Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Italy Data Center Storage Market is Segmented by Storage Technology (Network-Attached Storage, Storage Area Network, and More), Storage Type (Traditional HDD Arrays and More ), Data Center Type (Colocation Facilities and More), End User (IT and Telecommunication, BFSI and More), Form Factor (Rack-Mounted and More), Interface(sas / SATA, Nvme, Fibre Channel and ISCSI). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

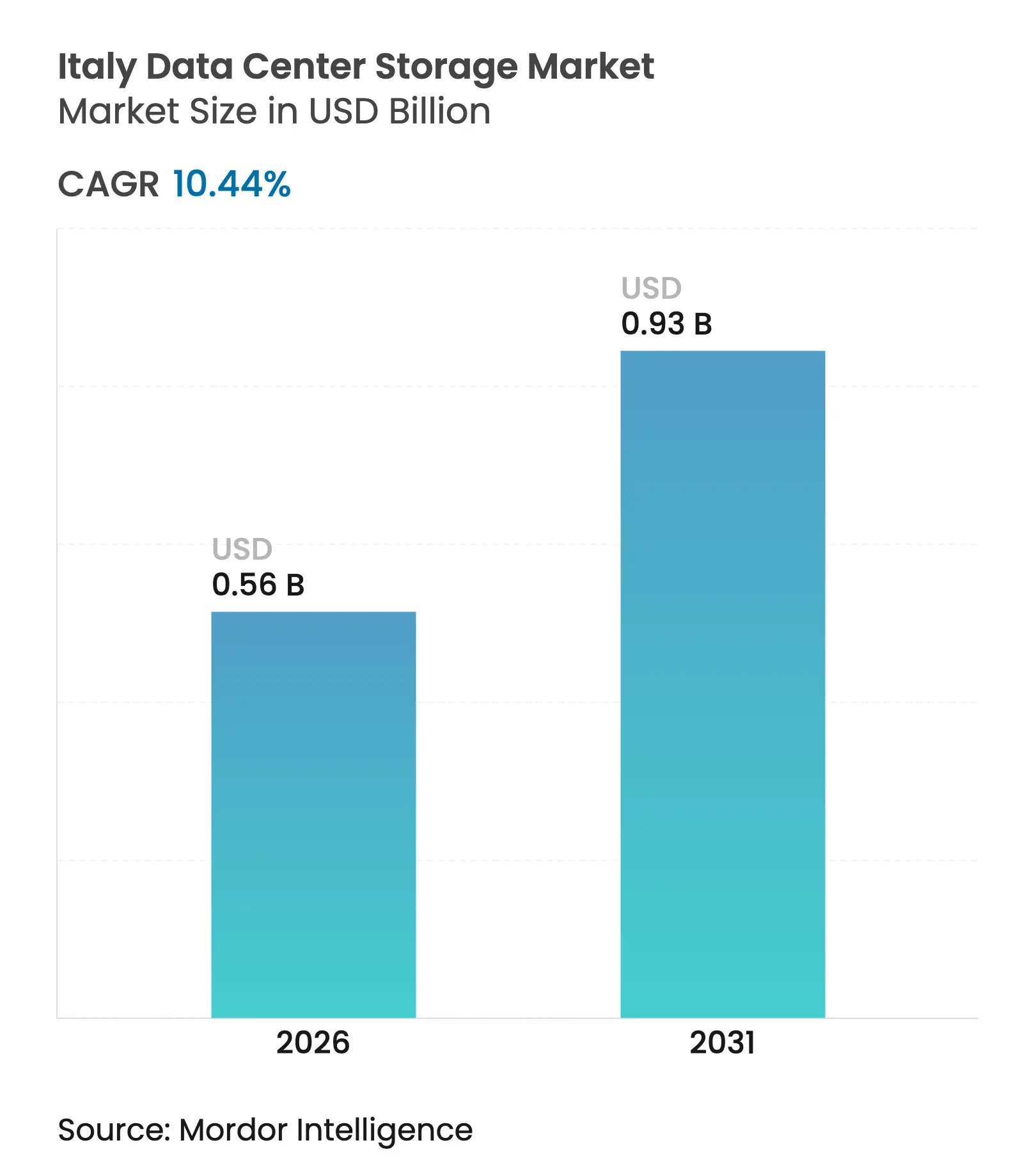

| Market Size (2026) | USD 0.56 Billion |

| Market Size (2031) | USD 0.93 Billion |

| Growth Rate (2026 - 2031) | 10.44 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Italy data center storage market size in 2026 is estimated at USD 0.56 billion, growing from 2025 value of USD 0.51 billion with 2031 projections showing USD 0.93 billion, growing at 10.44% CAGR over 2026-2031. The jump reflects sustained government digital-sovereignty programs, a national pivot to cloud, and a wave of storage-intensive AI workloads. Hyperscaler entrance, 71 GWh of grid-storage auctions for on-site renewables, and a clear shift toward energy-efficient, high-density arrays combine to lift capacity demand and compress operating costs. Storage Area Networks remain dominant thanks to entrenched enterprise architectures, yet Network Attached Storage is scaling faster as distributed teams and edge locations proliferate. All-flash arrays are taking share from HDD arrays as power-per-IOPS advantages outweigh their capital premium, especially in regions with high electricity tariffs. Competitive intensity is moderate: global incumbents retain channel depth while local integrators secure public sector projects under the Polo Strategico Nazionale framework.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Surge in cloud and hyperscale build-outs Surge in cloud and hyperscale build-outs | +2.8% | National, concentrated in Milan, Rome, Naples | Medium term (2-4 years) | (~)% Impact on CAGR Forecast:

+2.8%

|

Geographic Relevance

:

National, concentrated in Milan, Rome, Naples

|

Impact Timeline

:

Medium term (2-4 years)

|

Shift toward energy-efficient, high-density designs

Shift toward energy-efficient, high-density designs

| +2.1% | National, with early adoption in Northern Italy | Long term (≥ 4 years) | |||

Rapid adoption of all-flash and NVMe arrays Rapid adoption of all-flash and NVMe arrays | +1.9% | National, enterprise-led in Lombardy, Lazio | Short term (≤ 2 years) | |||

71 GWh grid-storage auctions enabling on-site renewables

71 GWh grid-storage auctions enabling on-site renewables

| +1.4% | National, with focus on Southern Italy solar integration | Long term (≥ 4 years) | |||

Underground/mine data-center projects lowering PUE

Underground/mine data-center projects lowering PUE

| +1.2% | Regional, concentrated in Alpine and Apennine regions | Medium term (2-4 years) | |||

Digital-sovereignty push via "Polo Strategico

Nazionale"

Digital-sovereignty push via "Polo Strategico

Nazionale"

| +1.1% | National, government-led initiatives | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Surge in Cloud and Hyperscale Build-outs

Record cloud capital expenditure exceeding USD 215 billion in 2025 is pushing hyperscalers to place Italian availability zones close to end users and within EU data-residency rules. [1]Diana Goovaerts, “AWS, Azure lead hyperscale investment surge,” Fierce Network, fiercewireless.com Regional footprints demand petabyte-class storage clusters that can elastically scale across Milan’s carrier hotels and Rome’s government clouds. Domestic sovereignty clauses mandate that these new zones leverage locally controlled storage nodes, stimulating procurement of high-performance SAN and NAS gear. Dense wavelength division multiplexing backbones, forecast to top USD 3 billion in spend by 2029, further lower latency and make edge replication economical. Together, these factors swell the Italy data center storage market as providers race to meet service-level guarantees.

Shift toward Energy-Efficient, High-Density Designs

Electricity prices running 30-40 % higher than the EU mean make power efficiency a board-level variable. Dell Technologies’ Concept Astro platform uses digital twins to model workload power draw and cut consumption in live clusters. Operators in Turin and Bologna have begun pairing the software with immersion cooling and liquid-to-rack loops, compressing footprints while beating stringent PUE targets. Higher-density drives and dual-actuator HDDs also lift per-rack capacity, critical in metro colocation sites where real estate is scarce. As emission ceilings tighten under EU ETS Phase 4, energy-optimized arrays provide a compliance hedge and accelerate refresh cycles.

Rapid Adoption of All-Flash and NVMe Arrays

Latency-sensitive AI inference and real-time fraud analytics are fueling enterprise adoption of NVMe over Fibre Channel, now fully supported in Red Hat Enterprise Linux kernels.[2]Red Hat Documentation Team, “NVMe over Fibre Channel Technology Preview,” Red Hat, redhat.com Performance per watt improves by up to 3 times, offsetting Italy’s high utility rates and shrinking rack counts in legacy data halls. Flexible namespaces allow the same fabric to serve block and file workloads, simplifying operations for stretched IT teams. These benefits continue to pull capital away from spinning disk arrays and enlarge the Italy data center storage market footprint in flash.

71 GWh Grid-Storage Auctions Enabling On-Site Renewables

Government-run auctions earmarking 71 GWh of battery storage are unlocking co-located solar plus storage configurations, especially across Campania and Sicily. Data-center operators can arbitrage daytime PV surpluses, charging lithium-ion banks and discharging during evening peaks, shaving utility bills by up to 18 %. Enhanced geothermal systems under pilot near L’Aquila promise an additional baseload option, echoing renewable sourcing models adopted by global tech majors.[3]Global Energy Monitor Staff, “Enhanced Geothermal Systems for Data Centers,” Global Energy Monitor, globalenergymonitor.org The synergy of on-site batteries and high-density flash arrays reduces both space and cooling demand, aligning with Italy’s 55 % emissions-reduction pledge for 2030. Long-duration storage in turn improves uptime metrics, a key selling point for sovereign cloud deals.

Restraint Impact Analysis

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Skills and cyber-security talent shortage Skills and cyber-security talent shortage | -1.8% | National, acute in Southern Italy | Short term (≤ 2 years) | (~)% Impact on CAGR Forecast:

-1.8%

|

Geographic Relevance

:

National, acute in Southern Italy

|

Impact Timeline

:

Short term (≤ 2 years)

|

Electricity prices 30-40% above EU peers

Electricity prices 30-40% above EU peers

| -1.5% | National, most severe in industrial regions | Medium term (2-4 years) | |||

Regulatory vacuum delaying facility permits

Regulatory vacuum delaying facility permits

| -1.1% | National, varying by regional authorities | Short term (≤ 2 years) | |||

SSD/NAND price volatility and supply-chain risk SSD/NAND price volatility and supply-chain risk | -0.9% | Global impact, affecting Italian procurement | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Skills and Cyber-Security Talent Shortage

Italian operators face a limited pool of storage architects and security analysts, with salaries reaching EUR 100,000 for senior roles. Competition from Northern European employers exacerbates churn, delaying roll-outs of encrypted, sovereign-grade arrays. Many mid-market firms now outsource Level 2 operations to managed-service providers, raising opex and diluting in-house expertise. Training pipelines lag demand, particularly in Southern campuses where curricula still emphasize traditional engineering over cloud disciplines. Unless reskilling accelerates, the Italy data center storage market may see project backlogs and lower utilization in freshly built halls.

Electricity Prices 30-40 % Above EU Peers

Wholesale power tariffs hovering around EUR 150 /MWh during summer peaks inflate total cost of ownership for IOPS-hungry workloads. Operators respond by under-clocking controllers and delaying flash migrations, capping immediate revenue upside. High tariffs also skew hyperscaler site-selection models toward France or Spain, potentially tempering inbound investment momentum. While corporate PPAs and capacity-market incentives soften the blow, volatility compels finance teams to hedge energy exposure, diverting cash from capacity expansion. Persistent price gaps could shave 150-200 basis points off the projected CAGR if left unaddressed.

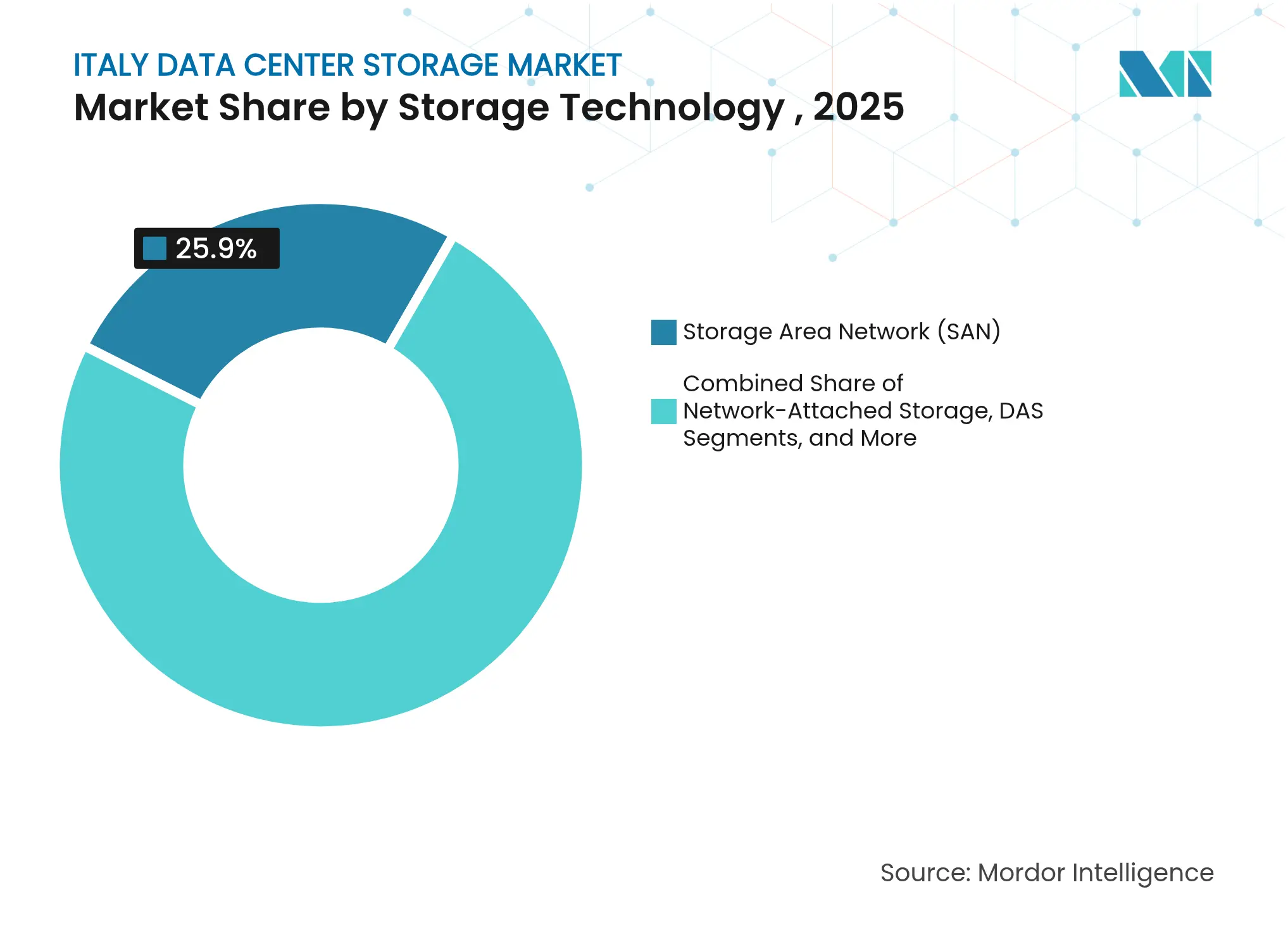

By Storage Technology: SAN Endurance Meets NAS Momentum

Storage Area Networks contributed 25.90% to Italy's data center storage market share in 2025 due to their fibre-channel reliability in banking, telecom, and public-sector deployments. Many Milanese banks attach tier-1 databases to redundant SAN fabrics for sub-millisecond latency guarantees. Yet NAS platforms, expanding at an 11.16 % CAGR, are closing the gap by offering scale-out file services ideal for video production in Rome’s media corridors. Vendors bundle SMB and NFS protocols with snapshot replication, easing hybrid-cloud collaboration. As containerized microservices multiply, NAS architectures add S3-compatible object gateways, further broadening appeal.

A parallel SAN upgrade cycle is underway: dual-100 Gbps fabrics and NVMe-FC transports lift throughput sixfold, extending the life of centralized designs. Converged management panes now surface telemetry across SAN and NAS arrays, aiding rightsizing efforts amid fluctuating AI training loads. With regulatory archives moving to object storage, certain workloads will migrate off SAN; however, mission-critical OLTP databases should keep SAN revenue steady through 2031.

Note: Segment shares of all individual segments available upon report purchase

By Storage Type: Flash Upswing Against HDD Capacity Pools

Traditional HDD arrays held 42.60% of the Italy data center storage market size in 2025, favored for sequential-heavy workloads such as video archiving and CCTV retention. Nevertheless, all-flash arrays, forecast to post a 11.86 % CAGR, are capturing OLTP, VDI, and AI inference tiers. Power per TB drops by as much as 65 % relative to 10 K RPM disks, an attractive proposition given national electricity premiums.

Hybrid arrays remain a bridge technology: Automated tiering places cold data on helium HDDs while hot datasets sit on TLC flash, easing capital budgets. Italian buyers pursuing cloud-first strategies still deploy local HDD pools for data-sovereignty backups, but de-duplication ratios in flash systems narrow the cost delta each year.

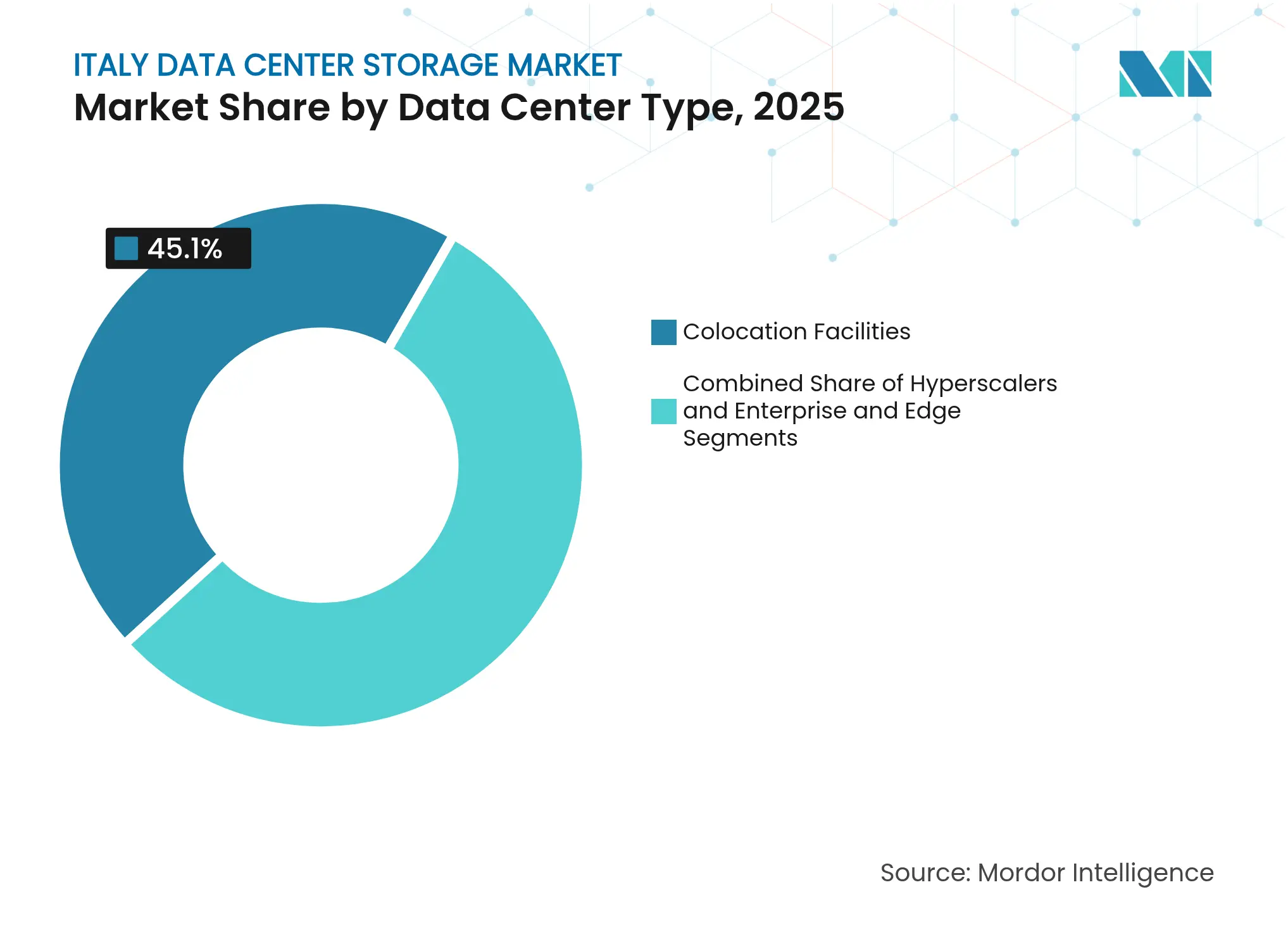

By Data Center Type: Colocation Strength with Hyperscale Tailwind

Colocation sites represented 45.10% of the Italy data center storage market in 2025 due to carrier-neutral ecosystems around Via Caldera and east Rome. These facilities bundle multi-cloud connectivity, easing hybrid-IT adoption for mid-size corporations wary of full cloud repatriation risks. Power-dense cabinets exceeding 20 kW host all-flash rigs that shrink footprint fees. Meanwhile, hyperscalers are scaling Italian footprints at a 12.58 % CAGR, lured by government incentives and Southern solar yields. Edge micro-data centers, often containerized, emerge along 5G corridors in Apulia and Veneto to serve latency-critical IoT applications.

Enterprise on-prem halls, once the default, now specialize in regulatory workloads requiring air-gapped isolation. Their share declines incrementally but remains relevant in defense and critical-infrastructure contexts. As sovereign cloud regions open, colocation firms partner with international operators to deliver in-country availability zones, preserving colocation’s central role in the Italy data center storage market.

Note: Segment shares of all individual segments available upon report purchase

By End User: Telecom Dominance, BFSI Ascent

IT and Telecommunications providers controlled 25.20% of 2025 revenue, reflecting heavy investment by mobile operators rolling out 5G core networks that demand scale-out storage for subscriber data. Network function virtualization offloads call-detail records to NVMe arrays, cutting read times for analytics. Banking, financial services, and insurance are on course for an 11.24 % CAGR as digital-only banks drive always-on requirements. Open-banking APIs and real-time fraud detection send transaction bursts reaching hundreds of thousands of IOPS, ideal for flash.

Government workloads expand under the Polo Strategico Nazionale, where encrypted SANs host citizen-data lakes. Media firms in Turin leverage scalable NAS to deliver UHD content, while healthcare authorities migrate PACS imaging to object storage clusters for GDPR-compliant retention. Manufacturing plants in Emilia-Romagna collect IIoT sensor streams, feeding predictive-maintenance platforms and lifting localized edge-storage demand.

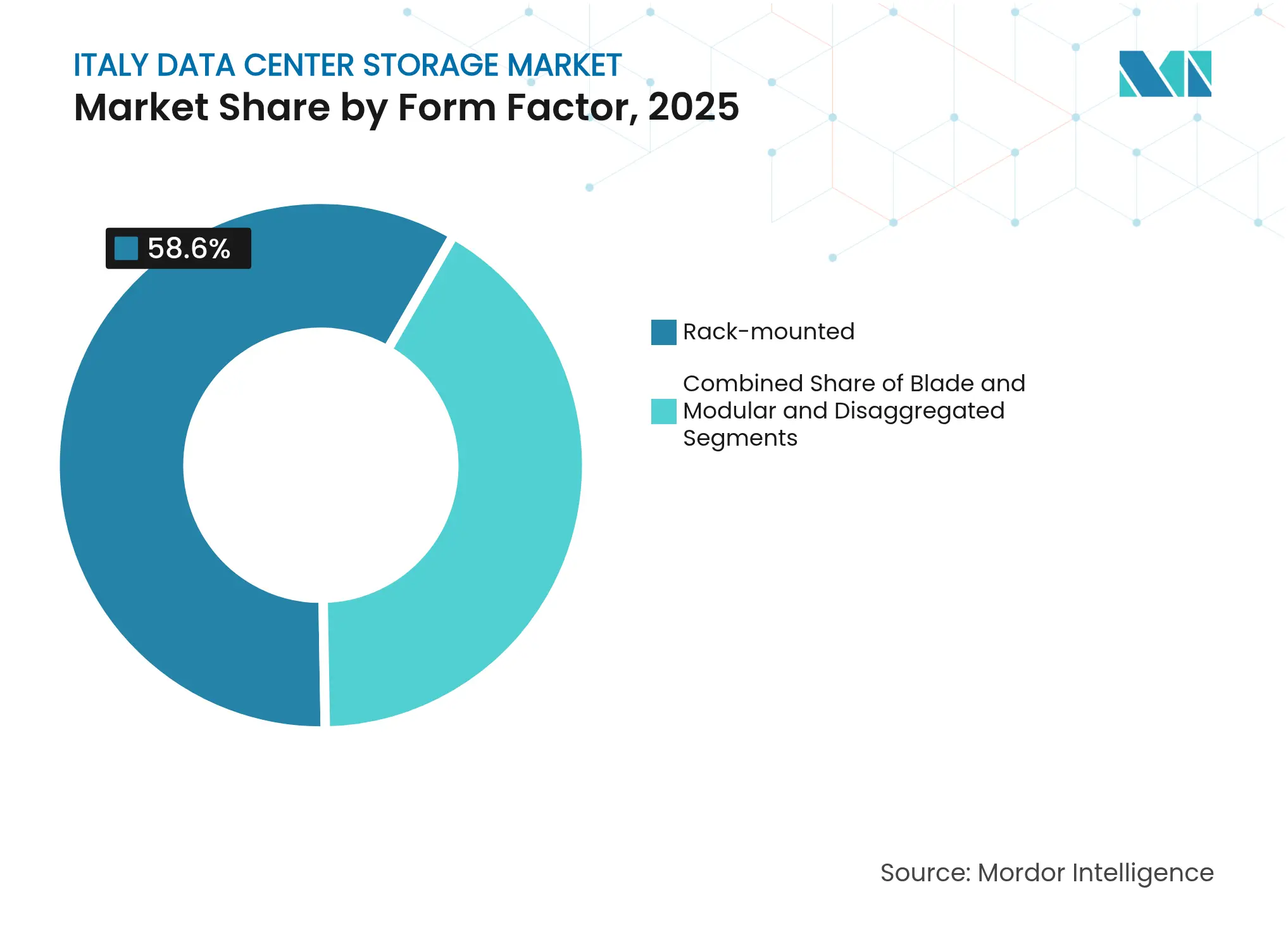

By Form Factor: Rack-Mounted Rule, Composable Breakthrough

Rack-mounted hardware owned 58.60% market share in 2025 as traditional 2U and 4U chassis align with standardized colocation cabinets. Cable familiarity and mature tooling keep change windows short. Disaggregated and composable architectures, rising at a 11.68 % CAGR, decouple flash pools from compute nodes so resources scale independently. Early adopters in Bologna leverage PCIe fabric switching to reassign drives between AI inference clusters and analytics farms in minutes, boosting utilization.

Blade enclosures find niche use in space-constrained edge pods where airflow is limited. Modular micro-data centers, pre-integrated with lithium-ion UPS and liquid cooling, ship to mining-conversion projects in Sardinia, turning dormant tunnels into secure storage bunkers. Over time, software-defined composable frameworks may erode rack-mount dominance, yet interoperability hurdles keep the transition measured, ensuring both designs coexist in the Italy data center storage market.

Note: Segment shares of all individual segments available upon report purchase

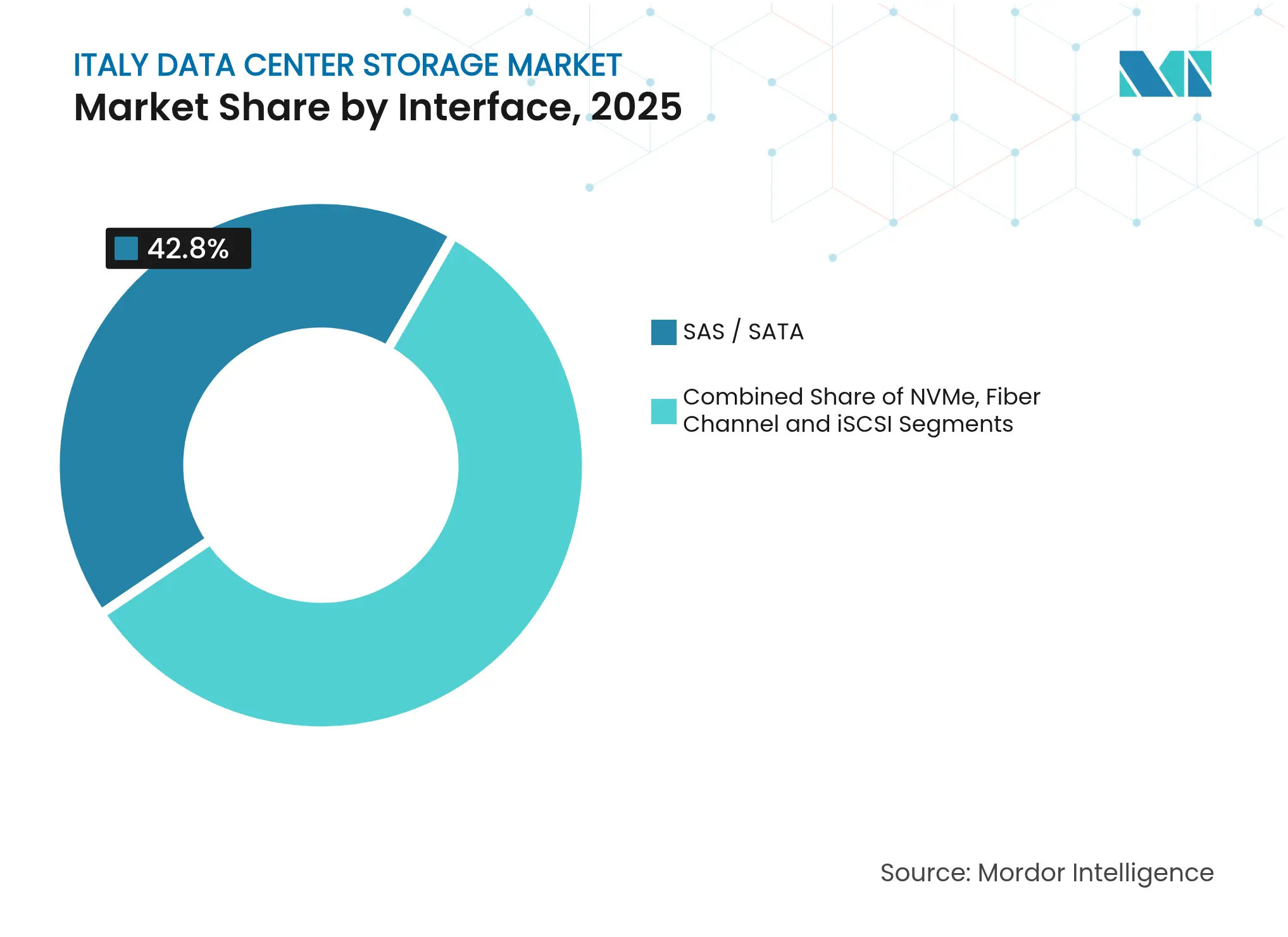

By Interface: Legacy Reliability Meets NVMe Disruption

SAS / SATA protocols retained 42.80% of 2025 shipments because decades-old toolchains remain entrenched in enterprise change-control policies. Mixed-mode controllers accepting both interfaces aid gradual flash adoption. NVMe’s 10.62 % CAGR, however, underscores growing demand for 1 M IOPS per shelf to support AI model inferencing and microsecond trading needs. Firmware-level dual-porting plus native namespace management strengthen NVMe’s enterprise fit, correcting early perceptions of scale complexity.

Fibre Channel endures in regulated verticals, its deterministic latency prized by Milan’s stock exchange. Conversely, iSCSI’s cost-effective Ethernet fabric attracts SMBs migrating to 25 Gbps switches. As switch-ASIC roadmaps tick up to 400 Gbps, NVMe-over-TCP stands to siphon volumes from legacy stacks, shrinking East-West latency penalties and fuelling further Italy data center storage market growth.

Note: Segment shares of all individual segments available upon report purchase

Northern Italy commands the bulk of installed capacity, with Lombardy alone hosting more than one-third of active racks. Abundant fiber backbones and proximity to pan-European transit routes draw hyperscalers seeking sub-20 ms latency to Frankfurt and Marseille. The region also secures preferential access to cross-border hydropower, trimming energy premiums and encouraging flash-dense retrofits. Rome and the wider Lazio area follow as government agencies migrate workloads under sovereign-cloud mandates, spurring NAS and object-storage orders within ministerial clouds.

Southern provinces such as Campania, Puglia, and Sicily are emerging growth corridors. Lower land costs and abundant solar irradiation allow large-footprint campuses with battery-assisted peak-shaving. Palermo’s new submarine-cable landing station positions the island as a gateway for North-African traffic, injecting fresh demand for edge-cache clusters. Underground facilities in the Apennines exploit stable ambient temperatures, achieving PUE figures below 1.2 and attracting archival storage customers sensitive to power bills; these sites already pilot disaggregated NVMe pools to further optimize watt-per-TB metrics.

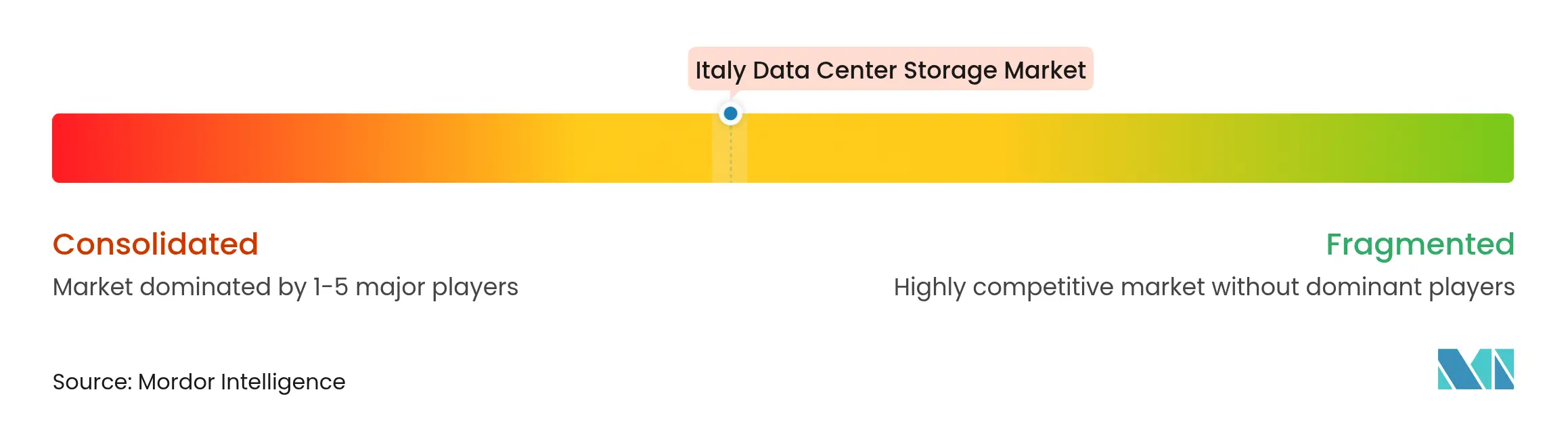

Market Concentration

Global vendors maintain the lion’s share of hardware revenue yet increasingly partner with local systems integrators to satisfy data-sovereignty clauses. Dell Technologies, NetApp, and Pure Storage leverage established channels to sell SAN, NAS, and all-flash platforms into regulated industries. Their differentiators include on-device encryption, NVMe-over-FC roadmaps, and energy-optimization engines such as Dell’s Concept Astro, which models power draw and dynamically throttles controllers to cut consumption by double digits.

Emerging disruptors focus on narrow slices: start-ups based in Turin ship composable NVMe-over-TCP appliances, while a Rome-based scale-out-file vendor aligns its metadata architecture with sovereign-cloud policy requirements.

Strategic moves underline a pivot toward services. NetApp rolled out pay-as-you-grow Keystone financing in Milan, easing cash-flow pressures for mid-caps that want flash but lack capex. Pure Storage doubled its European capacity for Evergreen//One, guaranteeing 99.999% availability backed by on-site spares. Local integrators combine these offerings with managed compliance monitoring, giving public-sector clients a single throat to choke. The result is a competitive yet collaborative environment that propels the Italy data center storage market toward solution-centric value propositions rather than raw hardware counts.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Market Definitions and Key Coverage

Segmentation Overview

Detailed Research Methodology and Data Validation

Primary Research

Desk Research

Market-Sizing & Forecasting

Data Validation & Update Cycle

Why Our Italy Data Center Storage Baseline Commands Confidence

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 0.51 B (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 7.70 B (2024) | Global Consultancy A | Combines servers, network, and storage; investment rather than revenue viewpoint | ||

USD 1.29 B (2033) | Trade Journal B | Uses long-range projection back-casted to 2024; limited primary validation |

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

US Market Entry for Taiwanese Machine Tool Manufacturers

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.