Europe Fixed Wireless Access (FWA) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

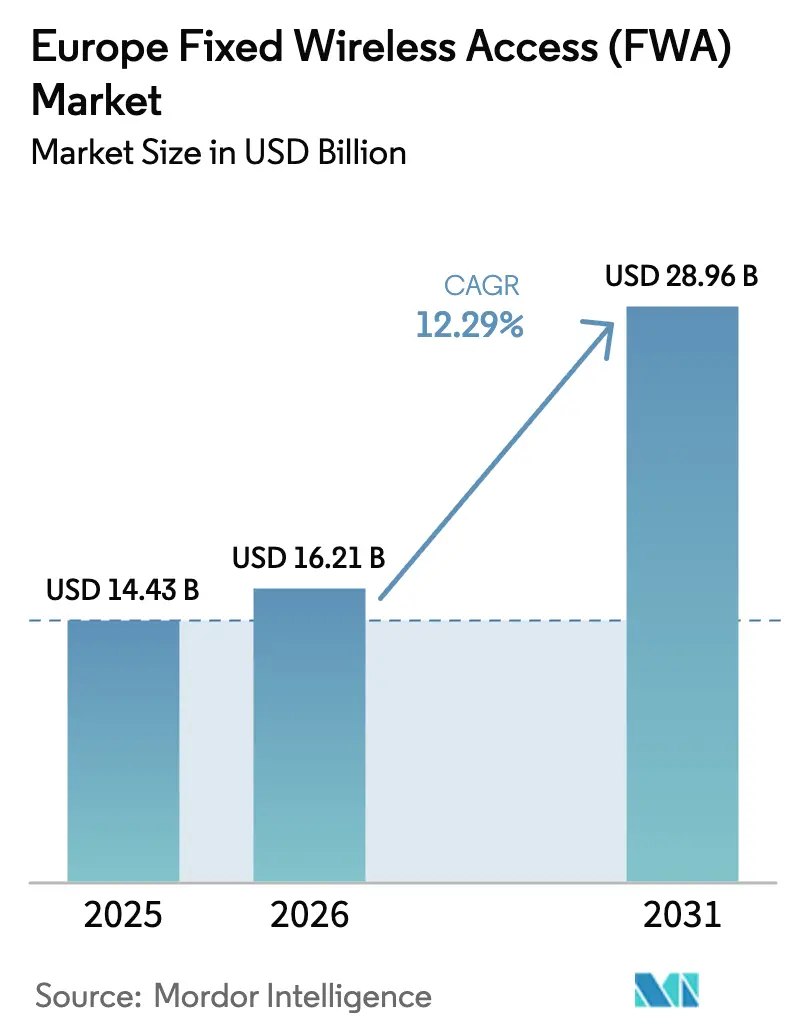

| Base Year Market Size (2025) | USD 14.43 Billion |

| Market Size (2026) | USD 16.21 Billion |

| Market Size (2031) | USD 28.96 Billion |

| Growth Rate (2026 - 2031) | 12.29% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Fixed Wireless Access (FWA) Market Analysis by Mordor Intelligence

The Europe Fixed Wireless Access market size is expected to grow from USD 14.43 billion in 2025 to USD 16.21 billion in 2026 and is forecast to reach USD 28.96 billion by 2031 at 12.29% CAGR over 2026-2031. The outlook aligns with the European Union’s Gigabit Society mandate, which aims for universal gigabit-class connectivity by 2030 [1]European Commission, “Gigabit Society Policy Framework,” digital-strategy.ec.europa.eu. Operators view the technology as a pragmatic way to cover rural gaps more quickly and at a lower cost than fiber, while 5G standalone upgrades unlock network-slicing revenue streams that strengthen business cases. Germany leads current adoption because Deutsche Telekom accelerated 5G FWA buildouts across underserved municipalities. France is expanding the fastest as Orange deploys FWA in historic city centers, where fiber trenching often fails to clear municipal approvals. Hardware still dominates spending, but managed services tied to fixed-mobile convergence bundles are the fastest-growing revenue stream.

Key Report Takeaways

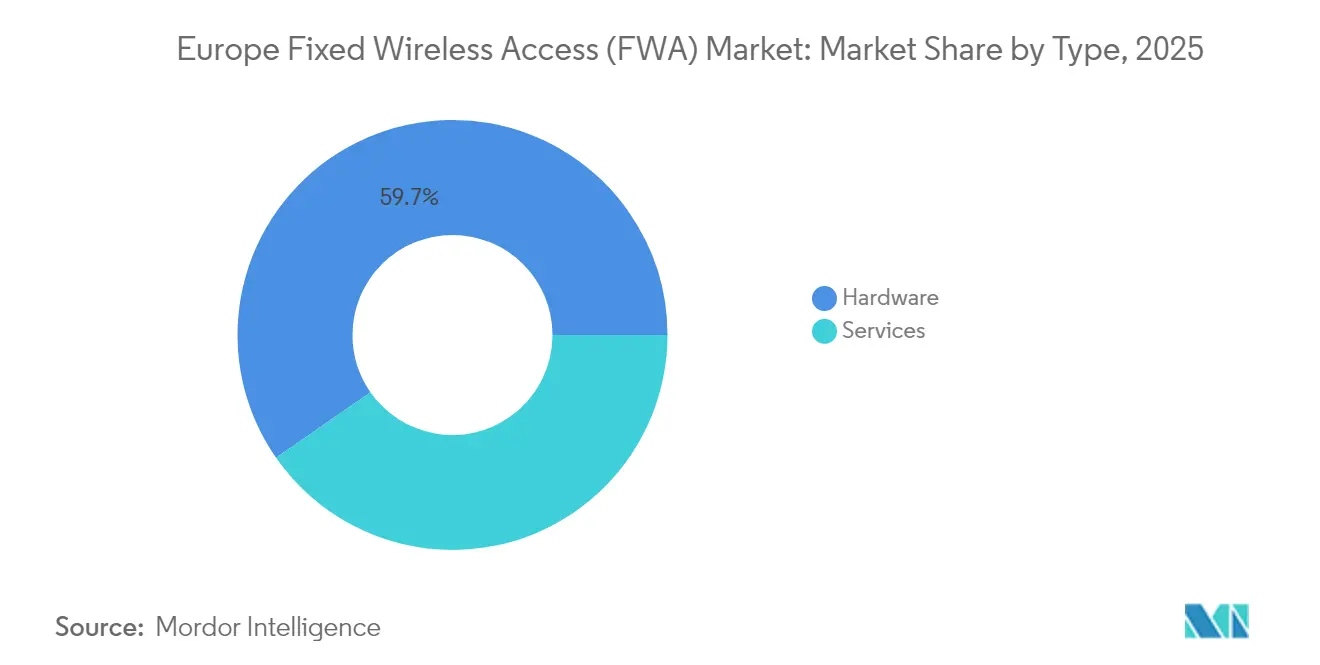

- By type, hardware commanded 59.68% of the European Fixed Wireless Access market share in 2025, while services are projected to advance at a 16.92% CAGR through 2031.

- By application, residential accounted for 53.12% of the European Fixed Wireless Access market size in 2025, and commercial deployments are projected to expand at a 15.86% CAGR through 2031.

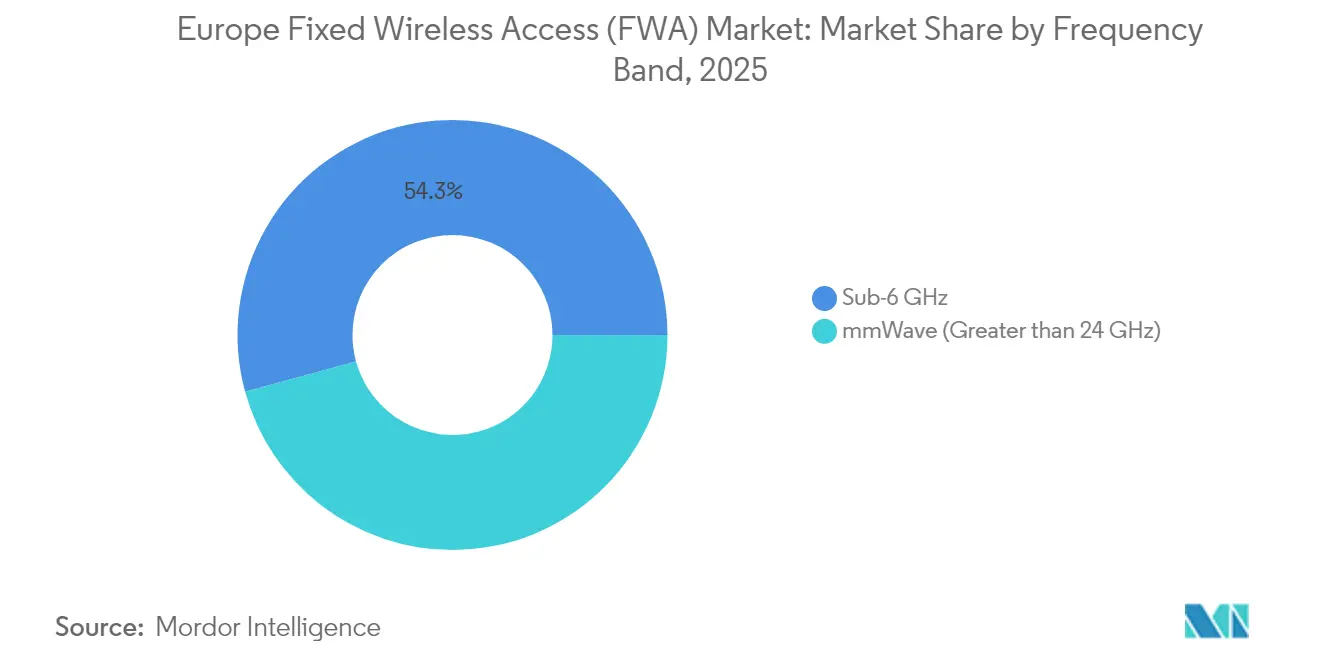

- By frequency band, Sub-6 GHz captured 54.25% of the European Fixed Wireless Access market share in 2025, while mmWave bands above 24 GHz are projected to grow at a 16.60% CAGR through 2031.

- By deployment mode, indoor CPE installations accounted for 59.74% of the European Fixed Wireless Access market size in 2025, whereas outdoor CPE is projected to grow at a 16.84% CAGR through 2031.

- By country, Germany led the European Fixed Wireless Access market with a 25.62% market share in 2025, and France is expected to show the highest forecast growth at a 15.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Fixed Wireless Access (FWA) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G SA roll outs accelerating C-band upgrades | +2.8% | Germany, France, Nordic region | Medium term (2-4 years) |

| National broadband targets and EU mandate | +2.1% | EU-wide, strongest in rural areas | Long term (≥ 4 years) |

| Cost-effective rural alternative to FTTH | +1.9% | Rural Germany, France, Italy | Medium term (2-4 years) |

| Fixed-mobile convergence bundles | +1.6% | Urban markets across major EU countries | Short term (≤ 2 years) |

| Private 5G networks for Industry 4.0 | +1.4% | Industrial regions in Germany, Netherlands | Medium term (2-4 years) |

| Energy-efficient Massive-MIMO CPE advances | +1.2% | Global, early adoption in Nordic countries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

5G SA Roll Outs Accelerating C-Band Upgrades

Standalone 5G cores enable carriers to utilize C-band spectrum without relying on 4G anchors, resulting in FWA downlink speeds that are up to 40% higher compared to non-standalone configurations. Deutsche Telekom completed nationwide SA coverage across 15 states in 2024, enabling network-slicing tiers that separate consumer, enterprise, and campus traffic for differentiated service quality. Orange followed with a France-wide SA core that supports premium guaranteed-bandwidth offers for business users at price points above standard fiber packages. Latency falls below 20 milliseconds, which expands the addressable pool of latency-sensitive applications that were historically reserved for dedicated fiber lines. The architecture also streamlines energy use, as a single 5G layer replaces the dual 4G/5G signaling, helping carriers meet their sustainability targets.

National Broadband Targets and EU Gigabit Society Mandate

The mandate requires every European household to access at least 1 Gbps by 2030, and it explicitly names FWA as an eligible technology. Member states have earmarked EUR 12.8 billion for rural connectivity grants, reimbursing up to 70% of project costs where population density falls below critical fiber thresholds. Italy alone allocates EUR 3.2 billion through 2026 to subsidize FWA in mountainous communes. The regulatory clarity accelerates spectrum auctions; all major markets now hold licenses in the 26 GHz band, giving operators consistent 400 MHz blocks needed for gigabit-class residential plans. Funding certainty shortens payback periods, encouraging multi-country rollouts rather than piecemeal pilots.

Cost-Effective Rural Last-Mile Alternative to FTTH

Vodafone’s field economics show rural FWA build costs average EUR 400 per premises passed, versus EUR 1,800 for FTTH in comparable terrain [2]Vodafone Group, “5G FWA Rural Deployment Economics,” vodafone.com. BT trials in Scotland confirm that one 5G site can cover 500 homes over a 5 km radius and break even at a 15% take-rate, while comparable fiber projects require a 40% penetration rate for cash-flow neutrality. Deployment cycles drop to 6-8 weeks, compared to 12-18 months for trenching, allowing operators to book revenue sooner and test price elasticity more quickly. The model also de-risks multi-tenant backhaul investments, as one tower serves multiple villages without requiring the digging of rights-of-way. As subsidies lower upfront costs, payback can compress to four years, solidifying ROI.

Fixed-Mobile Convergence Bundling by Telcos

Telcos pair FWA with unlimited mobile data to raise customer stickiness and curb churn. Telefónica’s Movistar Fusión bundle lifts average revenue per user by 23% over standalone mobile contracts [3]Telefónica S.A., “Movistar Fusión FWA Bundles 2024,” telefonica.com . Three UK reports show a 35% decline in churn where FWA is packaged with mobile and pay-TV. Shared spectrum and backhaul lower incremental cost, turning every 5G macro site into a dual-service asset. Bundling also neutralizes fiber rivals by allowing carriers to match triple-play offers without investing in new cable infrastructure. As more households adopt single-invoice plans, operators gain leverage in wholesale negotiations and spectrum renewals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent local cell-site zoning regulations | -1.8% | Urban heritage areas across the EU | Medium term (2-4 years) |

| mmWave backhaul CAPEX vs. fiber wholesale | -1.3% | Dense urban markets in the UK and Germany | Short term (≤ 2 years) |

| Line-of-sight constraints in heritage cores | -0.9% | Historic centers in Italy, France, Spain | Long term (≥ 4 years) |

| EMF-exposure public-opinion backlash | -0.7% | Switzerland plus pockets of Germany and France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Local Cell-Site Zoning Regulations

Municipal permits in historic districts can stretch to 18 months, more than quadruple the timeline in non-heritage zones, forcing carriers to rely on macro sites with poor propagation angles. Italian cities impose aesthetic mandates that increase per-site installation costs by EUR 15,000 to EUR 25,000. Because every EU member state follows unique zoning codes, operators cannot standardize equipment designs, which delays the realization of economies of scale. The restrictions also constrain small-cell density, capping achievable capacity just as mmWave adoption begins.

mmWave Backhaul CAPEX vs. Fiber Wholesale Rates

Ericsson finds mmWave base stations need dedicated fiber backhaul that costs EUR 800 to 1,200 per month, whereas retail fiber sold to homes averages EUR 25 to 35 monthly. The gap forces operators to sign up 30 to 40 paying subscribers per site for break-even, compared with 8 to 12 on Sub-6 GHz. High lease rates hit dense cities hardest, paradoxically, where mmWave delivers its greatest technical benefits. Without wholesale price relief or alternative backhaul such as microwave relay, expansion may slow.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Infrastructure Dominance Shifting Toward Managed Services

Hardware accounted for 59.68% of the European Fixed Wireless Access market share in 2025, as operators rushed to establish nationwide coverage footprints. Consumer premises equipment led spending, with Nokia’s FastMile 5G Gateway supplying Deutsche Telekom and Vodafone rollouts. Access units such as picocells gained traction when carriers densified urban grids to support mmWave. The services segment is expected to grow at a 16.92% CAGR, as operators are shifting their focus to installation, maintenance, and analytics packages that generate recurring revenue. Indoor Wi-Fi 6E integration from Qualcomm chipsets simplifies home networks, cutting truck-roll frequency and improving customer satisfaction.

Equipment vendors capitalize on first-wave spending but must now differentiate via software updates that enhance spectral efficiency. Ericsson’s Radio System portfolio integrates cloud-native management that optimizes beamforming in real time, helping carriers serve more users per site. As a result, the European Fixed Wireless Access market is moving from capital-intensive buildout to operations-centric monetization. Long-term winners will combine premium hardware with AI-driven support services that raise lifetime value.

By Application: Residential Leadership Meets Enterprise Momentum

Residential connections held 53.12% of the European Fixed Wireless Access market share in 2025, as rural families lacked viable fiber alternatives. Commercial uptake is rising fastest, charting a 15.86% CAGR driven by enterprises that need quick connectivity for pop-up offices, construction sites, and branch backups. Swisscom’s corporate FWA offer in Zurich guarantees 200 Mbps symmetrical throughput backed by service-level agreements, allowing firms to migrate off costly legacy leased lines.

Urban households still account for the bulk of new activations, thanks to bundles that combine mobile and video services at competitive price points. Yet large manufacturers such as Siemens are piloting private 5G FWA links on campus to digitalize production lines and enable AGV fleets. The enterprise swing diversifies revenue, shielding carriers from residential price pressure and raising average revenue per site.

By Frequency Band: Sub-6 GHz Foundation with mmWave Upside

The Sub-6 GHz spectrum achieved a 54.25% market share in the European Fixed Wireless Access market in 2025, driven by its favorable propagation characteristics and mature device ecosystems. Consistent 80 MHz allocations in the 3.5 GHz range enable nationwide blanket coverage without excessive tower builds. mmWave above 24 GHz is on a 16.60% CAGR path because recent 26 GHz auctions grant contiguous 400 MHz blocks. Telefónica’s Madrid pilot reached peak speeds beyond 2 Gbps, positioning the offer against premium fiber tiers.

Operators typically start with Sub-6 GHz to blanket suburbs and rural precincts, then layer mmWave in dense downtown corridors where gigabit-class demand justifies higher capital outlays. The bifurcated spectrum strategy lets carriers balance coverage and capacity while meeting EU performance benchmarks.

By Deployment Mode: Indoor Convenience Versus Outdoor Performance

Indoor CPE accounted for 59.74% of installations in 2025, as self-install kits avoid truck rolls and spur rapid adoption. Outdoor units, however, are growing at 16.84% CAGR as carriers address signal attenuation through concrete facades, especially in historic cores. Ericsson’s weather-hardened outdoor CPE delivers stable 500 Mbps links across Nordic winters, raising quality of service scores.

Carriers now conduct site surveys to determine whether to deploy indoor or outdoor units. Indoor options are effective when the signal-to-noise ratio exceeds the set thresholds. Outdoor versions excel in high-bandwidth environments and thick-walled buildings, ensuring operators can tailor offers without compromising the experience.

Geography Analysis

Germany controlled 25.62% of the European Fixed Wireless Access market share in 2025 as Deutsche Telekom blanketed 2,800 rural communities with 300-500 Mbps services. Early spectrum awards and federal broadband grants catalyzed rapid builds. Tiered packages now span from basic 50 Mbps to enterprise-class gigabit plans, underscoring the market's maturity.

France is the fastest-growing territory, with a 15.05% CAGR through 2031, driven by Orange’s FWA solutions in heritage city centers, where fiber trenching is subject to strict heritage preservation rules. Government stimulus via Plan France Très Haut Débit provides EUR 3.3 billion, enabling operators to subsidize CPE in both rural and urban use cases.

The UK pursues a bridge strategy; BT fills rural gaps in Scotland and Wales, pending fiber readiness beyond 2027, by leveraging the spectrum already invested in its mobile network. Italy draws on EUR 2.1 billion in subsidies for mountainous regions, accelerating the adoption of FWA where fiber costs exceed EUR 2,000 per home. Nordic operators Telia and Telenor use extensive mid-band holdings to mount credible challenges to entrenched fiber players, indicating the European Fixed Wireless Access market will remain fiercely contested across sub-regions.

Competitive Landscape

Competition is moderately fragmented. Nokia and Ericsson dominate radio access equipment while Huawei and ZTE vie for price-sensitive deals. Qualcomm shakes up the CPE space with Wi-Fi 7 chips that integrate seamlessly into carrier firmware roadmaps. Operators are increasingly forging vertical partnerships; Deutsche Telekom co-designs antenna tuning algorithms with Nokia to enhance cell-edge throughput.

Technology differentiation beats pure scale. Ericsson’s Massive-MIMO radios boost site capacity 30%, improving site economics in mmWave dense grids. Nokia holds 847 active FWA patents, compared to Ericsson’s 623, indicating an arms race in beamforming and AI-driven interference cancellation. Vendors also package cloud analytics that alert carriers to service degradation before end-users notice, creating sticky software revenue streams.

Component concentration contrasts with CPE diversity, where vendors such as Zyxel, OPPO, and Inseego compete on price and form factor. Carriers hedge supply by certifying two to three CPE brands per market, which caps individual vendor share and keeps innovation cycles brisk. With European security policies increasingly scrutinizing Chinese equipment, Western incumbents could consolidate their share if additional restrictions emerge.

Europe Fixed Wireless Access (FWA) Industry Leaders

Nokia Oyj

Telefonaktiebolaget LM Ericsson

Huawei Technologies Co., Ltd.

ZTE Corporation

Qualcomm Technologies Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Deutsche Telekom launched hybrid home plans that blend fixed wireless bandwidth on demand, reaching speeds up to 500 Mbps when household peak usage exceeds DSL limits.

- February 2025: Nokia and Qualcomm have entered a strategic alliance to deliver Wi-Fi 7-enabled FWA CPE optimized for dense-deployment environments in Europe.

Europe Fixed Wireless Access (FWA) Market Report Scope

Fixed wireless technology connects two fixed locations, such as buildings or towers, using wireless links like radio waves or laser bridges. Typically integrated into a wireless LAN infrastructure, fixed wireless links facilitate data communication between sites. Moreover, fixed wireless data (FWD) often serves as a cost-effective substitute for leasing fiber or installing cables between buildings.

The European fixed wireless access (FWA) Market is segmented by end user (residential/consumer and enterprises) and geography (United Kingdom, France, Germany, Italy, and Rest of Europe). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Hardware | Consumer Premises Equipment (CPE) |

| Access Units (Femto and Picocells) | |

| Services |

| Residential |

| Commercial |

| Industrial |

| Sub-6 GHz |

| mmWave ( > 24 GHz ) |

| Indoor CPE |

| Outdoor CPE |

| Germany |

| United Kingdom |

| France |

| Italy |

| Rest of Europe |

| By Type | Hardware | Consumer Premises Equipment (CPE) |

| Access Units (Femto and Picocells) | ||

| Services | ||

| By Application | Residential | |

| Commercial | ||

| Industrial | ||

| By Frequency Band | Sub-6 GHz | |

| mmWave ( > 24 GHz ) | ||

| By Deployment Mode | Indoor CPE | |

| Outdoor CPE | ||

| By Country | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe |

Key Questions Answered in the Report

What is the 2026 valuation of the Europe Fixed Wireless Access market?

It stands at USD 16.21 billion, rising toward USD 28.96 billion by 2031.

Which country holds the largest share of Europe’s fixed wireless access deployment?

Germany leads with 25.62% market share thanks to Deutsche Telekom’s rural buildouts.

Which frequency band dominates current European FWA services?

Sub-6 GHz bands deliver 54.25% market share, offering reliable coverage suited to suburban and rural areas.

Why is France the fastest-growing European FWA territory?

Orange leverages FWA in heritage city centers where fiber trenching is constrained, driving a 15.05% CAGR through 2031.

How are operators improving customer retention with FWA?

They bundle fixed wireless with mobile data and entertainment services, boosting average revenue per user by double-digit percentages.

What is the main restraint affecting mmWave FWA economics?

High fiber backhaul costs raise subscriber break-even thresholds in dense urban markets.

Page last updated on: