CAGR through 2031.

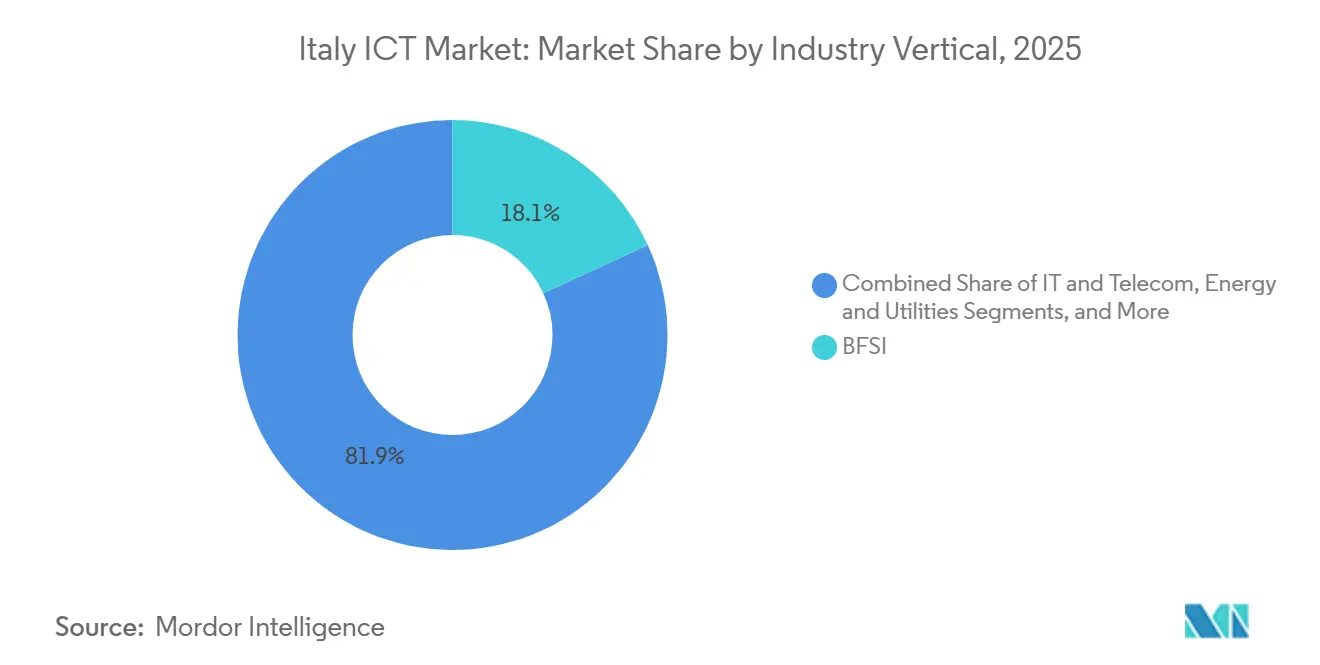

- By industry vertical, BFSI held an 18.13% slice of the Italy ICT market size in 2025 and Manufacturing and Industry 4.0 is advancing at a 9.16% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Italy's Ultra-Fast Broadband Networks | +1.2% | National, strongest in Lombardy, Veneto, Emilia-Romagna | Medium term (2–4 years) |

| Growing Adoption of Cloud-Native Digital Transformation Projects | +1.5% | National, led by BFSI and Manufacturing | Short term (≤ 2 years) |

| Government Incentives Under Italy's National Recovery and Resilience Plan (NRRP) | +1.8% | National, skewed toward Southern regions and islands | Long term (≥ 4 years) |

| Rising Demand for Cybersecurity Solutions Amid Increasing Threat Landscape | +1.0% | National, emphasis on BFSI, Energy, Public Administration | Short term (≤ 2 years) |

| Rapid Proliferation of Industry 4.0 and Smart Manufacturing Initiatives | +1.3% | Northern and Central industrial corridors | Medium term (2–4 years) |

| Increasing Mobile Workforce Fueling Managed Services Consumption | +0.9% | National, higher in professional services | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion Of Italy's Ultra-Fast Broadband Networks

The Italia 1 Giga and Italia 5G programs devote EUR 5.29 billion (USD 5.9 billion) to extend fiber to 8.5 million premises in underserved areas by 2026.[1]Ministry of Economic Development, “Transition 4.0 Incentives,” Ministry of Enterprises and Made in Italy, mise.gov.it Open Fiber reached 13.7 million connected premises by end-2025, enabling retail ISPs to offer symmetrical gigabit plans that underpin real-time collaboration, edge analytics, and streaming in Industry 4.0 settings. Manufacturing clusters benefit most because predictive maintenance, cobot coordination, and digital-twin synchronization require sub-10 millisecond latency. Regulatory pressure increases service-level transparency, as the 2024 Electronic Communications Code obliges carriers to publish symmetric bandwidth and latency guarantees, prompting investment in network-monitoring and SD-WAN overlays.

Growing Adoption Of Cloud-Native Digital Transformation Projects

Cloud and Platform Services expand at an 8.46% CAGR through 2031, fueled by containerization, microservices, and managed databases from AWS, Microsoft Azure, and Google Cloud. AWS’s second Milan availability zone, launched in 2025, provides single-digit millisecond latency for fintech fraud detection and e-commerce dynamic pricing. Microsoft pledged EUR 4.3 billion (USD 4.8 billion) for fresh Azure capacity and AI skilling programs that will reach 1 million Italians by 2028. Google Cloud and Engineering Ingegneria Informatica introduced a sovereign-cloud stack for public entities that embeds data-residency and encryption-key controls, aligning with NIS2 obligations. Multi-cloud penetration hit 62% among large enterprises in 2025 as CIOs arbitrage reserved-instance pricing and mitigate vendor lock-in.

Government Incentives Under Italy's National Recovery And Resilience Plan

The EUR 41.34 billion (USD 46.3 billion) digital envelope channels grants and tax credits into public-service cloud migration, SME digitization, and digital-health rollouts. The 2024-2026 Piano Triennale mandates a cloud-first stance for new public projects and a 75% workload migration target, redirecting roughly EUR 1.2 billion (USD 1.3 billion) annually to SaaS, PaaS, and managed hosting. Transition 4.0 reimburses up to 40% of CapEx on connected machinery and 20% on software, accelerating ERP, MES, and IoT deployments in SMEs. The plan earmarks 40% of digital-infrastructure funds for Campania, Puglia, Calabria, Sicily, and Sardinia, narrowing the historical connectivity gap.

Rapid Proliferation Of Industry 4.0 And Smart Manufacturing Initiatives

Manufacturing output valued at EUR 312 billion (USD 349 billion) drives demand for IoT sensors, industrial robots, and digital-twin software, giving the sector a 9.16% CAGR to 2031. Robot density reached 185 units per 10,000 workers in 2025, second only to Germany in the EU. Stellantis invested EUR 2 billion (USD 2.2 billion) in Mirafiori and Melfi plants, pairing cobots with SAP Digital Manufacturing Cloud to slash cycle time by 22%. Leonardo’s digital-twin simulations trimmed helicopter assembly by 18%, validating virtual changes before tooling commitments. Cluster suppliers in Emilia-Romagna adopted PTC ThingWorx to monitor asset health and avert costly downtime.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Shortage of Advanced ICT Skillsets in Domestic Labor Pool | -1.1% | National, deepest in Southern regions | Long term (≥ 4 years) |

| High Electricity Costs Impacting Data Center Economics | -0.7% | National, acute in Milan-area hubs | Medium term (2–4 years) |

| Fragmented Procurement Processes Within Italian Public Sector | -0.5% | Municipal and regional bodies | Medium term (2–4 years) |

| Legacy System Debt Slowing Enterprise Modernization Cycles | -0.6% | BFSI and Public Administration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Shortage Of Advanced ICT Skillsets In Domestic Labor Pool

Italy counted 135,000 unfilled ICT roles in 2025, while only 45.8% of citizens possessed basic digital skills.[2]European Commission, “DESI 2025 – Italy,” European Commission, ec.europa.eu STEM graduation flows cover less than half of annual retirements, and brain drain siphons talent to higher-wage EU markets. ITS Academy programs co-designed with Engineering, Reply, and Accenture enrolled 18,000 students in 2025, well below the 50,000 target. The scarcity inflates contractor pricing, slows project delivery, and forces near-shore or offshore outsourcing, diluting domestic value capture in the Italy ICT market.

High Electricity Costs Impacting Data Center Economics

Industrial power averaged EUR 0.25-0.30 per kWh in 2025, double the EU mean. A 20 MW hyperscale facility incurs more than EUR 50 million (USD 56 million) in annual electricity outlays, prompting providers to erect on-site solar arrays or sign long-term power-purchase agreements. Aruba installed 10 MW of rooftop photovoltaics and locked in a 15-year wind PPA, trimming energy expense by 35%. Equinix postponed its ML2 expansion because Milan’s electricity rates undercut return thresholds compared with Frankfurt and Amsterdam. Elevated power tariffs accelerate cloud migration yet squeeze colocation demand and hardware refresh cycles in the Italy ICT market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cloud Momentum Recasts Traditional Service Mix

IT Services accounted for 27.31% of the Italy ICT market size in 2025, anchored by multi-year system-integration projects that migrate ERP, CRM, and core-banking stacks to cloud-ready architectures. Accenture, IBM, and Capgemini secured headline contracts with Intesa Sanpaolo, Generali, and Enel to re-platform legacy workloads and deploy ServiceNow and Salesforce suites. Yet Cloud and Platform Services outpace every other category, logging an 8.46% CAGR that recalibrates vendor revenue toward usage-based models. AWS processed more than 1 exabyte of data through its Milan region in 2025, while Microsoft Azure and Google Cloud added sovereign instances to satisfy NIS2 residency clauses. Hardware demand stabilizes as virtualization and containerization compress server counts although Wi-Fi 6E, SD-WAN appliances, and next-gen firewalls preserve network-gear turnover. Subscription-based SaaS replaces perpetual licenses across collaboration, security, and line-of-business apps, reshaping balance sheets from capital to operating expense.

Enterprises increasingly standardize on Kubernetes orchestration and adopt abstraction layers that permit workload mobility between on-premises clusters, colocation cages, and hyperscale regions. That flexibility moderates vendor lock-in and enables cost arbitrage via reserved-instance marketplaces. The Italy ICT market thus rewards providers that couple local compliance assurances with global service catalogs spanning AI-ML, data lakes, and low-code development. Concurrently, zero-trust architectures and privileged-access management solutions grow in tandem with distributed cloud footprints.

By Enterprise Size: SMEs Close The Digital Gap At Speed

Large enterprises accounted for 64.68% of spending in 2025, reflecting capital depth and scale advantages that unlock volume discounts and specialized skill sets. UniCredit and Intesa Sanpaolo each invested more than EUR 500 million (USD 581.61 million) per year in digital programs, swapping monolithic cores for microservices and Kafka streams to enable real-time fraud detection. Yet SMEs, stimulated by Transition 4.0 credits, expand at an 8.27% CAGR, capturing an incremental share of the Italy ICT market. Government-funded Digital Innovation Hubs completed over 12,000 maturity assessments, mapping technology roadmaps, and brokering proofs of concept for cloud ERP, CRM, and e-commerce platforms.[3]Ministry of Economic Development, “Transition 4.0 Incentives,” Ministry of Enterprises and Made in Italy, mise.gov.it

SMEs still struggle with limited in-house expertise and budget constraints, prompting them to adopt bundled managed service offers. Vodafone Business combines Microsoft 365, Intune mobile-device management, and endpoint security with 24/7 support, creating an opex-friendly per-seat model. TIM Enterprise layers SOC-as-a-Service and threat-intel feeds atop connectivity, while Aruba provides green data-center hosting powered by solar offsets. Vertical SaaS for retail, hospitality, and micro-manufacturing further lowers barriers, delivering pre-configured workflows without custom coding.

By Industry Vertical: Manufacturing Surges Beyond BFSI Maturity

BFSI retained an 18.13% share of the Italy ICT market in 2025, propelled by open-banking APIs mandated under PSD2 and digital payment volumes exceeding 5 billion transactions via Nexi rails. Core-system modernization unlocks agile product launches and AI-based underwriting, yet growth now plateaus as incumbents near saturation in cloud migration. Manufacturing and Industry 4.0, by contrast, expands at 9.16% CAGR on tax-credit momentum and competitive imperative to digitize shop floors. Stellantis and Leonardo use cobots and digital twins to squeeze cycle times, while mid-tier machine builders integrate IoT telemetry into MES dashboards.

Public Administration ramps up cloud spending through the Polo Strategico Nazionale, complemented by SPID digital identity penetration that surpassed 32 million users. Energy and Utilities pilot smart-grid orchestration and DER management, and Telecom carriers virtualize network functions to support low-latency 5G services. Retail and logistics embrace omnichannel stacks that unify inventory and last-mile fulfillment, supported by warehouse automation. Healthcare accelerates telemedicine and AI-assisted diagnostics under parity reimbursement rules, expanding the TAM for secure connectivity, edge computing, and data analytics within the Italy ICT market.

Geography Analysis

Northern Italy represented the single largest contributor to the Italy ICT market in 2025, buoyed by Lombardy, Piedmont, Veneto, and Emilia-Romagna, which together yield 55% of national industrial output. Fiber-to-the-premises coverage reached 70% in the North against the 59.6% national baseline, ensuring low-latency access to hyperscale regions clustered around Milan. The metro hosts dual AWS availability zones, Azure nodes, Google Cloud PoPs, and more than 100 MW of colocation capacity across Aruba, Equinix, and Retelit sites. Higher GDP per capita of EUR 38,000 (USD 42,560) underwrites advanced analytics, AI automation, and zero-trust security rollouts.

Central Italy, led by Lazio and Tuscany, claims a sizable public-sector footprint as ministries migrate workloads to the sovereign cloud and expand SPID usage. The region’s ICT outlays grow at mid-single-digit rates through 2031 as the Polo Strategico Nazionale mandates 75% public-sector migration by 2026.[4]Agenzia per l’Italia Digitale, “Piano Triennale 2024-2026,” AGID, agid.gov.it Fragmented procurement across 20 regional administrations, however, slows standardization and bulk purchasing, tempering scale economies and elongating sales cycles.

Southern Italy and the islands trail on connectivity and per-capita spend but receive 40% of NRRP infrastructure funds, targeting 8.5 million premises in white and gray areas. Fiber coverage at 40% and GDP per capita of EUR 19,000 (USD 21,280) currently limit advanced ICT uptake. Nonetheless, the youthful demographic median age 42 vs 47 in the North presents a long-term skills-development upside. As connectivity improves, the Italy ICT market size attributable to the South is projected to outgrow the national average, powered by SME cloud adoption and remote-work enablement.

Competitive Landscape

The Italy ICT market is moderately fragmented, and the top 10 suppliers account for a major share of combined revenue. Global integrators Accenture, IBM, Capgemini, and DXC dominate large-enterprise and public-sector contracts, leveraging offshore delivery centers to achieve cost efficiency. Domestic champions Engineering Ingegneria Informatica, Reply, Almaviva, and Dedagroup win mid-market deals through proximity, Italian-language support, and familiarity with regional regulations. Hyperscalers expand their local availability zones and partner with these integrators to meet NIS2 data-sovereignty requirements.

White-space opportunities persist in managed security services for SMEs, vertical SaaS, and manufacturing edge-computing platforms. Cloud-native disruptors such as Scalapay, Satispay, and Prima Assicurazioni exploit API-driven architectures to bypass legacy constraints and capture niche demand. Vendors embed AI in ERP for demand forecasting, CRM for lead scoring, and SOC platforms for anomaly detection. Microsoft’s 2025 patent filings for AI-assisted code generation suggest an impending low-code future that will reduce skill barriers. Pricing pressure, however, remains acute as hyperscalers perpetually lower unit compute and storage costs, compressing integrator margins unless value-added analytics or industry expertise accompanies resell agreements.

Vendor partnerships trend toward co-innovation, Google Cloud and Engineering operate a sovereign stack, AWS collaborates with Poste Italiane on low-latency fintech workloads, and Microsoft allies with Telecom Italia to deliver AI skilling across the peninsula. Outbound M&A is selective, focusing on cybersecurity boutiques and data-analytics specialists that strengthen portfolio depth. Meanwhile, green-energy sourcing differentiates colocation providers as ESG-conscious clients embed scope-2 emission clauses in RFPs.

Italy ICT Industry Leaders

IBM Corporation

Accenture plc

Cisco Systems, Inc.

Engineering Ingegneria Informatica S.p.A.

Capgemini SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Microsoft confirmed a EUR 4.3 billion (USD 4.3 billion) investment to expand Azure capacity and train 1 million citizens in AI and cloud skills.

- September 2025: AWS opened a second Milan availability zone, lifting regional compute and storage capacity by 40%.

- August 2025: Nexi integrated its payment rails with the ECB’s TARGET Instant Payment Settlement system, enabling real-time cross-border euro transfers.

- July 2025: Stellantis committed EUR 2 billion (USD 2.37 billion) to digitize Mirafiori and Melfi plants, deploying cobots, AGVs, and SAP Digital Manufacturing Cloud.

Italy ICT Market Report Scope

The Italy ICT market report provides comprehensive insights, including market size and forecasts, segment analyses by product type, enterprise size, industry vertical, and deployment mode. It highlights key trends and growth drivers, such as digital transformation and smart city initiatives. The report also provides an in-depth overview of ICT infrastructure, focusing on advancements such as 5G and fiber-optics. Furthermore, it examines government initiatives and investment programs, alongside a detailed assessment of market opportunities and challenges for businesses.

The Italy ICT Market Report is Segmented by Product Type (IT Hardware, IT Software, IT Services, IT Infrastructure, IT Security/Cybersecurity, Communication Services), Enterprise Size (Small and Medium-sized Enterprises, Large Enterprises), Industry Vertical (Government and Public Administration, BFSI, IT and Telecom, Energy and Utilities, Retail E-commerce and Logistics, Manufacturing and Industry 4.0, Healthcare and Life Sciences, Oil and Gas, Other Industry Verticals). The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| IT Infrastructure | |

| IT Security/Cybersecurity | |

| Communication Services |

By Enterprise Size

| Small and Medium-sized Enterprises |

| Large Enterprises |

By Industry Vertical

| Government and Public Administration |

| BFSI |

| IT and Telecom |

| Energy and Utilities |

| Retail, E-commerce, and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| Oil and Gas |

| Other Industry Verticals |

| By Product Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | IT Consulting and Implementation | |

| IT Outsourcing (ITO) | ||

| Business Process Outsourcing (BPO) | ||

| Managed Security Services | ||

| Cloud and Platform Services | ||

| IT Infrastructure | ||

| IT Security/Cybersecurity | ||

| Communication Services | ||

| By Enterprise Size | Small and Medium-sized Enterprises | |

| Large Enterprises | ||

| By Industry Vertical | Government and Public Administration | |

| BFSI | ||

| IT and Telecom | ||

| Energy and Utilities | ||

| Retail, E-commerce, and Logistics | ||

| Manufacturing and Industry 4.0 | ||

| Healthcare and Life Sciences | ||

| Oil and Gas | ||

| Other Industry Verticals | ||

Key Questions Answered in the Report

What is the current value of the Italy ICT market?

The Italy ICT market size reached USD 92.74 billion in 2026.

How fast is the sector expanding?

It is forecast to grow at a 7.34% CAGR between 2026 and 2031.

Which product segment is growing the quickest?

Cloud and Platform Services post the highest growth at an 8.46% CAGR through 2031.

Why are SMEs adopting digital technology now?

Transition 4.0 tax credits reimburse up to 40% of machinery and 20% of software spend, lowering SME entry barriers and pushing their ICT outlays at an 8.27% CAGR.

Which region leads on ICT spending?

Northern Italy commands the largest share, supported by dense manufacturing clusters and superior fiber coverage.

What is the main challenge facing data centers?

Industrial electricity prices averaging EUR 0.25-0.30 per kWh double the EU mean, inflating operating costs and delaying facility expansion.

Page last updated on: